GCC Data Center Market Size, Share, Trends and Forecast by Application, Type, Component, Size, and Region, 2026-2034

GCC Data Center Market Size, Share, Trends & Forecast (2026-2034)

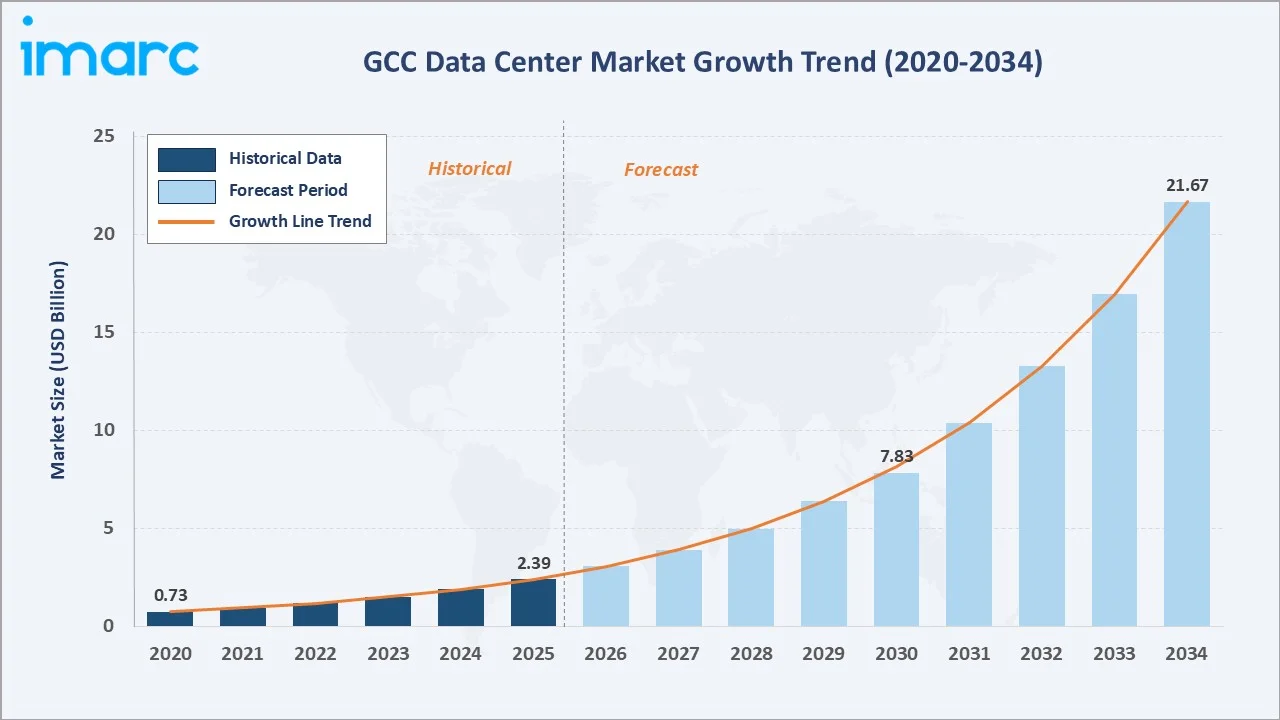

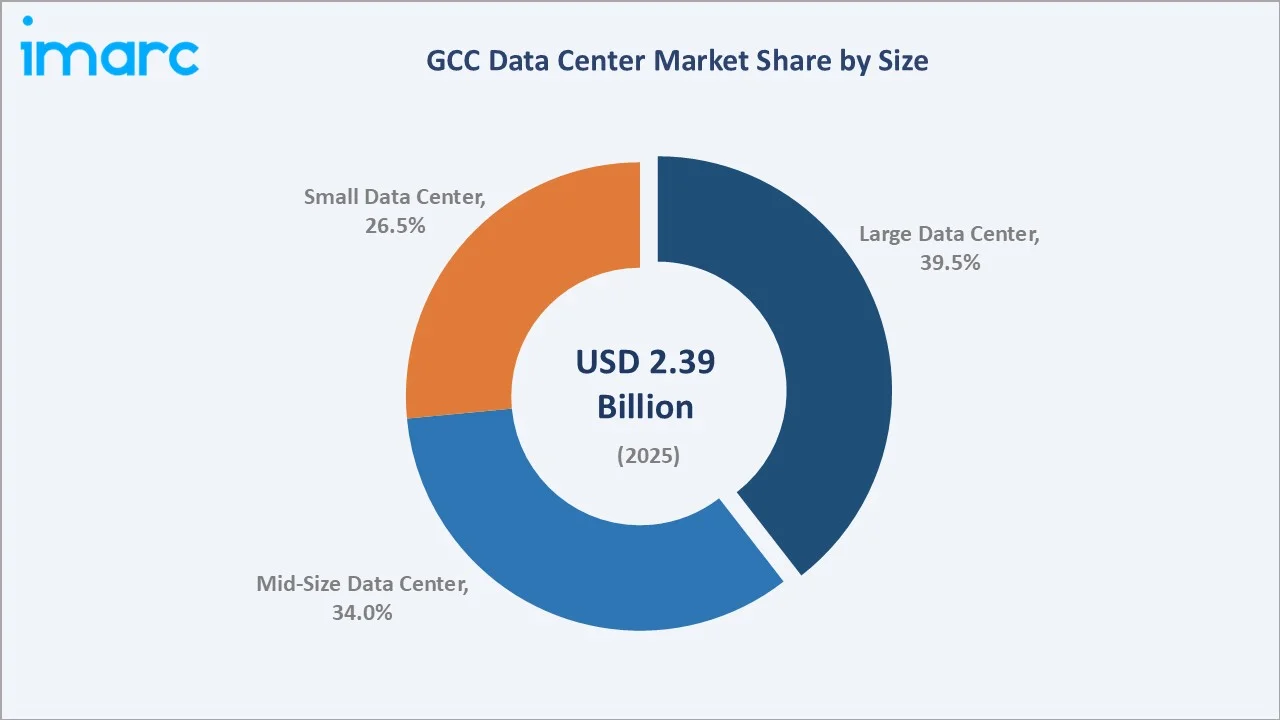

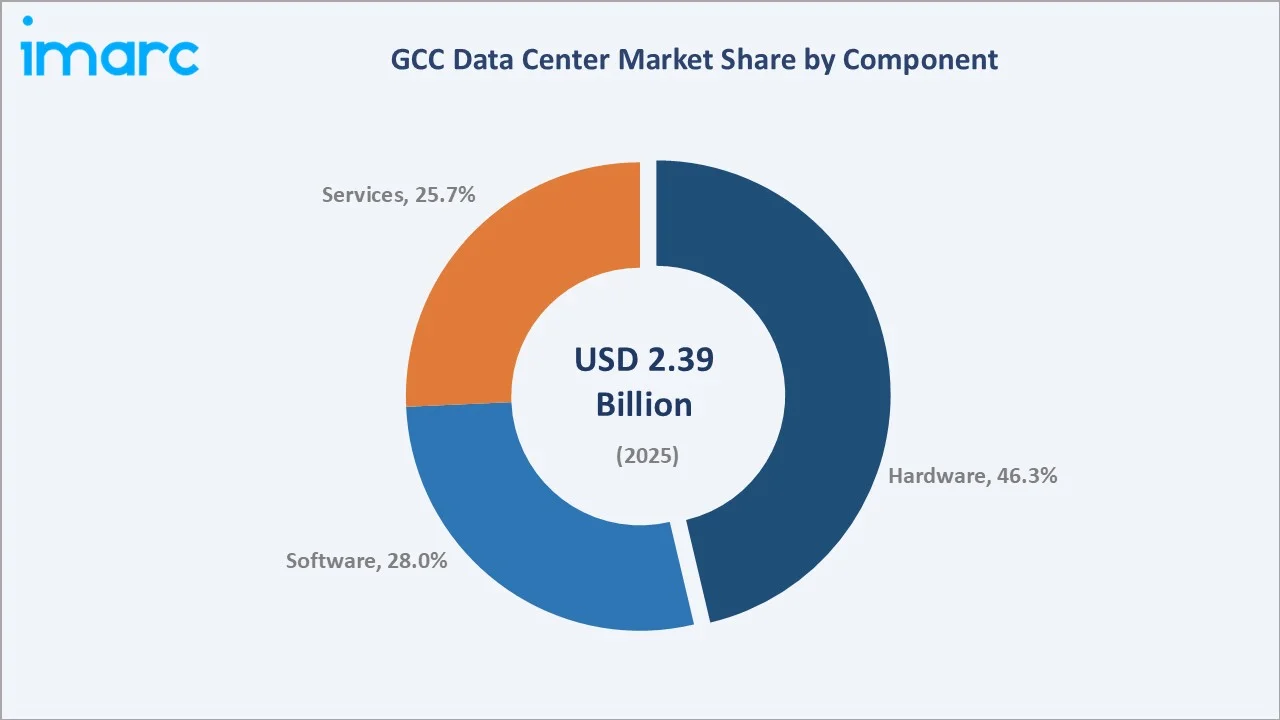

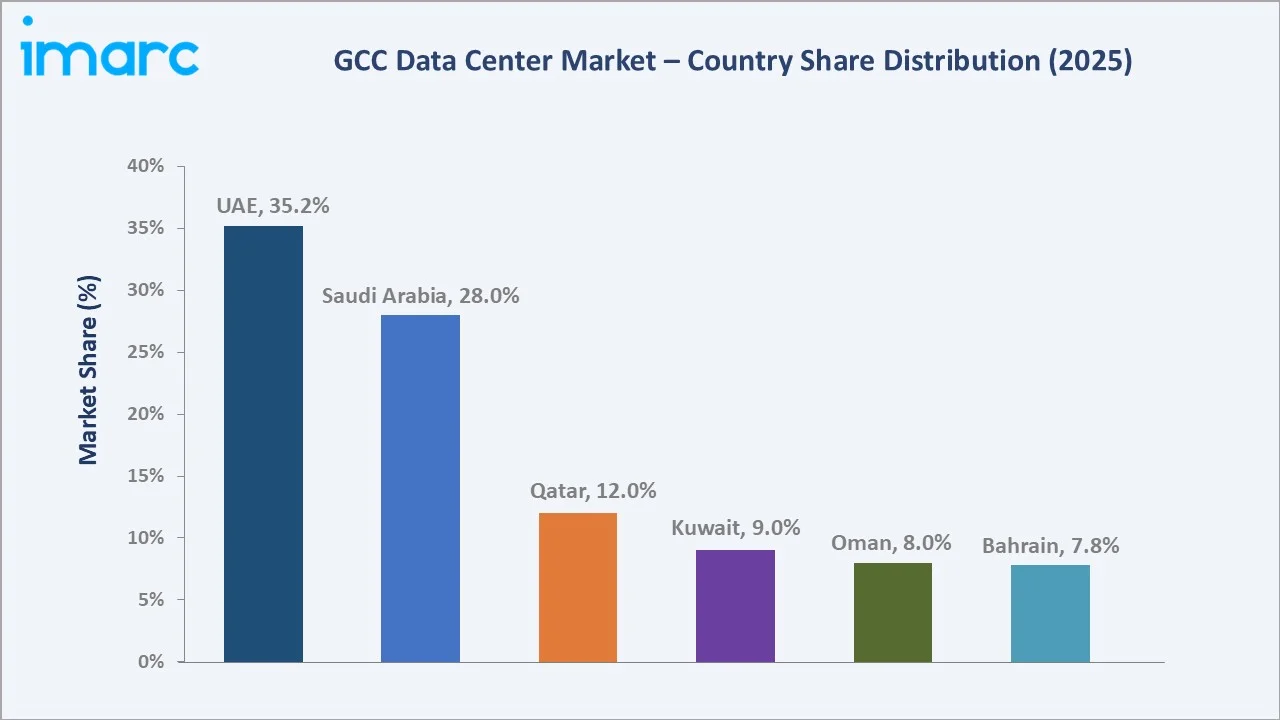

The GCC data center market size was valued at USD 2.39 Billion in 2025 and is projected to reach USD 21.67 Billion by 2034, exhibiting a CAGR of 26.78% during 2026-2034. Accelerating cloud migration, national digitalization programs, hyperscaler entry, and surging AI workload demand are collectively driving market growth. Among size segments, Large Data Centers held the leading 39.5% share in 2025, while Hardware dominated component revenue with 46.3%. The UAE led regional demand with a 35.2% share in 2025, supported by colocation capacity expansion, sovereign cloud initiatives, and rising enterprise digital adoption across the region.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.39 Billion |

|

Forecast Market Size (2034) |

USD 21.67 Billion |

|

CAGR (2026-2034) |

26.78% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

UAE (35.2% share, 2025) |

|

Fastest Growing Region |

Saudi Arabia |

|

Leading Size Segment |

Large Data Center (39.5%, 2025) |

|

Leading Component Segment |

Hardware (46.3%, 2025) |

The chart below illustrates GCC data center market growth from 2020 to 2034, reflecting accelerated capacity build-out after 2022 as hyperscalers entered the region.

To get more information on this market, Request Sample

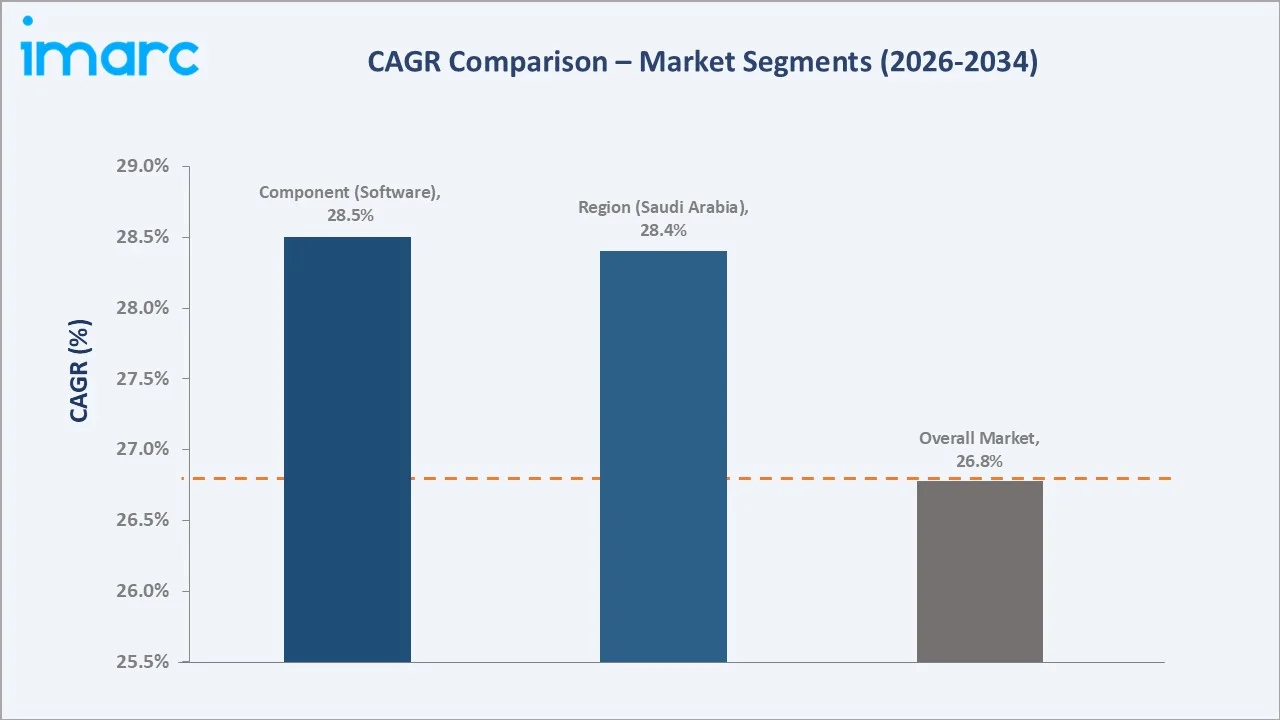

CAGR analysis indicates Software and Saudi Arabia as the fastest-growing sub-segments, reflecting sovereign cloud build-out and AI-driven platform demand through 2034.

Executive Summary

The GCC data center market is growing rapidly, driven by digital transformation, hyperscale cloud expansion, and rising enterprise demand. Valued at USD 2.39 Billion in 2025, the market is projected to reach USD 21.67 Billion by 2034 at a 26.78% CAGR. Government initiatives like UAE Vision 2031 and Saudi Vision 2030 are accelerating growth, with sovereign cloud, AI infrastructure, and data localization shaping capacity needs across the region.

Large data centers account for 39.5% share in 2025, driven by demand for high-density hyperscale facilities. Hardware dominates with 46.3%, supported by strong spending on servers, storage, and power systems. Key trends include liquid cooling for AI, edge deployments for 5G, renewable-powered campuses, and growing colocation JV investments in the UAE and Saudi Arabia.

The UAE leads with a 35.2% share (2025), driven by players like Equinix, Khazna, and Etisalat in Dubai and Abu Dhabi. Saudi Arabia follows at 28.0%, supported by investments in Riyadh, Jeddah, and NEOM, and is the fastest-growing market. Qatar (12.0%), Kuwait (9.0%), Oman (8.0%), and Bahrain (7.8%) hold the remaining share.

Key Market Insights

|

Insight |

Data |

|

Largest Size Segment |

Large Data Center – 39.5% share (2025) |

|

Second Size Segment |

Mid-Size Data Center – 34.0% share (2025) |

|

Leading Component |

Hardware – 46.3% share (2025) |

|

Second Component |

Software – 28.0% share (2025) |

|

Leading Region |

UAE – 35.2% revenue share (2025) |

|

Second Region |

Saudi Arabia – 28.0% revenue share (2025) |

|

Top Companies |

AWS, Equinix, Khazna, Microsoft |

Key Analytical Observations Supporting the Above Data:

- Large Data Centers' 39.5% dominance in 2025 reflects hyperscaler and enterprise preference for consolidated, high-density facilities that support cloud, AI, and enterprise workloads at lower unit cost.

- Mid-Size Data Centers, holding 34.0% in 2025, serve regional enterprise and government clients prioritizing flexibility, performance, and cost balance in their digital infrastructure investments.

- Hardware's 46.3% share in 2025 underscores high capex intensity, with servers, storage arrays, cooling systems, and power distribution units forming the bulk of investment in new facilities.

- Software at 28.0% in 2025 is expected to grow fastest, fueled by DCIM platforms, virtualization stacks, and AI-driven workload orchestration tools deployed across hyperscale and colocation sites.

- UAE's 35.2% lead in 2025 is anchored by Khazna's 300+ MW pipeline, Equinix's Dubai IBX facilities, and Microsoft and AWS cloud regions operating from Abu Dhabi and Dubai clusters.

- Saudi Arabia, as the fastest-growing market, is supported by NEOM Oxagon data hubs, STC's 300 MW Riyadh campus, and sovereign cloud frameworks aligned with Vision 2030 digital transformation targets.

GCC Data Center Market Overview

A data center is a facility that houses servers, storage, and networking systems to store, process, and deliver data for enterprise, cloud, and government use. In the GCC, the ecosystem includes hyperscale operators, colocation providers, telecom-led facilities, hardware OEMs, cooling specialists, and managed service providers.

Applications span BFSI, government, IT & telecom, media, retail, and manufacturing, with deployments from sovereign clouds to edge nodes. Growth is driven by national Vision programs, data localization laws, fiber and subsea expansion, 5G rollout, and increasing AI/ML adoption.

Market Dynamics

To evaluate market opportunities, Request Sample

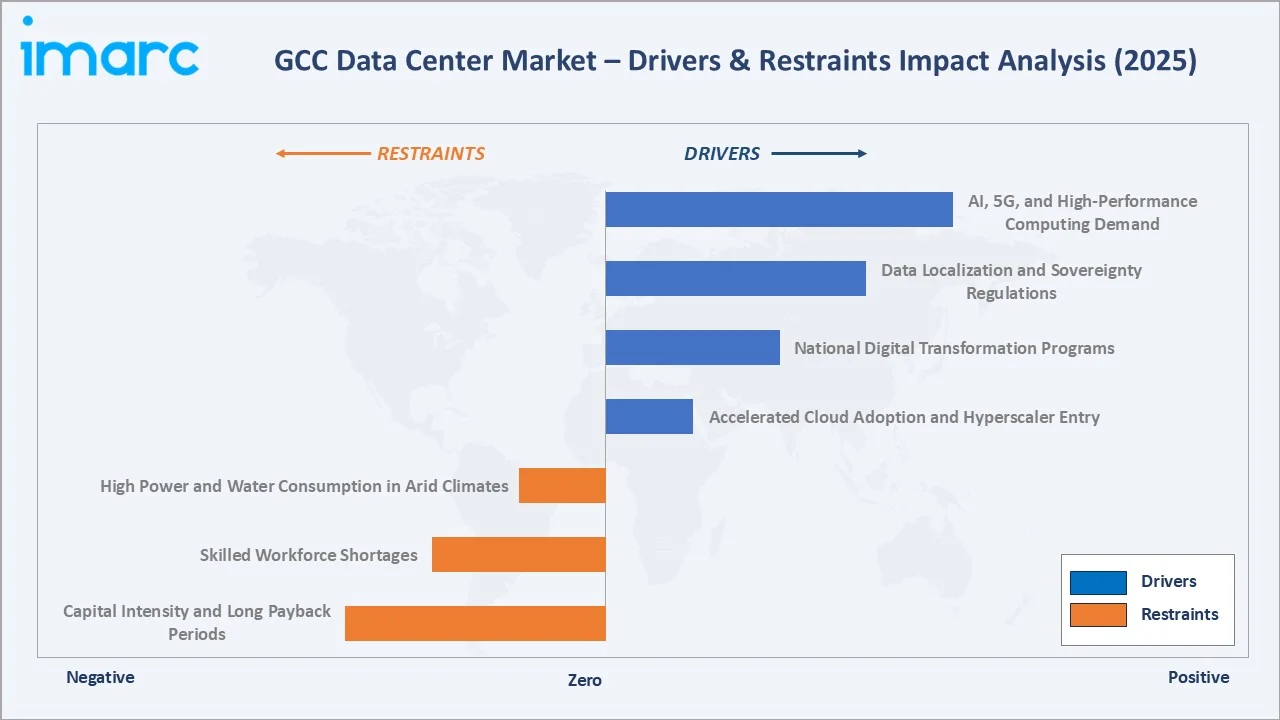

Market Drivers

- Accelerated Cloud Adoption and Hyperscaler Entry: Microsoft, Amazon Web Services, Oracle, and Google Cloud have established cloud regions in the UAE, Saudi Arabia, and Qatar since 2019, driving strong colocation demand and large-scale infrastructure investments across the GCC.

- National Digital Transformation Programs: Saudi Vision 2030, UAE Centennial 2071, Qatar National Vision 2030, and Oman Vision 2040 prioritize digital infrastructure. Government spending on e-services and AI platforms is a consistent demand driver.

- Data Localization and Sovereignty Regulations: Regulations such as Saudi Arabia’s PDPL, UAE’s PDPL, and Qatar’s data protection law mandate local data storage for sensitive information, encouraging domestic data center expansion and sovereign cloud collaborations.

- AI, 5G, and High-Performance Computing Demand: Rising adoption of AI and HPC workloads is increasing power density requirements in data centers, prompting upgrades such as advanced cooling systems and higher rack capacities across GCC facilities.

Market Restraints

- High Power and Water Consumption in Arid Climates: GCC data centers face high cooling demand due to extreme temperatures, increasing energy and water usage. Typical PUE levels in the region are often higher than global best-in-class benchmarks, raising operating costs and sustainability concerns.

- Skilled Workforce Shortages: The GCC faces a shortage of certified data center engineers, AI infrastructure specialists, and cybersecurity professionals, slowing facility commissioning and requiring reliance on expatriate hiring and training partnerships.

- Capital Intensity and Long Payback Periods: Data centers require significant upfront investment and long payback periods, limiting entry for smaller players and favouring large telecom operators, global colocation providers, and government-backed entities.

Market Opportunities

- AI-Ready Infrastructure Expansion: Saudi Arabia's PIF-backed HUMAIN is investing in AI compute platforms, while G42 in the UAE is scaling AI training campuses, opening a long runway for GPU-optimized colocation and wholesale capacity across the region.

- Edge Data Centers for 5G and IoT: GCC telecom operators, including e& and STC, are deploying edge sites in Tier-2 cities to support low-latency 5G, smart city, and autonomous mobility workloads tied to urban development programs.

- Renewable-Powered Sustainable Campuses: Solar-powered data centers at NEOM, Masdar City, and Duqm are attracting ESG-focused hyperscaler offtake agreements, creating a differentiated value proposition against traditional fossil-powered capacity.

Market Challenges

- Cybersecurity and Geopolitical Risk Exposure: The GCC is witnessing a rise in cyber threats targeting critical infrastructure, increasing the need for advanced security frameworks such as zero-trust architectures and sovereign cloud protections.

- Grid Reliability and Interconnection Bottlenecks: Rapid data center expansion is creating pressure on power infrastructure and connectivity networks in parts of the GCC, leading to delays in securing grid connections and scaling large facilities.

- Hardware Supply Chain Volatility: Global shortages of advanced GPUs and servers—particularly AI chips from NVIDIA—have increased lead times and constrained AI infrastructure deployment timelines for data center operators.

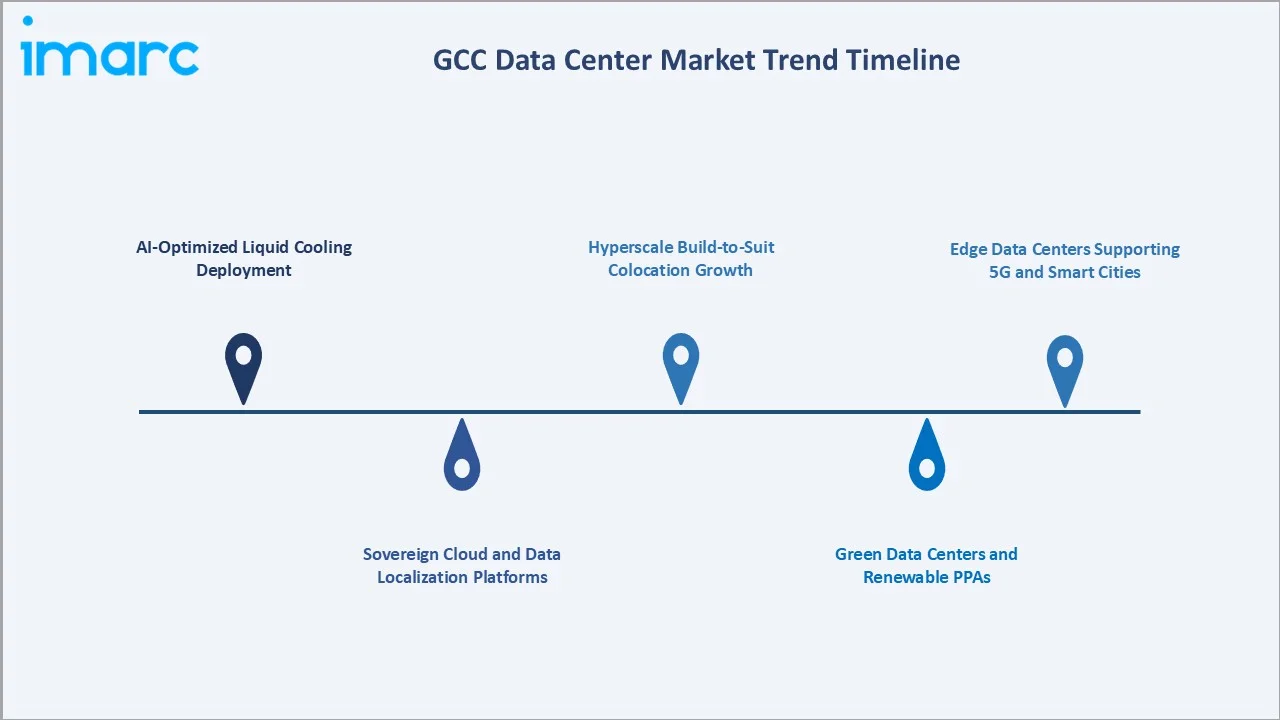

Emerging Market Trends

1. AI-Optimized Liquid Cooling Deployment

Deployment of direct liquid cooling is accelerating to support AI and HPC workloads. In 2024, Khazna and Hewlett Packard Enterprise launched UAE’s first liquid-cooled AI data center, improving energy efficiency versus air cooling.

2. Sovereign Cloud and Data Localization Platforms

Sovereign cloud adoption is rising as governments enforce data residency. Telecom operators are partnering with hyperscalers to deliver compliant cloud services for regulated sectors like BFSI and public sector.

3. Hyperscale Build-to-Suit Colocation Growth

Wholesale colocation tailored for hyperscalers is expanding rapidly. Khazna expanded its Abu Dhabi and Dubai campuses by over 100 MW in 2024, with dedicated halls serving AWS, Microsoft, and regional cloud partners under long-term leases.

4. Green Data Centers and Renewable PPAs

Operators are focusing on sustainability through energy-efficient designs and renewable integration, aligning with national net-zero strategies and reducing carbon footprint of data center operations.

5. Edge Data Centers Supporting 5G and Smart Cities

Edge data centers are expanding across GCC to support 5G, IoT, and smart city applications, enabling low-latency services for sectors like mobility, utilities, and public infrastructure.

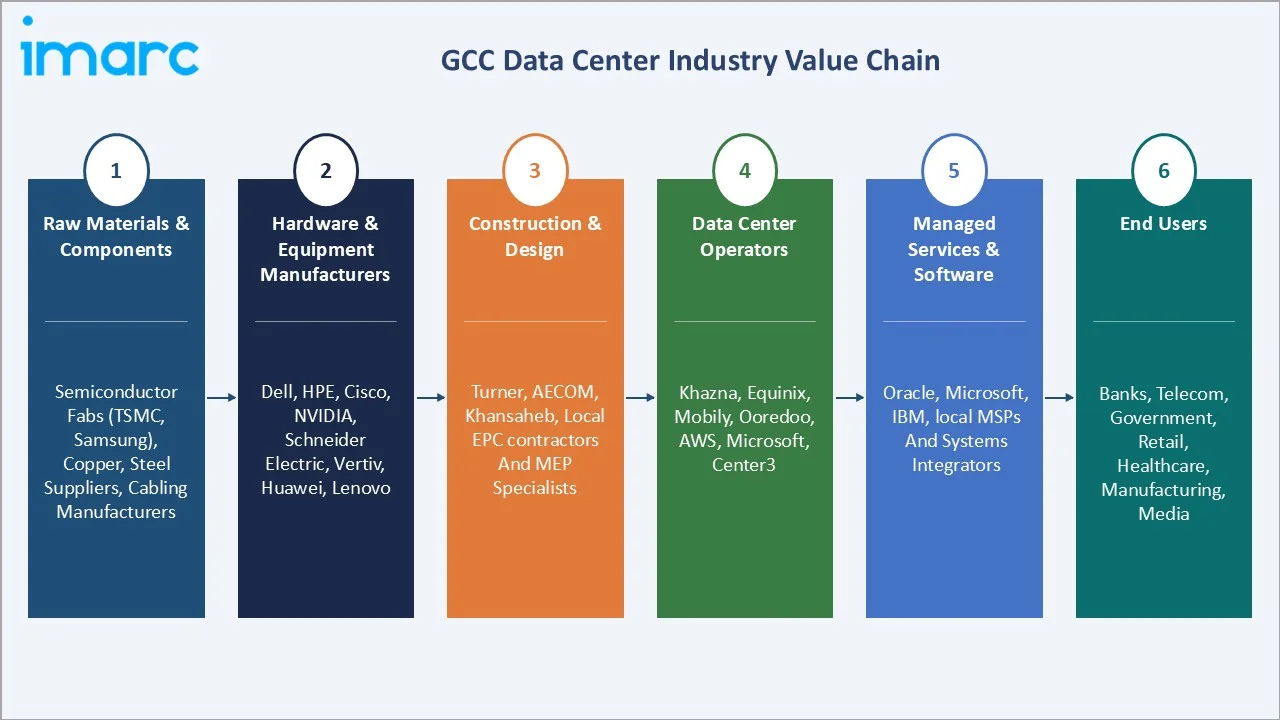

Industry Value Chain Analysis

The GCC data center value chain spans raw material suppliers, hardware manufacturers, facility operators, and end users, each with distinct margin profiles and competitive dynamics.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Semiconductor fabs (TSMC, Samsung), copper, steel suppliers, cabling manufacturers |

|

Hardware & Equipment Manufacturers |

Dell, HPE, Cisco, NVIDIA, Schneider Electric, Vertiv, Huawei, Lenovo |

|

Construction & Design |

Turner, AECOM, Khansaheb, local EPC contractors and MEP specialists |

|

Data Center Operators |

Khazna, Equinix, Mobily, Ooredoo, AWS, Microsoft, center3 |

|

Managed Services & Software |

Oracle, Microsoft, IBM, local MSPs and systems integrators |

|

End Users |

Banks, telecom, government, retail, healthcare, manufacturing, media |

Hardware OEMs and hyperscale operators capture the largest share of value due to scale, while local telecom-led operators benefit from sovereign contracts and incumbent network assets across the GCC data center market.

Technology Landscape in the GCC Data Center Industry

AI Infrastructure and GPU Clusters

GCC operators are expanding AI infrastructure with advanced GPU clusters. Firms like G42 are developing large-scale AI data centers in collaboration with NVIDIA to support regional AI workloads.

Advanced Cooling and Power Systems

Liquid cooling and advanced thermal management are gaining adoption to improve efficiency in high-density environments, particularly in hot climates, helping reduce energy consumption and enhance data center performance.

Automation, DCIM, and Smart Connectivity

Data Center Infrastructure Management platforms by Schneider Electric, Vertiv, and Nlyte are being adopted for real-time power, thermal, and workload monitoring, helping operators reduce downtime risk and improve operational efficiency across multi-site portfolios.

Sustainability and ESG Monitoring Platforms

Data center operators are integrating ESG monitoring tools to track energy, water, and emissions, aligning operations with sustainability targets and hyperscaler requirements across GCC markets.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Application | IT and Telecom | 38.5% | 2025 |

| Type | Colocation Data Centers | 42.4% | 2025 |

| Component | Hardware | 46.3% | 2025 |

| Size | Large Data Center | 39.5% | 2025 |

| Region | UAE | 35.2% | 2025 |

By Size

Large data centers hold a 39.5% share in 2025, driven by hyperscale cloud regions, sovereign cloud facilities, and build-to-suit colocation campuses supporting AI, cloud, and enterprise workloads at scale across UAE and Saudi Arabia.

To access detailed market analysis, Request Sample

Mid-Size data centers account for 34.0% in 2025, serving regional enterprise, BFSI, and government workloads where flexibility, compliance, and moderate scale outweigh the need for hyperscale deployment economics. Small Data Centers, holding 26.5% in 2025, support edge, branch, and Tier-2 city deployments, enabling low-latency connectivity for 5G, IoT, and smart city applications across the GCC.

By Component

Hardware commands 46.3% of the GCC data center market in 2025, reflecting heavy capex on servers, storage arrays, cooling, and power systems as hyperscalers, telecom operators, and enterprises commission new capacity across the region.

Software holds 28.0% in 2025, driven by virtualization, orchestration, DCIM, and AI workload platforms, and is the fastest-growing segment as operators enable multi-cloud and hybrid environments. Services account for 25.7%, covering design, integration, consulting, managed hosting, and support, with providers supporting sovereign cloud and AI infrastructure deployment.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

UAE |

35.2% |

Khazna and Equinix expansion, Microsoft and AWS cloud regions, G42 AI capacity, free zones, PDPL regulatory clarity |

|

Saudi Arabia |

28.0% |

Vision 2030, NEOM Oxagon, HUMAIN AI infrastructure, Google Cloud and Oracle regions |

|

Qatar |

12.0% |

Ooredoo-MEEZA colocation, 2022 World Cup digital legacy, Google Cloud Doha region, QNV 2030 digital transformation |

|

Kuwait |

9.0% |

Zain and Ooredoo edge deployments, banking sector modernization, Kuwait Vision 2035 digitalization agenda |

|

Oman |

8.0% |

Oman Data Park, Duqm and Salalah hubs, subsea cable landing points, Vision 2040 digital infrastructure focus |

|

Bahrain |

7.8% |

AWS Bahrain region since 2019, regulatory sandbox for fintech, Batelco colocation, Cloud First Policy |

The UAE commands a 35.2% regional revenue share in 2025, reflecting its role as the GCC's primary cloud and colocation hub. Dubai and Abu Dhabi host flagship facilities operated by Khazna, Equinix, and Microsoft, supported by the PDPL framework and investor-friendly free zone regulations.

Saudi Arabia holds 28.0% in 2025, leading growth driven by Vision 2030, AI investments, and sovereign cloud partnerships with Google, Oracle, and Microsoft. Qatar (12.0%) benefits from colocation and cloud expansion, while Kuwait (9.0%), Oman (8.0%), and Bahrain (7.8%) grow through sovereign and fintech-driven demand.

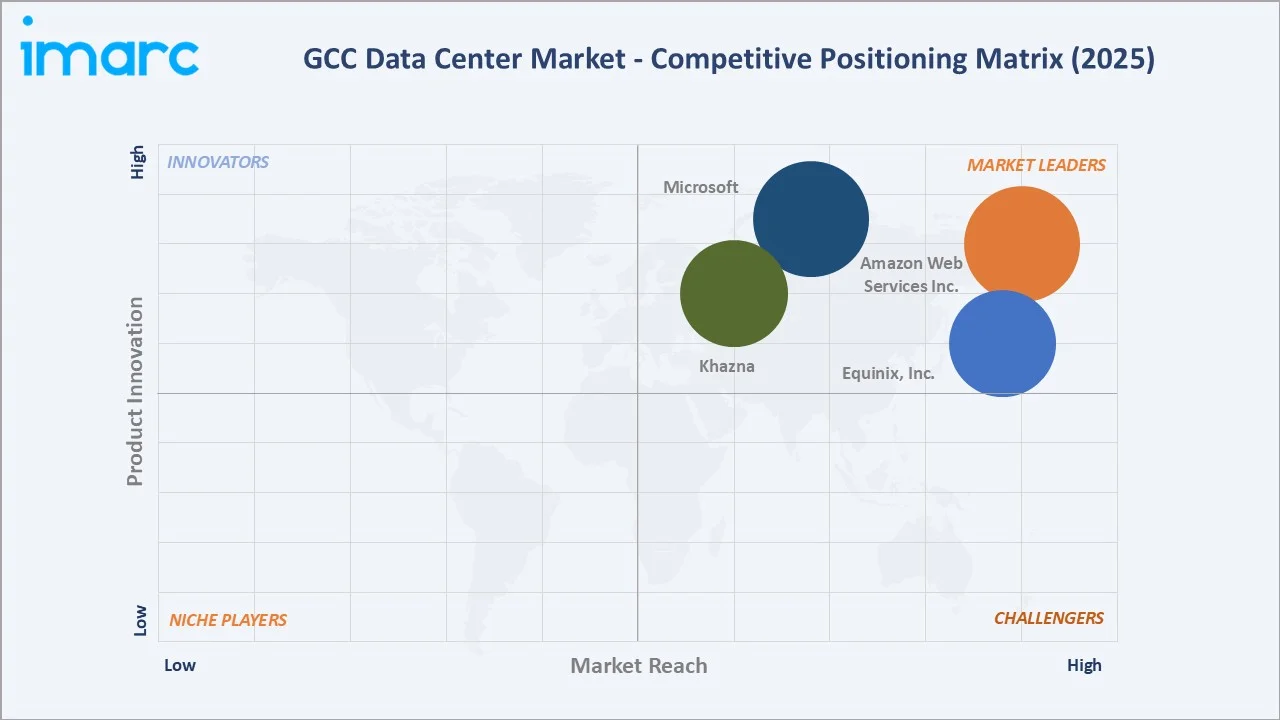

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Amazon Web Services, Inc. |

AWS |

Leader |

Global cloud scale, Bahrain and UAE regions, broad services |

|

Equinix, Inc. |

Equinix IBX® |

Leader |

Global colocation, Dubai, Abu Dhabi, Salalah and Muscat facilities, ecosystem density |

|

Microsoft |

Microsoft Azure |

Leader |

Sovereign cloud, AI and Copilot services, enterprise reach |

|

Khazna |

Khazna |

Leader |

UAE wholesale colocation, hyperscale build-to-suit |

The GCC data center market is led by a mix of global hyperscalers, regional colocation providers, and telecom-backed operators. Khazna stands as a leading player, with over 350 MW of operational capacity and total capacity exceeding 600 MW in the UAE, highlighting strong concentration of capacity among top-tier providers.

Key Company Profiles

Amazon Web Services, Inc.

Amazon Web Services, Inc. based in Seattle, operates cloud regions in Bahrain (2019) and the UAE (2022), serving GCC enterprises and governments. AWS continues expanding regional infrastructure, supported by strong global revenue growth and rising sovereign cloud and AI demand.

- Product & Service Portfolio: AWS provides compute (EC2), storage (S3), databases (RDS), AI/ML (SageMaker, Bedrock), hybrid solutions (Outposts), edge services (Local Zones), and sovereign/regulatory cloud offerings tailored for government and enterprise use.

- Recent Developments: In 2024, AWS announced a US$5.3 billion investment to launch a new cloud region in Saudi Arabia by 2026, expanding its GCC footprint and supporting digital transformation, AI adoption, and Vision 2030 initiatives.

- Strategic Focus: AWS prioritizes sovereign cloud infrastructure, generative AI deployment, public-sector partnerships, and regional capacity expansion to strengthen its leadership in the GCC digital and data center ecosystem.

Equinix, Inc.

Equinix, headquartered in Redwood City, operates a global platform of 260+ IBX data centers. In the GCC, it runs facilities in Dubai and Muscat, enabling regional interconnection, cloud access, and digital infrastructure growth, supported by strong global revenue performance.

- Product & Service Portfolio: Equinix offers colocation (IBX), interconnection via Equinix Fabric, Network Edge virtual networking, Equinix Metal bare-metal infrastructure, and multi-cloud connectivity through Cloud Exchange to major hyperscalers.

- Recent Developments: Equinix expanded its Muscat data center capacity and continued scaling its Dubai IBX footprint (DX1/DX2), strengthening Oman’s role as a subsea cable hub and enhancing interconnection capabilities across the GCC.

- Strategic Focus: Equinix focuses on carrier-neutral interconnection, multi-cloud ecosystems, AI-ready infrastructure, and sustainable data center expansion to strengthen its position as a regional digital connectivity hub in the GCC.

Microsoft

Microsoft, headquartered in Redmond, operates Azure cloud regions in the UAE (launched in 2019) with continued expansion across Abu Dhabi and Dubai. Its Intelligent Cloud segment drives growth, supported by rising Azure, AI, and sovereign cloud adoption across GCC markets.

- Product & Service Portfolio: Azure compute, storage, AI services, Microsoft 365, Dynamics 365, sovereign cloud offerings, and Copilot generative AI platforms.

- Recent Developments: In April 2024, Microsoft Corporation announced a US$1.5 billion investment in G42, acquiring a minority stake and board representation. The partnership enables G42 to run AI workloads on Microsoft Azure, strengthening AI infrastructure, sovereign cloud capabilities, and digital ecosystem growth in the UAE and broader GCC.

- Strategic Focus: Microsoft focuses on scaling AI-driven cloud infrastructure, sovereign cloud partnerships, and enterprise Copilot adoption while expanding regional data center capacity to support GCC digital transformation initiatives.

Market Concentration Analysis

The GCC data center market is moderately concentrated, with the top players – Khazna, AWS, Microsoft, and Equinix– collectively accounting for approximately 55–60% of total revenue in 2025. This concentration reflects the capital intensity of hyperscale and colocation infrastructure and the strategic role of telecom-backed operators in sovereign workloads.

Fragmentation increases at the mid-market and regional level, where Gulf Data Hub, MEEZA, Oman Data Park, and Batelco compete for enterprise, BFSI, and government colocation contracts. This creates a tiered structure where global leaders dominate wholesale hyperscale while regional players focus on retail and sovereign niches.

Consolidation trends are intensifying through sovereign and strategic investments. Microsoft's USD 1.5 Billion investment in G42 (2024) and Khazna's hyperscale joint ventures are reshaping the landscape, with sovereign wealth funds like PIF and Mubadala driving capacity build-out aligned with Vision 2030 and UAE Centennial 2071 priorities.

Investment & Growth Opportunities

Fastest-Growing Segments

AI-ready colocation and GPU-optimized capacity are among the fastest-growing segments in the GCC data center market, driven by rising AI workloads and hyperscaler demand. Advanced cooling (including liquid cooling) and high-density racks are increasingly adopted by operators such as Khazna Data Centers and G42.

Software and managed services are expanding faster than traditional hardware, supported by growth in virtualization, DCIM, and hybrid/multi-cloud deployments. Increasing adoption of sovereign cloud solutions is further accelerating this shift.

Emerging Market Expansion

Saudi Arabia is a major investment hub for data centers, supported by Vision 2030 and growing hyperscaler presence including Microsoft, Google Cloud, and Oracle. Large-scale investments have been announced, although exact cumulative values vary by source.

Oman and Bahrain are emerging as alternative hubs. Oman benefits from subsea cable connectivity and renewable energy potential, while Bahrain has strengthened its position through early cloud region launches such as Amazon Web Services in 2019 and a supportive fintech regulatory environment.

Venture & Strategic Investment Trends

Sovereign wealth funds, including PIF, Mubadala, and ADQ, are anchoring capital-intensive data center investments. Private equity firms including Brookfield and KKR have participated in MENA colocation platforms, while G42's AI and cloud ventures have attracted multi-billion-dollar strategic investments from Microsoft and other global technology partners.

Future Market Outlook (2026-2034)

The GCC data center market forecast projects sustained expansion from USD 2.39 Billion in 2025 to USD 21.67 Billion by 2034 at a CAGR of 26.78%, representing value growth of over USD 19 Billion. Growth will be powered by AI infrastructure, sovereign cloud, hyperscale colocation, and edge deployment aligned with national digitalization and smart city programs.

Three transformational shifts will reshape the market. First, AI-first design, with liquid-cooled, GPU-dense campuses becoming the standard for new capacity. Second, sovereign cloud regions expanding across all GCC states in partnership with global hyperscalers. Third, renewable-powered, sustainability-compliant facilities becoming a competitive necessity under ESG-driven procurement frameworks.

By 2034, the GCC is expected to emerge as a globally significant data center hub, supported by abundant capital, favorable regulation, and strategic geographic positioning between Europe, Africa, and South Asia. Operators investing in AI capacity, sovereign cloud, and sustaina` ṁ.ble infrastructure are expected to capture disproportionate value through the forecast period.

Research Methodology

Primary Research

Primary research included structured interviews and surveys conducted in 2024–2025 with GCC data center industry stakeholders including operations directors at Tier-1 colocation operators, CIOs at regional banks, government CTOs, hyperscaler regional leadership, and cooling and power equipment OEMs supplying the market.

Secondary Research

Secondary sources include company annual reports (AWS, Microsoft, Ooredoo, Equinix), regulatory publications (UAE TDRA, Saudi CST, Qatar CRA), trade associations (MENA Digital Group, DCD), sovereign investment fund disclosures, and industry trade media including Data Center Dynamics and Uptime Institute publications.

Forecasting Models

Market sizing and forecasts were developed using a combination of top-down and bottom-up models, incorporating IT workload growth, cloud penetration rates, facility capacity pipelines, sovereign investment commitments, and macroeconomic scenario analysis under base, optimistic, and conservative GDP and capex assumptions through 2034.

GCC Data Center Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | Banking Financial Services & Insurance (BFSI), Government, IT and Telecom, Media, Retail, Manufacturing, Others |

| Types Covered | Enterprise Data Centers, Colocation Data Centers, Edge Data Centers, Hyperscale Data Centers |

| Components Covered | Hardware, Software, Service |

| Sizes Covered | Small Data Center, Mid-size Data Center, Large Data Center |

| Regions Covered | Saudi Arabia, UAE, Qatar, Bahrain, Kuwait, Oman |

| Companies Covered | Amazon Web Services, Inc., Equinix, Inc., Microsoft, Khazna, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the GCC Data Center Market Report

The GCC data center market was valued at USD 2.39 Billion in 2025, driven by hyperscale cloud expansion, sovereign digitalization agendas, and rising enterprise and AI workload demand across the region.

The market is projected to reach USD 21.67 Billion by 2034, growing at a CAGR of 26.78% during 2026-2034, supported by AI infrastructure, sovereign cloud, and hyperscale build-out.

Large Data Centers lead with a 39.5% share in 2025, driven by hyperscaler cloud regions, sovereign facilities, and build-to-suit colocation campuses supporting AI and enterprise workloads.

Hardware dominates with 46.3% share in 2025, reflecting heavy capex on servers, storage, cooling, and power systems as new hyperscale and colocation capacity is commissioned.

The UAE leads with a 35.2% regional share in 2025, supported by Khazna, Equinix, Etisalat, and Microsoft and AWS cloud regions across Dubai and Abu Dhabi clusters.

Key drivers include cloud adoption, hyperscaler entry, data localization laws, Vision 2030 and 2071 programs, AI and 5G workload growth, and sovereign cloud partnerships.

Saudi Arabia is the fastest-growing market, supported by Vision 2030, HUMAIN AI investments, STC's Riyadh campus, and hyperscale cloud region commitments from Microsoft, Oracle, and Google.

Leading companies include Amazon Web Services, Inc., Equinix, Inc., Microsoft, Khazna, and others serving regional demand.

Mid-Size Data Centers hold a 34.0% share in 2025, serving regional enterprise, BFSI, and government workloads that require flexibility, compliance, and moderate operational scale.

Hyperscale colocation growth is driven by cloud region expansion, data localization, AI training capacity, and long-term build-to-suit leases signed by AWS, Microsoft, Google, and Oracle.

AI is driving adoption of liquid cooling, GPU clusters, and 80–120 kW per rack densities. Operators are retrofitting facilities and building new AI-optimized campuses to meet demand.

IT and Telecom, together with BFSI and Government, represent the largest application base, driven by cloud adoption, sovereign workloads, and regulated sector digital transformation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)