GCC Facility Management Market Size, Share, Trends and Forecast by Service, Mode of Facility, End User, and Country, 2026-2034

GCC Facility Management Market Size, Share, Trends & Forecast (2026-2034)

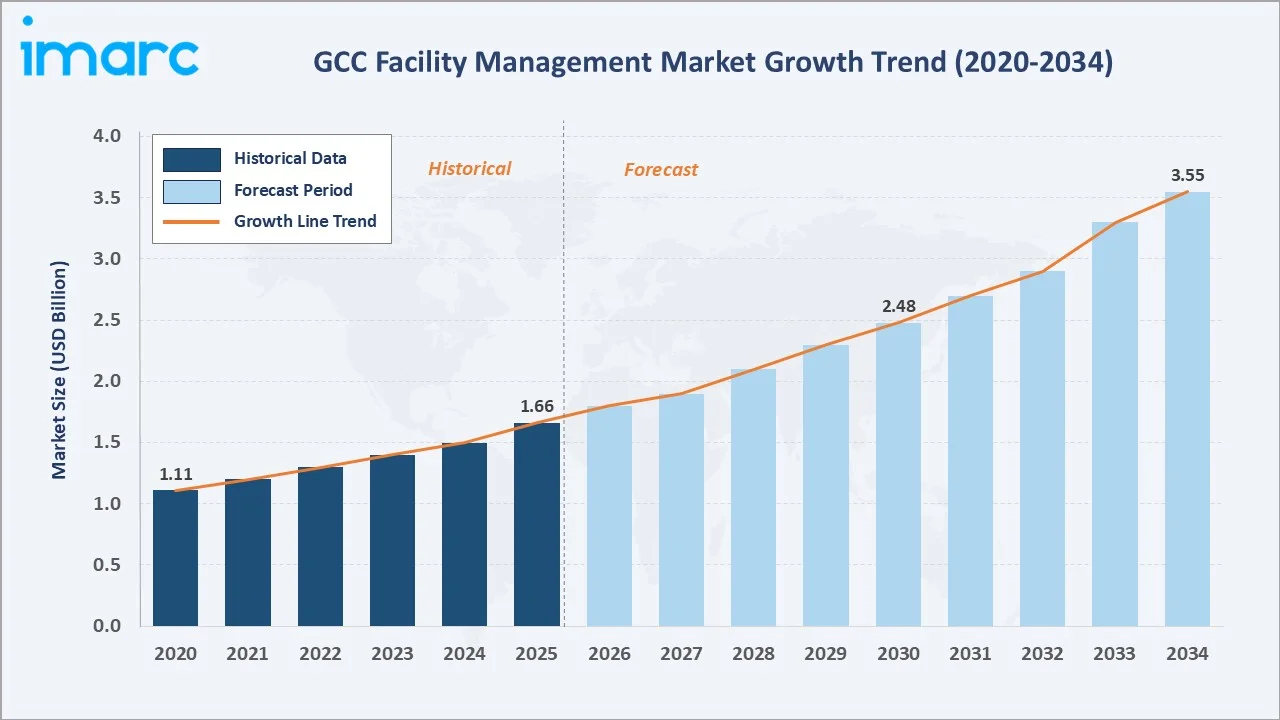

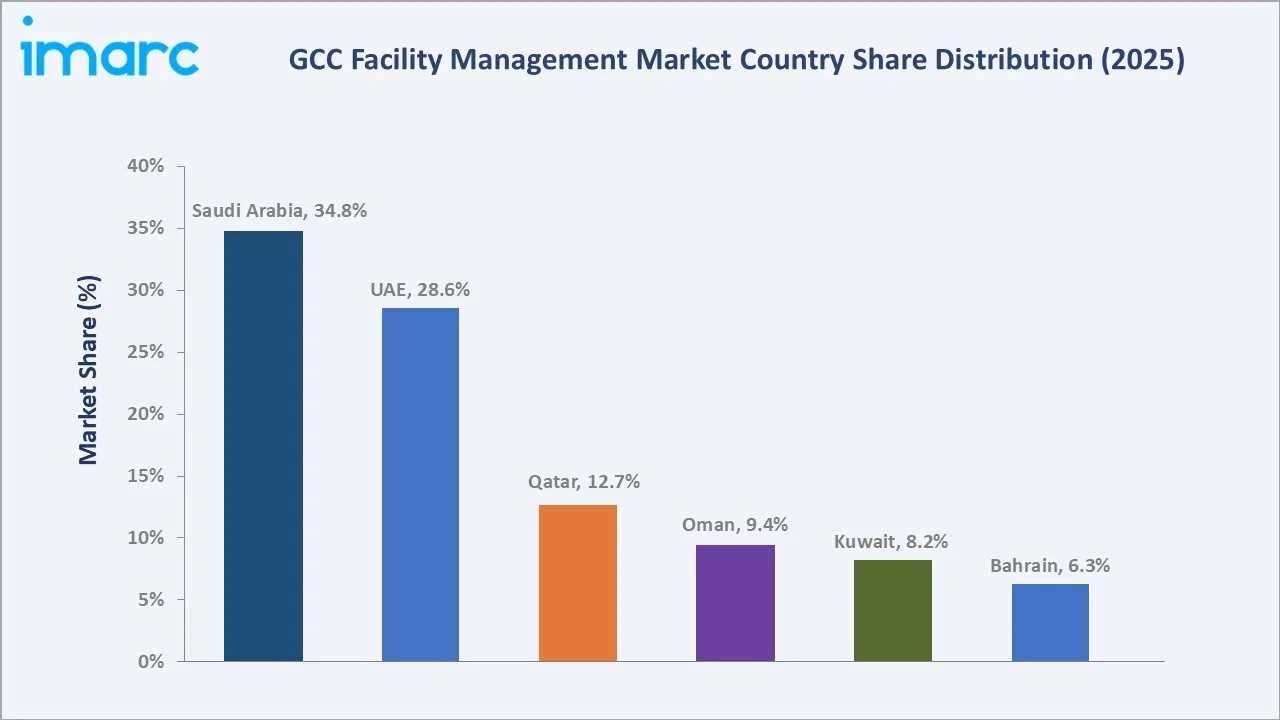

The GCC facility management market was valued at USD 1.66 Billion in 2025 and is projected to reach USD 3.55 Billion by 2034, expanding at a CAGR of 8.35% during 2026-2034. Growth is anchored by Vision 2030, driven by ambitious giga projects such as NEOM, Red Sea Project, and Qiddiya, rising outsourcing adoption for non-core operations, smart building technology integration, and rapid hospitality and commercial real estate expansion across the six GCC nations. Outsourced facility management dominates at 61.8%, commercial end users lead at 57.5%, and Saudi Arabia commands 34.8% of the regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.66 Billion |

|

Forecast Market Size (2034) |

USD 3.55 Billion |

|

CAGR (2026-2034) |

8.35% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Country |

Saudi Arabia (34.8%, 2025) |

|

Fastest Growing Country |

Qatar (CAGR ~9.2%, 2026-2034) |

The GCC facility management market growth grew from USD 1.11 Billion in 2020 to USD 1.66 Billion in 2025, demonstrating FM’s essential service classification. Anchored at USD 2.48 Billion in 2030, the forecast to USD 3.55 Billion by 2034.

To get more information on this market, Request Sample

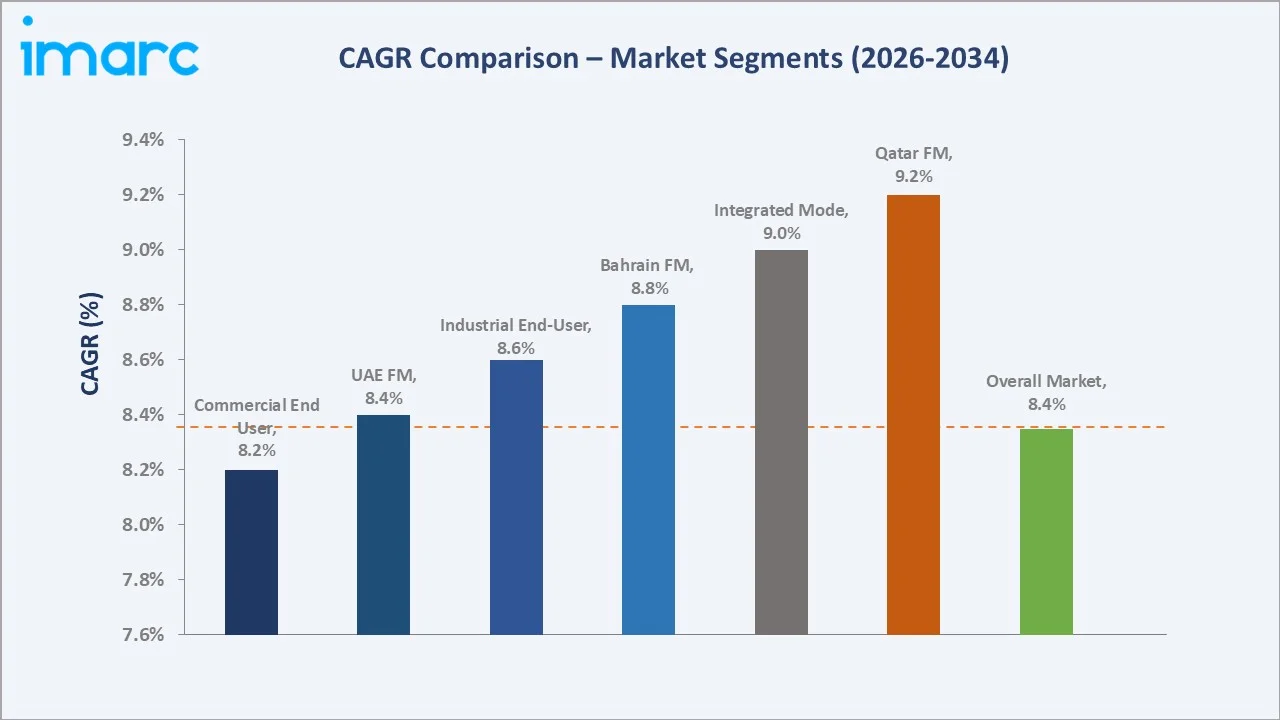

The CAGR across key segments with Qatar at ~9.2% CAGR grows fastest regionally, driven by post-FIFA World Cup 2022 legacy asset management and Lusail City commercial development. Integrated mode at ~9.0% CAGR reflects clients’ progressive consolidation of hard and soft FM into single IFM contracts, capturing cost synergies through unified service delivery.

Executive Summary

The GCC facility management market grew from USD 1.1 Billion in 2020 to USD 1.66 Billion in 2025, driven by a rapid post-pandemic recovery fueled by record government infrastructure spending and the GCC’s systematic transition from in-house to outsourced and integrated FM models as governments and corporations increasingly recognize FM as a specialist profession rather than an administrative function. Facility management in the GCC context encompasses the full spectrum of hard services, soft services, catering and hospitality services, energy management, and the overarching integrated and total facilities management models that bundle these services under a single contract and accountability structure.

Outsourced facility mode leads at 61.8% as GCC governments, private sector corporations, and real estate developers systematically transfer FM operations to specialist service providers under long-term performance-based contracts. Commercial end users lead at 57.5% through GCC’s extensive commercial office, retail, hospitality, and healthcare real estate portfolio. Saudi Arabia’s 34.8% dominance reflects the kingdom’s unmatched infrastructure investment pipeline.

Key Market Insights

|

Insight |

Data |

|

Dominant Mode of Facility |

Outsourced – 61.8% revenue share (2025) |

|

Dominant End User |

Commercial – 57.5% revenue share (2025) |

|

Leading Country |

Saudi Arabia – 34.8% share (2025) |

|

Fastest Growing Country |

Qatar (CAGR ~9.2%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Outsourced FM at 61.8% reflecting GCC’s structural outsourcing transition: GCC governments and corporations are in the midst of the most significant FM outsourcing transition in the region’s history, driven by Vision 2030’s efficiency and value-for-money mandates.

- Commercial end users at 57.5% driven by GCC’s commercial real estate boom: GCC’s commercial real estate pipeline is the world’s most active by value relative to GDP: Dubai’s development pipeline is set to deliver over 15.8 million sq. ft. of new office space by 2030, requiring high FM services.

- Saudi Arabia at 34.8% as GCC’s FM market growth anchor: Saudi Arabia is expected to invest $1 trillion in Infrastructure by 2030, creating the world’s largest single-country FM market development program in the world’s most concentrated geographic region.

GCC Facility Management Market Overview

Facility management (FM) in the GCC context encompasses the full spectrum of technical and soft services required to maintain, operate, and optimize the built environment across commercial, industrial, and residential asset classes. Hard FM services include HVAC (Heating, Ventilation, and Air Conditioning) maintenance, mechanical and electrical (M&E) maintenance, building management systems (BMS), fire protection, plumbing, structured cabling, and elevator maintenance.

Soft FM encompasses cleaning and janitorial services, security (manned guarding, CCTV, access control), landscaping and grounds maintenance, catering and hospitality services, pest control, and waste management. Environmental management FM (energy efficiency, carbon tracking, water management, sustainability reporting) is the fastest-growing FM service category, driven by Vision 2030’s UAE Net Zero 2050 and Saudi Green Initiative sustainability mandates.

The GCC FM market’s structural distinction from European and North American FM markets lies in three unique characteristics: the extreme heat making HVAC maintenance the dominant single hard service by contract value; the rapid pace of real estate development creating a continuous stream of new facility commissioning FM contracts; and the predominantly expatriate workforce creating unique labor management, visa processing, and training requirements that domestically-focused FM models in other regions do not encounter. Macroeconomic drivers include Vision 2030’s infrastructure investment, Saudi tourism economy targeting 150 million visitors by 2030, Green Building Regulations mandating energy-efficient FM operations, and the progressive shift from manual to digital FM operations through CAFM and IoT adoption.

Market Dynamics

To evaluate market opportunities, Request Sample

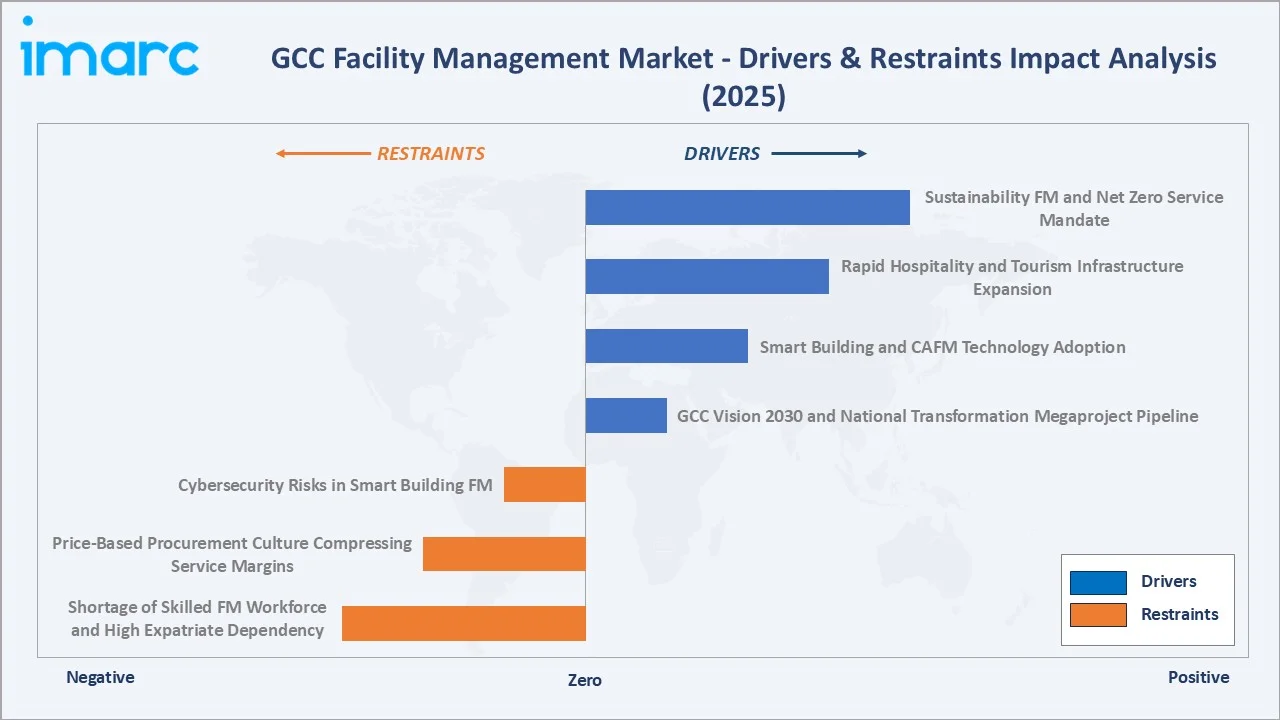

Market Drivers

- GCC Vision 2030 and National Transformation Megaproject Pipeline: Saudi Arabia’s Vision 2030 represents the world’s largest national transformation program with direct FM market implications: NEOM’s five regions (Sindalah, The Line, Oxagon, Trojena, and Magna) when fully operational require FM services; Red Sea Project’s luxury tourism infrastructure (50 resorts, 8,000 hotel rooms, 1,000 residential properties) requires world-class resort FM.

- Smart Building and CAFM Technology Adoption: GCC’s new real estate developments are being built with smart building infrastructure as standard, BMS (Building Management Systems), IoT-enabled MEP equipment, automated energy management, and digital twin building models, creating systematic demand for technology-enabled FM services that traditional in-house FM cannot competently deliver.

- Rapid Hospitality and Tourism Infrastructure Expansion: GCC’s tourism economy is the world’s fastest growing. Saudi Arabia’s tourism target of 150 million visitors by 2030 requires new hotel rooms and hospitality facilities with all-inclusive hospitality FM services.

Market Restraints

- Shortage of Skilled FM Workforce and High Expatriate Dependency: GCC’s FM sector faces an acute skilled workforce challenge: most of the GCC FM field staff are expatriate workers from South Asia, creating structural dependency on work visa processing, labor camp accommodation management, and annual leave rotation logistics that add to FM labor cost versus equivalent markets.

- Price-Based Procurement Culture Compressing Service Margins: GCC’s public sector FM procurement remains predominantly price-driven rather than value-driven: government tenders for FM contracts frequently award on lowest-price criteria, creating a race to the bottom where FM companies absorb labor cost increases to win contracts at unsustainable margins.

Market Opportunities

- Sustainability FM and Net Zero Service Mandate: UAE Net Zero 2050 and Saudi Arabia built environment targets to reduce carbon emissions by 278 mtpa by 2030, are creating a new FM service category: sustainability-focused FM with guaranteed energy performance contracts.

- Healthcare FM as GCC’s Highest-Value Specialist FM Segment: GCC’s healthcare infrastructure investment, the Saudi government plans to raise private sector involvement in the healthcare sector from 20% to 35% by 2030 through the privatization of 290 hospitals and 2,300 primary health centers, creates GCC’s fastest-growing FM service sub-segment.

Market Challenges

- Cybersecurity Risks in Smart Building FM: Progressive IoT-connected building system adoption creates expanding cybersecurity attack surfaces. GCC FM clients are imposing ISO 27001 certification, penetration testing, and data sovereignty restrictions that limit cloud deployment options and increase compliance costs for technology-deploying FM companies.

- Economic Cycle Vulnerability: Despite diversification, FM market demand remains sensitive to oil price cycles through public sector infrastructure investment budgets.

Emerging Market Trends

1. NEOM and Giga-Project FM: Creating the World’s Largest New FM Market

Saudi Arabia’s NEOM represents the world’s largest single FM opportunity in history: The Line accommodate 9 million people and built on a footprint of just 34 square kilometers, Sindalah’s 86-berth marina and 75 offshore buoys, Tropicana’s island entertainment destination, and NEOM’s industrial zone at Sharma collectively require high-demand FM services when fully operational by 2030–2035.

2. Integrated FM Model Replacing Fragmented Sub-Contracting

GCC’s FM market is experiencing a fundamental structural shift from fragmented sub-contracting to Integrated Facility Management. Qatar’s FIFA World Cup FM legacy contracts demonstrate GCC’s most significant institutional clients transitioning to IFM.

3. Sustainability FM and Green Building Certification Maintenance

GCC’s Green Building Regulations mandate ongoing certified energy performance from completed buildings, creating a new FM service category: Green Building Certification Maintenance.

4. FM Technology Platforms: CAFM-to-Digital-Twin Evolution

GCC’s FM technology landscape is evolving from CAFM (Computer-Aided Facility Management) toward integrated Digital Twin FM platforms where real-time sensor data from building IoT networks creates a live virtual model of building performance that FM teams use for predictive intervention.

Industry Value Chain Analysis

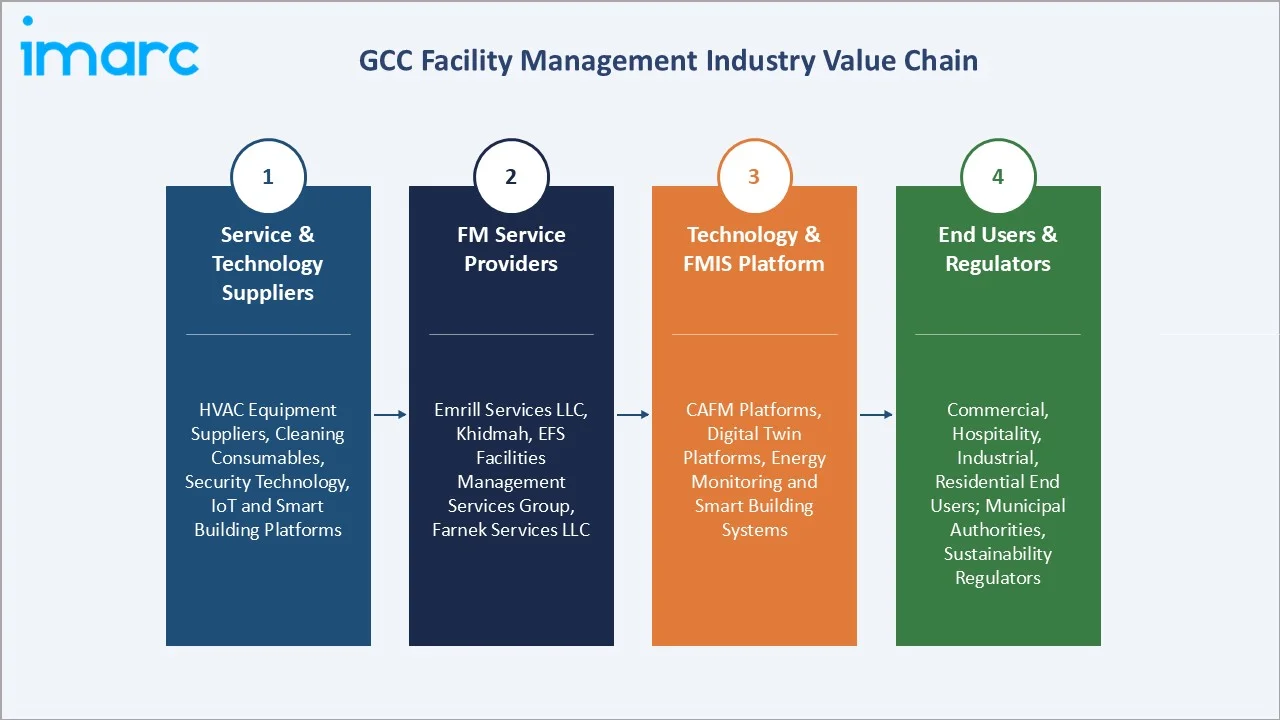

The GCC facility management value chain integrates technology and equipment suppliers, FM service providers, specialist sub-contractors, FM technology platforms, and end-user clients under a regulatory framework of municipal authorities, sustainability certifiers, and national standards bodies.

|

Stage |

Key Participants |

|

Service & Technology Suppliers |

HVAC equipment suppliers; cleaning consumables and equipment; security technology; IoT and smart building platforms; energy management |

|

FM Service Providers |

Emrill Services LLC, Khidmah, EFS Facilities Management Services Group, Farnek Services LLC |

|

Technology & FMIS Platform |

Computer-Aided Facility Management (CAFM) platforms, digital twin platforms, and energy monitoring |

|

End Users & Regulators |

Commercial end users, Hospitality, Industrial, Residential, Sustainability Regulators |

FM service providers capture 35‐45% of total value chain revenue through contract margin on direct labor and overhead. Technology and platform subscription services represent a growing 8‐12% revenue layer as CAFM and IoT platform adoption accelerates. The value chain’s highest-margin tier is the integrated digital FM platform provider role, where predictive analytics and AI capability command 25‐35% gross margins versus 5‐12% for traditional labor-intensive FM service delivery.

Technology Landscape in the GCC Facility Management Industry

CAFM and Work Order Management Platforms

Computer-Aided Facility Management (CAFM) systems digitize FM operations through centralized work order management, preventive maintenance scheduling, asset lifecycle tracking, and service level agreement (SLA) compliance monitoring.

IoT and Building Management System Integration

GCC’s smart building infrastructure generates continuous operational data from 10,000–100,000 sensors per major commercial building, covering HVAC performance, energy consumption, occupancy patterns, and equipment health parameters.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Service | 🔒 | 🔒 | 2025 |

| Mode of Facility | Outsourced | 61.8% | 2025 |

| End User | Commercial | 57.5% | 2025 |

| Country | Saudi Arabia | 34.8% | 2025 |

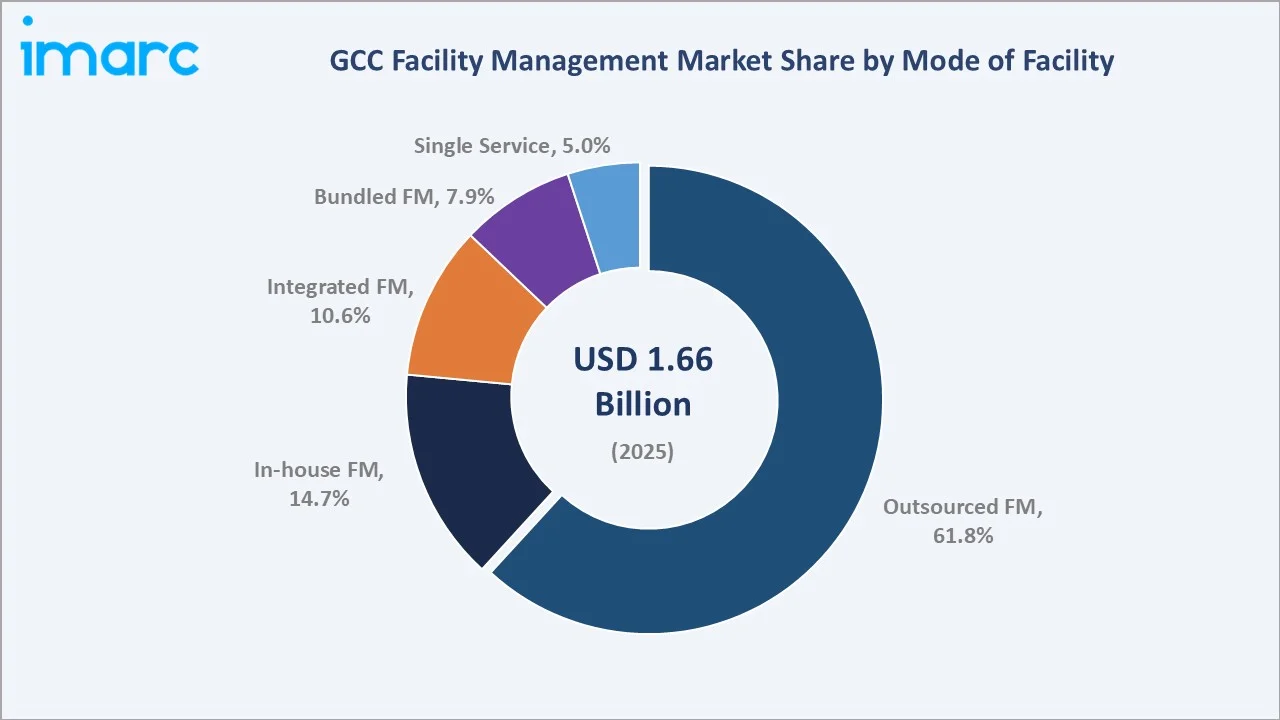

By Mode of Facility

Outsourced FM leads at 61.8% as the dominant mode across all GCC countries and end-user sectors. GCC’s outsourced FM market encompasses total facilities management (TFM) mega-contracts, integrated FM contracts, and single-service outsourced contracts.

To access detailed market analysis, Request Sample

In-house FM at 14.7% persists primarily in government entities and family-owned industrial businesses where FM is a politically sensitive employee base rather than a commercial decision. Integrated FM at 10.6%, the fastest-growing mode, represents long-term contracts (10–25 years) where a single FM company delivers all hard and soft services. Bundled FM at 7.9% represents groupings of 2–3 related services (cleaning+security+landscaping) under a single provider. Single service at 5.0% captures specialist single-discipline contracts.

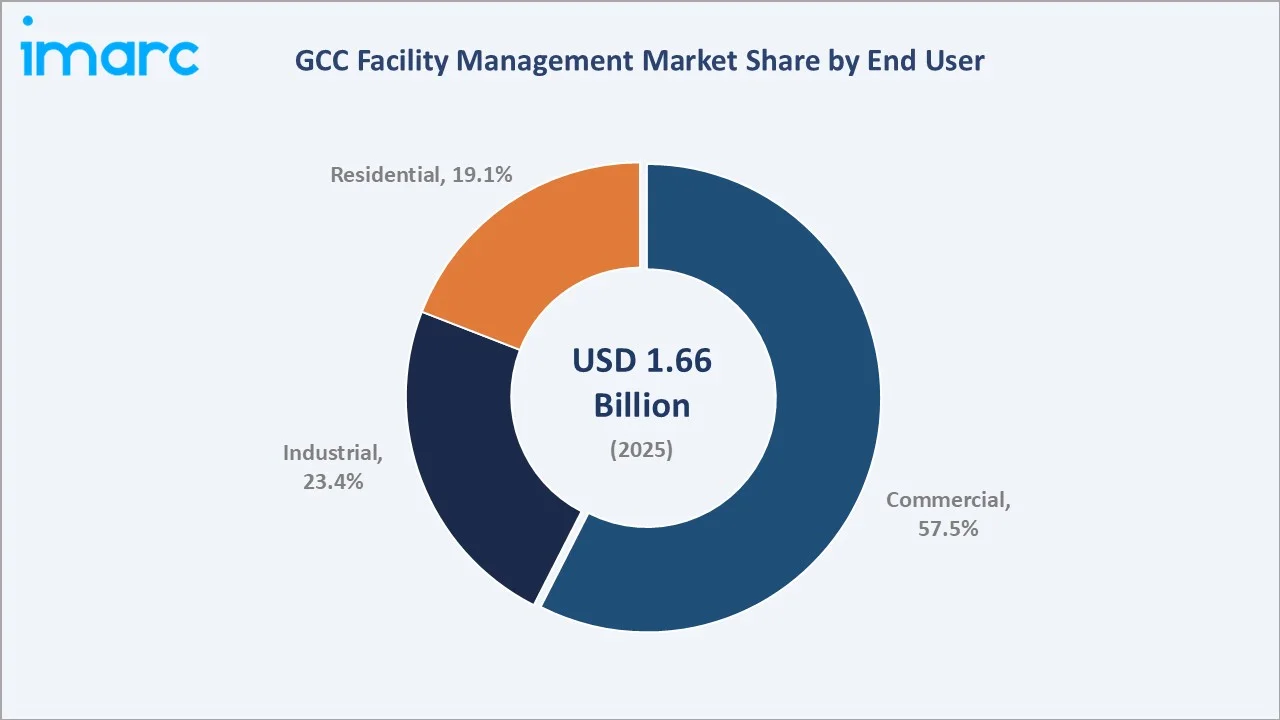

By End User

Commercial end users lead at 57.5% encompassing GCC’s office, retail, hospitality, healthcare, education, and airport sectors. GCC’s commercial FM is uniquely diverse: Dubai’s hotels require 5-star hospitality FM; Saudi Arabia’s healthcare Giga-Project hospitals require ISO 15224 healthcare FM; GCC’s 15 international airports require IATA-compliant aviation FM.

Industrial at 23.4% serves the oil and gas, petrochemical, manufacturing, and utilities sectors. Residential at 19.1% covers managed residential communities where community FM services are bundled at USD 8‐15 per sq m per year.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Saudi Arabia |

34.8% |

Saudi Vision 2030’s infrastructure investment pipeline – NEOM, Red Sea Project (luxury tourism), Diriyah Gate (heritage), Qiddiya (entertainment), Sindalah Island, collectively creates the largest concentration of greenfield commercial FM contracts |

|

UAE |

28.6% |

Dubai’s post-Expo 2020 legacy infrastructure requiring 20-year FM service contracts; Abu Dhabi’s Aldar Properties’ managed portfolio expanding under Abu Dhabi Economic Vision 2030; the UAE’s hospitality sector requiring premium 5-star FM standards at hotel rooms |

|

Qatar |

12.7% |

Qatar FIFA World Cup 2022 legacy infrastructure requiring 10‐15-year post-event FM contracts for 8 stadiums, Lusail City, Al Bayt complex, media and hospitality facilities – estimated accumulated FM contract value |

|

Oman |

9.4% |

Oman Vision 2040’s economic diversification driving infrastructure development: Oman Convention & Exhibition Centre (OCEC) FM, Muscat Bay luxury residential FM |

|

Kuwait |

8.2% |

Kuwait Vision 2035 infrastructure programme: Silk City, new Kuwait City Airport Terminal, Kuwait University main campus FM |

|

Bahrain |

6.3% |

Bahrain Economic Vision 2030’s financial services hub expansion – Bahrain Bay FM, Bahrain Financial Harbor FM |

Saudi Arabia’s 34.8% dominance will intensify through 2030 as Vision 2030’s Giga-Projects transition from construction to operations phase, creating a high new annual FM contract value from NEOM, Red Sea Project, Diriyah, and Qiddiya alone. Saudi Arabia’s Saudization mandate for FM is simultaneously the market’s greatest workforce challenge and its most significant competitive barrier to entry for FM providers without established Saudi national training programs.

UAE’s 28.6% market reflects the most mature FM market in the GCC with the highest adoption of integrated FM, digital FM platforms, and sustainability FM services. Dubai’s EXPO 2020 legacy and Abu Dhabi’s Aldar Properties’ expanding residential portfolio creation continue to create new FM demand without depending on single megaproject timing risks.

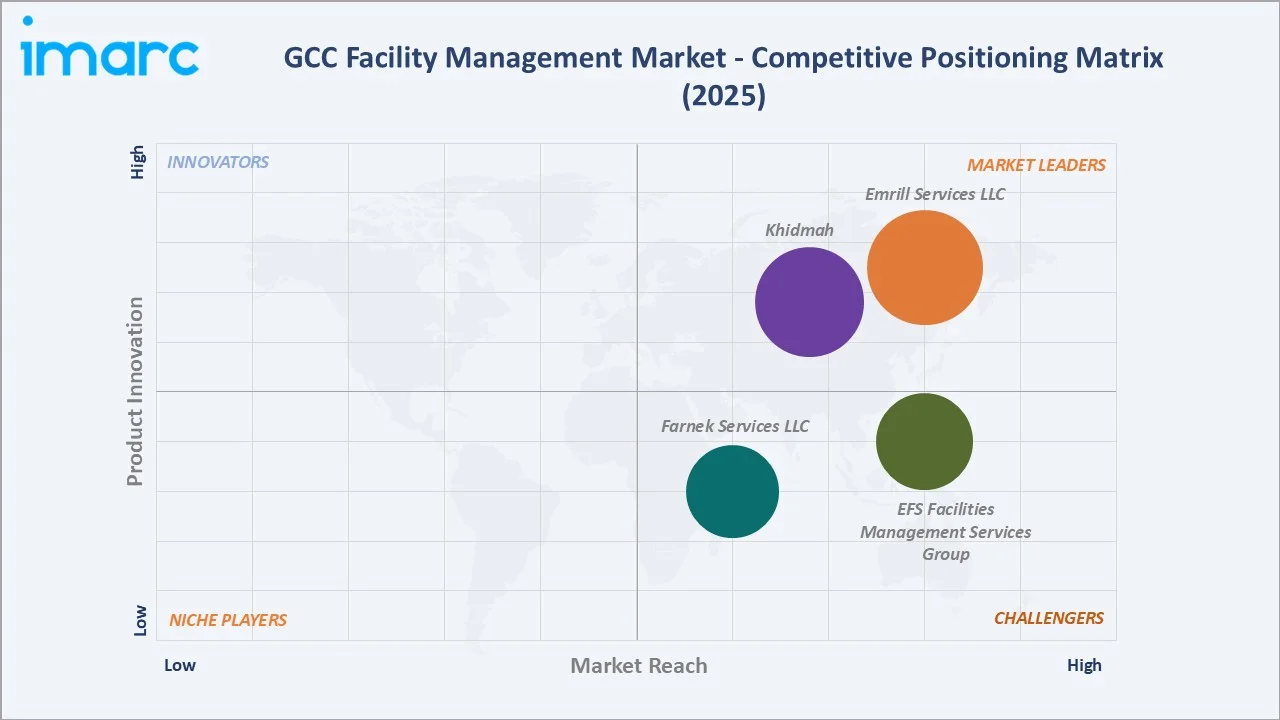

Competitive Landscape

The GCC facility management market exhibits moderate concentration, with the top-5 companies accounting for approximately 30‐35% of total market revenue. The remaining 65‐70% is distributed across 500+ FM service providers ranging from regional specialists to local single-service operators, with the fragmentation reflecting GCC’s large number of sub-contracting and single-service contracts.

|

Company Name |

Service Line |

Market Position |

Core Strength |

|

Emrill Services LLC |

Integrated Management System, Energy Management System, Quality Management System, Hard FM Services, Soft FM Services, Security Services, Heights (High-level Access Services) |

Market Leader |

Dubai-headquartered Emrill Services is the UAE’s largest domestically headquartered integrated FM company |

|

Khidmah |

Integrated Facility Management, Maintenance Solutions, Landscaping and Gardening Solutions, Housekeeping and Cleaning Solutions, Hospitality Solutions, Pest Control, MEP Services, Concierge Services |

Market Leader |

Abu Dhabi-headquartered Khidmah LLC manages the FM-managed property portfolio plus third-party contracts. |

|

EFS Facilities Management Services Group |

Management of Third-Party Providers, HSEQ (Health, Safety, Environment, and Quality), Quality Assurance, Call Center Management, Help-desk Management, Contracts Compliance, Computer-Aided Facilities Management System Integration (CAFM) |

Strong Challenger |

Dubai-headquartered EFS Facilities Services Group is GCC’s most geographically diverse independent FM company. |

|

Farnek Services LLC |

Security Services, Hospitality Services, Cleaning, Maintenance |

Strong Challenger |

Dubai-headquartered Farnek Services LLC differentiates itself as GCC’s leading sustainability-focused FM company, with its smart and green facility management services positioning around energy efficiency, carbon reduction, and smart energy management. |

The competitive landscape is evolving toward bi-polarisation: the top companies are investing in technology, IFM capability, and geographic expansion, while smaller operators face margin pressure from price competition and increasing regulatory compliance costs.

Key Company Profiles

Emrill Services LLC

Emrill Services LLC is the UAE’s largest domestically headquartered integrated FM company, equally owned by Emaar Properties and Al-Futtaim Real Estate Investment Company.

- Service Portfolio: Integrated Management System, Energy Management System, Quality Management System, Hard FM Services, Soft FM Services, Security Services, Heights (High-level Access Services).

- Recent Developments: In March 2023, Emrill introduced TECHSPHERE, an advanced digital FM solution designed to enhance technical capabilities, streamline operations, and improve information accessibility for both Emrill employees and clients. Developed through comprehensive research and client feedback, this integrated solution aims to deliver a more sophisticated system, boosting efficiencies in the facility management sector.

- Strategic Focus: Smart FM differentiation through 100% IoT sensor connectivity of all Emrill-managed critical assets by 2026; Saudi Arabia expansion through direct presence in NEOM, Red Sea Project, and Riyadh commercial FM.

Khidmah

Khidmah, a subsidiary of Aldar Properties, is Abu Dhabi’s market-leading FM company managing residential community units and operating the FM of Aldar’s entire managed portfolio.

- Service Portfolio: Integrated Facility Management, Maintenance Solutions, Landscaping and Gardening Solutions, Housekeeping and Cleaning Solutions, Hospitality Solutions, Pest Control, MEP Services, Concierge Services.

- Recent Developments: In February 2022, Khidmah launched its new innovative digital platform, Khidmah Home, to enable residents and property owners to benefit from the company’s professional maintenance services.

- Strategic Focus: Third-party FM market entry in Abu Dhabi as revenue diversification beyond Aldar captive portfolio; Smart Community FM expansion including AI security surveillance, automated waste management, and solar energy community FM.

EFS Facilities Management Services Group

EFS Facilities Management Services Group is GCC’s most geographically expansive independent FM company and the recipient of CBNME Innovative FM Company of the Year.

- Service Portfolio: Management of Third-Party Providers, HSEQ (Health, Safety, Environment, and Quality), Quality Assurance, Call Center Management, Help-desk Management, Contracts Compliance, Computer-Aided Facilities Management System Integration (CAFM).

- Recent Developments: In April 2021, EFS Facilities Services Group (EFS) launched the first center of excellence for cleaning services.

- Strategic Focus: World FM Award innovation leadership as brand positioning for IFM mega-contract pursuit; EFS Drone Inspection commercialization across GCC’s solar panel installations, supertall buildings, and industrial facilities.

Market Concentration Analysis

The GCC facility management market exhibits moderate concentration at the premium IFM tier and high fragmentation at the single-service tier. The top-5 integrated FM providers collectively represent approximately 25‐30% of total market revenue but an estimated 55‐65% of integrated FM contract value, reflecting a market where integration capability, technology investment, and financial depth create significant barriers to entry for smaller competitors in the highest-value contract tier.

Market concentration is increasing through three mechanisms: GCC’s megaproject FM contracts require IFM capability that only the top-8 to top-10 providers possess at required scale and technology depth; ADNOC’s, ARAMCO’s, and major real estate developers’ vendor consolidation programs are reducing preferred FM provider lists from 20‐30 companies to 5‐10 strategic partners; and increasingly complex FM regulatory compliance eliminates smaller providers who cannot invest in specialist compliance capability.

Investment & Growth Opportunities

Fastest Growing Segments

Integrated FM mode (~9.0% CAGR), industrial end user (~8.6% CAGR), Qatar country (~9.2% CAGR), sustainability/green FM (~15‐18% CAGR from 2025 base), and healthcare FM (~12‐15% CAGR) represent GCC FM’s highest-growth investment vectors.

Emerging Technology Investment Themes

CAFM-to-Digital-Twin evolution, drone inspection services for supertall buildings and solar installations, AI predictive maintenance platforms, green building certification FM, and smart community FM collectively define GCC FM’s highest-margin emerging service categories.

Investment Themes

Listed equity and private investment access to GCC FM growth includes international FM companies with GCC exposure.

- Direct market entry investment: Integrated FM company formation targeting Saudi Giga-Project FM tenders; FM technology platform development.

- Technology partnerships: IoT and BMS system integration with GCC FM companies; AI predictive maintenance platform licensing to GCC FM operators; drone inspection technology providers.

Future Market Outlook (2026-2034)

The GCC facility management market is entering its most consequential and transformative growth phase. From USD 1.66 Billion in 2025, the market will reach USD 3.55 Billion by 2034, at a sustained 8.35% CAGR that reflects the systematic convergence of three irreversible structural forces defining GCC FM’s expansion trajectory. First, GCC’s Giga-Project operational transition is the world’s most predictable FM demand creation event: NEOM’s The Line, Red Sea Project’s resort islands, Diriyah Gate’s UNESCO heritage precinct, Qiddiya’s entertainment city, Lusail City’s residential district, and Ruwais City’s industrial complex collectively represent high-demand operational FM requirements.

Second, GCC governments’ systematic outsourcing of FM from in-house to specialist providers under Vision 2030 efficiency mandates is a structural transition that will continue regardless of oil price cycles, political transitions, or global economic conditions outsourcing FM creates irreversible institutional knowledge transfer that makes in-house reconstitution economically irrational once completed. Third, smart building technology’s systematic penetration of GCC’s new construction stock is creating an FM technology platform that elevates FM from a labor-intensive service to a data-driven intelligence business, systematically increasing FM contract values and the technical barrier to entry that protects premium IFM providers’ market position.

Research Methodology

Primary Research

Primary research included 120+ structured interviews with GCC FM industry stakeholders in 2025, comprising FM company CEOs and commercial directors, GCC government FM procurement officers, ARAMCO and ADNOC FM category managers, real estate developer FM directors, BIFM/CBRE Certified FM professionals based in GCC, and independent GCC FM industry consultants.

Secondary Research

Secondary research encompassed GCC country government annual reports and Vision 2030 program updates, IMARC facilities management global intelligence database, BIFM MENA market publications, IFMA (International Facility Management Association) GCC chapter data, company financial disclosures, RICS GCC built environment market reports, and proprietary industry tender and contract value databases. Over 130 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using a bottom-up mode of facility × end-user × country disaggregated model validated against top-down GCC construction completion and built environment stock models. Key inputs include GCC Giga-Project completion timeline data, Vision 2030 capital expenditure programme schedules, GCC construction pipeline value, ARAMCO and ADNOC capital budget disclosures, and GCC hotel room addition pipeline.

GCC Facility Management Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Services Covered |

|

| Modes of Facility Covered | In-house, Outsourced, Integrated, Bundled, Single |

| End Users Covered | Commercial, Industrial, Residential |

| Countries Covered | Saudi Arabia, UAE, Qatar, Bahrain, Kuwait, Oman |

| Companies Covered | Emrill Services LLC, Khidmah, EFS Facilities Management Services Group, Farnek Services LLC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the GCC facility management market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the GCC facility management market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the GCC facility management industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the GCC Facility Management Market Report

The GCC facility management market was valued at USD 1.66 Billion in 2025 and is projected to reach USD 3.55 Billion by 2034.

The GCC FM market is forecast to grow at a CAGR of 8.35% during 2026-2034, driven by Vision 2030 megaproject FM requirements, outsourcing transition, smart building technology adoption, and GCC tourism infrastructure expansion.

Outsourced FM leads with 61.8% revenue share (2025), as GCC governments and corporations systematically transfer FM operations to specialist providers under long-term performance-based contracts.

Commercial end users lead with 57.5% share (2025), encompassing GCC’s office, retail, hospitality, healthcare, education, and airport sectors.

Saudi Arabia leads with 34.8% share (2025), driven by Vision 2030’s infrastructure pipeline, including NEOM, Red Sea Project, Diriyah Gate, and Qiddiya giga-projects.

Key companies include Emrill Services LLC, Khidmah, EFS Facilities Management Services Group, Farnek Services LLC, and others.

Key drivers include Vision 2030 and national transformation megaproject infrastructure rollouts, rising trend to outsource non-core FM operations, smart building and CAFM technology adoption, and rapid hospitality and tourism infrastructure expansion across GCC.

Key trends include NEOM smart city FM requirements forcing AI/robotics adoption, integrated FM replacing fragmented sub-contracting, sustainability FM and net zero building certification maintenance, drone and robot deployment in FM operations, and CAFM-to-digital-twin platform evolution.

Key challenges include shortage of skilled FM workforce with 85‐95% expatriate dependency, price-based procurement culture compressing service margins to 4–7% in government tenders, fragmented regulatory standards across 6 GCC nations, and extreme climate HVAC maintenance cost structures 3–5× higher than temperate markets.

Top opportunities include IFM company formation targeting Saudi Giga-Project FM tenders, FM technology platform development, drone inspection services for GCC solar installations and supertall buildings, sustainability FM ESPCs delivering guaranteed energy savings, and healthcare FM specialization.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade