Flame Retardants Market Size, Share, Trends and Forecast by Type, Application, End Use Industry, and Region, 2026-2034

Global Flame Retardants Market Size, Share, Trends & Forecast (2026-2034)

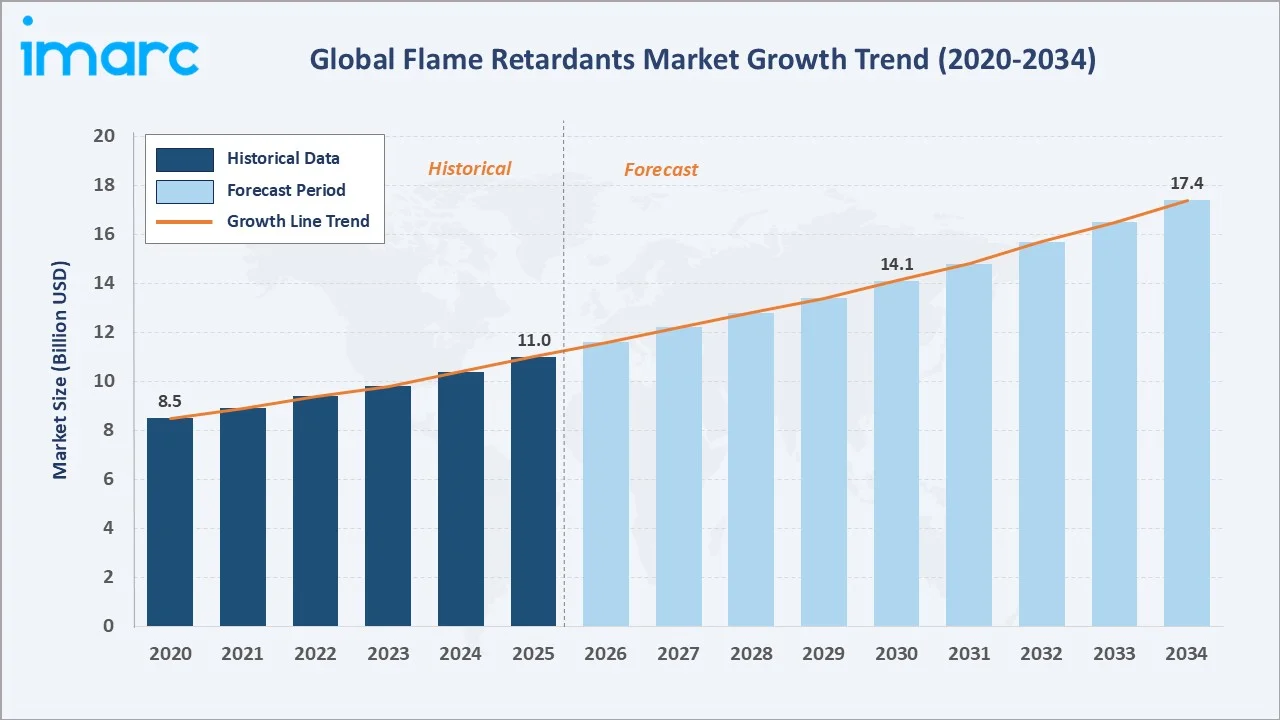

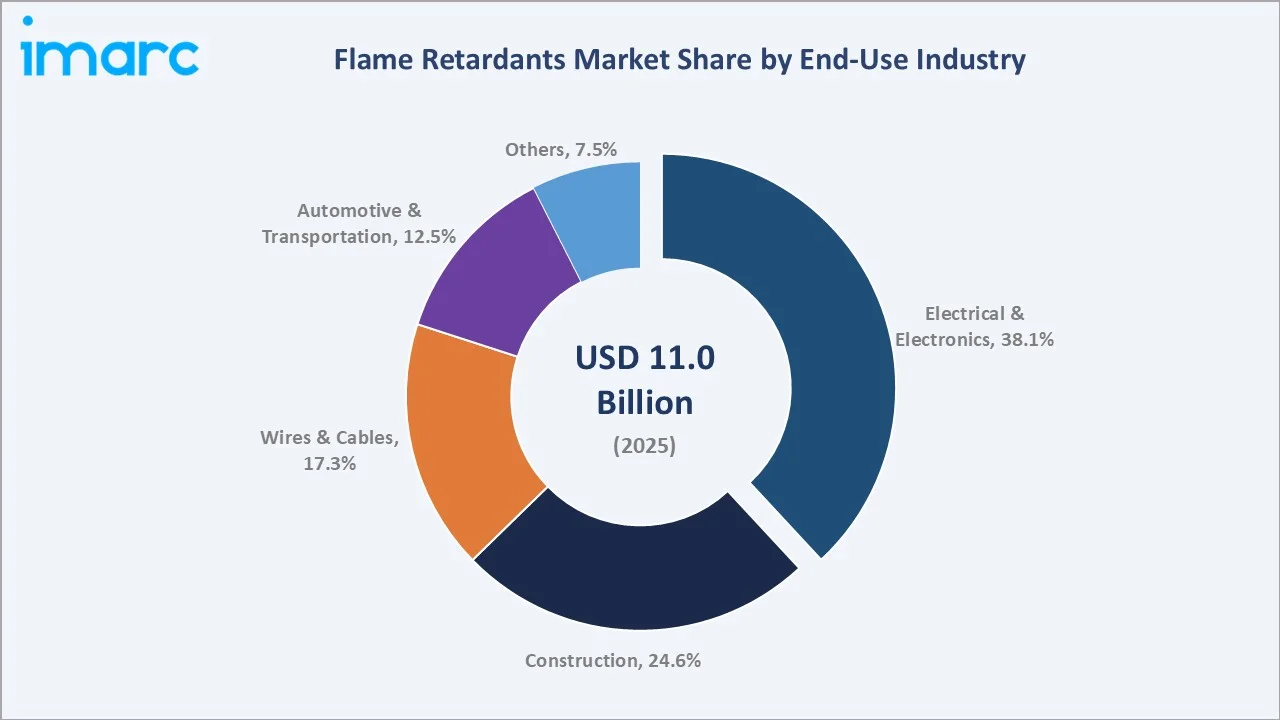

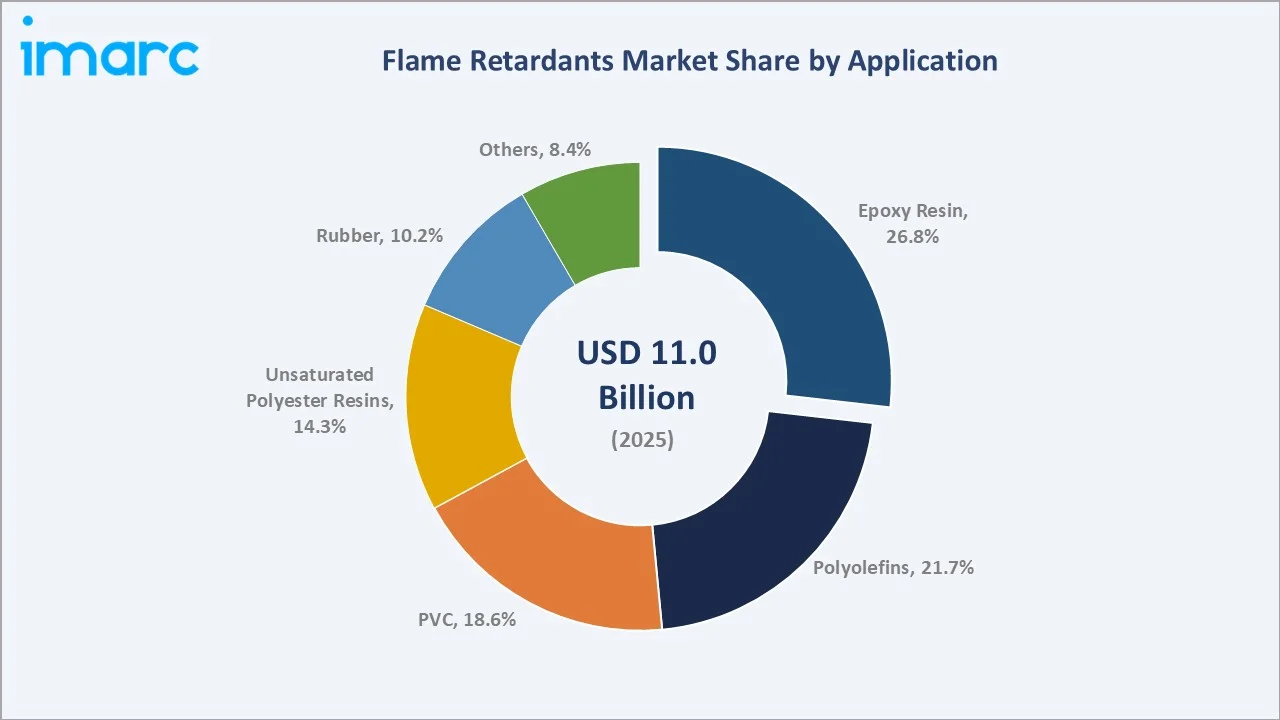

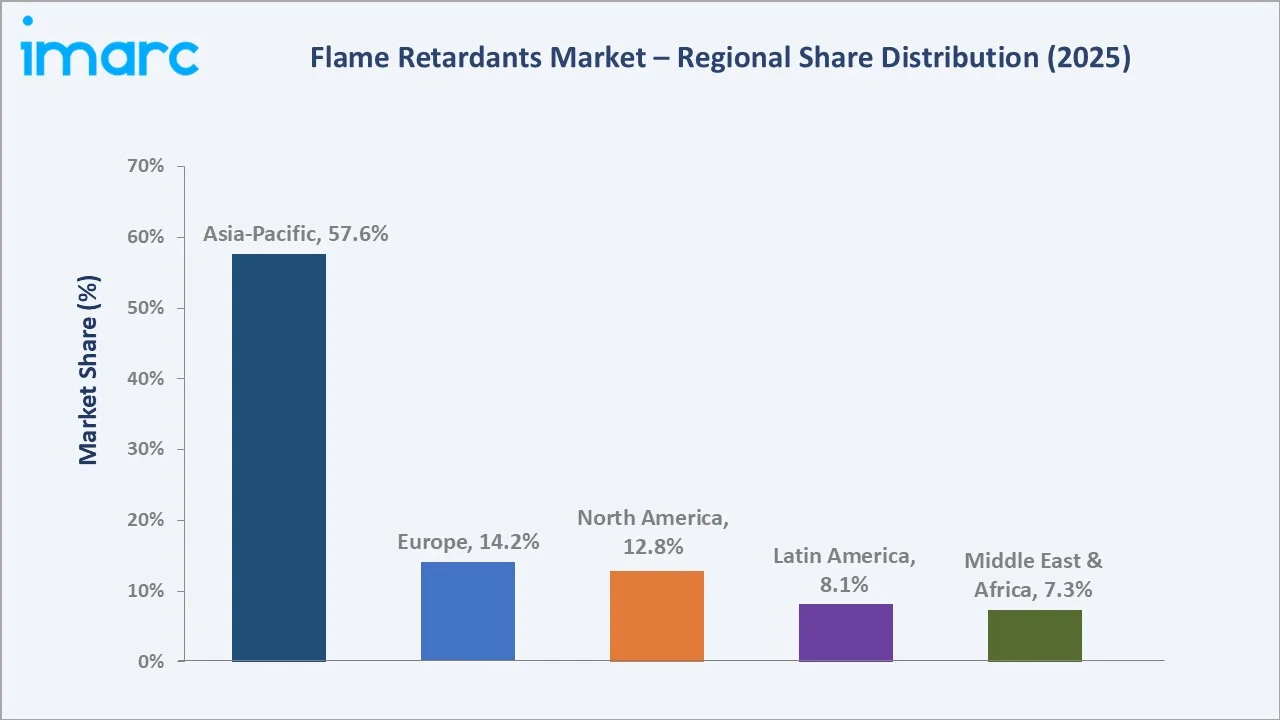

The global flame retardants market size was valued at USD 11.0 Billion in 2025 and is projected to reach USD 17.4 Billion by 2034, exhibiting a CAGR of 5.12% during the forecast period 2026-2034. Tightening fire-safety regulations, rapid expansion of the electrical and electronics sector, rising construction activity, and surging demand from electric vehicle batteries and wiring systems are key growth enablers. Electrical and Electronics leads end-use at 38.1% in 2025, while Epoxy Resin dominates the application segment at 26.8%. Asia-Pacific accounts for 57.6% of global revenue in 2025, anchored by China, India, and South-East Asia manufacturing demand.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 11.0 Billion |

|

Forecast Market Size (2034) |

USD 17.4 Billion |

|

CAGR (2026-2034 |

5.12% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (57.6% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~6.2%) |

|

Leading End-Use Industry |

Electrical and Electronics (38.1%, 2025) |

|

Leading Application |

Epoxy Resins (26.8%, 2025) |

The chart below tracks the global flame retardants market trajectory from 2020 through 2034, contrasting a steady historical expansion base against a sustained forecast curve powered by electrification, rising construction demand, and stricter fire-safety mandates worldwide.

To get more information on this market, Request Sample

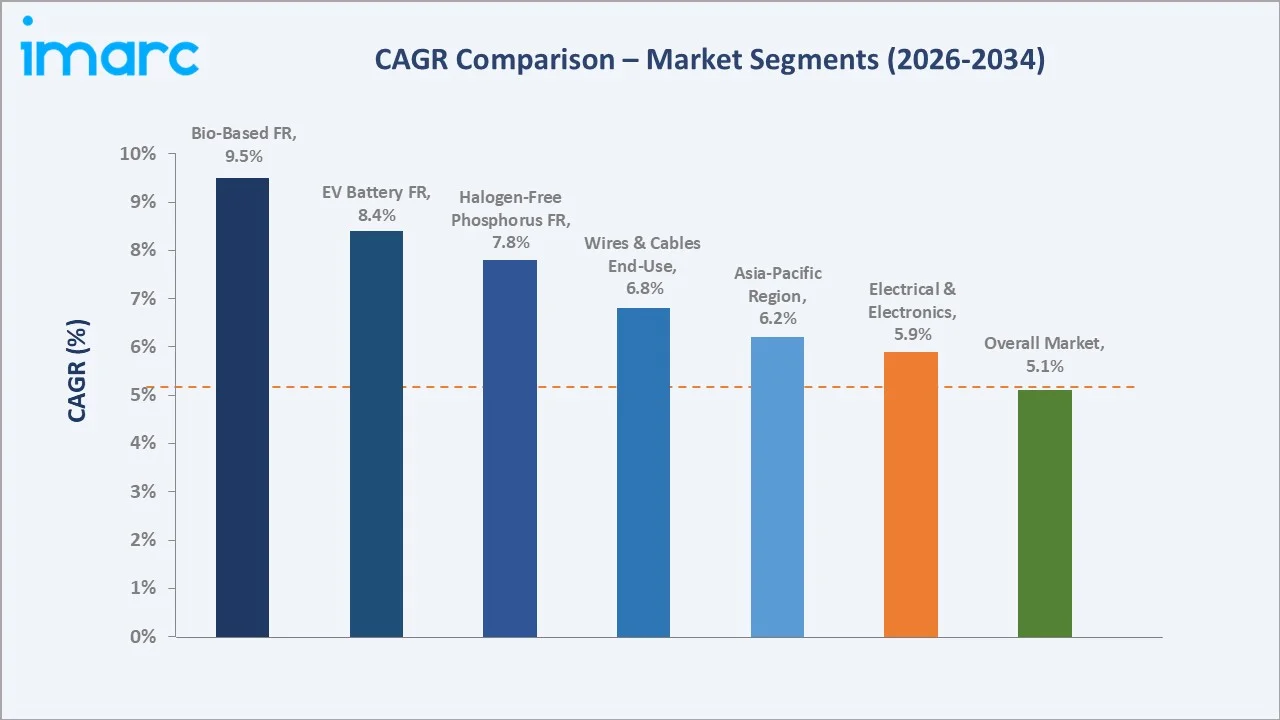

Segment-level CAGR comparisons highlight bio-based and EV battery flame retardants as the two fastest-growing sub-categories within the global flame retardants industry analysis through 2034.

Executive Summary

The global flame retardants market is undergoing a structural shift driven by the convergence of fire-safety regulation, electrification, and sustainability priorities. Valued at USD 11.0 Billion in 2025, the market is forecast to reach USD 17.4 Billion by 2034 at a CAGR of 5.12%. Stricter building codes, rising EV battery pack volumes, and expanded electronics production are collectively enlarging the addressable base year over year.

Electrical and Electronics commands the dominant end-use share at 38.1% in 2025, supported by global consumer electronics shipments and stricter UL 94 V-0 rating requirements across enclosures, PCBs, and connectors. Construction follows at 24.6%, fuelled by large-scale infrastructure programmes in Asia-Pacific and the Gulf region. Within applications, Epoxy Resin leads at 26.8% in 2025, reflecting heavy use in PCB laminates, coatings, and composite structures.

Asia-Pacific dominates with a 57.6% global revenue share in 2025, led by China as the world's largest flame retardant producer and consumer, alongside India's rapid electronics and construction build-out. Europe holds 14.2% and North America 12.8%, both shaped by REACH-driven halogen-free transitions and advanced polymer formulation ecosystems.

Key Market Insights

|

Insight |

Data |

|

Largest End-Use Industry |

Electrical and Electronics - 38.1% share (2025) |

|

Leading Application |

Epoxy Resins - 26.8% share (2025) |

|

Leading Region |

Asia-Pacific - 57.6% revenue share (2025) |

|

Second Region |

Europe - 14.2% revenue share (2025) |

|

Top Companies |

Albemarle Corporation, LANXESS, ICL Group, Clariant, Nabaltec AG, Huber Engineered Materials, DIC Corporation, Italmatch Chemicals S.p.A, RTP Company, and DAIHACHI Chemical |

Key Analytical Observations Supporting the Above Data Points:

- Electrical and Electronics accounted for 38.1% share in 2025, underpinned by stricter UL 94 V-0 standards and rising global consumer electronics shipments, with the printed circuit board market alone exceeding USD 90 Billion in 2024.

- Epoxy Resins led applications at 26.8% in 2025, driven by PCB laminate demand, wind turbine composites, and protective coatings where fire-safety certification is mandatory.

- Asia-Pacific's 57.6% dominance in 2025 reflects China’s role as the world’s largest electronics hub, producing ~70% of smartphones and 60% of laptops, alongside a strong regional polymer and composite manufacturing base.

Global Flame Retardants Market Overview

Flame retardants are chemical additives incorporated into polymers, textiles, coatings, and composites to inhibit ignition, slow flame propagation, and reduce smoke generation during combustion. Major chemistries include brominated, phosphorus-based, nitrogen-based, and inorganic mineral compounds such as aluminium trihydrate and magnesium hydroxide.

Applications span electrical and electronics enclosures, construction insulation, wires and cables, automotive interiors, EV battery packs, and industrial textiles. Macroeconomic drivers include global construction output exceeding USD 15 Trillion in 2024, electric vehicle sales crossing 17 Million units, and the International Code Council's continued tightening of fire-safety provisions across various countries.

Market Dynamics

To evaluate market opportunities, Request Sample

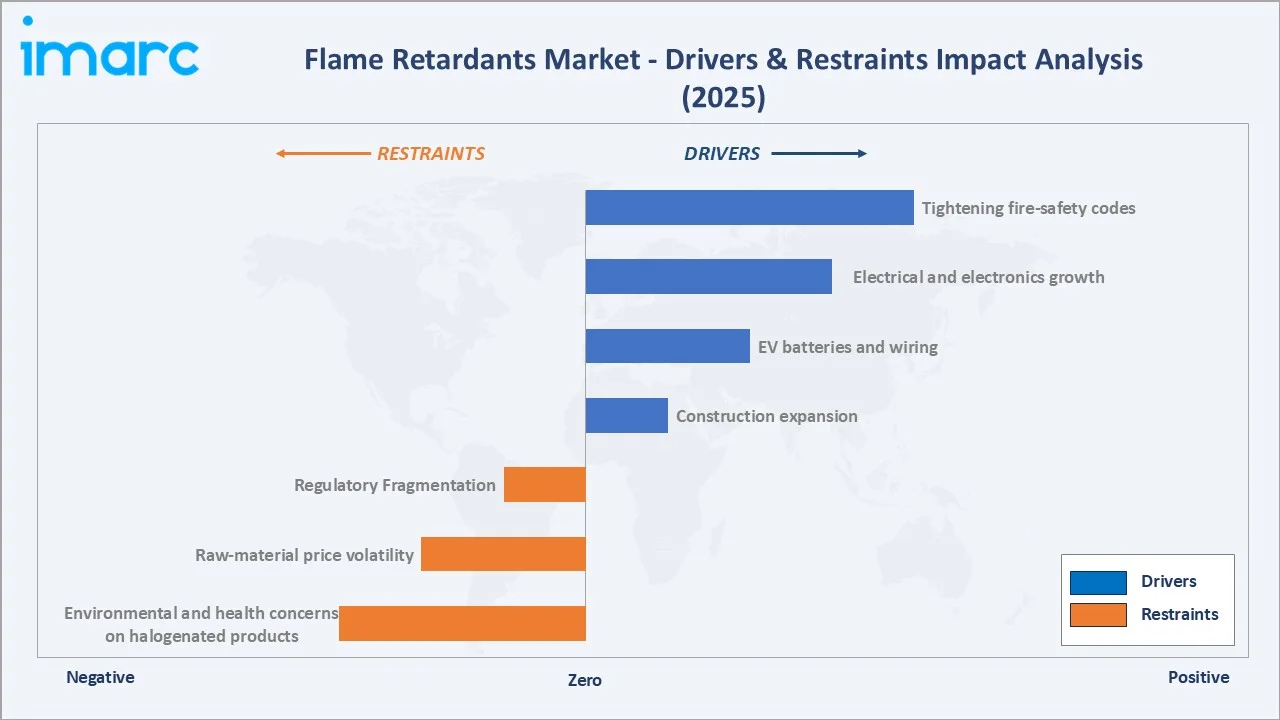

Market Drivers

Structural demand is anchored in regulation, electrification, and infrastructure growth. These three forces jointly explain why the market has expanded from USD 8.5 Billion in 2020 to USD 11.0 Billion in 2025.

- Tightening fire-safety codes: The European CPR, US NFPA standards, and China GB codes increasingly require flame-retarded polymers in insulation, cabling, and enclosures, directly lifting per-building flame retardant intensity.

- Electrical and electronics growth: Global consumer electronics revenue crossed USD 1 Trillion in 2024, driving UL 94 V-0 rated flame retardant use across smartphones, data-centre servers, and appliances.

- EV batteries and wiring: Electric vehicle sales of 17 Million units in 2024 require flame-retarded battery pack housings, separator films, and high-voltage wire insulation at levels far above ICE vehicles.

- Construction expansion: Global construction output reached USD 15 Trillion in 2024, combined with high-rise fire-safety compliance, is expanding mineral-based flame retardant volumes in insulation boards and cable trays.

Market Restraints

- Environmental and health concerns on halogenated products: Certain brominated flame retardants face restrictions under EU REACH and the Stockholm Convention, forcing costly reformulation cycles for downstream compounders.

- Raw-material price volatility: Bromine, antimony trioxide, and phosphorus intermediates saw price swings in 2023-2024, pressuring margins for mid-sized formulators.

- Technical trade-offs: High flame retardant loadings in halogen-free systems can reduce mechanical strength and processing ease, creating formulation challenges for engineering plastics producers.

Market Opportunities

- Halogen-free and bio-based chemistries: Phosphorus, nitrogen, and mineral-based systems are replacing brominated grades in EU and North American programmes, opening premium-priced reformulation revenue opportunities.

- EV battery pack safety: Thermal-runaway mitigation is driving new flame retardant specifications across cell-to-pack architectures, with leading OEMs including BYD, Tesla, and CATL expanding fire-protection chemistry partnerships.

- Data-centre and 5G infrastructure: Global data-centre capital expenditure reached USD 290 Billion in 2024, creating demand for flame-retarded cable sheathing and low-smoke-zero-halogen (LSZH) compounds.

Market Challenges

- Regulatory fragmentation: Divergent chemical restrictions across the EU, US EPA, and Chinese MEE frameworks raise compliance complexity and slow product launches.

- Recyclability friction: Flame retardants can complicate polymer recycling, conflicting with circular-economy targets and creating pressure to develop recycling-compatible chemistries.

- Supply-chain concentration: Over 70% of global antimony trioxide originates from China, creating geopolitical and pricing risk for formulators in Europe and North America.

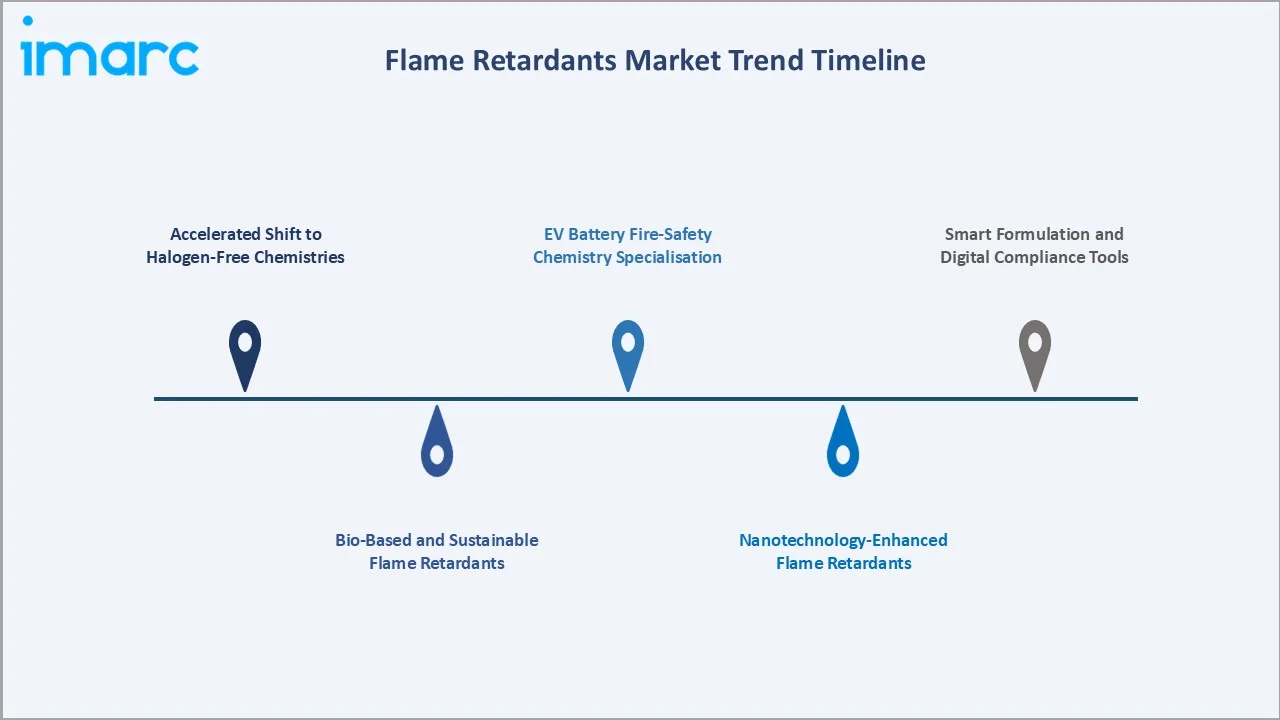

Emerging Market Trends

Five trend vectors are reshaping the competitive logic of the flame retardants market through 2034, from chemistry substitution to sustainability-linked product design.

1. Accelerated Shift to Halogen-Free Chemistries

OEMs in consumer electronics, automotive, and construction are prioritising phosphorus, nitrogen, and mineral-based flame retardants. This transition is reinforced by REACH restrictions on select brominated grades and corporate sustainability mandates at firms such as Apple, Samsung, and Dell.

2. Bio-Based and Sustainable Flame Retardants

Manufacturers are commercialising flame retardants derived from phytic acid, lignin, and chitosan derivatives. These bio-based systems target building insulation, textiles, and packaging segments where circularity and low toxicity are emerging procurement criteria.

3. EV Battery Fire-Safety Chemistry Specialisation

The surge in EV production has created a dedicated sub-segment for battery-pack flame retardants. Formulations combining intumescent phosphorus systems with ceramic fillers are being deployed in pack housings to delay thermal runaway propagation during cell failures.

4. Nanotechnology-Enhanced Flame Retardants

Nanocomposite flame retardants using layered double hydroxides, montmorillonite clays, and graphene oxide are gaining traction. These additives achieve UL 94 V-0 performance at lower loadings, preserving polymer mechanical properties and reducing part weight.

5. Smart Formulation and Digital Compliance Tools

Leading producers are deploying AI-driven formulation platforms and digital material passports to accelerate REACH and UL certification cycles, shortening time-to-market for halogen-free grades from 24 months to under 12 months in several programmes.

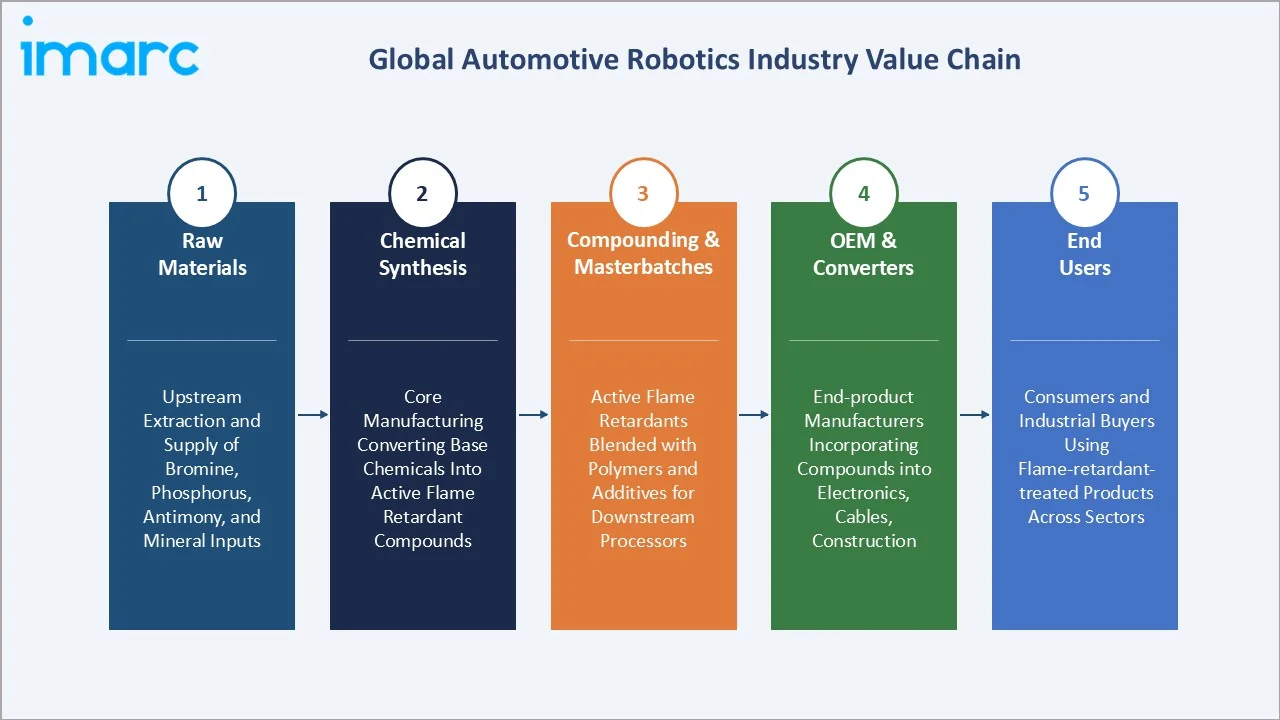

Industry Value Chain Analysis

The flame retardants value chain spans five integrated stages, each with distinct margin profiles, regulatory burdens, and innovation intensities.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Upstream extraction and supply of bromine, phosphorus, antimony, and mineral inputs used in flame retardant formulations. |

|

Chemical Synthesis |

Core manufacturing stage where base chemicals are converted into active flame retardant compounds and molecules. |

|

Compounding & Masterbatches |

Active flame retardants are blended with polymers and additives to create application-ready compounds for downstream processors. |

|

OEM & Converters |

End-product manufacturers incorporate flame-retardant compounds into electronics, cables, construction materials, and automotive components. |

|

End Users |

Final consumers and industrial buyers are using flame-retardant-treated products across residential, commercial, electronics, and transportation sectors. |

Chemical synthesis and compounding stages capture the highest margins, driven by IP-protected flame retardant grades. Compounders convert specialty additives into certified polymer masterbatches for tier-1 OEM supply.

Technology Landscape in the Flame Retardants Industry

Chemistry Innovation and Halogen-Free Systems

Phosphorus-based flame retardants, including DOPO and ammonium polyphosphate, are gaining share across engineering plastics. In 2025, Clariant completed a ~€107 million expansion of its Daya Bay, China Exolit OP facility, launching new UL 94 V-0 halogen-free grades for PBT e-mobility applications.

Materials and Nanocomposite Advances

Next-generation mineral flame retardants use high-surface-area aluminium trihydrate and magnesium hydroxide grades. Nabaltec's nanoscale ATH products enable up to 12% lower polymer loading while achieving equivalent UL 94 ratings in wire and cable compounds.

Smart Connectivity in Formulation Design

AI-based formulation design is emerging at firms including BASF and LANXESS. In January 2025, BASF launched flame retardant grade of Ultramid T6000 FR, designed for EV terminal block applications, replacing non-FR material and enhancing safety for inverter and motor systems.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Brominated Flame Retardants | 🔒 | 2025 |

| Application | Epoxy Resins | 26.8% | 2025 |

| End Use Industry | Electrical and Electronics | 38.1% | 2025 |

| Region | Asia Pacific | 57.6% | 2025 |

By End-Use Industry

Electrical and Electronics commands a 38.1% majority share in 2025, reflecting the universal UL 94 V-0 requirement across consumer electronics enclosures, PCB laminates, connectors, and data-centre hardware. The segment benefits from global smartphone shipments reaching approximately 1.24 billion units in 2025.

To access detailed market analysis, Request Sample

Construction captured 24.6% in 2025, driven by fire-safety regulations in insulation foams, wall panels, and cable management. Wires and Cables holds 17.3%, lifted by 5G, data-centre, and EV charging cable demand. Automotive and Transportation accounts for 12.5%, with EV battery-pack fire safety emerging as the fastest-growing sub-use. Others (7.5%) include textiles, furniture, and industrial coatings.

By Application

Epoxy Resin leads at 26.8% in 2025, reflecting PCB laminate demand, wind turbine blade composites, and industrial coatings where flame-retardant epoxy formulations are mandatory for safety certification.

Polyolefins holds 21.7% in 2025, reflecting polyethylene and polypropylene use in cables, pipes, and packaging. PVC represents 18.6%, supported by construction profiles and wire jacketing. Unsaturated Polyester Resins at 14.3% serves composites and marine applications. Rubber at 10.2% is tied to automotive hoses, seals, and conveyor belts. Others (8.4%) cover polyamides, polycarbonates, and specialty elastomers.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

57.6% |

China electronics and polymer base, India construction boom, South-East Asia EV assembly expansion |

|

Europe |

14.2% |

REACH halogen-free transition, EV battery plant build-out, stringent construction fire codes |

|

North America |

12.8% |

Data-centre growth, NFPA fire codes, US EV production scale-up, advanced polymer formulation ecosystem |

|

Latin America |

8.1% |

Brazil and Mexico construction activity, growing auto production, electrical grid upgrades |

|

Middle East & Africa |

7.3% |

GCC infrastructure megaprojects, Saudi Vision 2030, rising electrical and cable demand |

Asia-Pacific commands a 57.6% global revenue share in 2025, the most dominant regional position in the flame retardants market. China leads the region, driven by its position as the world's largest producer of electronics, polymers, and cable products. India's construction and electronics output expanded significantly, reinforcing the region's demand lead. Japan and South Korea contribute through specialty halogen-free phosphorus chemistries serving premium electronics and EV battery applications.

Europe, at 14.2% in 2025, is shaped by REACH regulations, which have accelerated halogen-free substitution across the electrical and construction sectors. Germany, France, and the United Kingdom collectively account for approximately 60% of regional demand. North America at 12.8%, is anchored by the US data-centre expansion, EV plant build-out by Ford and GM, and stringent NFPA fire codes.

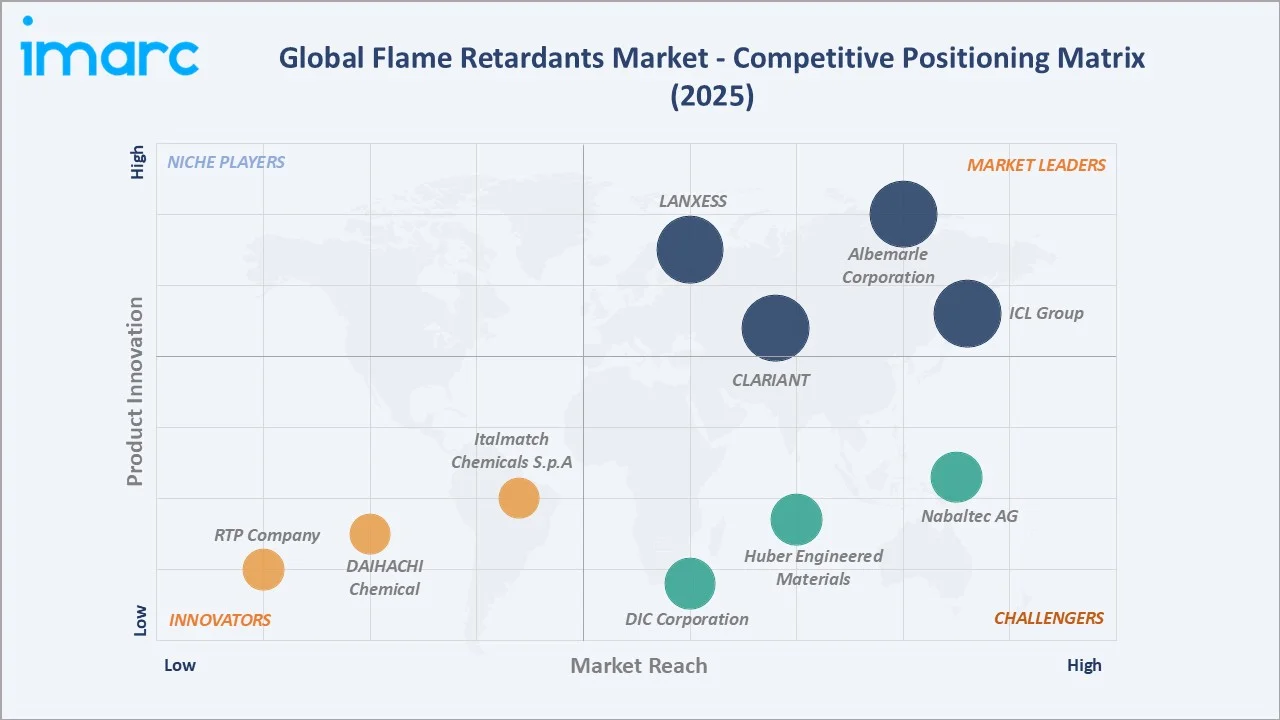

Competitive Landscape

|

Company Name |

Key Brand / Product |

Position |

Core Strength |

|

Albemarle Corporation |

SAYTEX |

Leader |

Bromine production, global scale |

|

LANXESS |

Disflamoll, Levagard |

Leader |

Phosphorus grades, EU leadership |

|

ICL Group |

FR-245, VeriQuel |

Leader |

Bromine and phosphorus range |

|

CLARIANT |

Exolit OP |

Leader |

Halogen-free portfolio |

|

Nabaltec AG |

APYRAL, APYMAG |

Challenger |

Mineral-based ATH, magnesium hydroxide |

|

Huber Engineered Materials |

MARTINAL, HYMOD |

Challenger |

Mineral fillers for cables |

|

DIC Corporation |

FUNECON |

Challenger |

Asia-Pacific reach, epoxy grades |

|

Italmatch Chemicals S.p.A |

PHOSLITE, MASTERET |

Emerging |

Specialty phosphorus grades |

|

RTP Company |

RTP Flame Retardant |

Emerging |

Custom compounds |

|

DAIHACHI Chemical |

DAIGUARD, CR-733S |

Emerging |

Japan-based phosphorus specialist |

The competitive landscape shows moderate consolidation at the chemistry tier, with Albemarle, LANXESS, and ICL collectively holding an estimated 35-40% of global revenue in 2025. Mid-tier specialists, including Nabaltec and Italmatch, are expanding through halogen-free innovation.

Key Company Profiles

Albemarle Corporation

Albemarle is among the world's largest producers of brominated flame retardants, headquartered in the United States with global operations across its specialty chemicals portfolio.

- Product & Brand Portfolio: Saytex brominated flame retardants, Antiblaze phosphorus systems, and specialty high-performance polymer additives for electronics, construction, and automotive.

- Recent Developments: In 2023, Albemarle's multi-year $540 million bromine facility expansion at Magnolia, Arkansas, increased capacity for its Saytex brominated flame retardants to serve growing fire-safety demand in EVs, electronics, and construction.

- Strategic Focus: Albemarle is prioritising next-generation polymeric brominated grades that address environmental concerns while maintaining UL 94 V-0 performance, alongside expanded phosphorus-based offerings for halogen-free segments.

LANXESS

LANXESS is a leading European specialty chemicals company with a strong flame retardants portfolio centred on phosphorus and brominated grades, serving automotive, electronics, and construction end-markets.

- Product & Brand Portfolio: Disflamoll phosphate esters, Levagard alkyl phosphates, and brominated aromatic flame retardants targeting engineering thermoplastics, polyurethanes, and epoxy systems.

- Recent Developments: In 2025, LANXESS exhibited at K 2025 in Düsseldorf, showcasing new flame retardants, including Levagard 2100, a reactive phosphonate that chemically bonds into the polymer for lower VOC emissions and enhanced durability.

- Strategic Focus: LANXESS is accelerating its halogen-free transition, investing in phosphorus-based chemistries, and deepening partnerships with European EV and construction OEMs to capture premium-priced reformulation demand.

CLARIANT

Clariant is a Swiss specialty chemicals group with a flame retardants business anchored in halogen-free phosphorus chemistry, particularly the Exolit OP product line targeting electrical, electronics, and transport applications.

- Product & Brand Portfolio: Exolit OP phosphorus-based flame retardants, AddWorks additive packages, and Exolit AP ammonium polyphosphate grades for engineering plastics, polyamides, and thermoset composites.

- Recent Developments: In 2023, Clariant inaugurated a new CHF 100 million Exolit OP halogen-free flame retardant plant in Daya Bay, China, serving rapidly growing EV, E&E, 5G, and infrastructure demand from Asian customers, supplementing its two existing plants in Knapsack, Germany.

- Strategic Focus: Clariant's strategy centres on halogen-free leadership, sustainable chemistries, and close OEM collaboration with automotive and electronics tier-1 suppliers to secure long-term supply agreements.

Market Concentration Analysis

The global flame retardants market exhibits moderate concentration at the top tier, with Albemarle, LANXESS, ICL, Clariant, and Nabaltec collectively accounting for approximately 45-52% of global revenue in 2025. The remaining share is distributed across regional compounders and specialty chemistry houses.

Consolidation trends are active at the premium end: the three bromine majors, Albemarle, ICL, and LANXESS, control over 75% of global brominated flame retardant capacity, reflecting the capital intensity of bromine extraction and synthesis.

Fragmentation is visible in the halogen-free space, where over 30 regional players in China, India, and South-East Asia compete on phosphorus and mineral chemistries. Chinese firms, including Kingfa and Wansheng, are scaling rapidly, lifting regional competitive intensity.

Investment & Growth Opportunities

Fastest-Growing Segments

Halogen-free phosphorus flame retardants are the highest-growth sub-category, driven by REACH-linked reformulation. Bio-based flame retardants are growing rapidly from a smaller base, supported by sustainability-linked procurement at consumer electronics OEMs.

Emerging Market Expansion

India's flame retardants market is expanding, underpinned by construction demand and expanding electronics production. South-East Asia, led by Vietnam and Thailand, benefits from EV assembly relocation and data-centre capex.

Venture & Strategic Investment Trends

Notable 2024-2025 transactions include Azelis’s appointment as exclusive U.S. distributor of LANXESS's phosphorus-based flame retardants, including Disflamoll and Levagard product lines, and multiple early-stage venture rounds into bio-based flame retardant start-ups. Chinese players are receiving state-backed investment to localise phosphorus chemistry supply.

Future Market Outlook (2026-2034)

The flame retardants market is projected to expand from USD 11.0 Billion in 2025 to USD 17.4 Billion by 2034 at a CAGR of 5.12%, a significant value expansion underpinned by regulatory tightening, electrification, and infrastructure investment through the forecast period.

Three technology discontinuities will reshape the competitive landscape through 2034. First, halogen-free phosphorus and bio-based systems will progressively displace legacy brominated grades across the EU and North American premium segments. Second, EV battery-pack flame retardants will emerge as a distinct specialised sub-market.

Third, nanocomposite and additive-efficient flame retardants will enable lower polymer loadings, preserving mechanical properties while meeting UL 94 V-0 standards. By 2034, sustainability credentials, recycling compatibility, and end-to-end traceability will become primary purchasing criteria alongside cost and flame retardancy performance.

Research Methodology

Primary Research

Primary research encompassed over 55 structured interviews conducted in 2024-2025 with stakeholders, including R&D directors at flame retardant producers, polymer compounders, OEM material engineers at electronics and automotive tier-1s, regulatory experts on REACH and UL standards, and institutional investors in specialty chemicals.

Secondary Research

Secondary sources include European Chemicals Agency (ECHA) REACH filings, UL Standards publications, NFPA code documents, Stockholm Convention POP decisions, IEA Global EV Outlook, OECD construction statistics, SpecialChem and Polymer Additives Market Intelligence, company annual reports, and trade press, including Plastics News and Chemical Week.

Forecasting Models

Market sizing combined top-down and bottom-up approaches, incorporating polymer consumption data, regional fire-code compliance rates, and historical flame retardant intensity metrics. Scenario analysis tested base, optimistic, and conservative cases around bromine pricing and halogen-free substitution timelines.

Report Coverage

|

Attribute |

Details |

|

Market Size (2025) |

USD 11.0 Billion |

|

Forecast (2034) |

USD 17.4 Billion |

|

CAGR (2026-2034) |

5.12% |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Segmentation |

By End-Use Industry, By Application, By Region |

|

Regional Analysis |

Asia-Pacific, Europe, North America, Latin America, Middle East & Africa |

|

Key Companies |

Albemarle Corporation, LANXESS, ICL Group, Clariant, Nabaltec AG, Huber Engineered Materials, DIC Corporation, Italmatch Chemicals S.p.A, RTP Company, and DAIHACHI Chemical |

|

Report Format |

PDF, Excel |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the flame retardants market from 2020-2034.

- The flame retardants market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the flame retardants industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Flame Retardants Market Report

The global flame retardants market was valued at USD 11.0 Billion in 2025, supported by fire-safety regulations and expanding electrical, construction, and EV demand.

The market is projected to reach USD 17.4 Billion by 2034, growing at a CAGR of 5.12% during 2026-2034, led by electronics, EV, and construction applications globally.

Electrical and Electronics leads with a 38.1% share in 2025, driven by UL 94 V-0 compliance in consumer electronics enclosures, PCB laminates, connectors, and data-centre hardware.

Epoxy Resins dominate with a 26.8% share in 2025, supported by PCB laminates, wind turbine composites, protective coatings, and safety-certified industrial formulations worldwide.

Asia-Pacific leads with a 57.6% share in 2025, driven by China's polymer and electronics base, India's construction boom, and South-East Asia's rapid EV assembly build-out.

Key drivers include tightening fire-safety regulations, rising electrical and electronics output, construction expansion, EV battery and wiring demand, and expanding data-centre capacity globally.

Leading companies include Albemarle Corporation, LANXESS, ICL Group, Clariant, Nabaltec AG, Huber Engineered Materials, DIC Corporation, Italmatch Chemicals S.p.A, RTP Company, and DAIHACHI Chemical.

REACH restrictions on select brominated grades are accelerating halogen-free substitution, creating premium-priced opportunities in phosphorus and mineral chemistries across European electronics and construction segments.

Flame retardants mitigate thermal runaway in EV battery packs, protecting pack housings, separator films, and high-voltage cable insulation, specified by OEMs including Tesla, BYD, and CATL.

Halogen-free flame retardants use phosphorus, nitrogen, or mineral chemistries to inhibit combustion without releasing halogens, enabling low-smoke low-toxicity performance in electronics, cables, and construction materials.

Bio-based flame retardants derived from phytic acid, lignin, and chitosan are scaling rapidly in building insulation, textiles, and packaging, supported by corporate sustainability and circular-economy mandates.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade