Food Safety Testing Market Size, Share, Trends and Forecast by Type, Food Tested, Technology, and Region, 2026-2034

Global Food Safety Testing Market Size, Share, Trends & Forecast (2026-2034)

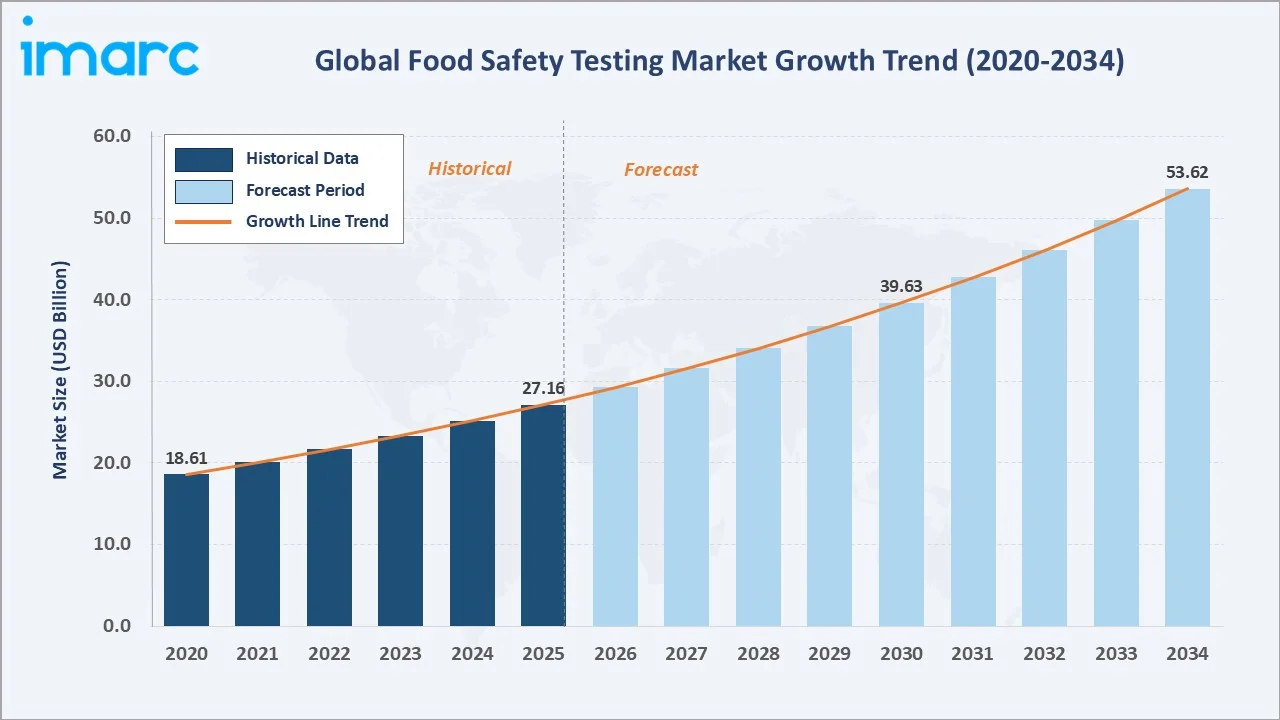

The global food safety testing market was valued at USD 27.16 Billion in 2025 and is projected to reach USD 53.62 Billion by 2034, expanding at a CAGR of 7.85% during the forecast period (2026-2034). Growth is driven by increasingly stringent food safety regulations worldwide, rising incidence of foodborne disease outbreaks with 600 million cases and 420,000 deaths annually, globalization of food supply chains, and rapid technological advances in pathogen detection and contaminant analysis. Pathogen testing dominates at 44.0% market share, while processed food leads in food tested at 36.1%. North America commands the largest regional share at 40.3%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 27.16 Billion |

|

Forecast Market Size (2034) |

USD 53.62 Billion |

|

CAGR (2026-2034) |

7.85% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (40.3%, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~9.2%, 2026-2034) |

The global food safety testing market growth expanded from USD 18.61 Billion in 2020 to USD 27.16 Billion in 2025. Anchored at USD 39.63 Billion in 2030, the forecast to USD 53.62 Billion by 2034, reflecting compounding regulatory compliance mandates and the global expansion of food trade requiring cross-border testing certification.

To get more information on this market, Request Sample

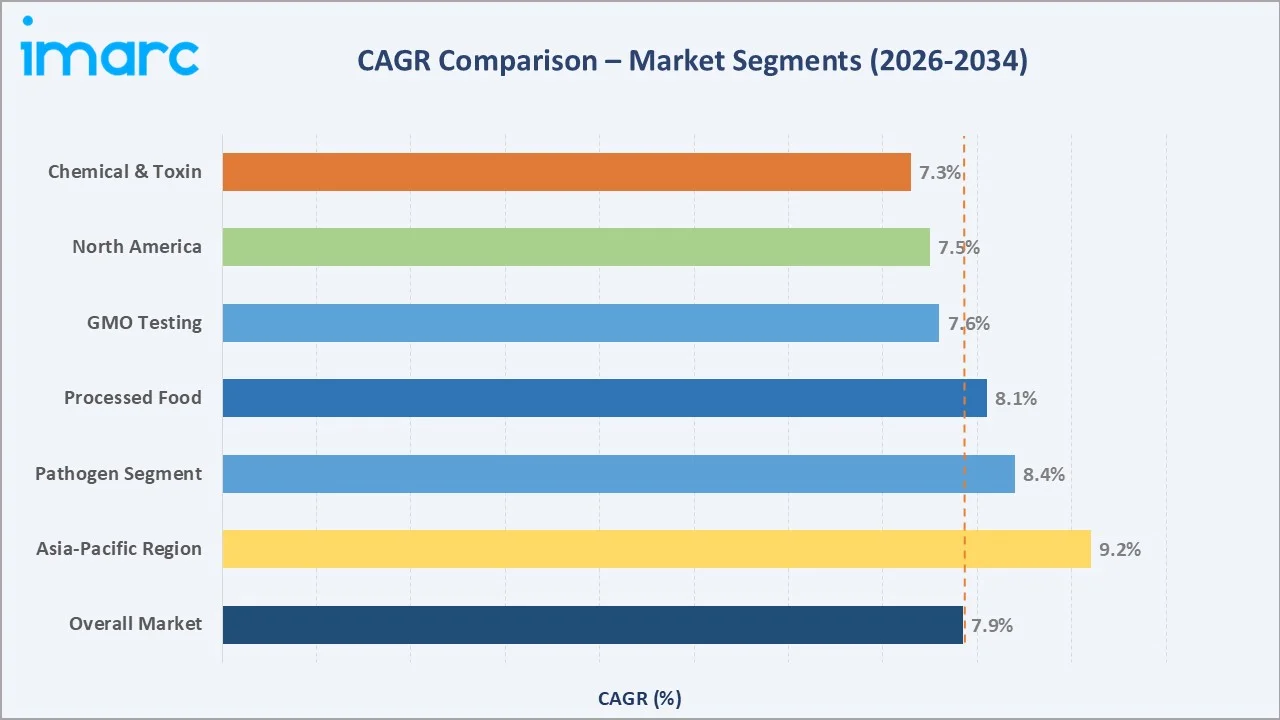

The CAGR across key segments with Asia-Pacific leads at ~9.2% CAGR, reflecting rapid regulatory harmonization, expanding food processing industries, and growing public health investment across China, India, and Southeast Asia. Pathogen testing at ~8.4% CAGR outpaces the overall market at 7.85%, driven by the rising incidence of Salmonella, Listeria, and E. coli contamination requiring real-time detection solutions.

Executive Summary

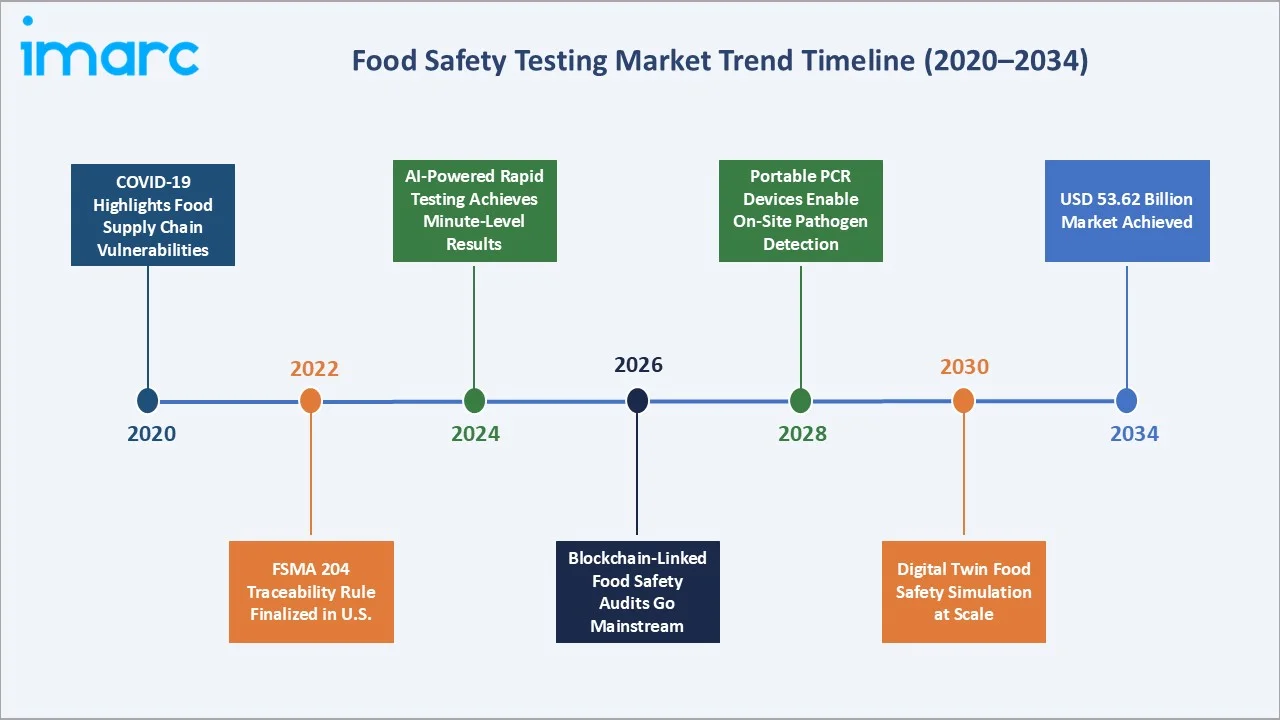

The global food safety testing market demonstrated robust growth from USD 18.61 Billion in 2020 to USD 27.16 Billion in 2025, driven by the COVID-19 pandemic’s acute spotlight on food supply chain vulnerabilities, landmark U.S. FSMA enforcement, EU Farm to Fork Strategy implementation, and the rapid proliferation of PCR-based rapid testing technologies that dramatically reduced time-to-result from 48–72 hours to under 30 minutes.

The forecast trajectory to USD 53.62 Billion by 2034 reflects five compounding structural drivers: expanding regulatory mandates across all geographies; the globalization of food trade requiring multi-country compliance testing; rising consumer demand for clean-label and allergen transparency; climate change increasing mycotoxin contamination incidents; and technological innovation in portable and AI-assisted testing platforms enabling the decentralisation of food safety testing from centralised labs to production-line environments.

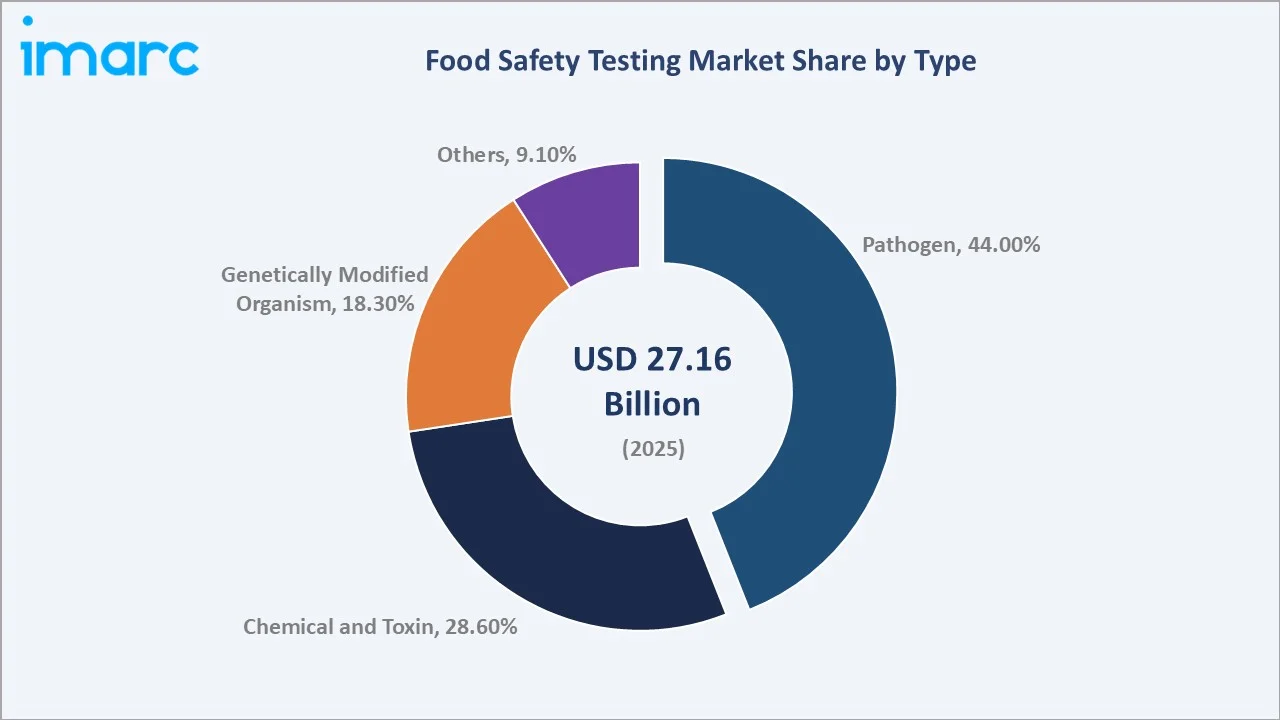

Pathogen testing at 44.0% (2025) is the dominant type, anchored by mandatory Salmonella, Listeria, and E. coli testing across meat, dairy, and ready-to-eat food categories in North America and Europe. Chemical and toxin testing at 28.6% covers pesticide residues, heavy metals, veterinary drug residues, and mycotoxins, a segment growing rapidly as EFSA and Codex Alimentarius progressively tighten Maximum Residue Level (MRL) thresholds across chemical-food category combinations. GMO testing at 18.3% is the fastest-growing type at ~7.6% CAGR, propelled by Asia Pacific’s stringent mandatory GMO labeling laws and the EU’s comprehensive GMO authorization framework.

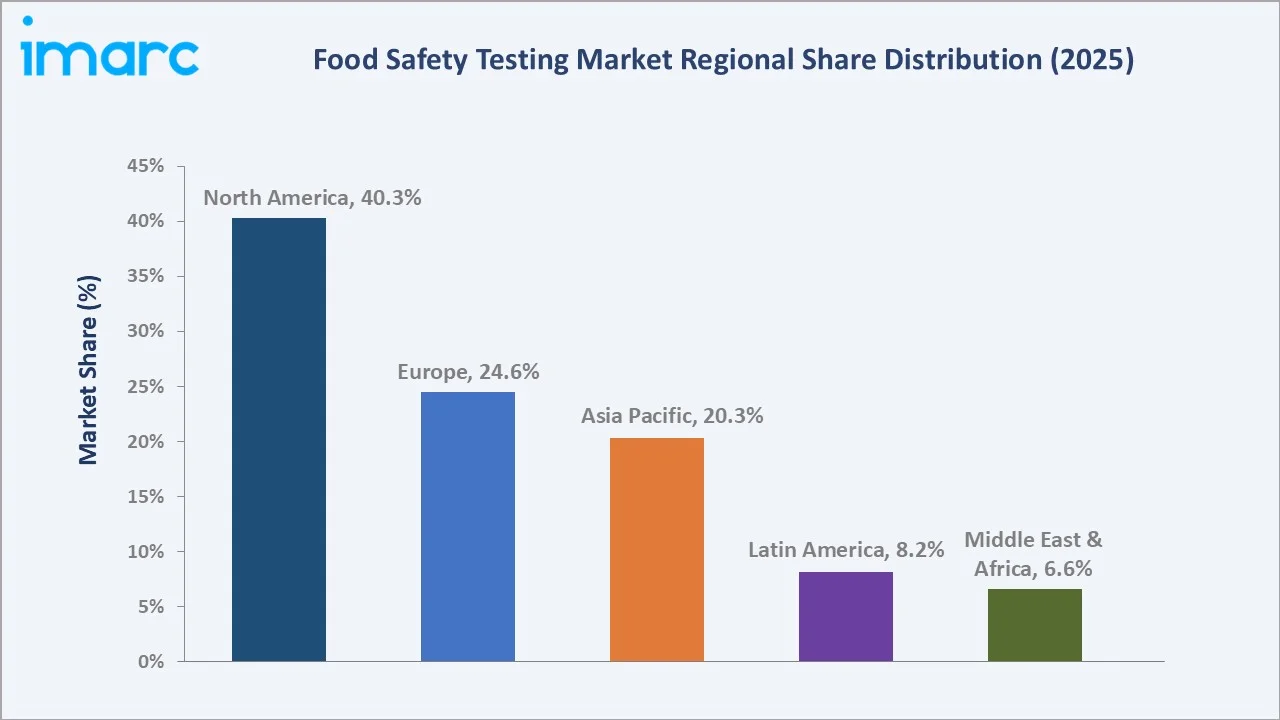

North America’s 40.3% market leadership reflects the U.S. FDA’s FSMA, the most comprehensive food safety reform in U.S. history, which mandates science-based preventive controls for registered food facilities, creating non-discretionary testing demand from FSMA-driven compliance alone. Asia Pacific at 20.3% is the fastest-growing region at ~9.2% CAGR, driven by the Chinese government investment of more than 100 billion yuan ($15 billion) over the next five years to improve farmland and food security and India’s FSSAI’s progressive enforcement escalation across food categories.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Pathogen Testing – 44.0% revenue share (2025) |

|

Dominant Food Tested |

Processed Food – 36.1% revenue share (2025) |

|

Leading Region |

North America – 40.3% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~9.2%, 2026-2034) |

Key Analytical Observations Supporting The Above Data:

- Pathogen testing dominates at 44.0% (2025): An estimated 600 million people suffer foodborne illness globally each year, causing 420,000 deaths. This disease burden, costing developed economies in healthcare costs, productivity losses, and recall expenses, drives mandatory pathogen testing as the non-negotiable baseline of food safety compliance.

- Processed food leads at 36.1% of food tested: Global processed food industry growth, with product complexity, multi-ingredient formulations using 20–50+ raw material inputs from multiple countries, creating exponentially greater contamination risk and testing obligation versus single-ingredient commodities.

- North America leads at 40.3% (2025): In the U.S., the total food spending reached $2.58 trillion in 2024, representing the world’s highest per-capita food testing investment.

- Asia Pacific fastest growing at ~9.2% CAGR: China’s 14th Five-Year Plan, including laboratory modernization and digital traceability systems. India’s FSSAI’s Food Safety Compliance System (FoSCoS) replaced manual licensing with digital-first enforcement for food businesses, bringing millions of previously informal food operators under systematic testing obligations for the first time.

Global Food Safety Testing Market Overview

The global food safety testing market encompasses laboratory services, rapid testing technologies, and reagent and consumable products used to detect and quantify biological, chemical, and physical hazards in food and feed products across the entire farm-to-fork supply chain. The market ecosystem integrates accredited third-party testing laboratories, food manufacturers' in-house quality control labs, regulatory government testing facilities, and technology providers supplying testing instruments, reagents, and digital platforms.

Applications span mandatory regulatory compliance testing, brand assurance and quality benchmarking, export certification, allergen management verification, GMO labeling compliance, and supply chain integrity auditing. Macroeconomic influences include global food trade growth, population growth increasing food production scale, climate change elevating mycotoxin and pathogen risk, and consumer wellness trends increasing tolerance for premium food safety investments.

Market Dynamics

To evaluate market opportunities, Request Sample

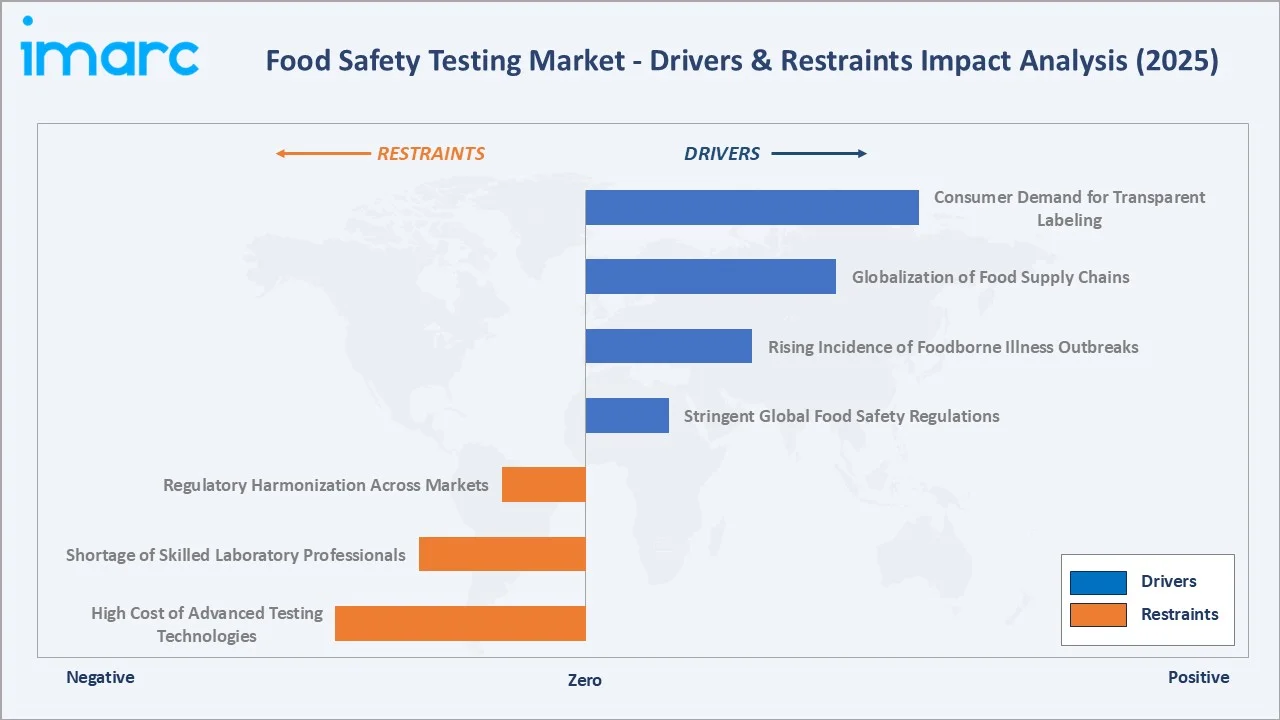

Market Drivers

- Escalating Global Food Safety Regulatory Mandates: The final rule plays a crucial role in the US FDA’s New Era of Smarter Food Safety Blueprint and enforces Section 204(d) of the FDA Food Safety Modernization Act (FSMA). The updated requirements in the rule will enable quicker identification and swift removal of potentially contaminated food from the market, leading to a reduction in foodborne illnesses and fatalities.

- Persistent Foodborne Illness Outbreaks Driving Testing Investment: In 2023, the CDC, in collaboration with state and regulatory public health partners, investigated 181 potential multistate outbreaks, 84 of which were confirmed as outbreaks. Of the 50 resolved outbreaks, 32 were linked to contaminated food, resulting in 1,219 illnesses, 421 hospitalizations, and 9 deaths. Each high-profile outbreak triggers industry-wide testing protocol reviews, increased environmental monitoring programs, and heightened regulatory scrutiny that systematically elevates baseline testing volumes across affected categories.

- Technology Innovation Enabling Higher-Frequency, Lower-Cost Testing: Next-generation rapid testing platforms are reducing the cost-per-test versus traditional culture methods while delivering results 10–20× faster. This economics improvement is enabling food companies to test more frequently at more supply chain points without proportionally increasing testing budgets, expanding total market volume even as per-test prices decline.

Market Restraints

- High Cost of Advanced Analytical Technology: State-of-the-art food safety testing instruments, LC-MS/MS (liquid chromatography–tandem mass spectrometry) systems for multi-residue pesticide analysis are costly. These capital investment barriers limit sophisticated testing capability to well-capitalized TIC companies and large food manufacturers, preventing small and medium food enterprises in emerging markets from accessing the analytical quality standards required for premium export market compliance.

- Shortage of Qualified Food Safety Laboratory Professionals: The food testing industry faces a severe talent shortage, with qualified food microbiologists and analytical chemists globally. This talent constraint limits laboratory throughput expansion capacity.

Market Opportunities

- Digital Transformation of Food Safety Testing Data Management: The convergence of laboratory information management systems (LIMS), blockchain traceability, and AI-powered risk analytics is creating a next-generation food safety digital infrastructure market.

- Allergen Testing Demand from Clean-Label Movement: The global free-from food market, gluten-free, dairy-free, nut-free, and soy-free products, is creating systematic allergen testing demand from food manufacturers making free-from claims. FALCPA (U.S. Food Allergen Labeling and Consumer Protection Act) mandates the top 9 allergens be declared, with Food Allergy Research & Education estimating 33 million Americans with food allergies who depend on accurate allergen labeling.

Market Challenges

- Matrix Complexity and False Positive Rates in Processed Foods: The chemical complexity of processed food matrices creates significant interference with immunoassay and PCR-based rapid testing methods, generating false positive rates that require time-consuming confirmatory testing by expensive reference methods.

- Emerging Contaminants Outpacing Established Testing Protocols: Novel food safety hazards, PFAS (per- and polyfluoroalkyl substances) in food packaging migration, microplastics in seafood and salt products, and antibiotic-resistant bacteria in animal products, are creating regulatory and testing methodology development challenges that established food safety testing infrastructure is not yet fully equipped to address.

Emerging Market Trends

1. FSMA 204 Food Traceability Rule Creating Next-Generation Testing Demand

The U.S. FDA’s Food Traceability Rule (FSMA 204 regulation), which introduced stricter requirements for tracking high-risk foods, effective from January 2026, is driving systematic integration of food safety testing data into digital supply chain platforms.

2. Rapid On-Site Testing Devices Decentralizing the Laboratory

Handheld PCR devices, smartphone-connected lateral flow readers, and portable mass spectrometers are enabling food safety testing at processing lines, border inspection points, and farm gates without laboratory infrastructure.

3. Whole Genome Sequencing Replacing Culture-Based Pathogen Typing

Whole genome sequencing (WGS) of food pathogens, providing strain-level identification that can link a food product to a specific patient illness cluster, is transitioning from public health research to routine commercial food safety testing. The genomic data from GenomeTrakr have been used in over 500 FDA investigations and several investigations by the CDC and USDA-FSIS.

5. Blockchain and Digital Food Safety Certificates Replacing Paper Certificates

Traditional paper-based food safety certificates, susceptible to fraud, difficult to verify, and slow to transmit across international supply chains, are being replaced by blockchain-anchored digital certificates from companies.

Industry Value Chain Analysis

The food safety testing value chain connects upstream reagent and equipment manufacturers through accredited laboratory service providers, regulatory certification systems, and ultimately to the food producers, processors, retailers, and consumers who depend on verified food safety assurance.

|

Stage |

Key Participants |

|

Reference Standards & Reagents |

Certified reference materials, culture media, immunoassay kits, and PCR master mixes for food pathogen detection |

|

Testing Equipment & Technology OEMs |

PCR instruments, ELISA readers, mass spectrometers, and rapid lateral flow devices |

|

Third-Party Testing Laboratories (TIC) |

Accredited ISO 17025 testing services globally |

|

In-House Food Industry Testing |

Internal food safety labs for production line QC, raw material incoming inspection, and finished goods testing |

|

Certification & Accreditation Bodies |

ISO 17025 lab accreditation and BRC/FSSC 22000/SQF food safety scheme certification |

|

Regulatory & Compliance Bodies |

US FDA (FSMA), FSSAI (India), MHLW (Japan), setting MRL thresholds, approving test methods, and enforcing mandatory testing requirements |

|

Food Producers & Exporters (End Clients) |

Meat processors, dairy cooperatives, grain traders, processed food manufacturers, nutraceutical companies, and food service chains commissioning testing for compliance and brand assurance |

The third-party testing laboratory service tier captures the highest revenue in the food safety testing value chain, with accredited TIC companies generating market revenue. Reagent and equipment manufacturers capture 25–30% at higher margins, while government and accreditation bodies operate on cost-recovery rather than profit-maximizing models.

Technology Landscape in the Food Safety Testing Industry

PCR-Based Rapid Testing and Next-Generation Molecular Diagnostics

Polymerase chain reaction (PCR) has become the gold-standard rapid testing technology for food pathogen detection, with quantitative PCR (qPCR) delivering pathogen concentration results within 2–4 hours versus 24–72 hours for traditional culture methods. Digital PCR (ddPCR), achieving absolute copy number quantification without standard curves, is enabling ultra-sensitive GMO content measurement.

Mass Spectrometry and Chromatographic Methods

LC-MS/MS (liquid chromatography tandem mass spectrometry) is the definitive confirmatory technology for multi-residue pesticide, veterinary drug, and chemical contaminant analysis in food, achieving quantification of residues simultaneously in a single analytical run.

Next-Generation Sequencing and Metagenomics

Next-generation sequencing (NGS) platforms enable simultaneous detection of all bacterial, viral, and fungal contaminants in a food sample without culture enrichment, including pathogens, spoilage organisms, and indicator bacteria, in a single metagenomics run. Oxford Nanopore Technologies is at the forefront of transforming food safety with its advanced DNA and RNA sequencing technology.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Pathogen | 44.0% | 2025 |

| Food Tested | Processed Food | 36.1% | 2025 |

| Technology | PCR-based Assay | 48.0% | 2025 |

| Region | North America | 40.3% | 2025 |

By Type

Pathogen testing dominates at 44.0% market share (2025). This segment covers the detection and enumeration of bacterial pathogens (Salmonella, Listeria monocytogenes, E. coli O157:H7, Campylobacter), viral pathogens (Norovirus, Hepatitis A), and parasites (Toxoplasma, Cyclospora) in food products.

To access detailed market analysis, Request Sample

Chemical and toxin testing at 28.6% encompasses pesticide residue analysis, heavy metal testing, mycotoxin analysis, veterinary drug residue testing, and food additive and preservative compliance testing. GMO testing at 18.3% is the fastest-growing type at ~7.6% CAGR, driven by proliferating mandatory GMO labeling laws across the Asia Pacific and the EU’s stringent GMO authorization process that creates ongoing monitoring requirements for approved and unauthorized GMO events in imported grain, soy, corn, and canola.

By Food Tested

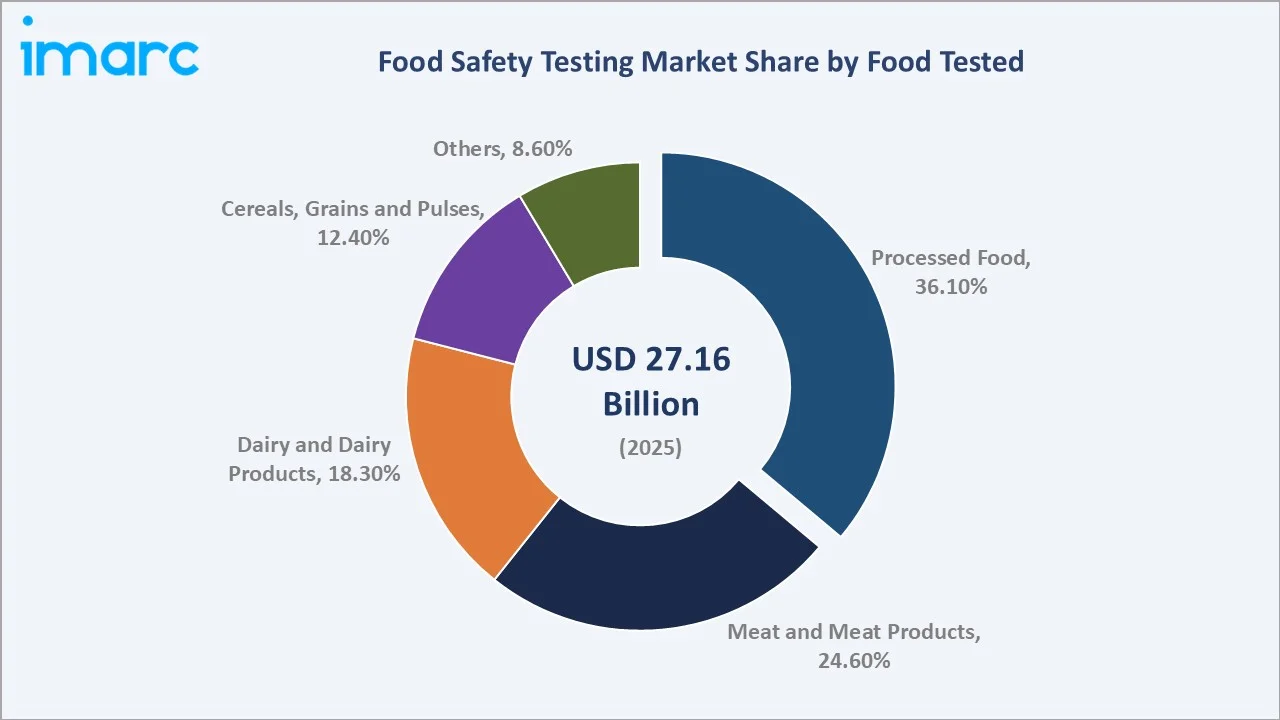

Processed food leads at 36.1% market share (2025). The processed food category’s testing dominance reflects its product complexity, multi-ingredient formulations requiring allergen verification, additive compliance, microbiological specification testing, and shelf-life validation testing across multiple regulatory jurisdictions simultaneously.

Meat and meat products at 24.6% represents the most intensively regulated food category globally, with mandatory Salmonella, Listeria, E. coli, and Campylobacter testing at slaughter, processing, and ready-to-eat production stages in the U.S., EU, and Australia. The global trade in meat and meat products reached 41.4 million tonnes in 2023, which requires extensive export certification testing that multiplies per-unit testing cost relative to domestic sales. Dairy at 18.3% covers mandatory antibiotic residue testing, aflatoxin M1 monitoring, and Listeria environmental monitoring programs.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

40.3% |

U.S. FSMA Section 204 enhanced traceability rule, high foodborne illness cost burden |

|

Europe |

24.6% |

EU General Food Law Regulation 178/2002, EFSA risk assessment authority, EU Farm to Fork Strategy targeting 50% pesticide reduction by 2030 |

|

Asia Pacific |

20.3% |

China National Food Safety Standard expansion, India FSSAI enforcement modernization, Japan MHLW positive list system for agricultural chemicals |

|

Latin America |

8.2% |

Brazil MAPA agricultural food safety expansion, Mexico Cofepris enforcement, growing export compliance requirements for meat, soy, and coffee destined for U.S. and EU markets |

|

MEA |

6.6% |

GCC Halal food safety testing expansion, Saudi Vision 2030 food security focus, UAE ESMA food import controls, Africa growing export certification demand for cocoa, coffee, and sesame |

North America’s 40.3% market dominance (2025) reflects the U.S.’s position as the world’s largest food safety testing market, driven by the world’s most comprehensive mandatory food safety framework (FSMA), the largest national food recall insurance market, and the highest per-capita food safety litigation risk environment globally. Canada’s SFCA (Safe Food for Canadians Act) has been fully implemented, further strengthening North America’s regulatory testing demand, requiring prevention-based written food safety plans from all federally licensed food businesses.

Europe’s 24.6% market share (2025) reflects the EU’s world-leading food safety regulatory architecture, with EFSA’s annual zoonoses monitoring program testing food samples across EU member states, the RASFF (Rapid Alert System for Food and Feed) issuing notifications indicating systematic contaminant detections requiring coordinated response.

Competitive Landscape

The global food safety testing market exhibits moderate concentration, with Eurofins Scientific, SGS SA, and Mérieux NutriSciences collectively accounting for approximately 35–40% of total TIC (testing, inspection, and certification) service revenue in the food testing segment.

|

Company Name |

Testing Services |

Market Position |

Core Strength |

|

Eurofins Scientific |

Allergen testing, GMO testing, Molecular Biology (protein or DNA based testing) |

Dominant Market Leader |

World’s largest food testing laboratory network, widest test menu portfolio covering pathogens, pesticides, GMO, allergens, and contaminants |

|

SGS Société Générale de Surveillance SA |

Food Contaminants, Food Allergens, Microbiology and Validation, Nutritional & Composition Analysis |

Market Leader |

Switzerland-headquartered global TIC leader, SGS Digicomply digital food intelligence platform for regulatory tracking |

|

Intertek Group plc |

Chemical & Nutritional Testing, Food Packaging Testing, Genetically Modified Organisms (GMOs) Detection, Microbiological Testing, Residues & Contaminants Testing |

Strong Challenger |

Strength in branded ingredient authentication, nutritional labeling verification, and allergen testing |

|

ALS |

Microbiology Testing, Virus Testing on Food Samples, Chemistry & Nutritional Testing, Genetically modified organisms (GMO) Testing, Allergens Testing |

Strong Challenger |

Australia-headquartered global testing group with food testing, ALS food testing specializes in environmental contaminants (dioxins, PCBs, heavy metals) in food |

|

Neogen Corporation |

Microbial Testing, Hygiene Monitoring, Food Quality Analysis, Natural Toxin Detection |

Specialist Technology Provider |

U.S. food safety specialist with rapid testing technologies, strong in meat, dairy, and grain pathogen testing |

|

Mérieux NutriSciences |

Food Additives Testing, Food Allergen Testing, EtO Testing |

Established |

American-French Mérieux group food safety laboratory network in Americas, Europe, Africa, Asia-Pacific; specialises in food additive testing, allergen testing and EtO testing |

The broader market, encompassing reagent/kit manufacturers, instrument OEMs, and in-house food industry testing, is more fragmented, with the top five companies representing approximately 25–30% of total market value, including all testing formats.

Key Company Profiles

Eurofins Scientific

Eurofins Scientific is the world’s unambiguous leader in food safety testing, operating accredited food testing laboratories across 60+ countries.

- Portfolio: Allergen testing, GMO testing, Molecular Biology (protein or DNA based testing).

- Recent Developments: In September 2025, Eurofins Food Chemistry Testing, Madison and Eurofins Assurance launched product certification designed to safeguard the quality of dietary supplements, ingredients and food.

- Strategic Focus: Organic growth through geographic expansion in underserved APAC and LATAM markets; digital transformation through Eurofins Connect laboratory data portal enabling client real-time results access; food technology-adjacent testing expansion into novel foods, alternative proteins, and cannabis food products; strategic M&A targeting specialized testing capabilities in emerging food safety analytes.

SGS Société Générale de Surveillance SA

SGS SA is a Swiss testing, inspection, and certification giant with offices and laboratories in 115 countries, with food, agriculture, and chemicals representing its second-largest segment.

- Portfolio: Food Contaminants, Food Allergens, Microbiology and Validation, Nutritional & Composition Analysis.

- Recent Developments: In December 2022, SGS launched the SGS Food Contact Product Certification Mark to help manufacturers and suppliers demonstrate the safety and performance of their products in regulated, global markets.

- Strategic Focus: Digital-physical integrated food safety services combining laboratory testing with AI-powered regulatory compliance monitoring; food supply chain sustainability verification as premium service extension; China regulatory penetration following CNAS accreditation expansion; TIC + digital platform bundled contracts for global food brand clients.

Neogen Corporation

Neogen Corporation is a U.S. food and animal safety specialist, positioning itself as the world’s leading provider of food safety rapid testing solutions.

- Portfolio: Microbial Testing, Hygiene Monitoring, Food Quality Analysis, Natural Toxin Detection.

- Recent Developments: In December 2024, Neogen Corporation launched a new addition to its Petrifilm product line, the Neogen Petrifilm Bacillus cereus Count Plate, which offers food safety professionals a simple, reliable, and efficient method for testing for Bacillus cereus, a persistent threat with potentially deadly consequences.

- Strategic Focus: In-house food manufacturer testing market as primary customer base (versus TIC company lab supplies); ANSR platform expansion to new pathogens and matrices; digital integration of testing data into NEOGEN Food Safety 360 analytics platform; grain and mycotoxin testing leadership in U.S. Corn Belt and South American soy-growing regions.

Intertek Group plc

Intertek Group is a UK-based testing, inspection, and certification company, with its Business Assurance and Products divisions covering food safety testing and food chain quality assurance services.

- Portfolio: Chemical & Nutritional Testing, Food Packaging Testing, Genetically Modified Organisms (GMOs) Detection, Microbiological Testing, Residues & Contaminants Testing.

- Recent Developments: In September 2025, Intertek Group acquired Envirolab, a high-quality environmental testing business in Australia with a strong growth and margin track record.

- Strategic Focus: Total Quality Assurance premium positioning over commodity testing; Alchemy digital training platform as recurring revenue SaaS extension; alternative protein and novel food testing as high-growth specialty; supply chain sustainability verification as ESG-driven food industry demand captures premium margins over compliance-only testing services.

Market Concentration Analysis

The global food safety testing market exhibits moderate concentration in the TIC service segment. Eurofins Scientific alone commands an estimated 15–18% of global accredited food testing laboratory revenue, while SGS and Mérieux NutriSciences each hold 8–12%. The combined top five TIC companies account for approximately 50–55% of the TIC food testing segment revenue. However, when the broader market is considered, including in-house food industry testing, reagent and instrument markets, and government laboratory testing, concentration falls to approximately 25–30% for the top five participants.

The market is highly fragmented below the top TIC tier. Thousands of national and regional food testing laboratories, including university-affiliated labs, government food safety institutes, and independent accredited laboratories, collectively provide a significant portion of food testing services, particularly in regulatory testing for government official food control programs, where local laboratory mandates prevent international TIC companies from capturing all market volume.

Investment & Growth Opportunities

Fastest Growing Segments

GMO testing (~7.6% CAGR), allergen testing (~11–13% CAGR), PFAS and emerging contaminant testing (~20–25% CAGR), and rapid on-site testing devices (~15–20% CAGR) represent the four highest-growth investment vectors in the food safety testing market through 2034.

Emerging Markets

India’s food safety testing market growth, driven by FSSAI’s enforcement capability, expands, and India’s food export industry requires international-standard accredited testing. Southeast Asia’s ASEAN food safety harmonization is creating systematic testing demand across Indonesia, Vietnam, and Thailand. Sub-Saharan Africa’s food safety laboratory network investment under AfCFTA is an infrastructure opportunity through 2030.

Investment Themes

Venture and institutional investment in food safety testing technology is accelerating, with particular focus on rapid detection platforms, food safety AI/ML analytics, and blockchain traceability integration.

- Key investment themes: CRISPR-based food pathogen diagnostics, AI-powered non-targeted contaminant screening, portable mass spectrometry for field deployment, food fraud authentication using isotope ratio analysis, and blockchain-linked digital food safety certificates.

- Corporate M&A pipeline: Eurofins, SGS and others are all active acquirers targeting specialty laboratory businesses in PFAS analysis, novel food testing, and digital food safety platforms that complement core testing service portfolios.

Future Market Outlook (2026-2034)

The global food safety testing market is positioned for transformational growth through 2034. From USD 27.16 Billion in 2025, the market is forecast to reach USD 53.62 Billion by 2034, at a 7.85% CAGR. This near-doubling of market value is structurally anchored by three irreversible megatrends: the global regulatory ratchet tightening food safety standards progressively across all geographies; technological democratisation enabling faster, cheaper, and more sensitive testing across more points in the supply chain; and consumer demand for verifiable food safety transparency that is transforming testing from a compliance cost into a brand differentiation tool.

Between 2026 and 2030, the defining transformations will be the mainstream deployment of AI-powered non-targeted contaminant screening, replacing the current model of testing only for known, pre-specified hazards with a comprehensive scan of the entire chemical space present in a food sample. The 2030–2034 period will be defined by the full decentralisation of food safety testing from centralised accredited laboratories to production-line, retail, and consumer endpoints. Portable PCR devices achieving full laboratory-grade sensitivity, smartphone-connected lateral flow readers with cloud-linked result databases, and AI-powered food fraud detection at retail checkouts using hyperspectral imaging will collectively create a distributed food safety testing infrastructure that is 100× more accessible than the current laboratory-dependent model.

Research Methodology

Primary Research

Primary research for this report included structured interviews with 160+ industry stakeholders in 2025, comprising food safety testing laboratory directors, food manufacturer quality assurance managers, regulatory officials (FDA, EFSA, FSSAI, Codex Alimentarius representatives), TIC company commercial executives, food safety testing technology developers, and international food trade compliance specialists. Geographic coverage included North America, Europe, China, India, Japan, Brazil, and the Middle East.

Secondary Research

Secondary research encompassed FDA FSMA enforcement data and import refusal records, EFSA annual zoonoses monitoring reports, RASFF notification database analysis, WHO global foodborne illness burden estimates, USDA AMS commodity testing data, national food regulatory agency annual reports across 35+ countries, company annual reports and earnings call transcripts, AOAC International method validation publications, and food industry trade publications. Over 310 secondary sources were reviewed.

Forecasting Models

Market size forecasts were developed using a bottom-up type–food tested matrix validated against top-down methodology. Key inputs include global food trade volume growth, regulatory testing frequency mandates by food category, test price deflation curves for rapid technologies, and new food safety regulatory implementation timelines across 50+ regulatory jurisdictions.

Food Safety Testing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Pathogen, Genetically Modified Organism, Chemical and Toxin, Others |

| Food Testeds Covered | Meat and Meat Products, Dairy and Dairy Products, Cereals, Grains and Pulses, Processed Food, Others |

| Technologies Covered | Agar Culturing, PCR-Based Assay, Immunoassay-Based, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Eurofins Scientific, SGS Société Générale de Surveillance SA, Intertek Group plc, ALS, Neogen Corporation, Mérieux NutriSciences, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the food safety testing market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global food safety testing market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the food safety testing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Food Safety Testing Market Report

The global food safety testing market was valued at USD 27.16 Billion in 2025and is projected to reach USD 53.62 Billion by 2034.

The food safety testing market is forecast to grow at a CAGR of 7.85% during 2026-2034, driven by regulatory mandates, foodborne illness outbreaks, globalized supply chains, and rapid testing technology adoption.

Pathogen testing dominates with 44.0% revenue share (2025), driven by mandatory Salmonella, Listeria, and E. coli testing requirements in meat, dairy, and ready-to-eat food categories globally.

Processed food leads with 36.1% market share (2025), due to multi-ingredient complexity requiring allergen, additive, pathogen, and multi-country regulatory compliance testing across each product SKU.

North America leads with 40.3% revenue share (2025), anchored by U.S. FSMA comprehensive mandatory testing requirements, the world’s highest food safety litigation risk, and annual testing spend.

Key market players include Eurofins Scientific, SGS Société Générale de Surveillance SA, Intertek Group plc, ALS, Neogen Corporation, and Mérieux NutriSciences.

Key drivers include FSMA and EU Farm to Fork regulatory mandates, 600M annual foodborne illness cases, global food trade complexity, and rapid PCR/LFIA technology reducing per-test cost.

GMO testing, allergen testing, PFAS/emerging contaminant testing, and rapid on-site testing devices lead market growth through 2034.

Asia Pacific grows fastest at ~9.2% CAGR, driven by China’s food safety investment, India FSSAI enforcement modernization, and Japan/Korea’s stringent positive list pesticide testing systems.

AI enables non-targeted contaminant screening on HRMS platforms, detecting unknown hazards in chemical signature libraries without pre-specified targets, fundamental shift from reactive to proactive surveillance.

Top opportunities include CRISPR-based rapid diagnostics, AI-powered non-targeted screening, portable mass spectrometry devices, blockchain-linked digital certificates, and India/ASEAN emerging laboratory infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)