Germany Data Center Market Size, Share, Trends and Forecast by Component, Type, Enterprise Size, End User, and Region, 2026-2034

Germany Data Center Market Size, Share, Trends & Forecast (2026-2034)

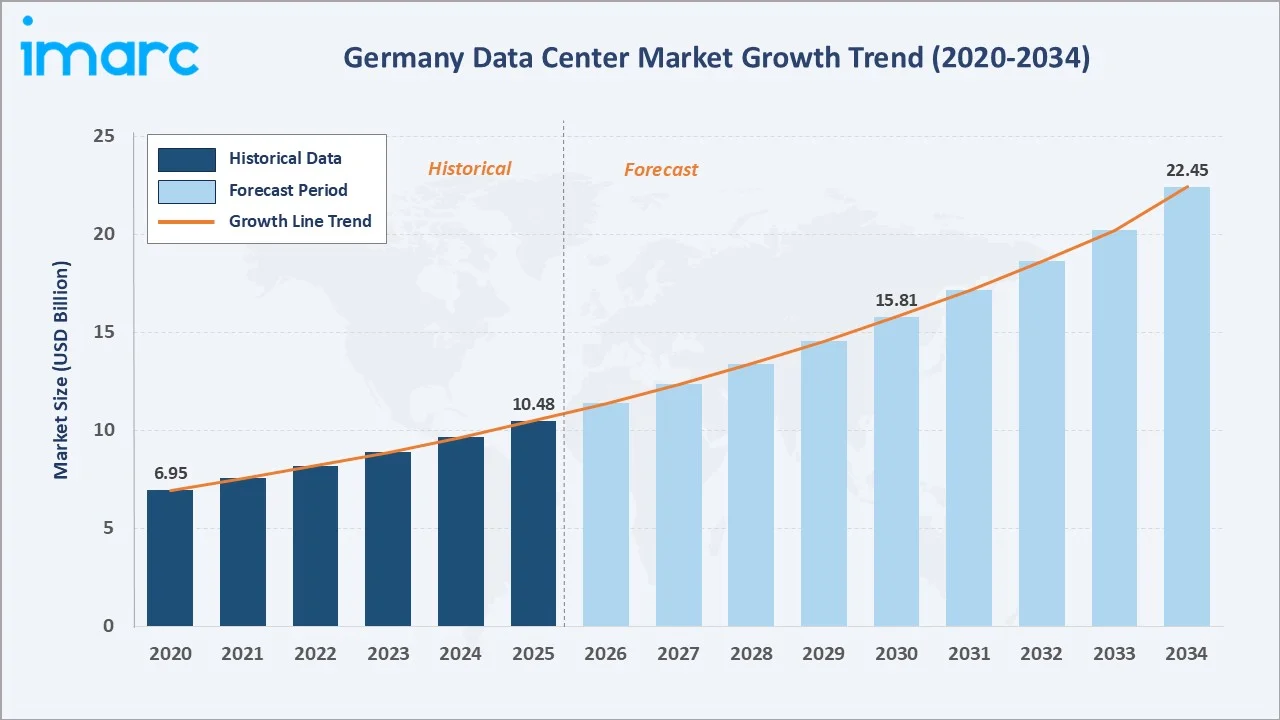

The Germany data center market reached USD 10.48 Billion in 2025 and is projected to reach USD 22.45 Billion by 2034, growing at a CAGR of 8.57% during 2026-2034. Accelerating AI and cloud adoption, Germany's role as Europe's premier internet exchange hub, large-scale hyperscaler campus investments, and the country's stringent data sovereignty framework are collectively driving sustained double-digit investment across colocation, hyperscale, and edge infrastructure throughout the forecast period.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 10.48 Billion |

|

Forecast Market Size (2034) |

USD 22.45 Billion |

|

CAGR (2026-2034) |

8.57% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

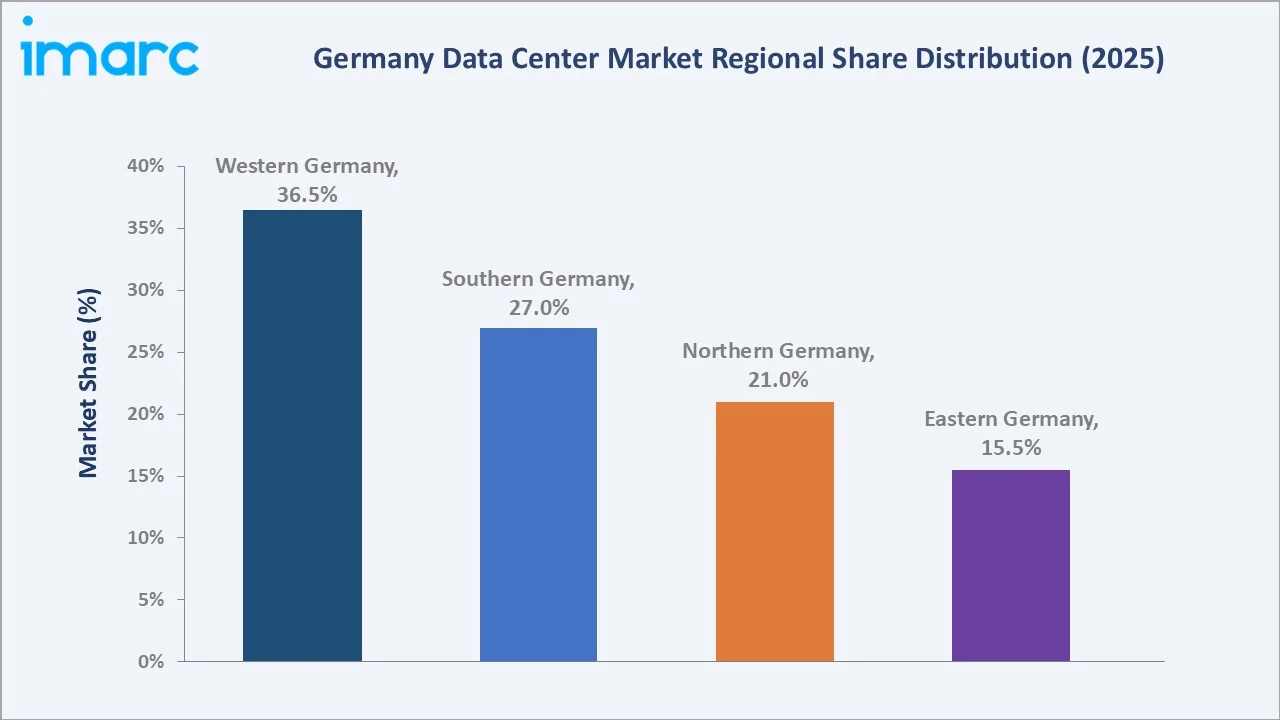

Western Germany leads regionally at 36.5% in 2025, anchored by Frankfurt, Europe's largest internet exchange and colocation hub. Solution components dominate at 68.0%, while colocation maintains the largest type share at 38.5%. Edge data centers represent the fastest-growing type at ~12.3% CAGR, driven by latency-sensitive AI inferencing and industrial IoT workloads across Germany's Mittelstand manufacturing belt.

To get more information on this market, Request Sample

Germany's data center market grew from USD 6.95 Billion in 2020 to USD 10.48 Billion in 2025, an absolute gain of USD 3.53 Billion over five years. The acceleration is structurally underpinned by three catalysts: Germany's role as the GDPR-compliant data sovereignty anchor for European multinationals, the Frankfurt internet exchange ecosystem's DE-CIX handling over 14 Tbps of peak traffic, and post-2023 GPU cluster demand that is doubling hyperscale pre-lease pipelines annually.

Executive Summary

Germany's data center market is expanding at an 8.57% CAGR, driven by AI workload proliferation, European cloud sovereignty mandates, and accelerating hyperscaler capex commitments. The market grew from USD 6.95 Billion in 2020 to USD 10.48 Billion in 2025 and is forecast to reach USD 22.45 Billion by 2034, adding USD 11.97 Billion in incremental value.

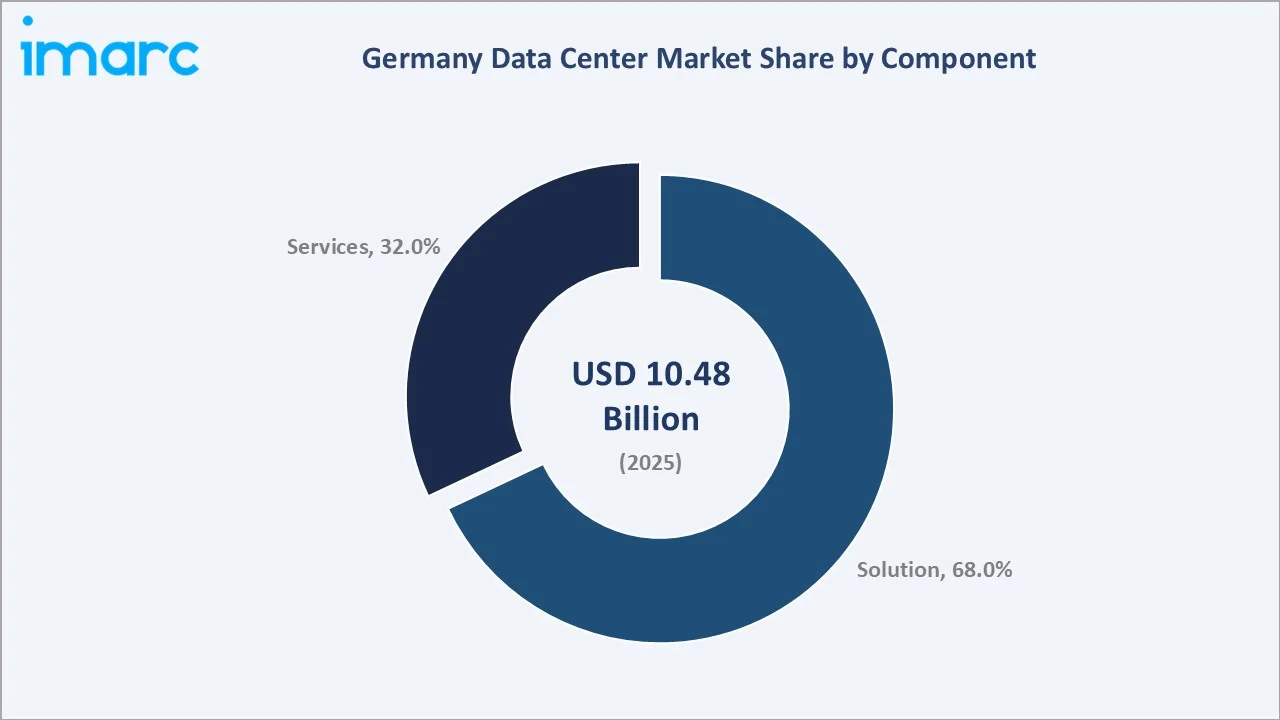

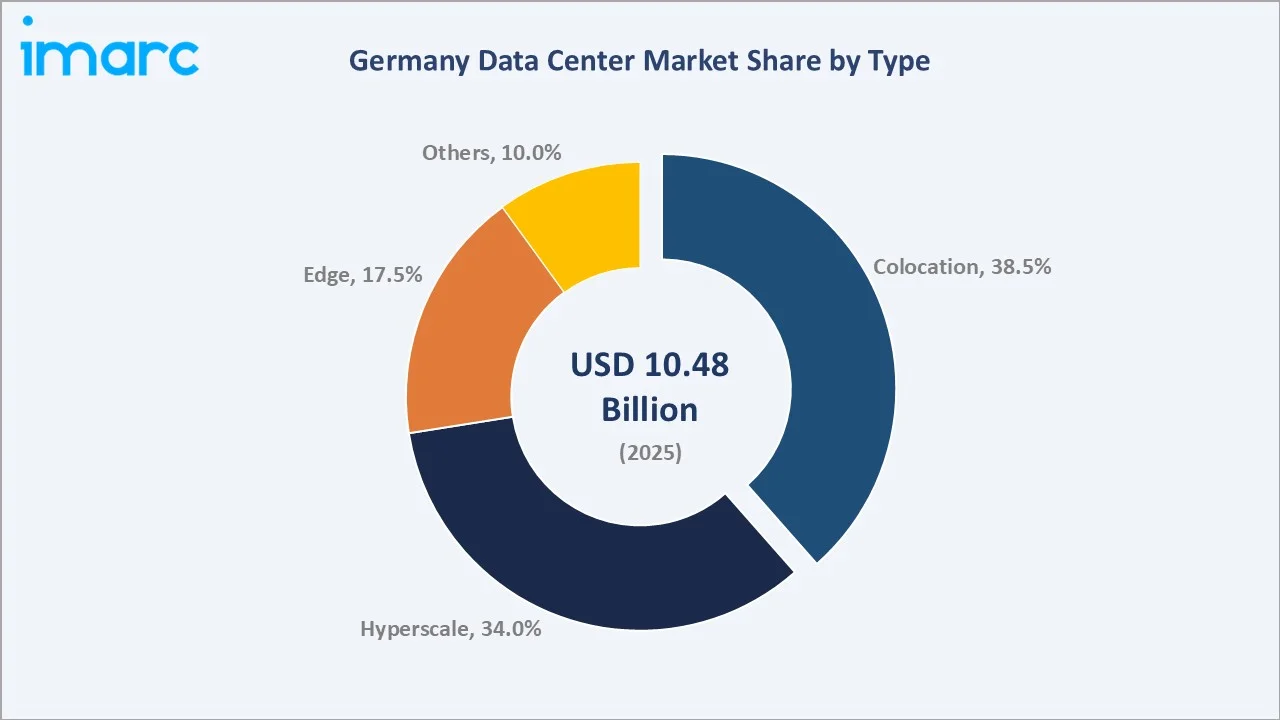

Solution components dominate at 68.0% in 2025, encompassing servers, storage, networking equipment, and power and cooling infrastructure. Services at 32.0% represent the fastest-growing component category at ~9.1% CAGR, as managed services, cloud-adjacent colocation, and professional services for AI infrastructure integration scale rapidly. Colocation leads the type segment at 38.5%, with hyperscale at 34.0% and edge at 17.5%.

Equinix Inc., Portus Data Centers S.à r.l., Deutsche Telekom AG, NTT DATA Group Corporation, and United Internet AG collectively anchor the competitive landscape. Key infrastructure investment milestones through 2034 include AWS's EUR 7.8 Billion German cloud region investment and Microsoft’s doubled capacity of its Azure cloud infrastructure in Germany, collectively adding over 500 MW of new IT load capacity.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Solution – 68.0% share (2025) |

|

Fastest Growing Component |

Services – ~9.1% CAGR (2026-2034) |

|

Largest Type |

Colocation – 38.5% share (2025) |

|

Fastest Growing Type |

Edge – ~12.3% CAGR (2026-2034) |

|

Leading Region |

Western Germany – 36.5% share (2025) |

|

Top Companies |

Equinix Inc., Portus Data Centers S.à r.l., Deutsche Telekom AG, NTT DATA Group Corporation, and United Internet AG |

Key Analytical Observations Supporting The Above Data:

- Solution at 68.0% (2025) reflects Germany's mature IT hardware refresh cycle and the large-scale AI infrastructure investment by hyperscalers. GPU server clusters for AI training, high-capacity NVMe storage arrays, and spine-leaf 400G networking equipment are the fastest-growing solution sub-categories, each growing at 15–25% annually as AI workloads intensify.

- Colocation at 38.5% (2025) is driven by Frankfurt's unrivalled connectivity ecosystem: DE-CIX, 10,000+ km of dark fiber, and 300+ cloud on-ramps enable enterprises to achieve sub-1ms latency to all major cloud platforms.

- Western Germany at 36.5% (2025) leads all regions, anchored by Frankfurt's hyperscale and colocation concentration in Hessen and the Rhine-Ruhr conurbation's dense enterprise IT base in NRW. A new 200 MW data center campus is planned by Argaman Group in Birstein, about 60 km northeast of Frankfurt, with construction expected to be completed by 2028.

- Edge at ~12.3% CAGR is the fastest-growing type, driven by autonomous vehicle processing at BMW's Munich facilities, smart factory latency requirements across Baden-Württemberg's manufacturing corridor, and 5G edge MEC (multi-access edge computing) deployments by Deutsche Telekom and Vodafone Germany.

Germany Data Center Market Overview

Germany's data center market encompasses colocation facilities, hyperscale campuses, enterprise-owned data centers, and distributed edge nodes providing compute, storage, networking, and managed services to enterprises, government agencies, financial institutions, and hyperscale cloud providers. Germany is Europe's largest national data center market by revenue, supported by Frankfurt's position as the continent's premier internet exchange hub and GDPR-enforced data residency requirements.

Germany's data center market has been shaped by landmark regulatory and investment events: the GDPR's May 2018 enforcement that cemented Germany's data sovereignty role, the 2020–2022 hyperscaler mega-campus announcement wave, and the 2023–2024 AI workload surge that is re-engineering facility power density requirements from 5 kW/rack to 40–100 kW/rack for GPU cluster deployments.

Market Dynamics

To evaluate market opportunities, Request Sample

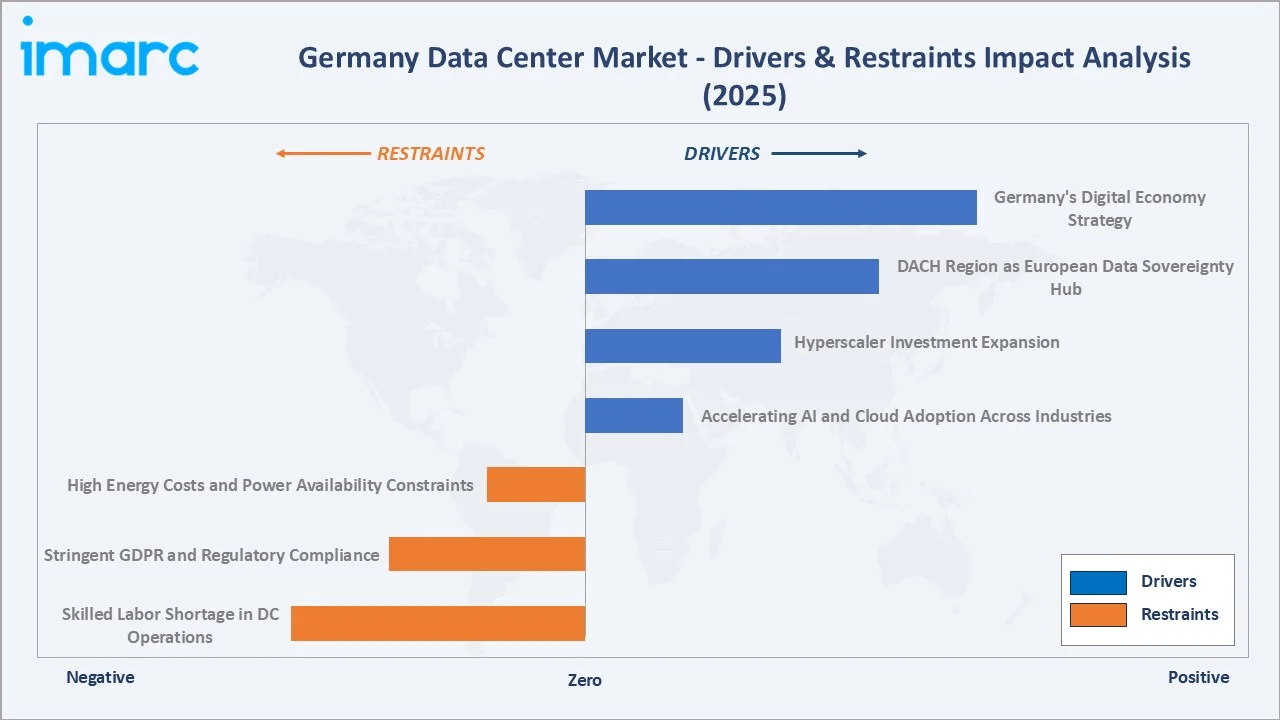

Market Drivers

- Accelerating AI and Cloud Adoption Across Industries: The EU’s Digital Connectivity policy for Germany outlines the country’s national Gigabit and Digital Strategies, aiming for nationwide fiber‑optic and advanced mobile coverage by 2030. AI adoption in automotive, financial services, and manufacturing is driving GPU cluster demand that requires 40–100 kW/rack density, an 8–20x increase over traditional enterprise workloads.

- Hyperscaler Investment Expansion: AWS announced a EUR 7.8 Billion investment in German cloud infrastructure through 2040; Microsoft doubled the capacity of its Azure cloud infrastructure in Germany in December 2023, significantly expanding the Frankfurt‑area data center region to meet rising demand for cloud and AI services.

- DACH Region as European Data Sovereignty Hub: GDPR enforcement and the EU Data Act 2025 require financial institutions, healthcare providers, and public sector entities to process personal data within German or EU borders. Germany's Gaia-X initiative is creating captive government and regulated-sector demand for compliant, domestically hosted data infrastructure.

- Germany's Digital Economy Strategy: The Federal Ministry for Digitalisation and State Modernisation (BMDS) is advancing Germany’s nationwide fiber optic rollout through its “Gigabitförderung 2.0” program, allocating €3.6 billion in 2023. This funding is expected to enable 638,000 new high-speed fiber connections across approximately 2,300 municipalities, expanding access to Germany’s high-performance broadband network.

Market Restraints

- High Energy Costs and Power Availability Constraints: According to Bundesnetzagentur, in 2025, the average day-ahead wholesale electricity price rose to EUR 89.32 per MWh, marking a 13.8% increase from the previous year’s EUR 78.51 per MWh. Power availability limitations in Frankfurt's inner city have forced colocation operators to pursue campus builds in suburban Hanau, Rüsselsheim, and Eschborn.

- Stringent GDPR and Regulatory Compliance: While GDPR drives demand for German-hosted data, compliance adds 15–20% to operational costs versus non-regulated markets. The Bundesdatenschutzgesetz (BDSG), state-level data protection authorities, and the forthcoming NIS2 Directive transposition impose continuous audit, certification, and incident reporting obligations.

- Skilled Labor Shortage in DC Operations: Germany faces a structural shortfall of approximately 137,000 IT professionals, with data center operations, network engineering, and AI infrastructure roles experiencing 12–18 month vacancy windows. The shortage is compressing new facility commissioning timelines and elevating managed services dependency.

Market Opportunities

- AI-Ready Hyperscale Campus Development: Frankfurt's power-constrained inner city is driving hyperscaler campuses to suburban greenfield sites in Hessen, NRW, and Brandenburg, where 100+ MW single-site deployments are feasible.

- Sustainable and Green Data Center Innovation: Germany's Energy Efficiency Act 2030 requires data centers to achieve PUE below 1.2 by 2030. Water-free cooling innovation, direct liquid cooling adoption, on-site renewable integration, and waste heat recovery systems supplying district heating networks represent significant technology procurement and ESG compliance opportunities.

Market Challenges

- Power Grid Capacity and Renewable Energy Integration: Germany's Energiewende transition is creating regional grid imbalances. Frankfurt's Hessen state transmission network requires EUR 2.5+ Billion in grid reinforcement to accommodate planned data center loads through 2030.

- Competitive Pressure from Amsterdam and Dublin: The AMS-IX (Amsterdam) and Ireland's tax-advantaged hyperscale ecosystem continue to attract major cloud region investments that could otherwise flow to Germany. Frankfurt's higher power costs and stricter regulatory environment require continuous investment justification against FLAP-D peer markets.

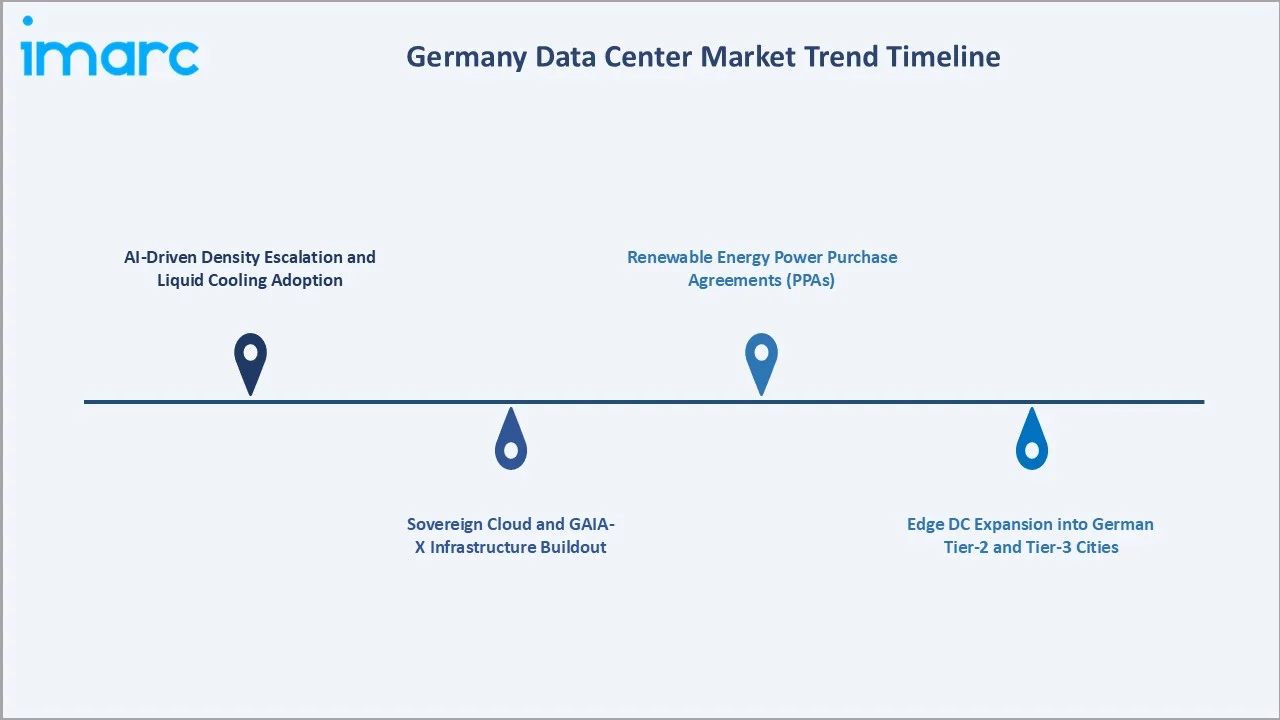

Emerging Market Trends

1. AI-Driven Density Escalation and Liquid Cooling Adoption

Equinix rolled out AI‑optimized, liquid‑cooling systems across about 100 of its IBX data centers, aiming to achieve a target PUE below 1.30 as rack power densities rise toward 150 kW to support AI workloads. At its Frankfurt facility, the AI cooling optimization cut energy use and improved efficiency, reducing the PUE and saving roughly 900 MWh annually.

2. Sovereign Cloud and GAIA-X Infrastructure Buildout

The German Federal Ministry of Economics and Technology launched a funding competition in 2021 to support GAIA‑X, allocating nearly EUR 200 Million from the national stimulus package to finance innovative use cases and data‑space projects across sectors that advance the federated European cloud ecosystem. This funding aims to enable organizations to develop and implement practical GAIA‑X applications, fostering data sovereignty, interoperability, and trust‑based digital infrastructure within the EU.

3. Edge DC Expansion into German Tier-2 and Tier-3 Cities

In April 2026, Deutsche Telekom activated 81 new mobile sites and upgraded capacity at 548 existing locations as part of its ultra‑capacity strategy. The carrier also ended Dynamic Spectrum Sharing (DSS) on the 2.1 GHz band to dedicate the full spectrum to 5G, enhancing network performance and capacity for users. Vertiv and Schneider Electric Germany reported 40%+ year-on-year growth in modular edge enclosure deployments in FY2024–25, driven by demand from automotive OEM factories in Bavaria, Baden-Württemberg, and Lower Saxony.

4. Renewable Energy Power Purchase Agreements (PPAs)

In March 2026, RWE signed a 10‑year power purchase agreement (PPA) with Munich Airport to supply about 40 GWh of renewable electricity annually from its Nordseecluster A offshore wind farm in the North Sea, supporting the airport’s sustainability and decarbonization goals. The deal enhances Munich Airport’s long‑term clean energy supply and contributes to Germany’s broader shift toward renewable power generation.

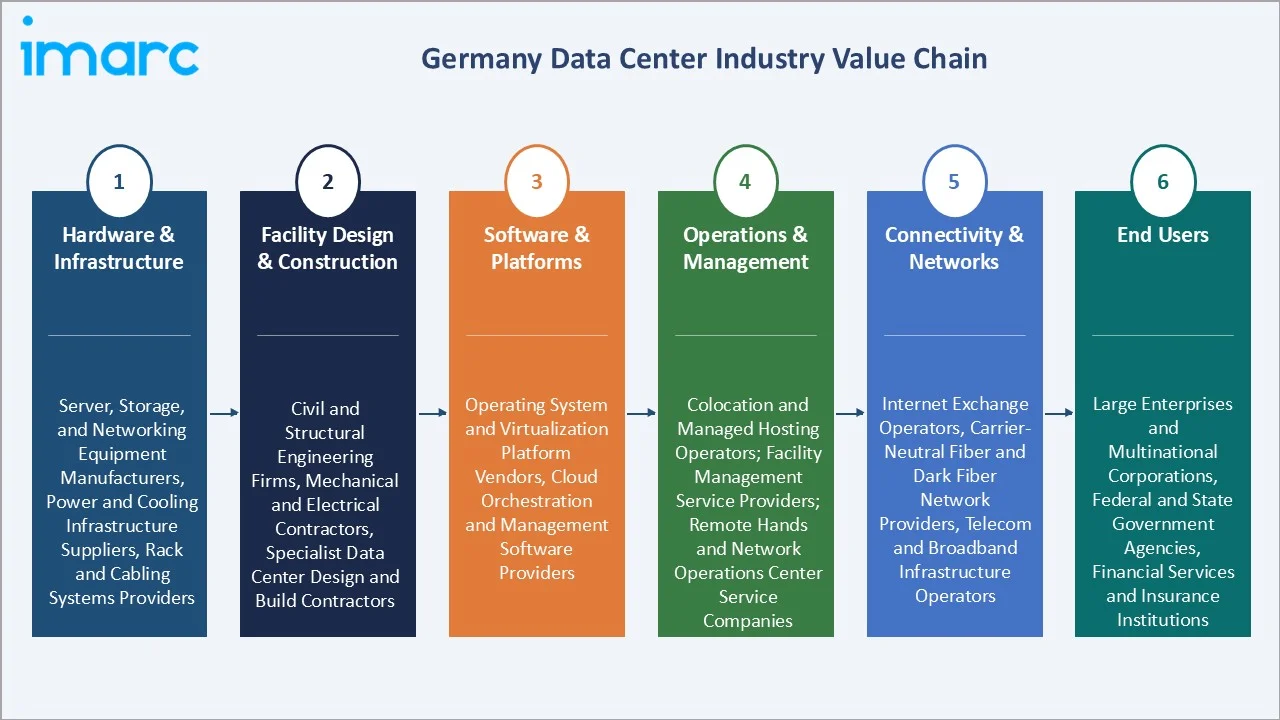

Industry Value Chain Analysis

Germany's data center value chain operates across six integrated stages, from hardware manufacturing and facility construction through operational management, connectivity provision, and end-user consumption, with each stage governed by German technical standards, BSI cybersecurity certifications, and BNetzA energy reporting requirements.

|

Stage |

Key Players / Examples |

|

Hardware & Infrastructure |

Server, storage, and networking equipment manufacturers, power and cooling infrastructure suppliers, rack and cabling systems providers |

|

Facility Design & Construction |

Civil and structural engineering firms, mechanical and electrical contractors, specialist data center design and build contractors |

|

Software & Platforms |

Operating system and virtualization platform vendors, cloud orchestration and management software providers |

|

Operations & Management |

Colocation and managed hosting operators; facility management service providers; remote hands and Network Operations Center service companies |

|

Connectivity & Networks |

Internet exchange operators, carrier-neutral fiber and dark fiber network providers, telecom and broadband infrastructure operators |

|

End Users |

Large enterprises and multinational corporations, federal and state government agencies, financial services and insurance institutions |

Technology Landscape in the Germany Data Center Industry

AI Infrastructure and GPU Cluster Technology

Germany's hyperscale operators are deploying NVIDIA H100 NVLink GPU clusters, AMD Instinct MI300X accelerators, and custom AI ASICs from Google and Amazon across Frankfurt, Munich, and Hamburg campuses. The technical requirement shift to 50–100 kW/rack power density is driving complete power distribution architecture redesigns, including 48V DC power buses, overhead busway systems, and high-voltage 415V 3-phase rack-level distribution that reduces transformer losses by 15–20% versus legacy designs.

Power and Cooling Innovation

Germany's Energieeffizienzgesetz (EnEfG) requires data centers above 1 MW to achieve PUE ≤ 1.5 by 2026 and ≤ 1.2 by 2030. This regulatory mandate is accelerating the adoption of adiabatic cooling, direct liquid cooling, and free-air economization. Siemens and Schneider Electric Germany are deploying AI-based DCIM (Data Center Infrastructure Management) systems that achieve 8–12% PUE improvement through predictive cooling optimization, reducing annual energy consumption per MW by EUR 150,000–250,000.

Carrier-Neutral Connectivity and DE-CIX Ecosystem

DE‑CIX reported a record 68 exabytes of global data traffic exchanged across its internet exchange locations in 2024, marking a 15% increase from 59 exabytes in 2023. The exchange's 900+ connected networks, including all major global CDNs, cloud platforms, and telecom operators, create an unrivalled peering ecosystem that reduces intercontinental latency by 30–50ms for German enterprise traffic.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Solution |

68.0% |

2025 |

|

Type |

Colocation |

38.5% |

2025 |

|

Enterprise Size |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Western Germany |

36.5% |

2025 |

By Component

Solution components command a 68.0% share in 2025. This dominance reflects the large upfront capital expenditure profile of German data center construction. A 10 MW hyperscale shell-and-core facility requires EUR 50–80 Million in hardware and infrastructure investment before the first tenant takes occupancy.

To access detailed market analysis, Request Sample

Services at 32.0% are the fastest-growing component at ~9.1% CAGR, driven by managed services growth as enterprises outsource data center operations to specialists. The post-COVID shift to hybrid cloud infrastructure has increased demand for professional services, which collectively represent approximately 40% of Germany's total data center services revenue.

By Type

Colocation leads at 38.5% in 2025, driven by Frankfurt's carrier-neutral ecosystem that enables enterprises to co-locate alongside 300+ cloud and network service providers. Frankfurt colocation pricing averages EUR 400–600 per kW/month, commands a premium due to unrivalled connectivity density, GDPR-compliant infrastructure, and zero-latency access to DE-CIX peering.

Hyperscale at 34.0% represents the fastest-scaling segment in absolute value terms, with AWS, Microsoft, Google, and Oracle collectively deploying over EUR 12 Billion in German hyperscale campus investment through 2030. Edge at 17.5% is the fastest-growing type at ~12.3% CAGR, driven by Deutsche Telekom's 5G MEC program, automotive ADAS processing, and smart factory latency requirements.

Regional Market Insights

Western Germany's market leadership (36.5%, 2025) is anchored by Frankfurt, home to DE-CIX and Equinix's largest European campus concentration. Frankfurt’s 745 MW of installed IT load capacity makes it Europe's largest single data center market, exceeding London and Amsterdam on a metropolitan comparison basis.

Southern Germany at 27.0% (2025) benefits from Munich's deep integration with the automotive sector's digital transformation and Bavaria's sovereign cloud initiative. Northern Germany, at 21.0%, is growing rapidly as Hamburg's renewable wind energy advantage reduces PPA costs for sustainable campus development.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Western Germany |

36.5% |

Frankfurt is Europe's largest internet exchange hub (DE-CIX); Rhine-Ruhr metro concentration of hyperscaler campuses; dense carrier-neutral colocation ecosystem |

|

Southern Germany |

27.0% |

Munich's automotive, semiconductor, and aerospace tech cluster drives edge and enterprise DC demand; BMW, industrial IoT, and Industry 4.0 workloads |

|

Northern Germany |

21.0% |

Hamburg port logistics and maritime digitization; renewable wind energy advantage for sustainable DC operations; Hamburg and Bremen growing hyperscale campus interest |

|

Eastern Germany |

15.5% |

Berlin startup ecosystem and creative tech scene; Brandenburg growing hyperscaler land investment; competitive power and land costs versus West Germany |

Eastern Germany at 15.5% represents the highest upside region, with Berlin's startup ecosystem and Brandenburg's large land availability attracting hyperscaler campus interest at significantly lower power and real estate costs than Western Germany.

Competitive Landscape

Germany's data center market exhibits moderate concentration at the national level, with Equinix Inc. commanding approximately 30–35% of organized colocation revenue. The managed services and enterprise segment is led by Deutsche Telekom AG, NTT DATA Group Corporation, and United Internet AG.

|

Company Name |

Services / Products |

Market Position |

Core Strength |

|

|

IBX, xScale, DU1, HH1, MU1 to 4, Equinix Fabric |

Market Leader |

Largest global carrier-neutral colocation; Frankfurt as the largest European hub; digital infrastructure ecosystem with 300+ on-ramps |

|

|

Colocation, Hybrid Cloud |

Strong Challenger |

Edge data center specialist; Tier 3 standard with 24/7 on-site support; direct private cloud connect to major CSPs |

|

|

T Cloud Public, sovereign cloud |

Strong Challenger |

German sovereign cloud for regulated industries; Telekom network integration; trusted partner for Bundesbehörden and Mittelstand |

|

|

Colocation, data center connectivity, data center implementation, and management |

Challenger |

One of Germany's largest colocation footprints via e-shelter acquisition; Frankfurt and Munich scale; global network integration |

|

|

IONOS cloud marketplace, managed hosting |

Challenger |

Largest European cloud provider by customer count; Karlsruhe and Berlin DC facilities; cost-competitive Mittelstand positioning |

The hyperscale segment is dominated by the three major US cloud providers (AWS, Microsoft Azure, Google Cloud), whose combined German infrastructure investment exceeds EUR 15 Billion through 2030.

Key Company Profiles

Equinix Inc.

Equinix Inc. is one of the world's largest carrier-neutral colocation providers and the market leader in Germany, operating IBX data centers.

- Product Portfolio: IBX xScale, DU1, HH1, MU1 to 4, and Equinix Fabric (software-defined interconnection).

- Recent Developments: In November 2025, Equinix launched a Lenovo-built high-performance computing (HPC) supercomputer in its AI-ready data center in Germany to accelerate AI, advanced analytics, and scientific research for Merck KGaA.

- Strategic Focus: AI-ready infrastructure deployment with DLC and immersion cooling; renewable energy PPA commitments; Equinix Fabric digital interconnection scaling.

Portus Data Centers S.à r.l.

Portus Data Centers S.à r.l. is a carrier-neutral edge colocation operator providing services in Germany. The company positions itself as a specialist in regional edge infrastructure, serving sectors including automotive, finance, healthcare, and systems integrators.

- Product Portfolio: Colocation (Tier 3 standard, 24/7 on-site support, bespoke cage and rack configuration) and Hybrid Cloud.

- Recent Developments: In May 2026, Portus Data Centers S.à r.l. topped out its second data center (MUC2) in Munich, Germany, a new 5.5 MW facility that will expand the Munich campus’ capacity to 7 MW when it goes live in early 2027.

- Strategic Focus: Hyperscale campus pre-lease pipeline expansion in power-constrained Frankfurt via suburban greenfield development; Connected Campus multi-site campus strategy.

Market Concentration Analysis

Germany's data center market exhibits moderate concentration in the colocation segment (Equinix Inc. controls ~35% of capacity) and high concentration in the hyperscale segment (top 3 cloud providers deploy ~90% of hyperscale investment). The enterprise-owned segment is highly fragmented, with thousands of corporate data centers representing a structural outsourcing conversion opportunity for colocation and managed service providers through 2034.

Market consolidation is accelerating through M&A: NTT Communications Corporation’s EUR 742 Million acquisition of e-shelter, Digital Realty's USD 8.4 Billion Interxion acquisition, and ongoing private equity activity are concentrating capital in the hands of operators capable of funding 100+ MW hyperscale campuses, a scale that requires EUR 1+ Billion in equity and debt commitment before first revenue.

Investment & Growth Opportunities

Fastest Growing Segments

Edge data centers (~12.3% CAGR), hyperscale services (~10.5% CAGR), and managed services (~9.1% CAGR) represent the highest-return investment vectors through 2034. Together, these segments address an incremental market of approximately USD 8+ Billion by 2034, above 2025 levels, as AI inferencing distribution, cloud sovereignty, and enterprise outsourcing converge.

Emerging Market Expansion

Eastern Germany's 15.5% regional share represents the highest upside geography, with Brandenburg's large greenfield land availability, competitive power prices, and proximity to Berlin's enterprise demand base attracting hyperscaler land acquisitions.

Investment and Infrastructure Trends

- In November 2025, Google announced its largest-ever investment plan in Germany, committing approximately EUR 5.5 billion toward new data centers, expansions, and technology infrastructure to bolster cloud and AI capabilities. The announcement marked a major push into digital and sustainable infrastructure, with plans to create thousands of jobs and expand its presence across key German cities.

- Renewable energy infrastructure investment is becoming a co-investment requirement for large-scale data center development. Equinix Inc. and NTT DATA Group Corporation are collectively committing investments in offshore wind and solar PPAs through 2030 to meet client sustainability requirements and the German Energy Efficiency Act 's data center energy reporting mandates.

Future Market Outlook (2026-2034)

Germany's data center market will expand from USD 10.48 Billion in 2025 to USD 22.45 Billion by 2034 at an 8.57% CAGR. Frankfurt will retain European colocation leadership but face increasing competition from suburban hyperscale campuses and Berlin's emerging tech cluster.

By 2034, Germany's data center market will be defined by three converging trajectories: sovereign cloud infrastructure mandated by GDPR successors and the EU AI Act, fully liquid-cooled AI campuses operating at 1.1 PUE, and distributed edge networks processing 40%+ of German enterprise workloads at the network periphery.

Germany's commitment to 100% renewable electricity by 2035 aligns data center sustainability targets with the national energy transition, positioning German DCs as global benchmarks for sustainable AI infrastructure.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants in 2024–2025, including data center operators, cloud architects, power infrastructure engineers, regulatory counsel, and institutional investors across Frankfurt, Munich, Hamburg, and Berlin.

Secondary Research

Secondary research covered BNetzA energy reporting data, Bitkom digital economy statistics, DE-CIX traffic data, Bundesnetzagentur grid capacity reports, European Data Center Association (EUDCA) publications, and company annual reports and investor presentations for all major German market participants.

Forecasting Models

Market estimations used bottom-up forecasting incorporating colocation pricing benchmarks, hyperscale pre-lease pipeline disclosures, power capacity data, and enterprise IT spending forecasts. An 8.57% CAGR through 2034 reflects consensus cross-validated against Bitkom's German digital economy growth projections and IMARC's primary expert panel validation.

Germany Data Center Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Solution, Service |

| Types Covered | Colocation, Hyperscale, Edge, Other |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium Enterprises |

| End Users Covered | BFSI, It and Telecom, Government, Energy and Utilities, Others |

| Regions Covered | Western Germany, Southern Germany, Eastern Germany, Northern Germany |

| Companies Covered | Equinix Inc., Portus Data Centers S.à r.l., Deutsche Telekom AG, NTT DATA Group Corporation, United Internet AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Germany data center market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Germany data center market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Germany data center industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Germany Data Center Market Report

The market reached USD 10.48 Billion in 2025 and is forecast to reach USD 22.45 Billion by 2034 at an 8.57% CAGR.

Solution components lead at 68.0% in 2025, encompassing IT hardware, power infrastructure, and cooling systems that represent the dominant capital expenditure category across German data center deployments.

Colocation leads at 38.5% in 2025, driven by Frankfurt's carrier-neutral ecosystem and the DE-CIX internet exchange connectivity advantage that sustains premium colocation pricing and occupancy rates.

Western Germany leads at 36.5% in 2025, anchored by Frankfurt's position as Europe's largest internet exchange hub and the Rhine-Ruhr conurbation's dense enterprise and hyperscale infrastructure concentration.

Key players, including Equinix Inc., Portus Data Centers S.à r.l., Deutsche Telekom AG, NTT DATA Group Corporation, and United Internet AG, are competing alongside hyperscaler cloud providers AWS, Microsoft Azure, and Google Cloud.

Edge data centers are the fastest-growing type at ~12.3% CAGR, driven by Deutsche Telekom's 5G MEC program, automotive ADAS processing requirements, and smart manufacturing latency demands across Germany's industrial corridor.

AI and cloud workload adoption, hyperscaler campus investment commitments, GDPR and data sovereignty mandates creating captive domestic demand, the Gigabit Strategy 2030, and Germany's Mittelstand industrial digitization program are the primary growth catalysts.

High electricity costs, power grid capacity constraints in Frankfurt, stringent GDPR and NIS2 compliance obligations, skilled IT labor shortages, and competition from FLAP-D peer markets with lower power costs are the primary challenges.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)