Generic Injectables Market Size, Share, Trends and Forecast by Therapeutic Area, Container, Distribution Channel, and Region, 2026-2034

Global Generic Injectables Market Size, Share, Trends & Forecast (2026-2034)

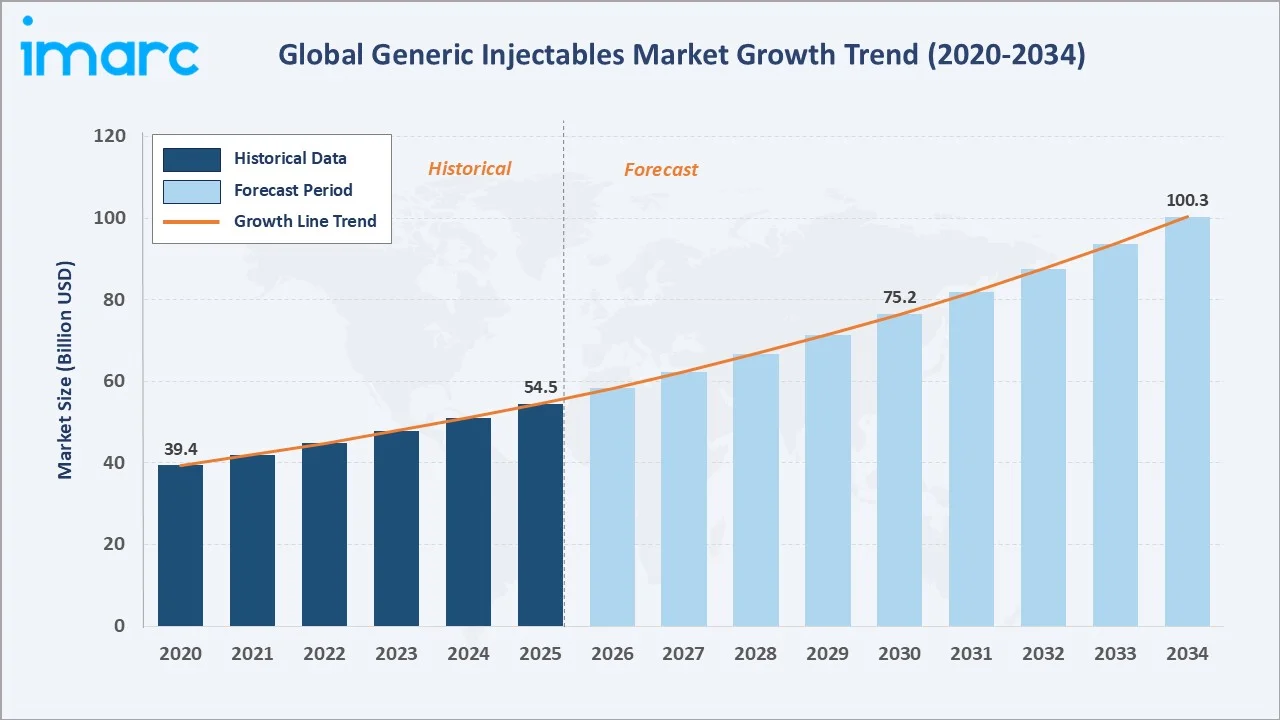

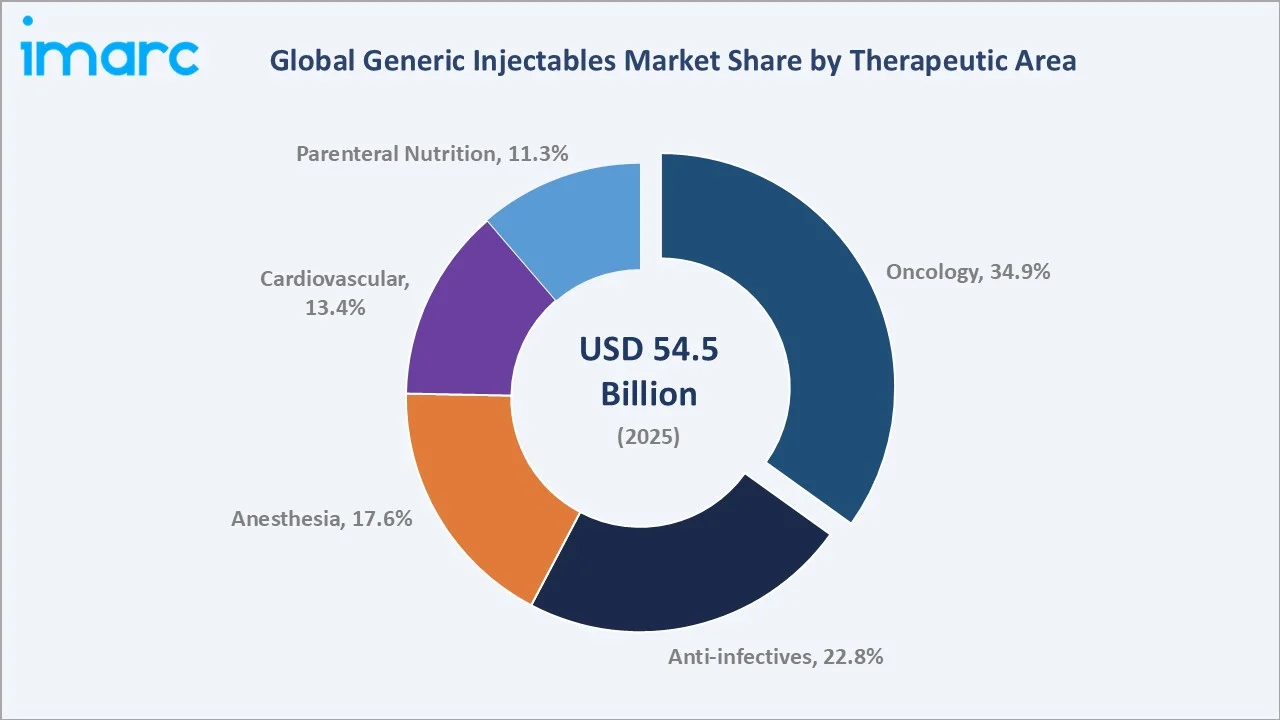

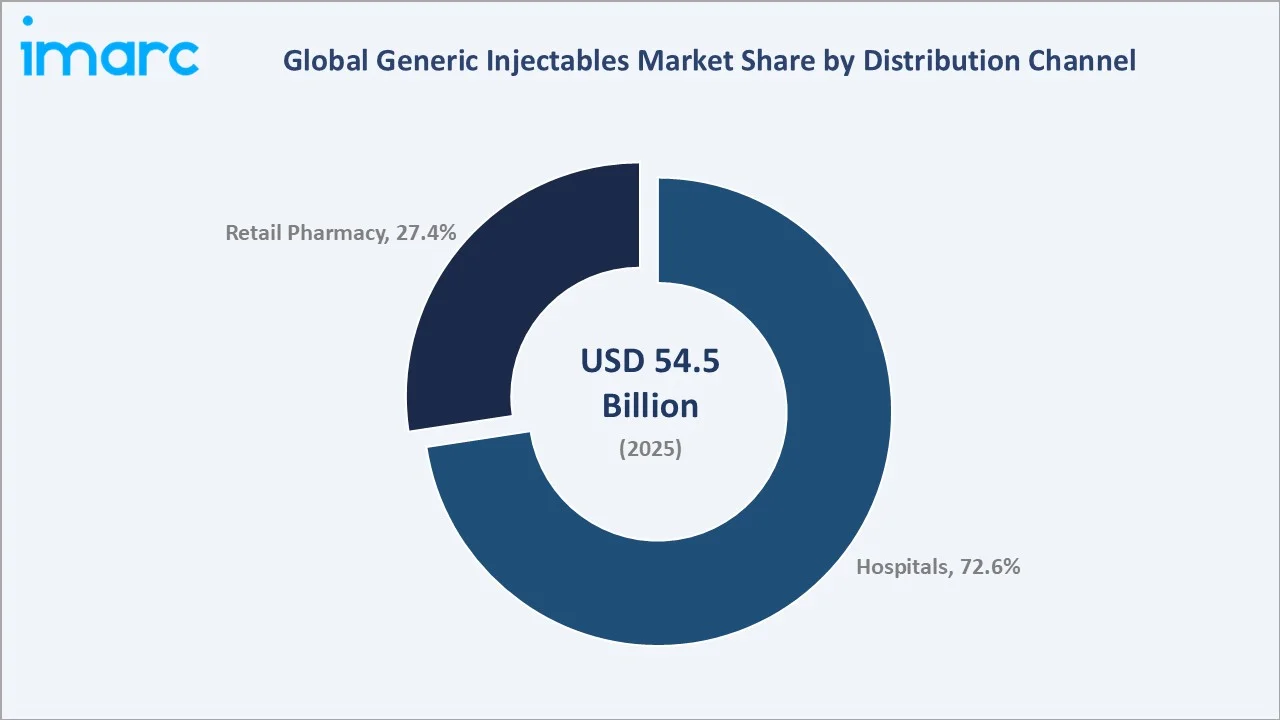

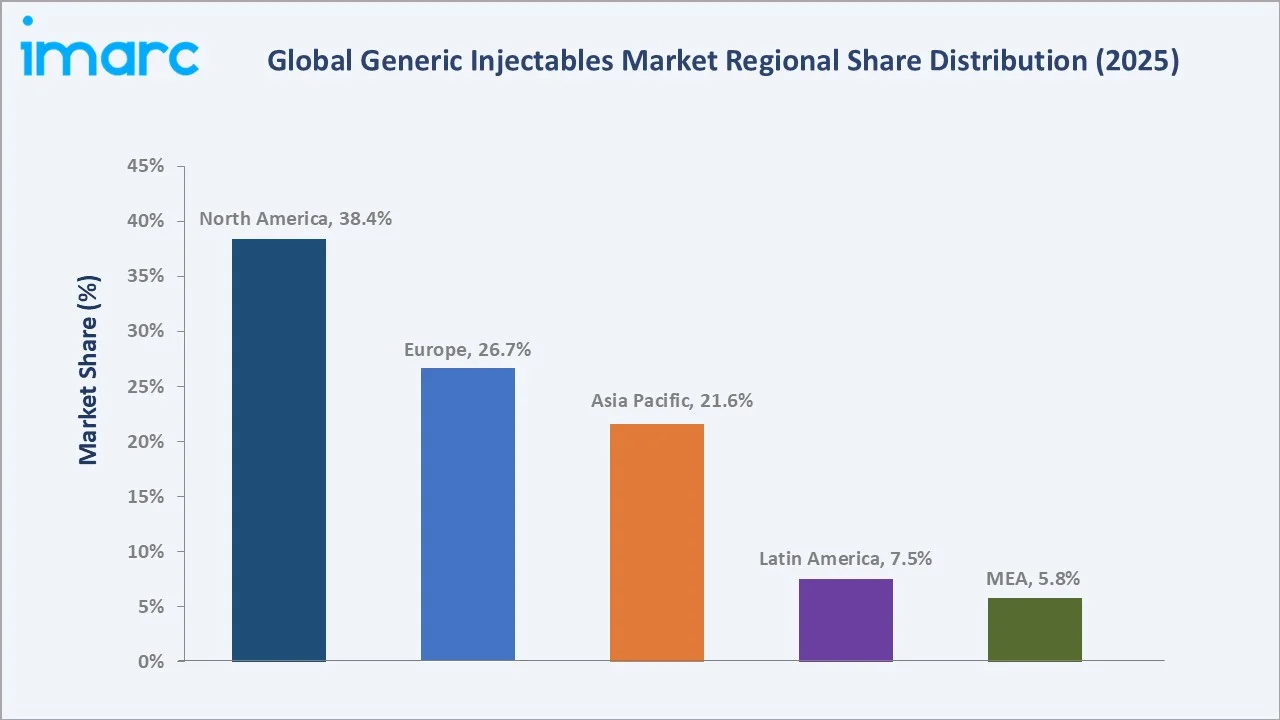

The global generic injectables market was valued at USD 54.5 Billion in 2025 and is projected to reach USD 100.3 Billion by 2034, expanding at a CAGR of 6.67% during 2026-2034. Growth is anchored by the global patent expiry wave for high-value oncology biologics, escalating cancer incidence with 2,041,910 new cancer cases and 618,120 cancer deaths occurred in 2025 in the United States, government-mandated generic utilization reducing healthcare costs, and expanding hospital infrastructure in emerging markets. Oncology leads the therapeutic area at 34.9%, hospitals dominate distribution at 72.6%, and North America commands 38.4% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 54.5 Billion |

|

Forecast Market Size (2034) |

USD 100.3 Billion |

|

CAGR (2026-2034) |

6.67% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

North America (38.4%, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~8.4%, 2026-2034) |

The global generic injectables market growth expanded from USD 39.4 Billion in 2020 to USD 54.5 Billion in 2025, driven by COVID-19 critical care injectable demand, accelerated biosimilar approvals, and the trastuzumab and bevacizumab biosimilar launches across North America and Europe. Anchored at USD 75.2 Billion in 2030, the forecast to USD 100.3 Billion by 2034, underpinned by continuous patent expiration events and expanding oncology generic portfolios.

To get more information on this market, Request Sample

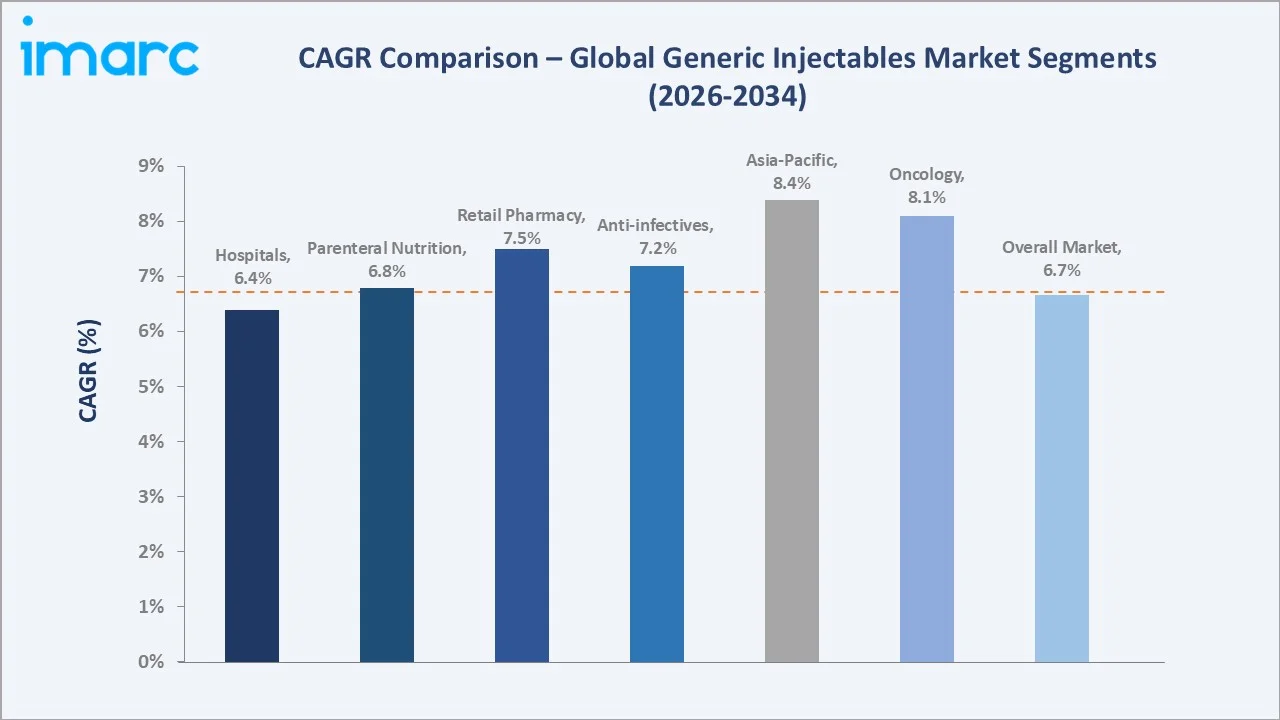

The CAGR across key segments with Asia Pacific at ~8.4% CAGR grows fastest regionally, driven by China’s volume-based procurement (VBP) policy mandating generic substitution, India’s CDMO export expansion, and Japan’s generic substitution target. The oncology segment at ~8.1% CAGR reflects the biennial approval pattern of major cancer biosimilars, with rituximab, trastuzumab, and bevacizumab biosimilar market maturation driving volume even as newer checkpoint inhibitor biosimilars enter the pipeline for post-2026 approval.

Executive Summary

The global generic injectables market expanded from USD 39.4 Billion in 2020 to USD 54.5 Billion in 2025, driven by COVID-19’s acceleration of hospital-based injectable demand, the commencement of major oncology biologic patent expiries, and global healthcare systems’ post-pandemic prioritization of pharmaceutical cost containment through generic mandates. Generic injectables represent the highest clinical value and highest complexity segment of the global generic pharmaceutical industry, sterile manufacturing’s capital intensity, regulatory rigor, and cold-chain logistics requirements create barriers to entry that sustain pricing above commodity oral generics while serving the acute care, oncology, and intensive care settings where injectable drug delivery is the only clinically appropriate route of administration.

Oncology leads at 34.9% as the global cancer burden reaches 20 million new diagnoses in 2022 and is predicted to increase to 35 million by 2050, with cancer treatment protocols requiring injectable chemotherapy, targeted therapy, or immunotherapy administration. Biosimilar oncology injectables are displacing branded biologic revenues at price discounts, driving biosimilar injectable pipeline expansion as the highest-value generic injectable category. North America’s 38.4% dominance reflects the US market’s unique combination of Inflation Reduction Act generic pricing pressure, Medicare’s mandatory generic substitution, and 340B Drug Pricing Program hospitals’ concentrated generic injectable procurement.

Key Market Insights

|

Insight |

Data |

|

Dominant Therapeutic Area |

Oncology – 34.9% revenue share (2025) |

|

Dominant Distribution Channel |

Hospitals – 72.6% revenue share (2025) |

|

Leading Region |

North America – 38.4% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~8.4%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Oncology at 34.9% as the defining growth engine for generic injectables: The global oncology drug market growth represents the largest patent expiry opportunity in pharmaceutical history for generic injectable manufacturers.

- Hospitals at 72.6% reflecting injectables’ inherent acute care delivery nature: Generic injectables’ hospital dominance is structurally fixed by pharmacology: IV bolus and infusion administration requires clinically supervised settings, sterile compounding environments, and real-time patient monitoring that home and retail pharmacy settings cannot routinely provide for acute care indications.

- North America at 38.4% as global generic injectable pricing benchmark: Generic drugs are a crucial part of the healthcare system in the United States, making up over 90% of all prescriptions filled in the country, driving the market growth in the region.

- Asia Pacific growing fastest at ~8.9% CAGR: India, with over 670 US FDA-approved facilities and major players like Sun Pharma, Cipla, and Dr. Reddy’s, positions India as the world’s lowest-cost generic injectable manufacturing hub for complex sterile products.

Global Generic Injectables Market Overview

Generic injectables are sterile pharmaceutical preparations administered parenterally, intravenously (IV bolus, IV infusion), intramuscularly (IM), subcutaneously (SC), or intrathecally (IT), containing active pharmaceutical ingredients whose brand-name equivalents have lost patent exclusivity or regulatory market exclusivity, enabling generic manufacturers to file Abbreviated New Drug Applications (ANDA) in the US, or equivalent abbreviated approval pathways in Europe and other regulated markets. The global generic injectable ecosystem encompasses API manufacturing, sterile manufacturing (vials, ampoules, premix bags, prefilled syringes), contract manufacturing organizations (CMOs), wholesale distribution, and hospital/retail pharmacy dispensing across therapeutic areas, including oncology, anti-infectives, anesthesia, cardiovascular, and parenteral nutrition.

Applications range from life-saving acute care (broad-spectrum antibiotic injectables for sepsis, vasopressor injectables for hemodynamic shock), through chronic disease management (insulin injectables for diabetes, immunosuppressant injectables for autoimmune diseases), to curative intent oncology treatment (cytotoxic chemotherapy, biosimilar monoclonal antibodies). Macroeconomic drivers include healthcare cost containment legislation, the oncology patent expiry wave, global cancer incidence, emerging market hospital infrastructure expansion, and the WHO’s essential medicines generic access programs, creating public sector demand.

Market Dynamics

To evaluate market opportunities, Request Sample

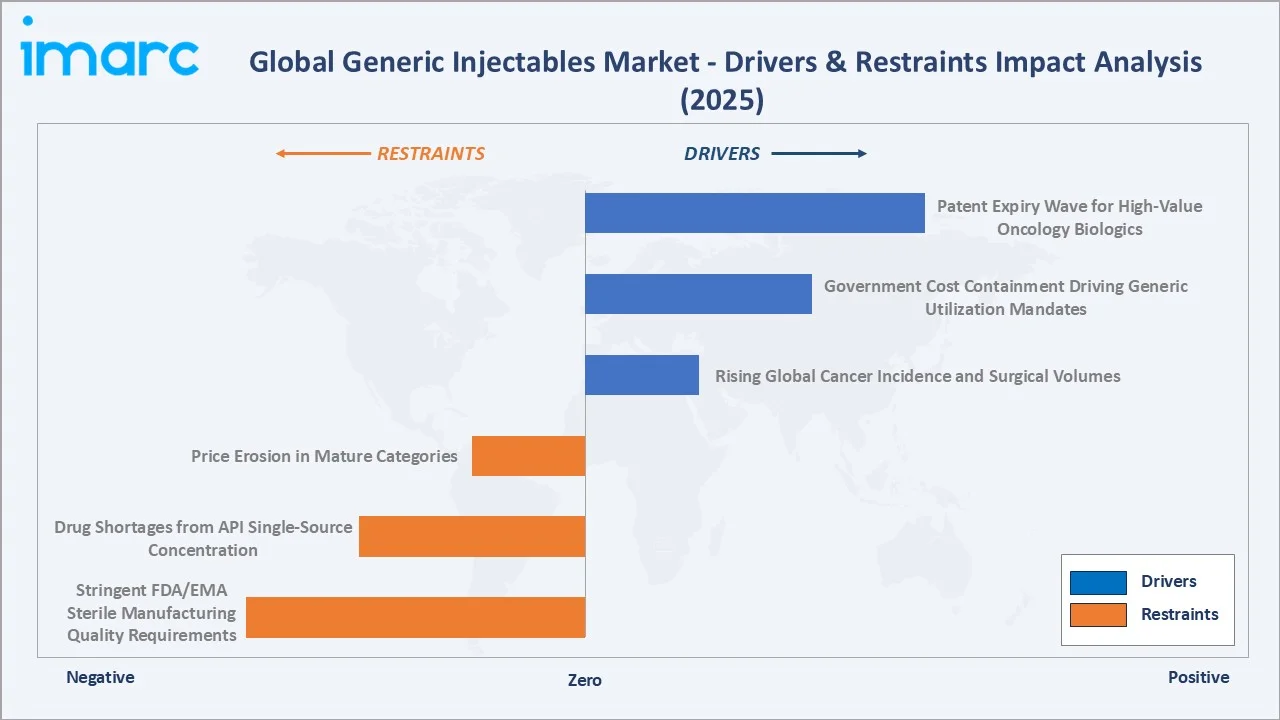

Market Drivers

- Patent Expiry Wave for High-Value Oncology Biologics: The global branded pharmaceutical industry faces the largest patent expiry wave in oncology history. This patent expiry wave is creating the largest individual generic injectable market entry opportunities in pharmaceutical history.

- Government Cost Containment Driving Generic Utilization Mandates: Healthcare payer systems globally are implementing progressively more aggressive generic utilization mandates specifically targeting injectable markets: US Medicare Part B average sales price (ASP) +6% reimbursement, creating automatic generic substitution incentives when generics are available at a lower ASP.

- Rising Global Cancer Incidence and Surgical Volumes: According to the American Cancer Society, 20 million new cancer cases occurred in 2022 and are projected to increase to 35 million by 2050. Each oncology patient undergoing chemotherapy consumes USD 5,000‐80,000 in generic injectable chemotherapy annually, carboplatin, paclitaxel, docetaxel, gemcitabine, and 5-fluorouracil collectively represent 5+ billion units of generic injectable oncology volume globally.

Market Restraints

- Stringent FDA/EMA Sterile Manufacturing Quality Requirements: FDA’s 21 CFR Part 211 and EU GMP Annex 1 requirements for sterile injectable manufacturing impose USD 50–500 million in facility investment and ongoing compliance costs that limit market entry to well-capitalized manufacturers.

- Drug Shortages from API Single-Source Concentration: FDA’s annual drug shortage list is dominated by generic injectables, 75%+ of active US drug shortages are sterile injectable products.

Market Opportunities

- Biosimilar Generic Injectables as the Highest-Value Growth Category: Biosimilar injectables, monoclonal antibodies, fusion proteins, cytokines, and peptide hormones administered by injection or infusion represent the fastest-growing and highest-value generic injectable category, with the global biosimilar market growth.

- Ready-to-Use (RTU) and Ready-to-Administer (RTA) Injectable Format Premiumization: Hospital pharmacy medication error reduction programs are driving systematic migration from pharmacy bulk reconstitution to RTU premixed and RTA prefilled syringe formats, commanding price premiums over equivalent bulk vial presentations.

Market Challenges

- Price Erosion in Commoditized Generic Injectable Categories: Mature commoditized generic injectable categories experience sustained annual price erosion of 5‐15% from multi-manufacturer competition, GPO competitive bidding, and government reference pricing.

- Supply Chain Geopolitical Concentration Risk: 70–80% of global generic injectable API supply originates from India and China, creating concentrated geopolitical supply risk that COVID-19 exposed when Indian export restrictions on API and finished pharmaceutical products in March–May 2020 threatened global hospital supply of generic injectables for critically ill COVID patients.

Emerging Market Trends

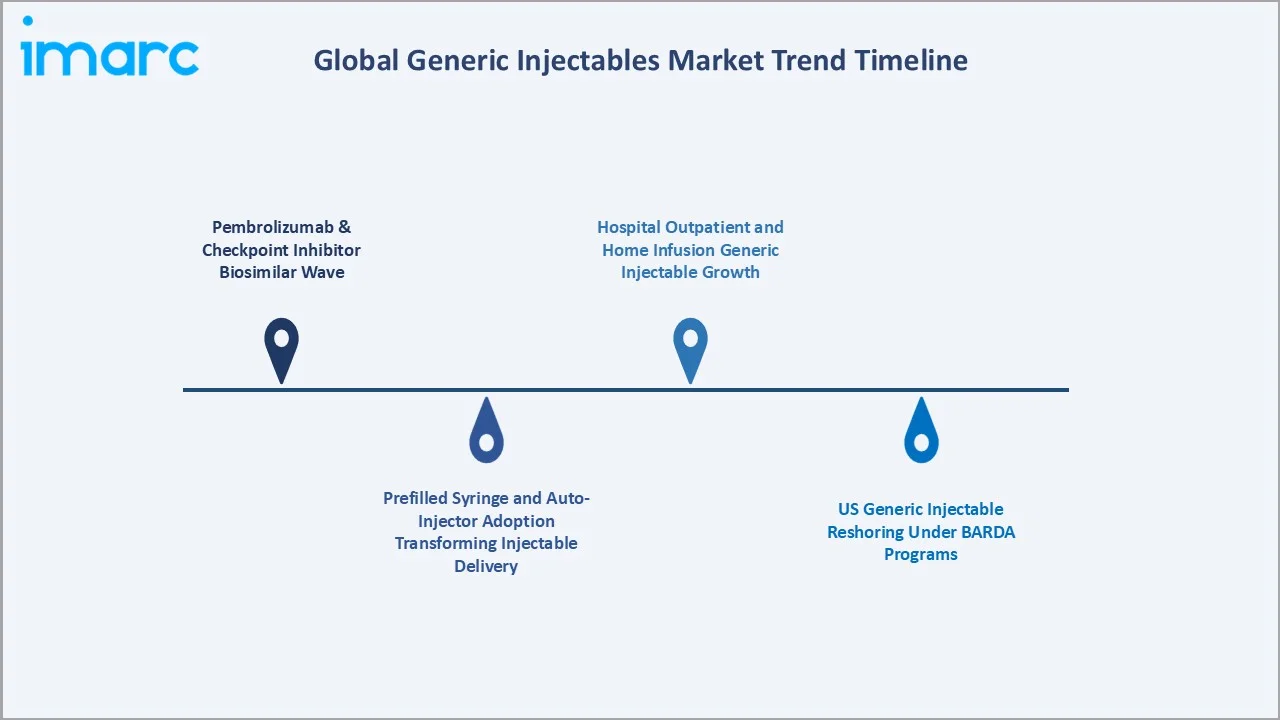

1. Pembrolizumab and Checkpoint Inhibitor Biosimilar Wave Creating Next Generic Oncology Super-Cycle

Merck’s pembrolizumab (Keytruda) faces composition-of-matter patent expiry in the US in 2028. This checkpoint inhibitor biosimilar wave, including nivolumab, atezolizumab, and durvalumab following pembrolizumab, will sustain a generic oncology injectable growth through 2034.

2. Prefilled Syringe and Auto-Injector Adoption Transforming Injectable Delivery

The global pharmaceutical industry’s systematic migration from multi-dose vials to prefilled syringes (PFS) and auto-injector formats is reshaping generic injectable container mix and pricing. Generic PFS products command price premiums over equivalent vial presentations due to unit-dose sterility, reduced medication error risk, and patient convenience.

3. US Generic Injectable Reshoring Under BARDA and PHEMCE Programs

In May 2020, the US Department of Health and Human Services (HHS) revealed a four-year, $354-million partnership with the private sector to manufacture generic sterile injectable medicines, from raw materials to completed drug products, for use in public health emergencies and the national stockpile. The program is funded with federal resources from the Biomedical Advanced Research and Development Authority (BARDA).

4. Hospital Outpatient and Home Infusion Generic Injectable Growth

US hospital outpatient infusion therapy, moving IV antibiotics, biologics, and specialty injectable administration from inpatient to outpatient and home settings, is growing annually, expanding the generic injectable addressable market beyond acute care hospital settings.

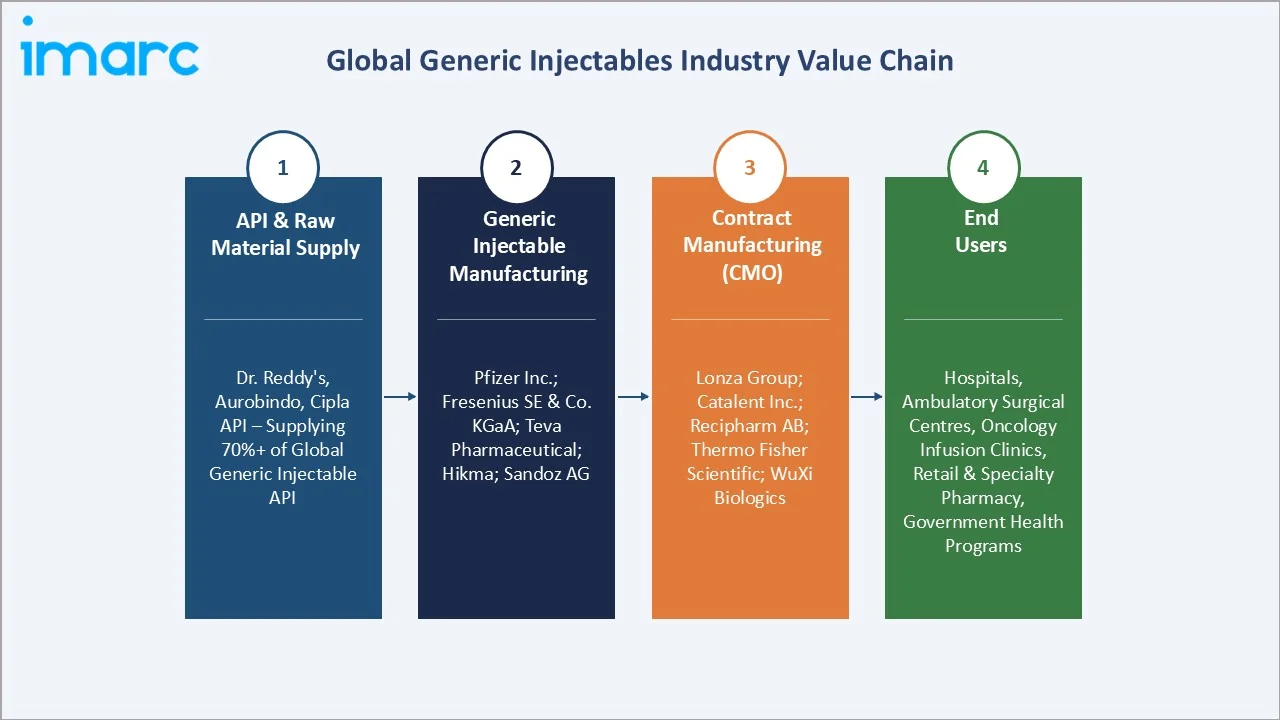

Industry Value Chain Analysis

The global generic injectable value chain integrates API manufacturing, primary packaging production, sterile fill-finish manufacturing, quality release, wholesale distribution, and hospital or retail pharmacy dispensing across 150+ countries under global regulatory oversight.

|

Stage |

Key Participants |

|

API & Raw Material Supply |

Active pharmaceutical ingredient (API) manufacturers: Dr. Reddy’s Laboratories API Division, Aurobindo Pharma API, Cipla API (India-based API exporters supplying 70%+ of global generic injectable API) |

|

Generic Injectable Manufacturing |

Pfizer Inc.; Fresenius SE & Co. KGaA; Teva Pharmaceutical; Hikma Pharmaceuticals; Sandoz AG |

|

Contract Manufacturing (CMOs) |

Lonza Group; Catalent Inc.; Recipharm AB; Almac Group; Thermo Fisher Scientific; WuXi Biologics |

|

End Users |

Hospitals and hospital pharmacies; ambulatory surgical centers (ASCs); oncology infusion clinics; retail pharmacy chains; specialty pharmacy; government health programs; specialty clinics |

Sterile fill-finish manufacturing captures the highest per-unit gross margin in the generic injectable value chain at 45‐65% gross margin for complex oncology injectables and 20‐30% for commodity IV solutions. API suppliers command 15‐25% of generic injectable COGS. CMOs generate 20‐30% EBITDA margins on fill-finish contract manufacturing services, with capacity premium pricing during drug shortage periods reaching 3–5× normal rates.

Technology Landscape in the Global Generic Injectables Industry

Continuous Manufacturing and Advanced Aseptic Processing

Traditional generic injectable batch manufacturing is being supplemented by continuous manufacturing approaches that reduce batch cycle time to 4-7 days and improve yield by 15‐25%. Continuous powder-to-vial manufacturing for lyophilized injectables reduces manufacturing cost by 20‐30% versus traditional batch processing for high-volume lyophilized generic injectables.

Biologics and Biosimilar Analytical Characterization Technology

Biosimilar generic injectable development requires more complex analytical characterization versus small-molecule generic injectables, demonstrating structural similarity between the biosimilar and reference biologic across 30‐50 quality attributes.

Cold-Chain Digital Monitoring and Track-and-Trace Technology

Generic biologics and biosimilar injectable cold-chain integrity is monitored through IoT-enabled temperature data loggers providing real-time temperature excursion alerts across global supply chains from India’s manufacturing sites to US hospital pharmacies.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Therapeutic Area | Oncology | 34.9% | 2025 |

| Container | Vials | 🔒 | 2025 |

| Distribution Channel | Hospitals | 72.6% | 2025 |

| Region | North America | 38.4% | 2025 |

By Therapeutic Area

Oncology leads at 34.9% market share (2025). This dominance is driven by the rising new cancer cases, with 20 million new cancer cases in 2022 and is projected to increase to 35 million by 2050, reflecting both the clinical centrality of injectable administration in oncology and the patent expiry-driven biosimilar injectable wave.

To access detailed market analysis, Request Sample

Anti-infectives at 22.8% serve sepsis, post-surgical prophylaxis, and AMR pathogens treatment in acute care settings. Anesthesia at 17.6% encompasses general anesthesia agents, analgesics, and neuromuscular blocking agents. Cardiovascular at 13.4% includes heparin, amiodarone, vasopressor injectables, and antihypertensive IV formulations. Parenteral nutrition at 11.3%, Fresenius Kabi’s dominated category, provides complete nutritional support for ICU patients, neonatal intensive care, and cancer cachexia management.

By Distribution Channel

Hospitals dominate at 72.6% market share (2025). Hospital pharmacies’ dominance is structurally entrenched by the clinical requirements of injectable administration, IV chemotherapy, ICU vasopressor infusions, and post-surgical antibiotic therapy, which require clinician supervision, real-time monitoring, and sterile compounding capabilities only hospital settings can provide.

Retail pharmacy at 27.4% is growing at ~7.5% CAGR, driven by home infusion therapy expansion, specialty pharmacy dispensing of self-injectable biologics (adalimumab biosimilars, insulin biosimilars, GLP-1 receptor agonist injectables), and ambulatory infusion center growth outside hospital systems. The GLP-1 receptor agonist market, with semaglutide (Ozempic generic) and liraglutide (Victoza generic) representing potential in generic injectable retail pharmacy revenue, will significantly shift distribution channel balance toward retail pharmacy as GLP-1 injectable biosimilars achieve FDA approval.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.4% |

US healthcare spending rose by 7.2% to 5.3 trillion in 2024, with generic injectables mandated under the Biologics Price Competition and Innovation (BPCI) Act and the FDA’s 505(b)(2) and ANDA pathways |

|

Europe |

26.7% |

The EU’s hospital drug procurement through national public tender systems generates predictable generic injectable volume at negotiated tender prices |

|

Asia Pacific |

21.6% |

70–80% of global generic injectable API supply originates from China |

|

Latin America |

7.5% |

Brazil’s Unified Health System (SUS) mandatory use of generic medications through government pharmaceutical procurement; Mexico’s IMSS and ISSSTE social security healthcare systems’ generic injectable tenders of hospital drug procurement |

|

Middle East & Africa |

5.8% |

Saudi Arabia’s Vision 2030 pharmaceutical localization program targeting domestic generic production by 2030; UAE’s Dubai Healthcare City as MENA pharmaceutical hub enabling generic injectable distribution across GCC’s population |

North America’s 38.4% dominance is sustained by the US market’s unique pricing environment where complex generic injectables command premiums over European equivalent prices due to market structure, GPO negotiation dynamics, and drug shortage-driven supply scarcity pricing. The US market’s 180-day exclusivity system for first-to-file ANDA generics, creating 6-month market exclusivity with near-branded pricing for breakthrough generic launches, generates first-to-market premium revenue for leading injectable ANDA filers.

Asia Pacific’s 21.6% and fastest CAGR (~8.4%) reflects India and China’s dual role as both the world’s largest generic injectable manufacturing exporters and rapidly growing domestic consumption markets. India’s 1.4 billion population’s growing middle class healthcare demand, Ayushman Bharat’s beneficiary generic prescription program, and India’s rapidly expanding private hospital sector collectively create a domestic generic injectable market growth. 70–80% of global generic injectable API supply originates from India and China, creating the world’s fastest-growing individual-country generic injectable market.

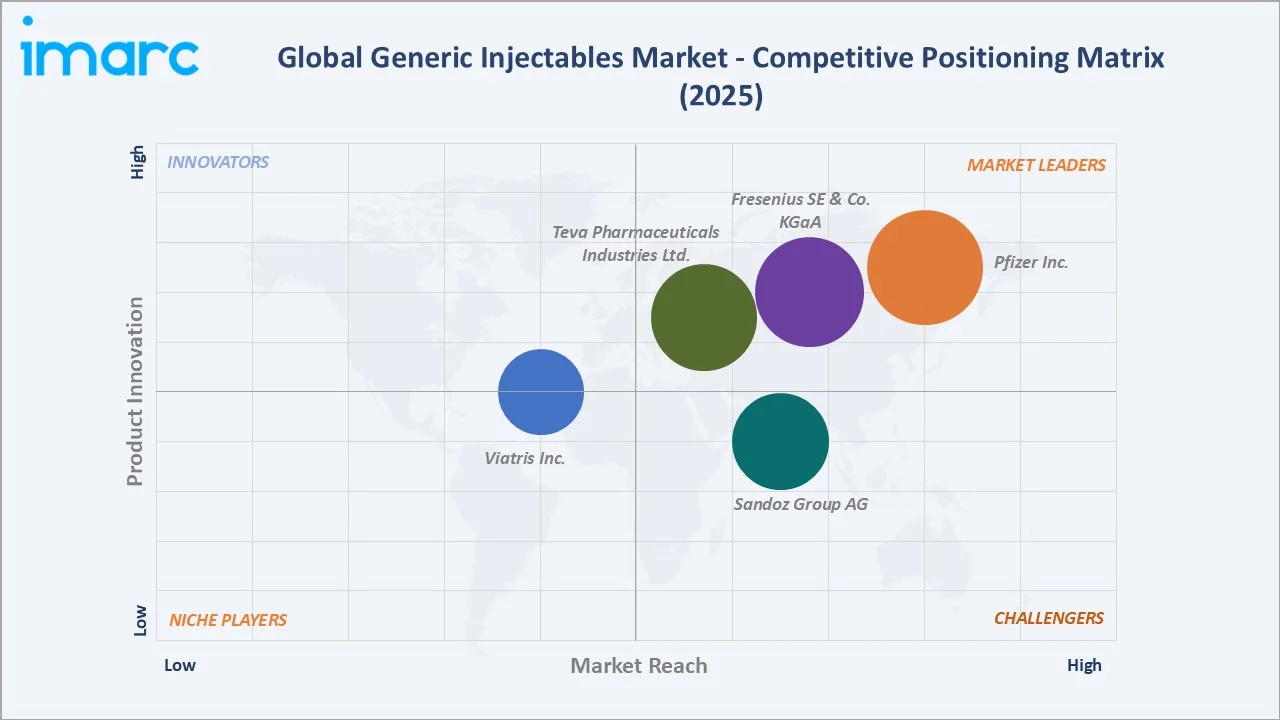

Competitive Landscape

The global generic injectables market is moderately concentrated at the corporate level and highly fragmented at the product/molecule level. Pfizer, Fresenius Kabi, and Teva collectively represent approximately 35‐40% of global organized generic injectable revenue by value. Adding Novartis and Viatris extends the combined share to approximately 55‐60% of the global organized market.

|

Company Name |

Division / Product Line |

Market Position |

Core Strength |

|

Pfizer Inc. |

Epinephrine, Propofol, Fentanyl Citrate, Heparin, Levofloxacin, Docetaxel and Irinotecan Injections |

Market Leader |

World’s largest sterile injectable manufacturer following Hospira acquisition |

|

Fresenius SE & Co. KGaA |

Analgesics and Anesthetics, Antibiotics and Antiinfectants |

Market Leader |

Germany-headquartered Fresenius is one of the world’s leading IV nutrition and parenteral nutrition injectable manufacturers |

|

Teva Pharmaceutical Industries Ltd. |

Carboplatin Injection, Cisplatin Injection, Dalbavancin for Injection, Doxorubicin Hydrochloride Injection, Epinephrine Injection, Fosaprepitant for injection, Hydromorphone Hydrochloride Injection, Liraglutide Injection, Methotrexate Injection, Metoclopramide Injection, Paclitaxel Injection |

Market Leader |

Israel-headquartered Teva is one of the world’s largest generic drug companies by volume |

|

Sandoz Group AG |

Antibiotics, Complex Generic Injectables, Biosimilars |

Strong Challenger |

Basel, Switzerland-headquartered Sandoz is the world’s largest biosimilar and generic injectable company by portfolio breadth |

|

Viatris Inc. |

ACETAMINOPHEN Injection, ACETAZOLAMIDE for injection, ADENOSINE Injection, AMIODARONE HYDROCHLORIDE Injection, ARGATROBAN Injection, BIVALIRUDIN for Injection, CIDOFOVIR Injection, DEXAMETHASONE SODIUM PHOSPHATE Injection, DOCETAXEL Injection, DOXORUBICIN HYDROCHLORIDE for Injection, DOXYCYCLINE for Injection, DECITABINE for Injection |

Established |

Canonsburg, PA-headquartered Viatris, created from Mylan and Pfizer’s Upjohn division merger in 2020, with an injectable portfolio from Mylan’s heritage generic injectable business |

The remaining 40‐45% is distributed across regional and national generic injectable manufacturers, with India’s US FDA-approved injectable manufacturers collectively supplying 20‐25% of global generic injectable volume at the lowest manufacturing cost globally.

Key Company Profiles

Pfizer Inc.

Pfizer Inc. is one of the world’s largest generic injectable manufacturers through its sterile injectables business, the business unit created from Pfizer’s acquisition of Hospira in 2015.

- Product Portfolio: Epinephrine, Propofol, Fentanyl Citrate, Heparin, Levofloxacin, Docetaxel and Irinotecan Injections.

- Recent Developments: In February 2026, Pfizer announced that its experimental ultra-long-acting injectable GLP-1 receptor agonist (PF-08653944 (MET-097i)) showed significant and continued weight loss with monthly dosing in a Phase 2b trial. The company plans to advance 10 Phase 3 trials for this injectable in 2026.

- Strategic Focus: US domestic manufacturing scale providing supply reliability advantage during drug shortage events; biosimilar injectable pipeline as the next revenue growth engine, pembrolizumab and nivolumab biosimilar development targeting 2028–2030 regulatory submissions

Fresenius SE & Co. KGaA

Fresenius SE & Co. KGaA is Germany’s largest healthcare company with Fresenius Kabi, the generic injectables, IV nutrition, and clinical nutrition division.

- Product Portfolio: Analgesics and Anesthetics, Antibiotics and Antiinfectants.

- Recent Developments: In December 2024, Fresenius, through its Fresenius Kabi, launched Epinephrine Injection, USP, which is now available in the United States as the first generic version of Epinephrine in a 1mg/1mL vial for U.S. customers.

- Strategic Focus: Parenteral nutrition market leadership through Kabiven/Perikabiven and Intralipid multi-decade hospital formulary incumbency; biosimilar generic injectable portfolio expansion.

Teva Pharmaceutical Industries Ltd.

Teva Pharmaceutical is the world’s largest generic drug company by total prescription volume, with numerous operating sterile manufacturing sites globally to produce the world’s most comprehensive generic injectable portfolio.

- Product Portfolio: Carboplatin Injection, Cisplatin Injection, Dalbavancin for Injection, Doxorubicin Hydrochloride Injection, Epinephrine Injection, Fosaprepitant for injection, Hydromorphone Hydrochloride Injection, Icatibant Injection, Liraglutide Injection, Methotrexate Injection, Metoclopramide Injection, Paclitaxel Injection.

- Recent Developments: In August 2025, Teva Pharmaceuticals, Inc. announced the FDA approval and U.S. launch of a generic version of Saxenda (liraglutide injection).

- Strategic Focus: Pivot to Growth strategy as margin differentiation from commodity generic erosion; integrated API-injectable vertical manufacturing reducing dependency on China/India API sourcing for key molecules; biosimilar injectable expansion through Celltrion (trastuzumab) and independent development (upcoming checkpoint inhibitor biosimilar program).

Market Concentration Analysis

The global generic injectables market is moderately concentrated at the corporate level top-5 players (Pfizer, Fresenius, Teva Sandoz, and Viatris) representing approximately 45–50% of global organized market revenue, while remaining highly fragmented at the molecule level, with 5‐15 manufacturers per molecule in most commoditized injectable categories. This dual structure creates a market where revenue concentration at the corporate level masks intense product-level competition that drives annual price erosion of 5‐15% in mature categories.

Biosimilar injectable manufacturing exhibits the highest market concentration, with Sandoz, Pfizer, Teva, and Fresenius Kabi collectively holding 65‐70% of the approved biosimilar injectable market share in Europe and 55‐60% in the US. Complex generic injectable formulations represent a moderately concentrated sub-market.

Investment & Growth Opportunities

Fastest Growing Segments

Oncology therapeutic area (~8.1% CAGR), Asia Pacific region (~8.4% CAGR), biosimilar injectables (~20% CAGR), retail pharmacy/home infusion channel (~7.5% CAGR), and complex generic injectable formulations (~12‐15% CAGR) represent the global generic injectable market’s highest-growth investment vectors.

Emerging Geographic Opportunities

China’s VBP program’s generic injectable procurement is the world’s fastest-growing individual country market; India’s domestic generic injectable market growing from Ayushman Bharat expansion; Africa’s essential medicines generic injectable demand growing from hospital infrastructure expansion; GCC’s pharmaceutical localization programs creating premium domestic manufacturing investment incentives; and Latin America’s regional public health tender programs through PAHO represent geographic expansion opportunities for generic injectable manufacturers with cost-competitive manufacturing.

Investment Themes

Global generic injectable investment is shifting from commodity manufacturing scale (IV solutions, basic anti-infectives) toward biosimilar R&D capability (monoclonal antibody characterization and manufacturing), complex formulation development (liposomal, depot, nanoparticle injectables), and US domestic manufacturing resilience (BARDA-funded essential medicines production).

- Biosimilar pipeline investment: Pembrolizumab, nivolumab, atezolizumab checkpoint inhibitor biosimilar development programs targeting 2028–2032 US and European market entry; GLP-1 receptor agonist biosimilars (semaglutide, liraglutide, dulaglutide) targeting 2031–2033 entry; second-generation antibody-drug conjugate (ADC) biosimilars entering development planning stage.

- Manufacturing technology investment: Continuous manufacturing platforms for sterile injectables, reducing batch cycle time, AI-powered quality control systems, Isolator and RABS technology for EU GMP Annex 1 compliance, prefilled syringe fill-finish capacity for self-injectable biosimilar formats.

Future Market Outlook (2026-2034)

The global generic injectables market is entering its most commercially significant phase since the Hatch-Waxman Act’s 1984 creation of the ANDA generic drug pathway. From USD 54.5 Billion in 2025, the market will reach USD 100.3 Billion by 2034, at a 6.67% CAGR driven by the convergence of three historical forces: the oncology biologic patent expiry wave transferring in branded biologic revenue to generic/biosimilar competition between 2025–2034; global healthcare systems’ fiscal sustainability imperatives that make generic injectable mandates politically non-negotiable regardless of pharmaceutical industry lobbying; and Asia Pacific’s emergence as both the world’s largest generic injectable manufacturing platform (India, China) and the world’s fastest-growing consumption market.

Research Methodology

Primary Research

Primary research included structured interviews with 140+ industry stakeholders in 2025, comprising generic injectable manufacturing executives, hospital pharmacy directors and GPO procurement officers, FDA Office of Generic Drugs biosimilar and injectable division representatives, IQVIA and MMIT pharmaceutical market intelligence analysts, regulatory affairs specialists at Sandoz and Baxter, oncology pharmacist advisory panel members, and BARDA essential medicines program policy representatives.

Secondary Research

Secondary research encompassed FDA Orange Book and Purple Book ANDA/BLA approval databases, FDA Drug Shortage Database, IQVIA MIDAS global pharmaceutical market intelligence, WHO Essential Medicines List injectable product classification, EMA European Public Assessment Reports for biosimilar injectable approvals, company annual reports, AABB/ASHP drug shortage survey data, Pharmexcil India pharmaceutical export statistics, and IMARC healthcare industry databases. Over 180 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using a bottom-up therapeutic area × molecule category × regional market aggregation model validated against top-down global pharmaceutical market share models. Key inputs include FDA ANDA approval pipeline trajectory for injectable categories, biosimilar patent expiry timelines and penetration curves derived from trastuzumab/rituximab European precedent analysis, WHO cancer incidence projections by region, global hospital volume growth forecasts, and manufacturing capacity expansion plans from public company capital program disclosures.

Generic Injectables Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Therapeutic Areas Covered | Oncology, Anaesthesia, Anti-infectives, Parenteral Nutrition, Cardiovascular |

| Containers Covered | Vials, Ampoules, Premix, Prefilled Syringes |

| Distribution Channels Covered | Hospitals, Retail Pharmacy |

| Regions Covered | Europe, North America, Asia, Latin America, Middle East and Africa |

| Companies Covered | Pfizer Inc., Fresenius SE & Co. KGaA, Teva Pharmaceutical Industries Ltd., Sandoz Group AG, Viatris Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the generic injectables market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global generic injectables market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the generic injectables industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Generic Injectables Market Report

The global generic injectables market was valued at USD 54.5 Billion in 2025 and is projected to reach USD 100.3 Billion by 2034.

The global generic injectables market is forecast to grow at a CAGR of 6.67% during 2026-2034, driven by oncology biologic patent expiries, government generic mandates, rising cancer incidence, and biosimilar injection scaling.

Oncology leads with 34.9% revenue share (2025), driven by 20 million new global cancer diagnoses in 2022 requiring injectable chemotherapy and biosimilar monoclonal antibody treatment protocols.

Hospitals lead with 72.6% share (2025) as IV administration requires clinical supervision, sterile compounding, and real-time monitoring that only hospital settings provide for acute care indications.

North America leads with 38.4% share (2025), driven by the US market’s premium generic injectable pricing, FDA ANDA 180-day exclusivity system, Medicare Part B generic mandates, and GPO hospital contract concentration.

Key companies include Pfizer Inc., Fresenius SE & Co. KGaA, Teva Pharmaceutical Industries Ltd., Sandoz AG, and Viatris Inc.

Key drivers include the oncology biologic patent expiry wave (trastuzumab, rituximab biosimilars established; pembrolizumab, nivolumab upcoming), government healthcare cost containment generic mandates, rising global cancer incidence, emerging market hospital infrastructure expansion, and Asia Pacific manufacturing scale.

Key trends include biosimilar injectable scaling, prefilled syringe migration, AI-powered sterile manufacturing QC, US domestic manufacturing reshoring (BARDA program), checkpoint inhibitor biosimilar development, and home infusion expansion of the retail injectable channel.

Key challenges include FDA/EMA sterile manufacturing warning letters disrupting supply, chronic drug shortages from API single-source concentration, biosimilar development cost of USD 100–300 million per program, cold-chain logistics cost for biologics, and 5‐15% annual price erosion in commoditized injectable categories.

Top opportunities include biosimilar pembrolizumab/nivolumab development, complex generic injectable formulations, US domestic manufacturing BARDA contracts, GLP-1 receptor agonist biosimilar entry, and China/India VBP program generic injectable supply.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)