Fluid Loss Additives Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Fluid Loss Additives Market Size and Share:

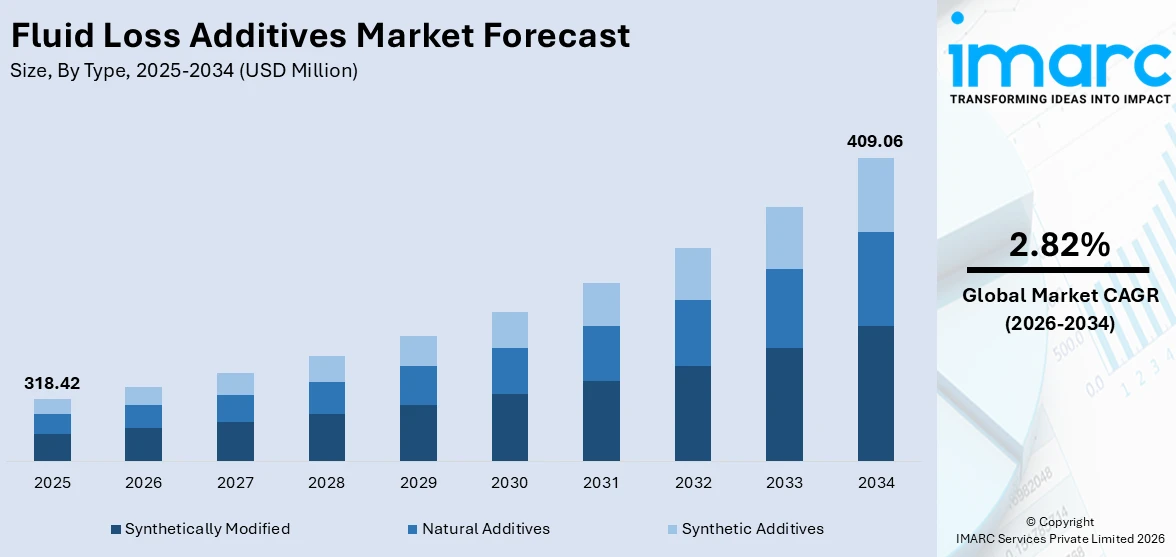

The global fluid loss additives market size was valued at USD 318.42 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 409.06 Million by 2034, exhibiting a CAGR of 2.82% from 2026-2034. North America currently dominates the market, holding a market share of 34.2% in 2025. The region benefits from extensive oil and gas exploration activities, well-established drilling infrastructure, increasing demand for advanced drilling chemicals, and a strong regulatory framework promoting efficient wellbore management practices, all contributing to the fluid loss additives market share.

The global fluid loss additives market is primarily driven by the expanding oil and gas exploration and production activities across both onshore and offshore environments. The growing need for efficient wellbore stability management during drilling operations is propelling the demand for advanced fluid loss control agents. Additionally, the rising complexity of drilling projects, including deepwater and ultra-deepwater wells, necessitates the use of high-performance additives to prevent formation damage and maintain optimal fluid properties. The increasing adoption of water-based drilling fluids, driven by environmental regulations favoring eco-friendly formulations, is further stimulating the fluid loss additives market growth. Moreover, the expansion of geothermal energy projects and underground storage applications is creating new avenues for fluid loss additive deployment.

The United States has emerged as a major region in the fluid loss additives market owing to many factors. The country maintains a dominant position in global oil and gas production, with extensive shale drilling operations across multiple basins driving consistent demand for advanced drilling fluid additives. As per sources, in 2024, SLB introduced Neuro™ autonomous geosteering, enabling AI-driven well placement for more efficient drilling while reducing operational emissions, highlighting technological innovation in U.S. oilfield operations. Furthermore, the growing emphasis on enhanced oil recovery techniques and horizontal drilling methodologies is boosting the consumption of high-performance fluid loss agents. The regulatory landscape in the United States favors the development and deployment of environmentally compliant drilling chemicals, encouraging innovation in bio-based and low-toxicity additive formulations. The robust oilfield services infrastructure and the presence of leading chemical manufacturers further strengthen the domestic market landscape.

To get more information on this market Request Sample

Fluid Loss Additives Market Trends:

Expanding Deepwater Exploration Activities

The expansion of deepwater and ultra-deepwater exploration activities is significantly driving the demand for fluid loss additives across the global oil and gas industry. As conventional onshore reserves experience gradual depletion, energy companies are increasingly turning to challenging offshore environments to secure new hydrocarbon resources. In May 2024, Halliburton introduced its SentinelCem Pro lost‑circulation cement system, specifically engineered to control severe fluid loss during offshore drilling operations, reflecting real-world innovation in fluid loss solutions for deepwater wells. These deepwater drilling operations encounter extreme temperatures, high pressures, and complex geological formations that require advanced fluid loss control solutions to maintain wellbore stability and prevent formation damage. The demanding conditions of subsea drilling necessitate additives that can perform reliably under severe downhole environments while maintaining the rheological properties of drilling fluids.

Growing Adoption of Eco-Friendly Formulations

The increasing regulatory pressure and environmental awareness are driving a notable shift toward eco-friendly fluid loss additive formulations across the drilling industry. Governments and regulatory authorities worldwide are implementing stringent environmental standards that restrict the use of toxic and non-biodegradable chemicals in drilling operations, particularly in environmentally sensitive regions. In 2025, IMDEX launched its xFORM multifunctional drilling fluids range designed to reduce environmental impact and eliminate hazardous chemicals, highlighting industry moves toward safer, sustainable fluid systems. This regulatory evolution is compelling manufacturers to develop bio-based and biodegradable fluid loss additives derived from natural polymers, starches, and cellulosic materials that offer comparable performance to conventional synthetic alternatives. The fluid loss additives market outlook is further strengthened by the growing preference among operators for green chemistry solutions that minimize the ecological footprint of drilling activities.

Technological Advancements in Additive Chemistry

Significant technological advancements in additive chemistry are reshaping the fluid loss additives landscape, enabling the development of next-generation products with superior performance characteristics. Innovations in polymer science, nanotechnology, and material engineering are facilitating the creation of additives that offer enhanced temperature stability, improved filtration control, and better compatibility with diverse drilling fluid systems. According to reports, AES Drilling Fluids expanded its capabilities by acquiring HydroLite Operating LLC, enhancing its portfolio of advanced fluid systems and fluid loss additives used for well drill‑outs and cleanouts, reflecting strategic company‑level investment in high‑performance formulations. The fluid loss additives market forecast is positively influenced by the introduction of smart additives that can adapt to changing downhole conditions, providing responsive fluid loss control throughout the drilling process.

Fluid Loss Additives Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global fluid loss additives market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type and application.

Analysis by Type:

- Synthetically Modified

- Natural Additives

- Synthetic Additives

Synthetically modified holds 42.5% of the market share, these are chemically engineered variants of natural polymers that have been processed to enhance their performance characteristics under demanding drilling conditions. These additives combine the inherent benefits of natural base materials with synthetic modifications that improve thermal stability, salt tolerance, and filtration control efficiency. The preference for synthetically modified additives stems from their ability to deliver consistent performance across a wide range of wellbore temperatures and pressures while maintaining compatibility with various drilling fluid systems. Operators favor these products because they offer a balanced combination of cost-effectiveness and technical performance compared to fully synthetic alternatives. The versatility of synthetically modified additives allows their deployment in both water-based and oil-based drilling fluid formulations, making them suitable for diverse geological environments. The ongoing refinement of modification techniques continues to expand the operational window and application scope of these additives in modern drilling operations worldwide.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Drilling Fluids

- Cement Slurries

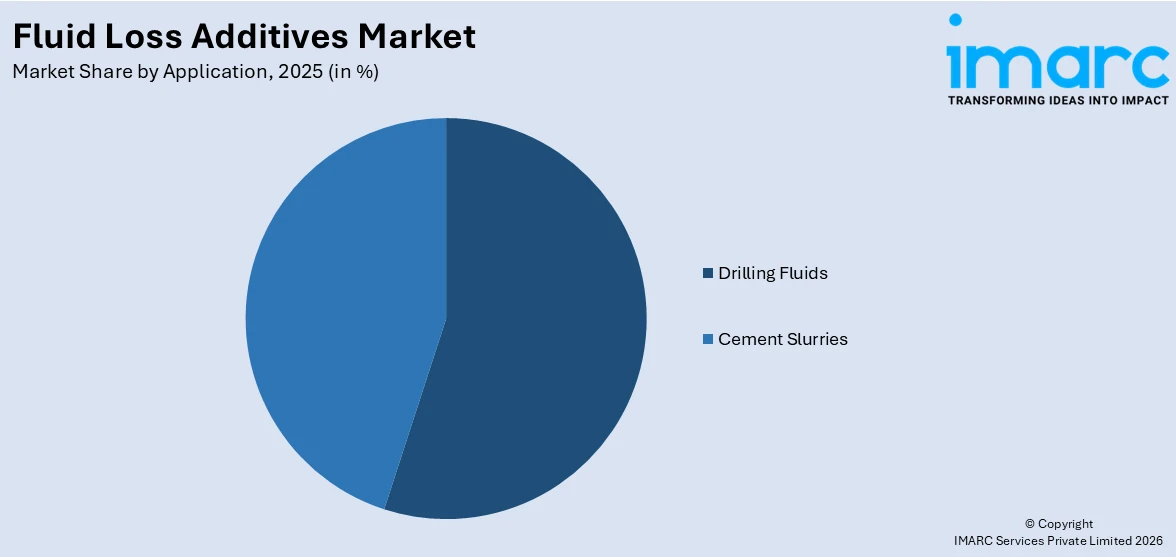

Drilling fluids leads the market with a share of 53.8%, as these chemicals play a critical role in maintaining the integrity and performance of the drilling fluid system during wellbore construction. Fluid loss additives are incorporated into drilling muds to control the filtration rate and prevent excessive fluid invasion into permeable formations, which can cause formation damage and compromise well productivity. The fluid loss additives market trends indicate sustained demand from drilling fluid applications as operators continue to prioritize wellbore stability and formation protection across increasingly complex drilling environments. The growing complexity of horizontal and directional drilling operations requires precisely formulated drilling fluids with optimized fluid loss characteristics to ensure smooth operations and minimize non-productive time. Additionally, the expansion of drilling activities in unconventional resource plays and challenging geological formations is reinforcing the central role of fluid loss additives within drilling fluid formulations globally.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 34.2% of the share, maintaining the leading position in the market. The region benefits from its extensive oil and gas production infrastructure, particularly the large-scale shale drilling operations that dominate the upstream sector. The active exploration and production campaigns across major formations require substantial volumes of drilling chemicals, including fluid loss additives, to ensure efficient wellbore management. The well-established oilfield services ecosystem in North America supports the rapid deployment and adoption of advanced additive technologies. Furthermore, the region is home to several leading drilling chemical manufacturers and research institutions that drive continuous innovation in fluid loss control solutions. The regulatory environment encourages the development of high-performance, environmentally compliant formulations that meet increasingly stringent operational and ecological standards. The combination of robust drilling activity levels, strong technological capabilities, and favorable market infrastructure positions North America as the dominant regional market for fluid loss additives globally.

Key Regional Takeaways:

United States Fluid Loss Additives Market Analysis

The United States represents the largest national market for fluid loss additives within North America, driven by its position as one of the leading global producers of oil and natural gas. The extensive shale drilling operations across prolific basins create consistent demand for high-quality fluid loss control agents that ensure wellbore stability and formation protection. The increasing adoption of horizontal and directional drilling techniques, which require precisely formulated drilling fluids, further strengthens the demand for advanced fluid loss additives in the country. The presence of major oilfield service companies and specialty chemical manufacturers fosters a competitive landscape that promotes continuous product innovation and performance improvement. The regulatory framework governing drilling operations encourages the use of environmentally responsible formulations, driving the development of bio-based and low-toxicity fluid loss additives. Additionally, the growing focus on enhanced oil recovery methods and the development of unconventional resources, including tight oil and shale gas formations, sustain long-term demand for specialized fluid loss control products. The well-developed supply chain infrastructure ensures efficient distribution and availability of drilling chemicals across operational regions.

Europe Fluid Loss Additives Market Analysis

Europe represents a significant market for fluid loss additives, supported by ongoing offshore drilling activities in the North Sea and emerging exploration prospects across the continent. The region maintains stringent environmental regulations that govern the use of chemicals in drilling operations, driving the adoption of eco-friendly and biodegradable fluid loss additive formulations. Key countries including the United Kingdom, Norway, and Germany contribute substantially to regional demand through their active upstream oil and gas sectors. The emphasis on sustainable drilling practices and the transition toward greener chemical solutions are shaping the product development strategies of additive manufacturers operating in the European market. Additionally, the growing interest in geothermal energy development across several European nations is creating supplementary demand for fluid loss control products tailored to geothermal drilling applications. The mature yet technologically advanced oilfield services sector in Europe facilitates the adoption of innovative additive solutions that meet both operational performance requirements and environmental compliance standards governing drilling fluid management.

Asia-Pacific Fluid Loss Additives Market Analysis

Due to the expansion of oil and gas exploration activities in major producing countries like China, India, Indonesia, and Australia, the Asia-Pacific market for fluid loss additives is expanding quickly. Investments in onshore and offshore drilling operations are being driven by the region's growing energy demand, which presents significant opportunities for suppliers of fluid loss additives. Exploration efforts in unexplored basins are accelerating due to government initiatives to increase domestic energy production and decrease reliance on imports. Market expansion is further supported by developing economies' increasing use of sophisticated drilling technologies and their modernisation of oilfield infrastructure. Furthermore, the region's shift to high-performance, ecologically friendly fluid loss additive products is being aided by growing environmental standards awareness and the progressive introduction of stronger chemical regulations.

Latin America Fluid Loss Additives Market Analysis

The significant oil and gas reserves in Brazil, Mexico, and other producing countries in Latin America are the main drivers of the region's expanding prospects for fluid loss additives. More money is being invested in pre-salt and deepwater exploration projects in the area, which call for sophisticated fluid loss control systems. Drilling activity is being stimulated, and international operators are being drawn in by government-led reforms aimed at opening energy sectors to foreign investment. High-performance drilling chemicals are in constant demand due to the growing offshore exploration efforts, especially in the Santos and Campos basins. The region's continuous modernisation of drilling techniques encourages the use of cutting-edge fluid-loss additive technologies.

Middle East and Africa Fluid Loss Additives Market Analysis

The Middle East and Africa region holds considerable potential for the fluid loss additives market, supported by extensive oil and gas reserves and active production operations across multiple countries. The ongoing drilling programs in major producing nations drive consistent demand for drilling fluid chemicals, including fluid loss control agents. The increasing focus on enhanced oil recovery methods and the development of mature field assets are creating additional demand for specialized additive formulations. Furthermore, the expansion of exploration activities into new frontier areas and the adoption of modern drilling technologies are contributing to the growing consumption of fluid loss additives across the region.

Competitive Landscape:

The competitive landscape of the global fluid loss additives market is characterized by the presence of several established multinational chemical companies and specialized oilfield chemical manufacturers. Key market participants are focusing on strategic initiatives including product innovation, capacity expansion, and collaborative partnerships to strengthen their competitive positions. Companies are investing in research and development to introduce advanced fluid loss additive formulations that offer superior performance under challenging drilling conditions while meeting evolving environmental standards. Mergers, acquisitions, and strategic alliances are common strategies employed by leading players to expand their geographic reach and diversify their product portfolios. The emphasis on developing bio-based and environmentally friendly additive solutions is emerging as a key differentiator among competitors.

The report provides a comprehensive analysis of the competitive landscape in the fluid loss additives market with detailed profiles of all major companies, including:

- BASF SE

- Clariant AG

- Global Drilling Fluids and Chemicals Limited

- Halliburton Company

- Kemira OYJ

- Newpark Resources Inc.

- Nouryon

- Schlumberger Limited

- Sepcor Inc.

- Solvay S.A

- Tytan Organics Pvt. Ltd

Latest News and Developments:

- In February 2025, Researchers Mohammad Khazaei and Mohsen Dehvedar introduced a novel cement slurry formulation using two fluid loss control additives (FLC1 and FLC2) plus a liquid dispersant. The blend optimizes rheology, compressive strength, and reduces transition time, minimizing gas migration in oil well cementing.

Fluid Loss Additives Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Synthetically Modified, Natural Additives, Synthetic Additives |

| Applications Covered | Drilling Fluids, Cement Slurries |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BASF SE, Clariant AG, Global Drilling Fluids and Chemicals Limited, Halliburton Company, Kemira OYJ, Newpark Resources Inc., Nouryon, Schlumberger Limited, Sepcor Inc., Solvay S.A, Tytan Organics Pvt. Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the fluid loss additives market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global fluid loss additives market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the fluid loss additives industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Fluid Loss Additives Market Report

The fluid loss additives market was valued at USD 318.42 Million in 2025.

The fluid loss additives market is projected to exhibit a CAGR of 2.82% during 2026-2034, reaching a value of USD 409.06 Million by 2034.

The key factors driving the fluid loss additives market include expanding oil and gas exploration activities, growing complexity of drilling operations, increasing adoption of eco-friendly drilling fluid formulations, rising deepwater and ultra-deepwater drilling projects, technological advancements in additive chemistry, and the emphasis on maintaining wellbore stability and formation protection during drilling operations.

North America currently dominates the fluid loss additives market, accounting for a share of 34.2%. The region benefits from extensive shale drilling operations, well-established oilfield services infrastructure, active exploration campaigns across major basins, and strong demand for advanced drilling chemicals.

Some of the major players in the fluid loss additives market include BASF SE, Clariant AG, Global Drilling Fluids and Chemicals Limited, Halliburton Company, Kemira OYJ, Newpark Resources Inc., Nouryon, Schlumberger Limited, Sepcor Inc., Solvay S.A, Tytan Organics Pvt. Ltd, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade