Flexible Packaging Market Size, Share, Trends and Forecast by Product Type, Raw Material, Printing Technology, Application, and Region, 2026-2034

Global Flexible Packaging Market Size, Share, Trends & Forecast (2026-2034)

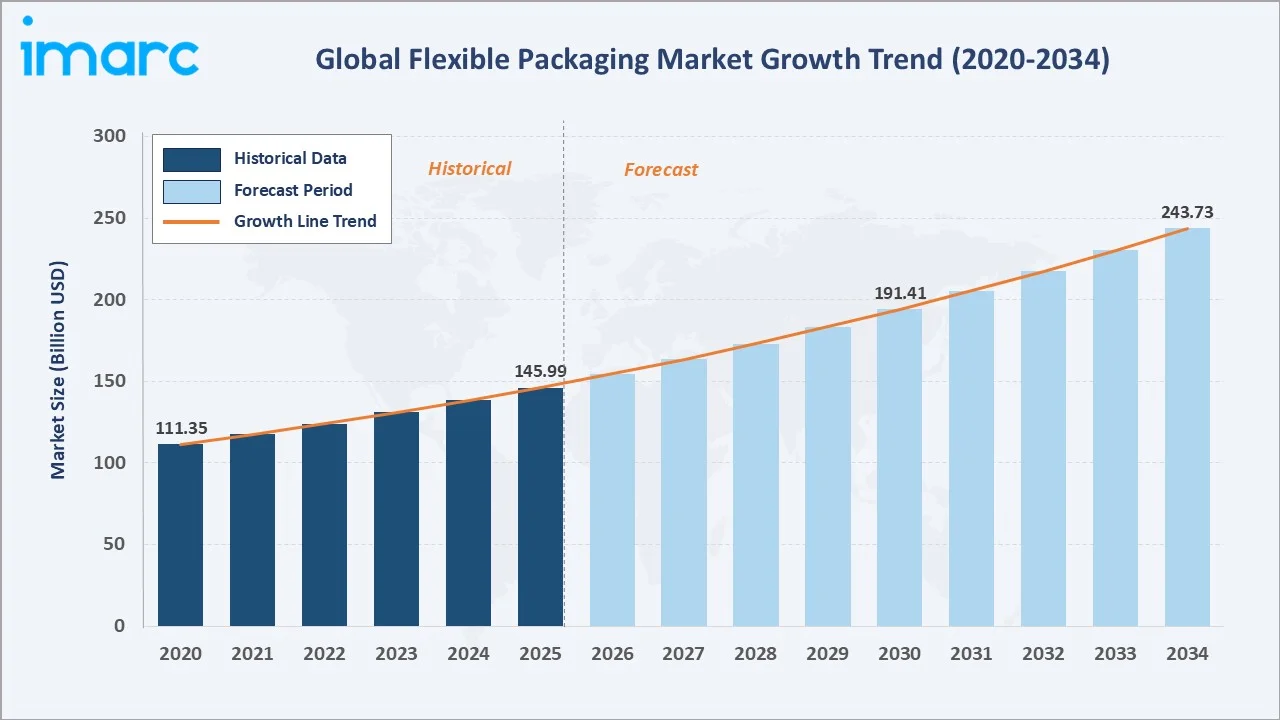

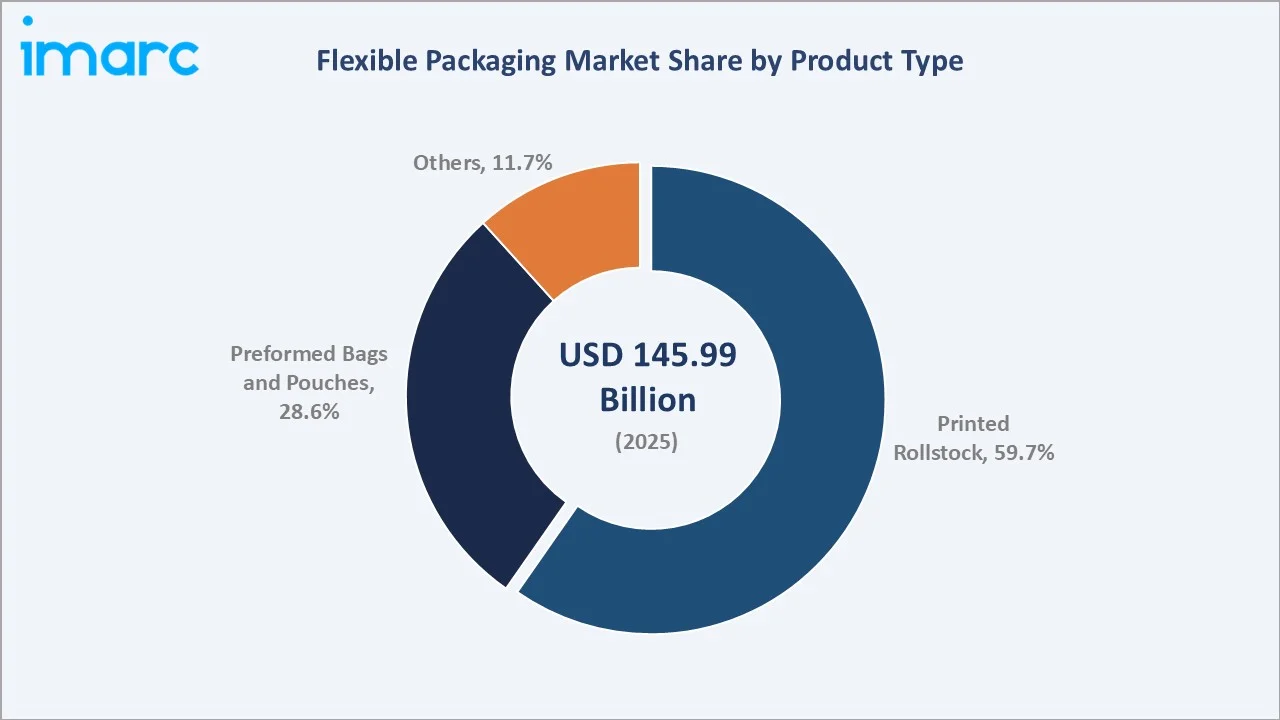

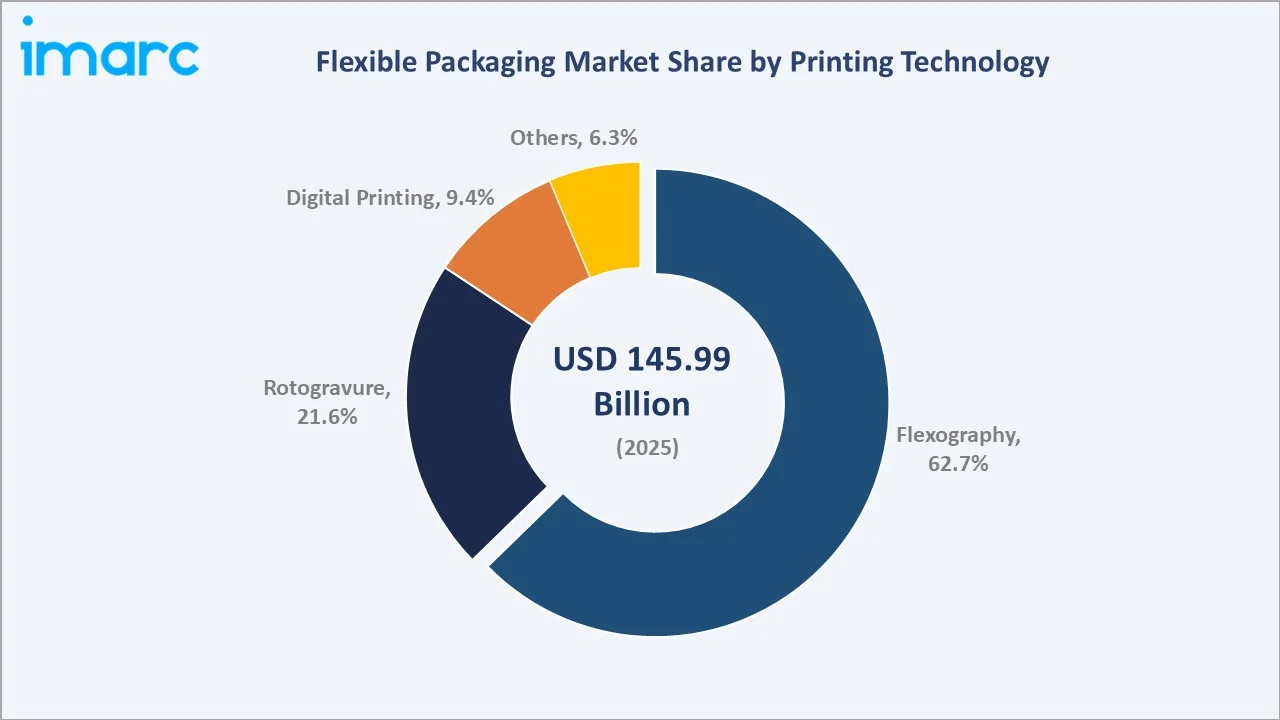

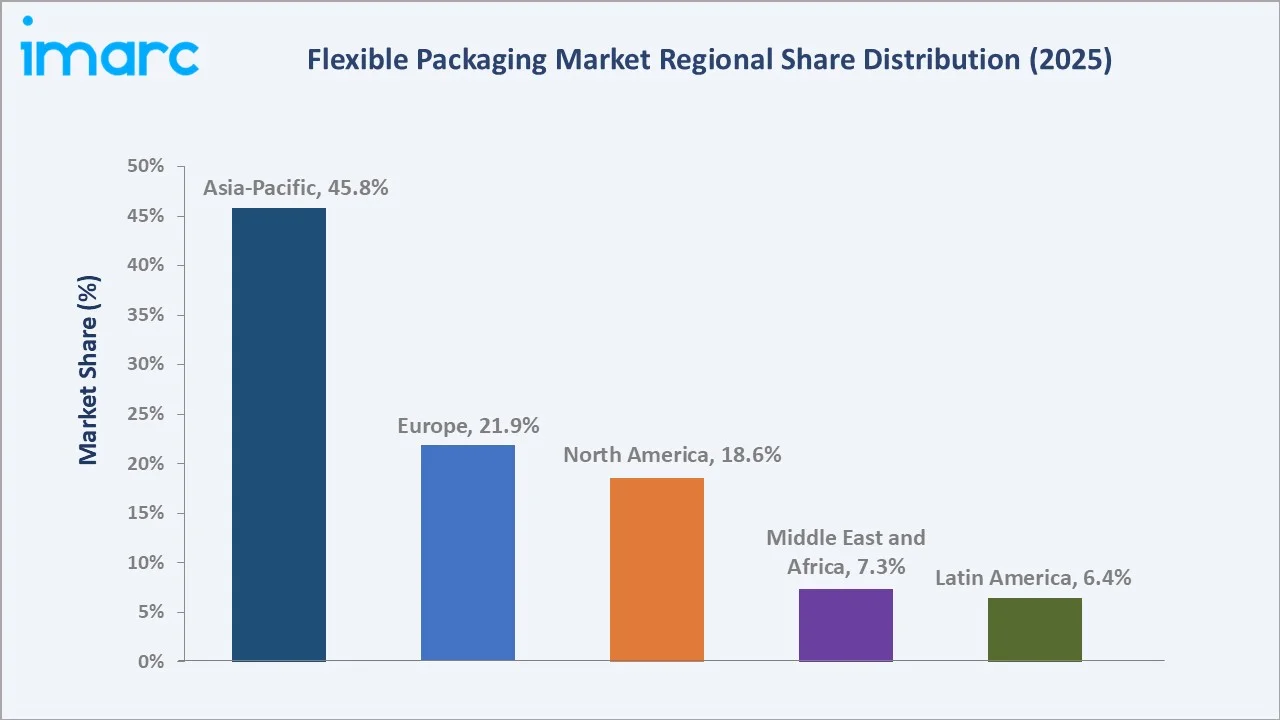

The global flexible packaging market was valued at USD 145.99 Billion in 2025 and is projected to reach USD 243.73 Billion by 2034, expanding at a CAGR of 5.57% during 2026-2034. Growth is driven by rising e-commerce demand, with over 90% of B2B companies now shifted to virtual sales since 2020 , food safety and shelf-life extension requirements, sustainability mandates for recyclable and lightweight packaging, and rapid middle-class consumption growth in Asia-Pacific and emerging markets. Printed rollstock dominates product type at 59.7%, flexography leads printing technology at 62.7%, and Asia-Pacific commands 45.8% of global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 145.99 Billion |

|

Forecast Market Size (2034) |

USD 243.73 Billion |

|

CAGR (2026-2034) |

5.57% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant and Fastest Growing Region |

Asia-Pacific (45.8%, 2025 and CAGR ~6.5%, 2026-2034) |

The global flexible packaging market expanded from USD 111.35 Billion in 2020 to USD 145.99 Billion in 2025, driven by COVID-19-induced packaged food demand acceleration and the structural shift toward convenience packaging in Asia-Pacific’s growing urban middle class. Anchored at USD 191.41 Billion in 2030, the forecast to USD 243.73 Billion by 2034, underpinned by Amcor’s 2023 acquisition of Phoenix Flexibles in India expanding high-growth market access.

To get more information on this market, Request Sample

The CAGR across key segments with digital printing at ~9.2% CAGR grows fastest, reflecting brand owners’ rapid adoption of short-run, variable-data digital printing for SKU proliferation, personalized packaging campaigns, and reduced minimum order quantities. Latin America at ~6.8% CAGR, driven by Brazil’s expanding packaged food sector and Mexico’s growing FMCG manufacturing base serving both domestic and export markets, supporting continued growth in the Flexible Packaging Market in Latin America.

Executive Summary

The global flexible packaging market expanded from USD 111.35 Billion in 2020 to USD 145.99 Billion in 2025, driven by COVID-19’s acceleration of home meal consumption and e-commerce, post-pandemic FMCG demand normalization, and a structural shift from rigid to flexible packaging formats driven by material reduction, logistics efficiency, and consumer convenience. Flexible packaging, encompassing printed rollstock films, stand-up pouches, retort pouches, sachets, bags, and functional barrier laminates – serves as the primary packaging format for the global food and beverage, pharmaceutical, cosmetics, and consumer goods industries, replacing rigid glass, metal, and paper packaging through material reduction, superior barrier performance, and the design flexibility that brand owners require for shelf differentiation and consumer convenience.

Printed rollstock leads at 59.7% as the foundational flexible packaging product form, printed film reels that are subsequently formed, filled, and sealed by brand owner form-fill-seal (FFS) equipment into finished packages at the point of fill. Flexography dominates printing at 62.7% through its versatility across BOPP, PET, PE, and paper substrates with 8–10 color process capability. Asia-Pacific’s 45.8% dominance reflects China’s massive food processing sector, India’s rapidly expanding packaged food market, and Southeast Asia’s FMCG growth.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Printed Rollstock – 59.7% share (2025) |

|

Dominant Printing Technology |

Flexography – 62.7% share (2025) |

|

Dominant and Fastest Growing Region |

Asia-Pacific (45.8%, 2025 and CAGR ~6.5%, 2026-2034) |

Key Analytical Observations Supporting The Above Data:

- Printed rollstock at 59.7% reflecting its role as flexible packaging’s primary high-volume format: BOPP printed rollstock for snack food packaging (chips, nuts, crackers) represents the world’s largest single flexible packaging product volume.

- Flexography at 62.7% sustained by volume economics and substrate versatility: Modern flexographic printing presses are achieving different color process printing. Water-based and UV-curable flexographic inks meeting food contact safety standards have addressed the historical solvent emission concern while maintaining the printing performance expected for retail shelf flexible packaging.

- Asia-Pacific at 45.8% as the structural center of global flexible packaging: China’s flexible packaging industry represents the world’s largest national flexible packaging market and production base simultaneously. China’s food delivery and e-commerce platforms represent an opportunity in flexible packaging consumption unique to China’s digital commerce ecosystem.

Global Flexible Packaging Market Overview

Flexible packaging encompasses a broad range of packaging solutions where the primary material can be bent, twisted, or shaped without breakage, distinguishing it from rigid and semi-rigid packaging. Commercial flexible packaging encompasses printed rollstock films (BOPP, PET, PE, PA, aluminium foil, paper, and multilayer laminates thereof) supplied to brand owners for use on form-fill-seal equipment; preformed stand-up pouches, flat bottom bags, retort pouches, and sachets; and other flexible formats including stretch and shrink wrap, flexible pouches with closures (zippers, spouts), and multi-layer high-barrier flexible structures for pharmaceutical and specialty applications.

Applications span food and beverages (snacks, frozen food, fresh produce, meat and dairy, beverages, confectionery), pharmaceuticals (blister foil, sachets, medicinal pouches, ophthalmic packaging), cosmetics (shampoo sachets, beauty product pouches, flexible tubes), and industrial/commercial uses (agricultural film, industrial flexible bags, e-commerce mailers). Macroeconomic growth drivers include the global packaged food market growth, food waste reduction driving extended shelf life, flexible packaging innovation, sustainability mandates driving material transition, and the Asia-Pacific’s FMCG market expansion, creating the world’s largest incremental flexible packaging demand.

Market Dynamics

To evaluate market opportunities, Request Sample

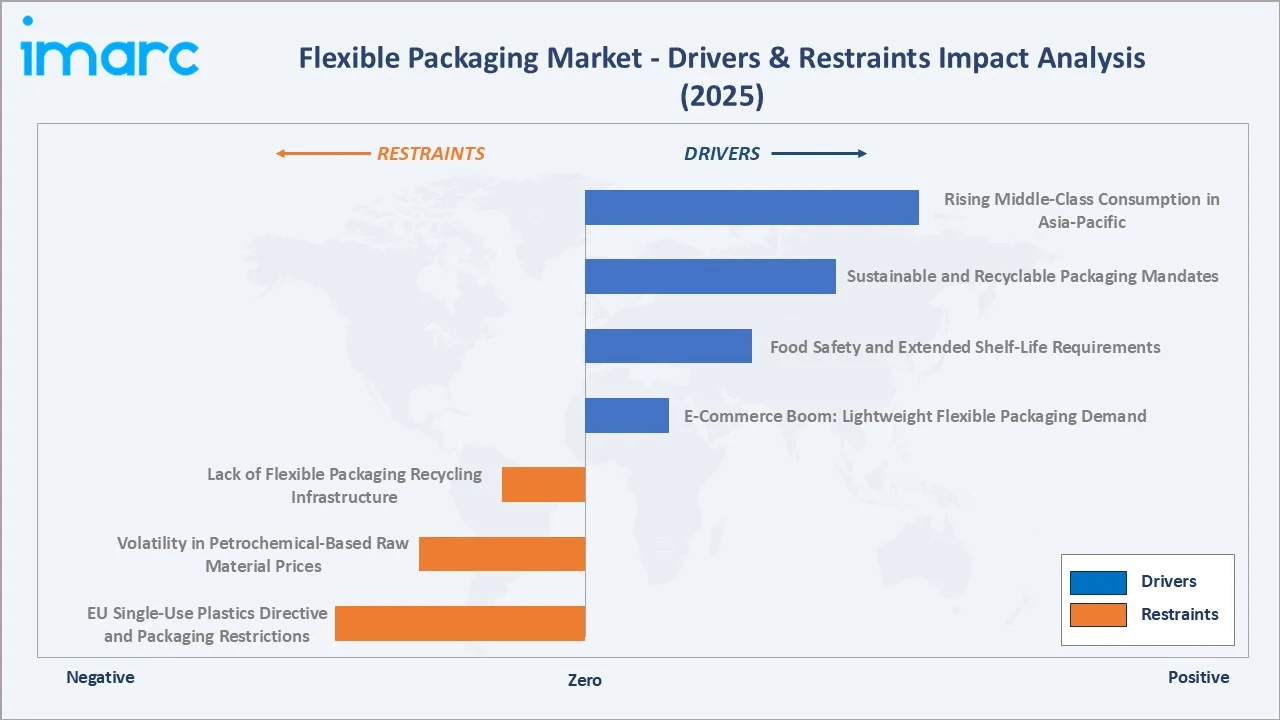

Market Drivers

- E-Commerce Boom Driving Demand for Lightweight Flexible Packaging: Global e-commerce retail sales growth generates extraordinary flexible packaging demand: every e-commerce parcel shipped requires poly mailers, bubble wrap, flexible protective film, or flexible void fill packaging.

- Food Safety and Extended Shelf-Life Requirements: The USD 940 billion annual global food waste cost creates systematic economic pressure for flexible packaging technologies that extend food shelf life and reduce waste.

- Sustainable and Recyclable Packaging Mandates: The Packaging and Packaging Waste Regulation 2025/40 (PPWR) came into force in February 2025 and will generally apply from August 2026, which is mandating recyclable flexible packaging, which is the single most impactful regulatory driver of flexible packaging innovation investment globally.

- Rising Middle-Class Consumption in Asia-Pacific and Emerging Markets: Asia-Pacific’s middle class is projected to reach 3.5 billion people by 2030, creating the world’s largest consumption market for packaged foods, personal care, and consumer goods products that require flexible packaging.

Market Restraints

- EU Single-Use Plastics Directive and Plastic Packaging Restrictions: EU Single-Use Plastics Directive 2019/904 , prohibiting certain single-use plastic products and requiring Extended Producer Responsibility (EPR) for all flexible plastic packaging created a compliance cost burden for European flexible packaging manufacturers.

- Volatility in Petrochemical-Based Raw Material Prices: Polyethylene, polypropylene, PET, and polyamide resins are derived from petrochemical feedstocks whose prices track crude oil and natural gas price cycles.

Market Opportunities

- Mono-Material Recyclable Flexible Packaging: The transition from multilayer non-recyclable to monomaterial recyclable flexible packaging represents the largest materials substitution opportunity in the packaging industry since the introduction of biaxially oriented films in the 1960s.

- Pharmaceutical Flexible Packaging Growth: Global pharmaceutical market growth, combined with aging population demographics aged 65 and older, is projected to reach 2.2 billion by 2070 , increasing chronic disease medication consumption, driving pharmaceutical flexible packaging demand growth.

Market Challenges

- Consumer Confusion and Greenwashing Scrutiny: Flexible packaging sustainability claims such as “recyclable,” “compostable,” and “bio-based” face increasing regulatory and consumer scrutiny.

- Lack of Flexible Packaging Recycling Infrastructure: Despite brand owner commitments to 100% recyclable flexible packaging by 2025–2030, flexible packaging recyclability is fundamentally constrained by the absence of consumer collection and sorting infrastructure for flexible plastic packaging in most markets.

Emerging Market Trends

1. Mono-Material Recyclable Flexible Packaging Achieving Mainstream Adoption

The transition from non-recyclable multilayer flexible packaging to recyclable mono-material (monomaterial) structures is the defining packaging industry transition of 2024–2030 by meeting internal sustainability commitments and pre-empting EU PPWR compliance requirements.

2. Active and Intelligent Packaging Functionality Integration

Flexible packaging is progressively evolving beyond passive containment toward active functions (modifying the package atmosphere to extend shelf life) and intelligent functions (communicating product status to consumers and supply chain partners). Active flexible packaging: oxygen scavenging sachets integrated into flexible pouches extending coffee, snack, and meat shelf life by 3‒6 months; desiccant pouches integrated into pharmaceutical flexible packaging; antimicrobial flexible films extending fresh produce shelf life.

3. Bio-Based and Compostable Flexible Packaging Scaling

Bio-based flexible packaging, flexible films and laminates derived from renewable bio-based raw materials, including PLA (polylactic acid from corn starch), bio-PE (sugarcane ethanol-derived polyethylene), and cellulose films, are growing as premium food brands, specialty food retailers adopt bio-based flexible packaging for sustainability brand differentiation.

4. E-Commerce Optimized Flexible Packaging as the Fastest Growing Application

The e-commerce category, with over 90% of B2B companies now shifted to virtual sales since 2020, encompasses poly mailers, padded flexible mailers, co-extruded poly bubble mailers, and flexible protective void fill materials, with the fastest growth in the flexible packaging market.

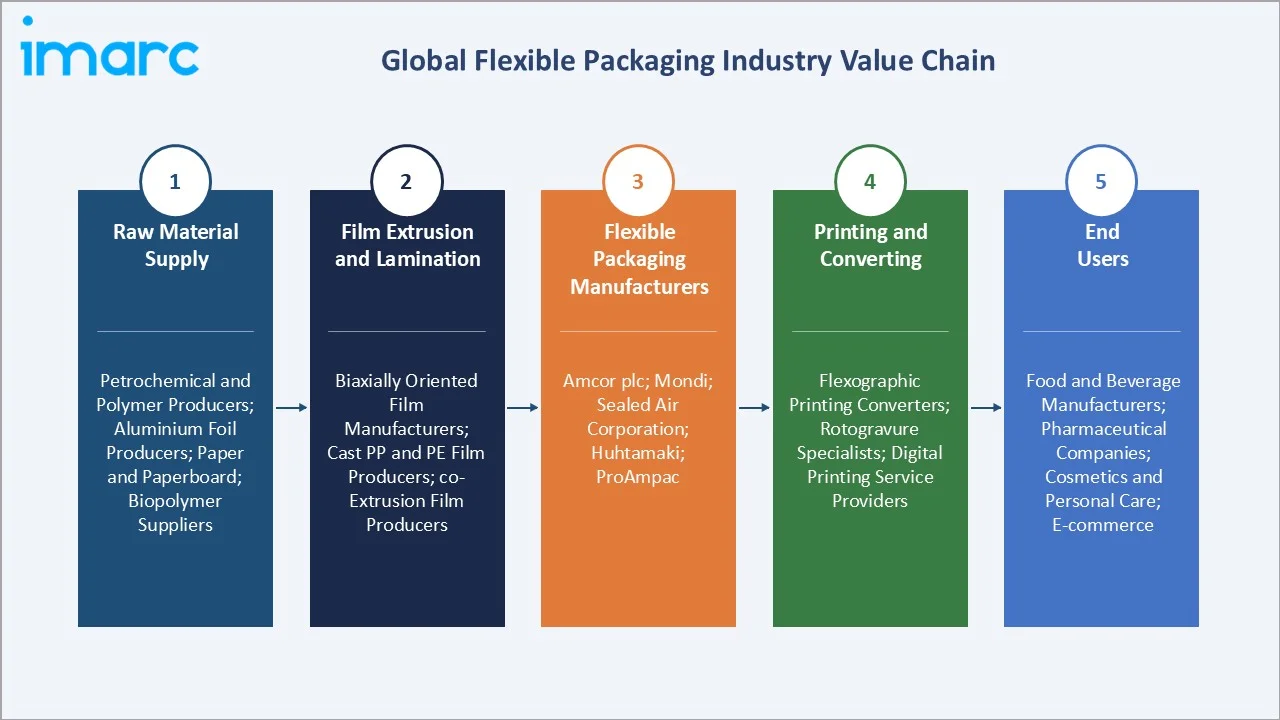

Industry Value Chain Analysis

The global flexible packaging value chain integrates petrochemical and bio-based raw material production, film extrusion and lamination, printing and converting, distribution, and end-user packaging operations.

|

Stage |

Key Participants |

|

Raw Material Supply |

Petrochemical and polymer producers; aluminium foil producers; paper and paperboard; biopolymer suppliers; sustainable flexible packaging |

|

Film Extrusion & Lamination |

Biaxially oriented film manufacturers; cast polypropylene (CPP) and cast polyethylene (CPE) film producers; co-extrusion film producers: aluminium foil lamination; coating and adhesive lamination |

|

Flexible Packaging Manufacturers (OEMs) |

Amcor plc, Mondi, Sealed Air Corporation |

|

Printing & Converting |

Commercial flexographic printing converters; rotogravure printing specialists; digital printing service providers; pouch forming and sealing equipment suppliers |

|

End Users |

Food and beverage manufacturers; pharmaceutical companies; cosmetics and personal care; retailers and e-commerce |

Flexible packaging converters and manufacturers capture 35‐45% of total supply chain value through film lamination, printing, and converting operations. Film extrusion and resin compounding add 20‐25% of value. The highest-margin value chain tier is intelligent and functional packaging integration, where gross margins of 40‐55% versus 15‐25% for commodity flexible film production create significant incentive for capability investment. Distribution and logistics represent 8‐12% of end-user flexible packaging cost.

Technology Landscape in the Global Flexible Packaging Industry

Barrier Film Technology for Extended Shelf Life

Modern barrier flexible packaging films achieve oxygen transmission rates (OTR) below 1.0 cm³/m²/day through EVOH (ethylene vinyl alcohol) co-extrusion layers, aluminium oxide (AlOx) vacuum deposition coatings, silicon oxide (SiOx) plasma deposition, and metallized polyester deposition.

Sustainable Ink and Adhesive Systems

Water-based flexographic inks meeting EN 71-3 toy safety are replacing solvent-based systems in European and North American flexible packaging printing under VOC emission reduction regulations. Primary packaging ink migration remains a critical food safety concern requiring EN 645 and EN 647 ink migration testing compliance documentation for every food-contact flexible packaging product.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Printed Rollstock | 59.7% | 2025 |

| Raw Material | Plastic | 61.8% | 2025 |

| Printing Technology | Flexography | 62.7% | 2025 |

| Application | Food and Beverages | 72.1% | 2025 |

| Region | Asia Pacific | 45.8% | 2025 |

By Product Type

Printed rollstock leads at 59.7%, encompassing BOPP rollstock for snack food packaging, PET rollstock for labels and lidding films, PE rollstock for frozen food and produce packaging, and laminated rollstock for coffee, pet food, and specialty food packaging.

To access detailed market analysis, Request Sample

Preformed bags and pouches at 28.6% are growing fastest at ~6.1% CAGR through stand-up pouch category expansion (pet food, baby food, liquid food, personal care), retort pouch adoption (ambient ready meals, wet cat food, infant formula), and e-commerce flexible packaging (poly mailers, padded flexible mailers). Others at 11.7% encompasses stretch and shrink wrap, flexible tubes, sachets, and specialty formats.

By Printing Technology

Flexography leads at 62.7% as the dominant commercial flexible packaging printing technology through its combination of versatility, speed, and multi-substrate capability. Rotogravure at 21.6% maintains a position in the highest-volume, highest-graphic-quality flexible packaging applications (confectionery wrappers, premium snack bags, coffee pouches) where rotogravure’s DPI imaging depth provides image quality that flexography cannot match for gold and silver metallic designs, fine tonal gradients, and process-sensitive product imagery.

Digital printing at 9.4% is growing at ~9.2% CAGR as HP Indigo’s installed flexible packaging presses enable commercial short-run flexible packaging, seasonal and promotional variant packaging, and mass-personalization campaigns. Others at 6.3% encompasses offset litho lamination, screen printing for specialty flexible packaging, and letterpress for flexible label printing.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

45.8% |

China’s massive food and beverage manufacturing sector requires a high amount of flexible packaging annually; India’s packaged foods consumption growth as urbanization drives snack food, processed food, and ready-to-eat category expansion |

|

Europe |

21.9% |

EU’s highly developed convenience food and premium snacking market; European pharmaceutical sector’s world-leading regulatory requirements driving premium barrier flexible packaging for blister films, sachets, and medicinal pouches |

|

North America |

18.6% |

US snacking and convenience food market driving high-volume flexible packaging consumption for chip bags, stand-up pouches, resealable snack packaging |

|

Middle East & Africa |

7.3% |

GCC countries’ food manufacturing expansion (Saudi Arabia Vision 2030 food industry localization, UAE’s FMCG export hub status, Egypt’s FMCG demand); Africa’s flexible packaging sachet market for water sachets, single-serve food sachets, and pharmaceutical sachets serving low-income consumer segments |

|

Latin America |

6.4% |

Brazil’s food manufacturing sector driving flexible packaging consumption for protein packaging, snack packaging, and coffee vacuum packaging; Mexico’s FMCG market serving North American CPG supply chains with flexible packaging manufacturing |

Asia-Pacific’s 45.8% dominance is structural and self-reinforcing: China’s high annual flexible packaging production base creates a scale manufacturing cost advantage that Asian converters use to supply not just domestic demand but also export markets in MEA and Latin America.

Europe’s 21.9% is the most sustainability-driven flexible packaging market globally. EU PPWR compliance is creating a 5‐10-year product replacement cycle across the entire European flexible packaging installed base that will require high capital investment from European converters for monomaterial recyclable structure development, certification, and line conversion. This compliance-driven capex cycle is simultaneously a market restraint (cost pressure) and growth driver (volume replacement) for European flexible packaging.

Competitive Landscape

The global flexible packaging market is moderately concentrated at the top tier, with Amcor and Mondi collectively representing approximately 20‐25% of global flexible packaging market revenue by value.

|

Company Name |

Brand / Product Line |

Market Position |

Core Strength |

|

Amcor plc |

Vento, Formpack Ultra, CanSeal Pro, Aluminium Capsule Materials |

Market Leader |

Amcor is the world’s largest flexible packaging company by revenue, with its flexible and rigid packaging segment |

|

Mondi |

FunctionalBarrier papers, re/cycle FlexiBags, Mono-material barrier packaging |

Market Leader |

Mondi occupies a unique flexible packaging market position as both the world’s leading sustainable paper-based flexible packaging manufacturer and a premium barrier flexible film producer |

|

Sealed Air |

Cryovac, Bubble Wrap, Autobag, Liquibox, |

Strong Challenger |

Sealed Air with Cryovac, the world’s most recognized flexible food packaging brand |

|

Huhtamaki |

blueloop Paper, blueloop PP Retort, blueloop PE |

Strong Challenger |

Huhtamaki, with its Flexible Packaging plants across South and Southeast Asia, the Middle East, and Africa |

|

ProAmpac |

ProActive Sustainability |

Strong Challenger |

ProAmpac is North America’s largest independent flexible packaging converter with high manufacturing plants |

Key Company Profiles

Amcor plc

Amcor is the world’s largest flexible packaging company. Amcor’s Flexible Packaging segment operates flexible packaging plants across Europe, North America, Latin America, and Asia-Pacific, manufacturing a comprehensive portfolio.

- Product Portfolio: Vento, Formpack Ultra, CanSeal Pro, Aluminium Capsule Materials, and others.

- Recent Developments: In March 2026, Amcor and DCM introduced recycle-ready mono-PE fertilizer packaging with 35% recycled content, supporting EU circular economy goals .

- Strategic Focus: Sustainable flexible packaging technology leadership through AmLite portfolio scale-up targeting recyclable/reusable flexible packaging revenue by 2027.

Mondi

Mondi occupies the most strategically differentiated position in flexible packaging through its unique combination of vertical integration and sustainability leadership.

- Product Portfolio: FunctionalBarrier papers, re/cycle FlexiBags, Mono-material barrier packaging.

- Recent Developments: In November 2025, Mondi reinforced its role as a reliable partner for the food industry by expanding its food packaging portfolio. The new portfolio incorporates solid board solutions and digital printing capabilities, following the acquisition of Schumacher Packaging, boosting Mondi’s capacity to serve customers throughout Europe. As a result, Mondi now provides one of the most extensive selections of food packaging available, including corrugated and solid board options, as well as a complete range of flexible packaging.

- Strategic Focus: BarrierPack Recyclable scaling as EU PPWR compliance driver accelerates brand owner migration from multilayer to recyclable flexible packaging; paper-based flexible packaging expansion as plastic-alternative premium positioning for European and North American sustainability-motivated brand owners.

Sealed Air

Sealed Air is the world’s most recognizable flexible packaging brand through its Cryovac food packaging and Bubble Wrap protective packaging divisions.

- Product Portfolio: Cryovac, Bubble Wrap, Autobag, Liquibox .

- Recent Developments: In September 2025, Sealed Air launched of the AUTOBAG 850HB Hybrid Bagging Machine.

- Strategic Focus: Cryovac brand premiumization through Simple Steps recyclable VSP and Darfresh recyclable VSP premium retail-ready fresh protein packaging as food retailer sustainability commitment enablers.

Market Concentration Analysis

The global flexible packaging market is notably fragmented. The Amcor and Mondi account for only approximately 15‐20% of global market revenue, significantly lower concentration than most industrial manufacturing markets, reflecting flexible packaging’s proximity to consumer demand (requiring regional manufacturing for responsiveness), the breadth of end-use applications (each application segment having specialist converters), and the technology diversity that fragments market share across hundreds of converters.

Investment & Growth Opportunities

Fastest Growing Segments

Preformed bags and pouches (~6.1% CAGR), digital printing technology (~9.2% CAGR), Asia-Pacific region (~6.5% CAGR), pharmaceutical flexible packaging (~7.5% CAGR), and sustainable/recyclable flexible packaging formats (~15‐20% CAGR from current small base) represent the global flexible packaging market’s highest-growth investment vectors. E-commerce flexible packaging at 15‐20% CAGR represents the single fastest-growing flexible packaging application globally.

Emerging Technology Opportunities

Chemical recycling of flexible plastic packaging waste enabling recycled flexible packaging content from previously non-recyclable multilayer structures; NFC and RFID integration in flexible packaging for supply chain traceability and consumer engagement; bio-based flexible packaging film scale-up; and paper-based flexible packaging barrier development for plastic-alternative premium positioning.

Investment Themes

Sustainable flexible packaging transition, digital printing capability buildout, and emerging market flexible packaging capacity expansion represent the three dominant investment themes for flexible packaging manufacturers, converters, and private equity-backed consolidators.

- Sustainability investment: Monomaterial PE and PP film development; bio-based resin qualification; post-consumer recycled (PCR) content integration in flexible packaging films; flexible packaging take-back program infrastructure funding.

- Geographic expansion investment: India flexible packaging manufacturing capacity; Southeast Asia FMCG-driven flexible packaging demand; Africa flexible packaging sachet and pouch manufacturing for base-of-pyramid consumer markets; Middle East GCC pharmaceutical flexible packaging for Saudi Vision 2030 healthcare localization.

Future Market Outlook (2026-2034)

The global flexible packaging market is entering a decade of dual transformation: volumetric growth from Asia-Pacific’s consumption expansion and e-commerce’s systematic increase in flexible packaging intensity, combined with a structural material transition from non-recyclable multilayer to recyclable monomaterial flexible packaging formats that will reshape every product specification, every capital investment decision, and every competitive advantage in the industry through 2034.

From USD 145.99 Billion in 2025, the market will reach USD 243.73 Billion by 2034, at a 5.57% CAGR that outpaces global GDP growth and reflects flexible packaging’s structural capture of shelf space and supply chain function from heavier, less efficient rigid packaging alternatives. Three structural forces underpin this growth path with high confidence: Asia-Pacific’s packaged food transition is a multi-decade consumption transformation; e-commerce’s inexorable flexible packaging intensity growth ensures that global e-commerce’s growth translates directly to flexible packaging market expansion; and pharmaceutical flexible packaging’s double-digit growth from aging population demographics and biosimilar injectable expansion creates the highest-value flexible packaging sub-segment growth.

Research Methodology

Primary Research

Primary research included structured interviews with 130+ industry stakeholders in 2025, comprising flexible packaging manufacturer executives, brand owner packaging managers, printing press OEM specialists, film extrusion technology experts, packaging sustainability consultants, and regulatory affairs specialists at EFSA, FPA, and CEFLEX.

Secondary Research

Secondary research encompassed IMARC packaging market database, European Flexible Packaging Association (EFPA) market statistics, Flexible Packaging Association (FPA) US market intelligence, CEFLEX Circular Economy for Flexible Packaging programme data, RecyClass recyclability assessment database, Ellen MacArthur Foundation New Plastics Economy Global Commitment signatory progress reports, company annual reports, IHS Markit polyolefin demand data, and Euromonitor International packaged food market statistics. Over 160 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using a bottom-up product type × printing technology × application × region disaggregated model validated against top-down global packaged food market share models. Key inputs include global packaged food market CAGR, e-commerce retail sales growth trajectory, pharmaceutical market growth forecasts, EU PPWR compliance investment timelines, Asia-Pacific middle-class consumption growth projections, and digital printing press capacity expansion plans from HP Indigo, Durst, and Xeikon.

Flexible Packaging Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Printed Rollstock, Preformed Bags and Pouches, Others |

| Raw Materials Covered | Plastic, Paper, Aluminium Foil, Cellulose |

| Printing Technologies Covered | Flexography, Rotogravure, Digital, Others |

| Applications Covered | Food and Beverages, Pharmaceuticals, Cosmetics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Amcor plc, Mondi, Sealed Air, Huhtamaki, ProAmpac, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the flexible packaging market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global flexible packaging market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the flexible packaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Flexible Packaging Market Report

The global flexible packaging market was valued at USD 145.99 Billion in 2025 and is projected to reach USD 243.73 Billion by 2034.

The global flexible packaging market is forecast to grow at a CAGR of 5.57% during 2026-2034, driven by e-commerce demand, food shelf-life extension requirements, sustainable packaging mandates, and Asia-Pacific consumption growth.

Printed rollstock leads with 59.7% revenue share (2025), driven by high-volume BOPP snack food packaging, PET lidding films, and PE frozen food packaging rollstock consumed by brand owners’ form-fill-seal operations.

Flexography leads with 62.7% revenue share (2025), sustained by its versatility across BOPP, PE, PET, and paper substrates and competitive economics at runs above 5,000 linear meters across different color process printing.

Asia-Pacific leads with 45.8% revenue share (2025), driven by China’s flexible packaging production base, India’s rapidly expanding packaged food market, and Southeast Asia’s FMCG sector growth.

Key companies include Amcor plc, Mondi, Sealed Air, Huhtamaki, and ProAmpac.

Key drivers include the global e-commerce boom, food safety and shelf-life extension requirements, EU and global sustainable packaging mandates, rising Asia-Pacific middle-class consumption, pharmaceutical flexible packaging growth, and digital printing enabling mass-customization.

Key trends include monomaterial recyclable flexible packaging, digital flexible packaging printing, active and intelligent packaging integration, bio-based and compostable film scaling, and e-commerce optimized flexible packaging growth.

Digital printing grows at ~9.2% CAGR as HP Indigo digital presses enable commercial short-run flexible packaging, seasonal and promotional packaging variants, and mass-personalization campaigns that flexographic printing cannot serve economically.

Key challenges include the EU Single-Use Plastics Directive and plastic packaging restrictions, petrochemical raw material price volatility, complex multilayer structures hindering recyclability, flexible packaging recycling infrastructure gaps, and EU PPWR compliance costs for European converters.

Top opportunities include monomaterial recyclable flexible packaging technology investment, digital flexible packaging printing press acquisition, Asia-Pacific manufacturing capacity expansion, pharmaceutical flexible packaging growth, e-commerce protective flexible packaging, and chemical recycling infrastructure co-investment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)