Germany Telemedicine Market Size, Share, Trends and Forecast by Component, Modality, Delivery Mode, Facility, Application, End User, and Region, 2026-2034

Germany Telemedicine Market Overview:

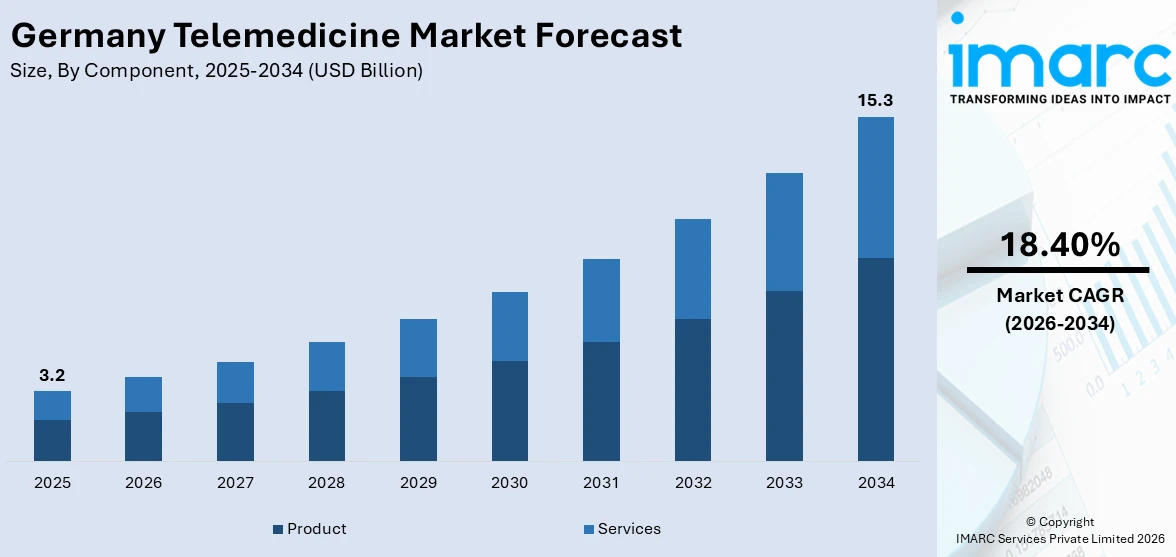

The Germany telemedicine market size reached USD 3.2 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 15.3 Billion by 2034, exhibiting a growth rate (CAGR) of 18.40% during 2026-2034. Advancements in digital health technologies, an increasing demand for remote healthcare services, a strong focus on improving healthcare accessibility and efficiency, government initiatives supporting digital health, coupled with an aging population base, and the increasing need for cost-effective medical solutions are some of the major factors propelling the market growth across the country.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 3.2 Billion |

| Market Forecast in 2034 | USD 15.3 Billion |

| Market Growth Rate (2026-2034) | 18.40% |

Germany Telemedicine Market Trends:

Government Support and Regulatory Framework

Strong government initiatives and supportive regulations, including funding and reimbursement policies for telemedicine services, encourage the adoption of digital health solutions. For example, on 14 December 2023, the German Bundestag passed the Act to Speed Up the Digitalisation of the Healthcare System (Digital Act – DigiG) during its second/third reading, which took effect on 26 March 2024. The purpose of this Act is to enhance daily healthcare in Germany through digital solutions like the electronic patient record (ePA) and electronic prescription (e-prescription). In recent years, the Federal Ministry of Health has created the essential framework for significantly enhancing digital transformation to improve healthcare delivery in Germany across all levels, establishing and providing the required foundational structures for a contemporary healthcare system and data-driven medical care, while primarily simplifying daily routines for individuals and offering a concrete benefit to patients, doctors, and all other healthcare professionals. Important initiatives in this regard involve creating secure networks within the healthcare system (telematics infrastructure - TI), launching the e-Health Card (eGK) along with its applications, implementing the electronic patient record (ePA) and the electronic prescription (e-prescription), providing new services via digital health applications (DiGA) and digital applications for long-term care (DiPA) for insurance beneficiaries, as well as expanding the use of video consultations and additional services in telemedicine.

To get more information on this market Request Sample

Increasing Demand for Accessible Healthcare

The need for more accessible and convenient healthcare services, especially in remote or underserved areas, drives the growth of telemedicine as it offers efficient solutions for patient management and consultation. The increasing adoption of digital health solutions, coupled with advancements in artificial intelligence and data analytics, further accelerates the expansion of telemedicine services. For instance, in February 2024, in cooperation with ADAC, TeleClinic developed an app integration that gives ADAC members access to online medical consultations at any time. This collaboration enhanced healthcare accessibility by providing immediate virtual consultations, reducing patient waiting times, and optimizing doctor availability. Members could use the medical app of Europe's largest and best-known mobility club to access telemedical services from around 1,500 doctors based in Germany. These included electronic sick notes, prescriptions, and medical consultations. The incorporation of secure digital payment methods and electronic health records enhanced the efficiency and reliability of telehealth services. Telemedicine makes it easier for people to access medical care, regardless of where they live. Additionally, growing investments in telehealth infrastructure and favorable government policies supporting digital healthcare contribute to market expansion. The TeleClinic team is delighted that ADAC, with its reach of over 21 million members, is helping to promote telemedicine services in Germany by offering low-threshold services. The increasing consumer preference for virtual healthcare solutions highlights a shift toward more technology-driven medical services.

Germany Telemedicine Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the regional level for 2026-2034. Our report has categorized the market based on component, modality, delivery mode, facility, application, and end user.

Component Insights:

- Product

- Hardware

- Software

- Others

- Services

- Tele-Consulting

- Tele-Monitoring

- Tele-Education

The report has provided a detailed breakup and analysis of the market based on the component. This includes product (hardware, software, and others) and services (tele-consulting, tele-monitoring, and tele-education).

Modality Insights:

- Real-time

- Store and Forward

- Others

A detailed breakup and analysis of the market based on the modality have also been provided in the report. This includes real-time, store and forward, and others.

Delivery Mode Insights:

- Web/Mobile

- Audio/Text-based

- Visualized

- Call Centers

The report has provided a detailed breakup and analysis of the market based on the delivery mode. This includes web/mobile (audio/text-based and visualized) and call centers.

Facility Insights:

- Tele-Hospital

- Tele-Home

A detailed breakup and analysis of the market based on the facility have also been provided in the report. This includes Tele-Hospital and Tele-Home.

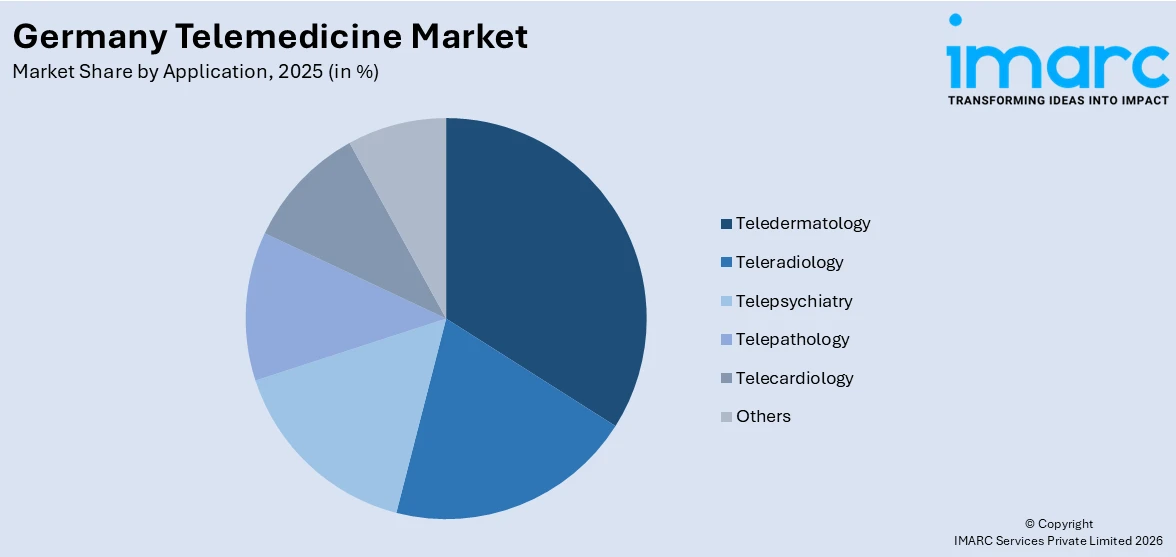

Application Insights:

Access the comprehensive market breakdown Request Sample

- Teledermatology

- Teleradiology

- Telepsychiatry

- Telepathology

- Telecardiology

- Others

The report has provided a detailed breakup and analysis of the market based on the application. This includes teledermatology, teleradiology, telepsychiatry, telepathology, telecardiology, and others.

End User Insights:

- Providers

- Payers

- Patients

- Others

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes providers, payers, patients, and others.

Regional Insights:

- Western Germany

- Southern Germany

- Eastern Germany

- Northern Germany

The report has also provided a comprehensive analysis of all the major regional markets, which include Western Germany, Southern Germany, Eastern Germany, and Northern Germany.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Germany Telemedicine Market News:

- In November 2024, Hamburg-based TCC raised €20 million in Series A funding to expand its AI-driven telemedicine solutions for intensive care units (ICUs). The round, led by Captain Thomas Pötzsch, supported TCC's goal of enhancing remote ICU support and optimizing hospital processes. The company was already managing over 3,000 beds worldwide.

- In October 2023, Sidekick Health, a digital healthcare firm, revealed it has ventured into the prescription digital therapeutics sector through a strategic acquisition of Aidhere, a producer of PDTs in Germany. The purchase allowed the company to integrate Zanadio, a thriving PDT that has completed more than 50,000 prescriptions and is recognized as permanently approved within Germany's regulated nationwide DiGA (Digitale Gesundheitsanwendungen) for digital apps that can be prescribed.

Germany Telemedicine Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Modalities Covered | Real-time, Store and Forward, Others |

| Delivery Modes Covered |

|

| Facilities Covered | Tele-Hospital, Tele-Home |

| Applications Covered | Teledermatology, Teleradiology, Telepsychiatry, Telepathology, Telecardiology, Others |

| End Users Covered | Providers, Payers, Patients, Others |

| Regions Covered | Western Germany, Southern Germany, Eastern Germany, Northern Germany |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Germany telemedicine market performed so far and how will it perform in the coming years?

- What is the breakup of the Germany telemedicine market on the basis of component?

- What is the breakup of the Germany telemedicine market on the basis of modality?

- What is the breakup of the Germany telemedicine market on the basis of delivery mode?

- What is the breakup of the Germany telemedicine market on the basis of facility?

- What is the breakup of the Germany telemedicine market on the basis of application?

- What is the breakup of the Germany telemedicine market on the basis of end user?

- What is the breakup of the Germany telemedicine market on the basis of region?

- What are the various stages in the value chain of the Germany telemedicine market?

- What are the key driving factors and challenges in the Germany telemedicine market?

- What is the structure of the Germany telemedicine market and who are the key players?

- What is the degree of competition in the Germany telemedicine market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Germany telemedicine market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Germany telemedicine market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Germany telemedicine industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)