Germany Electric Vehicle Charging Station Market Size, Share, Trends and Forecast by Charging Station Type, Vehicle Type, Installation Type, Charging Level, Connector Type, Application, and Region, 2026-2034

Germany Electric Vehicle Charging Station Market Size, Share, Trends & Forecast (2026-2034)

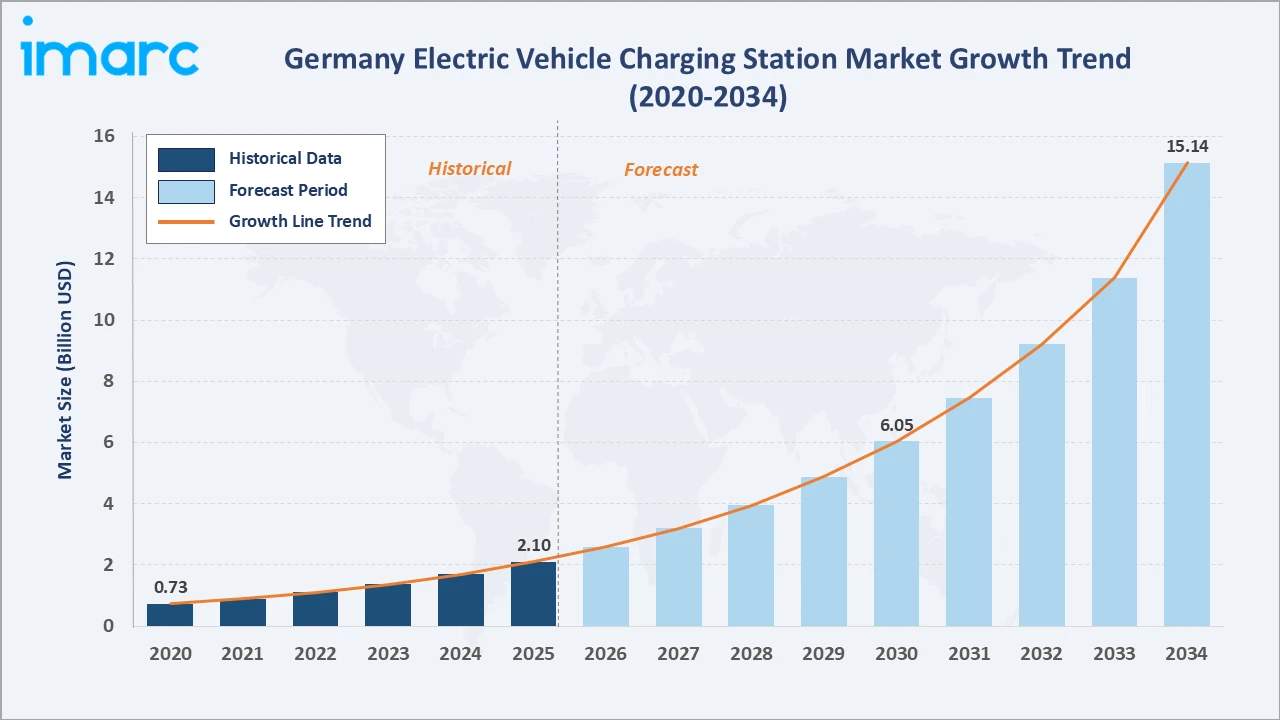

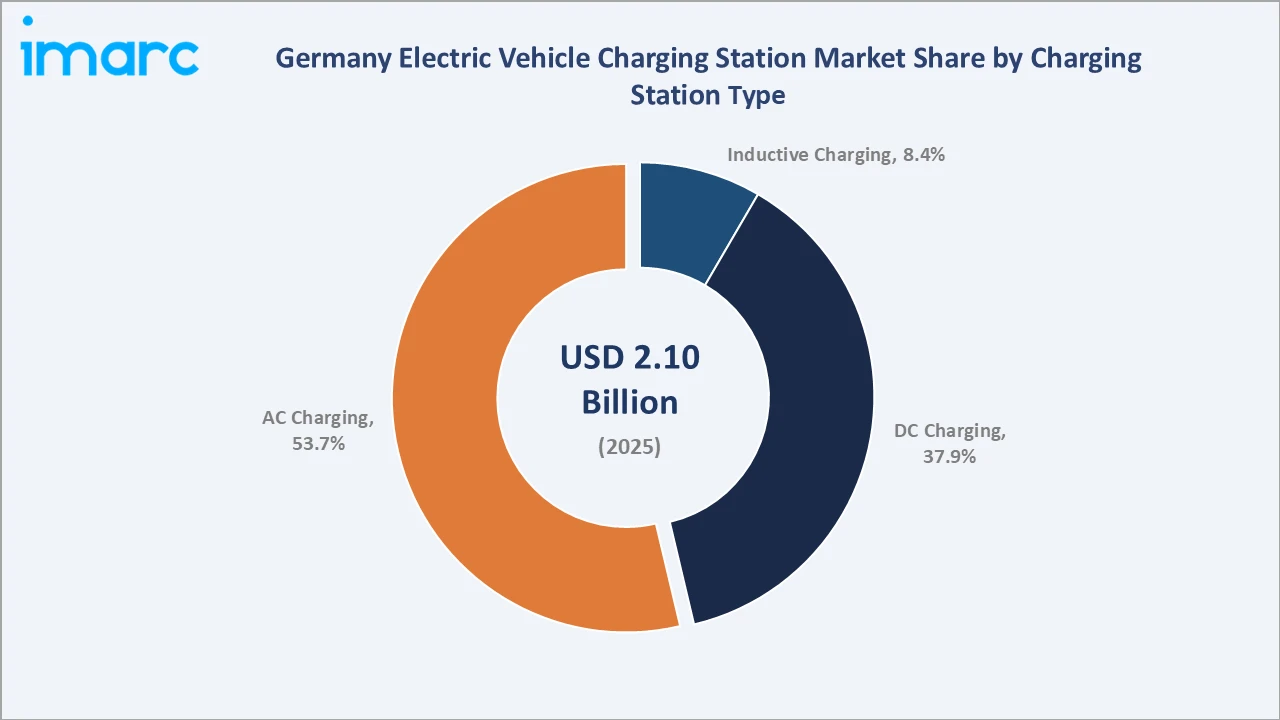

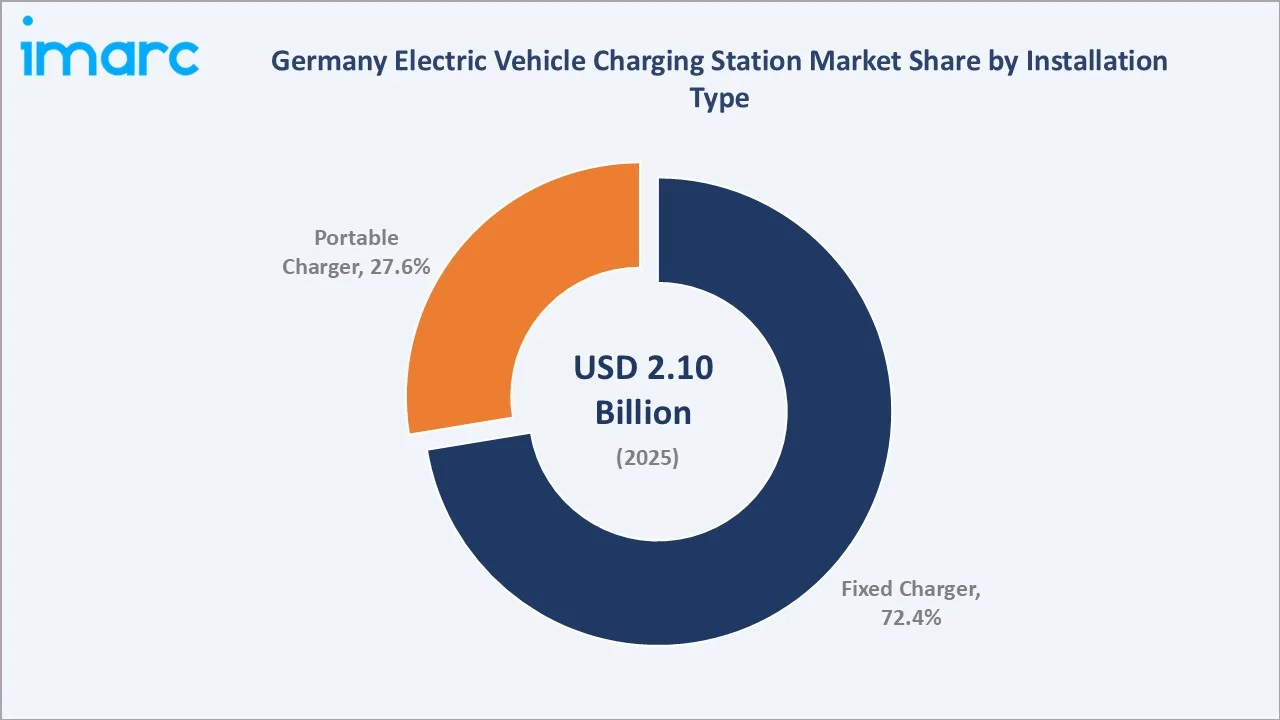

The Germany electric vehicle charging station market was valued at USD 2.10 Billion in 2025 and is projected to reach USD 15.14 Billion by 2034, exhibiting a CAGR of 23.53% during 2026-2034. Rising electric vehicle registrations, expanding DC fast-charging corridors, and increasing corporate fleet electrification are the primary drivers shaping market growth.

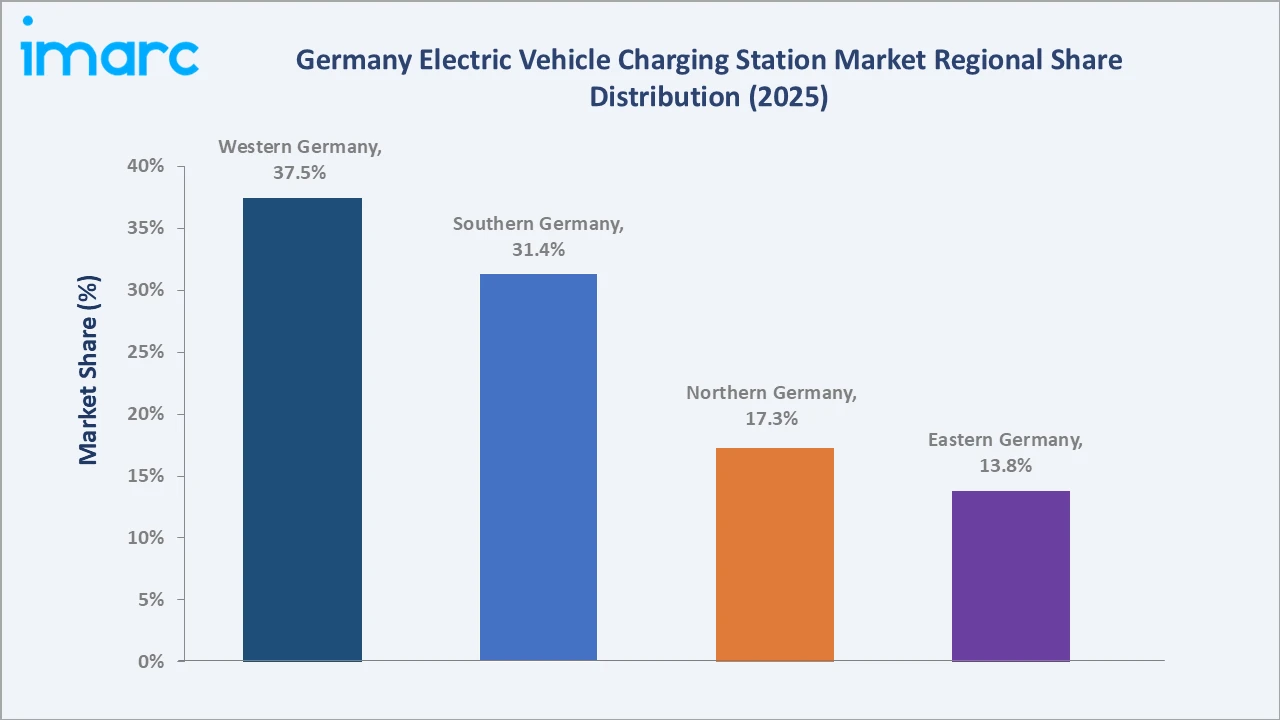

AC charging leads the charging station type segment at 53.7% in 2025, fixed charger dominates the installation type at 72.4%, and Western Germany commands the largest regional share at 37.5%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.10 Billion |

|

Forecast Market Size (2034) |

USD 15.14 Billion |

|

CAGR (2026-2034) |

23.53% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Western Germany (37.5%, 2025) |

|

Second Largest Region |

Southern Germany (31.4%, 2025) |

|

Largest Charging Station Type |

AC Charging (53.7%, 2025) |

|

Largest Installation Type |

Fixed Charger (72.4%, 2025) |

The Germany electric vehicle charging station market expanded from USD 0.73 Billion in 2020 to USD 2.10 Billion in 2025, driven by widening electric vehicle adoption, growing residential and commercial charging deployment, and rapid expansion of the public charging network across Germany's cities and highway corridors. Anchored at USD 6.05 Billion in 2030, the forecast to USD 15.14 Billion by 2034 is supported by accelerating DC fast-charging rollout on the Autobahn, mandatory building charging requirements, and increasing corporate and logistics fleet electrification programs.

To get more information on this market, Request Sample

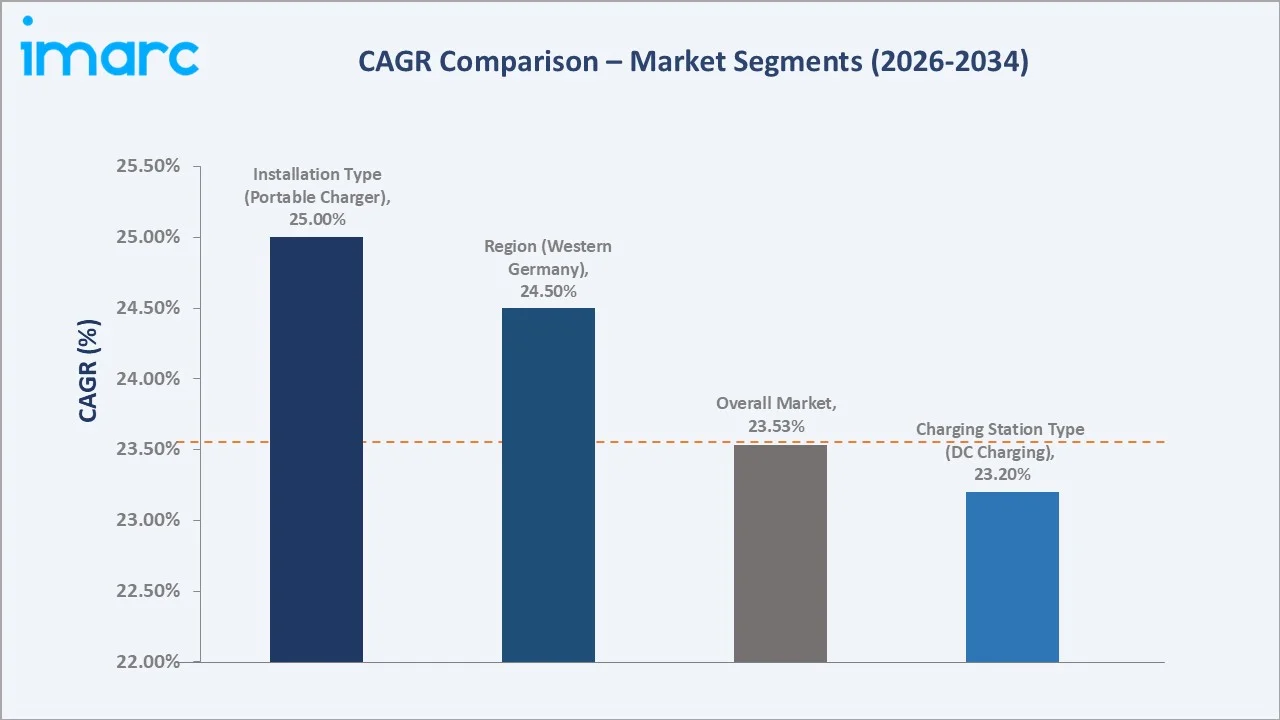

CAGR trajectories across charging station type and installation type sub-segments show DC charging and inductive charging expanding faster than the overall 23.53% market CAGR, driven by rising consumer demand for rapid charging, government highway corridor mandates, and growing adoption of wireless charging pilots for fleet and automated vehicle applications.

Executive Summary

The Germany electric vehicle charging station market is on a high-growth trajectory, expanding from USD 0.73 Billion in 2020 to USD 2.10 Billion in 2025 at a historical CAGR of approximately 23.5%, and is forecast to sustain this growth rate through 2034 to reach USD 15.14 Billion. The market is underpinned by strong electric vehicle sales growth, rapid expansion of public fast-charging networks, and increasing integration of smart charging technologies with Germany's evolving energy transition strategy. As per IEA, in Germany, electric car sales surged by 50% in 2025, hitting a new peak of 850,000.

AC charging remains the backbone segment, accounting for 53.7% of the 2025 market, primarily through workplace and residential charging. Fixed charger dominates at 72.4%, reflecting the preference for permanent, grid-connected infrastructure. Western Germany leads regionally at 37.5%, benefiting from high urbanization, industrial clusters, and automotive OEM proximity.

Key Market Insights

|

Insight |

Data |

|

Leading Charging Station Type |

AC Charging - 53.7% share (2025) |

|

Second Largest Charging Station Type |

DC Charging – 37.9% share (2025) |

|

Leading Installation Type |

Fixed Charger - 72.4% share (2025) |

|

Second Largest Installation Type |

Portable Charger – 27.6% share (2025) |

|

Leading Region |

Western Germany - 37.5% share (2025) |

|

Second Largest Region |

Southern Germany – 31.4% share (2025) |

|

Top Companies |

EnBW Energie Baden-Württemberg AG, E.ON SE, Siemens, ABB |

Key Analytical Observations Supporting the Above Data:

- AC charging dominance at 53.7% is supported by widespread deployment in homes, offices, and retail parking, where overnight and daytime dwell-time charging is the primary use case, reinforced by lower equipment costs and simpler grid connection requirements versus DC installations.

- DC charging at 37.9% is the second largest charging station type, driven by consumer demand for rapid charging at public and highway locations, and further accelerated by mandatory AFIR highway corridor requirements.

- Fixed charger at 72.4% reflects operators' preference for permanent grid-connected infrastructure enabling smart load management and billing. Its scalability and compatibility with networked software platforms support long-term infrastructure expansion and operational efficiency.

- Portable charger at 27.6% caters to residential users, small businesses, and fleet operators seeking flexible and cost-effective charging solutions. Ease of installation, mobility, and compatibility with existing electrical infrastructure make portable chargers an attractive option for locations where permanent installations are not feasible.

- Western Germany at 37.5% dominates regional share, supported by Bavaria, North Rhine-Westphalia, and Baden-Württemberg, which account for the majority of Germany's electric vehicle registrations and host a high concentration of charge point operators.

Germany Electric Vehicle Charging Station Market Overview

An electric vehicle charging station is a specialized infrastructure facility designed to supply electrical energy for recharging the batteries of battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs). The Germany electric vehicle charging station ecosystem spans AC level-2 chargers, DC fast chargers, inductive wireless systems, and emerging vehicle-to-grid (V2G) installations across residential, commercial, and public-use settings.

Germany is Europe's leading automobile market and the epicenter of its electric vehicle transition, with major OEMs headquartered in key cities, driving both vehicle demand and charging ecosystem development. Macroeconomic influences include EU Green Deal targets, rising electricity price volatility prompting smart energy management, and growing corporate ESG commitments that accelerate fleet electrification.

Market Dynamics

To evaluate market opportunities, Request Sample

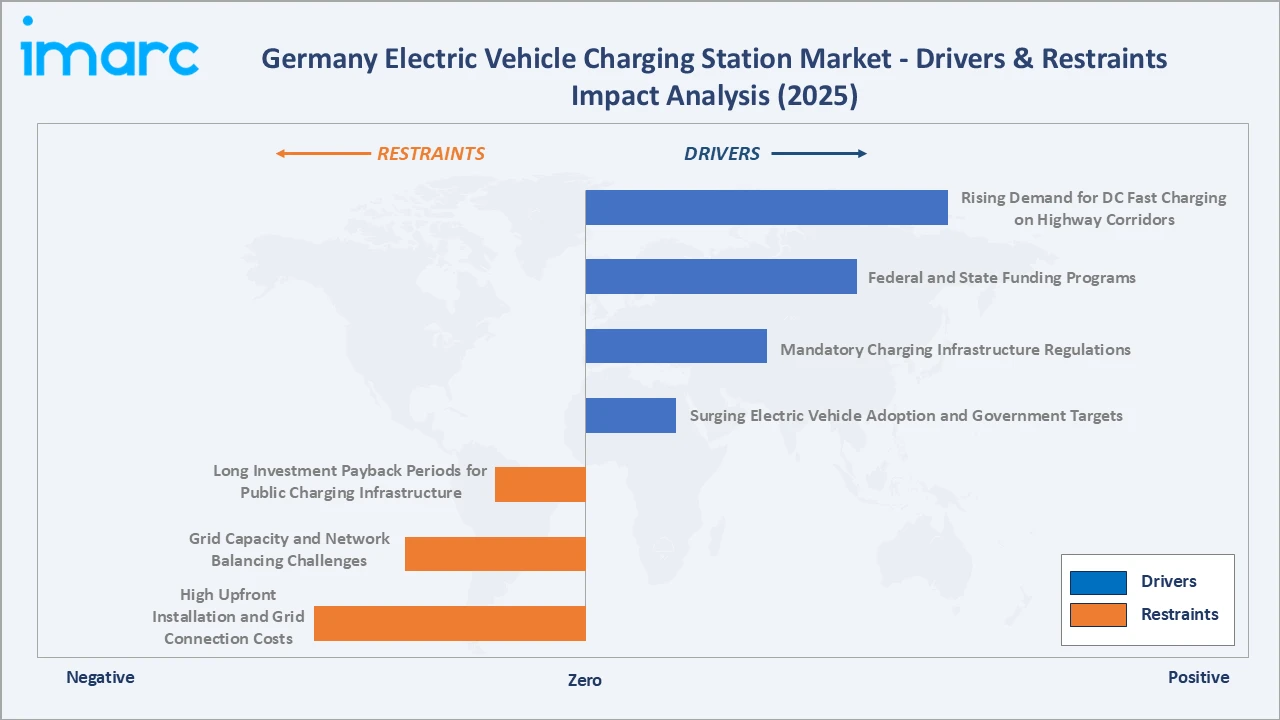

Market Drivers

- Surging Electric Vehicle Adoption and Government Targets: The rapid expansion of the electric vehicle fleet, supported by increasing consumer acceptance and the broader shift toward low-emission mobility, is creating sustained demand for accessible and reliable charging infrastructure across the country. As per IMARC Group, the Germany electric vehicle market size reached USD 41.9 Billion in 2025.

- Mandatory Charging Infrastructure Regulations: Government regulations and building requirements promoting the installation of charging facilities in residential, commercial, and public spaces are accelerating the nationwide rollout of electric vehicle charging networks.

- Federal and State Funding Programs: Financial incentives, infrastructure development programs, and investments in grid modernization are reducing deployment costs and encouraging private sector participation in charging station expansion.

- Rising Demand for DC Fast Charging on Highway Corridors: Rising adoption of long-distance electric mobility and increasing consumer preference for shorter charging times are driving the expansion of fast-charging infrastructure along highways, urban transit corridors, and key commercial locations.

Market Restraints

- High Upfront Installation and Grid Connection Costs: The deployment of electric vehicle charging infrastructure, particularly high-power fast chargers, requires substantial capital investment for equipment, civil works, and grid connection upgrades. These costs can slow network expansion, especially in areas with lower expected utilization.

- Grid Capacity and Network Balancing Challenges: The growing concentration of electric vehicle charging demand can place additional pressure on local electricity distribution networks, requiring infrastructure upgrades and advanced load management systems to maintain grid stability and reliable charger performance.

- Long Investment Payback Periods for Public Charging Infrastructure: Public charging networks often face extended return-on-investment timelines due to uneven charger utilization and the early stage of electric vehicle adoption in some regions. This can limit private sector investment and delay the rollout of charging stations outside high-demand locations.

Market Opportunities

- Expansion of Smart and Bidirectional Charging: The development of V2G and vehicle-to-building (V2B) bidirectional charging platforms creates new revenue opportunities for network operators and fleet managers by enabling electricity resale and grid balancing services.

- Electrification of Commercial and Logistics Fleets: Germany's large commercial fleet sector, including logistics, construction, and public transport, represents a major opportunity for high-power depot charging installations, fleet management software, and energy management systems.

Market Challenges

- Skilled Installer Workforce Shortage: Germany faces a shortage of certified electrical installers qualified for electric vehicle charging equipment, slowing deployment velocity particularly for high-power DC installations.

- Urban Permitting and Space Constraints: Installing public charging stations in dense urban environments faces challenges including lengthy permitting processes, limited footway space, and underground utility conflicts.

Emerging Market Trends

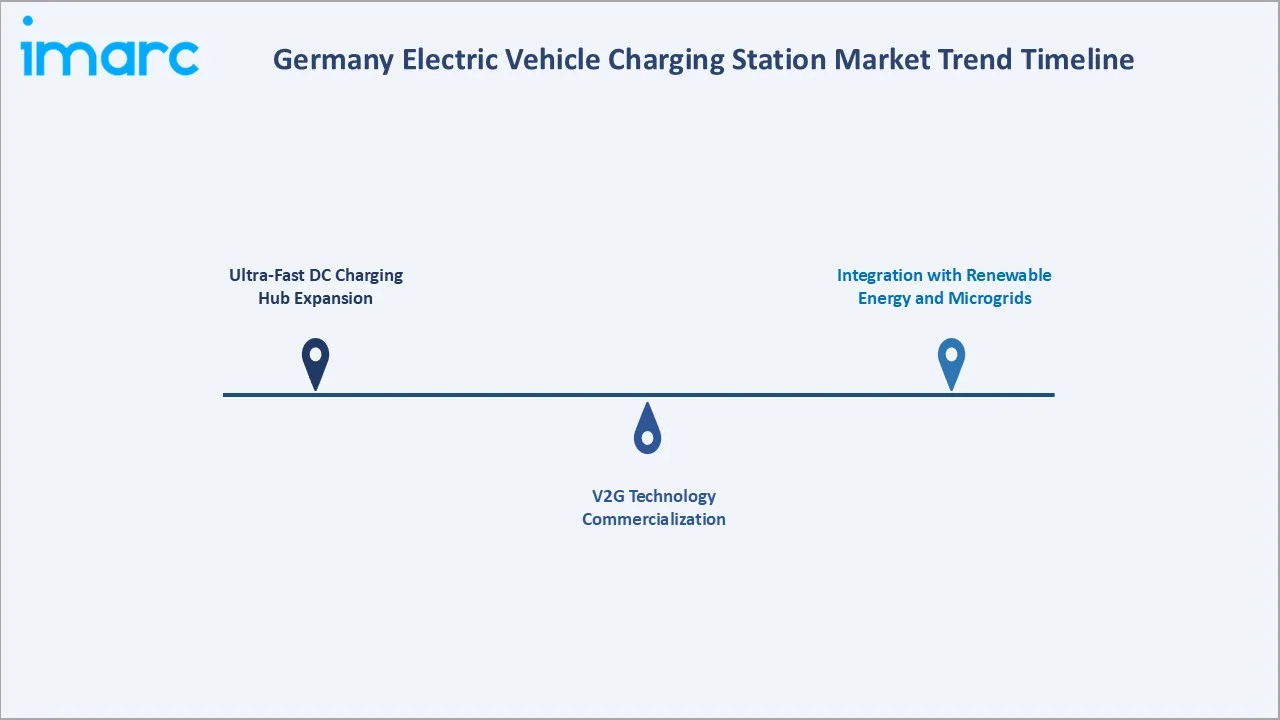

1. Ultra-Fast DC Charging Hub Expansion

The development of ultra-fast charging hubs at key motorway service areas and logistics nodes is redefining the user experience for long-distance electric vehicle travel. These hubs are attracting major investment from energy utilities and automotive OEMs.

2. V2G Technology Commercialization

Bidirectional charging technology enabling electric vehicles to export stored energy back to the grid or home is transitioning from pilot stages to early commercial deployment in Germany. Expanding regulatory support, standardization efforts, and collaboration between automakers, utilities, and charging network operators are accelerating the commercialization of V2G services and bidirectional charging ecosystems.

3. Integration with Renewable Energy and Microgrids

Charging operators and property developers are increasingly co-locating electric vehicle charging with on-site solar PV and battery energy storage systems (BESS). This hybrid approach reduces grid dependency, enables green charging credentials, and provides backup power resilience. Several large logistics parks and airport facilities in Germany have commissioned integrated solar-storage electric vehicle charging systems.

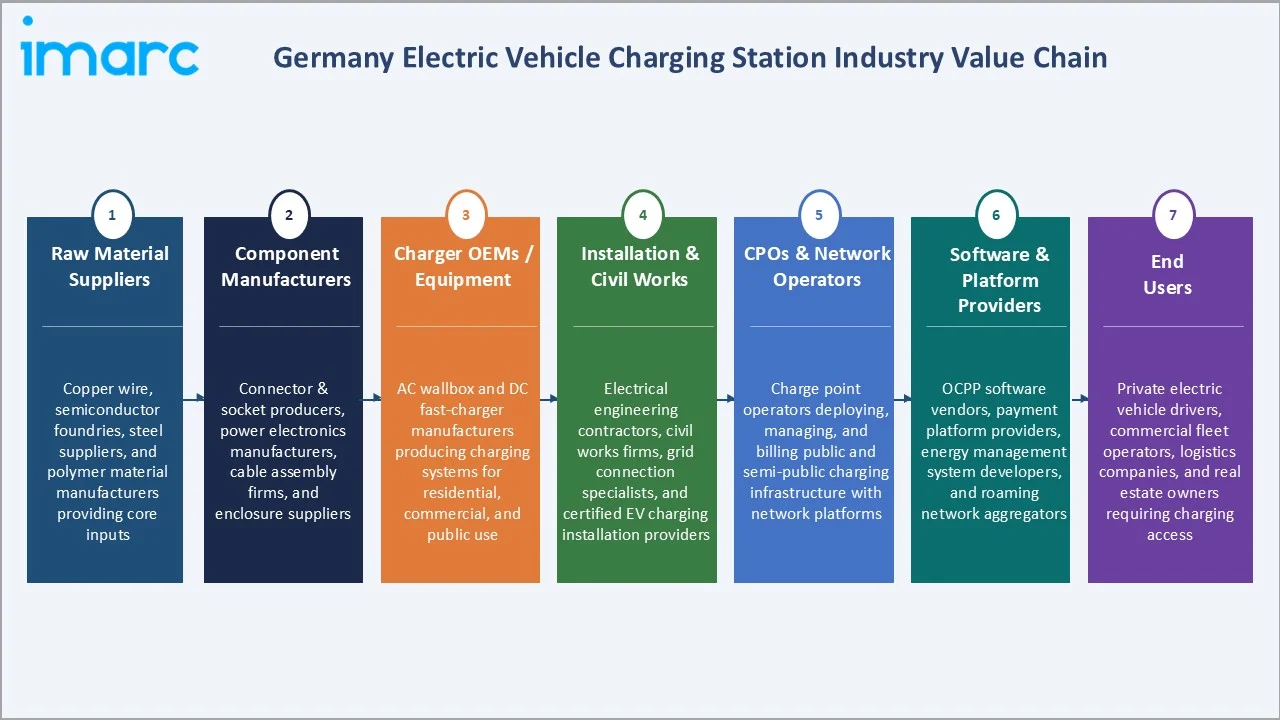

Industry Value Chain Analysis

The Germany electric vehicle charging station industry value chain spans multiple stages, from the sourcing of raw materials and manufacture of components to the deployment and operation of charging infrastructure and its consumption by end users. Each stage is interconnected, with upstream supply chain dynamics directly influencing the cost and pace of downstream network expansion. Understanding this value chain is essential for identifying competitive positioning, investment entry points, and potential supply-side bottlenecks in the market.

|

Stage |

Key Players / Examples |

|

Raw Material Suppliers |

Copper wire and cable producers, semiconductor foundries, steel suppliers, and polymer material manufacturers providing core inputs for charging hardware |

|

Component Manufacturers |

Connector and socket producers, power electronics manufacturers, cable assembly firms, and enclosure and thermal management component suppliers |

|

Charger OEMs / Equipment |

Charging equipment manufacturers producing AC wallboxes, DC fast chargers, and ultra-fast charging systems for residential, commercial, and public use |

|

Installation & Civil Works |

Electrical engineering contractors, civil works firms, grid connection specialists, and certified installation service providers |

|

CPOs & Network Operators |

Charge point operators deploying, managing, and billing public and semi-public charging infrastructure, including network management platform providers |

|

Software & Platform Providers |

OCPP-compliant software vendors, payment and billing platform providers, energy management system developers, and roaming network aggregators |

|

End Users |

Private electric vehicle drivers, commercial fleet operators, logistics companies, and real estate owners requiring charging access for residents and visitors |

Vertically integrated players that own proprietary hardware designs, software platforms, and direct customer relationships are positioned to capture greater value than participants reliant on third-party infrastructure.

Technology Landscape in the Germany Electric Vehicle Charging Station Industry

AC and DC Charging Systems

AC charging technology, leveraging established electrical grid standards, continues to dominate installation volumes for home and workplace settings due to lower equipment costs and simpler grid connection requirements. High-power DC chargers are simultaneously transforming highway and urban rapid charging.

Smart and Connected Charging Platforms

Smart charging solutions featuring remote monitoring, dynamic load balancing, and integration with building energy management systems are increasingly being deployed across public, commercial, and residential charging networks. Growing adoption of interoperable communication protocols is improving compatibility between charging hardware and central management platforms, while cybersecurity is emerging as a key priority as connected charging infrastructure expands and digital regulatory requirements become more stringent.

V2G and Bidirectional Charging

Bidirectional charging technology, which enables electric vehicles to return stored energy to the grid, homes, or commercial buildings, is progressing from pilot projects toward early commercial deployment. Increasing collaboration between automakers, utilities, and charging infrastructure providers, together with advances in smart metering and plug-and-charge technologies, is supporting the wider adoption of V2G solutions and enhancing their potential role in grid balancing and energy management.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Charging Station Type |

AC Charging |

53.7% |

2025 |

|

Vehicle Type |

🔒 |

🔒 |

2025 |

|

Installation Type |

Fixed Charger |

72.4% |

2025 |

|

Charging Level |

🔒 |

🔒 |

2025 |

|

Connector Type |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Western Germany |

37.5% |

2025 |

By Charging Station Type

AC charging leads with a 53.7% share in 2025, driven by widespread deployment in homes and workplaces where vehicles can charge during extended dwell times. The lower cost of AC equipment and simpler grid connection requirements support its continued dominance in volume terms.

To access detailed market analysis, Request Sample

DC charging accounts for 37.9% in 2025 and represents the most dynamic segment in value terms. Its growth is driven by increasing demand for rapid charging solutions that support long-distance travel, commercial fleets, and high-utilization public charging locations.

By Installation Type

Fixed charger dominates the installation type segment with a 72.4% share in 2025. Its leading position is supported by widespread deployment in residential properties, workplaces, commercial facilities, and public parking locations, where permanent grid-connected infrastructure offers greater reliability and operational efficiency.

Portable charger holds a 27.6% share in 2025. While limited primarily to low-power AC applications, portable charger provides flexibility for residential users, rental properties, and emergency or event-based charging use cases.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Western Germany |

37.5% |

Large urban population, strong electric vehicle adoption, dense grid infrastructure, high concentration of automotive OEM and energy company headquarters, and mature public charging network |

|

Southern Germany |

31.4% |

Presence of major automotive OEM headquarters, high purchasing power, robust highway charging demand along A8 and A9 corridors, and growing residential and workplace charging deployment |

|

Northern Germany |

17.3% |

Growing wind energy integration with charging infrastructure, increasing urban electric vehicle fleet deployments, and strong Energiewende-aligned green charging initiatives |

|

Eastern Germany |

13.8% |

Rapidly expanding public and semi-public charging network supported by federal infrastructure fund, EU structural co-investment, and rising electric vehicle adoption bridging the infrastructure gap |

Western Germany at 37.5% in 2025 leads the regional landscape, encompassing major states such as North Rhine-Westphalia, Hesse, and Rhineland-Palatinate. The region benefits from high electric vehicle ownership density, a strong grid backbone, proximity to the Netherlands and Belgium creating cross-border charging ecosystem linkages, and a large concentration of charge point operators and energy service companies.

Southern Germany at 31.4% represents the second largest region, driven by robust electric vehicle demand, advanced industrial infrastructure, and continued investment in charging network expansion.

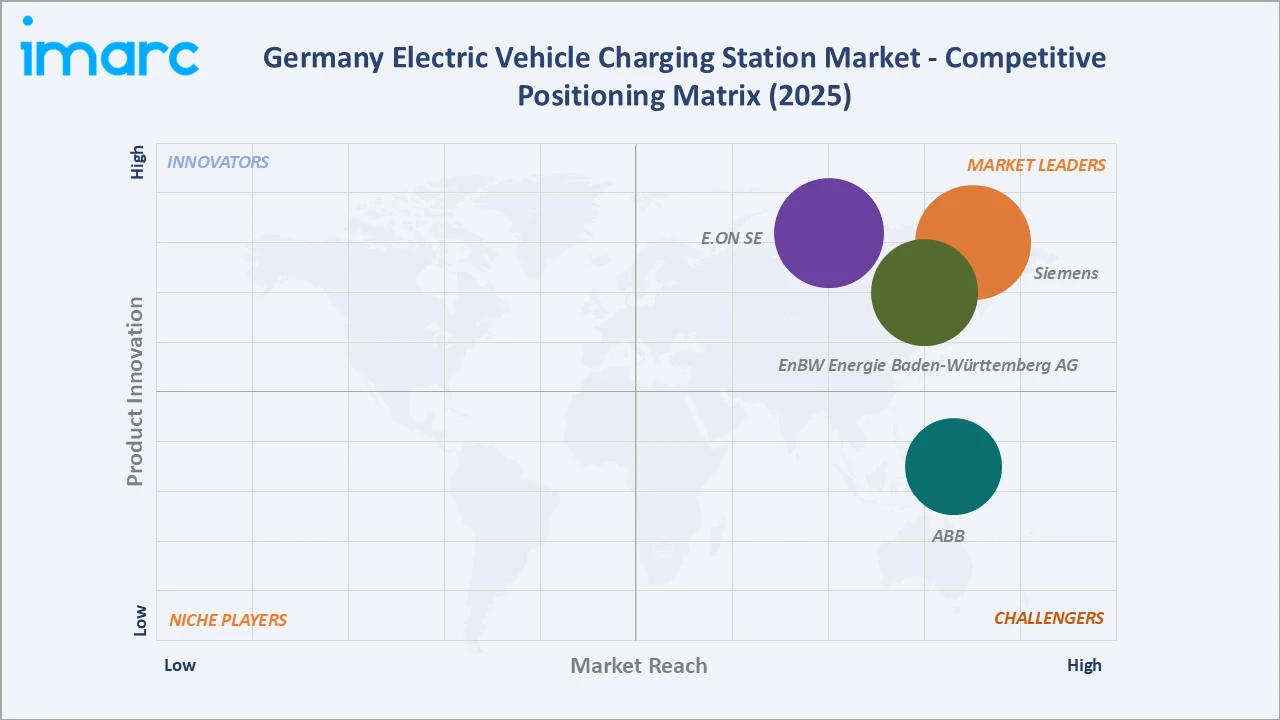

Competitive Landscape

The Germany electric vehicle charging station market features a moderately fragmented competitive landscape, with large utilities, automotive groups, and specialist charge point operators (CPOs) competing across network scale, technology capability, and service quality. The market is trending towards consolidation as smaller independent operators face margin pressure and seek partnerships or acquisition by capital-rich strategic players.

|

Company Name |

Key Brand / Product |

Position |

Strategic Focus |

|

EnBW Energie Baden-Württemberg AG |

EnBW mobility+ |

Leader |

Expanding public fast-charging network across German highways and urban centers |

|

E.ON SE |

E.ON Drive |

Leader |

Integrated home and public charging solutions with smart energy management |

|

Siemens |

SICHARGE D |

Leader |

Commercial and industrial charging infrastructure with grid-smart platforms |

|

ABB |

Terra 360 |

Challenger |

High-power DC fast charging solutions for highway and logistics applications |

Key players include EnBW Energie Baden-Württemberg AG, E.ON SE, Siemens, and ABB, among others.

Key Company Profiles

EnBW Energie Baden-Württemberg AG

EnBW Energie Baden-Württemberg AG is one of Germany's largest energy companies. It is a leading charge point operator in Germany, operating a nationwide network of AC and DC fast-charging stations under the EnBW mobility+ brand across highways, urban centers, and residential locations.

- Product Portfolio: EnBW mobility+ provides public DC fast-charging stations and AC charging at residential and commercial locations.

- Recent Developments: EnBW Energie Baden-Württemberg AG expanded its public charging network to more than 8,000 fast-charging points in Germany as of early 2026, with continued deployment of high-power chargers at motorway service areas and urban hubs.

- Strategic Focus: Scaling the nationwide DC fast-charging network along German motorways and in major cities and integrating renewable energy sourcing into charging operations.

E.ON SE

E.ON SE is a leading European energy company headquartered in Essen, Germany. The firm operates a pan-European public electric vehicle charging network and provides integrated home and workplace charging solutions to residential and corporate customers.

- Product Portfolio: E.ON Drive offers home wallbox installation and management, workplace charging solutions, public AC and DC charging infrastructure across Germany and Europe, smart energy management platforms, and corporate fleet charging services with consolidated billing.

- Recent Developments: In September 2026, E.ON SE partnered with BMW Group to launch a consumer vehicle-to-grid service in Germany, allowing drivers to earn revenue by feeding stored energy back to the grid.

- Strategic Focus: Building an integrated electric vehicle energy ecosystem that combines home charging, workplace charging, public infrastructure, and smart energy management under a single platform, with growing focus on vehicle-to-grid and dynamic electricity tariff products.

ABB

ABB is a multinational technology company and a global leader in electric vehicle charging infrastructure. The company supplies a broad portfolio of DC fast-charging solutions to charge point operators, automotive manufacturers, fuel retailers, and fleet operators, maintaining a strong presence across the European electric vehicle charging ecosystem, including Germany.

- Product Portfolio: Terra 360, Terra HP high-power liquid-cooled DC chargers, and Terra AC Wallbox.

- Recent Developments: ABB has continued to expand its portfolio of high-power and ultra-fast charging solutions to address the growing demand for scalable electric vehicle infrastructure. The company is also strengthening its software and digital service capabilities, enabling advanced remote monitoring, predictive maintenance, and seamless integration with smart charging management platforms.

- Strategic Focus: Supplying high-power DC fast-charging hardware to highway corridor operators, fuel retailers, and logistics fleet operators, with emphasis on ultra-fast charging reliability, serviceability, and integration with network management software platforms.

Market Concentration Analysis

The Germany electric vehicle charging station market is moderately concentrated, with the top three operators (EnBW Energie Baden-Württemberg AG, E.ON SE, and Siemens) accounting for a significant share of public charging network deployment and charge point management activity across residential, commercial, and highway segments.

Barriers to entry include high capital expenditure for grid connection and hardware installation, the need for scalable network management platforms, multi-state regulatory compliance capability, and the ability to establish utility or property partnerships for site access. These factors favor well-capitalized incumbents with established charge point footprints and diversified product and service portfolios.

Consolidation is accelerating as smaller independent CPOs exit under margin pressure and larger operators acquire network density, technology capabilities, and energy management expertise. Strategic partnerships between energy utilities, automotive OEMs, and real estate developers are further reinforcing competitive positioning across the structured segments of the market, and this trend is expected to intensify through the forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

DC charging is the fastest-growing charging station type, driven by urban fast-charging hubs and logistics fleet depot deployments. Portable charger represents a growing opportunity in residential and multi-dwelling segments seeking flexible, lower-cost charging solutions.

Emerging Markets

Eastern Germany at 13.8% presents the largest greenfield infrastructure gap and is receiving substantial federal and EU co-investment, creating favorable conditions for CPO expansion with lower competitive intensity than western markets.

Venture & Investment Trends

Investment is concentrated in fast-charging network operators, smart grid integration platforms, and V2G energy management software companies. Capital is also flowing into modular DC charging hardware, fleet depot management solutions, and subscription-led energy service models that align with Germany's growing electric vehicle owner base and corporate sustainability mandates.

Future Market Outlook (2026-2034)

The Germany electric vehicle charging station market is forecast to expand from USD 2.10 Billion in 2025 to USD 15.14 Billion by 2034 at a CAGR of 23.53%, adding approximately USD 13.04 Billion in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: Germany's binding decarbonization agenda and the phased transition away from combustion engine vehicles; the completion of a nationwide DC fast-charging corridor network along the Autobahn under AFIR mandates; the commercialization of smart and vehicle-to-grid bidirectional charging ecosystems; and the progressive scaling of inductive wireless charging technology from pilot deployments into commercial fleet and automated vehicle applications.

By 2034, Germany's electric vehicle charging infrastructure is expected to be defined by a mature, nationally integrated network spanning residential, commercial, highway, and fleet segments, unified under interoperable software platforms and seamless payment ecosystems. Regulatory consolidation, deepening automotive OEM and utility partnerships, and the expansion of renewable energy-powered charging are expected to further accelerate the evolution of the market toward full-scale commercial maturity within the forecast horizon.

Research Methodology

Primary Research

Primary research involves direct engagement with industry stakeholders including charge point operators, equipment manufacturers, energy utilities, automotive OEMs, government bodies, and industry associations. Structured interviews and surveys are conducted to obtain market sizing validation, competitive intelligence, and forward-looking qualitative insights.

Secondary Research

Secondary research draws on publicly available data sources including company annual reports, regulatory filings, national statistics (Federal Network Agency, Federal Motor Transport Authority), EU regulatory publications, industry association reports, and financial databases. Patent filings and technical standards bodies are also monitored for technology trend intelligence.

Forecasting Models

Market size forecasts are developed using a bottom-up modelling approach, beginning with electric vehicle fleet growth projections, average charging infrastructure requirements per vehicle, and segment-specific adoption curves. These are cross-validated against top-down macroeconomic and policy scenario models. CAGR calculations employ the standard compound annual growth rate formula across the historical and forecast periods.

Germany Electric Vehicle Charging Station Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Charging Station Types Covered | AC Charging, DC Charging, Inductive Charging |

| Vehicle Types Covered | Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), Hybrid Electric Vehicle (HEV) |

| Installation Types Covered | Portable Charger, Fixed Charger |

| Charging Levels Covered | Level 1, Level 2, Level 3 |

| Connector Types Covered | Combines Charging Station (CCS), CHAdeMO, Normal Charging, Tesla Supercharger, Type-2 (IEC 621196), Others |

| Applications Covered | Residential, Commercial |

| Regions Covered | Western Germany, Southern Germany, Eastern Germany, Northern Germany |

| Companies Covered | EnBW Energie Baden-Württemberg AG, E.ON SE, Siemens, ABB, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Germany electric vehicle charging station market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Germany electric vehicle charging station market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Germany electric vehicle charging station industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Germany Electric Vehicle Charging Station Market Report

The Germany electric vehicle charging station market was valued at USD 2.10 Billion in 2025, driven by accelerating electric vehicle adoption, supportive government policies, and continued investments in public and private charging infrastructure.

The market is expected to exhibit a CAGR of 23.53% during 2026-2034, reaching USD 15.14 Billion, supported by the rapid expansion of fast-charging networks, increasing electrification of transport, and ongoing advancements in smart and connected charging technologies.

AC charging holds the largest share at 53.7% in 2025, due to wide residential and workplace adoption.

Fixed charger accounts for 72.4% of the market in 2025, driven by high uptake in public and commercial locations.

Western Germany dominates with a 37.5% share in 2025, fueled by high electric vehicle penetration and strong infrastructure.

Key companies include EnBW Energie Baden-Württemberg AG, E.ON SE, Siemens, and ABB, among others.

Key drivers include rapid electric vehicle adoption, government subsidies, Autobahn charging corridors, and expanding grid connectivity.

Key challenges include high installation costs, grid capacity constraints, and standardization issues across charging networks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)