GCC Architectural Coatings Market Size, Share, Trends and Forecast by Technology, Resin, End User, and Country, 2026-2034

GCC Architectural Coatings Market Size, Share, Trends & Forecast (2026-2034)

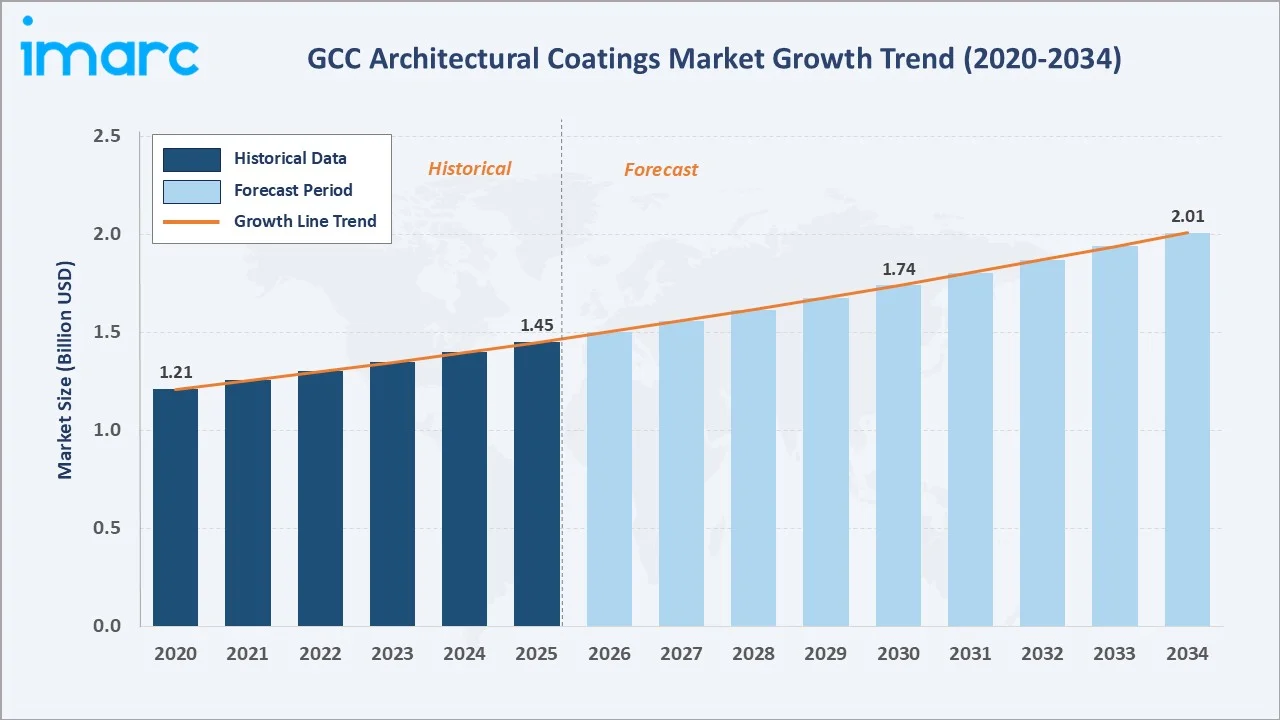

The GCC architectural coatings market reached USD 1.45 Billion in 2025 and is projected to reach USD 2.01 Billion by 2034, growing at a CAGR of 3.70% during 2026-2034. The market is driven by rising urbanization, large-scale construction projects under national Vision plans, stringent VOC regulations, and shifting preferences toward sustainable and waterborne coatings.

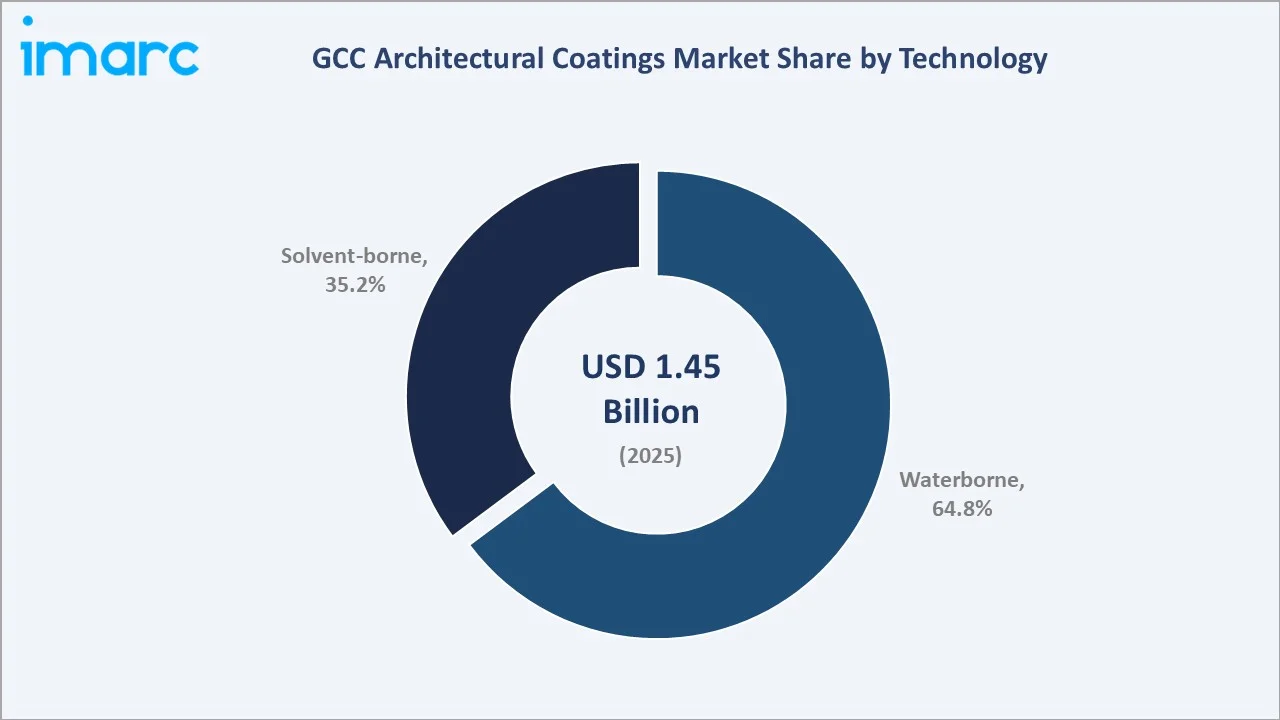

Waterborne technology dominates at 64.8% while commercial end users lead at 58.6%. Saudi Arabia commands 37.9% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.45 Billion |

|

Forecast Market Size (2034) |

USD 2.01 Billion |

|

CAGR (2026-2034) |

3.70% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Technology |

Waterborne (64.8%, 2025) |

|

Dominant End User |

Commercial (58.6%, 2025) |

|

Leading Country |

Saudi Arabia (37.9%, 2025) |

The GCC architectural coatings market expanded from USD 1.21 Billion in 2020 to USD 1.45 Billion in 2025, anchored at USD 1.74 Billion in 2030 and forecast to reach USD 2.01 Billion by 2034. Sustained growth is underpinned by mega-construction programs, Vision 2030 infrastructure spending, and the accelerating shift to low-VOC and waterborne coating solutions across the region.

To get more information on this market, Request Sample

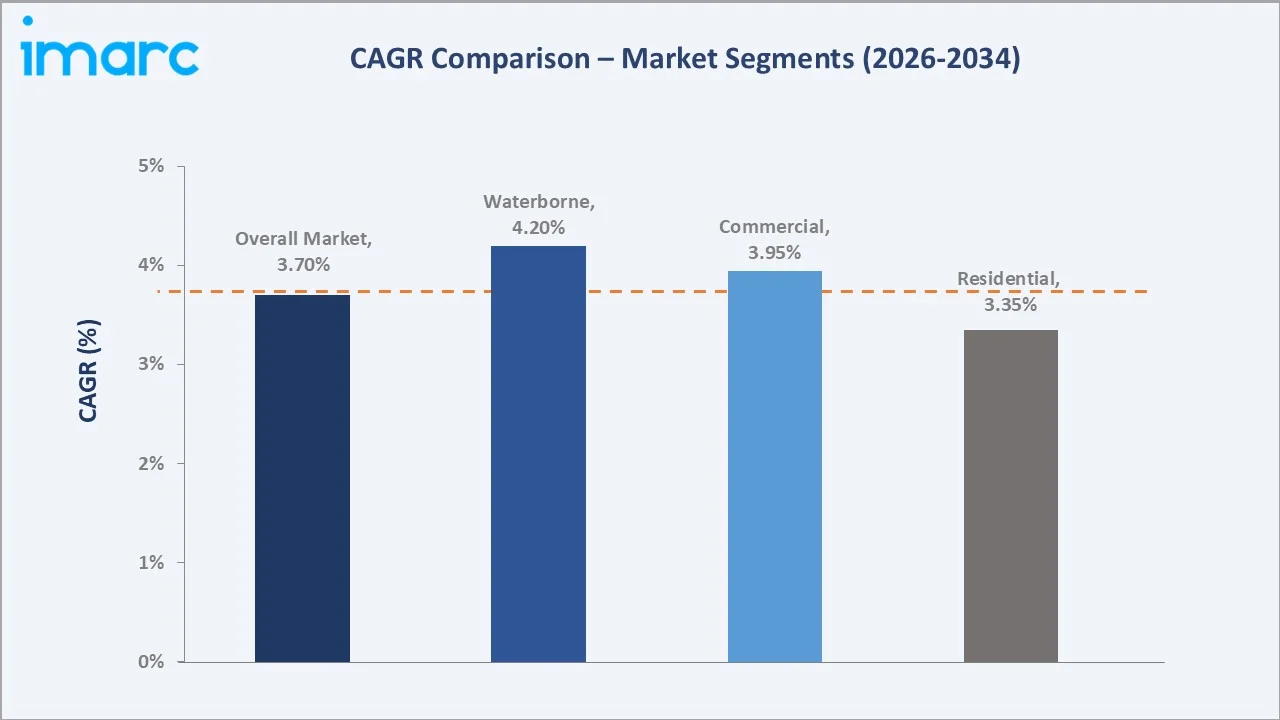

Waterborne technology grows at ~4.20% CAGR as regulatory mandates and growing environmental awareness push commercial and residential projects toward low-VOC formulations. Commercial end users, at 58.6%, drive the largest procurement volumes through ongoing hospitality, retail, and infrastructure developments across GCC nations.

Executive Summary

The GCC architectural coatings market reached USD 1.45 Billion in 2025, supported by an expanding construction and real estate base across Saudi Arabia, the UAE, Qatar, Kuwait, Oman, and Bahrain. Government-led diversification programs and ambitious urban development initiatives serve as the primary demand catalysts. The market is projected to reach USD 2.01 Billion by 2034.

Waterborne technology at 64.8% dominates as GCC authorities tighten VOC emission standards and green building certifications gain traction. Commercial end users at 58.6% lead through continuous demand from hospitality, commercial real estate, and infrastructure projects. Saudi Arabia at 37.9% leads regionally through Vision 2030 mega-projects and population-driven residential construction.

Key Market Insights

|

Insight |

Data |

|

Dominant Technology |

Waterborne – 64.8% share (2025) |

|

Dominant End User |

Commercial – 58.6% market share (2025) |

|

Leading Country |

Saudi Arabia – 37.9% market share (2025) |

|

Market Opportunity |

Sustainable coatings; nano-coatings; heat-reflective formulations; smart coating technologies |

Key Analytical Observations Supporting The Above Data:

- Waterborne at 64.8%: The waterborne technology segment dominates as stricter VOC regulations and growing green-building certifications across GCC push architects, contractors, and developers to prefer water-based coating solutions. Major real estate projects under Vision 2030 and UAE Net Zero 2050 are specifying compliant, eco-friendly formulations.

- Commercial at 58.6%: The commercial segment leads due to intense and continuous construction activity in hospitality, retail, office, and public infrastructure sectors. GCC nations host among the world's highest per-capita hotel developments, generating sustained demand for premium architectural coatings on interior and exterior surfaces.

- Saudi Arabia at 37.9%: Saudi Arabia leads the GCC market as the largest regional economy, with Vision 2030 driving unprecedented investment across NEOM, the Red Sea Project, Qiddiya, and Diriyah Gate, requiring large volumes of high-performance architectural coatings.

GCC Architectural Coatings Market Overview

The GCC architectural coatings market encompasses the formulation, manufacturing, and supply of all decorative and protective paints and coatings applied to buildings, infrastructure, and residential structures across Saudi Arabia, UAE, Qatar, Kuwait, Oman, and Bahrain.

The ecosystem integrates raw material suppliers, resin and pigment manufacturers, coating formulators, distributors, professional applicators, and regulatory bodies overseeing VOC standards and green building compliance. Macroeconomic factors include rising government infrastructure spending, population growth, tourism expansion, and national sustainability commitments.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

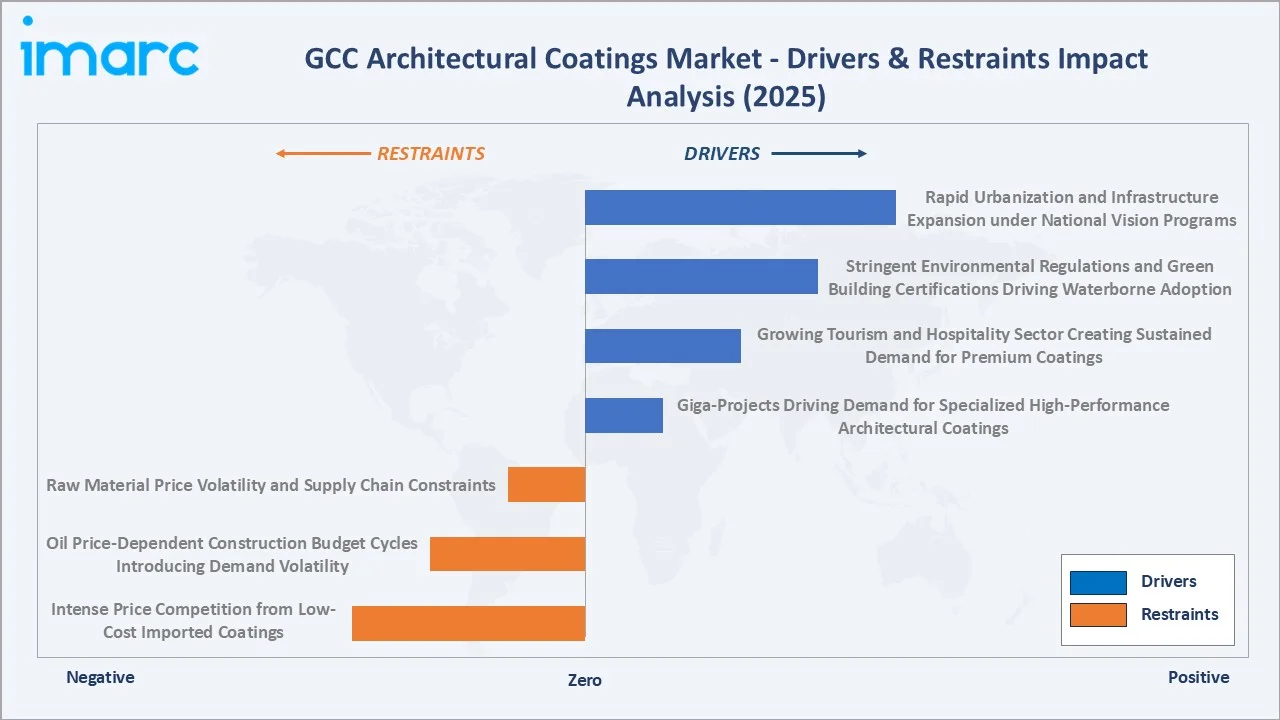

- Rapid Urbanization and Infrastructure Expansion under National Vision Programs: GCC governments are investing heavily in infrastructure under national Vision programs. Saudi Arabia's Vision 2030, UAE's centennial plan, and Qatar's post-World Cup development agenda drive continuous construction activity, directly increasing demand for architectural coatings across commercial and residential projects.

- Stringent Environmental Regulations and Green Building Certifications Driving Waterborne Adoption: GCC construction activity is shifting toward LEED, BREEAM, and Estidama-compliant projects. These certifications mandate low-VOC and eco-friendly coating formulations. The Green Building Council in the UAE and Saudi Arabia's sustainable construction code are enforcing waterborne adoption as a prerequisite for project approvals.

- Growing Tourism and Hospitality Sector Creating Sustained Demand for Premium Coatings: The rapid expansion of GCC hospitality portfolios, with Saudi Arabia targeting 150 million tourists annually by 2030 and Dubai sustaining its position as a global hospitality hub, drives high demand for premium interior and exterior architectural coatings in hotels, resorts, and entertainment complexes.

- Giga-Projects Driving Demand for Specialized High-Performance Architectural Coatings: Giga-projects such as NEOM, The Line, Red Sea Project, Qiddiya, and Diriyah Gate are creating unprecedented demand for specialized architectural coatings including heat-reflective, UV-resistant, and durable exterior coatings suited for extreme GCC climatic conditions.

Market Restraints

- Raw Material Price Volatility and Supply Chain Constraints: Architectural coatings raw materials including titanium dioxide, resins, and specialty additives are subject to global supply chain constraints and commodity price fluctuations, increasing manufacturing costs and compressing margins for coating producers across the GCC market.

- Intense Price Competition from Low-Cost Imported Coatings: Lower-priced coating products from Asian and South Asian manufacturers enter the GCC market through distributor networks, creating pricing pressure on established regional and international brands and limiting the ability to pass cost increases onto customers.

- Oil Price-Dependent Construction Budget Cycles Introducing Demand Volatility: Despite Vision 2030 ambitions, oil price cycles directly influence government construction budgets. Periods of reduced oil revenues can lead to project deferrals and slowdowns in new construction activity, creating demand volatility for architectural coatings suppliers.

Market Opportunities

- Smart and Functional Coating Technology Innovation: Smart coating technologies, including thermochromic, photocatalytic self-cleaning, and anti-microbial formulations, are gaining interest in GCC premium and healthcare construction, offering high-value growth avenues for innovative coating manufacturers.

- Heat-Reflective and Thermal Insulation Coatings for Net-Zero Building Compliance: The extreme GCC climate with temperatures exceeding 50°C creates a large addressable market for heat-reflective and thermal insulation coatings that reduce building energy consumption, aligned with regional net-zero commitments and mandatory green building codes.

Market Challenges

- Dominance of International Brands in Mega-Project Procurement Channels: Large-scale GCC projects engage global Tier-1 contractors who source coatings from approved global supplier lists, creating high barriers for regional manufacturers to access mega-project procurement channels dominated by established international brands.

- Skilled Applicator Workforce Shortage Limiting Premium Coating Adoption: Developing a sufficient pipeline of trained applicators and coating specialists for technically advanced formulations remains a workforce challenge, limiting adoption rates for premium and high-performance architectural coating products across the GCC.

Emerging Market Trends

1. Accelerating Adoption of Waterborne and Low-VOC Coatings under Green Regulatory Mandates

GCC environmental authorities are progressively lowering permissible VOC thresholds, aligning with European standards. This regulatory convergence is accelerating reformulation programs across coating manufacturers, driving both market composition shift toward waterborne and technology investment in water-based systems that match solvent-borne performance benchmarks.

2. Integration of Digital Color Visualization and Tinting Technology in Retail Distribution

GCC architectural coatings distributors are deploying in-store digital color visualization tools and automated tinting systems, enabling personalized and on-demand color matching for residential and commercial projects, improving purchase conversion and expanding value-added service revenues for retail distribution networks.

3. Rising Adoption of Self-Cleaning and Nano-Coating Technologies

Nano-coating formulations offering self-cleaning, anti-bacterial, and UV-resistant properties are gaining commercial traction in GCC premium construction. These coatings reduce long-term maintenance costs in the harsh regional climate, justifying higher price points and enabling manufacturers to capture premium margin above commodity coating products.

4. Localization of Architectural Coatings Manufacturing Under Industrial Policy Incentives

Saudi Arabia's National Industrial Development and Logistics Program (NIDLP) and the UAE's industrial strategy are incentivizing local coatings manufacturing through land allocation, tariff benefits, and government procurement preference, attracting international manufacturers to establish GCC production facilities.

Industry Value Chain Analysis

The GCC architectural coatings value chain integrates raw material sourcing, pigment and resin manufacturing, coating formulation and quality testing, packaging, distribution, professional application, and post-construction maintenance services.

|

Stage |

Key Participants |

|

Raw Material & Chemical Sourcing |

Procurement of key inputs including binders, resins, pigments, solvents, and specialty additives from global and regional suppliers |

|

Coating Formulation & Manufacturing |

Blending, processing, and quality testing of architectural coating formulations to meet VOC, performance, and environmental specifications |

|

Packaging & Quality Assurance |

Filling, packaging, and certification for compliance with GCC and international environmental and quality standards |

|

Distribution & Logistics |

Distribution through wholesalers, retail trade networks, project distributors, and direct supply channels to contractors |

|

Professional Application |

Application by trained contractors and decorators across residential, commercial, and infrastructure construction projects |

|

Aftersales & Maintenance |

Periodic recoating, touch-up services, and technical support for warranty compliance and long-term product performance assurance |

The raw material and chemical sourcing tier is the most cost-sensitive stage, as titanium dioxide and specialty resin prices significantly influence formulation costs and market pricing dynamics across the GCC. The distribution tier is the most commercially critical, where project-specific supply channels and trade distribution networks determine market access and volume share for coating manufacturers.

Technology Landscape in the GCC Architectural Coatings Industry

Waterborne Technology

Waterborne architectural coatings use water as the primary carrier instead of organic solvents, delivering significantly lower VOC emissions during application and drying. Advances in waterborne resin chemistry have narrowed the performance gap versus solvent-borne coatings, enabling waterborne systems to meet durability, adhesion, and sheen requirements for both interior and exterior GCC applications.

Solvent-borne Technology

Solvent-borne coatings offer superior adhesion, penetration, and durability in demanding applications including exterior metal structures, high-traffic floors, and industrial architectural finishes. Despite regulatory pressure and declining share, solvent-borne formulations retain a significant 35.2% market position for specialized applications where water-based alternatives have not yet achieved full performance equivalence.

Heat-Reflective and Cool Coating Technology

Heat-reflective coatings incorporating specialized pigments and IR-reflective technologies reduce roof and wall surface temperatures by reflecting solar radiation, lowering building energy consumption. These coatings are gaining adoption across GCC commercial and residential developments as energy efficiency requirements tighten under national net-zero commitments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

Waterborne |

64.8% |

2025 |

|

Resin |

🔒 |

🔒 |

2025 |

|

End User |

Commercial |

58.6% |

2025 |

|

Country |

Saudi Arabia |

37.9% |

2025 |

By Technology

Waterborne leads at 64.8% in 2025, reflecting accelerating regulatory-driven formulation shifts, green building certification requirements, and growing consumer environmental awareness across GCC residential and commercial segments.

To access detailed market analysis, Request Sample

Solvent-borne retains 35.2% through its performance advantages in specialized exterior, metal, and industrial architectural coating applications where waterborne alternatives have not yet fully displaced solvent-based systems. Regulatory timelines for solvent-borne restrictions vary by GCC country, sustaining near-term demand.

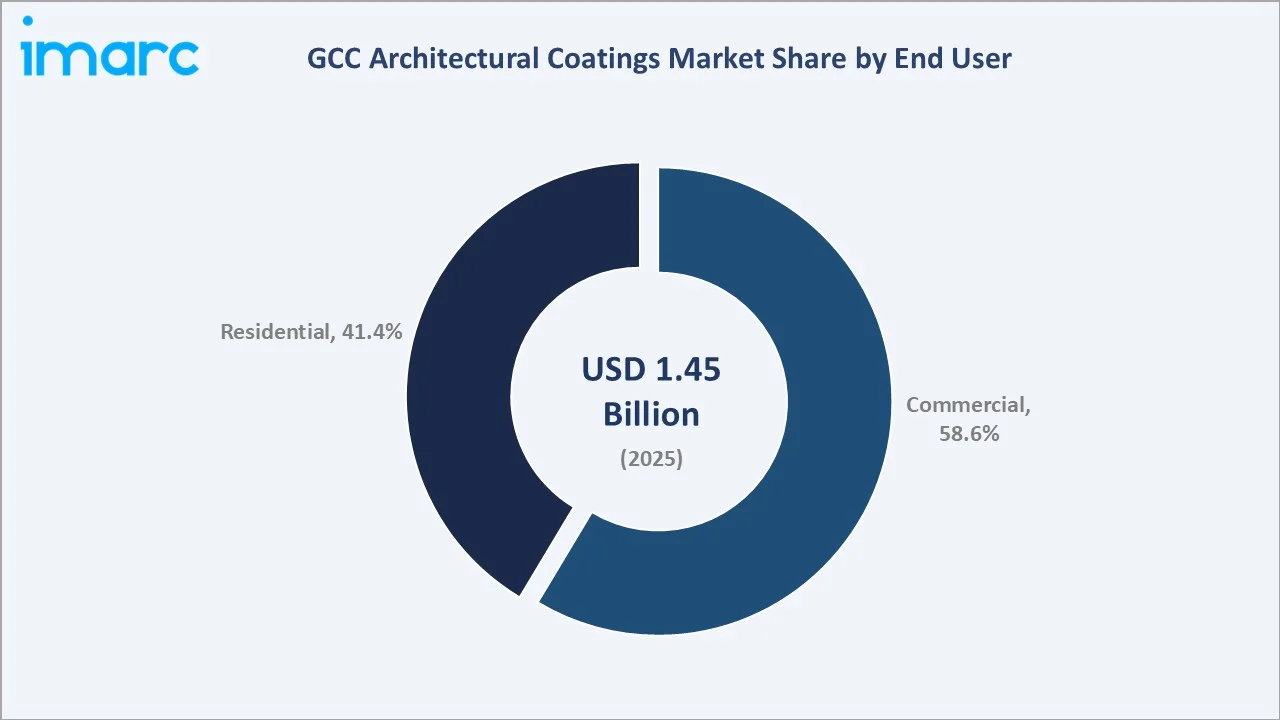

By End User

Commercial end users lead at 58.6% through continuous demand from hospitality, retail, office, healthcare, and infrastructure construction projects across GCC nations. GCC governments' aggressive tourism and economic diversification targets sustain elevated commercial construction activity through the forecast period.

Residential end users account for 41.4%, driven by population growth, affordable housing programs, and increasing urbanization across Saudi Arabia and the UAE. Government housing initiatives sustain residential painting demand across the GCC through the forecast period.

Regional Market Insights

|

Country |

Share (2025) |

Key Market Drivers & Characteristics |

|

Saudi Arabia |

37.9% |

Led by Vision 2030 mega-projects, growing hospitality sector, and government housing programs driving commercial and residential architectural coating demand |

|

UAE |

28.4% |

Driven by Dubai Expo legacy developments, Abu Dhabi urban expansion, and continuous premium commercial construction in tourism and retail sectors |

|

Qatar |

10.6% |

Post-FIFA World Cup infrastructure maintenance and Lusail City development sustaining architectural coating demand in commercial and institutional construction |

|

Kuwait |

8.7% |

Supported by Kuwait Vision 2035 infrastructure investments, government housing projects, and ongoing commercial construction activity |

|

Oman |

8.0% |

Driven by Oman Vision 2040 economic diversification, tourism infrastructure development, and growing residential construction in Muscat and Salalah |

|

Bahrain |

6.4% |

Supported by Bahrain Economic Vision 2030, commercial development projects, and ongoing residential housing activities in the Manama metropolitan area |

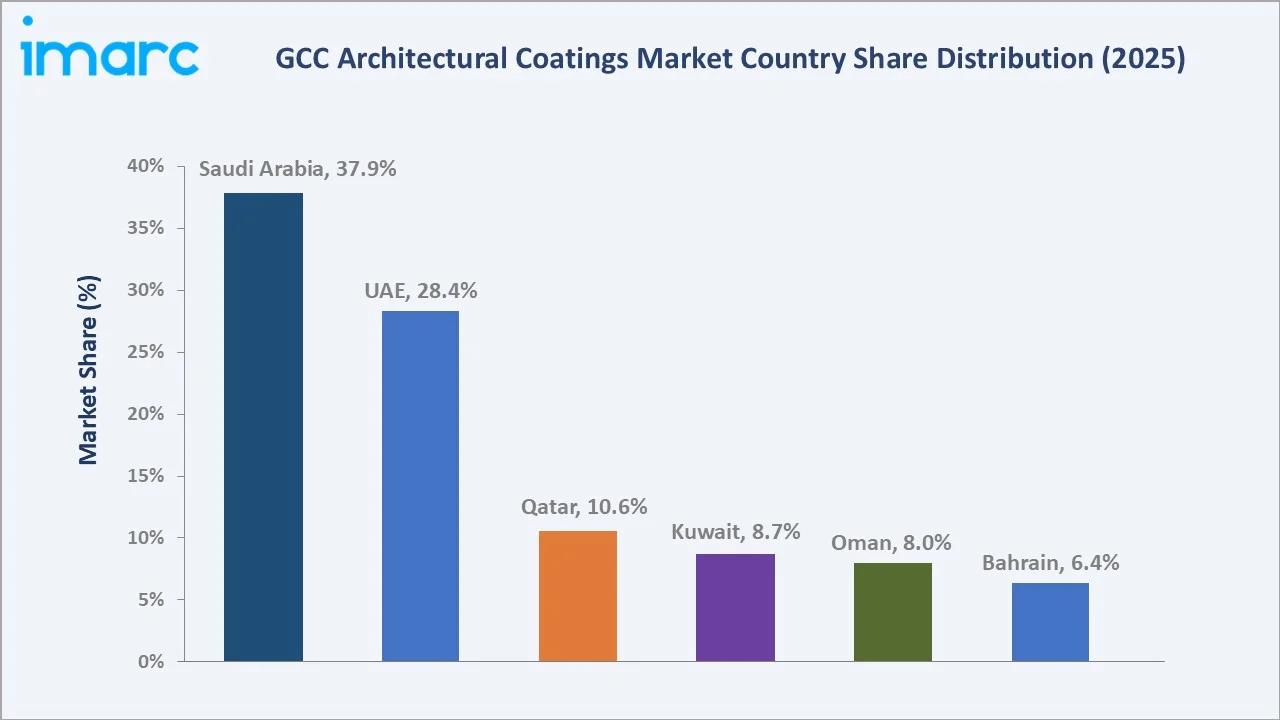

Saudi Arabia, at 37.9%, leads through Vision 2030 mega-projects including NEOM, the Red Sea Project, and Diriyah Gate requiring extensive high-performance architectural coatings across unprecedented construction volumes. UAE, at 28.4%, reflects sustained commercial premium construction and ongoing mixed-use development activity.

Qatar, at 10.6%, benefits from post-World Cup infrastructure maintenance and ongoing Lusail City commercial development. Kuwait at 8.7%, Oman at 8.0%, and Bahrain at 6.4% are growing markets driven by national Vision programs diversifying construction investment beyond oil sector revenues.

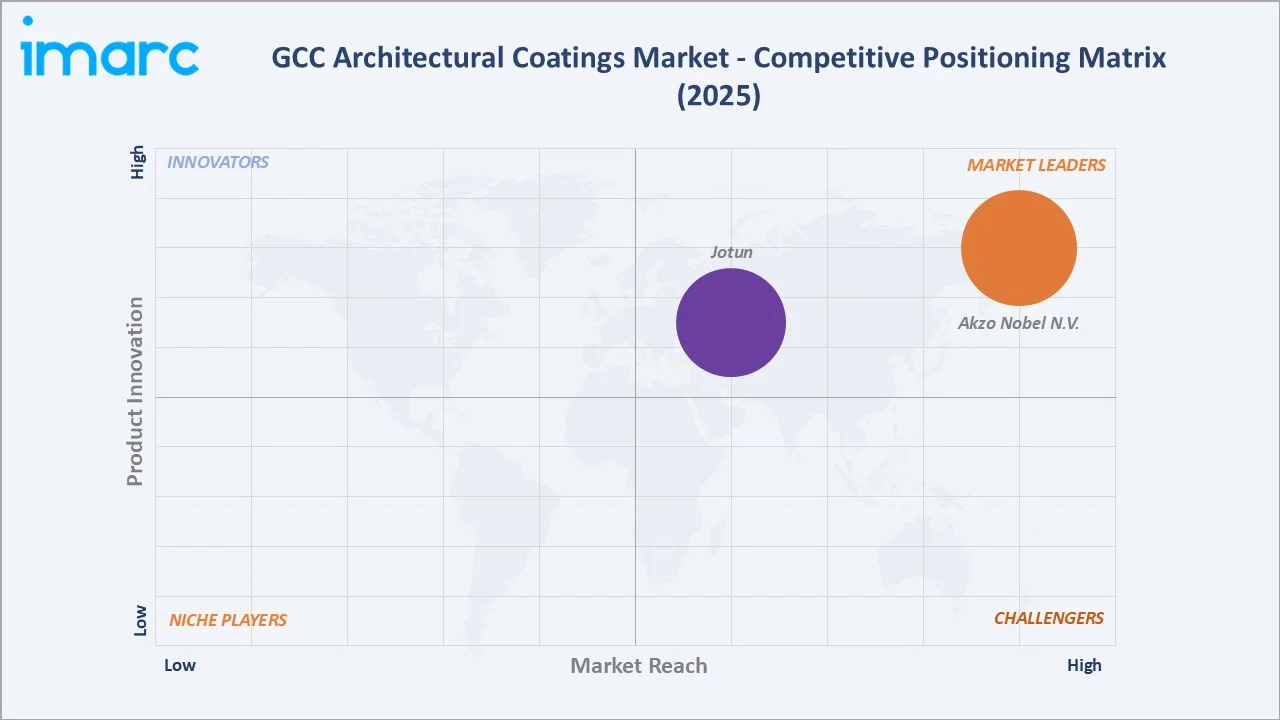

Competitive Landscape

The GCC architectural coatings market competitive landscape is moderately concentrated, with global multinational leaders, regional specialists, and local manufacturers competing across product, channel, and price dimensions. International brands dominate the premium and mega-project segments while regional players compete effectively in mid-market and residential channels.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Akzo Nobel N.V. |

Dulux, Sikkens, International Paints |

Market Leader |

Akzo Nobel leads through its Dulux premium brand, extensive GCC distribution network, and technical support for large-scale commercial and giga-project specifications. |

|

Jotun |

Jotaplast, Demidekk, Jotashield Extreme |

Market Leader |

Jotun holds strong regional presence through local manufacturing in Saudi Arabia and UAE, deep contractor relationships, and product lines tailored for GCC climatic conditions. |

Key players include Akzo Nobel N.V., Jotun, and others.

Key Company Profiles

Akzo Nobel N.V.

Akzo Nobel N.V. is a Netherlands-based multinational speciality chemicals and coatings company with a leading position in the GCC architectural coatings market through its Dulux, Sikkens, and International Paints brands, distributed and manufactured across the region.

- Key Products: Dulux WeatherShield, Dulux EasyCare, Sikkens Rubbol

- Strategic Focus: Expanding waterborne product portfolio, achieving low-VOC certification for GCC regulatory compliance, and deepening specifications in Vision 2030 mega-project procurement channels.

Jotun

Jotun is a Norway-headquartered global coatings manufacturer with one of the strongest GCC architectural coatings market positions, supported by local manufacturing plants in Saudi Arabia and the UAE, and a well-established regional brand presence across all six GCC countries.

- Key Products: Jotaplast, Demidekk, Jotashield Extreme

- Strategic Focus: Reinforcing GCC manufacturing footprint, expanding heat-reflective and sustainable coating product lines, and capturing specification share in Saudi Arabia Vision 2030 mega-project construction programs.

Market Concentration Analysis

The GCC architectural coatings market is moderately concentrated at the premium and commercial project level, with the top three key players collectively holding leading positions in commercial and mega-project specifications. Regional manufacturers including account for a significant share of mid-market and residential demand. Market concentration is expected to remain stable through the forecast period, with international brands retaining specification dominance while regional players strengthen in volume channels.

Investment & Growth Opportunities

Highest Growth Segments

Waterborne technology (~4.20% CAGR), commercial end user segment (~3.95% CAGR), heat-reflective specialty coatings (~6-8% CAGR from smaller base), Saudi Arabia market (~4.5% CAGR through Vision 2030 project pipeline), and nano-coating premium segment represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Saudi Arabia giga-projects represent the GCC architectural coatings market's highest absolute volume growth opportunity, with NEOM alone projected to require tens of millions of litres of specialized coatings. These projects demand advanced technical specifications, heat-reflective, UV-resistant, long-life formulations, at significant premium above standard architectural coatings.

Investment Themes

- GCC localization of architectural coatings manufacturing: National industrial policies incentivizing local production offer landed cost advantages, faster project supply logistics, and government procurement preference. International manufacturers establishing GCC production gain sustainable competitive advantages in project pricing and delivery against import-dependent competitors.

- Waterborne technology premium positioning: As regulatory timelines for VOC restriction tighten across GCC, manufacturers with certified waterborne product portfolios will capture the accelerating specification shift, particularly in commercial and mega-project segments where green building certification is becoming mandatory.

Future Market Outlook (2026-2034)

The GCC architectural coatings market is projected to grow from USD 1.45 Billion in 2025 to USD 2.01 Billion by 2034, delivering a 3.70% CAGR over the forecast period. The market anchor value of USD 1.74 Billion in 2030 represents a market at sustained structural expansion, underpinned by continuous Vision program construction activity, tourism infrastructure investment, and residential housing demand growth.

Three structural forces define market growth through 2034: the progressive buildout of giga-projects creating sustained high-volume coating demand through construction timelines extending into the early 2030s; the regulatory-driven technology shift from solvent-borne to waterborne formulations driving volume growth in premium and compliant product categories; and the residential construction wave tied to GCC population growth and urbanization creating a durable baseline demand floor beneath cyclical commercial project volumes.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders (2025), including Regional Architects and Project Specifiers; GCC Coatings Distributors and Retailers; Commercial Real Estate Developers; GCC Government Construction Agency Representatives; and Coating Application Contractors.

Secondary Research

Secondary research encompassed company annual reports; GCC Painting and Decoration Industry Association data; Saudi Vision 2030 project pipeline reports; UAE National Energy Strategy publications; Global VOC Regulation Monitor 2025; Architecture & Design Middle East market surveys; and regional construction market reports from MEED Projects and Construction Week GCC. Over 50 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts developed using a construction output-linked bottom-up model: (i) GCC construction output forecast by country and sector; (ii) architectural coatings consumption intensity per square metre by construction type; (iii) average price per litre by technology and end user segment; (iv) technology-shift adjustment for waterborne/solvent-borne migration over the forecast period; and (v) cross-validated against top-down macroeconomic GDP and construction investment indicators.

GCC Architectural Coatings Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Technologies Covered | Solvent-borne, Waterborne |

| Resins Covered | Acrylic, Alkyd, Epoxy, Polyester, Polyurethane, Others |

| End Users Covered | Commercial, Residential |

| Countries Covered | Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, Bahrain |

| Companies Covered | Akzo Nobel N.V., Jotun, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the GCC architectural coatings market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the GCC architectural coatings market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the GCC architectural coatings industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the GCC Architectural Coatings Market Report

The GCC architectural coatings market reached USD 1.45 Billion in 2025, driven by waterborne technology at 64.8%, commercial end user dominance at 58.6%, Saudi Arabia commanding 37.9% share, and large-scale construction across Vision 2030 giga-projects and regional tourism infrastructure development.

The GCC architectural coatings market grows at 3.70% CAGR during 2026-2034, reaching USD 2.01 Billion by 2034. This growth reflects sustained Vision program construction activity, waterborne technology adoption, tourism infrastructure investment, and residential housing demand across GCC nations.

Waterborne technology leads at 64.8%, driven by progressive VOC regulatory mandates, green building certification requirements, and growing environmental awareness among architects, developers, and end users across GCC commercial and residential construction projects.

Commercial end users lead at 58.6% through continuous hospitality, retail, office, healthcare, and infrastructure construction demand. GCC nations' aggressive tourism targets and economic diversification agendas sustain elevated commercial construction activity generating sustained architectural coatings procurement.

Saudi Arabia leads at 37.9% through the largest GCC economy, Vision 2030 mega-project pipeline including NEOM and the Red Sea Project, government housing programs, and the region's highest population base driving residential coating demand.

Leading companies include Akzo Nobel N.V., Jotun, and others.

The GCC architectural coatings market is projected to reach approximately USD 1.74 Billion by 2030, supported by advancing Vision 2030 giga-project construction, ongoing UAE and Qatar commercial development, waterborne technology adoption, and residential housing programs across GCC nations.

Three priority investment opportunities: GCC localization of architectural coatings manufacturing under industrial policy incentives, waterborne premium product portfolio development for green building compliance, and heat-reflective specialty coating technology for mega-project and net-zero building applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)