Glamping Market Size, Share, Trends and Forecast by Type, Age Group, Size, and Region, 2026-2034

Global Glamping Market Size, Share, Trends & Forecast (2026-2034)

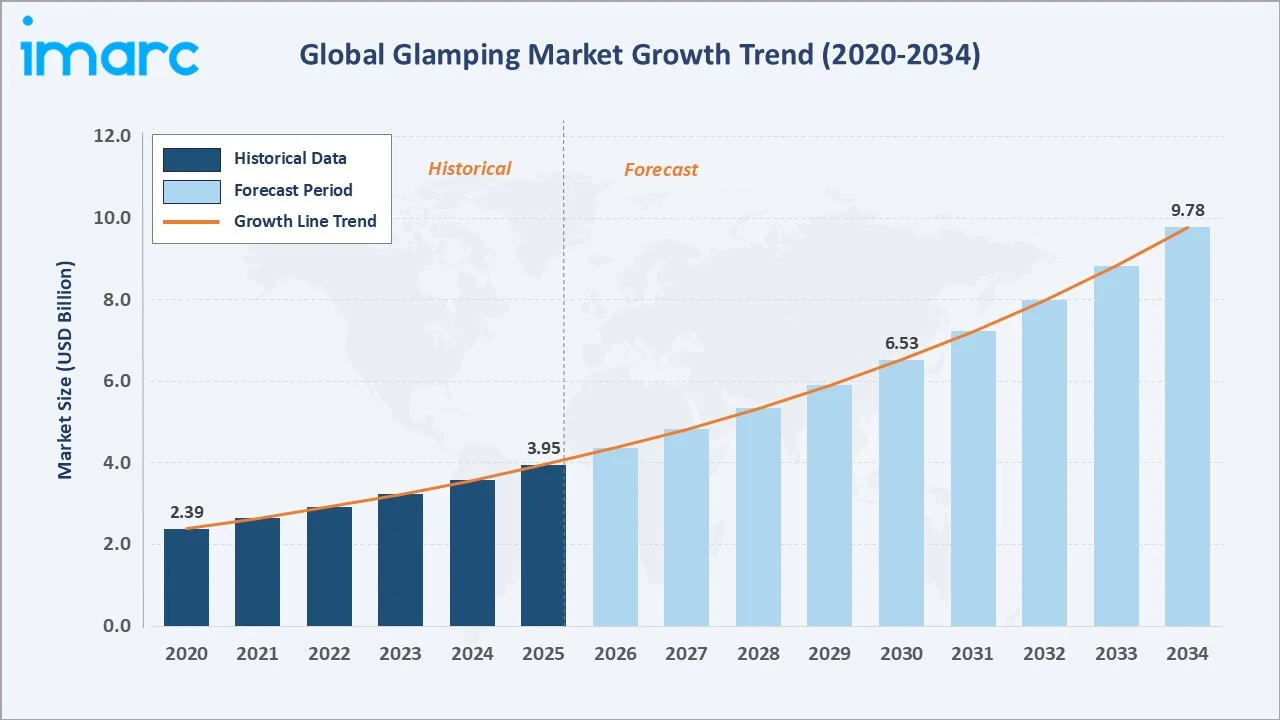

The global glamping market size reached USD 3.95 Billion in 2025 and is projected to reach USD 9.78 Billion by 2034, at a CAGR of 10.60% during 2026-2034. Rising consumer demand for unique, nature-immersive luxury experiences, the influence of social media in shaping travel aspirations, escalating eco-tourism preferences, and the entry of major hotel brands, including Marriott (Postcard Cabins acquisition, December 2024), Hyatt (Under Canvas alliance, July 2024), and Hilton (AutoCamp partnership, February 2024), are the primary growth catalysts. Cabins and pods lead the type segment at 44.3%, the 18–32 years age group dominates at 45.3%, and Europe holds the largest regional share at 35.3% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.95 Billion |

|

Forecast Market Size (2034) |

USD 9.78 Billion |

|

CAGR (2026-2034) |

10.60% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

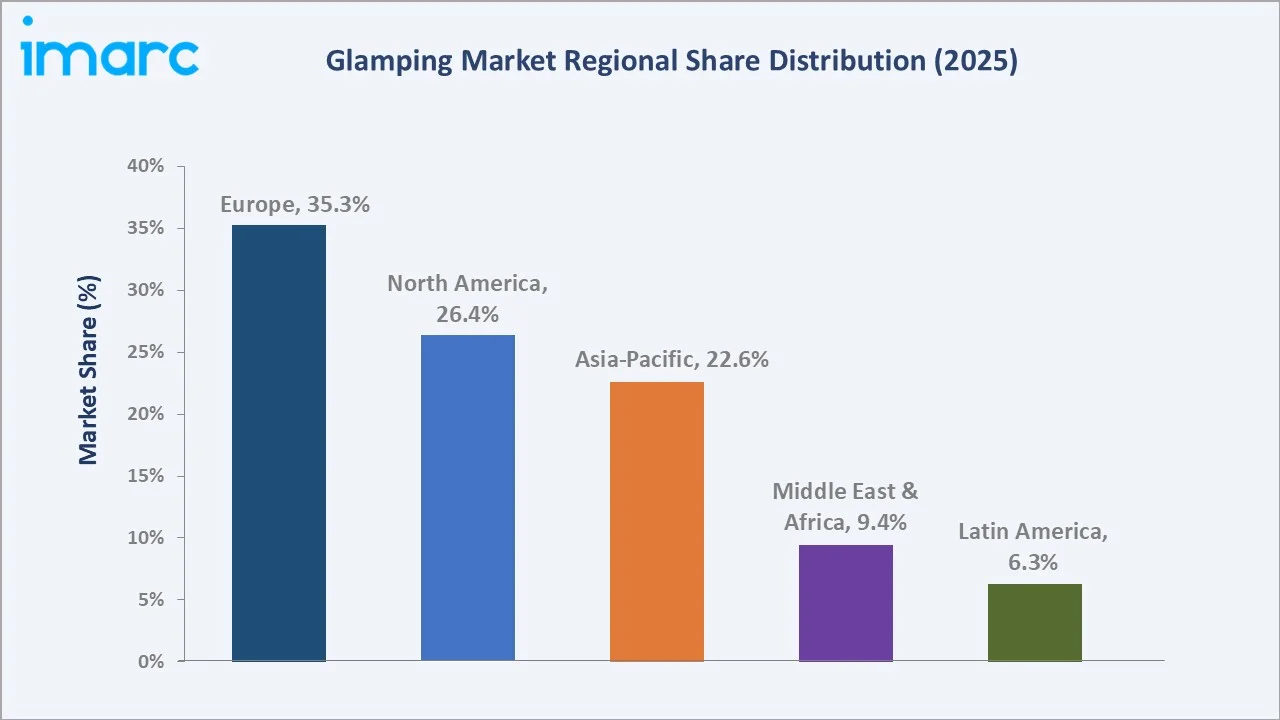

Europe (35.3%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (~12.6% CAGR, 2026-2034) |

|

Leading Type |

Cabins and Pods (44.3%, 2025) |

|

Leading Age Group |

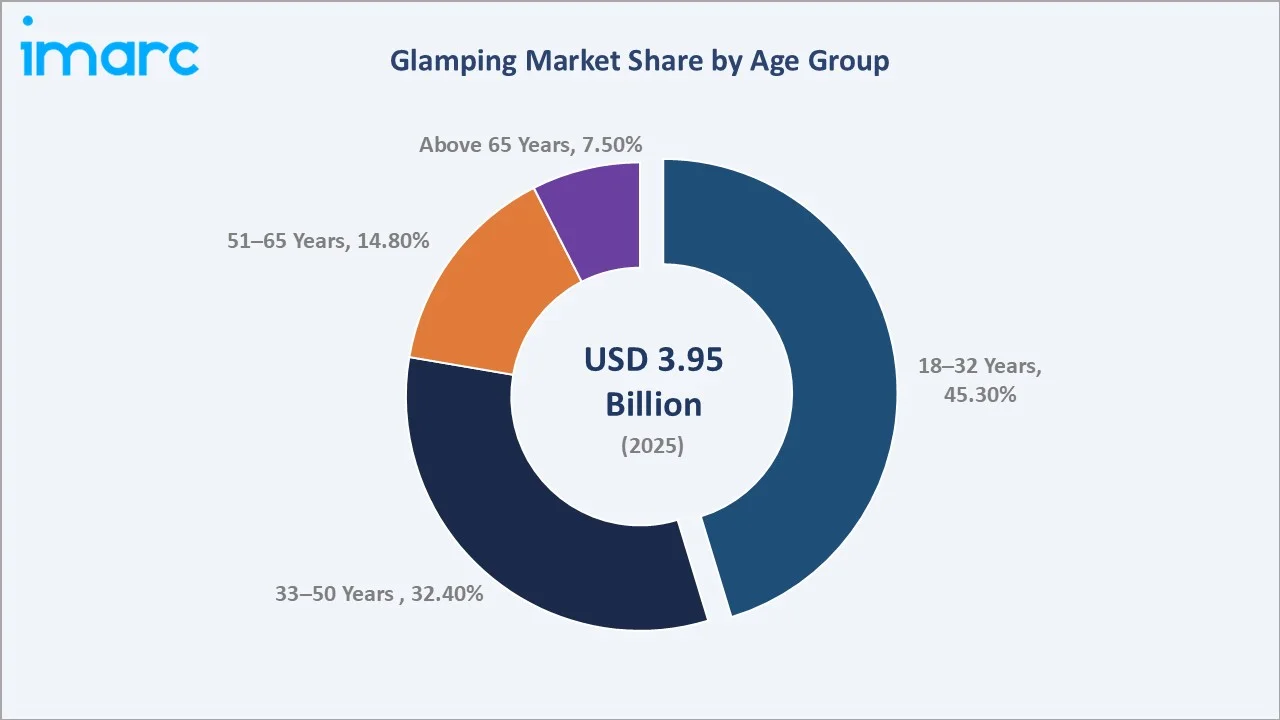

18-32 Years (45.3%, 2025) |

The glamping market from 2020 through 2034, expanded from USD 2.39 Billion in 2020 to USD 3.95 Billion in 2025, driven by the pandemic-era domestic travel surge and post-pandemic experiential travel boom, anchored at USD 6.53 Billion in 2030 before reaching USD 9.78 Billion by 2034.

To get more information on this market, Request Sample

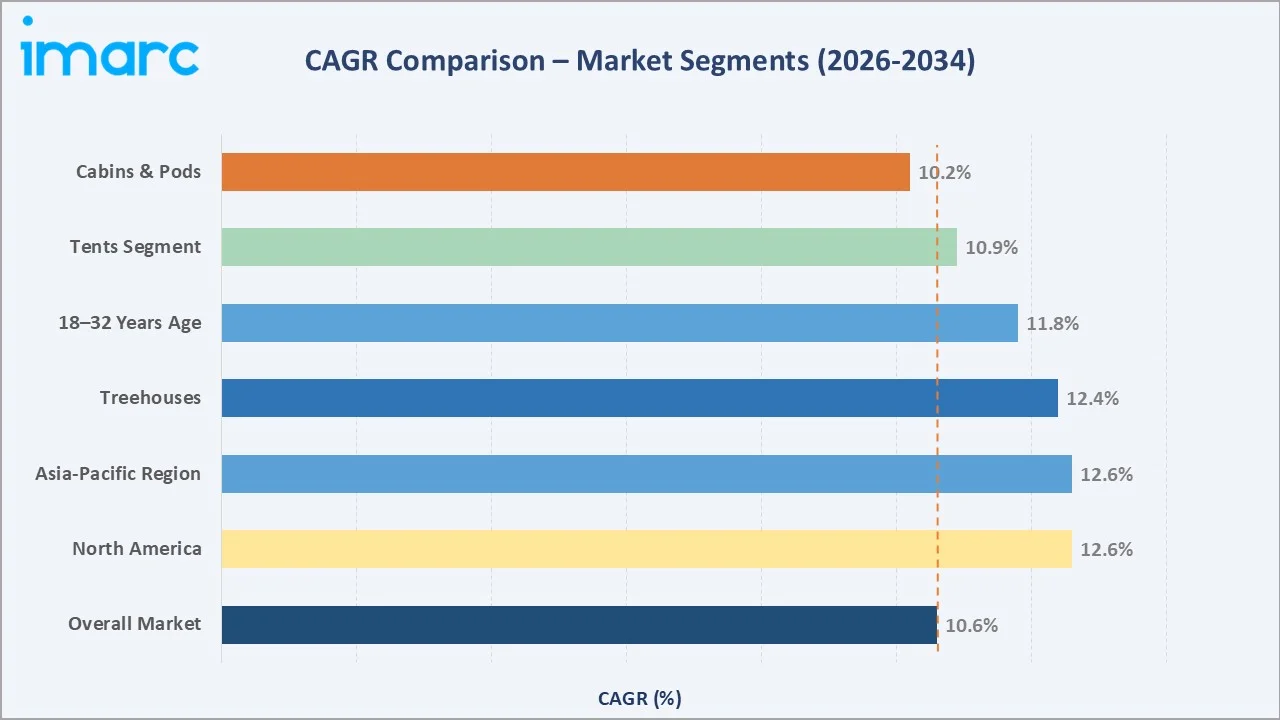

The CAGR across key segments, North America and Asia-Pacific jointly lead at ~12.6% CAGR and treehouses at ~12.4%, both materially above the overall 10.60%, reflecting rapid US glamping institutionalization and Asia-Pacific’s rapidly expanding luxury outdoor tourism infrastructure through 2034.

Executive Summary

The global glamping market is expanding at a robust 10.60% CAGR from USD 3.95 Billion in 2025 to USD 9.78 Billion by 2034. Glamping, a portmanteau of ‘glamorous’ and ‘camping’, refers to luxury outdoor accommodation experiences that combine nature immersion with premium amenities, including comfortable beds, climate control, en-suite bathrooms, gourmet dining, and Wi-Fi connectivity.

Cabins and pods command the dominant type share at 44.3% in 2025, valued for their all-weather versatility, higher amenity ceiling, and year-round operational capability versus tented structures. Under Canvas, which opened an 80-acre camp near Yosemite National Park in 2025, features safari-inspired tents with king-size beds, luxe linens, private decks, and ensuite bathrooms. The 18–32 age group dominates at 45.3% in 2025, reflecting Millennials’ and Gen Z’s documented preference for experiential travel over material possessions, amplified by Instagram and TikTok travel content that has made glamping a viral aspirational travel category.

Europe leads regionally at 35.3% in 2025, with the UK, France, Italy, and the Netherlands having the most mature glamping infrastructure. Major hotel brands’ entry into glamping, Marriott’s December 2024 acquisition of Postcard Cabins (29 outposts, 1,200+ cabins) with Goldman Sachs advising and Hyatt’s integration of 13 Under Canvas properties into World of Hyatt in July 2024, signals that institutional hospitality capital now views glamping as a durable, high-margin asset class.

Key Market Insights

|

Insight |

Data / Finding |

|

Largest Type |

Cabins & Pods - 44.3% (2025) |

|

Leading Age Group |

18-32 Years - 45.3% (2025) |

|

Leading Region |

Europe - 35.3% (2025) |

|

Fastest Region |

Asia-Pacific - ~12.6% CAGR |

Key Analytical Observations Supporting The Above Data:

- Cabins and pods at 44.3% in 2025, represent the most commercially mature glamping accommodation type. Their fixed, insulated structures enable year-round operations, avoiding the 2–4 month seasonal closures that afflict luxury tented operations in northern Europe and northern North America.

- The 18–32 age group at 45.3% in 2025 is driving glamping demand, which reflects a documented generational shift in travel values. A survey found that 85% individuals aged 18-41 want more technology at campgrounds, emphasizing connectivity while enjoying nature breaks, validating glamping’s Wi-Fi + nature positioning as the ideal product for digitally native consumers who seek ‘Instagram-worthy’ experiences.

- Europe’s 35.3% regional share in 2025reflects the continent’s longest-established glamping infrastructure.

- Asia-Pacific at 22.6% in 2025 is growing at ~12.6% CAGR, which is the market’s highest-growth region. Japan’s ‘glamping boom’, across its scenic mountains, coastlines, and volcanic landscapes, has made it the world’s second-largest individual country glamping market after the US.

Global Glamping Market Overview

Glamping is a luxury outdoor accommodation category that bridges the gap between traditional camping and boutique hotel experiences. It encompasses a diverse range of accommodation types such as cabins and pods, luxury tents, yurts, treehouses, geodesic domes, Airstream trailers, shepherd huts, and floating accommodations, typically located in scenic natural settings, including national parks, farms, vineyards, forests, mountains, and coastal areas.

The ecosystem connects land and property owners, glamping developers and operators, technology and amenity providers, booking platforms and OTAs, and end-user travelers across leisure, corporate retreat, and event segments.

Market Dynamics

To evaluate market opportunities, Request Sample

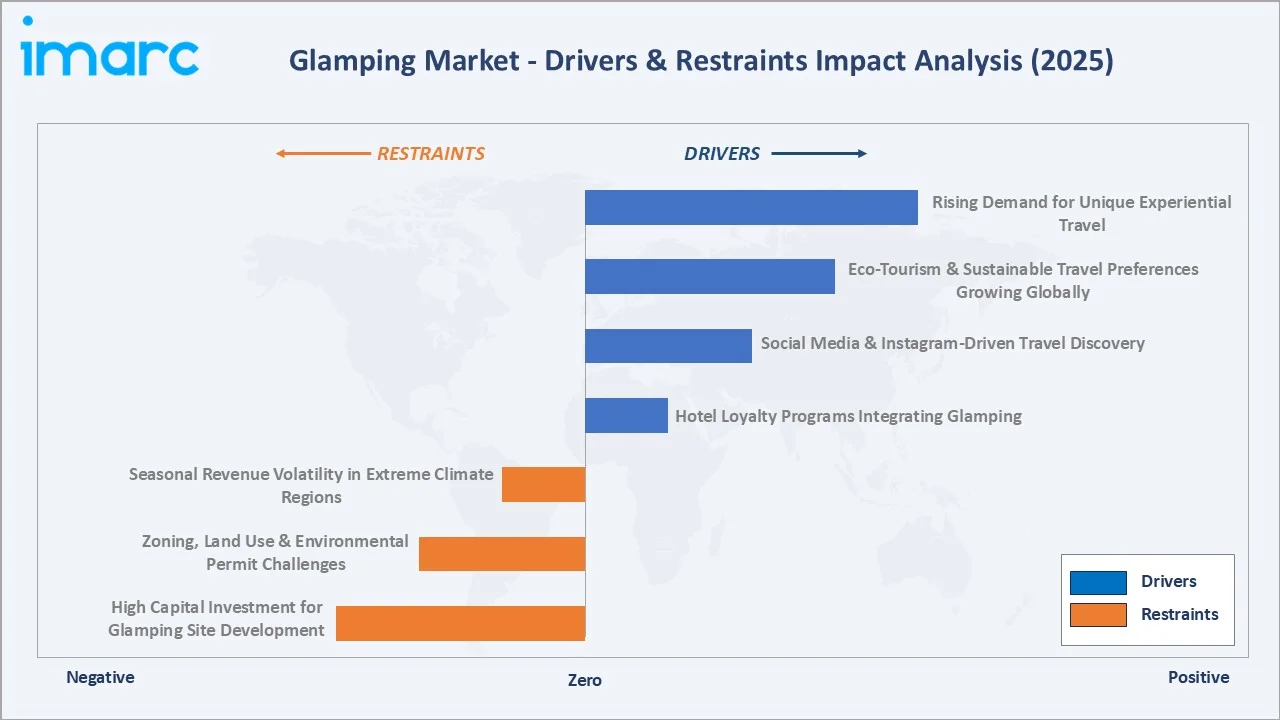

Market Drivers

- Rising Consumer Demand for Unique Experiential Travel: The ‘experience economy’ megatrend, where consumers prioritize memorable experiences over material possessions, is the fundamental structural driver of the glamping market. A survey found that 85% individuals aged 18-41 explicitly prioritize technology connectivity, comfort, and unique experiences at campgrounds, validating glamping’s proposition precisely.

- Eco-Tourism and Sustainable Travel Preferences Amplifying Glamping Appeal: 93% of global travelers aim to make more sustainable travel decisions and have already taken steps in that direction, and glamping’s nature-immersive positioning aligns uniquely with this sustainability value.

- Social Media and Digital Platform Amplification of Glamping Discovery: Instagram, TikTok, and Pinterest have collectively created an organic, user-generated marketing engine that continuously drives glamping discovery and aspiration among the 18–32 age group demographic.

Market Restraints

- High Capital Investment Requirements for Site Development: Developing a premium glamping site requires substantial upfront capital for land acquisition or lease, infrastructure development, accommodation structure construction, and amenity installations.

- Zoning, Land Use, and Environmental Permitting Complexity: Establishing glamping sites in scenic rural and natural areas requires navigating complex, multi-jurisdictional permitting processes, including agricultural zoning exceptions, environmental impact assessments, fire safety compliance, wastewater management approvals, and tourism operator licensing.

Market Opportunities

- Wellness and Corporate Retreat Integration Creating Premium Revenue Streams: The global wellness tourism market growth, with forest bathing, yoga retreats, digital detox programs, and spa integrations at glamping sites, is attracting premium corporate retreat spending.

- Asia-Pacific’s Rapidly Expanding Luxury Outdoor Tourism Market: China’s domestic camping and glamping market, recovering strongly post-pandemic as domestic nature tourism becomes a mainstream middle-class activity. Bali’s luxury jungle glamping properties and Thailand’s treehouse eco-resorts attract premium international travelers, generating foreign exchange revenue that is incentivizing Southeast Asian government tourism authorities to actively facilitate glamping development approvals.

Market Challenges

- Tariff and Supply Chain Risks for Glamping Structures: US tariffs of up to 150% on imported canvas tent materials with no domestic US textile manufacturing alternative capable of meeting glamping-grade quality and quantity requirements, represent an acute near-term cost risk for the US glamping industry.

- Labor Scarcity in Remote Rural Glamping Markets: Premium glamping guest experiences require trained hospitality staff, chefs, guides, concierge teams, and housekeeping at locations from major urban labor markets. Staff housing on-site, common at wilderness glamping operations, adds further capital and operating cost complexity.

Emerging Market Trends

1. Major Hotel Loyalty Program Integration Transforming Glamping Distribution

2024 marked the watershed moment when all three of the US’s largest hotel loyalty programs simultaneously entered glamping. Marriott’s Postcard Cabins acquisition in December 2024 added 1,200+ tiny cabins, providing glamping operators with demand generation at zero customer acquisition cost through established loyalty infrastructure.

2. Eco-Certification and Sustainability Becoming Core Competitive Differentiators

Glamping operators across Europe and North America are investing in comprehensive sustainability certifications, LEED certification for permanent structures, B Corp status for glamping operators, leave-no-trace protocols, and carbon-offset programs, as eco-conscious travelers increasingly specify sustainability credentials in booking decisions.

3. Wellness and Mindfulness Integration Elevating Average Daily Rates

The convergence of wellness tourism and glamping is creating a premium segment where spa treatments, guided meditation, sound bath ceremonies, forest therapy walks, and farm-to-table dining are packaged as integrated glamping wellness retreats. The global wellness tourism market provides the macroeconomic demand backdrop for sustained wellness glamping premium pricing power.

4. Smart Technology Integration Enhancing Guest Experience and Operational Efficiency

IoT-enabled glamping structures with app-controlled climate systems, smart lighting, keyless entry, and personalized in-room entertainment are progressively becoming standard at premium glamping properties.

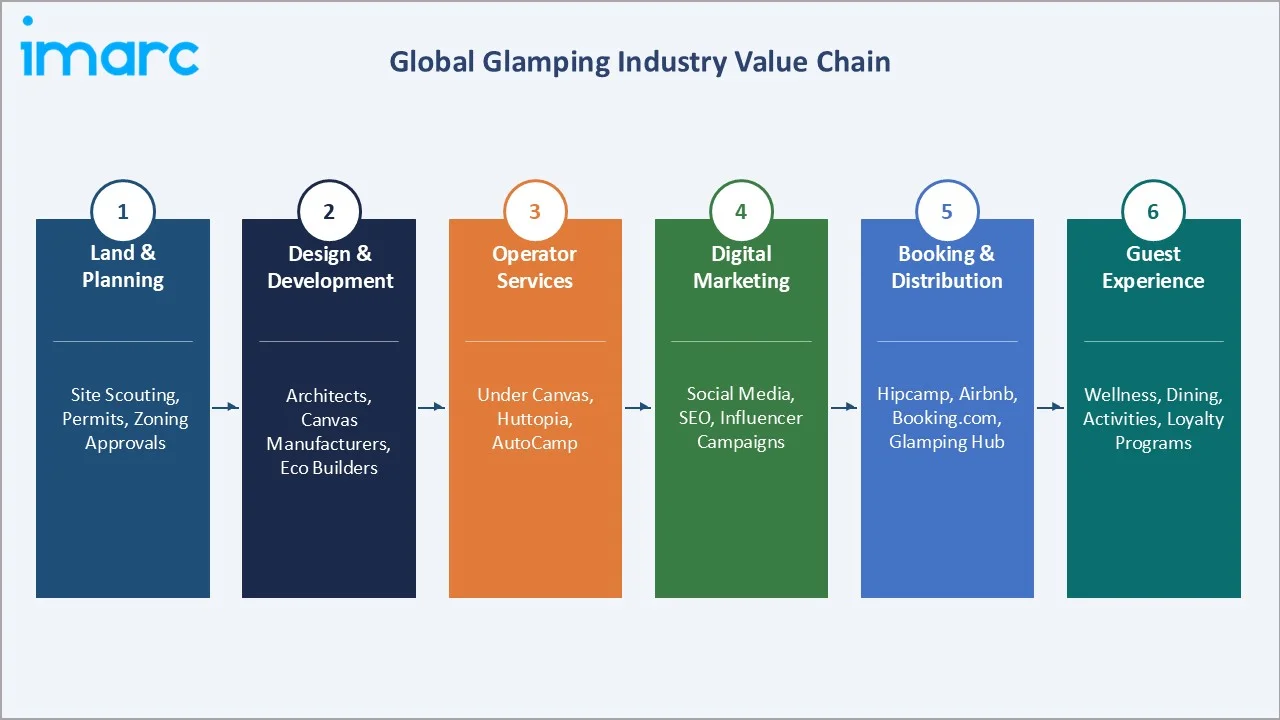

Industry Value Chain Analysis

The glamping value chain generates the highest margin at the branded operator stage, where operators like Under Canvas achieve EBITDA margins of 25–35% on premium tented properties, significantly above the 10–15% margins of independent single-site glamping operators competing without brand recognition, loyalty program access, or economies of scale.

|

Stage |

Key Players & Examples |

|

Land & Planning |

National Park concessionaires, private landowners, rural local authorities, site scouting agencies, and environmental impact consultants |

|

Design & Construction |

Canvas architects, eco-pod manufacturers, timber frame cabin builders, geodesic dome fabricators, and landscape architects |

|

Operator Services |

Under Canvas, Huttopia, and more |

|

Booking & Distribution |

Hipcamp, Glamping Hub, Airbnb, Booking.com, direct booking websites |

|

Guest Experience |

Guided nature activities, farm-to-table dining, wellness treatments, stargazing programs, campfire experiences, local cultural immersion, digital concierge services |

Booking platform commissions of 15–25% are driving premium glamping operators, AutoCamp, Under Canvas, Huttopia, to invest in direct booking capability through CRM systems, email marketing, and loyalty programs that reduce platform dependency. Direct bookings are growing relative to platform-mediated bookings, reflecting operators’ increasing sophistication in customer relationship management and the higher margin economics of direct channel bookings.

Technology Landscape in the Glamping Industry

Smart Accommodation Technology

IoT-enabled glamping structures are incorporating app-controlled Nest thermostats, Philips Hue smart lighting, keyless Schlage smart lock entry, and Amazon Echo voice control systems that allow guests to control their accommodation environment from smartphones before arrival.

Sustainable Construction Technology

Cross-laminated timber (CLT), a sustainable alternative to concrete and steel that offers equivalent structural performance with significantly lower carbon footprint, is being adopted for permanent glamping cabin and pod structures by leading eco-certified operators. Glamping tents utilizing ECONYL recycled nylon canvas, FSC-certified timber frames, and sheep’s wool insulation are achieving LEED and BREEAM certification points that support premium eco-destination marketing claims.

Booking and Revenue Management Technology

Dynamic pricing algorithms, comparable to hotel revenue management systems, are being adapted for glamping properties, enabling operators to automatically adjust nightly rates based on occupancy forecasts, local event calendars, competitor pricing, and weather forecasts.

Wellness Technology Integration

Biometric wellness technology, sleep quality monitoring, HRV measurement, and nature immersion ‘prescriptions’ based on evidence-based wellness research are being piloted at premium wellness glamping retreats targeting the stress-recovery travel segment.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Cabins and Pods |

44.3% |

2025 |

|

Age Group |

18-32Years |

45.3% |

2025 |

|

Size |

4 Persons |

37.7% |

2025 |

|

Region |

Europe |

35.3% |

2025 |

By Type

Cabins and pods command 44.3% in 2025, growing steadily as operators invest in all-weather permanent structures that enable year-round occupancy. AutoCamp’s Airstream suite portfolio, featuring enhanced amenities including spa-inspired bathrooms, queen beds, and private outdoor spaces, achieves average daily rates. The pod category within this segment, geodesic domes, bubble pods with panoramic windows, and eco-pods, is growing as their photogenic forms generate premium social media content that drives direct booking demand.

To access detailed market analysis, Request Sample

Tents at 24.6% include luxury safari-inspired canvas tents and luxury bell tents at premium locations. Under Canvas’ Yosemite camp, 80 acres of safari-inspired tents with private decks, ensuite bathrooms, and guided nature programming, demonstrated in 2025 that luxury tented glamping can command within the US domestic market. Treehouses at 10.4%, the fastest-growing type at ~12.4% CAGR, benefit from extreme social media shareability and scarcity-driven premium pricing. Yurts at 14.8% serve European cultural heritage glamping markets and wellness retreat applications where their circular interior creates natural meditation and community gathering spaces.

By Age Group

The 18–32 years age group at 45.3% in 2025 is the glamping market’s dominant consumer demographic, driven by Millennial and Gen Z travelers’ documented preference for experiential, photogenic, and nature-connected travel experiences. This cohort, the first ‘digital native’ generation raised on Instagram travel discovery, identifies glamping as the ideal intersection of their values: outdoor adventure, sustainability, luxury comfort, and Instagram-worthy aesthetics that generate social capital among peers.

The 33–50 age group at 32.4% in 2025, growing at ~10.2% CAGR represents the highest-spend-per-person glamping demographic, driven by family glamping and mid-life wellness retreat travel. This group is specifically targeted by glamping operators’ spa packages, couples’ retreats, and family activity programming, including children’s nature education and guided wildlife spotting. The 51–65 age group at 14.8% (2025), predominantly empty-nester couples, is attracted to boutique glamping’s intimate property scale and personalized service levels that large resort hotels cannot replicate, with a preference for wine-country, vineyard, and heritage farm glamping settings.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Data |

|

Europe |

35.3% |

UK licensed glamping sites, Huttopia expansion, France, Italy, Netherlands mature infrastructure |

|

North America |

26.4% |

All 3 major US hotel loyalty programs enter glamping, Under Canvas 13 properties, Hipcamp listings, Marriott acquires Postcard Cabins Dec 2024 |

|

Asia-Pacific |

22.6% |

Japan glamping sites; China domestic camping/glamping market, Huttopia Japan, Bali, Thailand, Vietnam luxury eco-resort expansion |

|

Middle East & Africa |

9.4% |

UAE luxury desert glamping, Safari glamping in Kenya, Tanzania, South Africa, Saudi Arabia Vision 2030 eco-tourism, star-rated desert camp glamping growth |

|

Latin America |

6.3% |

Brazil eco-lodge and glamping expansion, Patagonia high-end wilderness glamping, Mexico glamping resorts, Costa Rica rainforest glamping eco-tourism |

Europe’s 35.3% regional dominance in 2025 reflects the continent’s glamping maturity advantage over other regions. The Canopy & Stars with over 850 amazing places to stay in the outdoors, from yurts to treehouses, exemplifies the sophisticated booking platform and quality curation infrastructure that has developed around Europe’s established glamping supply base.

North America, with 26.4% in 2025, growing at ~12.6% CAGR, has been transformed by the 2024 hotel brand entry wave. Asia-Pacific (22.6%, 2025) growing equally at ~12.6% CAGR is driven by Japan’s explosive domestic glamping adoption and China’s post-pandemic nature tourism boom and glamping spending.

Competitive Landscape

The global glamping market is moderately fragmented overall but increasingly concentrated in the premium branded segment.

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Under Canvas |

Under Canvas |

Leader |

Hyatt World of Hyatt integration (July 2024) |

|

Huttopia |

Huttopia Nature Camps |

Leader |

Widest global geographic footprint, France, Canada, family-focused positioning |

|

AutoCamp |

AutoCamp |

Leader |

Hilton Honors integration, Airstream brand premium |

|

Collective Retreats |

Collective Retreats |

Leader |

Urban-adjacent luxury glamping, experiential programming, millennial focus |

|

Hipcamp |

Hipcamp |

Leader |

Index Ventures & BOND Capital |

|

Eco Retreats |

Eco Retreats Wales |

Challenger |

UK eco-certified pioneer, off-grid solar glamping, carbon-neutral operations |

|

Nightfall Camp Pty Ltd. |

Nightfall |

Emerging |

Australia luxury wilderness glamping, international eco-tourism positioning |

|

Paperbark Camp |

Paperbark Camp |

Emerging |

Australia’s first luxury safari camp |

The top 5 multi-site branded operators, Under Canvas, AutoCamp, Huttopia, Collective Retreats, and Marriott, collectively account for an estimated 15–20% of global glamping market revenue in 2025, with the remainder distributed across thousands of independent single-site operators globally.

Key Company Profiles

Under Canvas

Under Canvas, headquartered in Denver, is the US’s largest branded luxury glamping operator, managing 14 properties adjacent to or near major US national parks, including Yellowstone, Grand Canyon, Glacier, Zion, Bryce Canyon, Mount Rushmore, etc.

- Product Portfolio: Under Canvas offers safari-inspired luxury canvas tents, organized around centrally located camp hubs offering nightly campfire experiences, gourmet dining, curated guided activities, daily events, and concierge services.

- Recent Developments: In February 2026, Under Canvas announced an expansion and a series of guest experience enhancements set to launch for the 2026 season.

- Strategic Focus: Under Canvas’ strategy centers on national park adjacency as the primary location differentiation, placing premium glamping at the gateway to America’s most aspirational natural destinations, where the National Park Service’s restrictions on in-park accommodation create structural undersupply that commands above-market pricing.

Huttopia

Huttopia, headquartered in Lyon, France, is the world’s most geographically diversified glamping operator, managing nature camps across France, Canada, and the US.

- Product Portfolio: Huttopia offers accommodation categories across its sites, which include the cahutte, the canadienne tent, the bonaventure tent, the trappeur tent, the cabane.

- Recent Developments: In March 2025, Huttopia with more than 100 ready-to-camp sites around the world, expanded its footprint in North America.

- Strategic Focus: Huttopia’s family-focused strategy, positioning its nature camps as the premium alternative to conventional family camping rather than the affordable alternative to luxury hotels, creates a distinct competitive position from the couples-and-honeymoon focus of Under Canvas and the weekend-escape positioning of Getaway.

Collective Retreats

Collective Retreats, headquartered in Denver, is a premium urban-adjacent glamping operator managing luxury retreat properties near Governors Island (NYC), Yellowstone (Wyoming), Vail (Colorado), and Sonoma (California).

- Product Portfolio: Collective Retreats offers Journey Tents, and Outlook Shelters.

- Recent Developments: Collective Retreats launched a corporate retreat program targeting financial services and technology companies seeking distinctive off-site event venues near their NYC and Bay Area headquarters.

- Strategic Focus: Collective Retreats’ urban-adjacent strategy, ensuring all properties are reachable from a major city within 2 hours, eliminates the flight requirement that limits traditional destination resort glamping to infrequent vacation occasions, enabling Collective Retreats to capture monthly or quarterly short-break demand from affluent urban professionals.

Market Concentration Analysis

The global glamping market is highly fragmented, with the top 5 branded multi-site operators estimated to hold only 12-20% of total market revenue in 2025. The vast majority, 80–88% of global glamping revenue, is generated by independent single-site operators, who collectively define the market’s character but individually lack the brand, technology, and capital infrastructure of institutional operators.

Consolidation is accelerating at the multi-site operator level: Marriott’s Postcard Cabins acquisition (December 2024) and the wave of major hotel loyalty integrations collectively signal that the glamping market is transitioning from a fragmented cottage industry toward a more institutionalized sector where brand recognition, technology infrastructure, and loyalty program access become sustainable competitive advantages.

Investment & Growth Opportunities

Fastest-Growing Segments

Treehouses at ~12.4% CAGR and Asia-Pacific + North America at ~12.6% CAGR are the highest-growth investment opportunities. Treehouses’ extreme social media shareability, generating 5–10x more Instagram engagement than equivalent cabin glamping stays, drives occupancy through organic marketing that traditional advertising cannot replicate. The Asia-Pacific glamping market, with Japan as the template for rapid glamping institutionalization, offers first-mover positioning opportunities for international glamping operators willing to navigate Asia-Pacific regulatory and cultural complexity.

Emerging Markets

The Middle East, UAE’s luxury desert glamping, Saudi Arabia’s Vision 2030 eco-tourism investment pipeline, and Oman’s established desert camp glamping infrastructure, represents a rapidly professionalizing glamping market with structural demand from both domestic and incoming international tourists. Safari glamping in East Africa, Kenya, Tanzania, and Rwanda, commands the world’s highest glamping average daily rates at established luxury safari camps, including Singita, &Beyond, and Four Seasons Serengeti. These ultra-premium African glamping operations validate the ceiling of glamping’s pricing power and serve as global benchmarks for wilderness luxury hospitality ambition.

Venture and Investment Trends

Institutional investors are attracted by glamping’s 15–25% EBITDA margins at premium branded multi-site operations, 70–80% repeat booking intent rates, and structural demand growth driven by Millennial and Gen Z generational preference shifts that secular economic cycles cannot easily reverse. The Marriott Postcard Cabins acquisition (December 2024) with Goldman Sachs advising represents the glamping market’s formal entry into institutional M&A, with deal multiples for premium multi-site branded glamping operators expected to range 12–20x EBITDA through 2030.

Future Market Outlook (2026-2034)

The global glamping market is positioned for a decade of sustained double-digit growth, anchored by the irreversible generational shift in Millennial and Gen Z travel values toward experiential, sustainable, and nature-connected luxury. From USD 3.95 Billion in 2025, the market is forecast to reach USD 6.53 Billion by 2030 and USD 9.78 Billion by 2034, representing USD 5.83 Billion in absolute incremental market value over the nine-year forecast horizon at a 10.60% CAGR. The concurrent entry of Marriott, Hyatt, and Hilton into glamping in 2024 represents a structural inflection point that signals mainstream hospitality capital’s conviction in glamping’s long-term market permanence.

Technological disruptions expected between 2026 and 2034 include AI-personalized glamping experience curation, where machine learning models trained on guest behavior data automatically design individualized activity sequences, F&B menus, and sleep environment settings for each arriving guest without requiring manual preference collection, and carbon-neutral certification becoming a universal booking filter rather than a premium differentiator. Smart glamping structures with integrated biometric wellness monitoring, tracking sleep quality, HRV, and stress hormone levels during nature immersion stays, will quantify the wellness value of glamping in ways that justify premium pricing to evidence-seeking modern health consumers.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews in 2024-2025 with glamping market participants, including senior executives, independent glamping site owners across UK, France, US, and Australia, platform executives at Hipcamp and Glamping Hub, private equity investment professionals specializing in outdoor hospitality, and senior hotel executives discussing their glamping integration strategies.

Secondary Research

Key secondary sources include Sage Outdoor Advisory’s Glamping State of the Industry Report, Hipcamp Series C funding disclosures, KSL Capital Partners Under Canvas investment announcements, Whitman Peterson AutoCamp investment disclosure, Marriott International Getaway acquisition press release, World Tourism Organization UNWTO Global Tourism Report, and Global Wellness Institute Wellness Tourism Market Data.

Forecasting Models

IMARC’s Bottom-Up and Top-Down estimation models were applied. Bottom-Up aggregates glamping revenue by accommodation type (cabins, tents, yurts, treehouses) across age group segments and regional markets. Top-Down validates against global tourism spending forecasts (UNWTO), consumer experiential travel spending projections, and branded glamping operator revenue disclosures.

Glamping Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Cabins and Pods, Tents, Yurts, Treehouses, Others |

| Age Groups Covered | 18-32 years, 33-50 years, 51-65 years, Above 65 years |

| Sizes Covered | 4-Person, 2-Person, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Under Canvas, Huttopia, AutoCamp, Collective Retreats, Hipcamp, Eco Retreats, Nightfall Camp Pty Ltd., Paperbark Camp, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the glamping market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global glamping market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the glamping industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Glamping Market Report

The global glamping market reached USD 3.95 Billion in 2025, growing from USD 2.39 Billion in 2020. Growth is driven by Millennial experiential travel demand, hotel brand entries, and eco-tourism preference growth globally.

The market is projected to reach USD 9.78 Billion by 2034 at a CAGR of 10.60%, passing through USD 6.53 Billion in 2030. Hotel loyalty integration, Asia-Pacific growth, and wellness glamping premiumization are key revenue expansion drivers.

Cabins and pods lead at 44.3% in 2025, growing steadily due to all-weather year-round capability. Marriott acquired Postcard Cabins’s 1,200+ tiny cabins in December 2024 (Goldman Sachs advising). AutoCamp’s Airstream suites achieve occupancy rates.

The 18-32 years age group dominates at 45.3% in 2025. Millennial and Gen Z’s experiential travel preference, Instagram-driven glamping discovery, and survey findings that 18-41 year-olds want connectivity in nature drive this cohort’s dominant demand position.

Europe leads at 35.3% in 2025, with UK’s licensed glamping sites and Huttopia’s European expansion. France, Italy, and the Netherlands have the most mature glamping infrastructure globally.

North America and Asia-Pacific jointly grow fastest at ~12.6% CAGR. Japan glamping sites, US market, with all three major hotel loyalty programs entering glamping simultaneously.

Key players include Under Canvas, Huttopia, AutoCamp, Collective Retreats, Hipcamp, Eco Retreats, Nightfall Camp Pty Ltd., and Paperbark Camp.

Key drivers include Millennial/Gen Z experiential travel demand, couples citing uniqueness as top glamping selection criterion, eco-tourism growth, and Marriott-Hyatt-Hilton hotel loyalty integrations.

Marriott acquired Postcard Cabins (29 outposts, 1,200+ tiny cabins) in December 2024 with Goldman Sachs advising. Hyatt integrated 13 Under Canvas national park properties into World of Hyatt in July 2024. Hilton enabled Honors members to book AutoCamp Airstream stays in February 2024.

Hipcamp is the world’s largest outdoor hospitality booking platform with 500,000+ listings, 8 million users, and USD 98.6M total funding from Index Ventures and BOND Capital at a USD 300M+ valuation. Its announced acquisition of Glamping Hub (18,000 listings, 115 countries) creates the dominant outdoor hospitality platform globally.

Key challenges include US tariffs of up to 150% on imported tent canvas, rural labor scarcity at remote glamping sites, zoning and environmental permit complexity, seasonal revenue volatility in northern climates, and high capital requirements per accommodation unit.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade