Forage Seed Market Size, Share, Trends and Forecast by Product, Livestock, Species, and Region 2026-2034

Forage Seed Market Size, Share, Trends & Forecast (2026-2034)

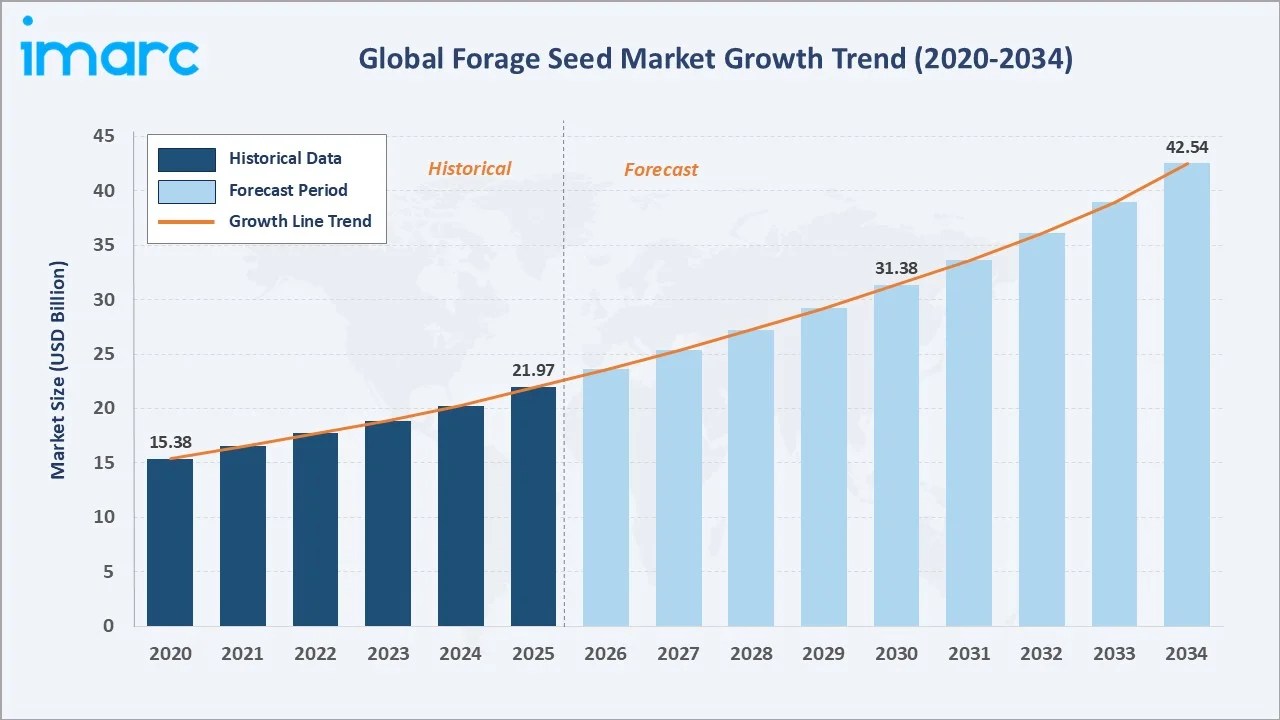

The global forage seed market size reached USD 21.97 Billion in 2025 and is projected to reach USD 42.54 Billion by 2034, exhibiting a CAGR of 7.39% during 2026-2034. The growing number of supportive policies and subsidies to promote forage seed cultivation is driving market demand, coupled with the rising adoption of precision techniques and increasing R&D investment in better quality seeds.

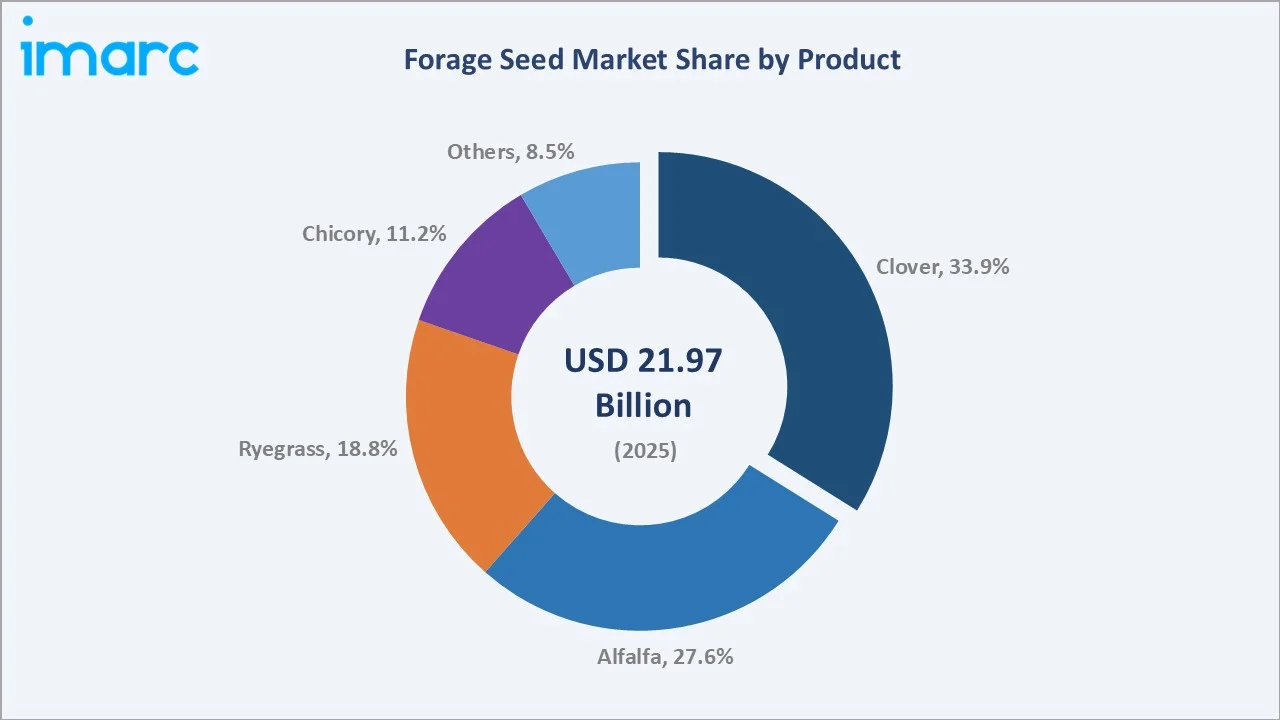

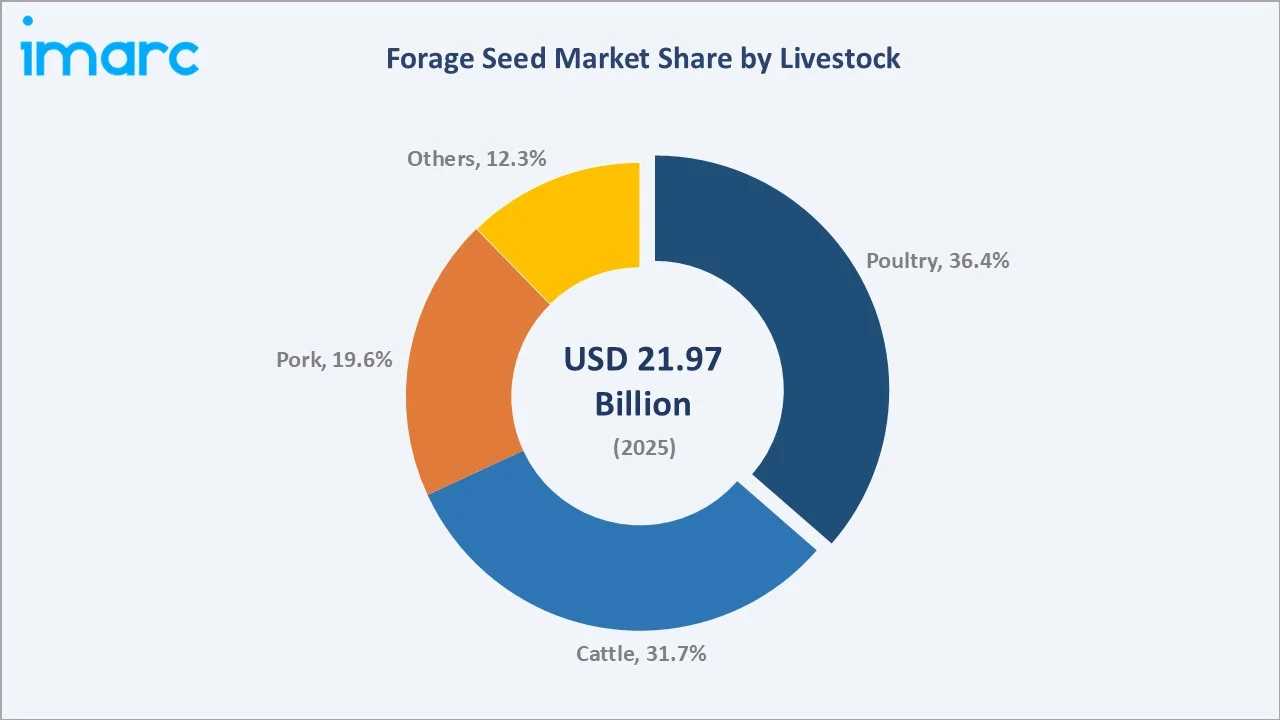

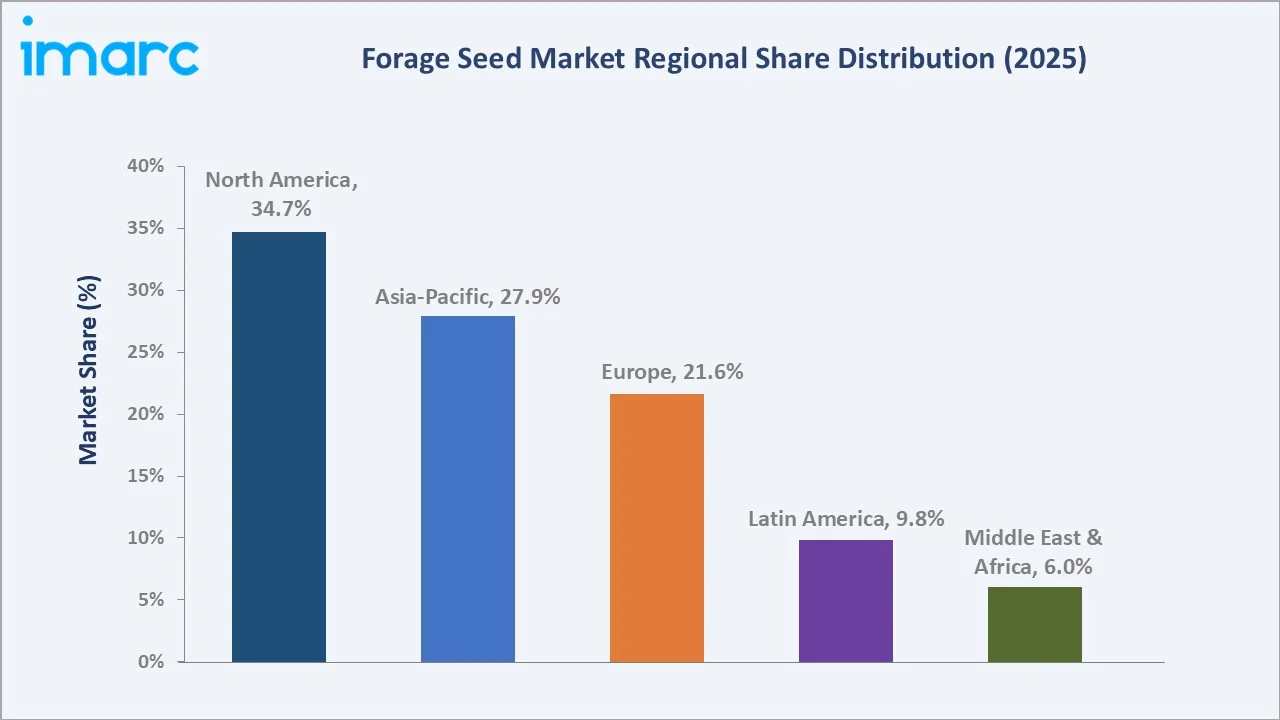

Clover leads the product segment at 33.9% in 2025, driven by its nitrogen-fixing properties and high palatability for livestock. Poultry dominates the livestock segment at 36.4%. North America commands 34.7% of the global market, underpinned by large-scale alfalfa production and strong government crop insurance programs.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 21.97 Billion |

|

Forecast Market Size (2034) |

USD 42.54 Billion |

|

CAGR (2026-2034) |

7.39% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product |

Clover (33.9% share, 2025) |

|

Dominant Livestock |

Poultry (36.4% share, 2025) |

|

Leading Region |

North America (34.7% share, 2025) |

The forage seed market growth from 2020 through 2034 reflects structural demand driven by global livestock expansion, government policy support, precision agriculture adoption, and seed biotechnology investment. The forecast to USD 42.54 Billion by 2034 captures sustained demand from North America and accelerating growth from Asia-Pacific.

To get more information on this market, Request Sample

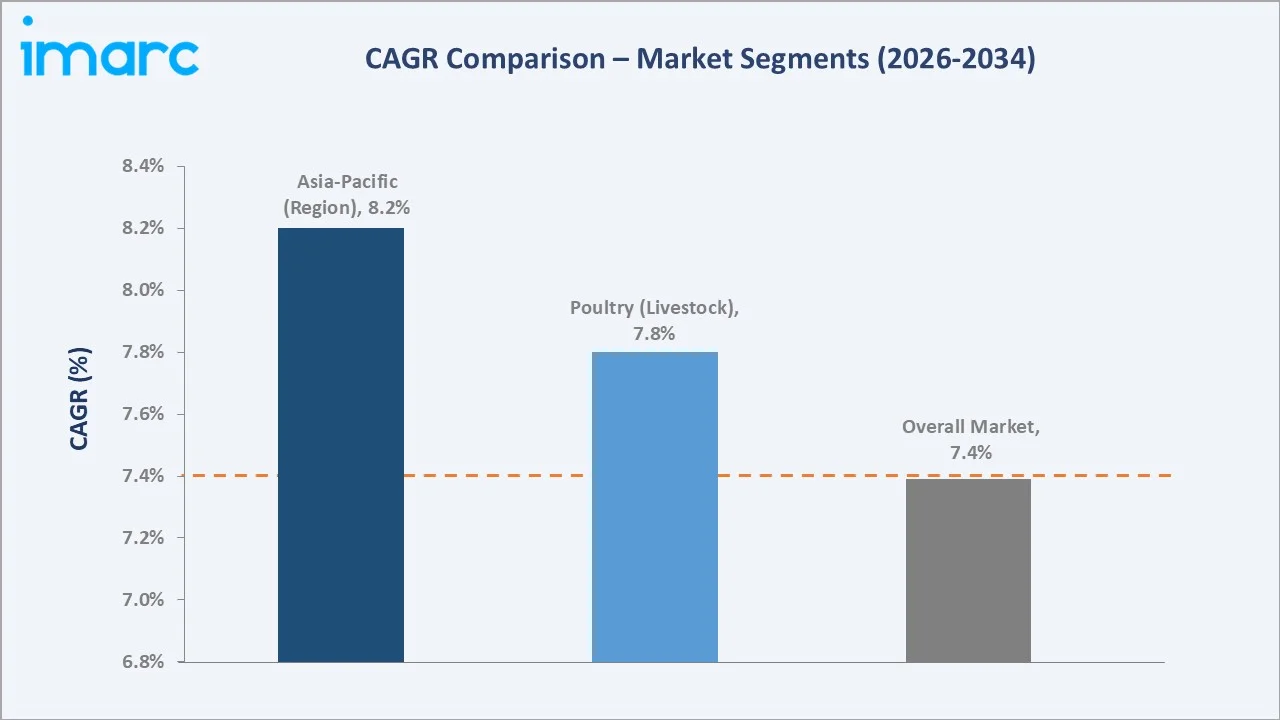

The CAGR trajectories across key product and livestock sub-segments highlight Asia-Pacific at approximately 8.2% CAGR and the Poultry livestock segment at approximately 7.8% CAGR as the fastest-growing categories within the forage seed market through 2034.

Executive Summary

The global forage seed market is on a sustained growth trajectory from USD 21.97 Billion in 2025 to USD 42.54 Billion by 2034. The market encompasses clover, alfalfa, ryegrass, chicory, and other forage seed varieties cultivated for poultry, cattle, pork, and other livestock systems across all major agricultural regions.

Clover leads at 33.9% in 2025, owing to its critical role in nitrogen fixation, soil improvement, and high-protein nutrition for ruminant and livestock. Alfalfa (27.6%) supports high-value hay production in North America and the Middle East. Ryegrass (18.8%) addresses temperate grass seed demand across Europe, Oceania, and North America.

Poultry livestock commands 36.4% share in 2025, underpinned by the global expansion of commercial broiler and layer production. Cattle at 31.7% reflects large-scale beef and dairy herd demand for consistent pasture and silage supply. North America dominates at 34.7%, while Asia-Pacific at 27.9% is the fastest-growing region.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Clover – 33.9% share (2025) |

|

Leading Livestock Segment |

Poultry – 36.4% share (2025) |

|

Leading Region |

North America – 34.7% share (2025) |

|

Second Largest Region |

Asia-Pacific – 27.9% share (2025) |

|

Top Companies |

DLF, Barenbrug, RAGT |

- Clover at 33.9% dominates because it delivers high-protein, nitrogen-fixing benefits across the widest range of temperate livestock systems, making it the most versatile and widely planted forage legume seed globally.

- Poultry at 36.4% leads because rapid global expansion of commercial poultry production requires high-quality pasture and forage-based feed formulations, with Asia and North America generating the largest procurement volumes.

- North America's 34.7% regional dominance reflects the US alfalfa hay export industry, established clover seed production clusters, and government-backed precision agriculture programs that maximize forage seed yield and farm profitability.

Forage Seed Market Overview

The global forage seed market encompasses the breeding, production, and commercial supply of all seed varieties cultivated as animal feed crops—including legumes such as alfalfa, clover, and chicory, and grasses such as ryegrass and fescue—deployed across poultry, cattle, pork, equine, and other livestock applications globally.

The ecosystem integrates seed breeders and biotechnology companies, commercial seed multiplication farms, quality certification agencies, wholesale distributors, agri-retailers, livestock farmers, and regulatory bodies overseeing seed quality standards, GM approvals, and organic certification programs.

Market Dynamics

To evaluate market opportunities, Request Sample

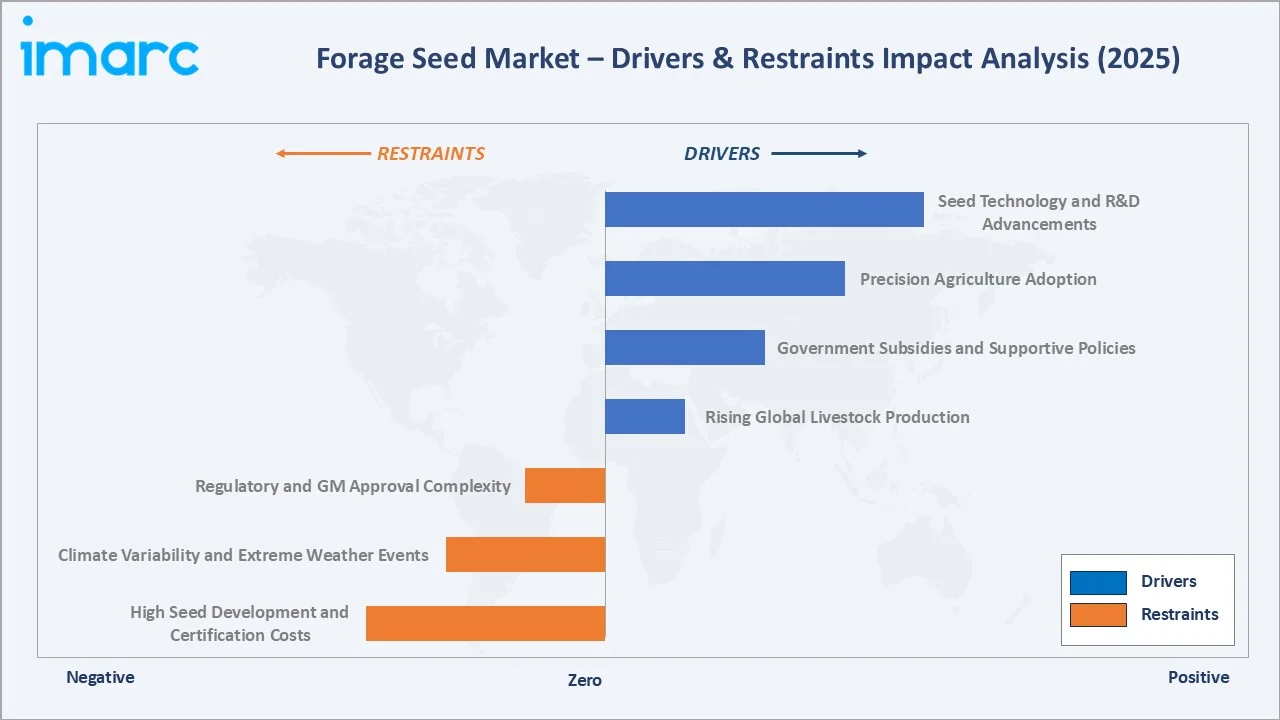

Market Drivers

- Rising Global Livestock Production: Expanding livestock inventories across Asia-Pacific and Latin America generate sustained demand for high-quality forage seed inputs. Greater herd sizes require more pastureland and improved forage varieties to optimize feed efficiency, animal health outcomes, and productivity across commercial and smallholder farming systems.

- Government Subsidies and Supportive Policies: Governments across North America, Europe, and emerging economies offer subsidies, crop insurance, and technical assistance to promote forage seed cultivation. Various countries usually expand crop insurance covering alfalfa and forage production, reducing farmer risk and accelerating adoption of certified improved forage seed varieties.

- Precision Agriculture Adoption: GPS-guided seeding, soil health mapping, and drone-based monitoring enable optimal forage seed selection and placement, improving germination rates, yields, and return on seed investment.

- Seed Technology and R&D Advancements: Biotechnology firms are developing forage varieties with drought tolerance, pest resistance, and enhanced nutritional profiles. In October 2024, Renovo Seed launched OptiHarv, a high-performance forage blend for dairy and cattle farmers, exemplifying the accelerating pace of commercial innovation driving seed replacement demand globally.

Market Restraints

- High Seed Development and Certification Costs: Developing and commercializing new forage seed varieties requires substantial R&D investment, multi-year field trials, and regulatory certification processes. These costs limit new entrant participation and slow advanced variety adoption in cost-sensitive emerging markets, particularly for smallholder farming systems across Asia and Africa.

- Climate Variability and Extreme Weather Events: Increasing frequency of droughts, floods, and temperature extremes disrupts forage crop production cycles and reduces seed supply availability. Climate-related yield losses in the US Great Plains and Australia directly affect forage seed supply chains, market pricing, and farmer procurement confidence across key producing regions.

- Regulatory Barriers to GM Seed Adoption: Stringent regulatory frameworks governing genetically modified forage seeds in the European Union and several emerging markets restrict market penetration for advanced biotech varieties. Lengthy approval timelines and public perception concerns create commercial barriers for seed companies developing next-generation GM forage products.

Market Opportunities

- Organic and Sustainable Forage Seed Demand: Rising consumer preference for organic meat and dairy products drives demand for certified organic forage seeds. Organic livestock operations require non-GM, chemical-free varieties, creating a premium segment with 20–40% price premiums above conventional equivalents and constrained supply relative to rapidly growing demand.

- Asia-Pacific Livestock Sector Expansion: Rapid livestock sector growth in China, India, and Southeast Asia creates large new forage seed demand pools. Government-led pasture improvement programs and increasing commercial farming adoption are opening significant new market opportunities for global forage seed exporters seeking international revenue growth.

Market Challenges

- Seed Supply Chain Fragmentation in Emerging Markets: Forage seed distribution networks in Africa, South Asia, and parts of Latin America remain fragmented, limiting farmer access to certified high-quality varieties. Poor rural logistics, limited seed distribution and rural logistics infrastructure, and low farmer awareness constrain market penetration and adoption of improved seed varieties.

- Competition from Low-Cost Generic Seed Substitutes: Informal seed markets and uncertified generic forage seed sources compete on price in cost-sensitive markets, eroding margins for certified seed producers. This competitive pressure limits adoption of improved, higher-yielding varieties in smallholder farming contexts across Asia, Africa, and Latin America.

Emerging Market Trends

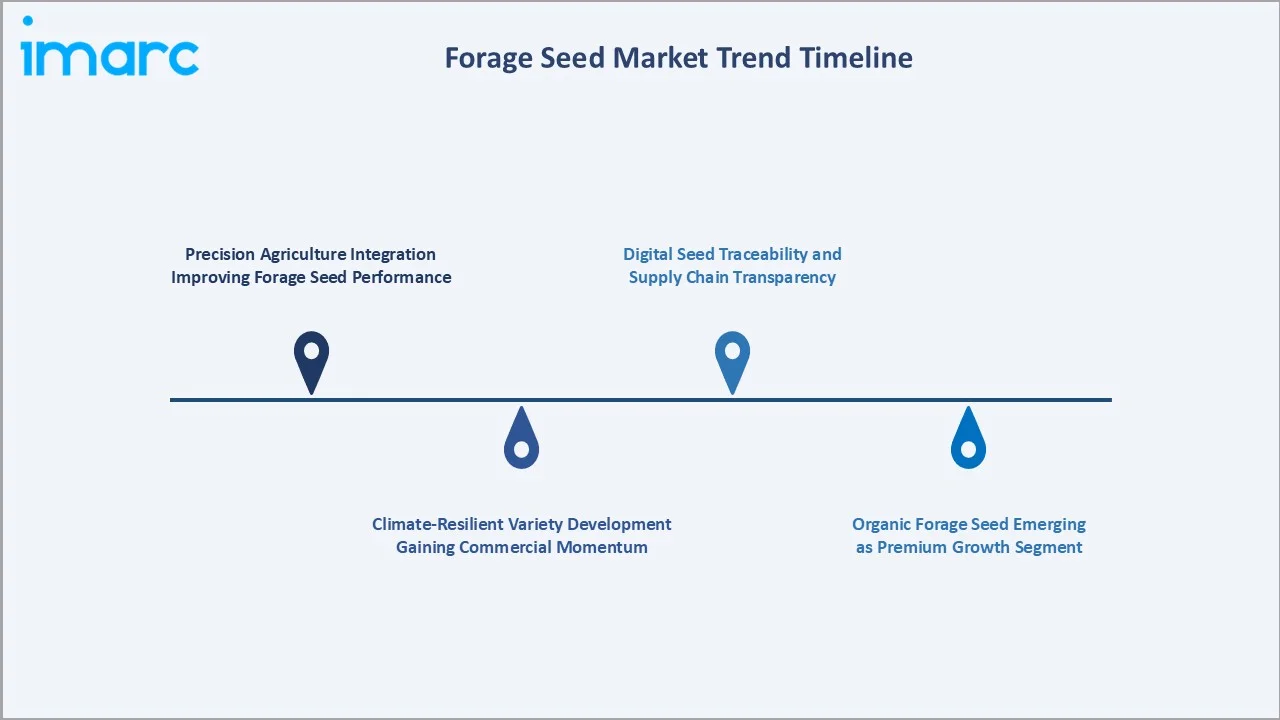

1. Precision Agriculture Integration Improving Forage Seed Performance

Precision agriculture tools enable site-specific forage seed selection and application, optimizing germination, yield, and nutritional output per hectare. GPS-guided seeding, soil health mapping, and drone monitoring are being integrated into forage farm management systems, improving return on seed investment across North America and Europe.

2. Climate-Resilient Variety Development Gaining Commercial Momentum

Seed biotechnology firms are accelerating R&D into drought-tolerant, heat-resistant, and flood-resilient forage varieties. These varieties command premium pricing and are gaining adoption across water-stressed farming regions in Australia, the Mediterranean, and sub-Saharan Africa, creating new commercial growth vectors for leading seed companies.

3. Organic Forage Seed Emerging as Premium Growth Segment

Consumer-driven demand for organic and naturally raised livestock products is creating a dedicated organic forage seed procurement market. Certified organic varieties are priced at 20–40% premiums above conventional equivalents, driving above-market revenue growth for organic-certified seed specialists and supply-chain-verified producers.

4. Digital Seed Traceability and Supply Chain Transparency

Blockchain-based seed traceability platforms are being piloted by major seed companies to provide provenance verification from breeding to farm application. This supports food safety compliance, premium product certification, and supply chain efficiency improvements across the global forage seed value chain.

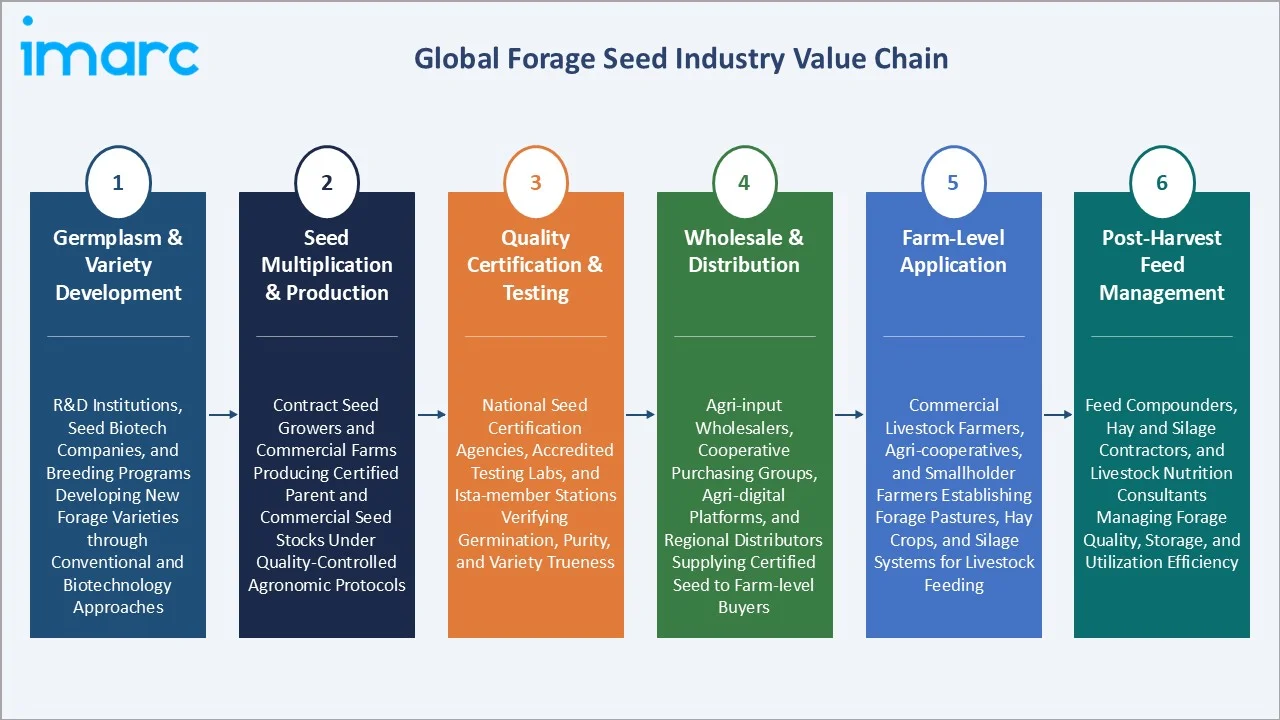

Industry Value Chain Analysis

The forage seed value chain spans six integrated stages from germplasm research through post-harvest feed management. Seed breeders and biotechnology firms capture primary value through variety development, while distributors and precision agronomy service providers generate recurring revenue supporting long-term farmer relationships.

|

Stage |

Key Activities |

|

Germplasm & Variety Development |

R&D institutions, seed biotech companies, and breeding programs developing new forage varieties through conventional and biotechnology approaches |

|

Seed Multiplication & Production |

Contract seed growers and commercial farms producing certified parent and commercial seed stocks under quality-controlled agronomic protocols |

|

Quality Certification & Testing |

National seed certification agencies, accredited testing laboratories, and ISTA-member stations verifying germination, purity, and variety trueness |

|

Wholesale & Distribution |

Agri-input wholesalers, cooperative purchasing groups, agri-digital platforms, and regional distributors supplying certified seed to farm-level buyers |

|

Farm-Level Application |

Commercial livestock farmers, agri-cooperatives, and smallholder farmers establishing forage pastures, hay crops, and silage systems for livestock feeding |

|

Post-Harvest Feed Management |

Feed compounders, hay and silage contractors, and livestock nutrition consultants managing forage quality, storage, and utilization efficiency |

Variety development and quality certification stages capture the highest value in the forage seed chain, requiring specialized breeding expertise and regulatory validation capability. Distribution and precision agronomy services represent growing recurring revenue streams improving long-term commercial relationships with farming customers.

Technology Landscape in the Forage Seed Industry

Conventional Breeding Technology

Conventional plant breeding remains the foundational technology for forage seed development, using selective crossing and phenotypic selection to improve yield, disease resistance, and nutritional quality. Modern genomic-assisted selection accelerates conventional programs by identifying superior genetic markers with greater precision.

Biotechnology and Genetic Modification

Biotechnology applications in forage seeds include transgenic herbicide tolerance, pest resistance, and enhanced nitrogen fixation traits. GM alfalfa with Roundup Ready technology has achieved significant commercial adoption in North America, improving weed management economics and reducing crop establishment costs for alfalfa hay producers.

Precision Seed Coating and Treatment Technology

Advanced seed coating technologies incorporating microbial inoculants, micronutrients, fungicides, and polymer films improve germination rates, early establishment, and seedling vigor. Rhizobium inoculant coatings for legume forage seeds significantly improve biological nitrogen fixation performance and reduce synthetic fertilizer dependency.

Digital Agronomy and Seed Analytics Platforms

Digital platforms integrating soil data, weather analytics, and seed performance databases are enabling precision forage seed variety selection. OEM seed companies are developing digital agronomy tools that recommend optimal forage seed varieties for specific farm conditions, improving yield outcomes and farmer adoption of premium products.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Clover |

33.9% |

2025 |

|

Livestock |

Poultry |

36.4% |

2025 |

|

Species |

🔒 |

🔒 |

2025 |

|

Region |

North America |

34.7% |

2025 |

By Product

Clover commanded a 33.9% majority share in 2025 owing to its essential role in nitrogen fixation, soil health improvement, and high-protein nutrition across the widest range of temperate livestock farming systems. Rapidly expanding demand from both intensive and organic livestock operations sustains high clover seed procurement volumes globally.

To access detailed market analysis, Request Sample

Alfalfa (27.6%) supports high-yield hay production for dairy, beef, and equine markets, commanding premium per-acre seed values in North America and the Middle East. Ryegrass (18.8%) addresses temperate grass seed demand across Europe and Oceania. Chicory (11.2%) is gaining adoption in pasture renovation programs for its deep-rooting and high mineral content.

By Livestock

Poultry led the forage seed livestock segment at 36.4% in 2025, driven by the global expansion of commercial broiler, layer, and turkey production requiring high-quality pasture and forage-based feed components for productivity and animal welfare compliance. Rising per-capita poultry consumption in Asia sustains large-scale procurement.

Cattle (31.7%) reflects large global beef and dairy herds requiring consistent pasture and silage forage supply, with North America and Latin America as primary demand anchors. Pork (19.6%) captures forage-based feed supplement demand in commercial hog systems. Others (12.3%) includes equine, sheep, goats, and specialty applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

34.7% |

Large-scale alfalfa and clover production, advanced precision agriculture, government crop insurance programs, strong beef, dairy, and poultry livestock sectors |

|

Asia-Pacific |

27.9% |

Rapidly expanding livestock sectors in China and India, government pasture improvement programs, growing demand for premium animal protein and organic livestock products |

|

Europe |

21.6% |

EU Common Agricultural Policy support for sustainable pasture management, strong organic forage seed demand, advanced seed biotechnology development |

|

Latin America |

9.8% |

Brazil and Argentina's expanding cattle and poultry sectors, growing commercial forage farming adoption, increasing pasture improvement investment for meat export markets |

|

Middle East & Africa |

6.0% |

Alfalfa cultivation for domestic food security, government agricultural productivity investment, increasing livestock herd development programs |

North America's 34.7% market dominance in 2025 is driven by the US alfalfa hay industry, established clover seed production clusters, and government-backed precision agriculture programs. The US alfalfa hay export market sustains high certified seed procurement volumes, while strong dairy and beef sectors create consistent demand for improved forage varieties.

Asia-Pacific at 27.9% is the fastest-growing region at ~8.2% CAGR, anchored by China's expanding dairy and beef sectors, India's rapidly growing livestock herd, and Southeast Asian government pasture improvement programs. Europe at 21.6% benefits from CAP green payment support and strong organic forage seed demand from certified organic livestock farms.

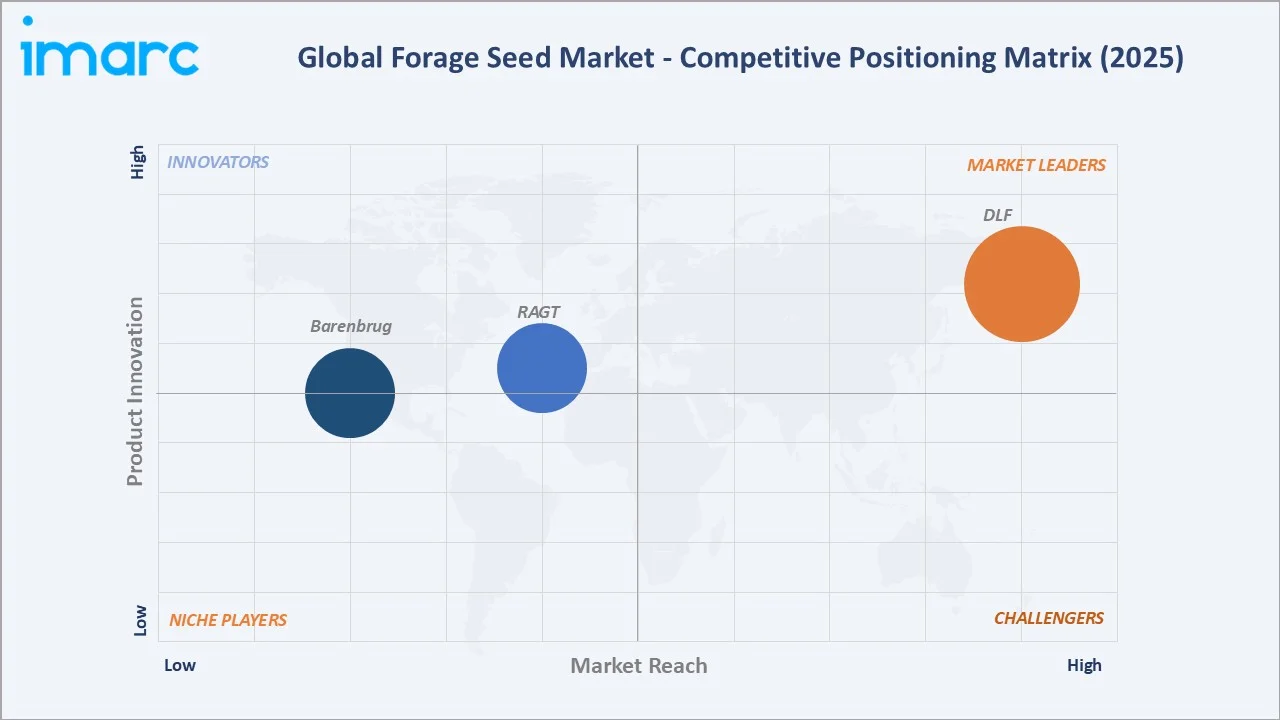

Competitive Landscape

The global forage seed market competitive landscape is moderately fragmented, with leading seed multinationals and specialized forage seed companies competing across product portfolio breadth, geographic scale, biotechnology capability, and distribution network depth. The landscape is evolving as consolidation, biotech investment, and organic certification create new differentiation axes.

|

Company Name |

Key Products / Operations |

Market Position |

Global Strategic Focus |

|

DLF |

Clover, Ryegrass, Alfalfa, Chicory, Grass blends |

Leader |

Expanding proprietary forage variety pipeline; strengthening distribution in Asia-Pacific and North America |

|

Barenbrug |

Brassicas, Grass Products, Legumes, Mixture & Blends |

Established |

Expanding proprietary grass breeding; strengthening Oceania, North America, and emerging market distribution |

|

RAGT |

Ryegrass, alfalfa, chicory, legume seed blends |

Emerging |

Strengthening European Forage Seed position; expanding international business through new market partnerships |

Key players include DLF, Barenbrug, RAGT, and others.

Key Company Profiles

DLF

DLF is a global seed company, specializing in forage crops, turf, and amenity seeds. DLF is the world's largest supplier of grass and legume forage seeds, with a comprehensive proprietary breeding program spanning all major forage species.

- Product Portfolio: Clover, Ryegrass, Alfalfa, Chicory, Grass blends

- Strategic Focus: Expanding proprietary forage variety pipeline, strengthening distribution networks in North America and Asia-Pacific, and investing in sustainable and organic seed product development to capture above-market premium pricing growth.

Barenbrug

Barenbrug is a Netherlands-based, family-owned global seed company, specializing in the research, development, and production of forage grasses, legumes, and turf seeds.

- Product Portfolio: Brassicas, Grass Products, Legumes, Mixture & Blends

- Strategic Focus: Advancing endophyte and beneficial-fungus seed technology to improve livestock productivity and pasture persistence; expanding forage grass breeding programs across Oceania, North America, and emerging markets; and developing climate-resilient varieties targeting drought-stressed and high-rainfall farming regions globally.

Market Concentration Analysis

The forage seed market is moderately fragmented globally, with top 4-5 companies collectively accounting for approximately 35–45% of global forage seed revenue. Specialized regional companies account for 20–30%, while domestic seed producers serve local markets across Asia, Latin America, and Africa with lower-cost varieties.

Market concentration is evolving as leading companies expand biotech variety portfolios, invest in international distribution, and develop organic and precision-agriculture-compatible products that differentiate them from commodity seed suppliers. Consolidation through acquisitions continues reshaping competitive dynamics at both global and regional levels through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Asia-Pacific forage seed market (~8.2% CAGR) represents the highest-growth regional segment through 2034, capturing government-incentive-driven demand for improved pasture varieties and commercial livestock feed. The organic forage seed premium segment (~10–12% CAGR) and climate-resilient biotech varieties (~9–11% CAGR) offer above-market growth potential.

Emerging Markets

Asia-Pacific and the Middle East are emerging as high-growth frontiers for forage seed investment. China's expanding dairy sector, India's government pasture improvement programs, and Gulf state food security alfalfa cultivation initiatives are generating incremental demand with significant untapped volume and premium pricing growth potential.

Venture & Investment Trends

Private equity and strategic investors are increasing capital allocation to biotech forage seed startups, precision agronomy platforms, and organic seed supply chain infrastructure. Government-linked investment in sustainable agriculture and food security programs is catalyzing private capital mobilization in forage seed biotechnology and distribution networks globally.

Future Market Outlook (2026-2034)

The global forage seed market is forecast to expand from USD 21.97 Billion in 2025 to USD 42.54 Billion by 2034 at a CAGR of 7.39%, driven by global livestock production growth, precision agriculture adoption, organic segment premiumization, and climate-resilient biotechnology variety adoption across all key regions through the forecast horizon.

Three structural forces will shape the market through 2034: sustained global livestock herd expansion—particularly in Asia-Pacific—will compound forage seed demand; climate adaptation investment will accelerate adoption of drought-tolerant and precision-optimized varieties; and the premiumization of organic and sustainably produced livestock products will drive dedicated organic forage seed market expansion as a high-margin growth segment.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including forage seed R&D directors, livestock farm managers, seed distribution executives, government agricultural policy officials, and precision agriculture technology providers across North America, Europe, and Asia-Pacific.

Secondary Research

Key secondary sources include FAO global livestock and feed production statistics, USDA forage crop reports and crop insurance notifications, ISTA seed testing standards, national seed certification agency publications, OEM annual reports, agri-biotech patent databases, and trade publications covering agriculture and livestock sectors. Over 60 secondary sources reviewed.

Forecasting Models

Market size estimations and growth projections were derived using bottom-up forecasting models incorporating global livestock herd size projections, average forage land area per livestock unit, seed application rates, variety replacement frequency, and average seed price per category. Premium adjustments were applied for biotech and certified organic variety segments.

Forage Seed Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Alfalfa, Clover, Ryegrass, Chicory, Others |

| Livestocks Covered | Poultry, Cattle, Pork, Others |

| Species Covered | Legumes, Grasses |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | DLF, Barenbrug, RAGT, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the forage seed market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global forage seed market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the forage seed industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Forage Seed Market Report

The global forage seed market reached USD 21.97 Billion in 2025, reflecting sustained demand driven by rising global livestock production, government subsidies for forage cultivation, precision agriculture adoption, and increasing investment in improved seed varieties across all major agricultural regions.

The market is projected to reach USD 42.54 Billion by 2034, growing at a CAGR of 7.39% during 2026-2034, driven by livestock sector expansion, precision agriculture adoption, organic forage segment growth, and Asia-Pacific market acceleration.

Clover leads the market with a 33.9% share in 2025, driven by its nitrogen-fixing properties, soil health benefits, and high-protein nutritional profile for ruminant and poultry livestock systems across temperate agricultural regions. This segment is expected to maintain leadership through 2034.

Poultry commands the largest livestock share at 36.4% in 2025, underpinned by global expansion of commercial poultry production and the nutritional role of forage-based feed inputs. Cattle at 31.7% is the second largest segment driven by dairy and beef herd demand.

North America dominates with a 34.7% share in 2025, supported by the US alfalfa hay export industry, large-scale dairy and beef operations, government crop insurance programs, and advanced precision agriculture adoption optimizing forage seed performance.

Key drivers include rising global livestock production, government subsidies and supportive policies promoting forage cultivation, precision agriculture adoption improving seed performance, and increasing R&D investment in drought-tolerant and nutritionally enhanced forage seed varieties.

Major challenges include high seed development and certification costs limiting new entrant participation, climate variability disrupting forage crop production, regulatory barriers to GM seed adoption in key markets, and supply chain fragmentation limiting farmer access to certified improved varieties.

Leading companies include DLF, Barenbrug, and RAGT, among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)