Fluoroscopy Equipment Market Size, Share, Trends and Forecast by Equipment Type, Application, End User, and Region, 2026-2034

Fluoroscopy Equipment Market Size, Share, Trends & Forecast (2026-2034)

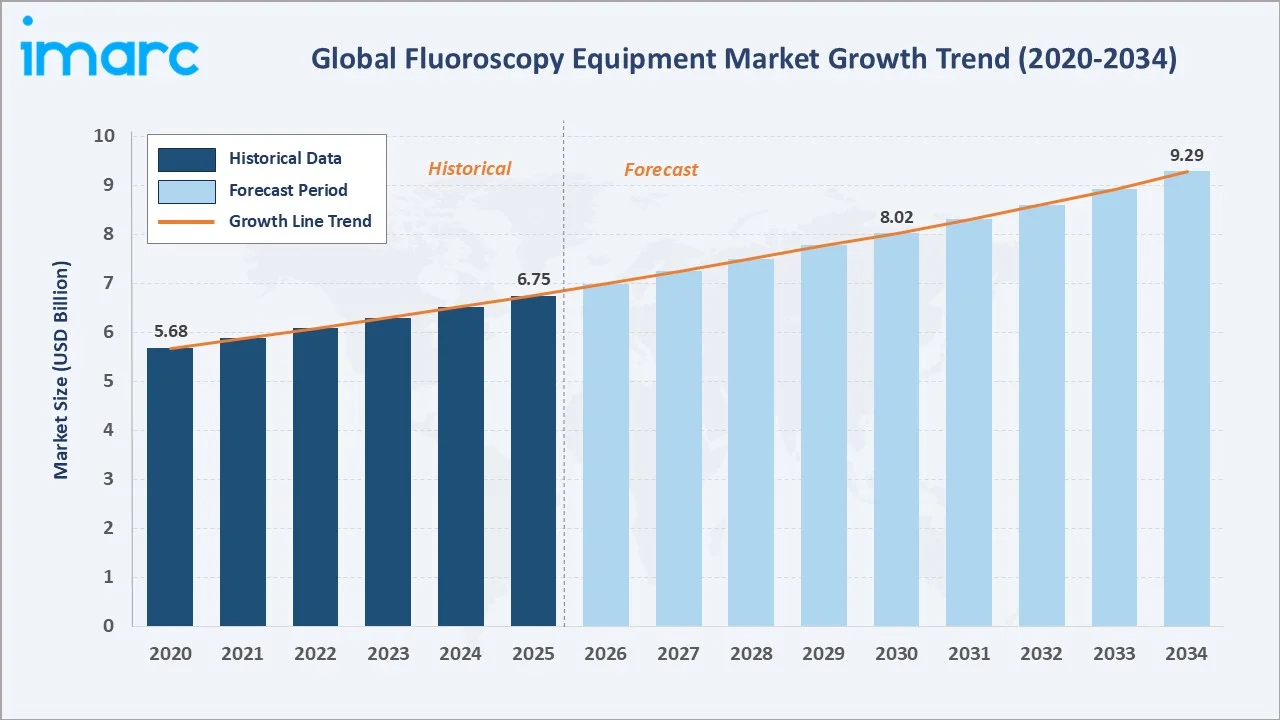

The global fluoroscopy equipment market size reached USD 6.75 Billion in 2025 and is projected to reach USD 9.29 Billion by 2034, exhibiting a CAGR of 3.50% during 2026-2034. Rising aging populations, technological advancements, and increasing chronic disease prevalence are the primary growth forces shaping this market.

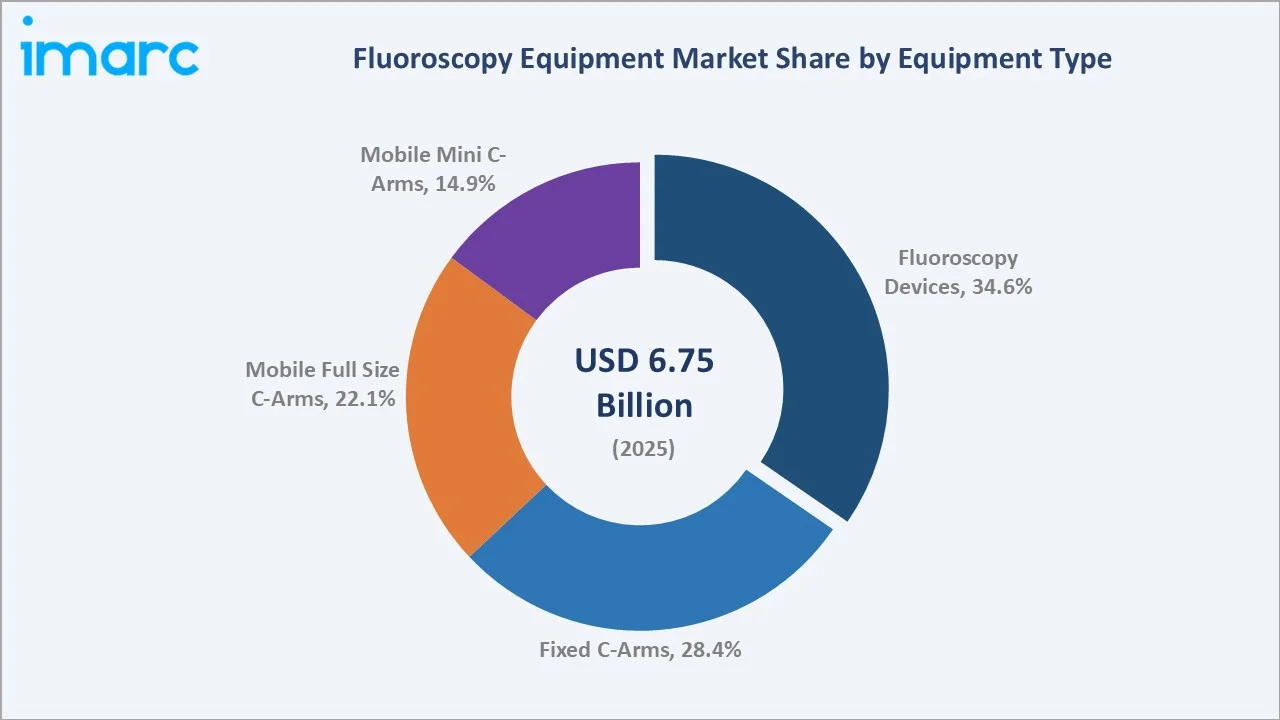

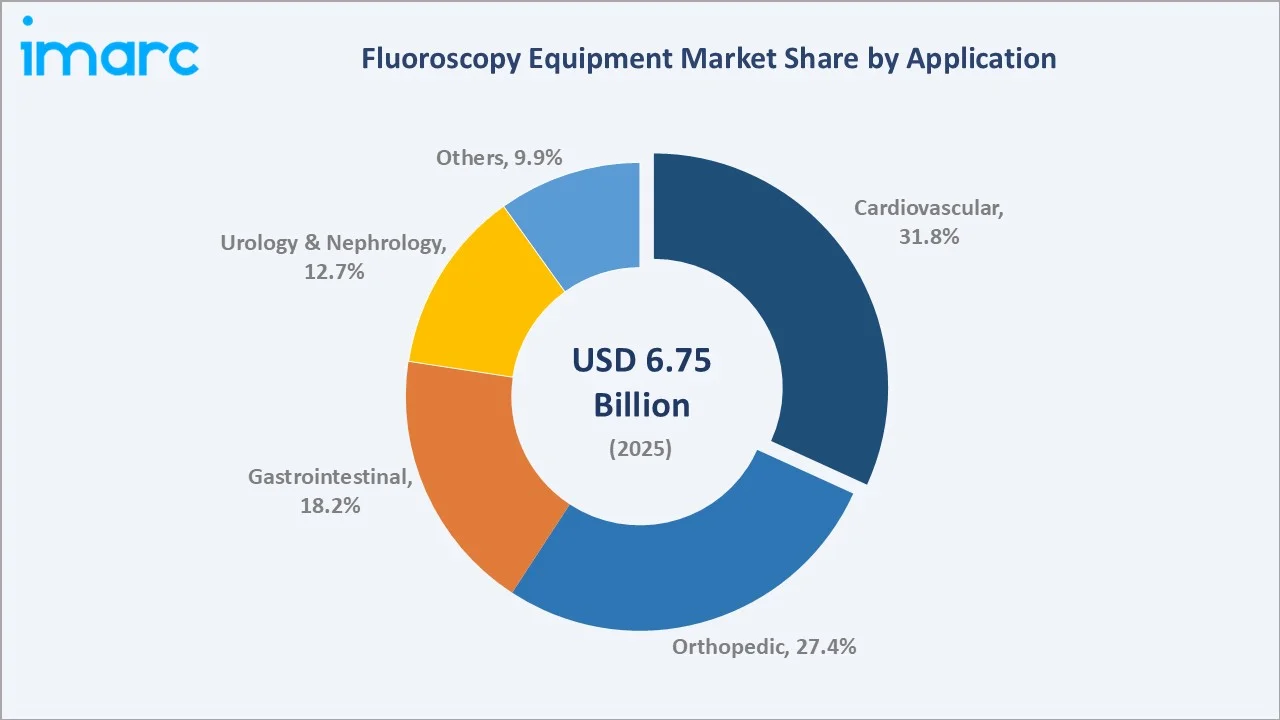

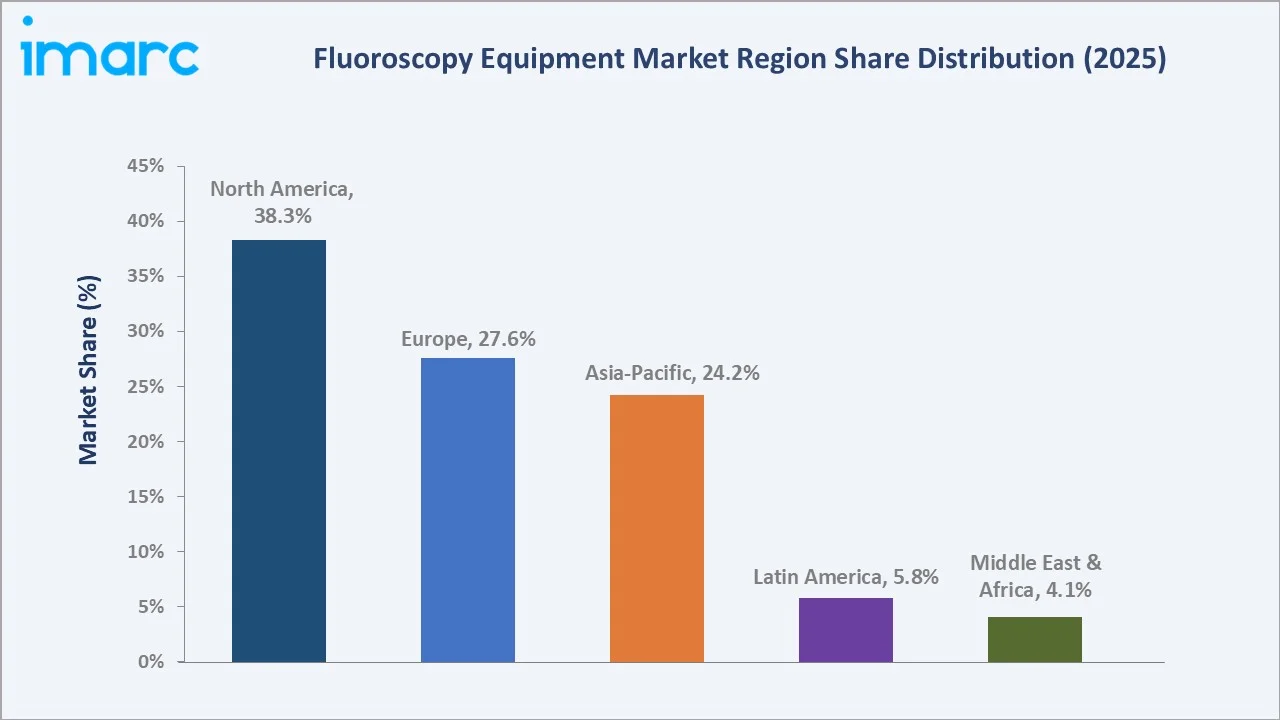

Fluoroscopy Devices lead equipment type segmentation at 34.6% in 2025, driven by broad diagnostic adoption across multiple clinical specialties. Cardiovascular commands 31.8% application share, reflecting real-time imaging demand in interventional cardiology. North America dominates the regional landscape with a 38.3% share, underpinned by advanced healthcare infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.75 Billion |

|

Forecast Market Size (2034) |

USD 9.29 Billion |

|

CAGR (2026-2034) |

3.50% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Equipment Type |

Fluoroscopy Devices (34.6% share, 2025) |

|

Leading Application |

Cardiovascular (31.8% share, 2025) |

|

Leading Region |

North America (38.3% share, 2025) |

The fluoroscopy equipment market growth trajectory from 2020 through 2034 reflects consistent demand driven by interventional procedure expansion and flat-panel detector adoption. The forecast to USD 9.29 Billion by 2034 captures accelerating mobile C-arm uptake, rising cardiovascular interventions, and sustained equipment upgrade cycles globally.

To get more information on this market, Request Sample

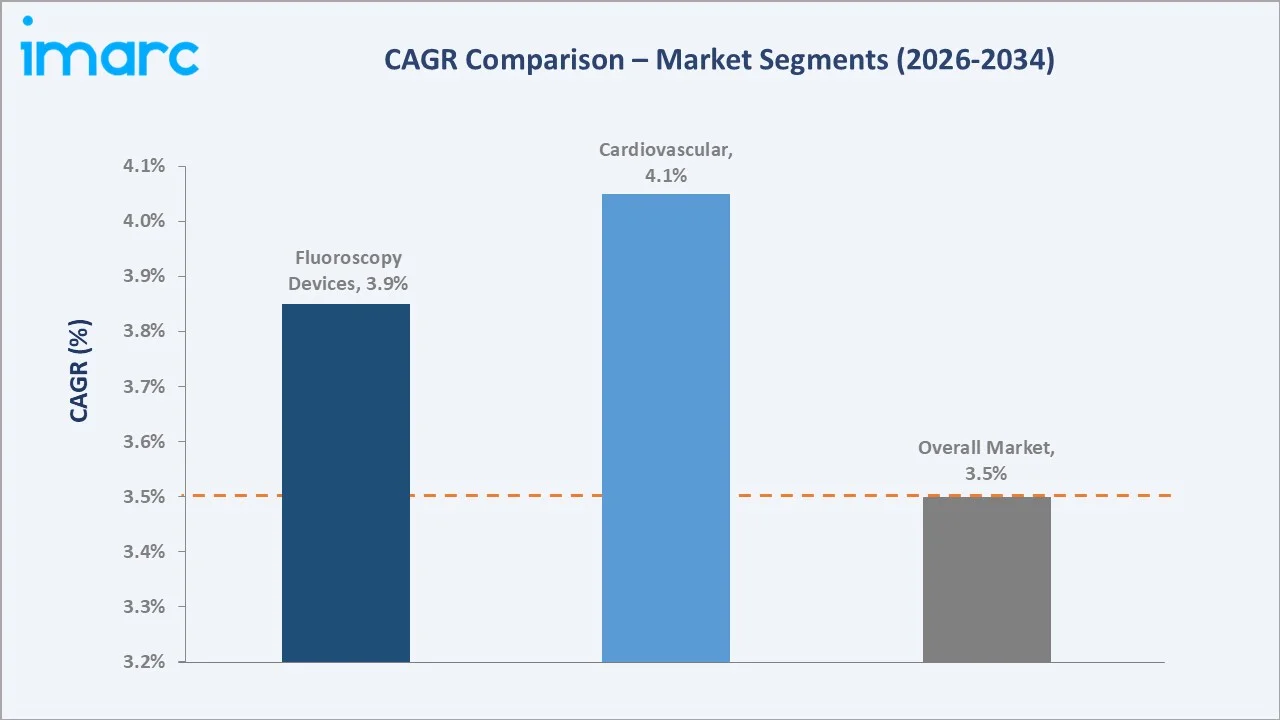

The CAGR trajectories across key equipment type and application sub-segments highlight Cardiovascular at approximately 4.05% CAGR and Fluoroscopy Devices at approximately 3.85% CAGR as the fastest-growing categories within the fluoroscopy equipment market through 2034.

Executive Summary

The global fluoroscopy equipment market is on a sustained growth trajectory from USD 6.75 Billion in 2025 to USD 9.29 Billion by 2034. The sector encompasses diagnostic fluoroscopy rooms, fixed C-arms, and mobile systems, benefiting from aging demographics and rising interventional procedure demand.

Fluoroscopy Devices lead at 34.6% in 2025, owing to their versatile role across cardiovascular, gastrointestinal, and orthopedic imaging. Fixed C-Arms (28.4%) serve high-volume surgical theatres requiring consistent intraoperative real-time imaging guidance throughout complex procedures.

Mobile Full Size C-Arms (22.1%) provide operating room flexibility for orthopedic and trauma surgeries. Mobile Mini C-Arms (14.9%) serve outpatient orthopedic and podiatry clinics, offering compact imaging solutions for extremity procedures across ambulatory and outpatient surgical settings.

Cardiovascular leads application at 31.8% in 2025, driven by interventional cardiology's reliance on fluoroscopic guidance for angioplasty, stenting, and electrophysiology. Orthopedic (27.4%) is second largest, supported by growing joint replacement and fracture management procedure volumes.

North America dominates at 38.3% in 2025, supported by advanced diagnostic infrastructure, high procedure utilization, and strong reimbursement frameworks. Europe follows at 27.6%, driven by systematic equipment modernization and expanding interventional radiology programs globally.

Key Market Insights

|

Insight |

Data |

|

Largest Equipment Type |

Fluoroscopy Devices – 34.6% share (2025) |

|

Leading Application |

Cardiovascular – 31.8% share (2025) |

|

Leading Region |

North America – 38.3% share (2025) |

|

Second Largest Region |

Europe – 27.6% share (2025) |

|

Top Companies |

GE HealthCare, Koninklijke Philips N.V., Canon Inc., Shimadzu Corporation, and Ziehm Imaging GmbH |

Key Analytical Observations Expanding on the Above Data:

- Fluoroscopy Devices dominate at 34.6% in 2025, because of their indispensable versatility across diagnostic and interventional applications. Their adoption of flat-panel detector technology and advanced dose reduction features sustains leading market share through the 2034 forecast horizon.

- Cardiovascular applications command 31.8% share because interventional cardiology procedures, including angioplasty, stenting, and electrophysiology, require continuous fluoroscopic guidance. Rising global cardiovascular disease prevalence sustains strong and growing procedure volume supporting this leading segment.

- North America's 38.3% regional dominance reflects its high procedure utilization rates, established payor reimbursement, and concentrated vendor presence. Continuous technology refresh cycles among major U.S. and Canadian hospitals maintain robust fluoroscopy equipment demand through 2034.

- Cardiovascular applications, growing at approximately 4.05% CAGR, benefit from structural heart disease programs, transcatheter valve procedures, and peripheral vascular interventions expanding procedure volumes across both developed and emerging healthcare markets through 2034.

Fluoroscopy Equipment Market Overview

The fluoroscopy equipment market encompasses real-time X-ray imaging devices used in diagnostic and interventional procedures across hospitals, diagnostic centers, and ambulatory surgical facilities. Product categories span large fixed fluoroscopy rooms, mobile C-arms, and compact mini C-arm systems for diverse clinical applications.

The ecosystem integrates global equipment manufacturers, component and detector suppliers, healthcare system buyers, regulatory agencies, and after-market service providers serving institutions across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa regions.

Market Dynamics

To evaluate market opportunities, Request Sample

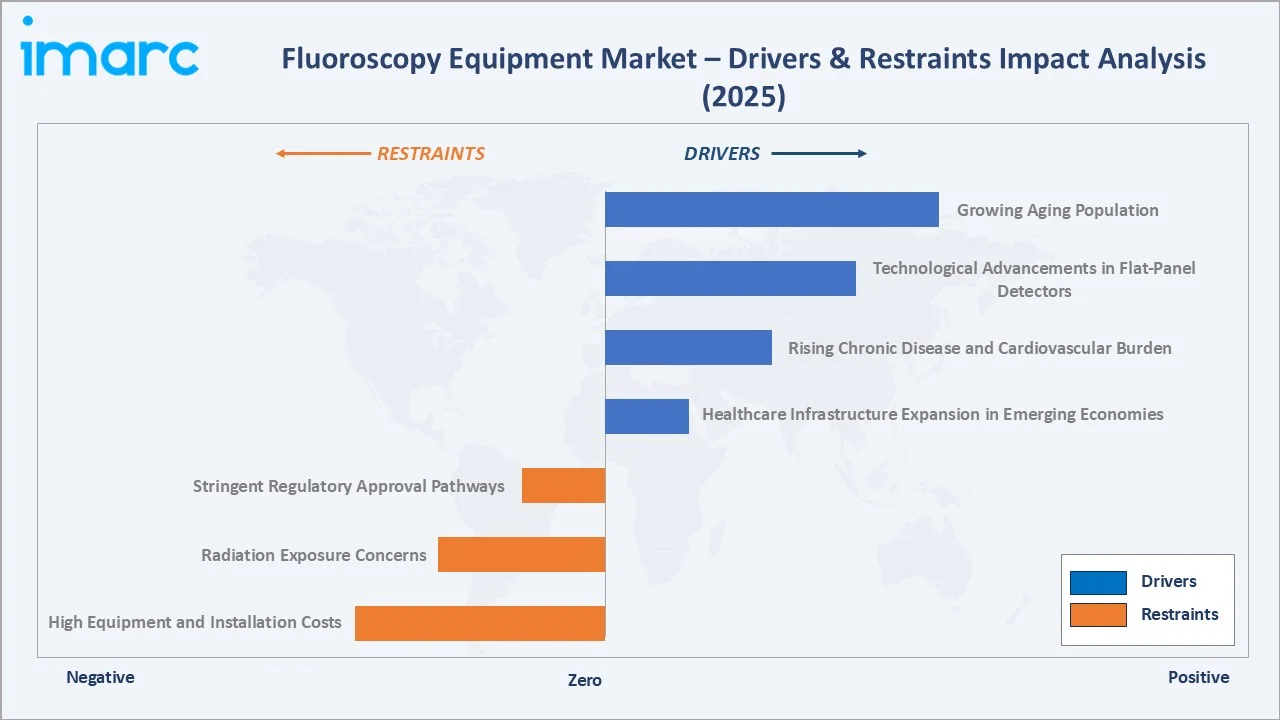

Market Drivers

- Growing Aging Population: The global aging population is driving demand for fluoroscopy-guided orthopedic, cardiovascular, and gastrointestinal procedures. Elderly patients require greater diagnostic imaging frequency, sustaining strong equipment procurement demand across hospitals and specialized imaging centers worldwide.

- Technological Advancements in Flat-Panel Detectors: Transition from image intensifiers to flat-panel detector systems improves image quality and reduces radiation dose. Major manufacturers continuously introduce advanced detector technologies that accelerate equipment upgrade cycles across global healthcare facilities and interventional procedure centers.

- Rising Chronic Disease and Cardiovascular Burden: Increasing prevalence of cardiovascular disease, cancer, and gastrointestinal disorders expands interventional procedure volumes requiring fluoroscopic guidance. Rising chronic disease burden creates sustained structural demand supporting consistent market growth through the entire 2034 forecast horizon.

- Healthcare Infrastructure Expansion in Emerging Economies: Rapid hospital construction and healthcare system modernization in Asia-Pacific, Latin America, and Middle East & Africa create substantial new equipment demand. Government healthcare initiatives and international development funding accelerate fluoroscopy equipment procurement across these high-growth regions.

Market Restraints

- High Equipment and Installation Costs: Advanced fluoroscopy systems require significant capital investment. High costs and complex installation requirements limit adoption among smaller healthcare facilities and resource-constrained healthcare systems, particularly across developing economies seeking to modernize diagnostic imaging infrastructure.

- Radiation Exposure Concerns: Occupational radiation exposure risks for healthcare staff and cumulative dose concerns for patients create clinical hesitation and regulatory scrutiny. Stringent radiation protection protocols increase operational complexity and training requirements, constraining utilization growth in some clinical environments.

- Stringent Regulatory Approval Pathways: Complex FDA, CE mark, and international regulatory clearance processes extend market entry timelines for new products. Extended approval cycles increase development costs and delay technology commercialization, particularly affecting smaller manufacturers introducing innovative fluoroscopy systems globally.

Market Opportunities

- AI Integration and Automated Imaging: Artificial intelligence integration enables automated image enhancement, real-time anatomy recognition, and dose optimization. AI-powered fluoroscopy systems represent a significant premium market opportunity as healthcare providers prioritize diagnostic accuracy and workflow efficiency improvements.

- Expansion of Ambulatory Surgery Centers: Rapid global growth of ambulatory surgery centers creates demand for compact mobile fluoroscopy solutions. Mini C-arms and portable systems serving outpatient orthopedic and pain management procedures represent an expanding segment with favorable reimbursement dynamics in developed economies.

Market Challenges

- Competition from Alternative Imaging Modalities: MRI, CT, and ultrasound technologies compete with fluoroscopy for procedure guidance in certain clinical applications. Continuous competing modality improvements require manufacturers to innovate in dose reduction, image quality, and workflow integration to maintain clinical preference and market positioning.

- Equipment Maintenance and Total Ownership Costs: Complex fluoroscopy systems require specialized service contracts, periodic tube replacement, and detector maintenance increasing total ownership costs. High ongoing maintenance expenditures influence healthcare provider procurement decisions and extend equipment replacement cycles in budget-constrained institutional settings.

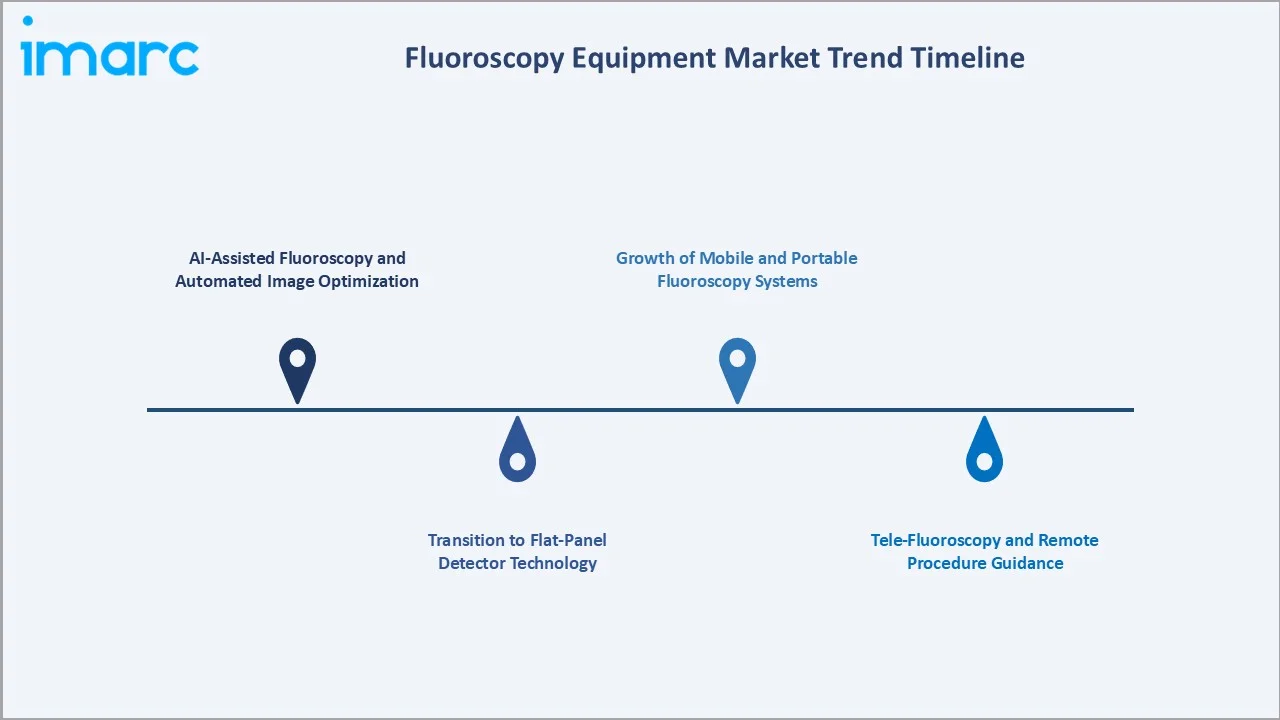

Emerging Market Trends

1. AI-Assisted Fluoroscopy and Automated Image Optimization

Machine learning algorithms are enabling real-time image enhancement, noise reduction, and automatic collimation in fluoroscopy systems. AI-assisted tools reduce radiation dose while maintaining diagnostic image quality, transforming interventional radiology workflow efficiency across major global healthcare systems.

2. Transition to Flat-Panel Detector Technology

The shift from analog image intensifiers to digital flat-panel detectors is accelerating market-wide. Flat-panel systems offer superior contrast resolution, compact footprint, and enhanced dose management, driving equipment upgrade cycles among hospitals and specialty imaging centers globally through 2034.

3. Growth of Mobile and Portable Fluoroscopy Systems

Increasing demand from ambulatory surgery centers, emergency departments, and point-of-care settings is driving mobile C-arm adoption. Compact wireless-enabled portable systems enable bedside fluoroscopic guidance, expanding clinical utilization beyond traditional imaging suite environments across diverse care settings.

4. Tele-Fluoroscopy and Remote Procedure Guidance

Telemedicine integration with fluoroscopy systems enables remote expert guidance for complex interventional procedures at underserved facilities. Advances in low-latency image transmission and robotic catheter systems support expanding tele-fluoroscopy capabilities, broadening clinical access in developing and remote healthcare markets.

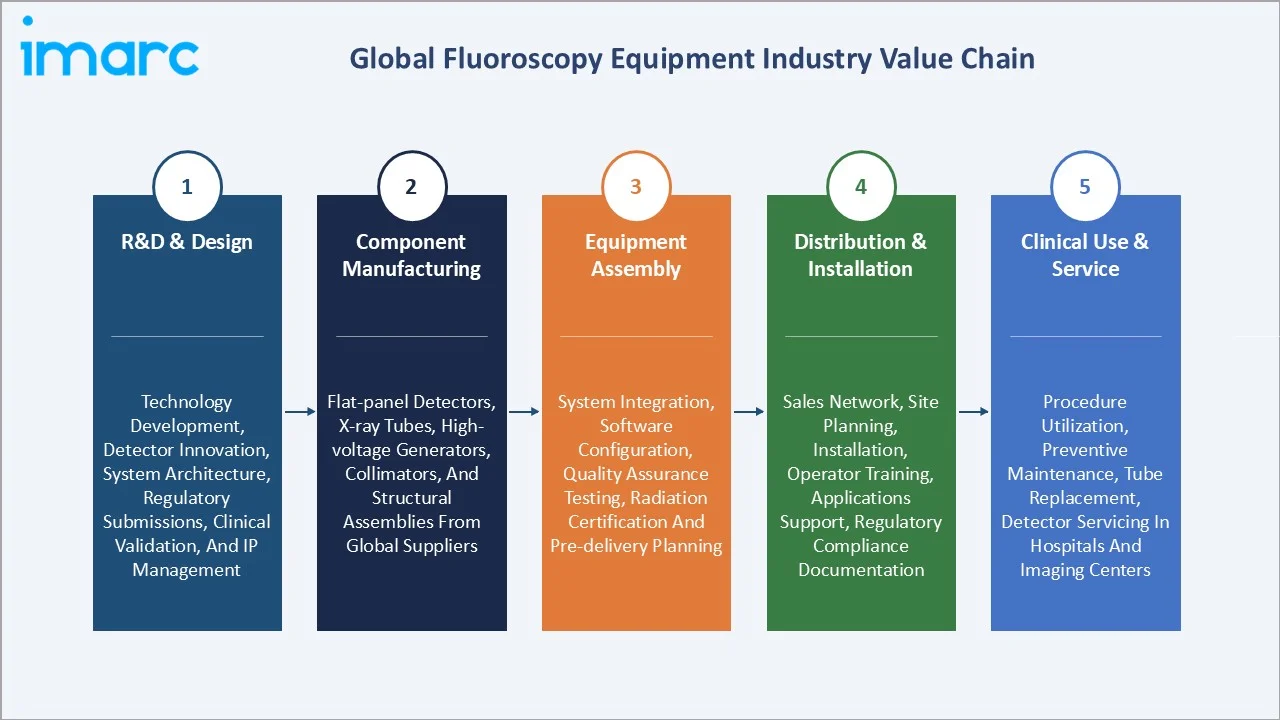

Industry Value Chain Analysis

The fluoroscopy equipment value chain spans five integrated stages from R&D through end-use service. Equipment design and component manufacturing capture primary engineering value, while distribution, installation, and post-sale service provide critical lifecycle support and generate recurring revenue streams globally.

|

Stage |

Key Activities |

|

R&D & Design |

Technology development, detector innovation, system architecture, regulatory submissions, clinical validation, and intellectual property management |

|

Component Manufacturing |

Flat-panel detectors, X-ray tubes, high-voltage generators, collimators, and structural assemblies sourced from specialized global suppliers |

|

Equipment Assembly |

System integration, software configuration, quality assurance testing, radiation certification, and pre-delivery customer site planning |

|

Distribution & Installation |

Sales network, site planning, equipment installation, operator training, applications support, and regulatory compliance documentation |

|

Clinical Use & Service |

Procedure utilization, preventive maintenance, tube replacement, detector servicing, software upgrades, and end-of-life equipment management |

R&D and component manufacturing capture the highest intrinsic value, representing core technological differentiation for market-leading manufacturers. Post-sale service contracts represent significant recurring revenue, with major OEMs generating substantial margins from multi-year comprehensive maintenance agreements globally.

Technology Landscape in the Fluoroscopy Equipment Industry

Flat-Panel Detector (FPD) Technology

Amorphous silicon and amorphous selenium flat-panel detectors deliver superior dynamic range and spatial resolution compared to conventional image intensifiers. Continuous refinement in pixel pitch and scintillator materials by manufacturers enhances diagnostic image fidelity.

AI-Powered Image Processing and Dose Management

Deep learning algorithms enable intelligent noise filtering, automatic exposure control, and anatomy-specific imaging protocols. AI-driven dose management tools reduce patient and operator radiation exposure while maintaining diagnostic quality across cardiovascular, orthopedic, and interventional radiology procedure types.

Robotic Fluoroscopy and Remote Navigation Systems

Robotically assisted C-arm positioning and remote catheter navigation systems enhance procedural precision while reducing operator radiation exposure. Integration of robotic fluoroscopy with electrophysiology mapping platforms represents a significant technology convergence opportunity for next-generation cardiac intervention suites.

3D Fluoroscopy and Cone-Beam CT Integration

Hybrid fluoroscopy–cone beam CT systems provide three-dimensional rotational angiography within interventional suites. This technology convergence enables intraoperative volume imaging, reducing need for separate CT procedures and enhancing guidance precision in complex vascular and neuro-interventional procedures.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Equipment Type |

Fluoroscopy Devices |

34.6% |

2025 |

|

Application |

Cardiovascular |

31.8% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

North America |

38.3% |

2025 |

By Equipment Type

Fluoroscopy Devices command a 34.6% majority share in 2025 owing to their versatility across diagnostic and interventional applications. Advanced digital flat-panel models with dose reduction features drive replacement demand across hospitals and diagnostic imaging centers globally through 2034.

To access detailed market analysis, Request Sample

Fixed C-Arms (28.4%) serve high-volume surgical theaters requiring consistent real-time imaging. Mobile Full Size C-Arms (22.1%) provide operating room flexibility for trauma and orthopedic cases, while Mobile Mini C-Arms (14.9%) serve outpatient orthopedic and podiatry applications across ambulatory care settings.

By Application

Cardiovascular dominates at 31.8% in 2025, driven by interventional cardiology's reliance on real-time fluoroscopic guidance for angioplasty, stenting, structural heart, and electrophysiology procedures. Rising cardiovascular disease prevalence sustains growing interventional procedure volumes across global healthcare systems.

Orthopedic (27.4%) captures C-arm demand for fracture fixation and joint replacement guidance. Gastrointestinal (18.2%) serves barium studies and endoscopic procedure fluoroscopy. Urology and Nephrology (12.7%) utilizes fluoroscopy for stone management, renal access, and urological intervention procedures.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.3% |

Advanced healthcare infrastructure; high procedure volumes; strong reimbursement frameworks; early technology adoption in United States and Canada |

|

Europe |

27.6% |

Equipment modernization programs; aging population; strong interventional radiology investment; regulatory harmonization across EU member states |

|

Asia-Pacific |

24.2% |

Rapid hospital expansion; rising healthcare expenditure; government health investment in China, India, and Southeast Asian emerging economies |

|

Latin America |

5.8% |

Growing private hospital sector; expanding diagnostic imaging access; government public health infrastructure programs in Brazil and Mexico |

|

Middle East & Africa |

4.1% |

Healthcare modernization initiatives; new hospital construction; medical tourism growth supporting advanced imaging equipment procurement |

North America's 38.3% market dominance in 2025 is driven by advanced interventional procedure volumes, strong payor reimbursement, and concentrated presence of leading technology vendors. The United States accounts for the majority of regional demand, supported by high per-capita healthcare expenditure and technology adoption rates.

Europe at 27.6% benefits from systematic equipment modernization across NHS and publicly funded healthcare systems in Germany, France, and the Netherlands. An aging population and expanding interventional cardiology programs sustain strong fluoroscopy demand across Western and Central European markets.

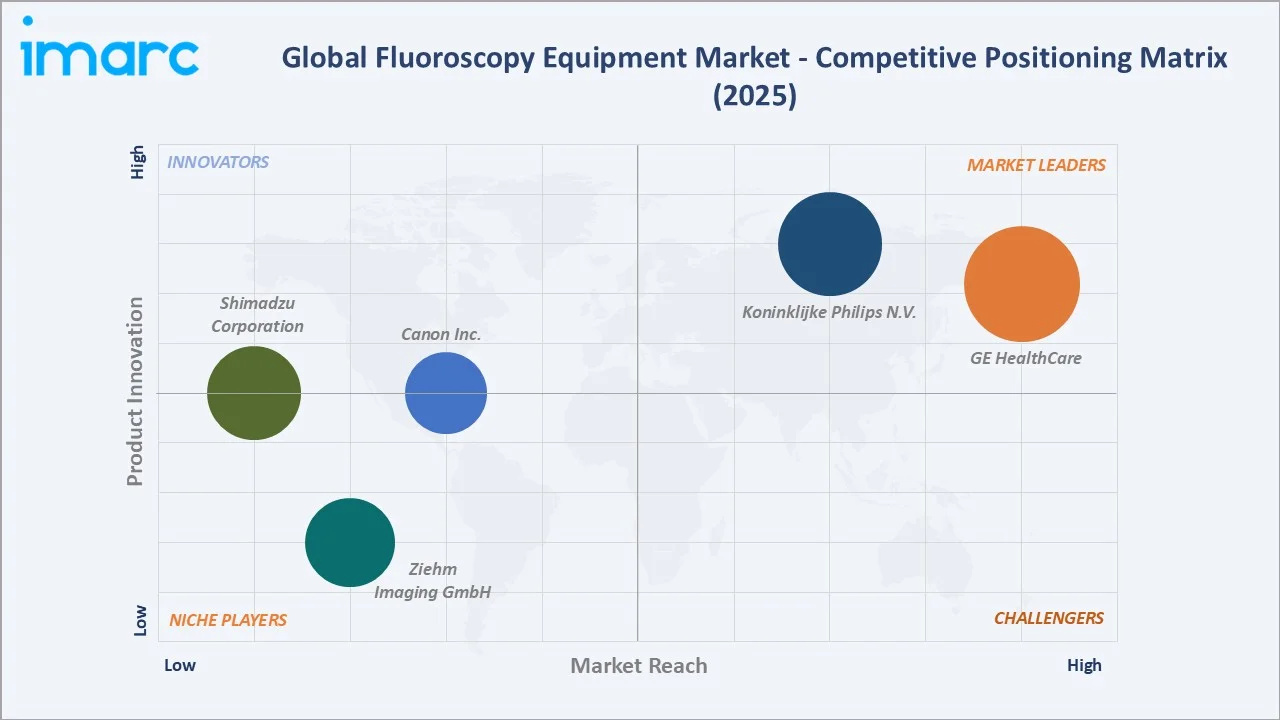

Competitive Landscape

The global fluoroscopy equipment market is moderately concentrated, with global medical imaging majors commanding leading positions through technological differentiation, service networks, and established regulatory clearances. Specialized C-arm manufacturers compete effectively on mobility, image quality, and procedure-specific optimization.

|

Company Name |

Key Products / Operations |

Market Position |

Global Strategic Focus |

|

GE HealthCare |

Discovery RF180 Radiography and Fluoroscopy System |

Leader |

AI imaging, emerging market expansion, service growth |

|

Koninklijke Philips N.V. |

Fluoroscopy 7000 N — ProxiDiagnost N90 |

Leader |

Image-guided therapy integration, cardiovascular workflow optimization, precision diagnostics |

|

Canon Inc. |

Ultimax-i, Zexira i9 digital fluoroscopy systems |

Established |

Flat-panel innovation, dose reduction, expanding Asia-Pacific market presence |

|

Shimadzu Corporation |

FLEXAVISION F4, FLEXAVISION HB/FD, FLUOROspeed X1 |

Established |

Precision imaging, expanding Asia-Pacific distribution reach |

|

Ziehm Imaging GmbH |

Ziehm Vision RFD, Ziehm Solo FD mobile C-arm systems |

Niche |

High-quality mobile C-arm specialization, surgical imaging focus, European market leadership |

Key players include GE HealthCare, Koninklijke Philips N.V., Canon Inc., Shimadzu Corporation, and Ziehm Imaging GmbH, among others.

Key Company Profiles

GE HealthCare

GE HealthCare operates as one of the largest global medical imaging portfolios. The company is a dominant force in mobile C-arm technology and fixed fluoroscopy systems, serving cardiovascular, orthopedic, and surgical imaging applications across healthcare facilities globally.

- Product Portfolio: Discovery RF180 Radiography and Fluoroscopy System

- Strategic Focus: GE HealthCare focuses on mobile C-arm leadership through AI-assisted imaging and remote connectivity. Expansion in Asia-Pacific and Latin America through distribution partnerships targets emerging market hospital procurement programs and public health infrastructure investments.

Koninklijke Philips N.V.

Koninklijke Philips N.V. is a global health technology leader with a strong interventional imaging portfolio. The company's Azurion image-guided therapy platform integrates fluoroscopy with hemodynamic monitoring and procedure planning, serving cardiovascular and interventional radiology applications globally.

- Product Portfolio: Fluoroscopy 7000 N — ProxiDiagnost N90

- Strategic Focus: Koninklijke Philips N.V. is executing an image-guided therapy strategy integrating fluoroscopy with AI clinical decision support and digital pathways. Investment in cardiovascular workflow optimization positions Philips as a strategic partner for complex cardiac intervention centers.

Market Concentration Analysis

The fluoroscopy equipment market is moderately concentrated at the product segment level. GE Healthcare, Koninklijke Philips N.V., and others collectively command leading positions, though specialized manufacturers such as Ziehm Imaging GmbH compete effectively in focused mobile C-arm niches.

Geographic concentration favors North America and Europe at the revenue level, while volume growth is increasingly driven by Asia-Pacific procurement programs. Regulatory fragmentation across key markets creates barriers favoring established global manufacturers with existing clearance portfolios across multiple regions.

Investment & Growth Opportunities

Fastest-Growing Segments

Cardiovascular applications represent the highest-growth segment at approximately 4.05% CAGR through 2034, capturing investment from structural heart programs and complex coronary interventions. Fluoroscopy Devices benefit from ongoing flat-panel technology migration and replacement procurement across aging installed bases globally.

Emerging Markets

Asia-Pacific and Latin America are key investment frontiers with hospital construction programs creating significant new equipment demand. India's expanding private hospital sector and China's healthcare modernization initiative represent transformative procurement opportunities with sustained growth through 2034.

Venture & Investment Trends

Private equity and strategic investors are targeting AI-enabled fluoroscopy software startups and robotic C-arm navigation companies. Integration of fluoroscopy with surgical robotics and augmented reality platforms represents an emerging high-value convergence investment theme globally attracting significant venture capital interest.

Future Market Outlook (2026-2034)

The fluoroscopy equipment market is forecast to expand from USD 6.75 Billion in 2025 to USD 9.29 Billion by 2034 at a CAGR of 3.50%, driven by aging demographics, interventional procedure growth, and sustained technology advancement in digital imaging and AI-integrated fluoroscopy systems.

Three structural forces will shape the market through 2034: flat-panel detector adoption will drive replacement cycles globally; AI integration will redefine imaging workflow efficiency; and Asia-Pacific infrastructure expansion will shift global volume concentration progressively toward high-growth emerging healthcare markets.

Research Methodology

Primary Research

Primary research encompassed structured interviews with hospital imaging directors, interventional cardiologists, radiology procurement managers, and leading fluoroscopy manufacturers. Primary data validated market sizing, segment shares, regional estimates, and technology adoption trends across key geographies.

Secondary Research

Key secondary sources include FDA device clearance databases, European CE marking registries, WHO health technology reports, IEC imaging equipment standards, annual reports of key manufacturers, and industry association publications on diagnostic imaging market trends and interventional procedure volume data.

Forecasting Models

Market size estimations used combined top-down and bottom-up models incorporating healthcare expenditure data, procedure volume projections, equipment replacement rates, and macroeconomic GDP growth scenarios. Base, optimistic, and conservative scenario modelling was applied through the 2034 forecast horizon.

Fluoroscopy Equipment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Equipment Types Covered | Fluoroscopy Devices, Fixed C-Arms, Mobile Full Size C-Arms, Mobile Mini C-Arms |

| Applications Covered | Orthopedic, Cardiovascular, Gastrointestinal, Urology and Nephrology, Others |

| End Users Covered | Hospitals and Specialty Clinics, Diagnostic Centres |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | GE HealthCare, Koninklijke Philips N.V., Canon Inc., Shimadzu Corporation, Ziehm Imaging GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Fluoroscopy Equipment Market Report

The global fluoroscopy equipment market reached USD 6.75 Billion in 2025, reflecting sustained demand driven by cardiovascular and orthopedic procedure growth, flat-panel technology adoption, and ongoing healthcare infrastructure expansion across developed and emerging markets worldwide.

The market is projected to reach USD 9.29 Billion by 2034, growing at a CAGR of 3.50% during 2026-2034, driven by aging demographics, rising interventional procedure volumes, and technology advancements in AI-powered imaging and flat-panel detector systems across global healthcare facilities.

Fluoroscopy Devices lead with a 34.6% market share in 2025. Fixed C-Arms are the second largest at 28.4%, followed by Mobile Full Size C-Arms at 22.1% and Mobile Mini C-Arms at 14.9%, serving diverse clinical settings from hospitals to ambulatory surgical centers.

Cardiovascular dominates with a 31.8% share in 2025, underpinned by interventional cardiology procedure growth. Orthopedic (27.4%) follows, with Gastrointestinal at 18.2%, Urology and Nephrology at 12.7%, and Others at 9.9% completing the application segmentation globally.

North America leads with a 38.3% market share in 2025, supported by advanced healthcare infrastructure. Europe follows at 27.6%, Asia-Pacific at 24.2%, Latin America at 5.8%, and Middle East & Africa at 4.1%, reflecting diverse levels of healthcare system development.

Cardiovascular applications represent the fastest-growing segment at approximately 4.05% CAGR through 2034, driven by structural heart programs and coronary interventions. Fluoroscopy Devices lead equipment type growth at approximately 3.85% CAGR, supported by flat-panel technology migration.

Leading companies include GE HealthCare, Koninklijke Philips N.V., Canon Inc., Shimadzu Corporation, and Ziehm Imaging GmbH, among others.

Key drivers include the growing aging population expanding interventional procedure demand, technological advancements in flat-panel detectors improving image quality, rising chronic disease burden, and healthcare infrastructure expansion across Asia-Pacific and Latin America providing new procurement opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)