Generative AI Market Size, Share, Trends and Forecast by Offering Type, Technology Type, Application, and Region, 2026-2034

Global Generative AI Market Size, Share, Trends & Forecast (2026-2034)

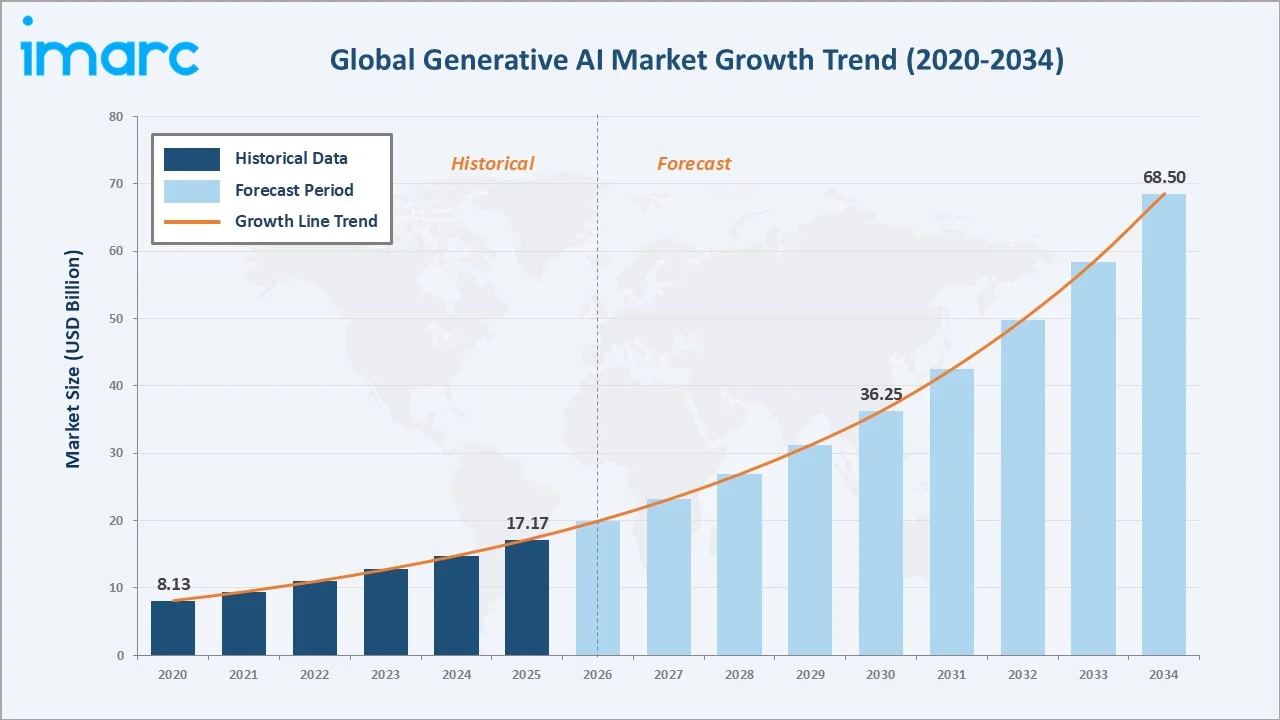

The global generative AI market was valued at USD 17.17 Billion in 2025 and is projected to reach USD 68.50 Billion by 2034, exhibiting a CAGR of 16.12% during 2026-2034. Rising private enterprise adoption, rapid advances in foundation model capabilities, expanding applications across healthcare and media, and growing demand for automated content generation are the primary drivers shaping the market growth. As per Stanford University, private investment in generative AI reached USD 33.9 Billion globally in 2024, reflecting an 18.7% year-over-year increase.

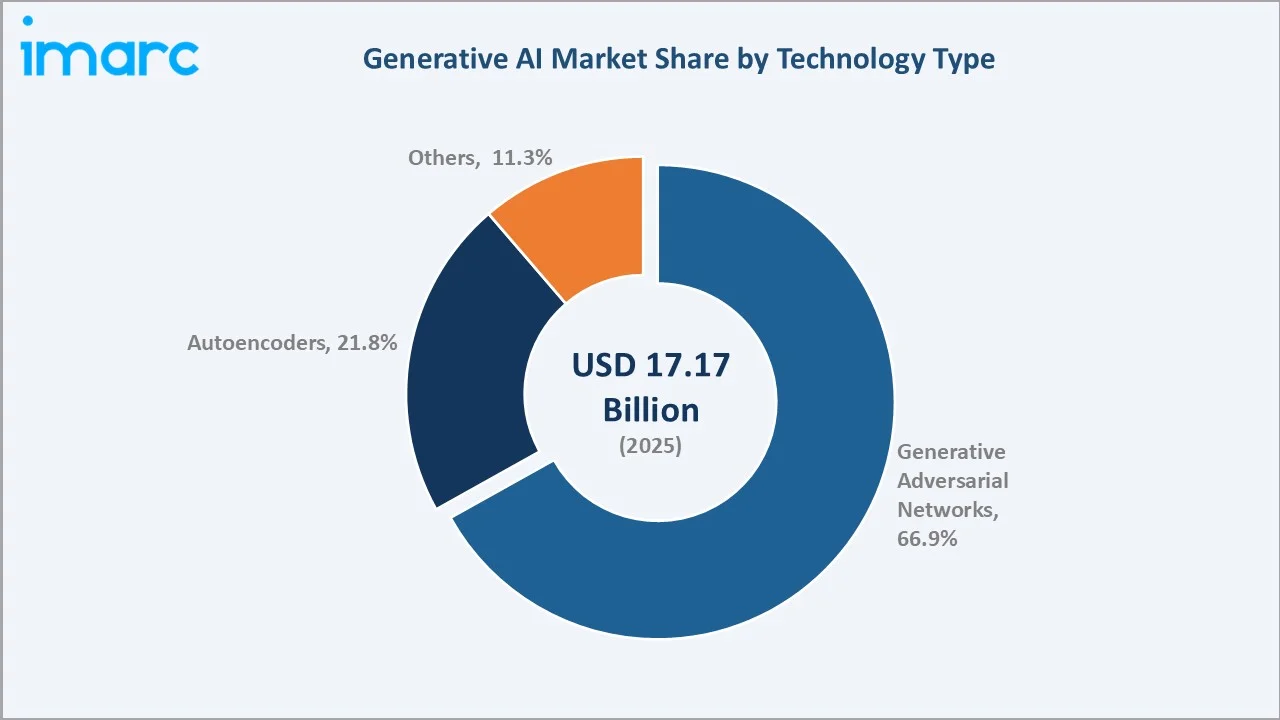

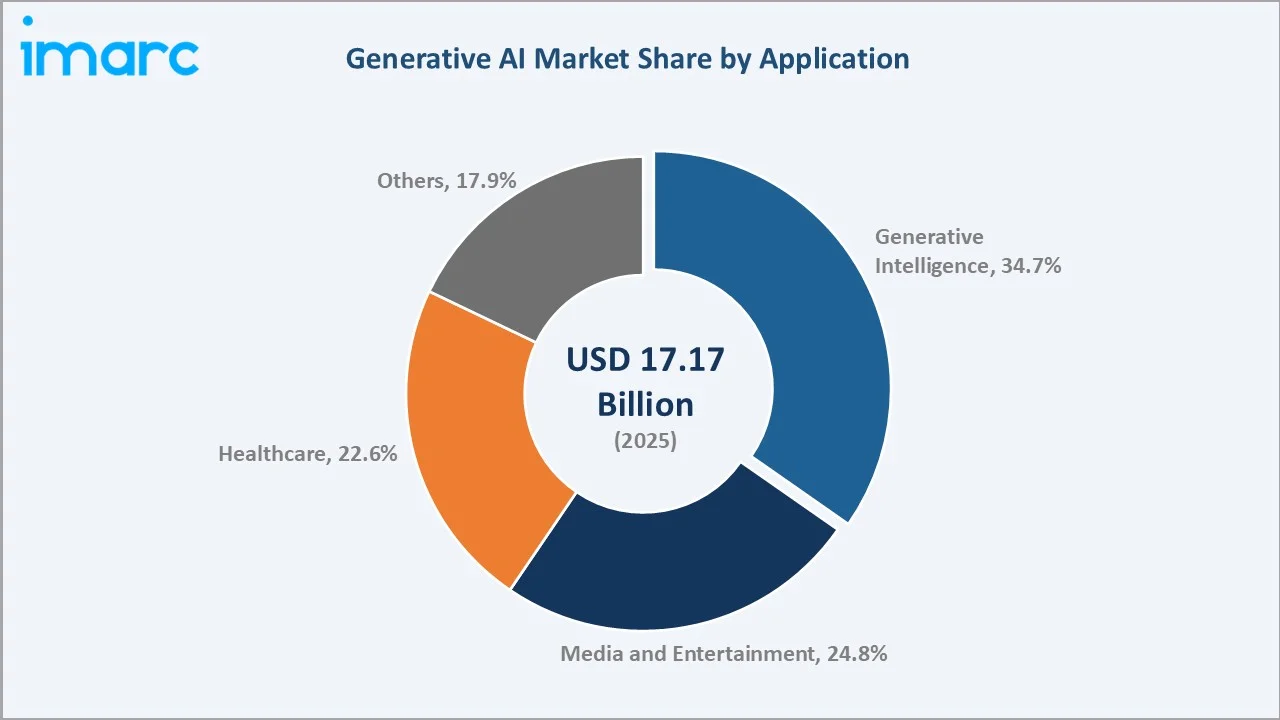

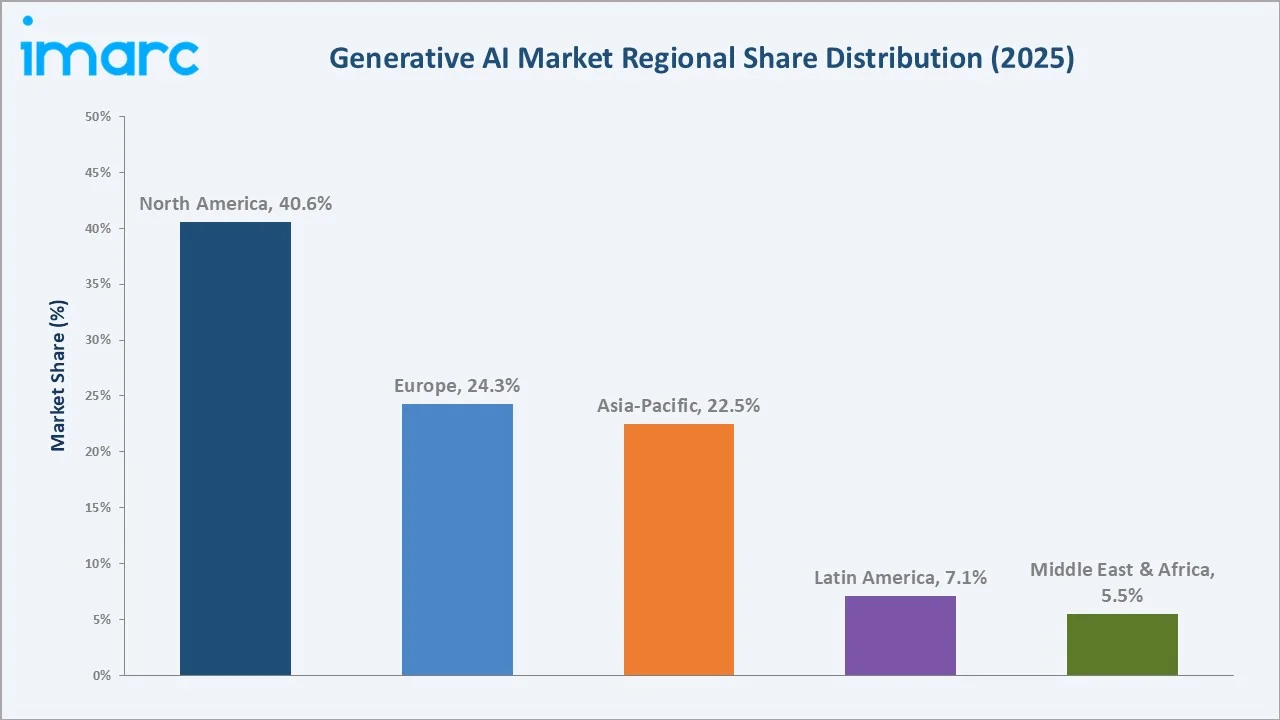

Generative adversarial networks lead the technology type segment at 66.9%, generative intelligence dominates the application segment at 34.7%, and North America commands 40.6% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 17.17 Billion |

|

Forecast Market Size (2034) |

USD 68.50 Billion |

|

CAGR (2026-2034) |

16.12% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (40.6%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (22.5%, 2025) |

|

Leading Technology Type |

Generative Adversarial Networks (66.9%, 2025) |

|

Leading Application |

Generative Intelligence (34.7%, 2025) |

The global generative AI market expanded from USD 8.13 Billion in 2020 to USD 17.17 Billion in 2025, driven by breakthroughs in transformer-based models, increasing enterprise adoption, and supportive cloud infrastructure investments. Anchored at USD 36.25 Billion in 2030, the forecast to USD 68.50 Billion by 2034 is supported by growing demand for AI-powered automation and content creation across industries.

To get more information on this market, Request Sample

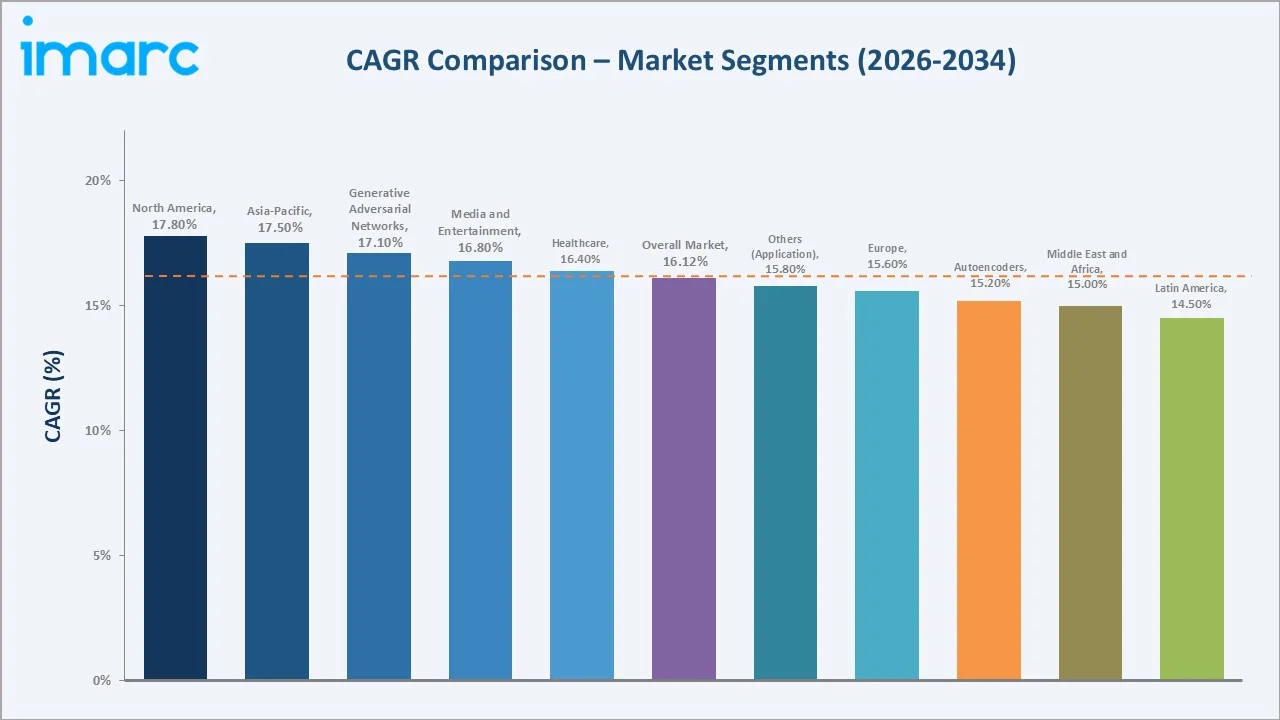

CAGR trajectories across technology type and application sub-segments show healthcare and generative adversarial networks expanding faster than the overall 16.12% market CAGR, driven by deepening clinical AI applications and advancing generative adversarial network architectures for enterprise use.

Executive Summary

The global generative AI market is on a strong growth path from USD 8.13 Billion in 2020 to USD 68.50 Billion by 2034. Foundation models have shifted from research experiments to essential enterprise infrastructure. Falling inference costs and expanding API accessibility are encouraging organizations to integrate AI-powered content generation, code automation, and data analytics into core workflows. Policy frameworks and responsible AI governance are further supporting adoption across regulated industries.

Generative adversarial networks dominate the technology type segment at 66.9% in 2025, supported by superior image synthesis and data augmentation capabilities. Generative intelligence leads the application segment at 34.7%, fueled by enterprise demand for automated reasoning, decision support, and workflow optimization. North America commands 40.6%, led by the United States, driven by deep venture capital ecosystems, hyperscaler investments, and a concentration of leading AI research labs. In January 2026, George Mason University established the Virginia AI Data Center Research Lab at Mason Square, supported by a USD 1.5 Million grant to advance AI-driven digital infrastructure and workforce development.

Key Market Insights

|

Insight |

Data |

|

Leading Technology Type |

Generative Adversarial Networks - 66.9% share (2025) |

|

Second Technology Type |

Autoencoders - 21.8% share (2025) |

|

Leading Application |

Generative Intelligence - 34.7% share (2025) |

|

Second Application |

Media and Entertainment - 24.8% share (2025) |

|

Leading Region |

North America - 40.6% share (2025) |

|

Fastest Growing Region |

Asia-Pacific - 22.5% share (2025) |

|

Top Companies |

Microsoft, OpenAI, Amazon.com, Inc., NVIDIA Corporation, Adobe |

Key Analytical Observations Expanding on the Data Above:

- Generative adversarial networks dominance at 66.9% is driven by strong demand for high-fidelity image synthesis, data augmentation in healthcare imaging, and creative content generation across the media and advertising industries.

- Autoencoders share at 21.8% is sustained by anomaly detection, dimensionality reduction, and representation learning applications across the manufacturing, cybersecurity, and financial services sectors.

- Generative intelligence leadership at 34.7% reflects enterprise preference for AI-driven decision support, automated reasoning, and intelligent workflow orchestration across business functions.

- Media and entertainment at 24.8% is expanding through automated video production, music composition, and personalized content delivery. This growth is also being accelerated by increasing adoption of generative AI tools across content creation workflows. Adobe reported that its Firefly generative AI models were used to create over 22 Billion assets, as of April 2025, underscoring the rapid acceleration of AI-driven content creation across media and creative industries.

- North America at 40.6% dominates owing to the concentration of leading AI research labs, hyperscaler cloud infrastructure, deep venture capital ecosystems, and favorable regulatory environments in the United States.

Global Generative AI Market Overview

Generative AI refers to a class of AI systems capable of creating new content, including text, images, video, audio, and code, by learning patterns from large training datasets. These systems leverage deep learning architectures, such as generative adversarial networks, variational autoencoders, and transformer models, to produce outputs that closely resemble human-generated content.

The global ecosystem integrates foundation model developers, cloud infrastructure providers, GPU and accelerator chip manufacturers, enterprise software integrators, data providers, AI safety and governance organizations, and end user applications, together enabling seamless deployment across healthcare, media, finance, and industrial verticals.

Market Dynamics

To evaluate market opportunities, Request Sample

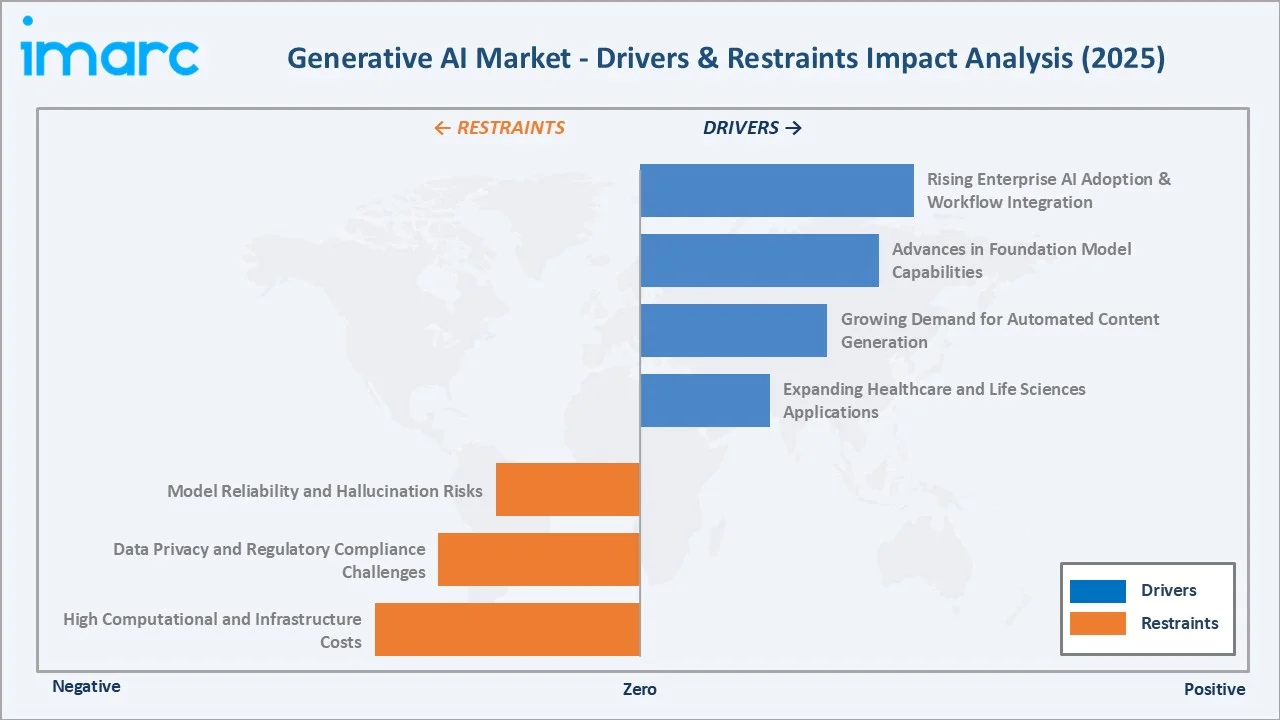

Market Drivers

- Rising Enterprise AI Adoption and Workflow Integration: Organizations across industries are embedding generative AI into core business processes, moving beyond pilot programs to production-scale deployments. This shift is reshaping software development, content creation, and customer engagement.

- Advances in Foundation Model Capabilities: Continuous improvements in large language models, multimodal AI systems, and reasoning architectures are expanding the scope of generative AI applications.

- Growing Demand for Automated Content Generation: Businesses are increasingly leveraging AI for marketing, documentation, code generation, and creative production, driven by the need to scale content output while reducing costs and production timelines.

- Expanding Healthcare and Life Sciences Applications: Generative AI is being deployed for drug discovery, medical imaging analysis, clinical documentation, and personalized treatment planning, creating substantial growth opportunities in regulated healthcare environments. In November 2025, researchers at the University of California, Berkeley and University of California, San Francisco unveiled Pillar (Pillar-0), an open-source AI model that could examine medical images and identify conditions with an unmatched level of diagnostic precision.

Market Restraints

- High Computational and Infrastructure Costs: Training and deploying large-scale generative AI models require significant investments in GPU clusters, cloud infrastructure, and energy consumption, creating affordability barriers for small and mid-sized enterprises.

- Data Privacy and Regulatory Compliance Challenges: Evolving regulations around data protection, AI transparency, and model governance across jurisdictions are creating compliance complexities for organizations deploying generative AI at scale, particularly in the healthcare, finance, and government sectors.

- Model Reliability and Hallucination Risks: Generative AI systems can produce inaccurate or biased outputs, raising concerns around trust, safety, and reliability in critical applications. These limitations often necessitate human oversight and validation before deployment in high-stakes environments.

Market Opportunities

- Agentic AI and Autonomous Workflow Execution: The emergence of AI agents capable of planning, reasoning, and executing multi-step tasks autonomously is opening transformative opportunities across enterprise operations, customer service, and software development.

- Emerging Market Expansion in Asia-Pacific and Latin America: Growing digital infrastructure, rising technology investments, and expanding enterprise AI adoption in countries, such as India, China, Brazil, and Southeast Asian nations, are creating strong opportunities for generative AI providers.

Market Challenges

- Model Bias, Hallucination, and Trust Concerns: Generative AI models continue to face challenges related to factual accuracy, bias in outputs, and hallucination risks, which can undermine trust and limit adoption in high-stakes applications such as legal, medical, and financial advisory.

- AI Talent Shortage and Skill Gaps: The rapid pace of generative AI innovation has created significant demand for specialized talent in machine learning (ML) engineering, prompt engineering, and AI safety, outpacing the available workforce in most global markets.

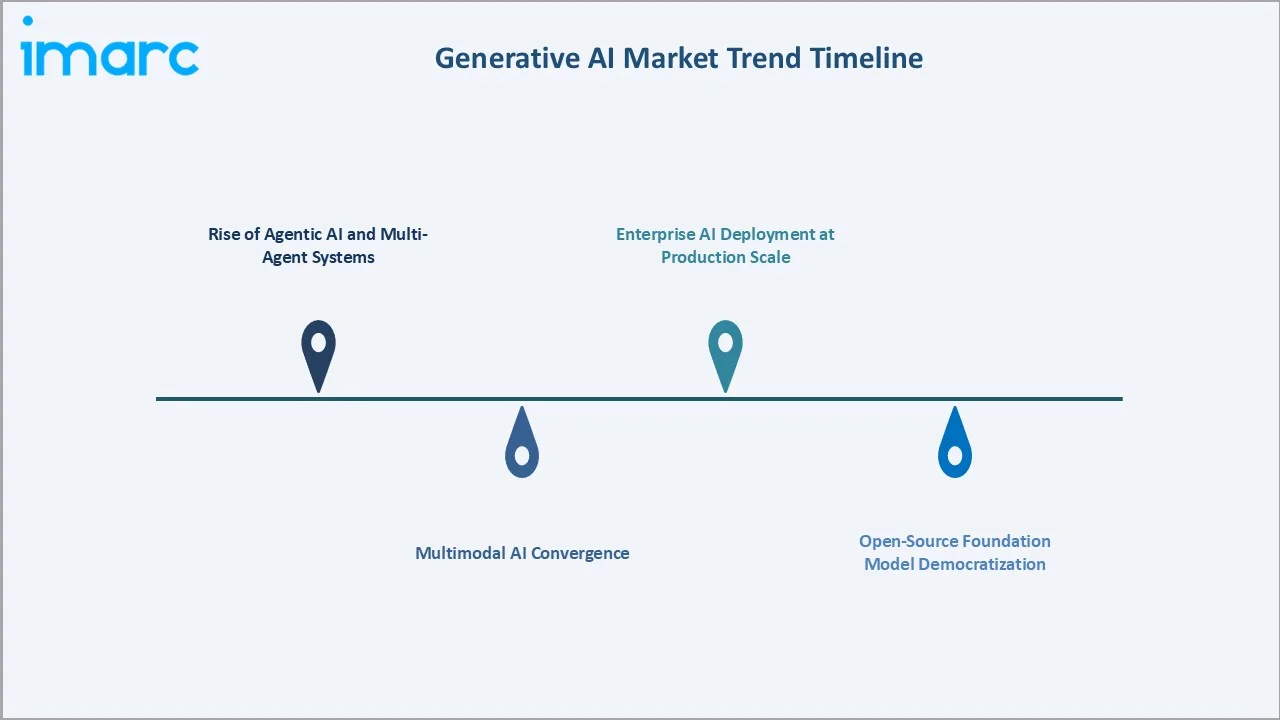

Emerging Market Trends

1. Rise of Agentic AI and Multi-Agent Systems

Agentic AI systems capable of autonomous task planning, reasoning, and multi-step execution are rapidly gaining traction across enterprise workflows. These systems are transforming customer service, software development, and operational decision-making by enabling AI to act independently within defined parameters.

2. Multimodal AI Convergence

Foundation models are increasingly integrating text, image, video, audio, and code generation within unified architectures. This convergence is enabling seamless cross-modal content creation and expanding the range of practical enterprise applications.

3. Enterprise AI Deployment at Production Scale

Organizations are moving beyond experimentation to embed generative AI into production workflows. This shift is being supported by the growing investments in secure, scalable AI infrastructure and governance frameworks.

4. Open-Source Foundation Model Democratization

Open-source foundation models are lowering barriers to entry for small and mid-sized enterprises, enabling broader participation in the generative AI ecosystem. This trend is accelerating innovation in fine-tuning, domain-specific adaptation, and cost-effective deployment strategies.

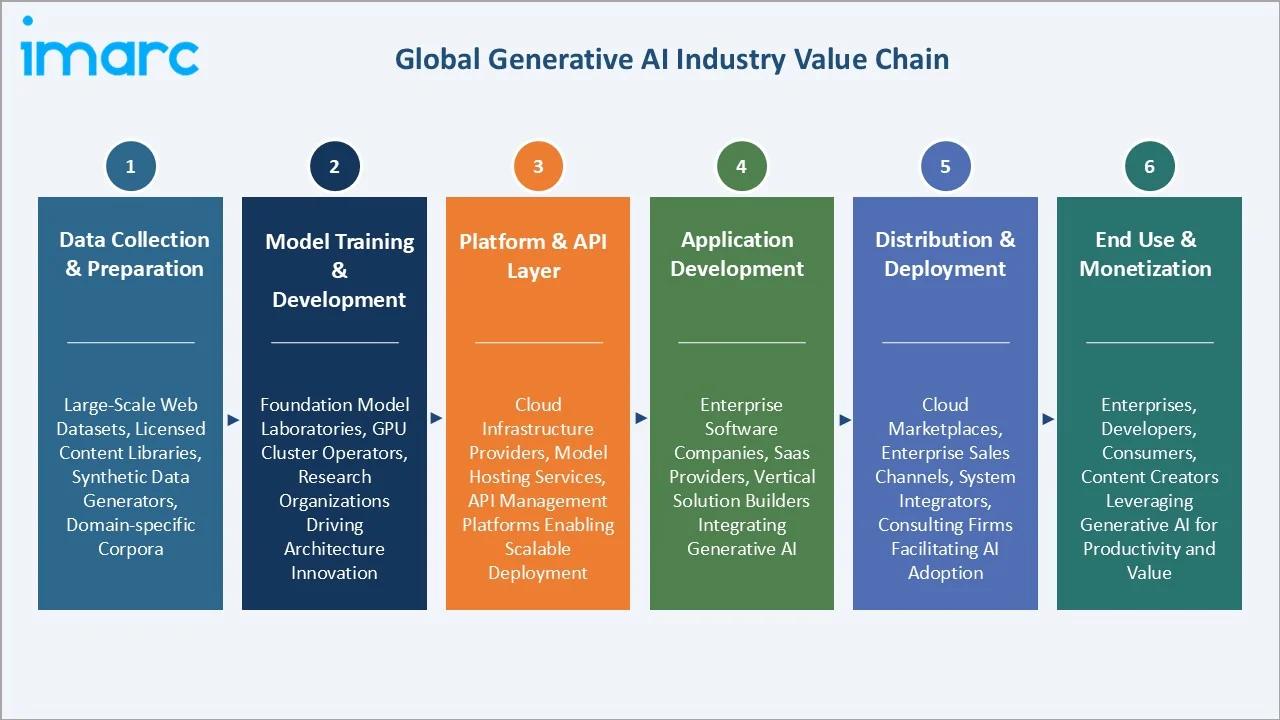

Industry Value Chain Analysis

The generative AI value chain spans six stages from data collection through end user monetization. Foundation model development and platform integration capture the highest value-add, while application development and distribution generate downstream competitive advantages in this rapidly evolving category.

|

Stage |

Key Players / Examples |

|

Data Collection & Preparation |

Large-scale web datasets, licensed content libraries, synthetic data generators, and specialized domain-specific corpora supporting model training |

|

Model Training & Development |

Foundation model laboratories, GPU cluster operators, and research organizations focused on architecture innovation and training optimization |

|

Platform & API Layer |

Cloud infrastructure providers, model hosting services, and API management platforms enabling scalable model deployment and integration |

|

Application Development |

Enterprise software companies, SaaS providers, and vertical solution builders integrating generative AI into domain-specific workflows |

|

Distribution & Deployment |

Cloud marketplaces, enterprise sales channels, system integrators, and consulting firms facilitating organizational AI adoption |

|

End Use & Monetization |

Enterprises, developers, consumers, and content creators leveraging generative AI for productivity, creativity, and business value generation |

Vertically integrated players that combine foundation model development, cloud infrastructure, and application-layer solutions, supported by strategic partnerships and enterprise distribution capabilities, achieve stronger market positioning than point-solution providers.

Technology Landscape in the Global Generative AI Industry

Foundation Model Architecture Innovation

Transformer architectures remain the dominant paradigm for generative AI, with ongoing innovations in attention mechanisms, mixture-of-experts configurations, and context window expansion enabling increasingly capable and efficient models. Emerging architectures, such as state-space models and diffusion transformers, are advancing toward commercial deployment for specialized applications.

Generative Adversarial Network Advances

Generative adversarial networks continue to evolve with improved training stability, higher resolution output capabilities, and conditional generation techniques. Applications in medical imaging, synthetic data generation, and creative content production are driving ongoing research and commercial investment in generative adversarial network-based systems.

Cloud and Edge AI Infrastructure

Cloud-native AI platforms with GPU-as-a-service offerings, model optimization tools, and hybrid deployment capabilities are becoming standard for enterprise generative AI adoption. Edge inference solutions are enabling real-time generative AI applications in healthcare, manufacturing, and autonomous systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Offering Type |

🔒 |

🔒 |

2025 |

|

Technology Type |

Generative Adversarial Networks |

66.9% |

2025 |

|

Application |

Generative Intelligence |

34.7% |

2025 |

|

Region |

North America |

40.6% |

2025 |

By Technology Type

Generative adversarial networks command a 66.9% majority share in 2025, driven by superior performance in image synthesis, data augmentation, and creative content generation. Generative adversarial networks remain the preferred technology for applications requiring high-fidelity visual output, including medical imaging, fashion design, and digital media production.

To access detailed market analysis, Request Sample

Autoencoders at 21.8% in 2025 serve critical functions in anomaly detection, dimensionality reduction, and representation learning across manufacturing, cybersecurity, and financial services.

By Application

Generative intelligence dominates with 34.7% share in 2025, reflecting enterprise demand for AI-powered reasoning, decision support, and automated workflow orchestration. This segment encompasses applications in business intelligence, strategic planning, and process optimization that leverage generative models for actionable insight generation.

Media and entertainment at 24.8% in 2025 is expanding rapidly through automated video production, AI-generated music and sound design, visual effects enhancement, and personalized content delivery platforms.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

40.6% |

Deep venture capital ecosystem, hyperscaler cloud investments, concentration of leading AI research labs, and supportive innovation policy frameworks |

|

Europe |

24.3% |

Strong regulatory leadership, growing enterprise AI adoption, expanding research collaborations, and increasing public-private investment in AI infrastructure |

|

Asia-Pacific |

22.5% |

Rapid digital transformation, large-scale government AI initiatives, expanding technology startup ecosystems, and growing enterprise demand for AI-powered automation |

|

Latin America |

7.1% |

Rising digital economy adoption, growing cloud infrastructure investments, expanding fintech and e-commerce AI integration, and increasing government digitalization programs |

|

Middle East and Africa |

5.5% |

National AI strategy implementations, growing investment in smart city and digital government initiatives, expanding technology hub development, and rising enterprise digitalization |

North America at 40.6% in 2025 leads the global market, driven by the United States housing the majority of leading AI research organizations, hyperscaler cloud providers, and a mature venture capital ecosystem. Well-established enterprise software markets and deep technology talent pools are further supporting sustained adoption of generative AI solutions.

Asia-Pacific at 22.5% is the highest-growth region through 2034. Strong government AI initiatives, rapid enterprise digital transformation, and expanding technology ecosystems in China, India, Japan, and South Korea are accelerating regional expansion.

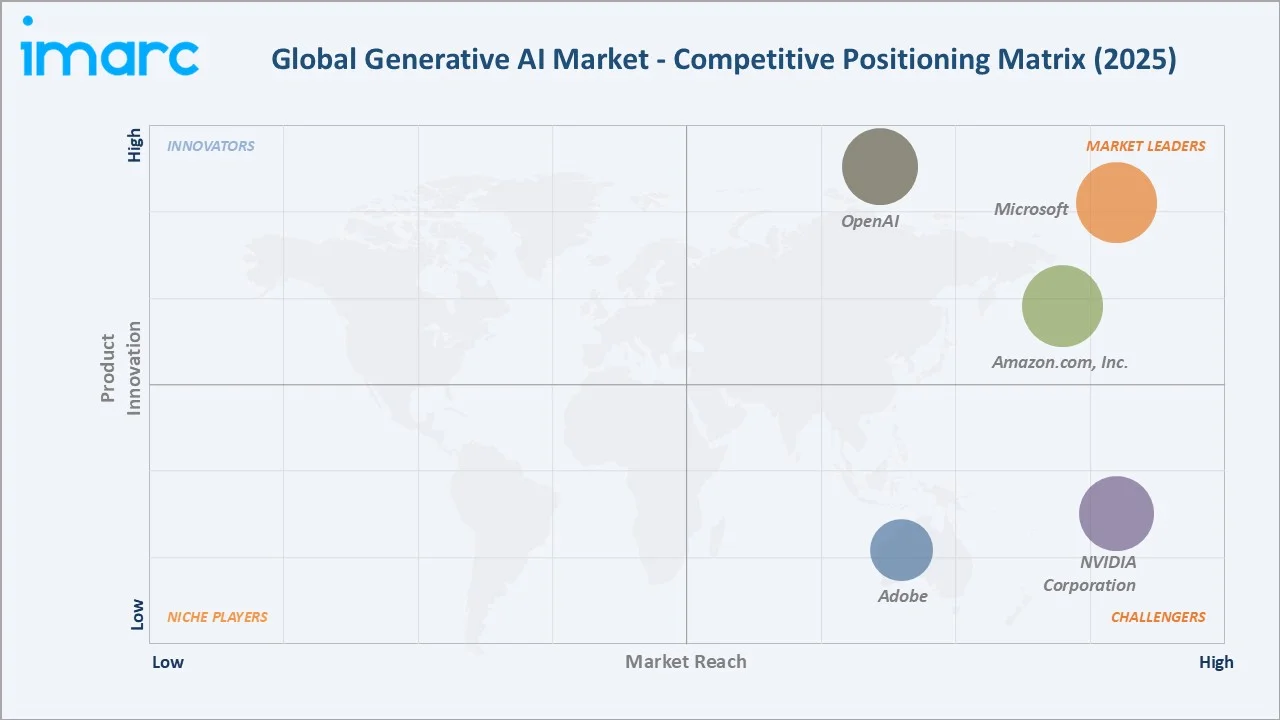

Competitive Landscape

The global generative AI market is moderately concentrated, with a small number of large technology companies dominating foundation model development and platform services, while a growing number of specialized players focus on vertical applications, model orchestration, and enterprise integration. Model development capabilities, cloud infrastructure scale, and enterprise distribution networks form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Microsoft |

Copilot |

Leader |

Deep enterprise integration through productivity suite, cloud platform, and strategic model partnerships |

|

OpenAI |

GPT-5.5 Instant, ChatGPT, Codex |

Leader |

Foundation model leadership with broad consumer and enterprise API distribution |

|

Amazon.com, Inc. |

Amazon Bedrock, Amazon Nova |

Leader |

Enterprise AI platform providing scalable model hosting, inference, and deployment infrastructure |

|

NVIDIA Corporation |

NIM microservices and Nemotron |

Challenger |

AI infrastructure and accelerator leadership enabling model training and inference at scale |

|

Adobe |

Adobe Firefly, Adobe Sensei GenAI |

Challenger |

Creative software integration with generative AI for design, marketing, and media production workflows |

Key players include Microsoft, OpenAI, Amazon.com, Inc., NVIDIA Corporation, and Adobe, among others.

Key Company Profiles

Microsoft

Microsoft is a global technology company delivering generative AI capabilities across enterprise productivity software, cloud computing platforms, and developer ecosystems. The company integrates advanced AI technologies into business applications, collaboration tools, and intelligent automation solutions, while leveraging its extensive cloud infrastructure and enterprise customer network to strengthen adoption across industries.

- Product Portfolio: Copilot, GitHub Copilot for developer productivity, and Microsoft Fabric for data and AI integration.

- Recent Developments: In 2025, Microsoft announced plans to invest USD 80 Billion in AI-focused data center infrastructure and unveiled multi-agent orchestration capabilities in Microsoft Copilot for enterprise workflow automation.

- Strategic Focus: Deep enterprise integration embedding generative AI across the full productivity stack, leveraging strategic model partnerships for broad market reach.

OpenAI

OpenAI is a pioneering generative AI company and the developer of the GPT series of large language models, ChatGPT consumer application, and Codex autonomous coding agent, serving both consumer and enterprise markets globally.

- Product Portfolio: GPT-5.5 Instant, ChatGPT consumer and enterprise applications, Codex autonomous coding agent, and enterprise API platform.

- Recent Developments: In April 2026, OpenAI released GPT-5.5, its latest frontier model with enhanced agentic coding, computer use, and deep research capabilities, followed by GPT-5.5 Instant as the new default ChatGPT model in May 2026.

- Strategic Focus: Foundation model leadership with a focus on advancing toward artificial general intelligence, while scaling enterprise API distribution and expanding consumer application reach through strategic cloud partnerships.

Amazon.com, Inc.

Amazon.com, Inc. is a global technology and e-commerce leader active in the generative AI market through Amazon Web Services (AWS), which provides enterprise-grade AI platform services, proprietary foundation models, and scalable cloud infrastructure for AI deployment.

- Product Portfolio: Amazon Bedrock enterprise AI platform and Amazon Nova foundation models (Nova 2).

- Recent Developments: At AWS re:Invent 2025, Amazon.com, Inc. launched the Nova 2 model family with enhanced reasoning and multimodal capabilities, and announced that Amazon Bedrock was powering generative AI for more than 100,000 organizations globally.

- Strategic Focus: Enterprise AI platform leadership through Amazon Bedrock, proprietary model development with Amazon Nova, custom AI chip innovation, and broad cloud infrastructure scale for AI workload deployment.

Market Concentration Analysis

The global generative AI market is moderately concentrated, with the top five companies (Microsoft, OpenAI, Amazon.com, Inc., NVIDIA Corporation, and Adobe) estimated to hold approximately 55-65% of global market share in 2025.

Barriers to entry include massive computational infrastructure requirements, multi-billion dollar model training costs, access to large-scale training datasets, specialized AI talent acquisition, and enterprise distribution channel development, favoring well-capitalized incumbents with deep technical and commercial moats.

Consolidation is accelerating through strategic partnerships, model licensing agreements, cloud platform integrations, and vertical AI application acquisitions. Scale advantages in model development, infrastructure, and enterprise relationships are further reinforcing the competitive position of established players.

Investment & Growth Opportunities

Fastest-Growing Segments

Healthcare at 22.6% is expanding faster than the overall 16.12% market CAGR through 2034, driven by clinical AI applications, drug discovery acceleration, and medical imaging innovations. Generative intelligence at 34.7% represents the largest application opportunity as enterprises deploy AI-powered reasoning and decision support at scale.

Emerging Markets

Asia-Pacific at 22.5% is the highest-growth region, with China, India, and Japan leading AI investments and enterprise adoption. Latin America and Middle East and Africa represent expanding opportunities as digital infrastructure matures and government AI strategies accelerate technology adoption.

Venture & Investment Trends

Venture capital investment is concentrated in foundation model development, enterprise AI application platforms, AI safety and governance solutions, and vertical-specific generative AI tools. Investment is also expanding into agentic AI systems, multimodal content generation, and edge AI deployment infrastructure that enable more scalable and cost-effective generative AI solutions.

Future Market Outlook (2026-2034)

The global generative AI market is forecast to expand from USD 17.17 Billion in 2025 to USD 68.50 Billion by 2034 at a CAGR of 16.12%, adding roughly USD 51.33 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: foundation model cost reductions enabling broader enterprise adoption; agentic AI systems transforming autonomous business workflows; multimodal AI convergence creating unified content generation platforms; and expanding regulatory frameworks establishing trust and governance standards across industries.

By 2034, generative AI is expected to be embedded in the majority of enterprise software platforms and will serve as foundational infrastructure for content creation, decision support, and operational automation. Open-source model availability and specialized vertical AI solutions are expected to accelerate adoption across mid-market and emerging economy enterprises.

Research Methodology

Primary Research

Primary research included interviews with senior AI product executives at leading technology companies, enterprise AI deployment leaders, cloud infrastructure decision-makers, venture capital investors, and enterprise adopters, validating market sizing, technology segmentation, regional demand patterns, and competitive positioning dynamics.

Secondary Research

Secondary sources included OECD AI Policy Observatory data, Gartner technology forecasts, IDC spending guides, and annual reports, press releases, and investor presentations from listed technology companies and AI research organizations.

Forecasting Models

Market forecasts used top-down and bottom-up models combining enterprise AI spending patterns, cloud infrastructure growth rates, model API usage trends, regional technology adoption curves, and venture capital investment trajectories. Scenario analysis addressed computational cost variation and regulatory environment evolution.

Generative AI Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Offering Types Covered | Image, Video, Speech, Others |

| Technology Types Covered | Autoencoders, Generative Adversarial Networks, Others |

| Applications Covered | Healthcare, Generative Intelligence, Media and Entertainment, Others |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Microsoft, OpenAI, Amazon.com, Inc., NVIDIA Corporation, Adobe, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the generative AI market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global generative AI market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the generative AI industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Generative AI Market Report

The global market was valued at USD 17.17 Billion in 2025, driven by enterprise adoption, foundation model advances, and expanding AI applications across industries.

The market is projected to grow at 16.12% CAGR from 2026 to 2034, reaching USD 68.50 Billion, supported by rising enterprise AI deployment and falling computational costs.

Generative adversarial networks lead at 66.9% in 2025, driven by image synthesis, data augmentation, and creative content generation. Autoencoders at 21.8% serve anomaly detection and representation learning.

Generative intelligence dominates at 34.7% in 2025, driven by enterprise demand for automated reasoning, decision support, and workflow optimization across business functions.

North America commands 40.6% in 2025, led by the United States, fueled by venture capital concentration, hyperscaler investments, and leading AI research organizations.

Leading players include Microsoft, OpenAI, Amazon.com, Inc., NVIDIA Corporation, and Adobe, among others.

Agentic AI growth is driven by enterprise demand for autonomous workflow execution, multi-step task planning, and AI-powered decision-making that reduces operational costs and improves efficiency.

Generative AI is accelerating drug discovery, improving diagnostic imaging accuracy, automating clinical documentation, and enabling personalized treatment planning across healthcare systems.

Cloud platforms provide scalable GPU access, model hosting, and API distribution that lower barriers to enterprise AI adoption and enable cost-effective deployment of generative AI solutions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)