Flavors and Fragrances Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2026-2034

Global Flavors and Fragrances Market Size, Share, Trends & Forecast (2026-2034)

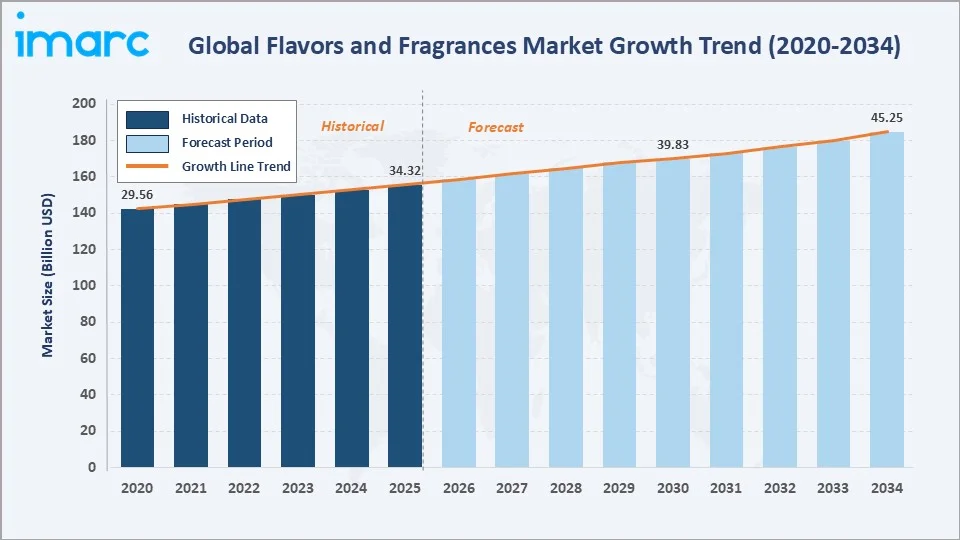

The global flavors and fragrances market size reached USD 34.32 Billion in 2025 and is projected to reach USD 45.25 Billion by 2034, exhibiting a CAGR of 3.03% during 2026-2034. Rising consumer demand for processed foods, personal care products, and premium fine fragrances are the primary forces driving market growth.

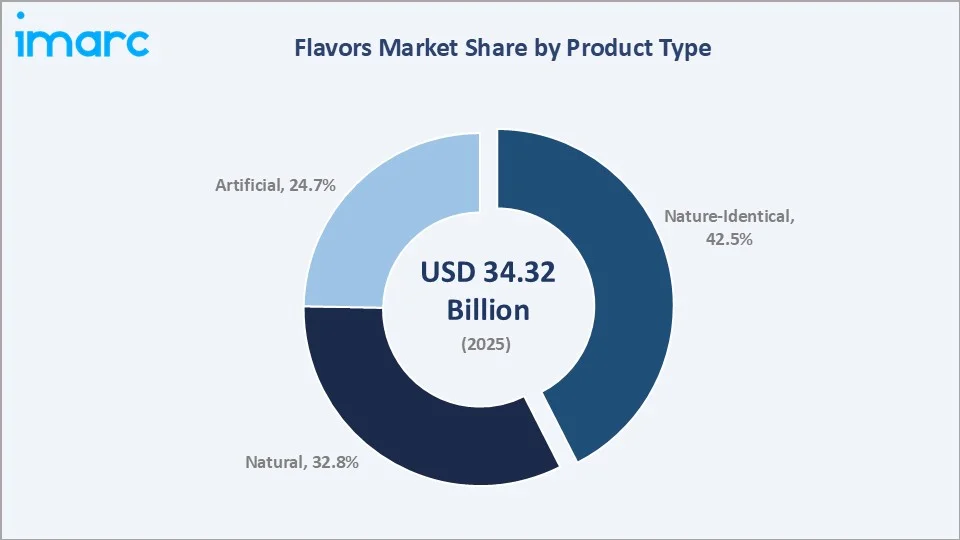

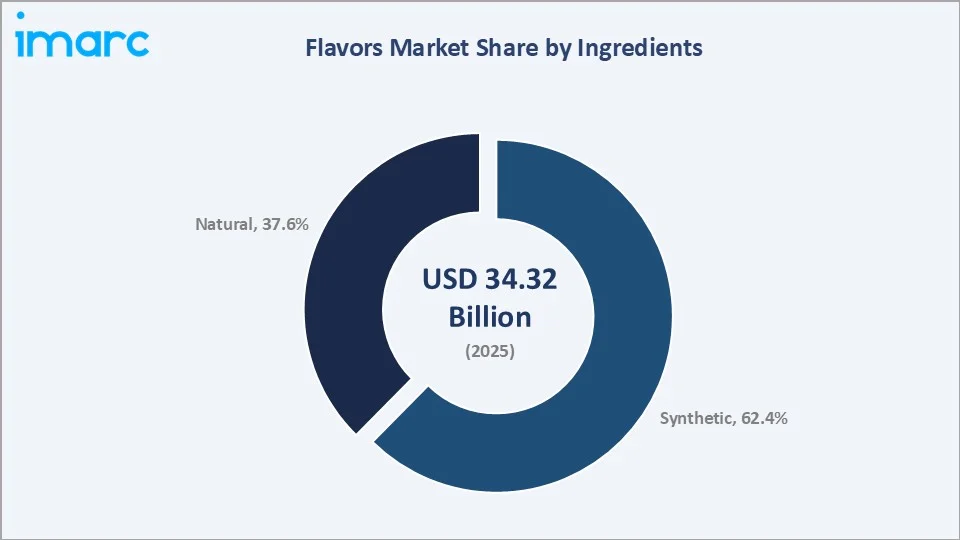

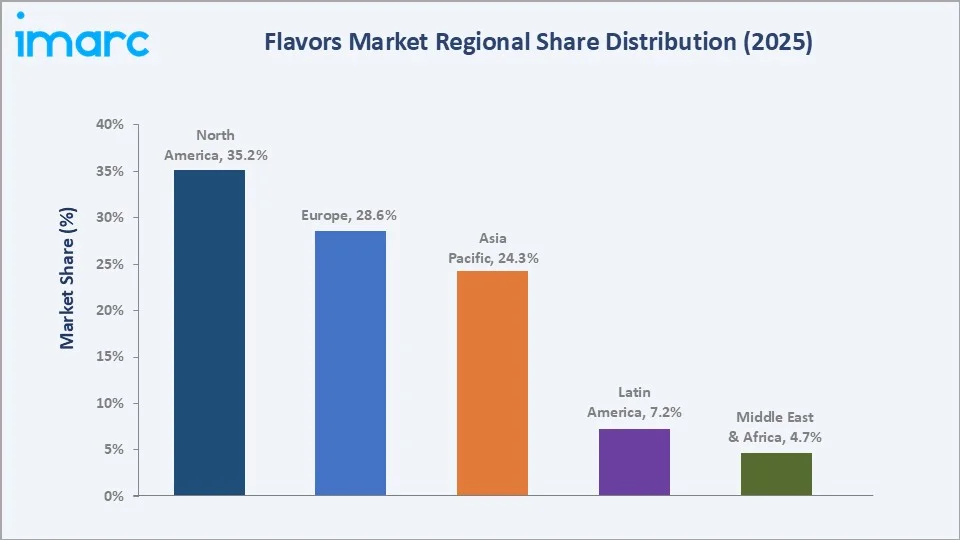

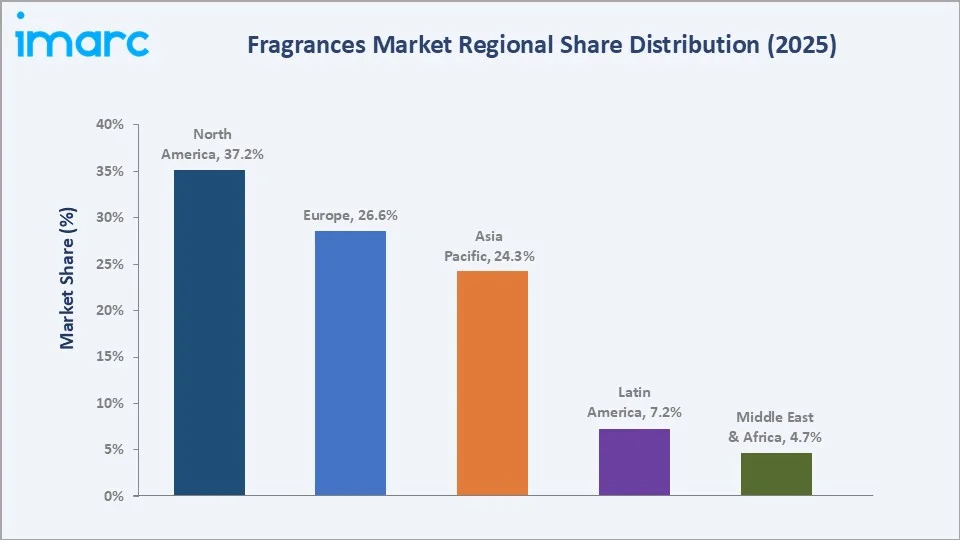

Nature-identical flavors dominate the product type segment at 42.5% in 2025, while synthetic fragrances lead the ingredients segment at 62.4%. North America commands the largest regional share at 35.2% for flavors and 37.2% for fragrances, reflecting strong food processing and personal care industries.

Market Snapshot

|

Metric |

Value |

| Market Size (2025) | USD 34.32 Billion |

| Forecast Market Size (2034) | USD 45.25 Billion |

| CAGR (2026-2034) | 3.03% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Largest Region (Flavors) | North America (35.2% share, 2025) |

| Largest Region (Fragrances) | North America (37.2% share, 2025) |

| Leading Flavor Product Type | Nature-Identical (42.5%, 2025) |

| Leading Fragrance Ingredient | Synthetic (62.4%, 2025) |

The global flavors and fragrances market growth trajectory from 2020 through 2034 reflects consistent demand from food, beverage, and personal care sectors. The forecast to USD 45.25 Billion captures accelerating clean-label trends, premiumization, and expanding markets in Asia Pacific and Latin America.

To get more information on this market, Request Sample

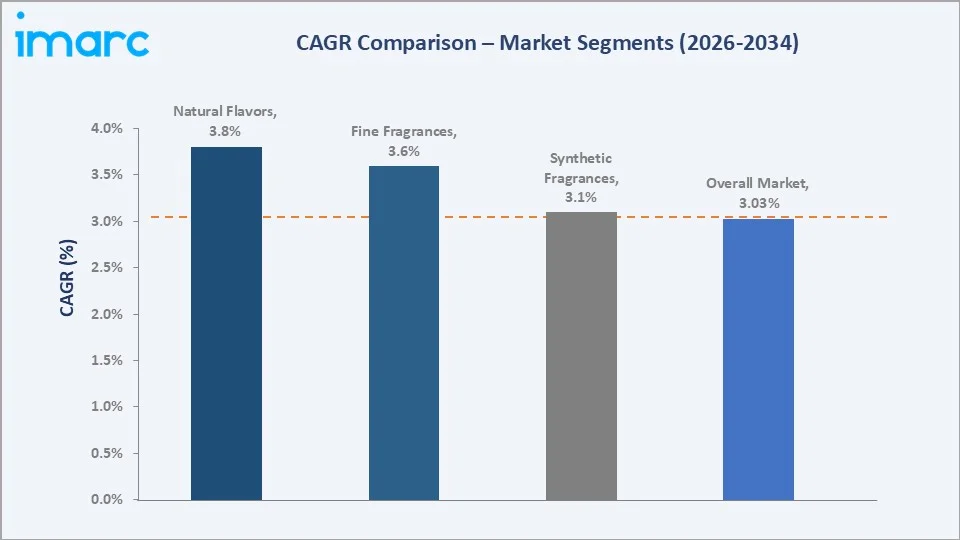

The CAGR trajectories across key sub-segments, with natural flavors at ~3.8% CAGR and fine fragrances at ~3.6% CAGR, are among the fastest-growing categories within the global flavors and fragrances industry analysis through 2034.

Executive Summary

The global flavors and fragrances market is on a sustained growth trajectory from USD 34.32 Billion in 2025 to USD 45.25 Billion by 2034. Flavors and fragrances are essential inputs for food, beverage, personal care, and household products, benefiting from the non-discretionary nature of consumer demand.

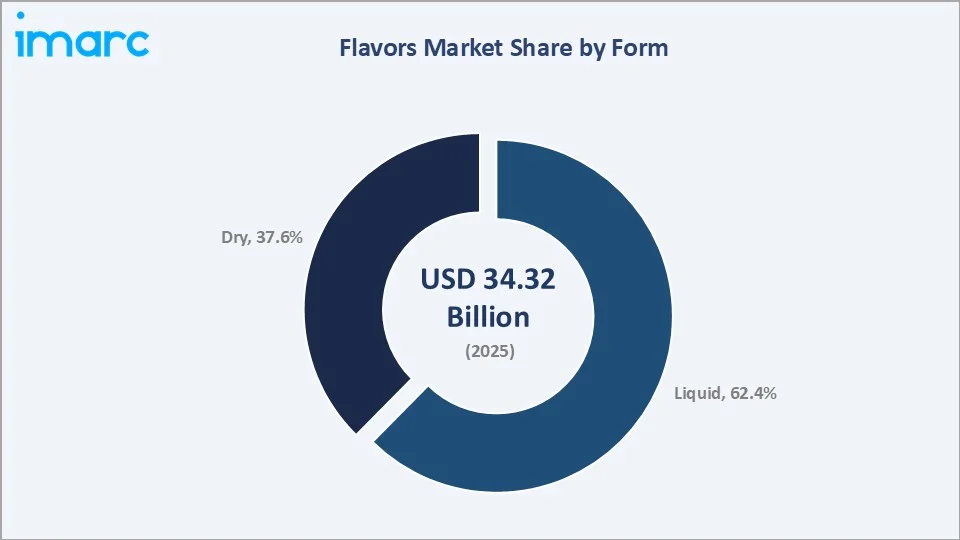

Nature-identical flavors dominate at 42.5% in 2025, prized for their cost-effectiveness and consistent sensory profile. Natural flavors (32.8%) command premium pricing driven by clean-label trends. Liquid form leads at 62.4%, reflecting its ease of integration in beverage and food applications.

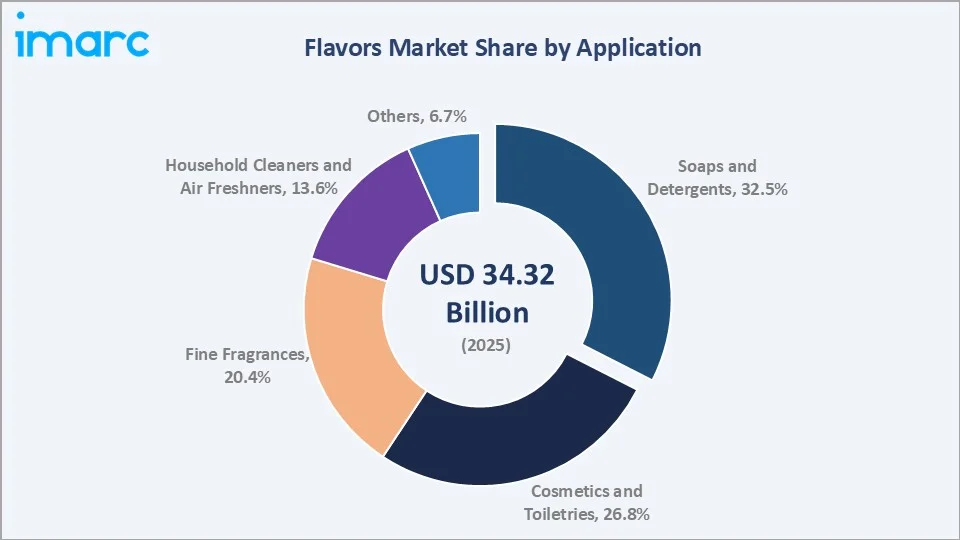

Synthetic fragrances lead at 62.4% for ingredients, providing cost efficiency and olfactory consistency for mass-market products. Soap and detergents represent the largest fragrance application at 32.5%, followed by cosmetics and toiletries at 26.8%.

North America leads both flavor (35.2%) and fragrance (37.2%) segments in 2025, supported by a mature food processing sector and strong personal care demand. Europe and Asia Pacific follow, with Asia Pacific showing significant long-term growth potential.

Key Market Insights

|

Insight |

Data |

| Leading Flavor Product Type | Nature-Identical – 42.5% share (2025) |

| Leading Fragrance Ingredient | Synthetic – 62.4% share (2025) |

| Leading Flavor Form | Liquid – 62.4% share (2025) |

| Leading Fragrance Application | Soap and Detergents – 32.5% (2025) |

| Leading Region (Flavors) | North America – 35.2% share (2025) |

| Leading Region (Fragrances) | North America – 37.2% share (2025) |

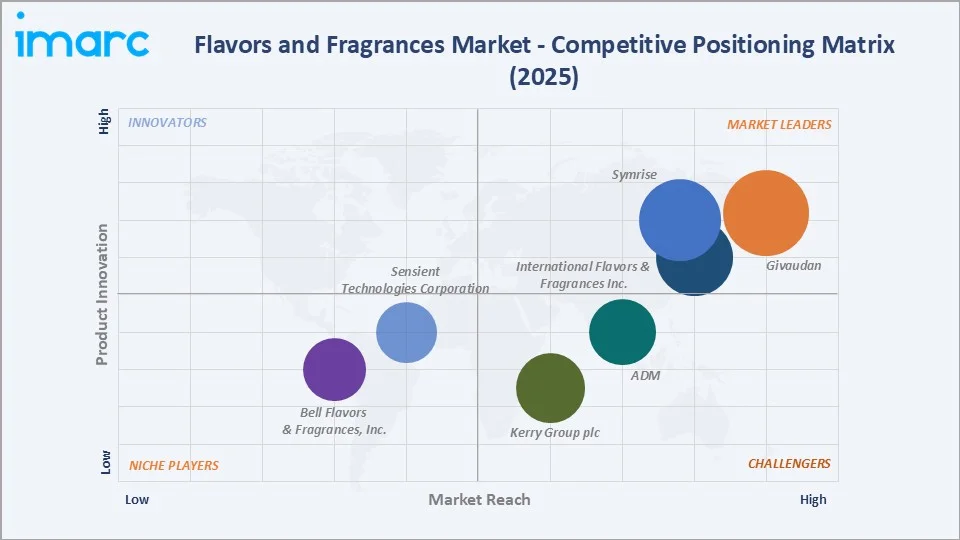

| Key Companies | ADM, Bell Flavors & Fragrances, Inc., Givaudan, International Flavors & Fragrances Inc., Kerry Group plc, Sensient Technologies Corporation, Symrise |

Key Analytical Observations Expanding On The Above Data:

- Nature-identical flavors, with 42.5% in 2025, dominate because they replicate natural taste profiles at significantly lower production costs, making them the preferred choice for mass-market food and beverage applications globally.

- Synthetic fragrances, with 62.4% in 2025, lead due to their superior stability, consistency, and cost advantages over natural alternatives, remaining indispensable in high-volume applications such as soaps, detergents, and household cleaners.

- North America's 35.2% flavors dominance reflects its position as home to the world's largest food and beverage manufacturers, including PepsiCo, Nestlé USA, and Kraft Heinz, creating concentrated procurement demand.

- Soap and detergents at 32.5% lead fragrance applications due to the high fragrance loading levels required in personal and household hygiene products, creating sustained volume demand from FMCG manufacturers worldwide.

Global Flavors and Fragrances Market Overview

Flavors are substances added to food and beverages to impart, modify, or enhance taste and aroma. They are classified as natural, nature-identical, and artificial, delivered in liquid, dry, or encapsulated forms across beverages, dairy, bakery, confectionery, and savory applications.

Fragrances are complex mixtures of aroma compounds used in personal care, household, and fine fragrance products. They are formulated from natural ingredients such as essential oils and extracts, as well as synthetic aroma chemicals, regulated by IFRA guidelines for safety and application standards.

The global ecosystem integrates raw material suppliers, flavor and fragrance houses, formulators, distributors, and diverse end-use industries. Leading companies such as Givaudan, IFF, and DSM-Firmenich operate globally, with extensive R&D capabilities for custom formulation.

Market Dynamics

To evaluate market opportunities, Request Sample

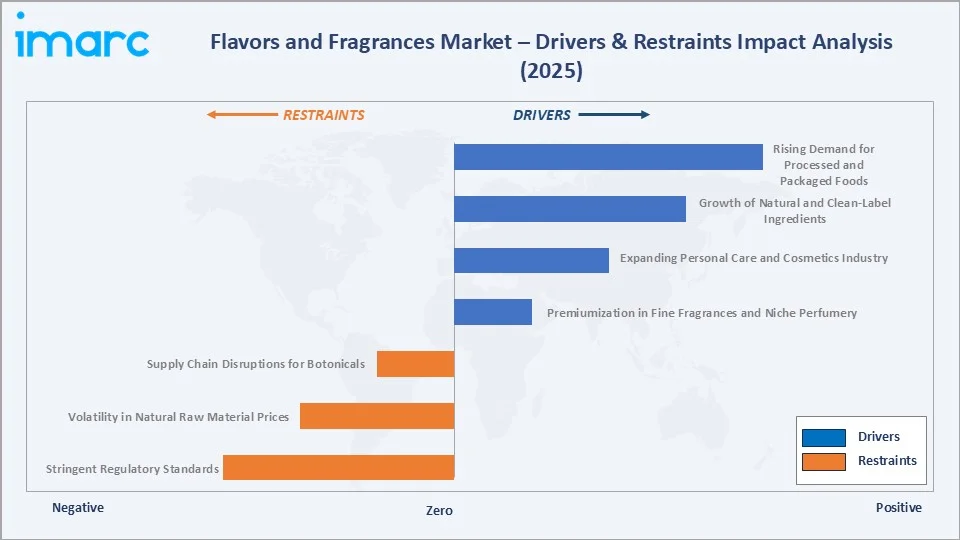

Market Drivers

- Rising Demand for Processed and Packaged Foods: Global urbanization and changing lifestyles are driving consumption of convenience foods, ready-to-eat meals, and packaged beverages, all requiring flavor enhancement to meet evolving consumer taste preferences. U.S. consumers purchase more than 400,000 different packaged food and beverage products each year at grocery stores, with new products constantly being added to shelves, thereby increasing the demand of flavors and fragrances used in the processed and packaged foods.

- Growth of Natural and Clean-Label Ingredients: Consumer preference for transparent ingredient lists is accelerating adoption of natural flavors, botanical extracts, and clean-label fragrance ingredients across food, beverage, and personal care categories globally.

- Expansion of Personal Care and Cosmetics Industry: The global beauty and personal care market, driven by premiumization in skincare and fine fragrances, is generating sustained demand for innovative, long-lasting fragrance formulations and natural aromatic ingredients. By 2025, along with this growth, India will constitute 5% of the total cosmetics market and reach the top five global markets in terms of revenue, thereby increasing the demand of flavors and fragrances used in the personal care and cosmetics industry.

Market Restraints

- Stringent Regulatory Standards: Evolving IFRA, EU, and FDA regulations on permitted flavor and fragrance compounds, including allergen disclosure requirements and restrictions on certain synthetic aroma chemicals, create compliance costs and formulation complexity.

- Volatility in Natural Raw Material Prices: Dependence on agricultural commodities such as citrus, vanilla, rose, and sandalwood exposes natural flavor and fragrance producers to significant supply chain risks from weather events, crop failures, and disruptions.

Market Opportunities

- Biotechnology and Fermentation-Based Ingredients: Advances in precision fermentation and metabolic engineering are enabling cost-effective production of rare natural aroma compounds such as vanillin and sandalwood, reducing reliance on traditional agricultural supply chains.

- Premiumization in Fine Fragrances and Niche Perfumery: The growing luxury fragrance segment, driven by millennial and Gen Z consumers seeking unique scent experiences, is creating opportunities for artisanal fragrance houses and premium ingredient suppliers. In December 2025, LVMH, through its investment arm LVMH Luxury Ventures, acquired a minority stake in BDK Parfums, marking the brand’s first external investment. The partnership is aimed at supporting BDK Parfums’ next phase of growth, particularly by accelerating its international expansion, strengthening distribution channels, and enhancing product development.

Market Challenges

- Consumer Allergy and Safety Concerns: Increasing incidence of fragrance sensitivity and allergic reactions is driving demand for hypoallergenic formulations and greater ingredient transparency, requiring manufacturers to reformulate existing products at significant cost.

- Complexity of Natural Ingredient Authentication: Verifying the authenticity of natural ingredients and preventing adulteration requires advanced analytical technologies such as isotope ratio mass spectrometry and chromatographic fingerprinting.

Emerging Market Trends

1. Clean-Label and Natural Ingredient Demand Reshaping Flavor Portfolios

Consumer preference for natural and clean-label products is transforming flavor development. Food and beverage manufacturers are replacing artificial flavors with natural alternatives, driving growth in botanical extracts, fermentation-derived compounds, and non-GMO certified flavor systems across mainstream CPG categories.

2. AI-Driven Flavor and Fragrance Development Accelerating Innovation

Artificial intelligence and machine learning are revolutionizing flavor and fragrance creation. Companies like Givaudan and IFF are deploying AI platforms that predict consumer preferences, optimize formulations, and accelerate the development cycle from concept to commercial product, reducing time-to-market by up to 50%.

3. Sustainable Sourcing and Green Chemistry Gaining Strategic Priority

ESG commitments and circular economy principles are reshaping ingredient sourcing. Major fragrance houses are implementing blockchain traceability for key botanicals, investing in upcycled ingredients from food waste streams, and adopting green chemistry principles to reduce solvent use and environmental impact.

4. Biotechnology Enabling Cost-Effective Natural Aroma Production

Precision fermentation and synthetic biology are enabling scalable production of high-value natural aroma chemicals. Biotech-derived vanillin, squalane, and iso E super offer consistent quality and sustainable sourcing, addressing supply chain vulnerabilities of traditional agricultural raw materials.

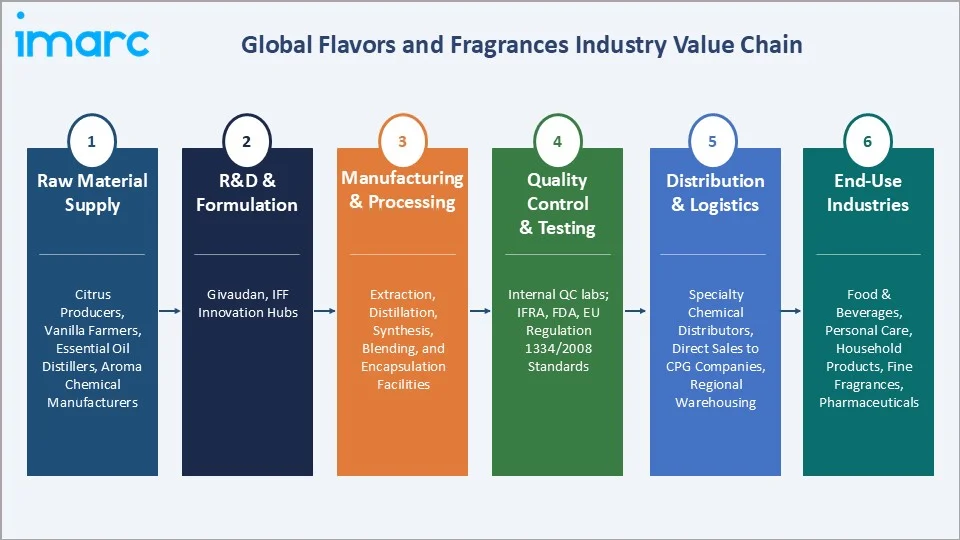

Industry Value Chain Analysis

The flavors and fragrances value chain spans six stages from raw material sourcing through end-use consumer products. R&D and formulation capture the highest value-add margins, while quality control and regulatory compliance generate significant operating cost requirements that favor established mid-to-large manufacturers.

|

Stage |

Key Players / Examples |

| Raw Material Supply | Citrus producers, vanilla farmers, essential oil distillers, aroma chemical manufacturers |

| R&D & Formulation | Givaudan, IFF Innovation Hubs |

| Manufacturing & Processing | Extraction, distillation, synthesis, blending, and encapsulation facilities |

| Quality Control & Testing | Internal QC labs; third-party testing to IFRA, FDA, EU Regulation 1334/2008 standards |

| Distribution & Logistics | Specialty chemical distributors, direct sales to CPG companies, regional warehousing |

| End-Use Industries | Food & Beverages, Personal Care, Household Products, Fine Fragrances, Pharmaceuticals |

Integrated flavor and fragrance manufacturers with captive R&D capabilities and proprietary ingredient libraries, such as Givaudan's naturals platform, achieve differentiated product positioning that commands premium pricing over commodity formula suppliers. This R&D integration is a meaningful competitive advantage.

Technology Landscape in the Flavors and Fragrances Industry

Encapsulation Technology: Protecting Flavor Integrity

Microencapsulation and nano-encapsulation technologies protect volatile flavor compounds from heat, oxidation, and moisture during food processing and storage. Spray drying, fluid bed coating, and coacervation techniques enable controlled release of flavors, extending perceived intensity and shelf life in food products.

Extraction and Isolation: Supercritical CO₂ and Molecular Distillation

Supercritical CO₂ extraction is increasingly adopted for high-value botanical extracts, preserving thermally labile aroma compounds destroyed by steam distillation. Molecular distillation enables isolation of high-purity fractions from complex essential oils, producing premium naturals with consistent sensory profiles.

Digital Formulation: AI and Sensory Analytics

AI-driven formulation platforms analyze vast sensory databases to predict human olfactory and taste responses. Electronic noses and tongues, combined with gas chromatography-olfactometry, accelerate sensory evaluation and enable objective quantification of flavor and fragrance performance attributes.

Market Segmentation Analysis

The report covers the following segments by Flavor:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Product Type | Nature-Identical | 42.5% |

2025 |

| Form | Liquid | 62.4% |

2025 |

| Application | Beverages | 🔒 |

2025 |

| Region | North America | 35.2% |

2025 |

By Product Type (Flavor)

Nature-identical flavors command a 42.5% majority share in 2025, prized for replicating natural taste profiles at commercially viable cost structures. They serve as the default specification across beverages, confectionery, dairy, and snack applications where authentic taste profile is critical but cost-sensitivity limits natural ingredient use.

To access detailed market analysis, Request Sample

Natural flavors at 32.8% in 2025 command premium pricing in premium food and beverage products, growing fastest as clean-label mandates expand globally. Artificial flavors (24.7%) serve cost-sensitive mass-market applications where regulatory acceptance and price competitiveness are the primary selection criteria.

By Form (Flavor)

Liquid flavors dominate the form segment at 62.4% in 2025, reflecting ease of incorporation in beverages, liquid dairy products, sauces, and confectionery coating systems. Liquid formats allow precise dosing, rapid dispersion, and compatibility with standard mixing and filling equipment across food processing operations.

Dry flavors at 37.6% serve bakery, snack seasoning, dry beverage mixes, and infant nutrition applications where moisture stability and extended shelf life are essential. Encapsulated and spray-dried dry flavor forms are growing rapidly in functional food and sports nutrition categories.

The report covers the following segments by Fragrance:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Application | Soap and Detergents | 32.5% |

2025 |

| Ingredients | Synthetic | 🔒 |

2025 |

| Region | North America | 37.2% |

2025 |

By Application (Fragrance)

Soap and detergents lead fragrance applications at 32.5% in 2025, reflecting the high fragrance loading levels used in personal wash, laundry, and dishwashing formulations. Fragrance performance in rinse-off and wash-off systems requires substantivity and stability engineering under alkaline and surfactant-rich conditions.

Cosmetics and toiletries at 26.8% represent the most innovation-intensive segment, driven by premiumization in skincare, haircare, and body care. Fine fragrances at 20.4% command the highest per-unit value. Household cleaners and air fresheners (13.6%) benefit from the wellness home trend globally.

By Ingredients (Fragrance)

Synthetic fragrances dominate at 62.4% in 2025, providing cost efficiency, olfactory consistency, and availability at commercial scale. Synthetic aroma chemicals enable creation of novel olfactory effects impossible with natural materials, underpinning the creative differentiation of fine fragrance houses.

Natural fragrances at 37.6% are growing at a faster rate, driven by clean beauty, COSMOS-certified, and vegan formulation trends. Premium naturals including Grasse rose, oud, and certified organic bergamot command significant price premiums in luxury and niche fragrance categories.

Regional Market Insights

|

Region |

Flavor Share (2025) |

Fragrance Share (2025) |

Key Growth Drivers |

| North America | 35.2% | 37.2% | Mature F&B processing; premium personal care; strong fragrance retail |

| Europe | 28.6% | 26.6% | Clean-label leadership; luxury fine fragrances; strict IFRA compliance |

| Asia Pacific | 24.3% | 24.3% | Rapid urbanization; growing middle class; expanding FMCG sector |

| Latin America | 7.2% | 7.2% | Brazil & Mexico food processing growth; rising personal care adoption |

| Middle East & Africa | 4.7% | 4.7% | Strong oud & oriental fragrance culture; growing halal cosmetics |

North America's 35.2% flavor share and 37.2% fragrance share in 2025 reflect the world's most sophisticated food and personal care markets. The US houses the global headquarters of major CPG companies and maintains high per-capita spend on premium flavor and fragrance-enhanced products.

Europe's combined market leadership in luxury fine fragrances, anchored by the Grasse perfumery tradition and Paris luxury houses, offsets its smaller share in mass-market flavors. REACH and EU Regulation 1334/2008 compliance drive significant reformulation investment from global manufacturers targeting European consumers.

Asia Pacific at 24.3% is the fastest-growing major region for both flavors and fragrances, driven by China's expanding middle class, India's booming FMCG sector, and ASEAN urbanization. Regional taste preferences for umami, fermented, and floral profiles are creating distinct innovation requirements for global flavor and fragrance players.

Competitive Landscape

The global flavors and fragrances market is moderately consolidated, with the top four companies, collectively holding approximately 55-60% of global market revenue. Regional and specialty players hold strong positions in niche ingredient categories and local market knowledge.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

| ADM | Natural flavors, extracts, botanical ingredients | Challenger | Integrated ag supply chain; natural ingredients platform |

| Bell Flavors & Fragrances, Inc. | Flavors, fragrances | Niche | Global mid-market; customized flavor, fragrance, and botanical solutions |

| Givaudan | Flavors, fragrances | Leader | Largest global player; digital formulation leadership |

| International Flavors & Fragrances Inc. | Flavors, fragrances | Leader | Portfolio optimization and divestitures; biosciences and scent leadership |

| Kerry Group plc | Flavors | Challenger | B2B food science; clean-label and health focus |

| Sensient Technologies Corporation | Flavors | Niche | Dual flavor & color platform; pharma and industrial |

| Symrise | Flavors, fragrances | Leader | Balanced portfolio; strong LatAm and APAC presence |

Key players include ADM, Bell Flavors & Fragrances, Inc., Givaudan, International Flavors & Fragrances Inc., Kerry Group plc, Sensient Technologies Corporation, Symrise, and others.

Key Company Profiles

Givaudan

Givaudan is the world's largest flavor and fragrance company, serving food, beverage, personal care, and fine fragrance customers globally. The company's Taste & Wellbeing and Fragrance & Beauty divisions deliver integrated sensory solutions with an industry-leading R&D investment rate.

- Product Portfolio: Taste & wellbeing solutions including flavors, taste modulation, and functional food ingredients; fragrance compounds for fine fragrances, cosmetics, toiletries, and home care.

- Recent Developments: In March 2026, Givaudan expanded its office presence in Turkey, strengthening its footprint in a key growth market for fragrance and beauty. The move is aimed at supporting rising regional demand while enhancing the company’s ability to serve local and nearby markets more effectively.

- Strategic Focus: Givaudan's strategy centers on leading in naturals and health & wellness platforms, capturing premiumization in fine fragrances, and deploying digital tools to accelerate customization and reduce formulation turnaround times for CPG customers.

International Flavors & Fragrances Inc. (IFF)

The company operates across four segments: Taste, Food Ingredients, Scent, Health & Biosciences, serving around 100 countries with a comprehensive ingredient and solution portfolio.

- Product Portfolio: Flavors, fragrances, specialty ingredients.

- Strategic Focus: The company has sharpened its strategic focus through several divestitures and the launch of a sale process for its Food Ingredients segment, improving financial flexibility to direct resources toward its highest-value businesses. IFF is integrating biotechnology into its Health & Biosciences business and reinvesting in R&D and commercial capabilities to advance its innovation pipeline and support long-term profitable growth.

Symrise

Symrise is a global flavor and fragrance company with strong positions in both flavors and fragrances as well as cosmetic ingredients through its Symrise Cosmetic Ingredients unit. The company demonstrates balanced geographic exposure across all major regions.

- Product Portfolio: Flavors (beverage, savory, sweet), fragrances, and cosmetic active ingredients.

- Recent Developments: In November 2020, Symrise AG announced the acquisition of the fragrance and aroma chemicals business unit from Sensient Technologies Corporation. The acquired business includes a diverse portfolio of fragrance ingredients and aroma molecules, many of which are derived from natural and renewable sources. Through this acquisition, Symrise will also broaden its customer base and strengthen its presence across key regions, particularly in Europe, the Middle East and Africa (EAME), as well as Latin America.

- Strategic Focus: Symrise focuses on balanced growth across flavors, fragrances, and cosmetic ingredients, with a differentiated pet nutrition platform providing diversification. Its above-average investment in emerging markets positions it well for Asia Pacific growth through 2034.

Market Concentration Analysis

The global flavors and fragrances market is moderately consolidated at the global level, with the top four companies holding approximately 55-60% of market revenue. Unlike more fragmented industrial goods markets, this industry demonstrates meaningful global-scale consolidation driven by R&D investment requirements and global CPG customer relationships.

Consolidation through M&A has been the primary growth mechanism in this industry. The DSM-Firmenich merger, IFF's acquisition of DuPont N&B, and numerous bolt-on acquisitions by Givaudan and Symrise reflect a strategy of broadening ingredient platforms and acquiring specialty capabilities in naturals and biotechnology.

Investment & Growth Opportunities

Fastest-Growing Segments

Natural flavors at ~3.8% CAGR through 2034 represent the highest-growth flavor type, driven by clean-label mandates and consumer preference for authentic taste profiles. Fine fragrances at ~3.6% CAGR benefit from luxury consumption growth in emerging markets and premiumization in developed markets globally.

Emerging Markets

Asia Pacific at ~4.0% CAGR is the fastest-growing major region for flavors and fragrances through 2034. India's rapidly growing food processing sector, China's premiumizing beauty and personal care market, and ASEAN's expanding FMCG industry are the primary drivers of regional outperformance versus the global average.

Venture & Investment Trends

Private equity and strategic investment in biotechnology-derived flavor and fragrance ingredients is accelerating. Fermentation-based aroma chemical companies are attracting venture capital, while large flavor houses are making equity investments in synthetic biology platforms to secure future natural ingredient supply at scale.

Future Market Outlook (2026-2034)

The global flavors and fragrances market is forecast to expand from USD 34.32 Billion in 2025 to USD 45.25 Billion by 2034 at a CAGR of 3.03%, adding USD 10.93 Billion in incremental annual market value. This consistent growth reflects the market's consumer staples-linked, non-discretionary demand characteristics.

Three strategic forces will most significantly shape the industry through 2034: biotechnology and precision fermentation disrupting traditional supply chains for high-value naturals; AI-driven formulation compressing development cycles; and sustainability imperatives reshaping ingredient portfolios and supplier relationships globally.

Research Methodology

Primary Research

Primary research encompassed over 60 structured interviews in 2024-2025 with flavors and fragrances industry stakeholders, including senior commercial managers at leading fragrance houses, CPG procurement specialists, food technologists, cosmetic chemists, and FEMA and IFRA technical committee members.

Secondary Research

Key secondary sources include IFRA Annual Report (2024), FEMA market data, RIFM fragrance safety database, Euromonitor International consumer packaged goods data, and trade publications including Perfumer & Flavorist, Flavour and Fragrance Journal, and SOFW Journal, supplemented by company annual reports.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis was performed to account for macroeconomic uncertainty and raw material volatility.

Flavors and Fragrances Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

Global Flavors Market

Global Fragrances Market

|

| Product Types Covered | Nature-Identical, Artificial, Natural |

| Forms Covered | Liquid, Dry |

| Applications Covered | Global Flavors Market: Beverages, Dairy and Frozen Desserts, Bakery and Confectionary Products, Savories and Snacks, Others Global Fragrances Market: Soap and Detergents, Cosmetics and Toiletries, Fine Fragrances, Household Cleaners and Air Fresheners, Others |

| Ingredients Covered | Natural, Synthetic |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, United Kingdom, France, Italy, Spain, China, Japan, India, South Korea, Brazil, Argentina, Turkey, Saudi Arabia, Iran, United Arab Emirates |

| Companies Covered | ADM, Bell Flavors & Fragrances, Inc., Givaudan, International Flavors & Fragrances Inc., Kerry Group plc, Sensient Technologies Corporation, Symrise, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the flavors and fragrances market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global flavors and fragrances market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the flavors and fragrances industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Flavors and Fragrances Market Report

The global flavors and fragrances market reached USD 34.32 Billion in 2025, reflecting consistent demand from global food and beverage, personal care, and household product industries.

The market is projected to reach USD 45.25 Billion by 2034, growing at a CAGR of 3.03% during 2026-2034, driven by clean-label trends, premiumization, and Asia Pacific market expansion.

Nature-identical flavors lead with a 42.5% product type share in 2025, valued for replicating natural taste profiles at cost-effective price points for mass-market food and beverage manufacturers.

Synthetic fragrances lead at 62.4% in 2025, representing the most cost-efficient and consistent ingredient source for high-volume applications in soaps, detergents, and household care products.

Liquid flavors dominate at 62.4% in 2025, favored for their ease of incorporation, precise dosing, and compatibility with standard beverage and liquid food manufacturing equipment globally.

Soap and detergents lead fragrance applications at 32.5% in 2025, driven by the high fragrance loading requirements of personal wash and laundry products in global FMCG supply chains.

North America commands a 35.2% flavor market share in 2025, driven by the world's largest concentration of CPG food and beverage manufacturers and high per-capita packaged food consumption.

North America also leads fragrances at 37.2% in 2025, supported by a large and sophisticated personal care market, strong fine fragrance retail, and significant home care fragrance demand.

Leading companies include ADM, Bell Flavors & Fragrances, Inc., Givaudan, International Flavors & Fragrances Inc., Kerry Group plc, Sensient Technologies Corporation, Symrise, and others.

Natural flavors are the fastest-growing flavor segment at ~3.8% CAGR through 2034, driven by clean-label consumer demands, while fine fragrances grow at ~3.6% CAGR from luxury market premiumization.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade