Feed Additives Market Size, Share, Trends, and Forecast by Source, Product Type, Livestock, Form, and Region, 2026-2034

Global Feed Additives Market Size, Share, Trends & Forecast (2026-2034)

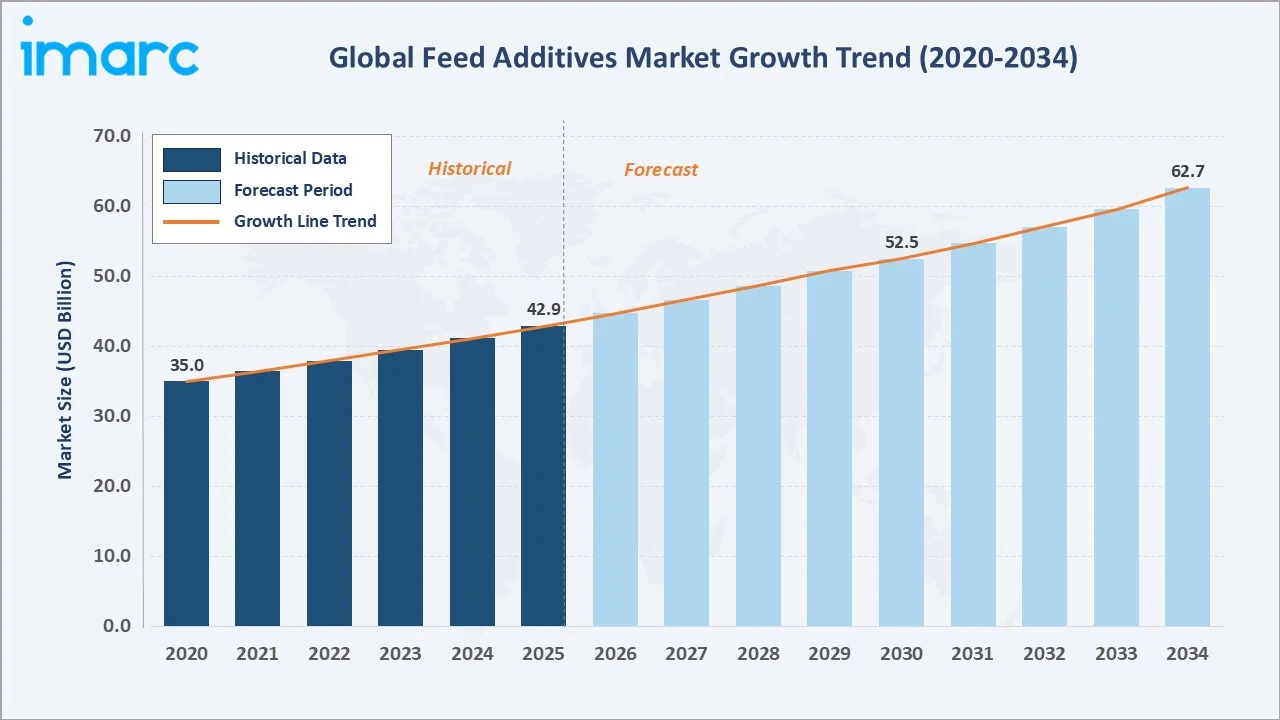

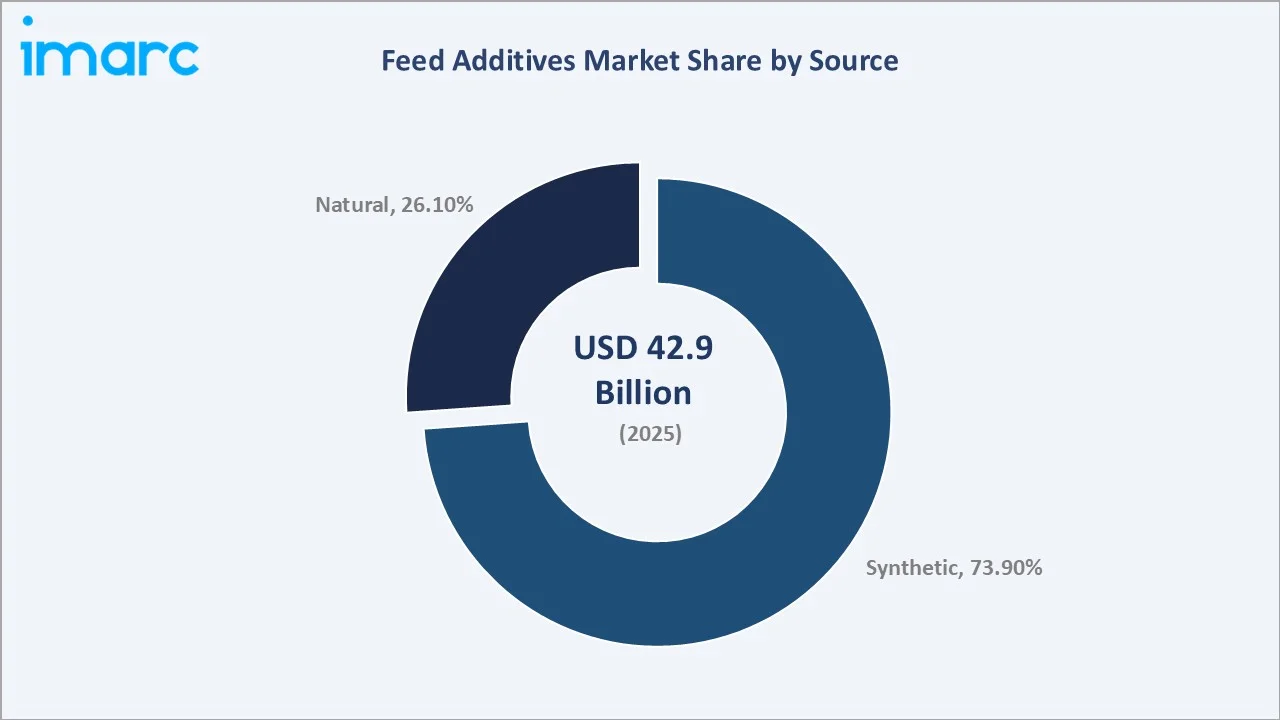

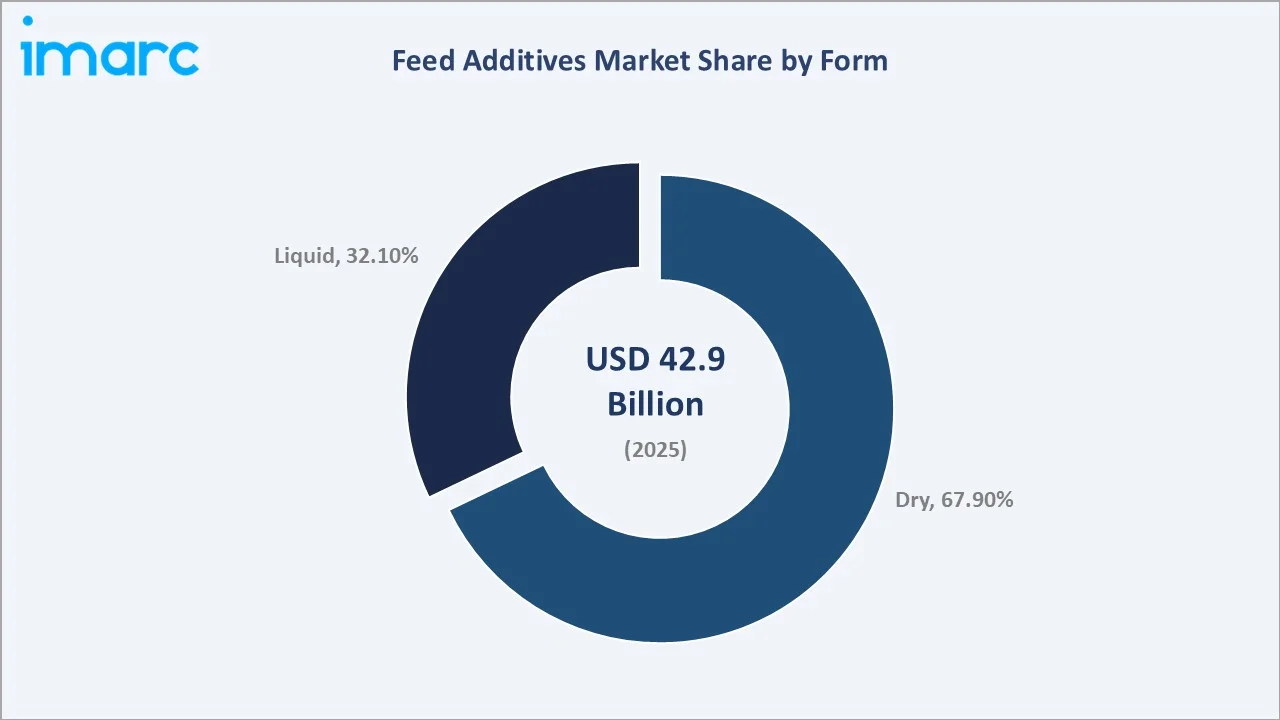

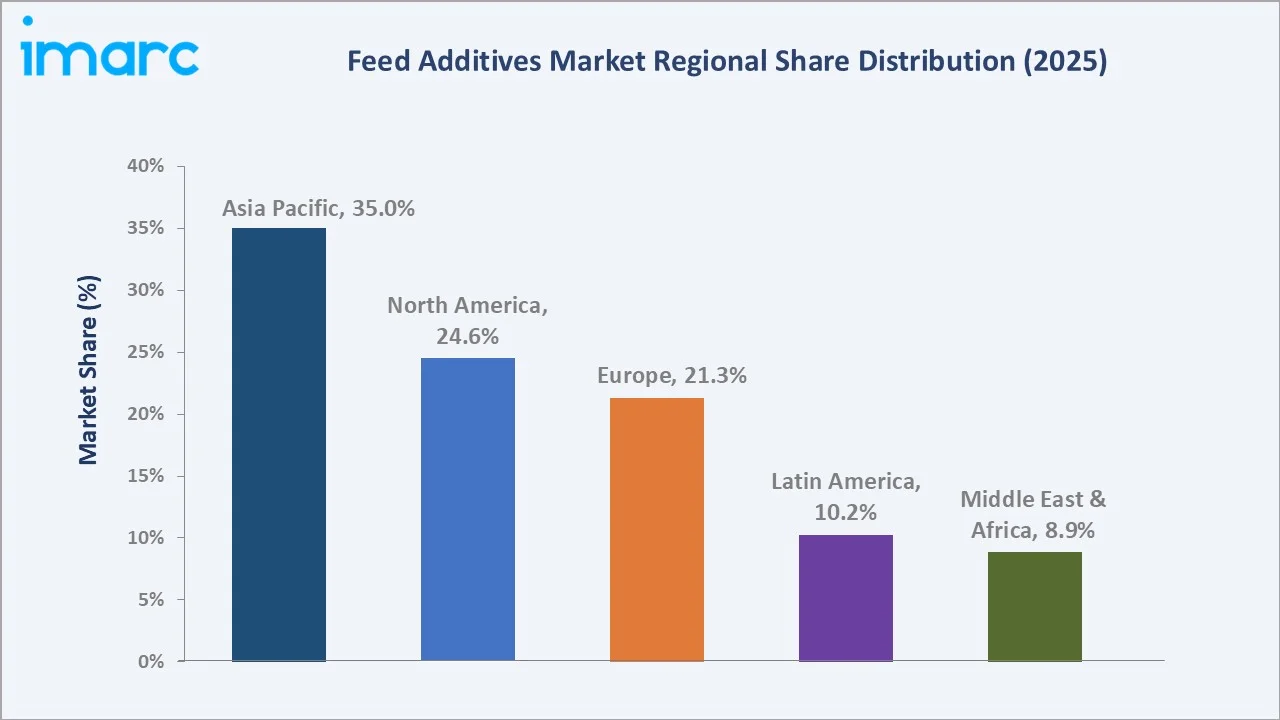

The global feed additives market size was valued at USD 42.9 Billion in 2025 and is projected to reach USD 62.7 Billion by 2034, exhibiting a CAGR of 4.14% during the forecast period 2026-2034. Escalating global demand for high-quality animal protein, accelerating antibiotic growth promoter phase-outs across the EU, China, and other key markets, and landmark advances in precision animal nutrition are driving the feed additives market growth. Synthetic additives dominate at 73.9% in 2025, dry-form leads at 67.9%, and the Asia Pacific commands 35.0% of global revenue in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 42.9 Billion |

|

Forecast Market Size (2034) |

USD 62.7 Billion |

|

CAGR (2026-2034) |

4.14% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (35.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~5.9%) |

|

Leading Source Segment |

Synthetic (73.9%, 2025) |

|

Leading Form Segment |

Dry (67.9%, 2025) |

The global feed additives market growth trajectory from 2020 through 2034, contrasting consistent historical expansion against a sustained forecast curve powered by rising global protein demand, antibiotic growth promoter phase-outs, and accelerating natural additive adoption.

To get more information on this market, Request Sample

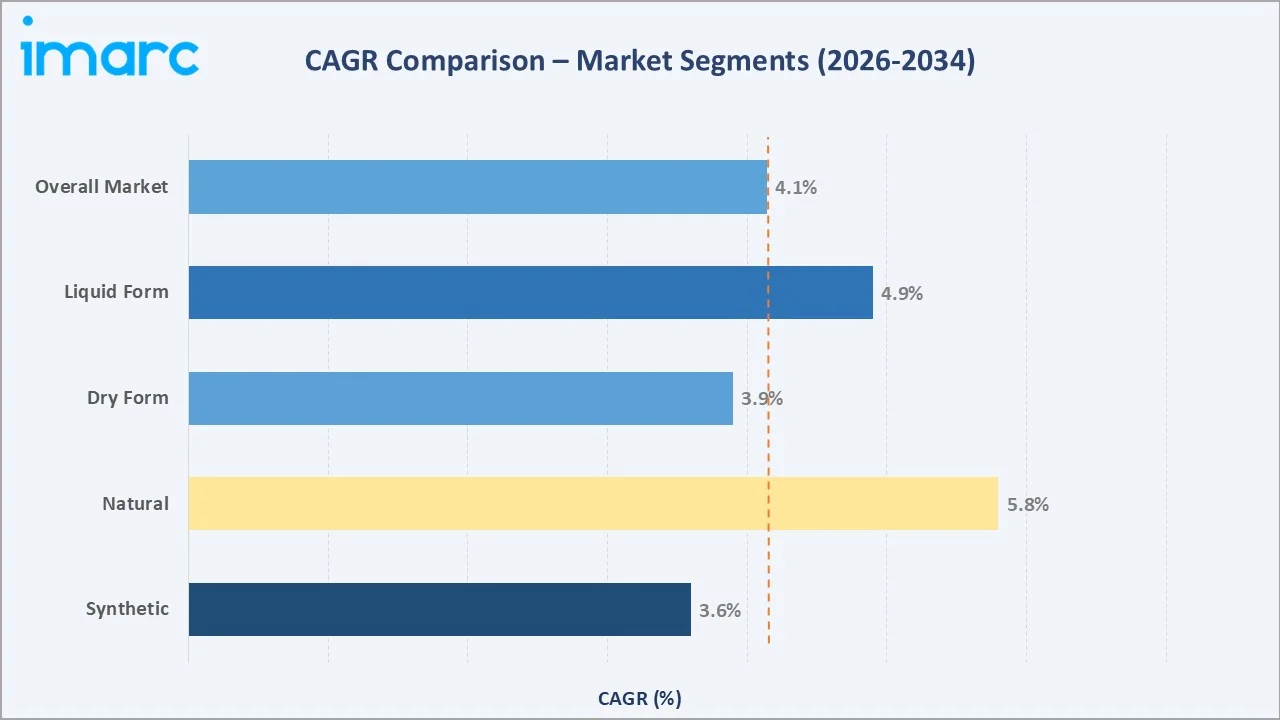

Segment-level CAGR comparisons highlighting natural additives and liquid-form products as the two fastest-growing sub-categories within the global feed additives industry through 2034.

Executive Summary

The global feed additives market is undergoing robust structural expansion driven by rising animal protein consumption, tightening food safety regulations, and advances in precision animal nutrition. Valued at USD 42.9 Billion in 2025, the market is forecast to reach USD 62.7 Billion by 2034 at a CAGR of 4.14%. The OECD-FAO Agricultural Outlook (July 2025) projects global meat, dairy, and egg output to grow 17% over the next decade, each percentage point of that growth translating directly into expanded demand for performance-enhancing feed additives across all livestock categories globally.

Synthetic additives command 73.9% of 2025 revenue, driven by cost-efficiency, proven efficacy at commercial scale, and precision-dosing advantages. The natural segment at 26.1% is the fastest-growing sub-category, accelerated by AGP bans across 40+ countries and consumer demand for antibiotic-free, clean-label products. Dry-form additives captured 67.9% of 2025 revenue, reflecting superior shelf stability and seamless integration with industrial pelleting equipment at feed mills worldwide.

Asia Pacific dominates with a 35.0% global revenue share in 2025, anchored by China, the world's largest compound feed producer at over 280 million metric tons annually, and India's rapidly scaling commercial poultry and dairy sectors. North America holds 24.6% and Europe 21.3%, both characterised by advanced animal nutrition research and accelerating demand for antibiotic-free products.

Key Market Insights

|

Insight |

Data |

|

Largest Source Segment |

Synthetic – 73.9% share (2025) |

|

Fastest Growing Segment |

Natural additives – antibiotic-free & clean-label demand |

|

Leading Form Segment |

Dry – 67.9% share (2025) |

|

Leading Region |

Asia Pacific – 35.0% revenue share (2025) |

|

Second Region |

North America – 24.6% revenue share (2025) |

|

Top Companies |

Adisseo, ADM, BASF SE, Cargill, Evonik, Kemin, Lallemand |

Key Analytical Observations Supporting The Above Data:

- Synthetic additives' 73.9% dominance reflects unmatched cost-efficiency, precision-dosing capability, and compatibility with high-volume industrial feed manufacturing serving over 1.15 billion metric tons of annual compound feed production.

- Natural segment's accelerating growth, phytogenics, probiotics, fermentation-derived enzymes, is driven by AGP bans in 40+ countries and consumer demand for residue-free, clean-label animal products in premium retail supply chains.

- Asia Pacific's 35.0% global dominance reflects China's role as the world's largest compound feed producer and the rapid commercialisation of large-scale poultry, swine, and aquaculture operations across the broader region.

Global Feed Additives Market Overview

Feed additives are substances incorporated into animal diets to enhance nutritional value, improve feed conversion ratios, boost animal immunity, and preserve feed quality. The product ecosystem spans amino acids, vitamins, minerals, enzymes, probiotics, acidifiers, antioxidants, mycotoxin detoxifiers, phytogenics, and preservatives, each addressing specific nutritional and functional requirements across poultry, ruminant, swine, and aquaculture production systems globally.

Applications span the full livestock sector: commercial broiler and layer operations, swine grow-finisher programmes, dairy and beef cattle, aquaculture species, and specialty livestock. Macroeconomic enablers include rapid urbanisation, income growth in developing economies, dietary protein transition, and globalised livestock trade standards. Feed additives market trends increasingly reflect the convergence of food safety imperatives, environmental sustainability mandates, and precision nutrition science, compelling manufacturers to develop validated, residue-free solutions.

Market Dynamics

To evaluate market opportunities, Request Sample

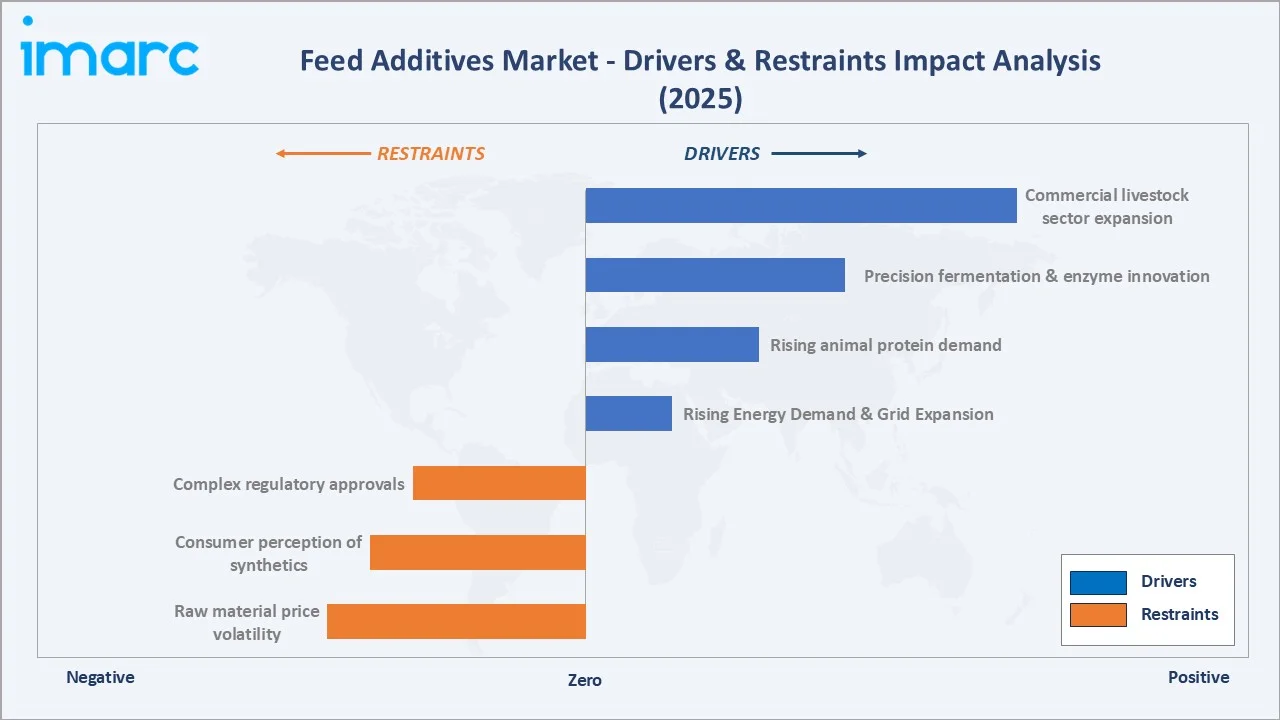

Market Drivers

- Rising Animal Protein Demand: Global meat, dairy, and egg output is projected to grow 17% by 2034 per the FAO-OECD Agricultural Outlook (July 2025) , directly compelling livestock producers to adopt advanced feed additives that maximise feed efficiency, growth performance, and health outcomes.

- Antibiotic Growth Promoter Phase-Out: Bans across the EU, China, Vietnam, and 40+ markets are compelling producers to replace AGPs with functional alternatives, probiotics, prebiotics, organic acids, and phytogenics, creating accelerating structural demand.

- Biotechnology and Precision Fermentation: Innovations in enzyme engineering, microencapsulation, and synthetic biology are enabling next-generation additives with superior bioavailability, species-specific performance, and measurably reduced environmental footprint.

Market Restraints

- Raw Material Price Volatility: Fluctuations in amino acid, vitamin, and mineral input prices periodically compress manufacturer margins and raise end-user costs, creating demand-side resistance in price-sensitive emerging markets.

- Complex Regulatory Approvals: Region-specific and lengthy approval pathways for novel formulations extend time-to-market and raise compliance costs, limiting agility for smaller specialised manufacturers.

Market Opportunities

- Aquaculture Sector Expansion: Expanding steadily across Southeast Asia, Latin America, and Africa, aquaculture represents a high-growth frontier for specialised formulations targeting fish, shrimp, and crustacean production, with currently low levels of additive penetration.

- Premium Natural Segments: Consumer demand for organic, antibiotic-free animal products is creating premium-margin opportunities for certified natural additive manufacturers across both developed and fast-growing emerging markets.

Market Challenges

- Synthetic Additive Perception: Growing consumer scepticism toward synthetic feed additives is prompting producers to reformulate feed programmes, adding complexity and cost across major markets worldwide.

- Supply Chain Concentration Risk: Geographic concentration of amino acid and vitamin production creates supply chain vulnerability, with geopolitical tensions periodically impacting availability and pricing globally.

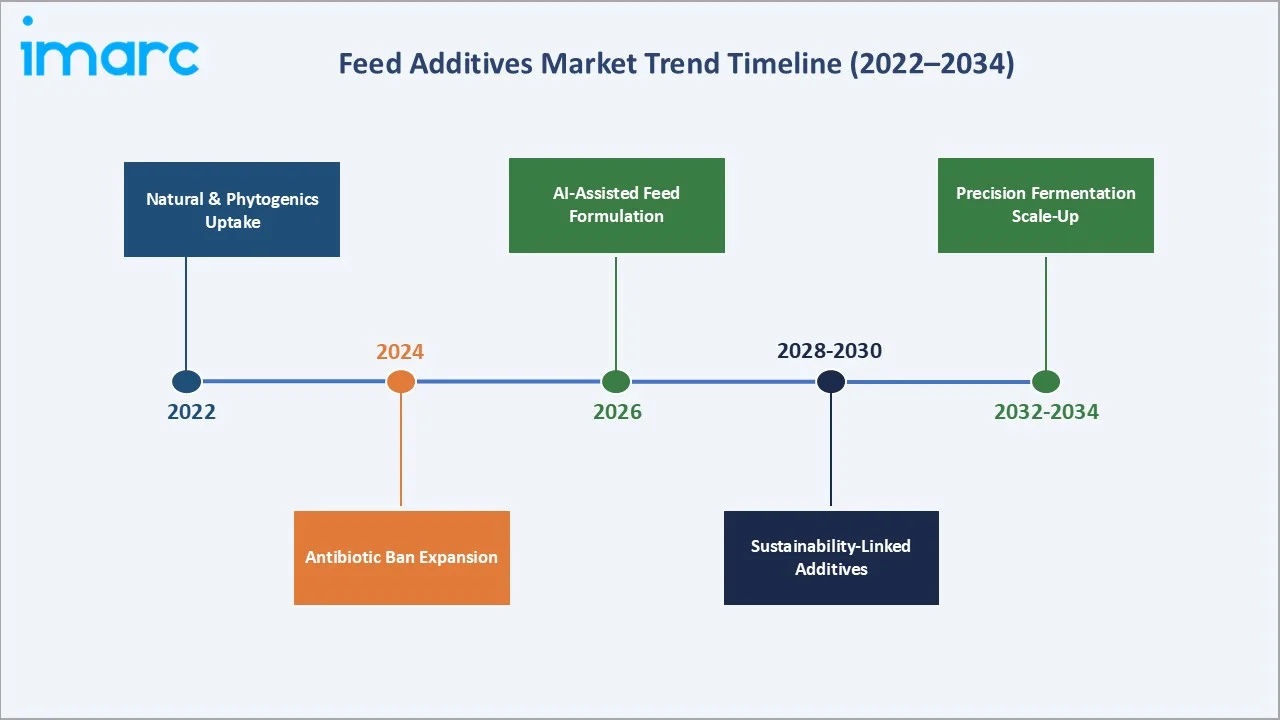

Emerging Market Trends

1. Accelerating Shift Toward Natural and Phytogenic Additives

Consumer demand for antibiotic-free, clean-label animal products is reshaping the feed additives landscape. Phytogenics, essential oils, herbs, and oleoresins, are gaining share for their antimicrobial and gut health properties. China’s nationwide ban on antibiotic growth promoters in animal feed has accelerated the adoption of natural alternatives, particularly probiotics. Emerging evidence indicates that probiotic supplementation can significantly improve animal health, enhance disease resistance, and reduce reliance on antibiotics in commercial livestock systems, although outcomes vary by species and production conditions.

2. AI-Assisted Precision Feed Formulation

AI platforms are transforming feed formulation from empirical mixing to precision nutritional targeting, optimising additive inclusion rates in real time based on animal performance metrics and ingredient costs. In recent years, major U.S. agribusiness players have formed strategic collaborations with biotechnology firms to develop next-generation feed additives leveraging advanced fermentation technologies, underscoring the growing focus on sustainable, high-performance animal nutrition.

3. Sustainability and Emissions Reduction as Product Imperatives

Livestock producers face intensifying pressure to reduce methane emissions, nitrogen excretion, and phosphorus runoff. Japan has been advancing the regulatory evaluation and adoption of methane-reducing feed additives, supporting the transition toward lower-emission livestock systems. Concurrently, major European specialty chemicals and nutrition companies have continued to expand their portfolios of sustainable feed additives designed to reduce greenhouse gas emissions from livestock operations, reflecting growing regulatory and commercial momentum in this space.

4. Expansion of Aquaculture-Specific Additive Solutions

With aquaculture production rising steadily worldwide, demand for specialised, species-specific additives is accelerating. In response, global animal nutrition leaders are expanding their manufacturing footprint in key markets such as India, with dedicated investments in aquaculture-focused additives and mycotoxin mitigation solutions, reinforcing the segment’s growing strategic significance.

5. Regionalisation and Vertical Integration of Supply Chains

Leading manufacturers are investing in regional production footprints to reduce supply chain risk and respond faster to local requirements. This trend is pronounced in Asia Pacific and Latin America, where rapid livestock sector growth creates strategic rationale for in-market manufacturing investment that gives locally present players a demonstrable service advantage over import-dependent competitors.

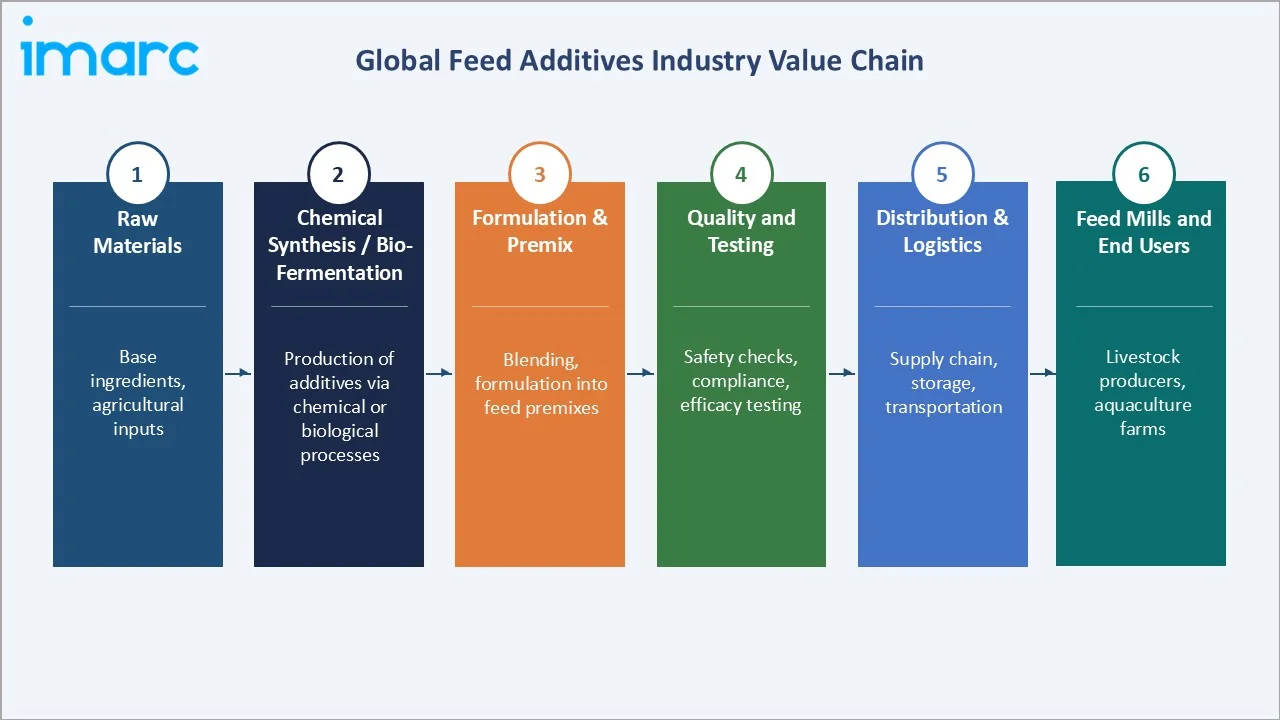

Industry Value Chain Analysis

The feed additives value chain spans five integrated stages from raw material supply through end-livestock-producer delivery, each presenting distinct competitive dynamics and margin profiles.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Corn, soybean meal, mineral salts, fermentation substrates, plant-derived extracts |

|

Chemical Synthesis / Bio-Fermentation |

Evonik (amino acids), BASF (vitamins), Novonesis (enzymes), Lallemand (yeasts/probiotics) |

|

Formulation & Premix Production |

Adisseo, Kemin Industries, Alltech, Bentoli — formulated premixes, encapsulated additives |

|

Commercial Feed Milling |

Cargill, ADM, Nutreco, regional co-operative mills — compound feed and premix integration |

|

End Users (Livestock Producers) |

Poultry integrators, swine operations, dairy farms, aquaculture producers, and beef feedlots |

Additive manufacturers occupy the highest strategic value position, integrating upstream chemistry or bio-fermentation with downstream formulation to deliver turnkey nutritional solutions. This position is increasingly challenged by vertically integrated milling companies developing proprietary premix capabilities to capture additive margin.

Technology Landscape in the Feed Additives Industry

Synthetic Production: Chemical Synthesis and Fermentation Technologies

Synthetic amino acid production relies on advanced bacterial fermentation platforms with continuous process improvements, reducing costs and improving yields. Vitamin synthesis pathways are transitioning from petrochemical to bio-based fermentation routes to reduce environmental impact and strengthen regulatory acceptance in sustainability-sensitive markets.

Natural Additive Innovation: Enzymes, Probiotics, and Phytogenics

Enzyme engineering is delivering phytases and proteases with enhanced thermostability and substrate specificity, enabling meaningful reductions in phosphorus excretion and nitrogen waste. Probiotic strain selection platforms leverage genomic screening to identify strains with superior gut colonisation and immune modulation. Phytogenic active compound standardisation is addressing historically variable potency to enable reproducible commercial outcomes.

Delivery Systems and Formulation Technologies

Microencapsulation technologies enable controlled release of heat-sensitive probiotics, volatile essential oils, and pH-sensitive organic acids through the feed pelleting process. Liquid delivery systems are advancing for precision supplementation in lactating sow systems, aquaculture recirculating operations, and high-performance broiler programmes, where in-line dosing offers superior accuracy versus dry premix blending.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Source |

Synthetic |

73.9% |

2025 |

|

Product Type |

Amino Acids |

16.8% |

2025 |

|

Form |

Dry |

67.9% |

2025 |

|

Livestock |

Poultry |

36.9% |

2025 |

|

Region |

Asia Pacific |

35.0% |

2025 |

By Source

Synthetic commands 73.9% majority share in 2025, reflecting the industry's broad reliance on cost-efficient, precision synthetic amino acids, vitamins, and enzymes for large-scale commercial feed production. The synthetic segment benefits from proven supply chain reliability, regulatory acceptance across all major markets, and consistent potency at volumes serving over 1.15 billion metric tons of compound feed produced annually worldwide.

To access detailed market analysis, Request Sample

Natural at 26.1% in 2025 represent the fastest-growing sub-category, driven by AGP bans, clean-label consumer demand, and commercial maturation of phytogenic, probiotic, and fermentation-derived platforms. Natural additives command premium pricing, increasingly favoured by producers supplying antibiotic-free certified supply chains in Europe, North America, and premium Asian markets.

By Form

Dry-form commanded 67.9% market share in 2025, underpinned by superior stability in industrial feed manufacturing, enhanced stability during transportation, minimal contamination risk, longer shelf life, and homogeneous blending with pelleted and mash feed matrices. Feed mills globally have optimised equipment around dry additive integration, creating substantial infrastructure-driven preference.

Liquid additives at 32.1% in 2025 are gaining share in precision liquid feeding applications, lactating sow systems, aquaculture recirculating tank dosing, and high-performance broiler programmes, where in-line dosing offers superior accuracy and enables incorporation of heat-sensitive bioactive compounds degraded during pelleting.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

35.0% |

China antibiotic ban; poultry & aquaculture expansion; rising incomes; India dairy modernisation |

|

North America |

24.6% |

200M+ tons/yr US feed output; antibiotic-free demand; advanced animal nutrition R&D |

|

Europe |

21.3% |

EU Regulation 1831/2003; natural/organic additive demand; sustainability mandates |

|

Latin America |

10.2% |

Brazil/Argentina livestock export growth; rising domestic protein demand; new investments |

|

Middle East & Africa |

8.9% |

Food security policies; expanding commercial livestock; modernising feed supply chains |

Asia Pacific commands a 35.0% global revenue share in 2025. China is the dominant national market, combining the world's largest compound feed production volume, over 280 million metric tons annually, with aggressive AGP phase-out policies accelerating probiotic, enzyme, and phytogenic adoption at scale. The Asia Pacific feed additives market is projected to grow from USD 17.56 Billion in 2025 to USD 24.01 Billion by 2030 at a CAGR of 6.4%. India's modernising poultry sector and government livestock productivity programmes are further accelerating regional adoption.

North America, with 24.6% in 2025, is anchored by the United States is the world’s second-largest compound feed producer, supported by a network of over 5,500 manufacturing facilities and generating more than 270 million metric tons of feed annually, underscoring its scale and technological leadership in the global animal nutrition industry. Advanced livestock farming practices, stringent FDA quality standards, and high consumer demand for antibiotic-free certified products are reinforcing the transition toward premium functional additive formulations.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Cargill, Incorporated |

Cargill Animal Nutrition |

Leader |

Global scale, integrated supply chain, premix, and compound feed leadership |

|

BASF SE |

Lutavit / Lucantin |

Leader |

Vitamins, carotenoids, organic acids; European R&D and scale leadership |

|

Evonik Industries AG |

MetAMINO® / Biolys® |

Leader |

Global methionine leadership; amino acid fermentation scale and precision nutrition |

|

ADM |

ADM Animal Nutrition |

Leader |

Amino acids, vitamins, feed ingredients; global origination and processing network |

|

Adisseo |

Rhodimet / Smartamine |

Challenger |

Methionine and vitamin specialisation; China and Asia Pacific market leadership |

|

Kemin Industries, Inc. |

Kemtrace / Formyl |

Challenger |

Antioxidants, phytogenics, mycotoxin binders; specialty functional niche leadership |

|

Lallemand Inc. |

Levucell / Bactocell |

Challenger |

Yeast-based probiotics and fermentation expertise; ruminant and swine focus |

|

Alltech |

Sel-Plex / Bio-Mos |

Challenger |

Organic trace minerals, mycotoxin management, yeast-derived functional additives |

|

Novonesis Group |

BioProtect / Phytase |

Emerging |

Enzyme bio-innovation, fermentation platform leadership, and sustainability focus |

|

Novus International, Inc. |

MINTREX / ACTIVATE |

Emerging |

Chelated trace minerals, methionine hydroxy analogue, feed acidifier solutions |

The feed additives competitive landscape is characterised by a small number of global leaders with substantial OEM relationships alongside biotechnology-native entrants challenging incumbents on performance and sustainability credentials. Strategic alliances, joint ventures, and targeted acquisitions are intensifying as leading firms seek expanded geographic reach and stronger technology capabilities.

Key Company Profiles

Cargill, Incorporated

Cargill is a global leader in animal nutrition, operating an integrated supply chain spanning origination, processing, and formulated additive delivery across more than seventy countries, serving poultry, swine, ruminant, and aquaculture producers with a comprehensive portfolio of amino acids, vitamins, minerals, and premix solutions.

- Product & Platform Portfolio: Cargill Animal Nutrition premix systems, PhytaFeed phytogenic additives, NovaSil mycotoxin binders, sodium butyrate products, and organic acid blends for gut health and feed preservation.

- Recent Developments: In July 2025, Cargill announced the acquisition of Brazilian animal nutrition company Mig-Plus, expanding its manufacturing footprint and strengthening its presence in Latin America. The move enhances regional production capacity and brings the company closer to key livestock producers, reinforcing Brazil’s strategic importance in the global animal nutrition market.

- Strategic Focus: Cargill centres its strategy on integrated supply chain advantages combined with regional manufacturing investment in high-growth markets, increasingly emphasising sustainability-linked additive solutions as major producers require partners with demonstrable carbon reduction credentials.

BASF SE

BASF is one of the world's largest producers of feed-grade vitamins, carotenoids, and organic acids, with large-scale chemical synthesis capabilities delivering reliable supply and competitive cost positions across all major vitamin categories for the global animal nutrition market.

- Product & Platform Portfolio: Lutavit vitamin premix portfolio, Lucantin carotenoids for poultry and aquaculture, Luctarom natural flavour enhancers, SelPlus organic selenium, and Luprosil organic acid blends for feed preservation and gut health.

- Recent Developments: In October 2025, BASF is launching Lutavit A/D3 1000/200 NXT – a next-generation vitamin formulation – that combines vitamin A and vitamin D3 in a single, microencapsulated form. This innovative product marks BASF’s return to the market with a product that delivers convenience, performance, and sustainability.

- Strategic Focus: BASF prioritises scale in vitamin and carotenoid production, sustainability leadership through bio-based production transitions, and innovation in functional organic acid and phytogenic categories, investing in renewable-feedstock processes to meet ESG procurement requirements from global livestock producers.

Evonik Industries AG

Evonik is the global leader in feed-grade methionine through its MetAMINO brand, and a major producer of threonine (Biolys), tryptophan, and valine, with world-scale fermentation assets delivering cost-competitive amino acid supply to poultry and swine feed markets worldwide.

- Product & Platform Portfolio: MetAMINO DL-methionine, Biolys L-lysine, ThreAMINO threonine, TrypAMINO tryptophan, ValAMINO valine, and AMINODat precision nutrition software platform for feed formulation optimisation.

- Recent Developments: In 2021, Evonik expanded AMINODat with updated nutrient digestibility coefficients, enabling feed formulators to reduce amino acid overfortification and cut costs without compromising animal performance .

- Strategic Focus: Evonik focuses on amino acid market leadership through continuous fermentation cost reduction, complemented by diversification into probiotics, enzymes, and precision micronutrients. The AMINODat digital platform embeds Evonik's amino acids into feed formulation workflows at major global feed mill customers.

Market Concentration Analysis

The global feed additives market exhibits moderate fragmentation, with the top five players, Cargill, BASF SE, Evonik, ADM, and Adisseo, collectively accounting for 30-38% of global market revenue in 2025. This level reflects the breadth of additive product categories and the continued strength of regional specialists in each sub-segment.

A bifurcated dynamic is emerging: in commodity amino acid and vitamin categories, consolidation is intensifying as large-scale assets create high barriers to new entrant competition. Simultaneously, the specialty and natural additive segments are fragmenting, with biotechnology-native companies capturing niche share through proprietary strain libraries, novel extraction technologies, and formulation expertise that large commodity players cannot easily replicate.

Investment & Growth Opportunities

Fastest-Growing Segments

Natural and phytogenic additives are the highest-growth category at an estimated CAGR of ~5.8% through 2034. Commercial maturation of phytogenic essential oil blends, standardised herbal extracts, and third-generation probiotics, combined with regulatory tailwinds from expanding antibiotic bans, is driving strong revenue growth in leading natural sub-categories. Aquaculture-specific formulations are the fastest-growing application, driven by global aquaculture output growth at over 3% annually.

Emerging Market Expansion

India, Indonesia, Brazil, Vietnam, and Sub-Saharan Africa represent the highest-growth frontiers, combining expanding livestock production with low current additive penetration. India's National Livestock Mission and Indonesia's productivity initiatives are directly incentivising performance-enhancing additive adoption. Sustainability-linked categories, methane reducers, nitrogen-efficiency enhancers, are attracting ESG-focused investment and premium pricing from environmentally committed producers.

Venture & Private Investment Trends

Significant private capital is flowing into biotechnology-native companies developing fermentation-derived probiotic strains, precision enzyme engineering platforms, and AI-assisted formulation systems. Notable areas include synthetic biology platforms for bespoke amino acid production, microbiome-based additive companies with proprietary strain IP, and digital nutrition platforms embedding additive optimisation into feed mill management systems.

Future Market Outlook (2026-2034)

The global feed additives market forecast projects value expansion from USD 42.9 Billion in 2025 to USD 62.7 Billion by 2034 at a CAGR of 4.14%, a 46% increase underpinned by volume growth in emerging markets and value-mix improvement as higher-margin natural and sustainability-linked additives capture increasing share from commodity synthetic products.

Three structural forces will reshape the market through 2034. Antibiotic phase-out acceleration, with 60+ countries implementing comprehensive AGP restrictions by 2030, will redirect significant additive spend toward functional alternatives. Precision fermentation platforms will lower bio-derived amino acid, probiotic, and enzyme production costs to levels competitive with synthetic equivalents. Sustainability-linked procurement policies from major food companies will create new product specification requirements, reshaping buyer-supplier dynamics across the value chain.

Research Methodology

Primary Research

Primary research encompassed structured interviews with feed additives industry stakeholders, including product directors at leading manufacturers, animal nutritionists at major feed mills, livestock producer operations managers, regulatory specialists, and institutional investors. Primary insights validated market sizing, segmentation assessments, competitive positioning, and technology adoption timeline projections.

Secondary Research

Secondary sources include the FAO-OECD Agricultural Outlook 2025, Alltech Global Feed Survey (2025), International Feed Industry Federation production data, national agriculture ministry statistics from China, India, Brazil, the US, and EU member states, company annual reports, and trade publications including Feed Navigator, Feed International, and World Grain.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting models incorporating livestock population growth rates, compound feed production volumes, additive inclusion rate trends, average selling price trajectories, and regional economic indicators. Scenario analysis covering base, optimistic, and conservative cases was conducted to account for regulatory uncertainty and commodity price volatility.

Feed Additives Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Sources Covered | Synthetic, Natural |

| Product Types Covered |

|

| Livestocks Covered |

|

| Forms Covered | Dry, Liquid |

| Regions Covered | Asia Pacific, North America, Europe, Middle East and Africa, Latin America |

| Companies Covered | Cargill, Incorporated, BASF SE, Evonik Industries AG, ADM, Adisseo, Kemin Industries, Inc., Lallemand Inc., Alltech, Novonesis Group, Novus International, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the feed additives market from 2020-2034.

- The feed additives market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the feed additives industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Feed Additives Market Report

The global feed additives market was valued at USD 42.9 Billion in 2025, driven by rising animal protein demand, antibiotic-free livestock transitions, and the rapid expansion of poultry, swine, and aquaculture sectors worldwide.

The market is projected to reach USD 62.7 Billion by 2034, growing at a CAGR of 4.14% during 2026-2034, driven by precision nutrition advances, antibiotic alternative adoption, and expanding livestock operations across the Asia Pacific and Latin America.

Synthetic additives lead with a 73.9% share in 2025. Natural additives at 26.1% are the fastest-growing sub-category, supported by antibiotic bans across 40+ markets and consumer clean-label demand globally.

Dry-form additives account for 67.9% of the 2025 market due to superior shelf stability, ease of handling, and compatibility with industrial feed pelleting and blending processes at commercial feed mills worldwide.

Asia Pacific dominates at 35.0% in 2025, led by China as the world's largest compound feed producer and India's rapidly scaling commercial poultry and dairy sectors, driving sustained regional demand.

Key drivers include rising global meat and dairy consumption, AGP bans across 40+ countries, precision fermentation and enzyme technology advances, and rapid commercialisation of livestock operations in the Asia Pacific and Latin America.

Key trends include accelerating natural and phytogenic additive adoption, AI-assisted precision feed formulation, sustainability-linked additive innovation for emissions reduction, and expansion of aquaculture-specific additive solutions globally.

Leading companies include Adisseo, ADM, Ajinomoto Co. Inc., Alltech, BASF SE, Bentoli, Cargill, Evonik Industries AG, Kemin Industries, Lallemand Inc., Novonesis Group, Novus International Inc., and Solvay S.A.

Asia Pacific is projected to grow from USD 17.56 Billion in 2025 to USD 24.01 Billion by 2030 at a CAGR of 6.4%, driven by China's AGP phase-out policy, India's poultry sector modernisation, and Southeast Asian aquaculture expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)