Food Logistics Market Size, Share, Trends and Forecast by Transportation Mode, Product Type, Service Type, Segment, and Region, 2026-2034

Food Logistics Market Size, Share, Trends & Forecast (2026-2034)

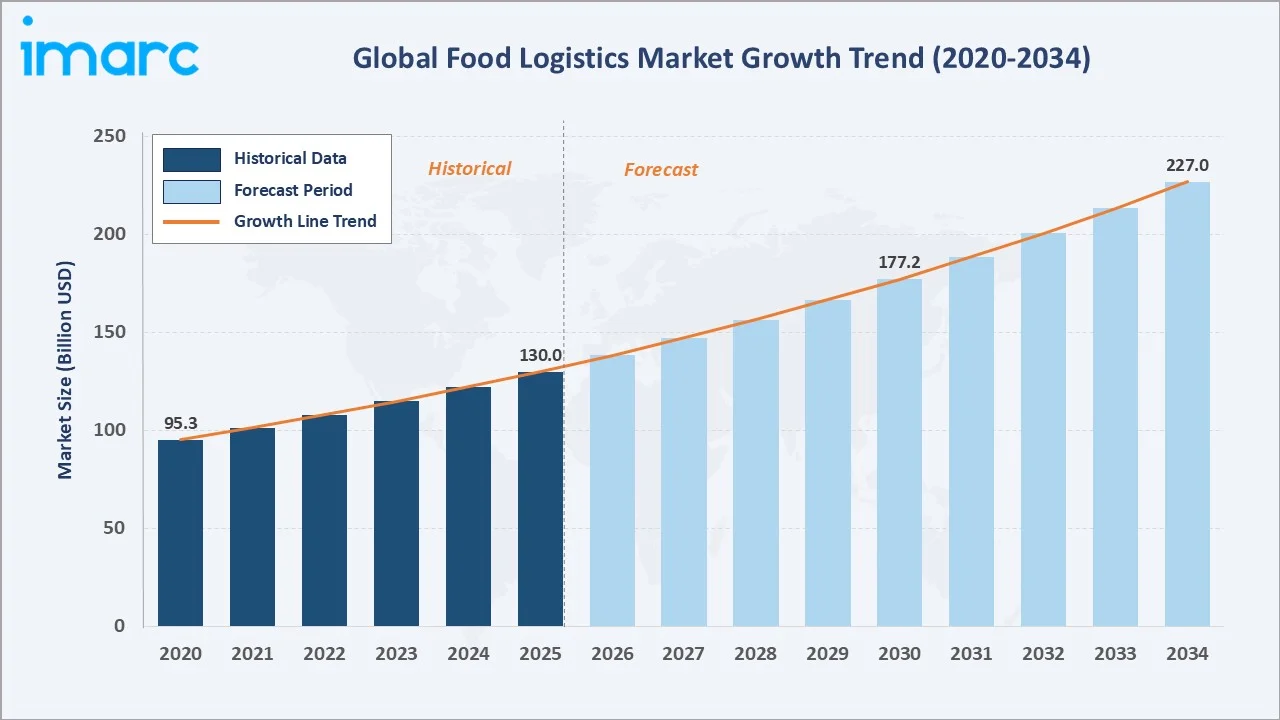

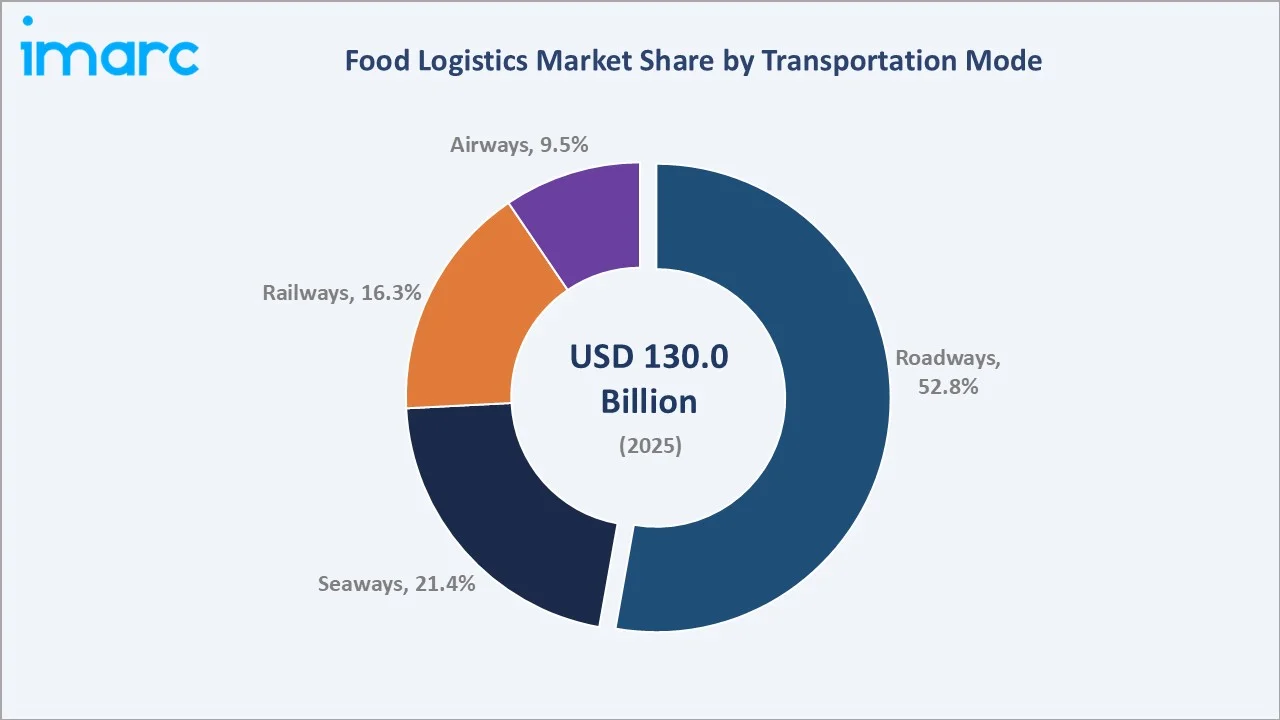

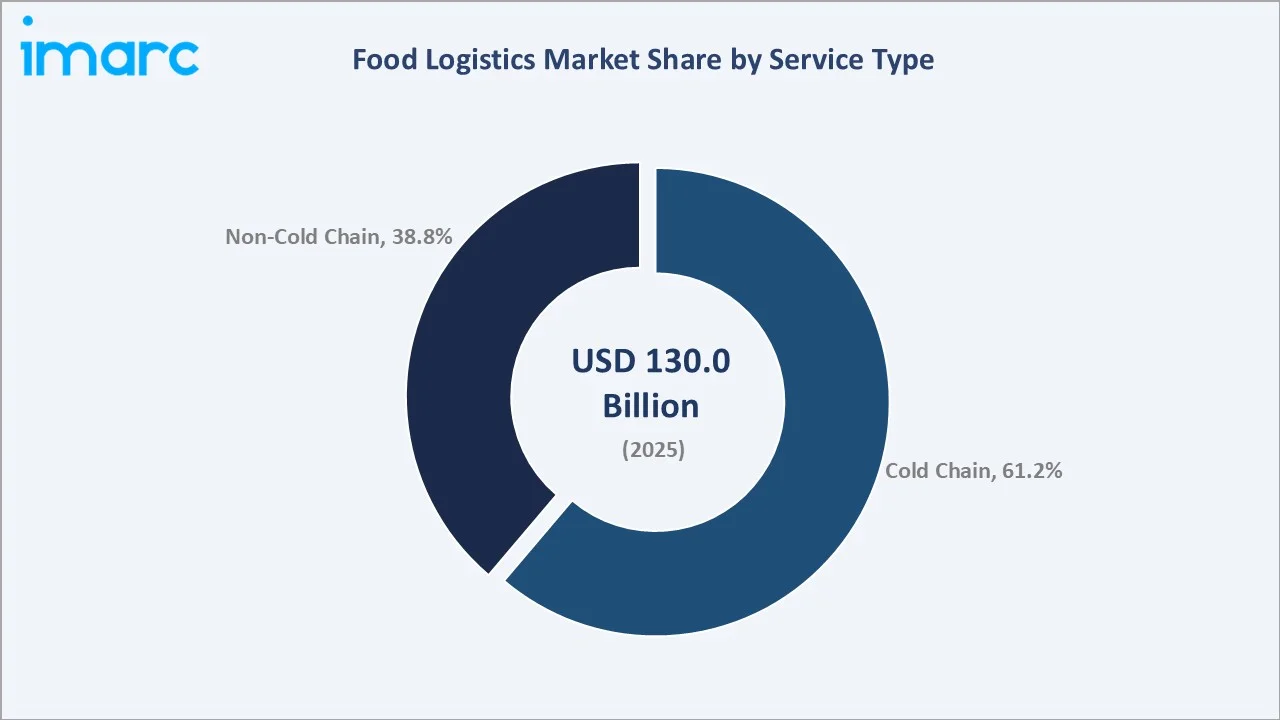

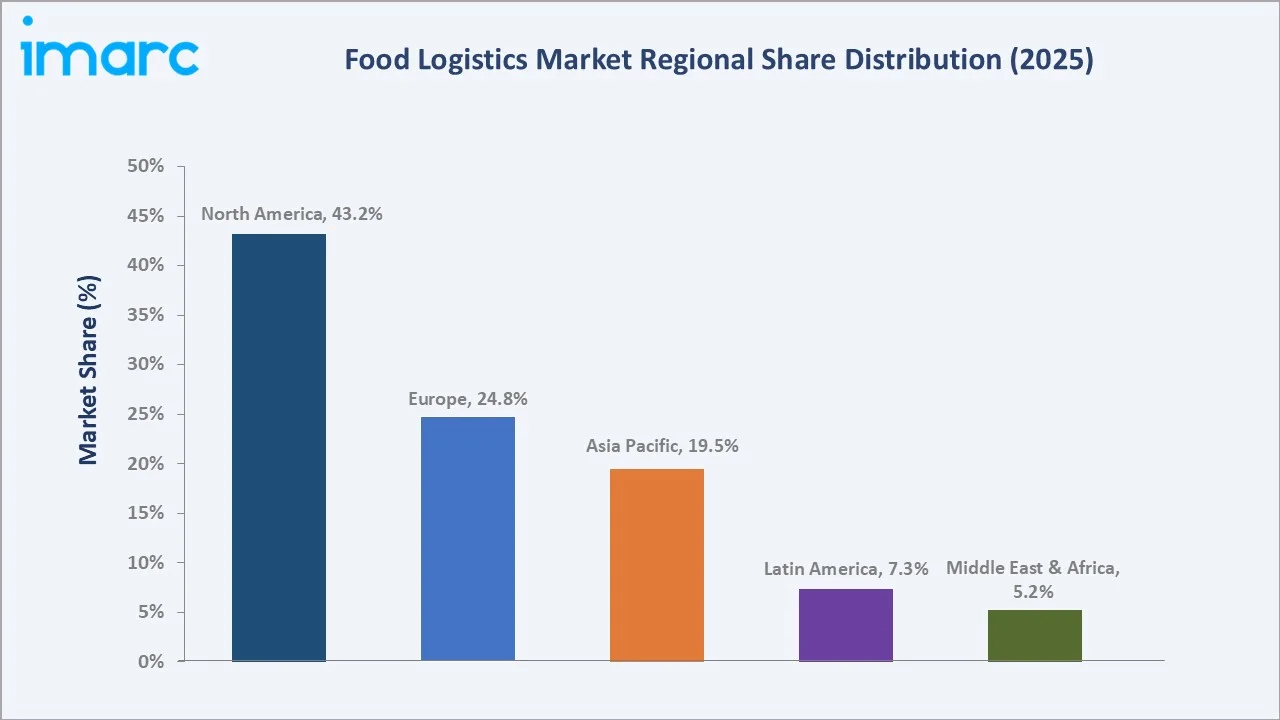

The global food logistics market reached USD 130.0 Billion in 2025 and is projected to reach USD 227.0 Billion by 2034, growing at a CAGR of 6.39% during 2026-2034. The market is driven by the increasing demand for fresh and perishable goods, coupled with advancements in supply chain technology, such as temperature-controlled storage and real-time tracking systems, which ensure product quality and timely deliveries. With 25% of global food production traded internationally and food trade valued at USD 2.3 trillion in 2024, the growing demand for efficient global food logistics to manage this expansive trade is driving market growth. Roadways dominate the transportation mode at 52.8%. Cold chain leads service type at 61.2%. North America commands 43.2% of global market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 130.0 Billion |

|

Forecast Market Size (2034) |

USD 227.0 Billion |

|

CAGR (2026-2034) |

6.39% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Transport Mode |

Roadways (52.8%, 2025) |

|

Dominant Service Type |

Cold Chain (61.2%, 2025) |

|

Leading Region |

North America (43.2%, 2025) |

The market expanded from USD 95.3 Billion in 2020 to USD 130.0 Billion in 2025, anchored at USD 177.2 Billion in 2030, and forecast to reach USD 227.0 Billion by 2034. COVID-19's stress on global food supply chains accelerated investment in cold chain resilience, real-time tracking technology, and domestic food logistics infrastructure, permanently increasing the sophistication and value-added nature of food logistics services as food manufacturers and retailers prioritized supply chain visibility and redundancy over pure cost optimization.

To get more information on this market, Request Sample

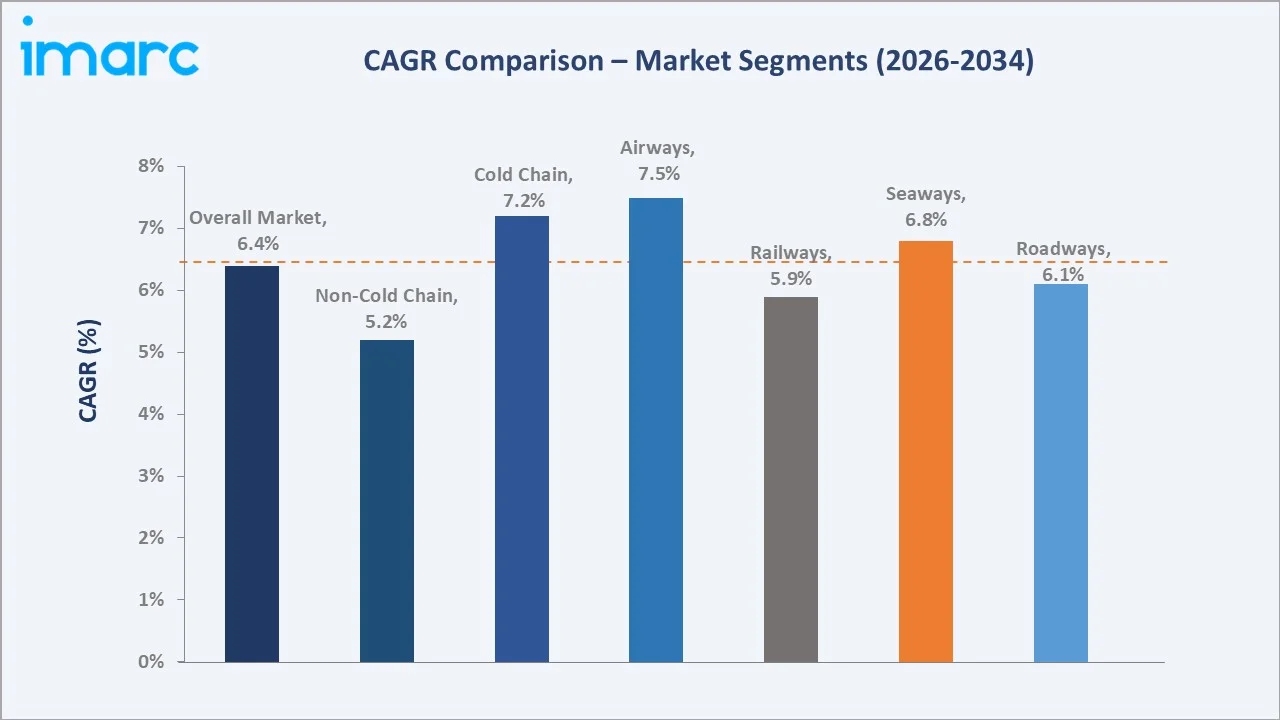

Airways grow fastest at ~7.5% CAGR (2026-2034), driven by high-value perishable air freight where time sensitivity outweighs transport cost premium. Cold chain service type grows at ~7.2% CAGR, outpacing non-cold chain's ~5.2% CAGR, as the global frozen and chilled food markets expand and emerging market cold chain infrastructure investment narrows the cold chain deficit in Asia Pacific, Latin America, and Africa.

Executive Summary

The global food logistics market reached USD 130.0 Billion in 2025, driven by the world's annual food retail and food service economy, which requires sophisticated multimodal, temperature-controlled supply chains. Food logistics encompasses the full spectrum of activities moving food from farm to fork - refrigerated warehousing, temperature-controlled transport, customs clearance for international food trade, last-mile food delivery, and digital supply chain visibility platforms that ensure food safety compliance across complex global supply networks. The market is projected to reach USD 227.0 Billion by 2034 at 6.39% CAGR.

Cold chain services command 61.2% market share (2025), reflecting global consumer preference for fresh, refrigerated, and frozen food categories. Roadways, at 52.8% of transportation mode revenues, serve the inherently local and regional nature of most food distribution. North America, at 43.2%, leads through the US's massive food retail infrastructure and world-class cold chain logistics network.

Key Market Insights

|

Insight |

Data |

|

Dominant Transport Mode |

Roadways - 52.8% share (2025) |

|

Dominant Service Type |

Cold Chain - 61.2% share (2025) |

|

Leading Region |

North America - 43.2% market share (2025) |

Key Analytical Observations Supporting The Above Data:

- Roadways at 52.8% reflecting food logistics' inherently local and regional supply chain character: Road transport dominates because most food distribution is domestic, grocery retailers receive daily deliveries from regional distribution centers via refrigerated trucks, restaurants receive twice-weekly food service deliveries from broadline distributors, and fresh produce moves from regional packing houses to retail stores via local refrigerated trucking fleets.

- Cold chain at 61.2% driven by consumer shift toward fresh, chilled, and frozen food categories: Global fresh and chilled food represents the fastest-growing retail food category with organic fresh produce, premium chilled ready meals, artisanal cheese, sashimi-grade seafood, all requiring a continuous cold chain from 0-4°C without interruption.

- North America at 43.2%, driven by US food retail and food service supply chain sophistication: The United States maintains the world's most sophisticated food logistics infrastructure, mandating end-to-end temperature records for produce and FDA-regulated foods, which drives US cold chain traceability technology.

Food Logistics Market Overview

The food logistics market encompasses all services involved in moving, storing, and distributing food products from point of production to point of consumption, including refrigerated and ambient warehousing, road/rail/sea/air transportation, customs brokerage for international food trade, last-mile food delivery, and digital supply chain management platforms enabling real-time food traceability and temperature monitoring. The market serves global consumers through food supply chains spanning agricultural production zones, food processing facilities, distribution networks, and retail/food service delivery points across all countries.

The ecosystem integrates food producers, 3PL logistics providers, cold chain warehousing REITs, temperature-controlled transport operators, technology platforms, regulatory authorities, and end consumers through retail, e-grocery, restaurant, and institutional food service channels. Macroeconomic factors include rising global trade, increasing disposable incomes, urbanization, the growing demand for convenience and fresh food, and advancements in technology that enhance supply chain efficiency, such as automation and real-time tracking systems.

Market Dynamics

To evaluate market opportunities, Request Sample

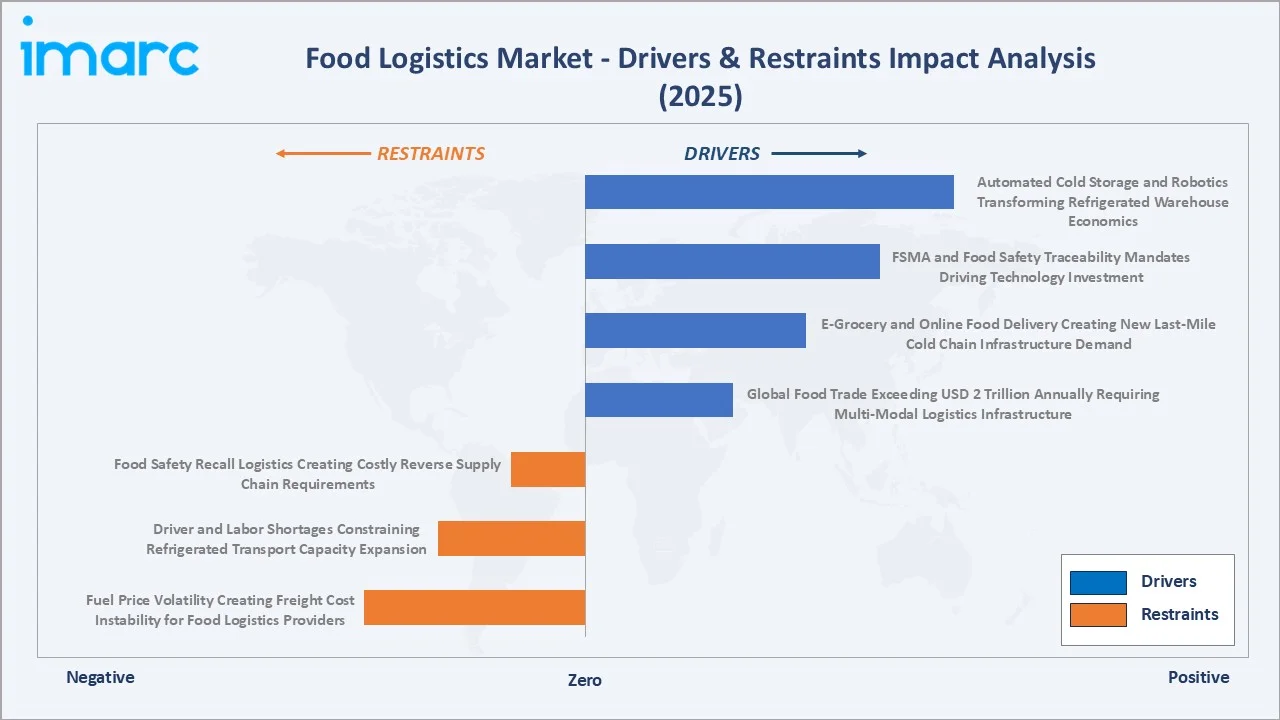

Market Drivers

- Global Food Trade Exceeding USD 2 Trillion Annually Requiring Multi-Modal Logistics Infrastructure: In 2024, 25% of global food production is exchanged internationally, with the value of food and agricultural trade reaching USD 2.3 trillion, with fresh produce, seafood, dairy, meat, and processed foods crossing borders requiring temperature-controlled shipping containers, air cargo perishable handling, customs clearance with food safety documentation, and domestic distribution upon market entry.

- E-Grocery and Online Food Delivery Creating New Last-Mile Cold Chain Infrastructure Demand: Each online grocery order requires a dedicated temperature-controlled picking, packing, and delivery process, creating new demand for automated temperature-controlled fulfillment centers, insulated packaging systems, and last-mile refrigerated vehicle fleets.

- FSMA and Food Safety Traceability Mandates Driving Technology Investment: The US FDA's Food Safety Modernization Act (FSMA) Rule 204 mandates electronic traceability records for high-risk foods across the supply chain, requiring food logistics providers to implement IoT temperature sensors, blockchain-enabled record systems, and cloud traceability platforms.

Market Restraints

- Fuel Price Volatility Creating Freight Cost Instability for Food Logistics Providers: Refrigerated trucks consume 20-30% more fuel than ambient temperature vehicles due to refrigeration unit diesel consumption, making food logistics providers disproportionately exposed to diesel price volatility.

- Driver and Labor Shortages Constraining Refrigerated Transport Capacity Expansion: The driver shortage in refrigerated transport is particularly affected by the additional training requirements for temperature-controlled logistics.

Market Opportunities

- Automated Cold Storage and Robotics Transforming Refrigerated Warehouse Economics: Automated Storage and Retrieval Systems (ASRS) for cold storage are reducing frozen warehouse operating costs through labor reduction, energy efficiency, and utilization improvement.

- Blockchain and IoT Real-Time Food Traceability Creating Premium Service Tier: IoT temperature data loggers embedded in food shipments transmit real-time temperature, humidity, and location data to cloud platforms, enabling food manufacturers to remotely monitor temperature compliance across simultaneous shipments. These traceability services command premium pricing over standard food logistics, creating margin expansion opportunities.

Market Challenges

- Last-Mile Cold Chain Economics Creating Unit Cost Pressure for E-Grocery Business Models: The fundamental economics of e-grocery last-mile cold chain are challenging, delivering a grocery order with fresh, chilled, and frozen items in temperature-segregated packaging to a home costs in delivery expense, representing 16-24% of order value. In comparison, a consumer driving to a store generates zero retailer delivery cost.

- Food Safety Recall Logistics Creating Costly Reverse Supply Chain Requirements: USDA FSIS and FDA food safety recall events require rapid reverse logistics to retrieve potentially contaminated food from retail shelves, distribution centers, and consumer homes.

Emerging Market Trends

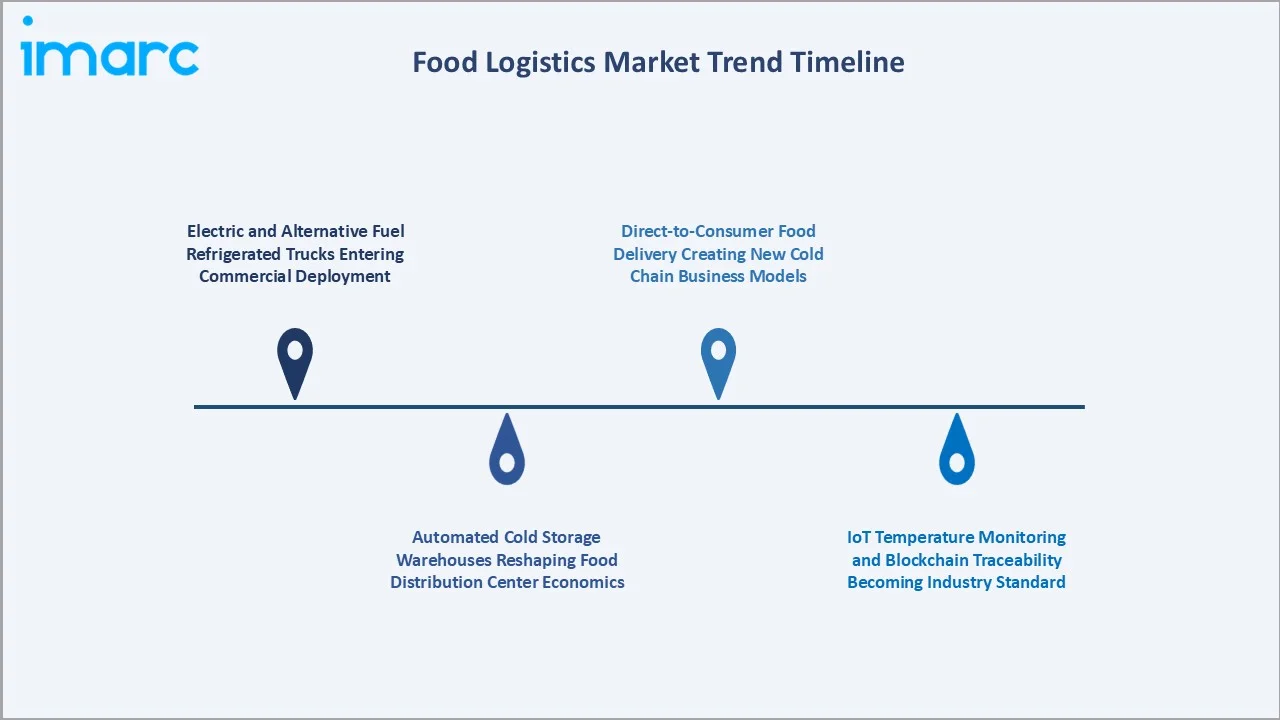

1. Electric and Alternative Fuel Refrigerated Trucks Entering Commercial Deployment

The refrigerated trucking fleet's transition to electric power is entering the commercial deployment phase. This shift is driven by the need to reduce carbon emissions, lower fuel costs, and comply with increasing sustainability regulations, all while ensuring the efficiency and reliability of cold chain transportation.

2. Automated Cold Storage Warehouses Reshaping Food Distribution Center Economics

Automated cold storage warehouses are transforming food distribution center economics by enhancing operational efficiency, reducing labor costs, and improving inventory management. These innovations help optimize space utilization and energy consumption, making the cold chain more cost-effective and responsive to growing demand for fresh food.

3. IoT Temperature Monitoring and Blockchain Traceability Becoming Industry Standard

IoT temperature monitoring and blockchain traceability are becoming industry standards as they improve visibility and control over food safety and quality. These technologies enable real-time monitoring of conditions throughout the supply chain, enhancing transparency and reducing the risk of spoilage or fraud. In September 2022, EROAD launched the CoreHub Xtreme, an advanced IoT trailer monitoring and control gateway designed to enhance supply chain reliability and optimize fleet efficiency in cold chain transportation. The CoreHub Xtreme provides real-time data from all connected assets on a single platform, improving driver safety and fleet performance.

4. Direct-to-Consumer Food Delivery Creating New Cold Chain Business Models

Direct-to-consumer food delivery services are driving the development of new cold chain business models by enabling faster, more efficient distribution of perishable goods. This shift requires innovative solutions for temperature-controlled logistics, ensuring product quality and reducing delivery times to meet consumer expectations for fresh food.

Industry Value Chain Analysis

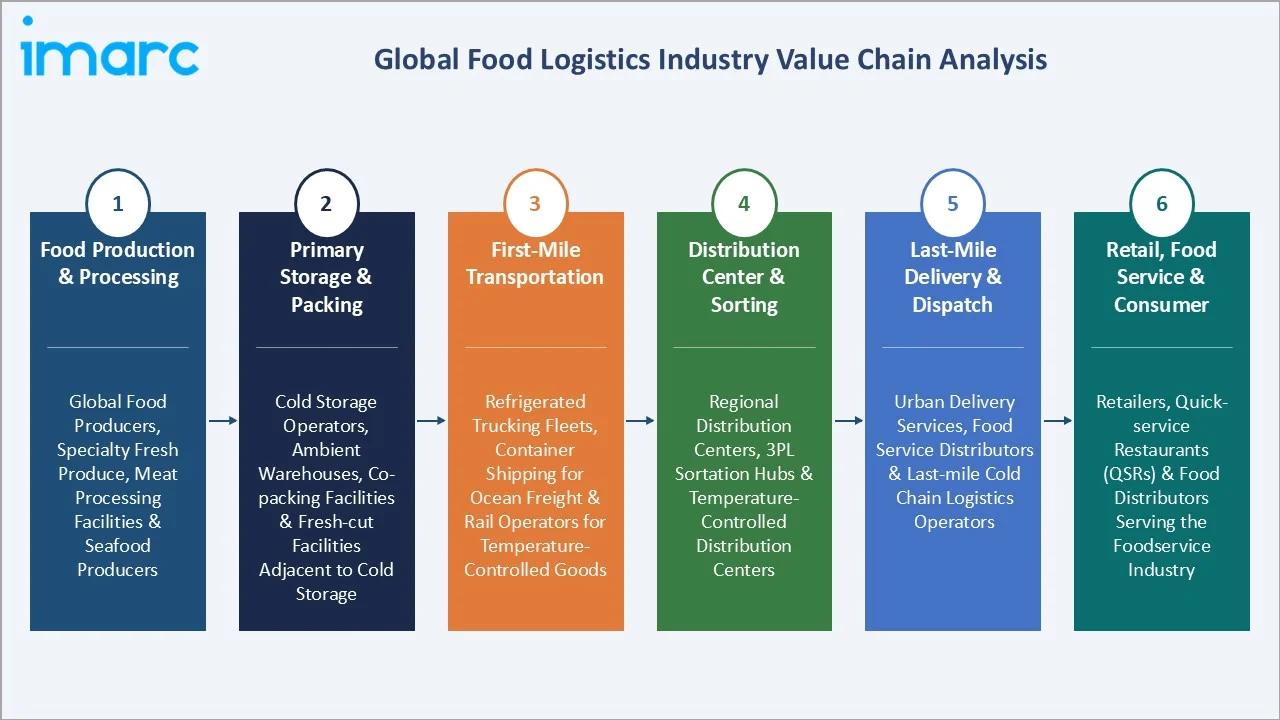

The food logistics value chain spans agricultural production through primary processing, storage, multi-modal transportation, distribution center operations, and last-mile delivery to retail, food service, and direct consumer channels, serving global consumers. 3PL providers and cold chain specialists capture 20-35% gross margins on temperature-controlled services; commodity ambient road transport earns 8-15%; specialized air perishables freight earns 25-40%. The cold chain warehousing REIT structure generates stable 60-70% gross margins on cold storage rental revenues.

|

Stage |

Key Participants |

|

Food Production & Processing |

Global food producers, specialty fresh produce, meat processing, and seafood producers. |

|

Primary Storage & Packing |

Cold storage operators, ambient warehouses, co-packing facilities, and fresh-cut facilities adjacent to cold storage. |

|

First-Mile Transportation |

Refrigerated trucking fleets, container shipping for ocean freight, and rail operators for temperature-controlled goods. |

|

Distribution Center & Sorting |

Regional distribution centers, third-party logistics (3PL) sortation hubs, and temperature-controlled distribution centers. |

|

Last-Mile Delivery & Dispatch |

Urban delivery services, food service distributors, and last-mile cold chain logistics operators. |

|

Retail, Food Service & Consumer |

Retailers, quick-service restaurants (QSRs), and food distributors serving the foodservice industry. |

The last-mile food delivery tier is the value chain's fastest-growing and most economically challenging segment. The last-mile cold chain's fundamental economic improvement through automation, subscription model revenue, and order aggregation is a critical commercial development that will determine e-grocery's long-term profitability and food logistics growth.

Technology Landscape in the Food Logistics Industry

IoT Temperature Monitoring and Cold Chain Visibility Platforms

Real-time temperature monitoring across food supply chains has transformed from periodic manual recording (food safety inspectors checking warehouse logs) to continuous IoT sensor networks transmitting telemetry every 5-15 minutes. These platforms generate compliance records automatically, meeting regulatory requirements and enabling food manufacturers to remotely manage temperature excursion responses across simultaneous shipments without manual monitoring.

Warehouse Management Systems for Temperature-Controlled Food Logistics

Warehouse Management Systems (WMS) for temperature‑controlled food logistics optimize cold chain operations through real‑time inventory visibility, automated task management, and precise environmental control. These systems enhance accuracy in handling perishable goods, reduce waste and operational costs, and improve compliance with food safety and traceability standards across the supply chain.

Reefer Container Technology and Ocean Cold Chain Innovation

Reefer container technology and ocean cold chain innovations enable real‑time monitoring, advanced temperature control, and enhanced connectivity across long‑distance marine transport. These advancements improve cargo visibility, reduce spoilage risks, and support more reliable, efficient handling of perishable goods throughout international supply chains. In June 2024, ORBCOMM introduced its next-generation reefer container monitoring solution, the CT 3600 device, marking the beginning of a new era in intelligent reefer management for shipping lines, container leasing companies, and others.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Transportation Mode |

Roadways |

52.8% |

2025 |

|

Product Type |

Fish, Shellfish, and Meat |

🔒 |

2025 |

|

Service Type |

Cold Chain |

61.2% |

2025 |

|

Segment |

Transportation |

🔒 |

2025 |

|

Region |

North America |

43.2% |

2025 |

By Transportation Mode

Roadways lead at 52.8% market share (2025). Road transport dominates because domestic food distribution is inherently local and regional, served by refrigerated trucking fleets that provide door-to-door temperature-controlled delivery capability. Road transport grows at ~6.1% CAGR (2026-2034) as e-grocery last-mile delivery volume grows and refrigerated vehicle fleets expand to serve additional food delivery addresses.

To access detailed market analysis, Request Sample

Seaways at 21.4% serve the global food trade through reefer containers, transporting frozen meat, fresh produce, dairy, and seafood across ocean trade lanes. Railways at 16.3% serve bulk grain, refrigerated meat, and fresh produce. Airways at 9.5% grow fastest at ~7.5% CAGR serving ultra-premium time-sensitive perishables, where air freight cost premium is commercially justified by fresh product value.

By Service Type

Cold chain leads at 61.2% market share (2025). The cold chain encompasses refrigerated warehousing (0-4°C for fresh/chilled food, -18°C to -25°C for frozen food), temperature-controlled transport across all modes, cold chain monitoring and compliance documentation, and temperature excursion management. Cold chain grows at ~7.2% CAGR (2026-2034), faster than the overall market, driven by three converging forces: consumer preference shift toward fresh and frozen food categories requiring continuous temperature control; food safety regulation expansion requiring verified cold chain records; and emerging market cold chain infrastructure investments.

Non-cold chain at 38.8% serves ambient temperature food logistics, such as dry grocery distribution (canned goods, packaged foods, beverages, confectionery), grain and agricultural commodity transport, and shelf-stable processed food international trade. Non-cold chain grows at ~5.2% CAGR as fresh food's share of total global food consumption gradually increases at ambient food's expense.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

North America |

43.2% |

Largest food logistics market driven by strong retail and food service sectors, extensive warehouse networks, and efficient domestic distribution systems. |

|

Europe |

24.8% |

Growth driven by stringent food safety regulations, consolidation of food retail, and well-established cold chain infrastructure. |

|

Asia Pacific |

19.5% |

Rapidly growing region with increasing demand for efficient food logistics driven by infrastructure development and expanding cold chain networks. |

|

Latin America |

7.3% |

Brazil leads the region, supported by expanding refrigerated logistics and growing food export operations. |

|

Middle East & Africa |

5.2% |

Growth driven by strategic food logistics hubs and large-scale cold storage facilities supporting food imports. |

North America's 43.2% dominance reflects the United States' exceptional food logistics infrastructure density, the world's most developed combination of refrigerated warehousing, temperature-controlled trucking, and sophisticated supply chain technology serving the US food retail and food service market.

Europe's 24.8% reflects the EU's unified single market, enabling cross-border food logistics efficiency and the UK, Germany, France, and the Netherlands' highly developed retail food supply chains. Asia Pacific's 19.5% is the fastest-growing region, as China's cold chain capacity tripled and India's cold chain infrastructure investment accelerates under government agricultural modernization programs. Latin America's 7.3% is driven by Brazil's massive agricultural export logistics and Mexico's produce cold chain to the US.

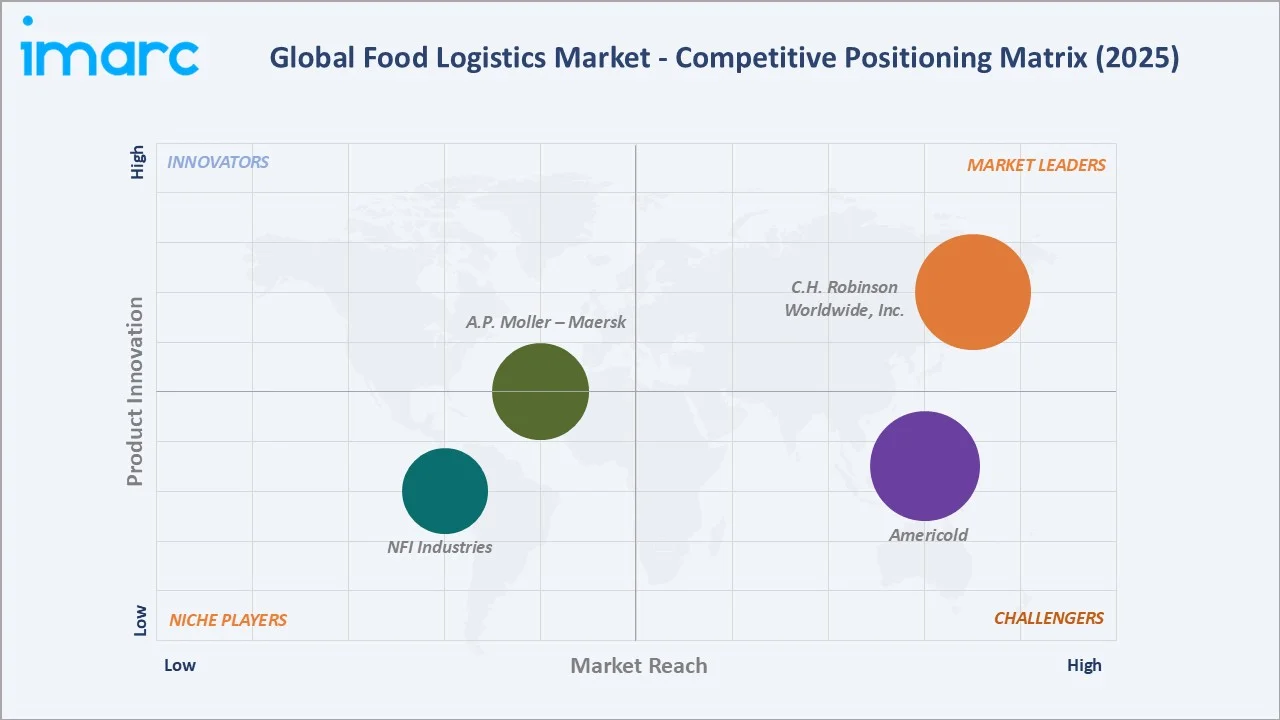

Competitive Landscape

The global food logistics market is moderately concentrated at the regional level and highly fragmented globally. North America's top 5 food logistics providers collectively serve 15-20% of the US food logistics market, while thousands of regional refrigerated trucking companies, independent cold storage operators, and regional food distributors serve the remaining market. The cold chain warehousing REIT segment is more concentrated.

|

Company Name |

Services |

Market Position |

Core Strength |

|

C.H. Robinson Worldwide, Inc. |

Essential freight services, Item-level Solutions, Consolidation and warehousing |

Market Leader |

Combining the power of artificial intelligence, the world’s top logisticians, and the principle of Lean Methodology delivers more immediate and long-term results. |

|

Americold |

Cold Storage and Transportation Management Services |

Strong Challenger |

Americold powers the global cold chain with strategically located facilities, tailored solutions, and deep expertise, delivering safer, faster, and more efficient movement of food worldwide. |

|

A.P. Moller - Maersk |

Cold Chain Logistics, Cold Storage, Captain Peter, Refrigerated Cargo |

Established Player |

With more than a century of experience in transporting refrigerated cargo globally, Maersk has gained in-depth knowledge of each commodity, allowing it to continually improve how these goods are handled. |

|

NFI Industries |

Freight Brokerage, Transportation Management, Intermodal |

Niche Player |

NFI Industries' accuracy-driven approach optimizes distribution, tackles seasonal challenges, and ensures compliance, allowing you to focus on production. |

The competitive landscape is being shaped by two opposing forces: consolidation among major players through M&A and competing with fragmentation from the emergence of e-grocery platforms, creating entirely new food logistics demand. Technology is the primary differentiator; logistics providers with proprietary TMS, IoT monitoring, and traceability platforms are commanding premium pricing from food manufacturers requiring FSMA compliance documentation and real-time supply chain visibility.

Key Company Profiles

C.H. Robinson Worldwide Inc.

C.H. Robinson is the global leader in Lean AI supply chains. Trusted by 80,000+ customers and 450,000 carriers, the company manage an unmatched 37 million shipments annually, representing $23 billion in freight.

- Service Portfolio: Essential freight services, Item-level Solutions, Consolidation and warehousing.

- Recent Developments: In August 2025, C.H. Robinson introduced its Always-on Logistics Planner, a premium service experience powered by AI agents and designed to deliver continuous execution quality across the shipment lifecycle.

- Strategic Focus: Providing integrated, temperature‑controlled supply chain solutions that enhance visibility, reliability, and efficiency for perishable goods transport.

Americold

Americold plays a crucial role in the global cold chain, offering cold storage facilities at every stage from production to consumption. The company assist customers in managing complex supply chain requirements by strategically placing their facilities near key manufacturing hubs, major ports, and population centers, ensuring timely product delivery.

- Service Portfolio: Cold Storage and Transportation Management Services.

- Recent Developments: In August 2025, Americold opened its new $100+ million Import-Export Hub in Kansas City, Missouri. The facility features on-site USDA inspections to avoid border delays, a load capacity of over 50,000 pounds per container to reduce highway congestion, and a 300-mile service radius to enhance regional food distribution.

- Strategic Focus: Expanding and optimizing temperature‑controlled infrastructure to support seamless end‑to‑end cold chain operations and enhance regional food distribution.

Market Concentration Analysis

The global food logistics market is moderately concentrated at the regional level and highly fragmented globally. North America's top 5 food logistics providers collectively represent 15-20% of the USD 130.0 Billion total market, while thousands of regional operators serve the remaining 80%. The cold chain warehousing sub-segment is meaningfully more concentrated, creating a duopoly in US large-format temperature-controlled warehousing.

Ocean reefer container shipping is highly concentrated. Road food freight remains highly fragmented, with no single carrier holding more than 2-3% of North American refrigerated trucking capacity, providing food manufacturers with meaningful competition and carrier optionality in domestic food distribution. Consolidation is structurally intensifying in cold storage warehousing through REIT acquisition strategies, in food freight brokerage through technology platform consolidation.

Investment & Growth Opportunities

Fastest Growing Segments

Airways (~7.5% CAGR), cold chain (~7.2% CAGR), e-grocery last-mile cold chain (~15%+ CAGR from current base), automated cold storage (~15-20% CAGR), and food traceability technology platforms (~12% CAGR) represent the global food logistics market's highest-growth investment vectors through 2034. Automated cold storage represents the highest-ROI capital investment in food logistics, with payback periods of 7-12 years on new automated cold storage developments.

Emerging Market Opportunities

Asia Pacific's cold chain deficit creates the single largest addressable cold chain investment opportunity globally. India's government cold chain subsidies, China's domestic cold chain market, and Vietnam/Indonesia's modern trade expansion are collectively creating an opportunity in cold chain investment opportunities through 2034.

Investment Themes

- Cold chain REIT and infrastructure development: Cold storage development in underserved markets offers development yields of 8-12% on cost versus 4-5% cap rates in mature North American markets, creating superior risk-adjusted returns for cold chain development capital.

- Food traceability technology platforms: Food logistics providers integrating proprietary traceability as a value-added service are commanding premium pricing, creating sustainable revenue streams beyond commodity freight and storage margins.

Future Market Outlook (2026-2034)

The global food logistics market is projected to grow from USD 130.0 Billion in 2025 to USD 227.0 Billion by 2034, delivering a 6.39% CAGR over the forecast period. The market's anchor value of USD 177.2 Billion in 2030 reflects a food logistics industry undergoing its most significant transformation since the introduction of refrigerated transport, driven by the simultaneous forces of e-grocery reshaping food distribution channels, automation revolutionizing cold storage economics, and regulatory traceability requirements standardizing digital supply chain visibility across the global food system.

Three structural forces define the food logistics market's growth trajectory with high certainty through 2034: the irreversible shift toward fresh, perishable, and frozen food categories that require continuous cold chain from production to consumer delivery, making cold chain logistics mandatory rather than optional for an expanding share of global food commerce; regulatory mandates for end-to-end food traceability creating permanent technology investment in digital food supply chain platforms that generate recurring service revenue for logistics providers; and e-grocery's growing penetration creating new last-mile cold chain infrastructure requirements at scale.

Research Methodology

Primary Research

Primary research comprised structured interviews with 70+ industry stakeholders (2025), including VP Supply Chain executives from Walmart, Kroger, and Sysco; cold storage operations directors from Lineage Logistics, Americold, and Burris Logistics; food logistics technology specialists; regulatory affairs specialists at FDA FSMA implementation offices; refrigerated trucking fleet managers; and international perishable freight specialists.

Secondary Research

Secondary research encompassed USDA AMS Agricultural Marketing Service cold storage data, FDA FSMA Food Traceability Rule implementation guidance (2023-2025), Global Cold Chain Alliance (GCCA) industry statistics 2025, FAO Global Food Losses and Food Waste report, WTO global food trade statistics 2024, American Trucking Associations driver shortage report 2024, company investor presentations and annual reports, and specialized food logistics trade publications (Food Logistics Magazine, Supply Chain Dive). Over 110 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up transportation mode x service type models calibrated against GCCA cold storage capacity data, US DOT refrigerated freight statistics, WTO food trade volume projections, and e-grocery delivery volume forecasts from Nielsen and FMI. Key inputs include USDA cold storage utilization trends, FDA FSMA compliance investment forecasts, Walmart/Amazon e-grocery delivery volume projections, global food trade growth by commodity category (fresh produce, seafood, dairy, meat), and cold chain automation capital expenditure trends from GCCA member surveys.

Food Logistics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Transportation Modes Covered | Railways, Roadways, Seaways, Airways |

| Product Types Covered | Fish, Shellfish, and Meat, Vegetables, Fruits, and Nuts, Cereals, Bakery and Dairy Products, Coffee, Tea, and Vegetable Oil, Others |

| Service Types Covered | Cold Chain, Non-Cold Chain |

| Segments Covered | Transportation, Packaging, Instrumentation |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | C.H. Robinson Worldwide, Inc., Americold, A.P. Moller - Maersk, NFI Industries, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the food logistics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global food logistics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the food logistics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Food Logistics Market Report

The global food logistics market reached USD 130.0 Billion in 2025, driven by global food trade, e-grocery penetration in North America, cold chain expansion in the Asia Pacific and Latin America, and FSMA food safety traceability compliance investment.

The market grows at 6.39% CAGR during 2026-2034, reaching USD 227.0 Billion by 2034, driven by e-grocery last-mile cold chain expansion, automated cold storage adoption, FSMA traceability mandates, and emerging market cold chain infrastructure development.

Roadways lead at 52.8%, reflecting food distribution's local and regional character served by refrigerated trucking fleets.

Cold chain dominates at 61.2% and grows fastest at ~7.2% CAGR, driven by consumer preference for fresh and frozen food, food safety regulation expansion requiring verified cold chain records, and emerging market cold chain infrastructure investment reducing post-harvest food losses.

North America leads at 43.2%, anchored by the US's food retail and food service industry, Walmart and Amazon's massive food distribution infrastructure, FSMA compliance requirements, and e-grocery penetration of total US grocery sales.

Leading companies include C.H. Robinson Worldwide, Inc., Americold, A.P. Moller – Maersk, and NFI Industries, among others.

The market is projected to reach approximately USD 177.2 Billion by 2030, driven by FSMA Food Traceability Rule implementation, new purchases of electric refrigerated trucks, cold chain automated warehouses expansion, and e-grocery growth in total food retail.

The FDA's FSMA Food Traceability Rule mandates electronic traceability records for high-risk foods across the supply chain, requiring food logistics providers to implement IoT temperature sensors, blockchain records, and cloud platforms.

Cold chain grows at ~7.2% CAGR versus non-cold chain's ~5.2% as fresh and frozen food categories outpace ambient shelf-stable categories, food safety regulations mandate verified temperature records, and emerging market cold chain deficits in infrastructure investment through 2034.

E-grocery in US grocery sales creates new last-mile cold chain infrastructure requirements, driving an opportunity in cold chain logistics investment while creating unit economics pressure that is accelerating automation and subscription models.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)