GCC Agricultural Robots Market Size, Share, Trends and Forecast by Product Type, Offering, Application, and Country, 2026-2034

GCC Agricultural Robots Market Size, Share, Trends & Forecast (2026-2034)

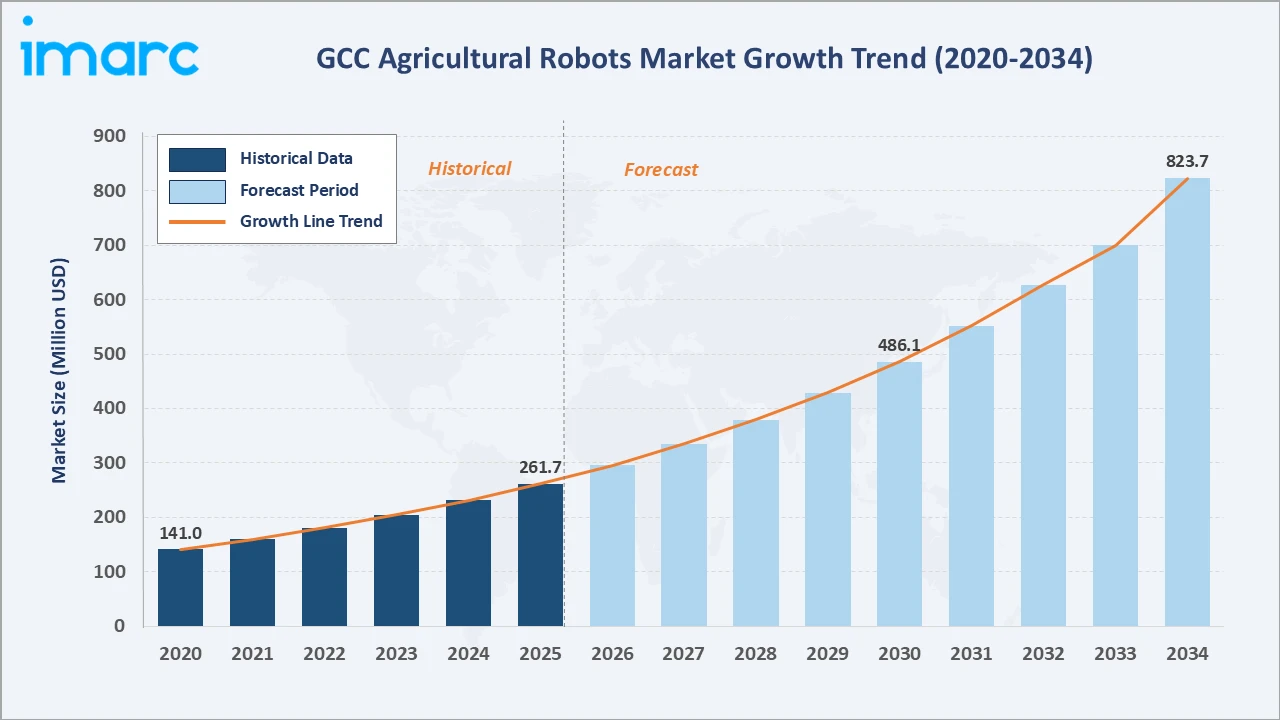

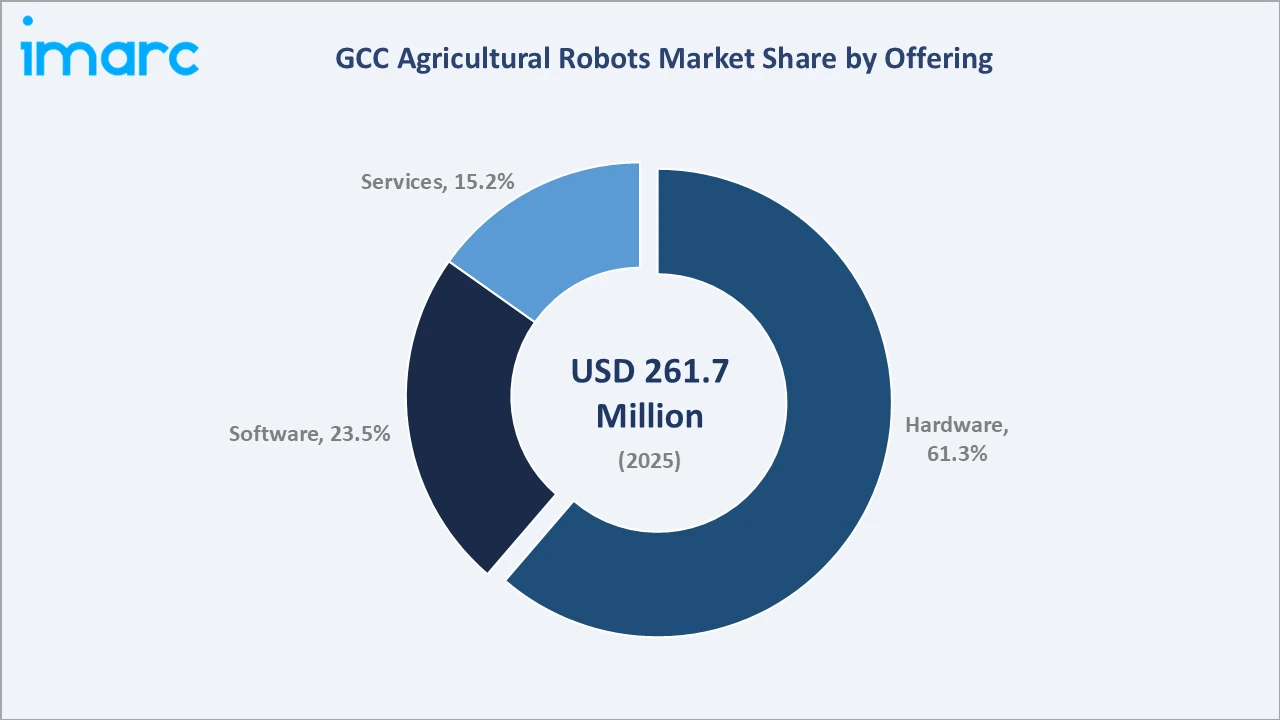

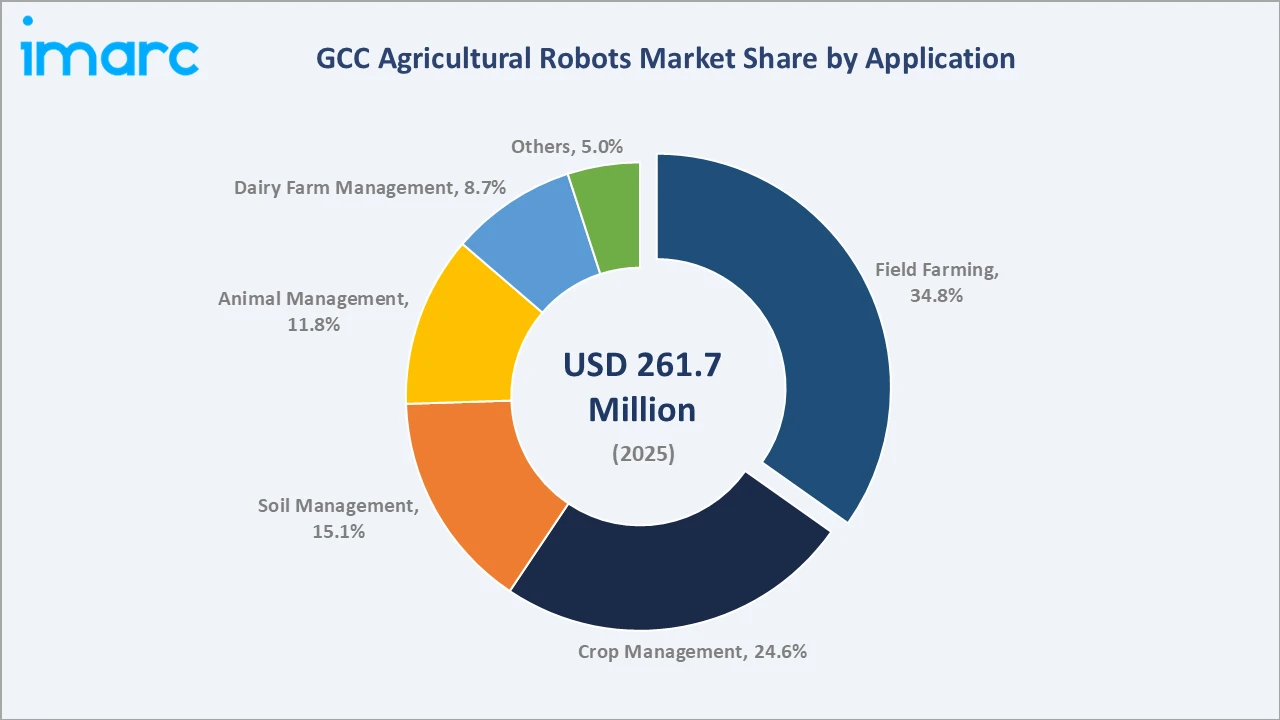

The GCC agricultural robots market reached USD 261.7 Million in 2025 and is projected to reach USD 823.7 Million by 2034, growing at a CAGR of 13.18% during 2026-2034. The market is driven by precision agriculture adoption, rising labor scarcity, government agri-tech vision programs, and expanding specialty crop demand.

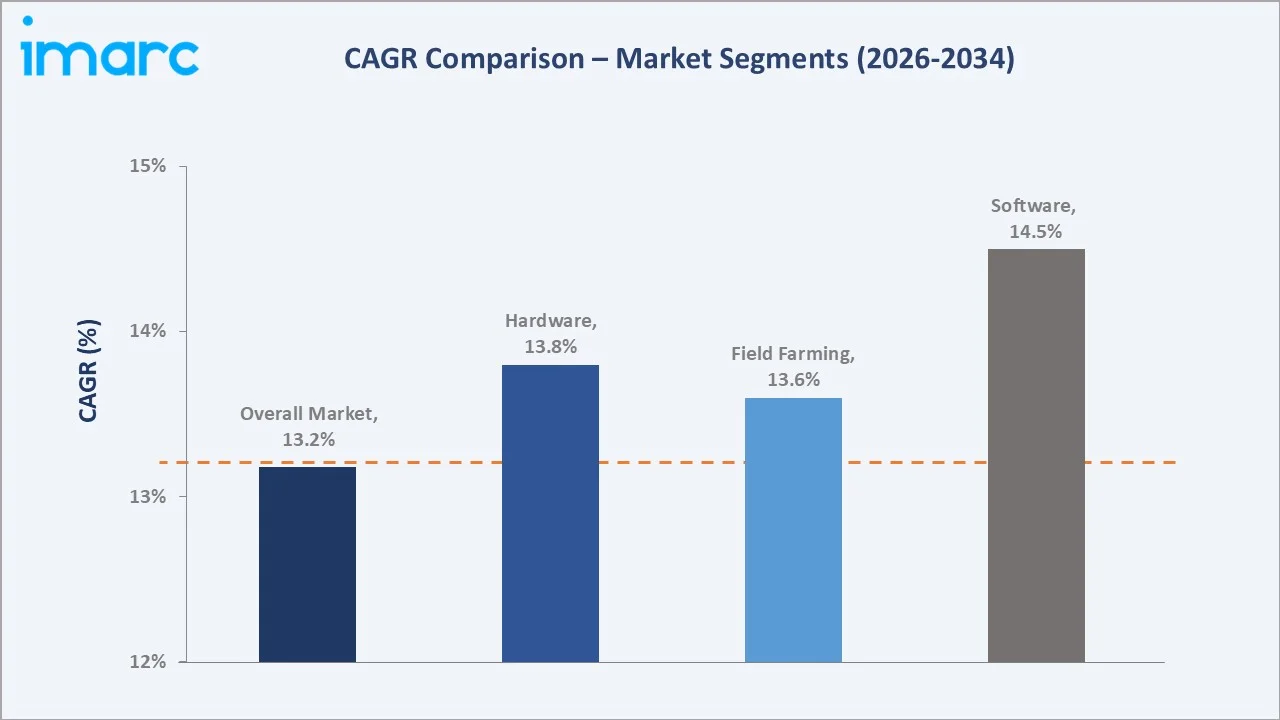

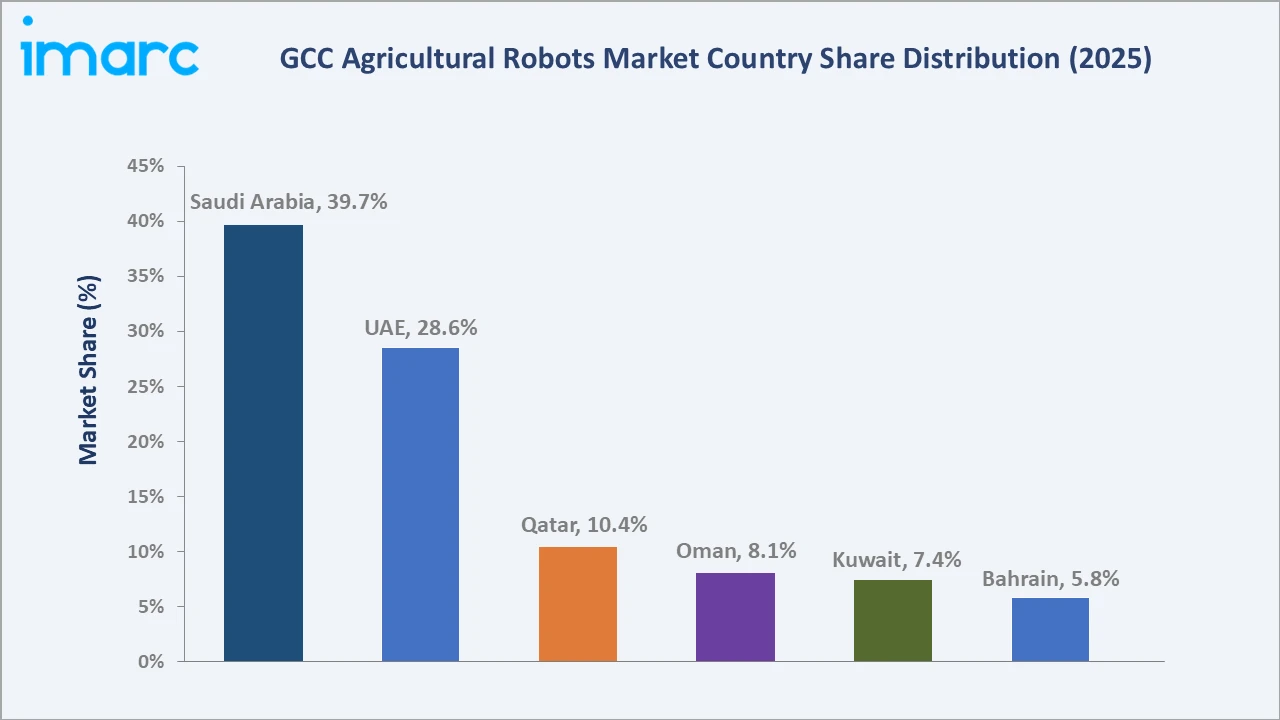

Hardware dominates at 61.3%, Field Farming leads applications at 34.8%, and Saudi Arabia commands 39.7% of regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 261.7 Million |

|

Forecast Market Size (2034) |

USD 823.7 Million |

|

CAGR (2026-2034) |

13.18% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Offering |

Hardware (61.3%, 2025) |

|

Dominant Application |

Field Farming (34.8%, 2025) |

|

Leading Country |

Saudi Arabia (39.7%, 2025) |

The market expanded from USD 141.0 Million in 2020 to USD 261.7 Million in 2025, anchored at USD 486.1 Million in 2030 and forecast to reach USD 823.7 Million by 2034. Limited arable land and water scarcity across GCC countries are accelerating demand for precision agribots that maximise resource utilisation and crop output.

To get more information on this market, Request Sample

Field farming application grows at ~13.6% CAGR as UAV-based crop monitoring and driverless tractors proliferate across Saudi Arabia's mega-farm projects. The hardware segment grows at ~13.8% CAGR as sensor costs decline and ruggedised robotic hardware becomes viable for GCC desert environments.

Executive Summary

The GCC agricultural robots market reached USD 261.7 Million in 2025, driven by the fundamental transformation of Gulf Cooperation Council agricultural practice toward technology-intensive, resource-efficient precision farming. The market is projected to reach USD 823.7 Million by 2034.

Hardware at 61.3% dominates by capturing robot platforms, drone airframes, sensor systems, and control hardware powering GCC agri-automation. Field farming at 34.8% leads through large-scale UAV deployment in Saudi Arabia's Vision 2030 mega-farm zones. Saudi Arabia at 39.7% leads all GCC countries through its large farmland base and government-led digital agriculture initiatives.

Key Market Insights

|

Insight |

Data |

|

Dominant Offering |

Hardware – 61.3% share (2025) |

|

Dominant Application |

Field Farming – 34.8% market share (2025) |

|

Leading Country |

Saudi Arabia – 39.7% market share (2025) |

|

Market Opportunity |

UAV crop-health analytics; AI soil sensors; robotic milking; driverless tractors for desert mega-farms |

Key Analytical Observations Supporting The Above Data:

- Hardware at 61.3%: Hardware dominates as robot platforms, UAV airframes, rugged sensors, and control electronics constitute the primary capital expenditure in GCC agricultural automation. Strong government procurement programs in Saudi Arabia and UAE are driving high-value hardware contracts.

- Field Farming at 34.8%: Field farming leads because large-scale open farmland across Saudi Arabia, Oman, and UAE is most accessible for UAV crop surveillance, automated irrigation systems, and GPS-guided driverless tractors. Vision 2030 agricultural productivity programs amplify this segment.

- Saudi Arabia at 39.7%: Saudi Arabia leads due to its significant farmland area, robust government investment under Vision 2030, and strategic agricultural diversification to reduce food import dependence. The Kingdom's large-scale greenhouse and hydroponics projects create high robot deployment density.

GCC Agricultural Robots Market Overview

The GCC agricultural robots market encompasses the design, manufacture, and supply of autonomous robotic systems used across all agricultural tasks in Gulf Cooperation Council member states, including crop monitoring, precision irrigation, automated harvesting, robotic milking, soil analysis, and livestock management.

The ecosystem integrates hardware OEMs, AI and software developers, IoT connectivity providers, precision agriculture sensor manufacturers, drone airframe producers, end-user farms and agri-enterprises, and government regulatory and incentive bodies. Macroeconomic factors include Vision 2030 food security programs, limited arable land, water scarcity, declining expatriate agricultural labour, and rising food import costs.

Market Dynamics

To evaluate market opportunities, Request Sample

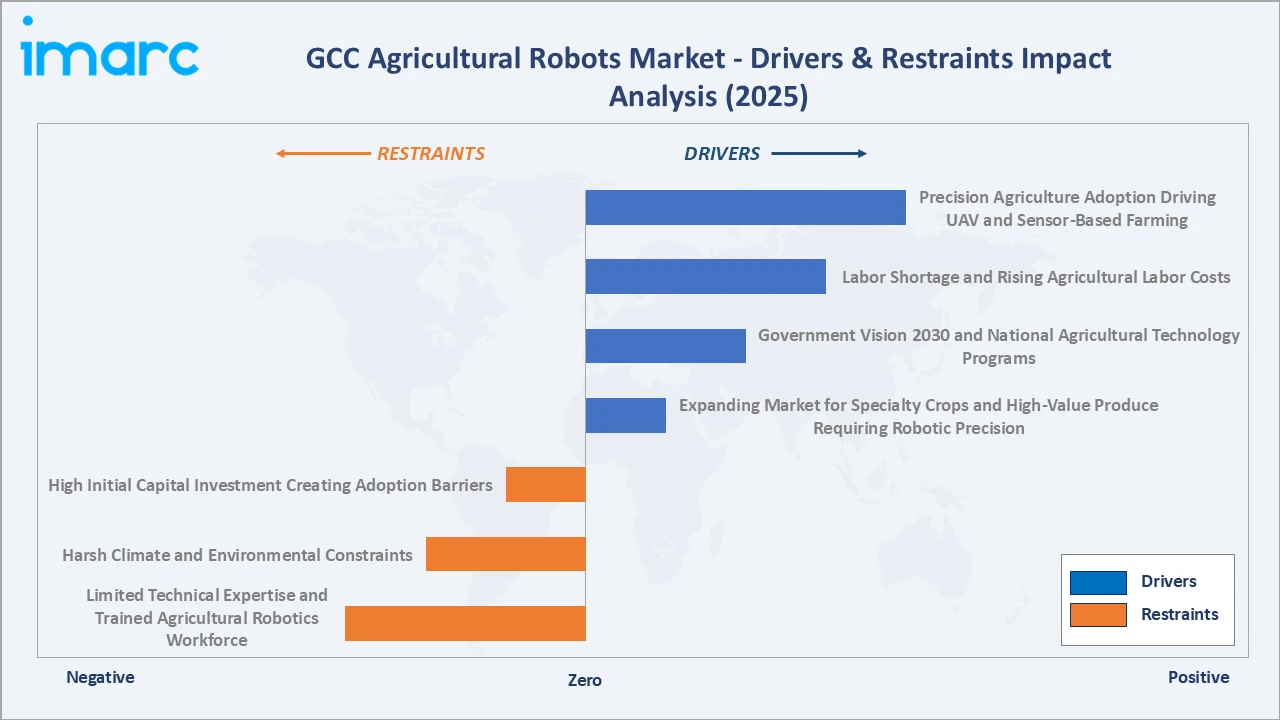

Market Drivers

- Precision Agriculture Adoption Driving UAV and Sensor-Based Farming: Precision agriculture technologies, including multispectral UAVs, AI-driven soil sensors, and autonomous irrigation robots, enable GCC farmers to optimise water use, reduce chemical inputs, and maximise yields from limited arable land. Robotic precision spraying reduces pesticide consumption by up to 30%, a critical efficiency gain in GCC water-stressed farming environments.

- Labor Shortage and Rising Agricultural Labor Costs: Agricultural labour availability in GCC countries has declined sharply due to reduced expatriate workforce inflows and rising minimum wages. Robotic systems offer a permanent, scalable alternative to seasonal manual labour for planting, harvesting, and livestock management.

- Government Vision 2030 and National Agricultural Technology Programs: Governments across the GCC are accelerating investments in agricultural technology through long-term food security and economic diversification initiatives. National strategies are encouraging the adoption of robotics, precision farming, smart irrigation, IoT-enabled monitoring, and other advanced farming technologies to improve productivity, resource efficiency, and domestic food production.

- Expanding Market for Specialty Crops and High-Value Produce Requiring Robotic Precision: GCC demand for locally grown specialty produce, including dates, vegetables, herbs, and aquaculture, is growing due to consumer preference for freshness and food safety. High-value crops require precise care that agricultural robots deliver more consistently than manual labour, making automation a financially justified investment for GCC specialty farm operators.

Market Restraints

- High Initial Capital Investment Creating Adoption Barriers: Agricultural robotics solutions involve significant initial investments for advanced automation systems, precision sensors, AI-enabled software, and maintenance infrastructure. While these technologies offer long-term operational efficiencies, the high acquisition and implementation costs remain a key barrier for many agricultural producers, particularly small and medium-sized enterprises.

- Harsh Climate and Environmental Constraints: The GCC's extreme climatic conditions, including high temperatures, dust, sand, and humidity in certain regions, can affect the performance, reliability, and maintenance requirements of agricultural robots. These environmental challenges often necessitate specialized equipment designs and more frequent servicing, increasing operational costs and slowing technology adoption.

- Limited Technical Expertise and Trained Agricultural Robotics Workforce: GCC countries face a shortage of qualified technicians and engineers capable of operating, maintaining, and programming advanced agricultural robot systems. Dependence on foreign technical support for maintenance reduces operational uptime, increases ongoing service costs, and limits confidence among GCC farm operators in robot system reliability.

Market Opportunities

- Robotic Milking and Automated Dairy Farm Management Expansion: GCC dairy sector growth, with increasing demand for locally produced milk and dairy products, is creating substantial demand for automated milking systems. UAE and Saudi Arabia are investing in large automated dairy farms that require robotic milking units, automated feeding systems, and AI-driven herd management platforms.

- AI-Integrated Soil and Crop Health Monitoring Robots: AI-powered soil analysis robots and crop health monitoring drones that provide real-time nutrient mapping, irrigation scheduling, and disease detection represent a high-growth GCC market opportunity. Government digital agriculture programs and private farm operators are increasingly investing in data-driven precision agronomy platforms.

Market Challenges

- Regulatory Frameworks for Agricultural UAV Operations Requiring Harmonisation: Drone regulations for agricultural applications vary significantly across GCC member states, creating operational compliance complexity for multi-country agricultural robot deployments. Harmonised GCC-wide agricultural UAV regulatory frameworks are still under development, slowing large-scale cross-border agri-drone service provider operations.

- High Dependency on Technology Imports Creating Supply Chain Vulnerability: GCC agricultural robot markets depend heavily on technology imports from Europe, Japan, and China. Supply chain disruptions, geopolitical trade restrictions, and currency fluctuations can increase robot procurement costs and extend delivery timelines, creating operational planning challenges for GCC farm operators.

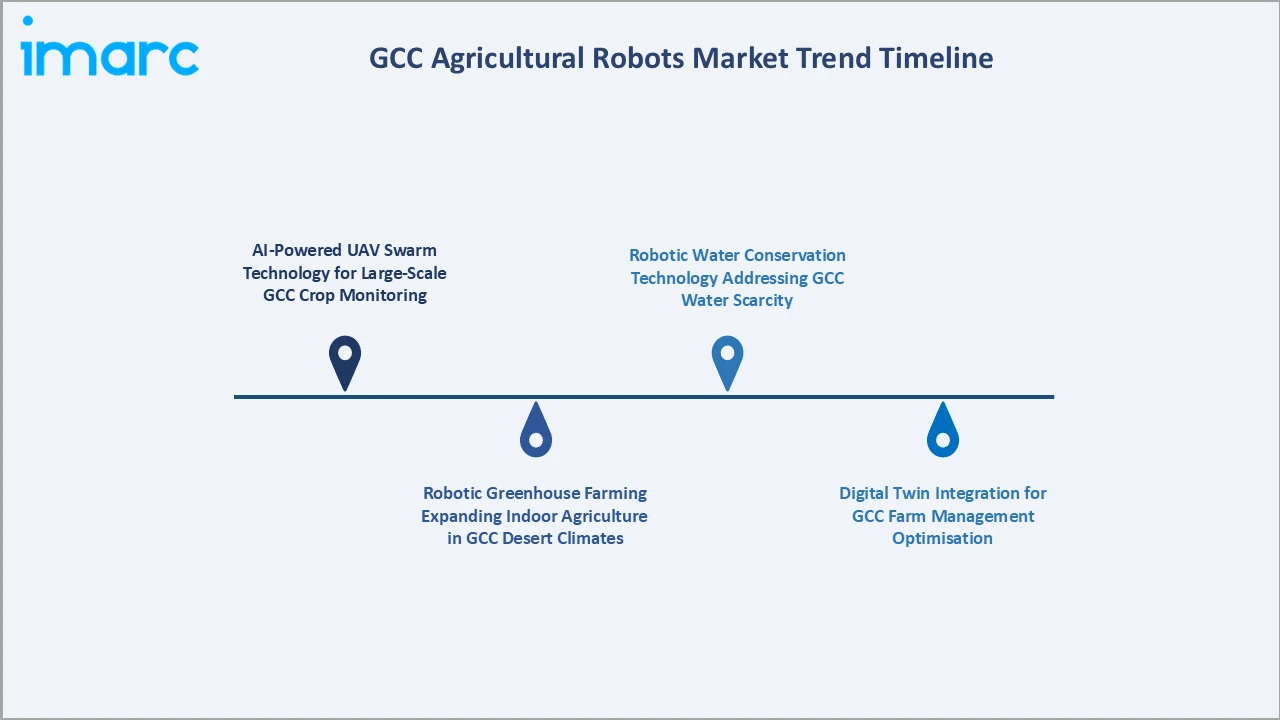

Emerging Market Trends

1. AI-Powered UAV Swarm Technology for Large-Scale GCC Crop Monitoring

AI-powered UAV swarm technology is transforming large-scale agricultural monitoring by enabling multiple drones to operate collaboratively across extensive farmland. These systems support real-time crop health assessment, irrigation monitoring, pest and disease detection, and precision input application, helping farmers improve operational efficiency, optimize resource utilization, and enhance overall crop productivity.

2. Robotic Greenhouse Farming Expanding Indoor Agriculture in GCC Desert Climates

Climate-controlled greenhouse robotic systems are enabling year-round crop production independent of GCC extreme weather. Automated seeding, transplanting, harvesting, and climate control robots inside hydroponic and aeroponic facilities are proliferating across UAE and Saudi Arabia, creating a high-growth niche for indoor agricultural automation.

3. Digital Twin Integration for GCC Farm Management Optimisation

Digital twin platforms integrating real-time robot sensor data with farm management systems create virtual farm replicas that enable GCC operators to optimise planting schedules, irrigation timing, and harvest logistics. Digital twin adoption is accelerating through GCC government smart agriculture programs that mandate data-driven farm management reporting.

4. Robotic Water Conservation Technology Addressing GCC Water Scarcity

The integration of robotic precision irrigation technologies is emerging as a key trend in the GCC agricultural sector, where efficient water management remains a strategic priority. Equipped with advanced sensors, AI-driven irrigation controls, and automated monitoring capabilities, these systems enable targeted water application, reduce resource wastage, and support sustainable agricultural production under challenging climatic conditions.

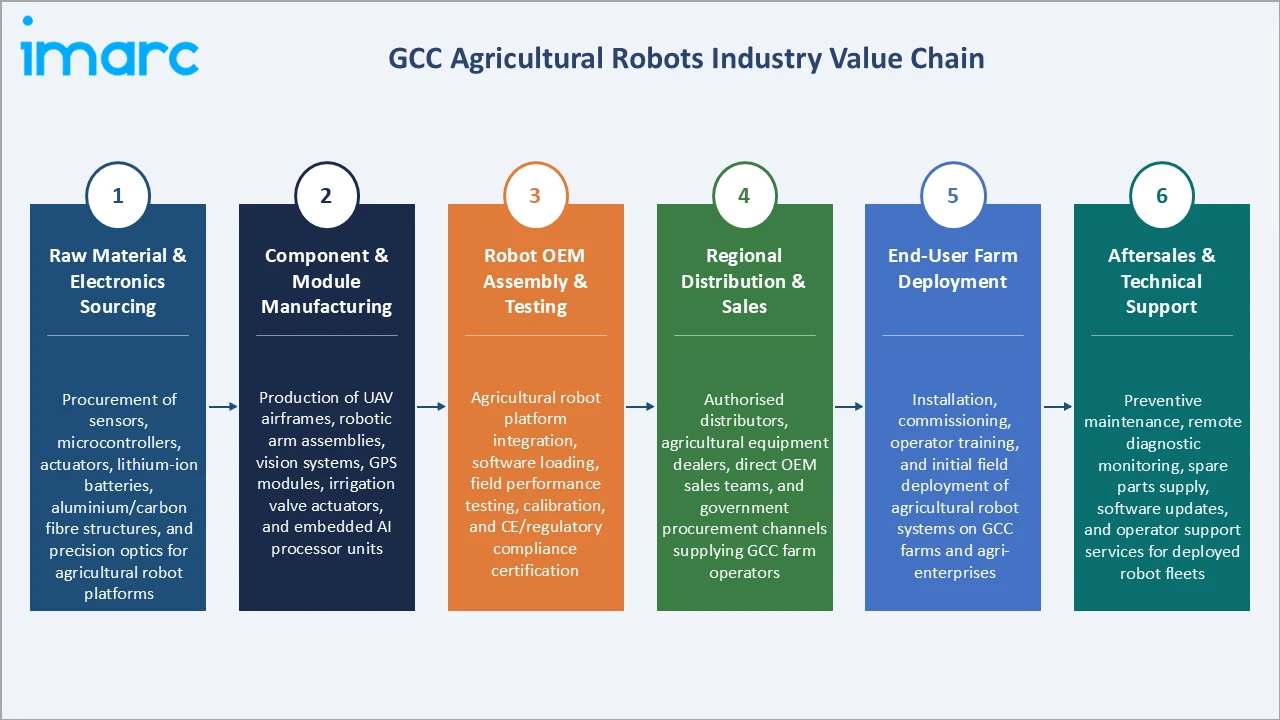

Industry Value Chain Analysis

The GCC agricultural robots value chain integrates raw material sourcing, electronic component manufacturing, robot platform assembly, software and AI development, regional distribution, end-user farm deployment, and aftersales technical support. The chain is predominantly import-dependent, with OEM manufacturing concentrated in North America, Europe, and Asia.

|

Stage |

Key Activities |

|

Raw Material & Electronics Sourcing |

Procurement of sensors, microcontrollers, actuators, lithium-ion batteries, aluminium/carbon fibre structures, and precision optics for agricultural robot platforms. |

|

Component & Module Manufacturing |

Production of UAV airframes, robotic arm assemblies, vision systems, GPS modules, irrigation valve actuators, and embedded AI processor units. |

|

Robot OEM Assembly & Testing |

Agricultural robot platform integration, software loading, field performance testing, calibration, and CE/regulatory compliance certification. |

|

Regional Distribution & Sales |

Authorised distributors, agricultural equipment dealers, direct OEM sales teams, and government procurement channels supplying GCC farm operators. |

|

End-User Farm Deployment |

Installation, commissioning, operator training, and initial field deployment of agricultural robot systems on GCC farms and agri-enterprises. |

|

Aftersales & Technical Support |

Preventive maintenance, remote diagnostic monitoring, spare parts supply, software updates, and operator support services for deployed robot fleets. |

The raw material and electronics sourcing tier is the most geopolitically sensitive stage due to GCC dependence on semiconductor imports. The regional distribution tier is the most commercially dynamic stage as GCC government tenders for large-scale precision farming programs create high-value distribution contracts.

Technology Landscape in the GCC Agricultural Robots Industry

Unmanned Aerial Vehicle (UAV) / Drone Technology

Agricultural UAV technology enables multispectral and hyperspectral imaging, precision spraying, seed broadcasting, and real-time crop health mapping. GCC-optimised UAVs feature extended battery endurance for large-farm coverage, dust-sealed motors for desert environments, and AI-powered autonomous flight path planning that reduces operator skill requirements for large-scale GCC agricultural deployments.

Automated Milking Robot Technology

Automated milking robots use computer vision, robotic arms, and teat detection sensors to perform milking without human intervention, enabling 24/7 dairy operations. GCC dairy expansion programs in Saudi Arabia and UAE are adopting robotic milking systems from Lely and DeLaval that integrate with AI herd management platforms, tracking individual cow health, milk yield, and feeding requirements.

AI-Powered Computer Vision for Crop and Livestock Management

In June 2025, Trimble Inc. launched its AI-enhanced Ag Vision platform for precision crop monitoring, integrating satellite imagery, UAV multispectral data, and ground-sensor data streams into a unified GCC farm management dashboard. The platform enables GCC farm operators to detect crop stress, estimate yield variations across farm zones, and automate irrigation adjustments with field-level precision, directly supporting GCC national food security digitalisation objectives.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Unmanned Aerial Vehicles (UAVs)/Drones |

🔒 |

2025 |

|

Offering |

Hardware |

61.3% |

2025 |

|

Application |

Field Farming |

34.8% |

2025 |

|

Country |

Saudi Arabia |

39.7% |

2025 |

By Offering

Hardware leads at 61.3% in 2025, capturing robotic platforms, drone airframes, sensor arrays, and control hardware as the primary capital expenditure in GCC agricultural automation. The high hardware share reflects the early adoption stage where farm operators invest primarily in physical robot systems before building complementary software and services infrastructure.

To access detailed market analysis, Request Sample

Software at 23.5% encompasses farm management platforms, AI analytics suites, drone flight management software, and precision agriculture decision-support systems. Services at 15.2% includes installation, operator training, preventive maintenance contracts, and remote monitoring services, with growing importance as GCC robot fleets scale and operators seek managed-service deployment models.

By Application

Field farming leads at 34.8% through high-volume UAV deployments for crop health surveillance, automated irrigation management, and driverless tractor operations across GCC large-scale open farmland. Field farming's above-market CAGR reflects Saudi Arabia's mega-farm program expansion requiring extensive precision agriculture robotics coverage.

Crop management at 24.6% captures AI-driven planting optimisation, fertiliser precision application, and automated pest management. Soil management at 15.1% reflects growing adoption of robotic soil sampling and nutrient analysis systems. Animal management at 11.8% and dairy farm management at 8.7% reflect GCC livestock sector automation, primarily in Saudi Arabia and UAE.

Regional Market Insights

|

Country |

Share (2025) |

Key Agricultural Robots Market Drivers & Characteristics |

|

Saudi Arabia |

39.7% |

Driven by Vision 2030 mega-farm programs, government agri-tech subsidies, large farmland base, and strategic food security diversification investments. |

|

UAE |

28.6% |

Driven by high-technology greenhouse farming, National Food Security Strategy 2051, advanced hydroponic automation, and strong private sector agri-tech investment. |

|

Qatar |

10.4% |

National Food Security Program post-blockade driving rapid agri-tech adoption and greenhouse automation for self-sufficient domestic food production. |

|

Oman |

8.1% |

Growing date palm and vegetable cultivation automation, Vision 2040 agriculture modernisation, and expanding precision irrigation robot deployments. |

|

Kuwait |

7.4% |

Government-led food security programs and emerging greenhouse automation investments driving initial agricultural robotics adoption. |

|

Bahrain |

5.8% |

Smallest market but growing through intensive vertical farming and protected agriculture automation driven by severe arable land limitations. |

Saudi Arabia at 39.7% leads through Vision 2030's agricultural productivity mandates, large-scale government-owned farm robotics procurement, and the highest farmland area among GCC member states. UAE at 28.6% reflects its technology-forward smart farming model, high-density greenhouse automation, and advanced agri-tech startup ecosystem.

Qatar at 10.4% reflects rapid post-2017 food security investment following the diplomatic blockade, which dramatically accelerated domestic agricultural production and robot deployment. Oman at 8.1% and Kuwait at 7.4% represent growing but earlier-stage adoption markets. Bahrain at 5.8% has the smallest market but highest robot-to-farmland intensity due to severe land constraints forcing intensive automated vertical farming.

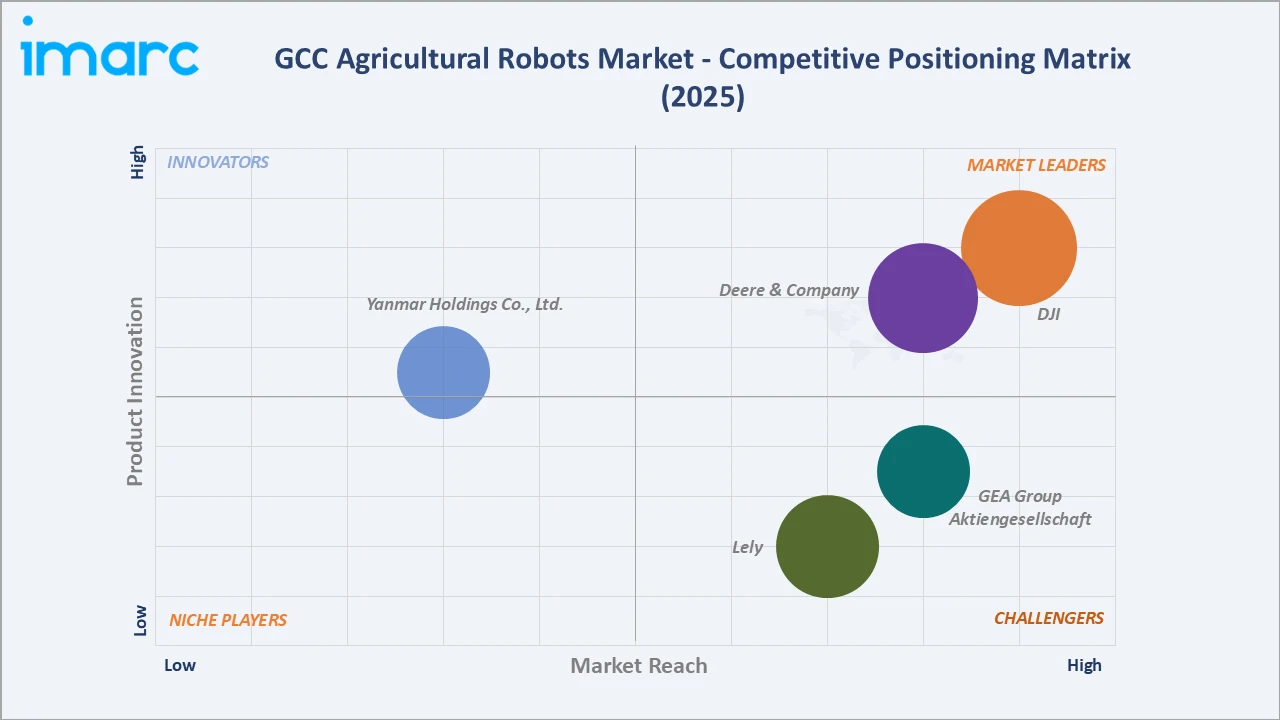

Competitive Landscape

The GCC agricultural robots market competitive landscape is moderately concentrated with three distinct tiers: global agricultural equipment majors with GCC distribution presence, specialist agricultural robotics companies, and regional agri-tech solution providers serving GCC-specific farm requirements.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Deere & Company |

Autonomous Tractor Systems |

Market Leader |

Deere & Company leads through autonomous tractor technology and precision farming platform integration across GCC large-scale farming operations. |

|

DJI |

DJI AGRAS T55, DJI AGRAS T100, DJI AGRAS T70P, DJI AGRAS T25P, DJI AGRAS T50, DJI AGRAS T25 |

Market Leader |

DJI dominates GCC agricultural UAV segment through cost-competitive, high-performance agricultural drone systems with strong regional distributor networks. |

|

Lely |

Lely Astronaut A5, Lely Vector, Lely Discovery 120 |

Strong Challenger |

Lely specialises in automated milking and dairy farm management robots for GCC's expanding large-scale dairy farming sector. |

|

GEA Group Aktiengesellschaft |

DairyRobot R9500, DairyRobot R9650 |

Strong Challenger |

GEA Group provides integrated dairy automation solutions and automated milking robots for GCC commercial dairy enterprises. |

|

Yanmar Holdings Co., Ltd. |

Yanmar YT5113A Autonomous Tractor, Yanmar Robot Tractor |

Emerging Player |

Yanmar offers autonomous tractor systems with GPS and precision navigation suited to GCC open field farming environments. |

Key players include Deere & Company, DJI, Lely, GEA Group Aktiengesellschaft, Yanmar Holdings Co., Ltd., and others.

Key Company Profiles

Deere & Company

Deere & Company is a US-based global agricultural equipment manufacturer with a leading presence in the GCC agricultural robots’ market through its autonomous tractor systems, precision farming platforms, and AI-powered spraying technologies.

- Key Products: Autonomous Tractor Systems

- Strategic Focus: Expanding AI-integrated autonomous farming systems and cloud-based farm management platforms targeting GCC large-scale commercial farming and government agricultural modernisation programs.

DJI

DJI is a China-based UAV manufacturer with dominant presence in the GCC agricultural robots’ market through its Agras series agricultural drones optimised for precision spraying, seeding, and crop monitoring.

- Key Products: DJI AGRAS T55, DJI AGRAS T100, DJI AGRAS T70P, DJI AGRAS T25P, DJI AGRAS T50, DJI AGRAS T25, and others.

- Strategic Focus: Expanding GCC agricultural drone market penetration through localised distributor partnerships, government agricultural program procurement, and development of heat-resistant drone systems for extreme GCC climate agricultural operations.

Market Concentration Analysis

The GCC agricultural robots market is moderately concentrated, with the top five key players collectively accounting for approximately 45-55% of regional market revenue. Government procurement programs tend to concentrate orders among proven global brands with regional service capabilities.

Investment & Growth Opportunities

Highest Growth Segments

Software (~14.5% CAGR), crop management applications (~14.2% CAGR), UAE market (~13.9% CAGR), automated greenhouse farming systems (~16% CAGR from a smaller base), and AI-integrated precision irrigation robots (~17% CAGR) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

GCC indoor vertical farming automation represents the market's highest per-unit-value emerging opportunity. Fully automated vertical farm systems in UAE and Saudi Arabia at USD 500,000-USD 2 Million per installation generate substantially higher revenue per deployment than open-field agricultural robots, with government food security programs creating a structurally growing demand pool.

Investment Themes

- Robotic-as-a-Service (RaaS) models for GCC farm operators: Subscription-based agricultural robot deployment reduces capital barriers for GCC farm operators. RaaS providers offering UAV fleet management, precision irrigation robots, and crop monitoring on a per-hectare subscription model can address the high upfront cost restraint and accelerate broader market adoption.

- GCC agri-tech localisation and manufacturing investment: GCC governments under Vision 2030 and UAE Industrial Strategy 2031 are incentivising local manufacturing and assembly of agricultural technology. Investment in GCC-based agricultural robot assembly operations, sensor calibration centres, and AI software development teams can capture preferential government procurement positioning.

Future Market Outlook (2026-2034)

The GCC agricultural robots market is projected to grow from USD 261.7 Million in 2025 to USD 823.7 Million by 2034, delivering a 13.18% CAGR over the forecast period. The market anchor of USD 486.1 Million in 2030 represents the GCC agricultural automation industry at its commercial inflection point when autonomous field systems will have achieved mainstream adoption in Saudi Arabia's large-scale farms.

Three structural forces define GCC agricultural robot market growth through 2034 with high confidence. National food security programs across all six GCC member states provide government-funded demand that insulates the market from private-sector economic cycles. GCC population growth and urbanisation create rising domestic food demand that cannot be met without agricultural productivity gains that robotics uniquely enable. Water and land scarcity fundamentally mandate precision technology adoption as the only viable pathway to sustainable GCC agricultural output growth.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ GCC agricultural industry stakeholders (2025), including Ministry of Agriculture officials, commercial farm operators, agricultural robot distributors, agri-tech startup founders, and precision agriculture technology specialists across Saudi Arabia, UAE, Qatar, and Oman.

Secondary Research

Secondary research encompassed GCC government agricultural strategy documents, company annual reports, GCC food security program publications, FAO GCC agricultural data reports, IFR World Robotics agricultural robot statistics 2024-2025, GCC agricultural investment reports, and regional agri-tech industry association publications. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using bottom-up model: (i) GCC agricultural land area and crop production by country; (ii) robot penetration rate by application type and country; (iii) average robot system value by product category; (iv) government procurement program additions; (v) annual robot fleet expansion by GCC farm operator category.

GCC Agricultural Robots Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Unmanned Aerial Vehicles (UAVs)/Drones, Milking Robots, Automated Harvesting Systems, Driverless Tractors, Others |

| Offerings Covered | Hardware, Software, Services |

| Applications Covered | Field Farming, Dairy Farm Management, Animal Management, Social Management, Crop Management, Others |

| Countries Covered | Saudi Arabia, UAE, Qatar, Bahrain, Kuwait, Oman |

| Companies Covered | Deere & Company, DJI, Lely, GEA Group Aktiengesellschaft, Yanmar Holdings Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the GCC agricultural robots market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the GCC agricultural robots market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the GCC agricultural robots industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the GCC Agricultural Robots Market Report

The GCC agricultural robots market reached USD 261.7 Million in 2025, driven by hardware at 61.3%, field farming application leadership at 34.8%, Saudi Arabia's 39.7% country share, and growing GCC government investment in agricultural technology under national food security and Vision 2030 programs.

The GCC agricultural robots market grows at 13.18% CAGR during 2026-2034, reaching USD 823.7 Million by 2034. This reflects GCC government food security investment, expanding precision agriculture adoption, labour shortage-driven automation demand, and growing specialty crop production requiring robotic precision.

Hardware leads at 61.3%, capturing robot platforms, UAV systems, precision sensors, and control electronics as the primary capital expenditure in GCC farm automation. Software at 23.5% and Services at 15.2% represent fast-growing complementary segments as GCC operators seek complete integrated solutions.

Field farming leads at 34.8% through large-scale UAV deployment for crop surveillance, autonomous irrigation systems, and driverless tractors across GCC open farmland. Field farming grows above market average as Saudi Arabia's mega-farm program expansion requires extensive robotic field coverage for cost-efficient large-scale operations.

Saudi Arabia leads at 39.7% through its largest GCC farmland base, Vision 2030 agricultural productivity investment programs, and government procurement of precision farming robot systems. UAE at 28.6% follows through smart greenhouse automation and National Food Security Strategy 2051 technology investment.

Leading companies include Deere & Company, DJI, Lely, GEA Group Aktiengesellschaft, Yanmar Holdings Co., Ltd., and others.

The GCC agricultural robots market is projected to reach approximately USD 486.1 Million by 2030, with autonomous UAV fleets becoming standard on commercial GCC farms, robotic dairy adoption reaching mainstream scale, and software and AI analytics platforms achieving high penetration across Saudi Arabia and UAE's digitised farm enterprises.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)