Grease Market Size, Share, Trends and Forecast by Thickener Type, Base Oil, End User, and Region, 2026-2034

Grease Market Size, Share, Trends & Forecast (2026-2034)

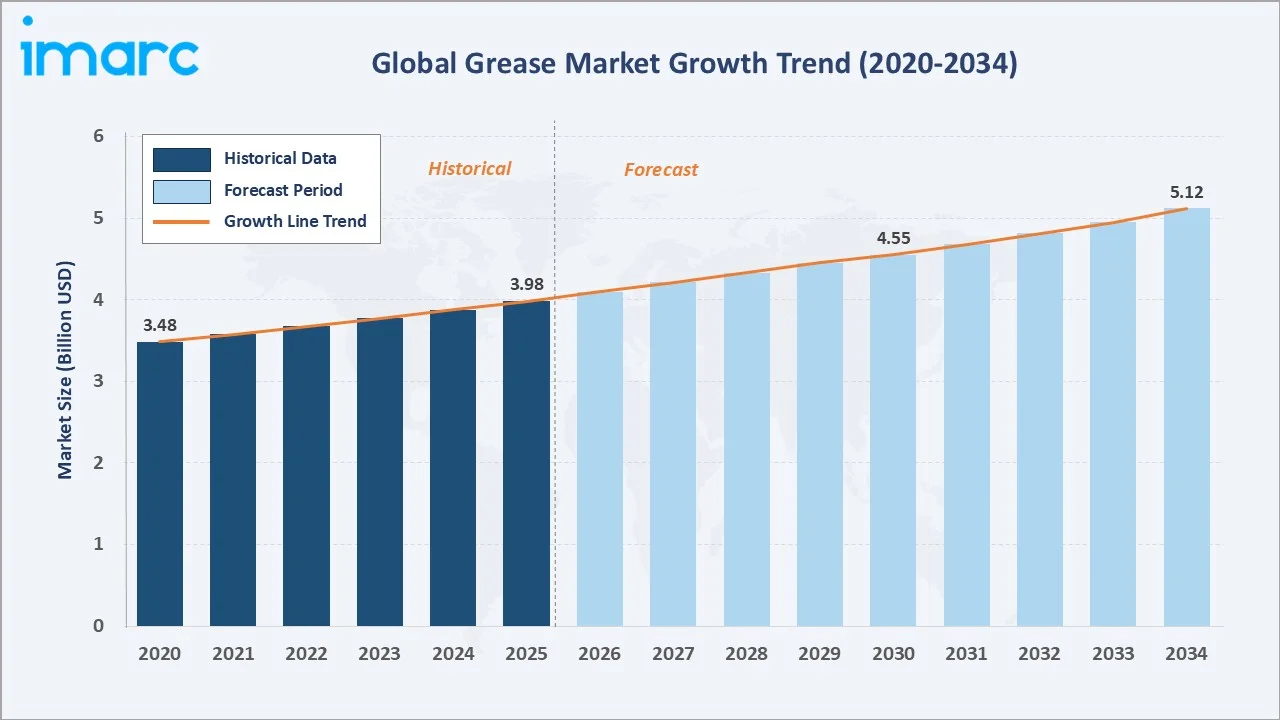

The global grease market reached USD 3.98 Billion in 2025 and is projected to reach USD 5.12 Billion by 2034, growing at a CAGR of 2.71% during 2026-2034. Sustained automotive production and fleet maintenance demand, expanding industrial machinery and construction activity, and the progressive adoption of high-performance synthetic and bio-based formulations are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.98 Billion |

|

Forecast Market Size (2034) |

USD 5.12 Billion |

|

CAGR (2026-2034) |

2.71% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

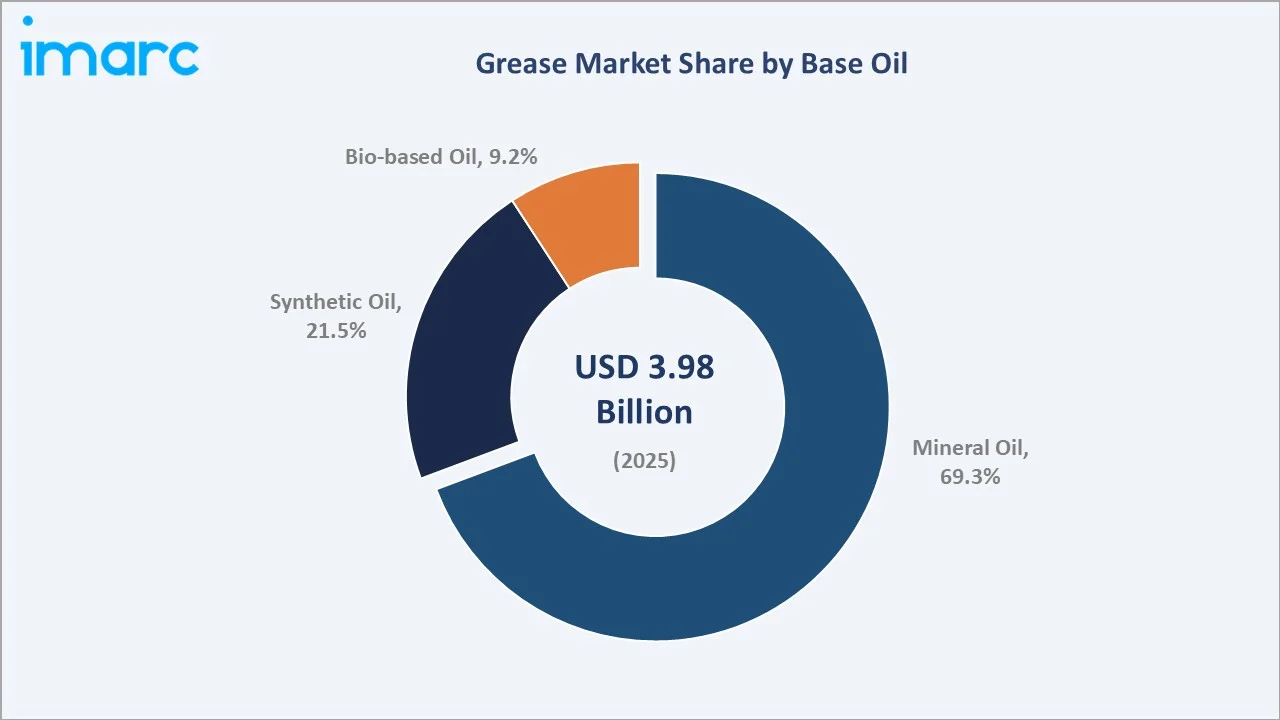

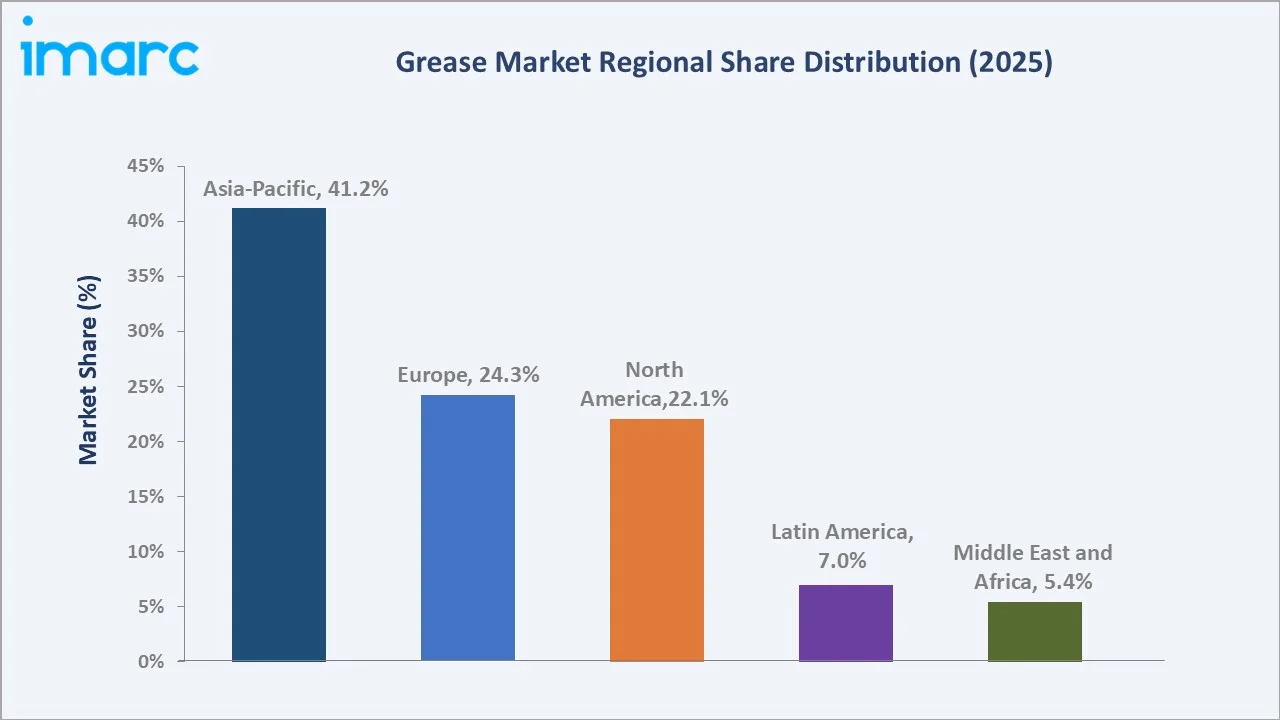

Asia-Pacific leads regionally with a 41.2% market share in 2025, driven by the region’s massive automotive manufacturing base, rapid industrialization across China, India, and Southeast Asia, and the extensive use of grease across construction, steel, and mining sectors that collectively sustain the highest regional grease consumption volume. Mineral oil commands the dominant 69.3% base oil share, reflecting the established cost-effectiveness and performance adequacy of petroleum-derived base oils across the majority of industrial grease applications.

To get more information on this market, Request Sample

The grease market is sustained by three structural demand forces: the indispensable role of grease in reducing friction and preventing corrosion across all mechanical systems in automotive, industrial, and infrastructure applications; the ongoing expansion of Asia-Pacific manufacturing and construction activity, creating new grease consumption volume; and the progressive premiumization of grease formulations toward synthetic and bio-based products that increases per-unit market value even as volume growth remains moderate.

Executive Summary

The global grease market is experiencing steady growth, driven by the convergence of sustained automotive and industrial demand, ongoing infrastructure and construction activity across emerging economies, and the progressive shift toward high-performance synthetic and environmentally compliant bio-based grease formulations. The market was valued at USD 3.98 Billion in 2025 and is forecast to reach USD 5.12 Billion by 2034, growing at a CAGR of 2.71%.

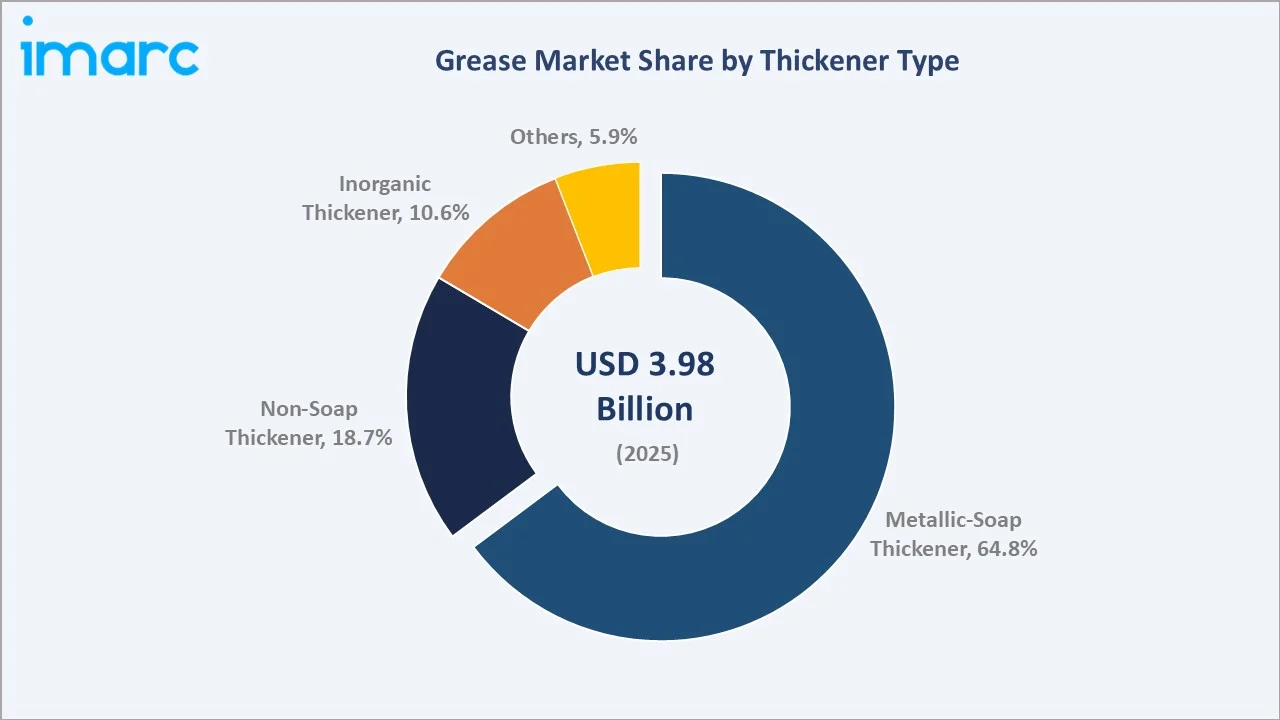

Mineral oil accounts for 69.3% of the base oil segment in 2025, reflecting its cost competitiveness and performance adequacy across the majority of standard temperature and load-bearing grease applications in automotive, construction, and general manufacturing. Metallic-soap thickener dominates the thickener type segment at 64.8%, with lithium and lithium complex soaps collectively representing the majority of this category due to their superior multipurpose performance across automotive and industrial applications.

Asia-Pacific leads regionally at 41.2%, anchored by China’s dominance in both automotive production and heavy industrial machinery, complemented by India’s rapidly expanding automotive and construction sectors. Key players collectively lead the competitive landscape through integrated formulation capability, global OEM approval portfolios, and extensive distribution networks spanning all major industrial markets.

Key Market Insights

|

Insight |

Data |

|

Largest Base Oil |

Mineral Oil – 69.3% share (2025) |

|

Fastest Growing Base Oil |

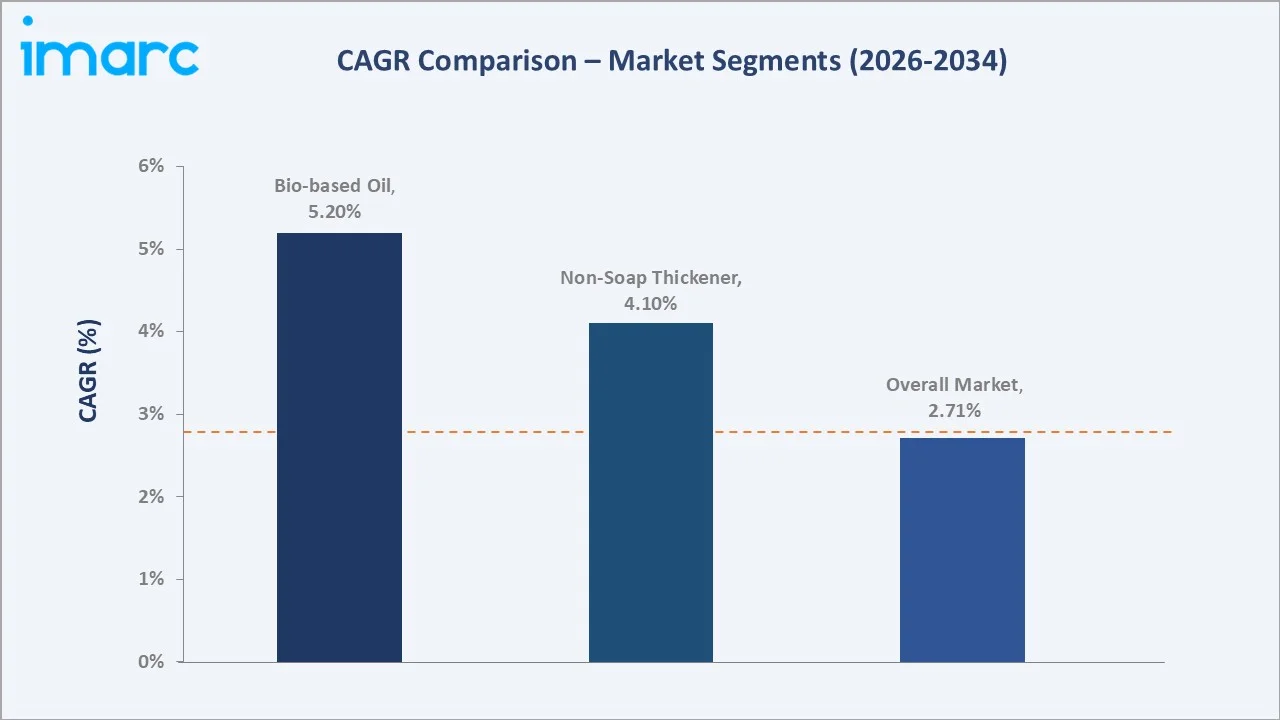

Bio-based Oil – ~5.2% CAGR (2026-2034) |

|

Largest Thickener Type |

Metallic-Soap Thickener – 64.8% share (2025) |

|

Fastest Growing Thickener Type |

Non-Soap Thickener – ~4.1% CAGR (2026-2034) |

|

Leading Region |

Asia-Pacific – 41.2% share (2025) |

|

Top Companies |

Shell plc, Exxon Mobil Corporation, Chevron Corporation, FUCHS SE |

Key Analytical Observations Supporting the Above Data:

- Mineral oil at 69.3% (2025) dominates the base oil segment as petroleum-derived mineral base oils deliver the required viscosity range, oxidation stability, and additives compatibility across the majority of standard grease applications at significantly lower cost than synthetic alternatives. The widespread availability of mineral oil through the established petroleum supply chain further reinforces its dominance across price-sensitive industrial applications.

- Metallic-soap thickener at 64.8% (2025) leads as lithium and lithium complex soaps are the most versatile thickener types, providing broad temperature range performance, high mechanical stability, and water resistance that makes them suitable across automotive wheel bearings, industrial bearings, and chassis lubrication applications from a single multipurpose product.

- Synthetic oil at 21.5% (2025) is driven by the OEM specification trend toward longer service intervals, higher operating temperatures, and extended equipment life requirements that standard mineral oil greases cannot meet. Polyurea, PAO, and ester synthetic greases command 30–60% price premiums over mineral equivalents, supporting market value growth independent of volume increases.

- Asia-Pacific’s 41.2% share (2025) reflects China’s position as the world’s largest automotive producer and the region’s dominance in steel production, construction equipment manufacturing, and mining operations, all of which sustain high-volume grease consumption across bearing, gear, and chassis lubrication applications.

Grease Market Overview

Grease is a semi-solid lubricant consisting of a base oil (mineral, synthetic, or bio-based), a thickener (metallic-soap, non-soap, or inorganic compound), and performance-enhancing additives including anti-wear agents, extreme pressure additives, corrosion inhibitors, and antioxidants. Unlike liquid lubricants, the semi-solid consistency of grease enables it to remain in place at the application point without a circulation system, making it the preferred lubricant form for sealed-for-life bearings, chassis components, open gears, wire ropes, and applications subject to shock loading, oscillating motion, or intermittent operation where oil lubrication is impractical.

Macroeconomic drivers include global car production growing by 4.2% to 78.7 million in 2025 as per ACEA, construction equipment fleet growth in Asia and Africa, and India’s Index of Industrial Production (IIP), which rose 3.5% year-on-year in July 2025, driven by a 5.4% year-on-year increase in manufacturing output. Moreover, the steel, mining, and energy sectors are collectively sustaining above-GDP growth rates in Asia-Pacific, which directly translates to proportional grease demand growth in the region.

Market Dynamics

To evaluate market opportunities, Request Sample

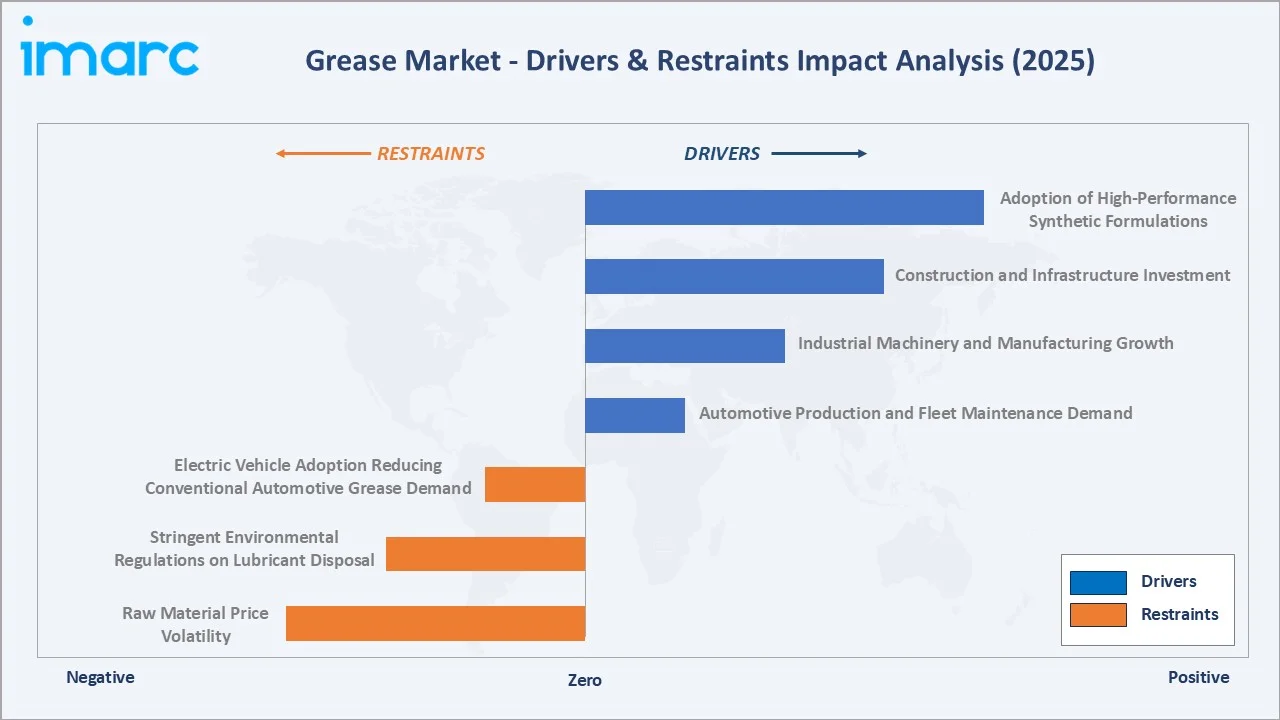

Market Drivers

- Automotive Production and Fleet Maintenance Demand: Grease is an essential consumable in every automotive powertrain, chassis, and body system, used in wheel bearings, CV joints, steering components, door hinges, and gear systems. Global car production grew by 4.2% to reach 78.7 million in 2025, adding to the large global in-service vehicle fleet requiring regular grease replacement in maintenance cycles, which represents the largest single demand foundation for the grease market.

- Industrial Machinery and Manufacturing Growth: Rolling element bearings, electric motor bearings, and conveyor systems across industrial manufacturing all rely on grease as the primary lubricant across industrial manufacturing, power generation, and processing facilities. The ongoing growth of global manufacturing output, particularly in Asia-Pacific’s expanding industrial sector, is directly driving grease consumption volume growth in the machinery lubrication segment.

- Construction and Infrastructure Investment: Construction equipment, including excavators, cranes, concrete pumps, and tunnelling machinery, requires intensive grease lubrication of undercarriage components, slewing rings, and hydraulic cylinder rods. According to McKinsey & Company, global private infrastructure investment rose from USD 95 billion in 2023 to USD 126 billion in 2024, before accelerating to a record nearly USD 200 billion in 2025, which is a significant structural driver of construction equipment grease demand.

- Adoption of High-Performance Synthetic Formulations: The OEM specification trend toward longer service intervals, extended equipment warranty periods, and higher operating temperature requirements is driving progressive adoption of synthetic and semi-synthetic grease formulations that command significant price premiums over mineral oil equivalents. This premiumization trend supports market value growth at a moderate volume CAGR.

Market Restraints

- Raw Material Price Volatility: Grease formulation costs are sensitive to base oil price volatility, which in turn reflects crude oil market dynamics, and to metallic soap commodity price fluctuations. Lithium hydroxide in particular has experienced significant price volatility driven by battery-grade lithium demand competition from the EV sector, creating cost pressure for lithium soap grease manufacturers.

- Stringent Environmental Regulations on Lubricant Disposal: Spent grease disposal is subject to increasing environmental regulations across Europe and North America, with hazardous waste classification and disposal cost creating lifecycle cost pressure for industrial grease users. These regulations are accelerating the adoption of longer-lasting and re-refinable synthetic greases, adding complexity and lifecycle cost to conventional mineral grease applications.

- Electric Vehicle Adoption Reducing Conventional Automotive Grease Demand: EV powertrains eliminate the conventional automotive drivetrain components that represent major grease application points in ICE vehicles. As EV penetration increases through 2034, the conventional automotive grease demand segment faces structural volume reduction that partially offsets growth from industrial and emerging market demand.

Market Opportunities

- Bio-Based and Biodegradable Grease Development: Regulatory pressure and corporate sustainability commitments are driving investment in bio-based grease formulations using vegetable oil base stocks and environmentally acceptable thickeners. The bio-based grease segment holds a 9.2% share in 2025 and is the fastest-growing base oil category. EU biocide regulation and US EPA vessel general permit requirements are creating specific demand in marine, food processing, and environmentally sensitive applications.

- EV-Specific High-Performance Grease Applications: While EVs reduce some conventional grease application points, they create new specialized grease demand for electric motor bearings, battery cooling system components, e-axle gear systems, and high-speed motor spindle bearings that require low-noise, high-speed, thermally stable synthetic greases.

Market Challenges

- Lithium Supply Chain Competition from Battery Sector: The EV battery sector’s rapidly growing demand for battery-grade lithium carbonate and lithium hydroxide is creating direct competition with the grease industry’s lithium hydroxide supply requirements for metallic soap thickener production. Structural tightening of lithium supply availability and price increases for lithium hydroxide are incentivizing grease formulators to develop alternative thickener systems.

- Technical Complexity of Bio-Based Formulation Performance Matching: Bio-based greases using vegetable oil base stocks face performance challenges, including lower thermal stability, higher pour points, and inferior oxidation resistance compared to mineral and synthetic alternatives in demanding operating conditions. Closing these performance gaps challenges the limits of bio-based adoption in high-temperature and heavy-duty industrial applications.

Emerging Market Trends

1. Lithium Alternative Thickener Development

Calcium sulphonate complex, aluminum complex, and polyurea thickeners are gaining traction as lithium-free alternatives offering competitive performance in key application segments. In April 2024, FUCHS Lubricants South Africa introduced RENOLIT CSX ULTRA, a calcium sulphonate complex grease for mining equipment. It offers high-temperature stability, water resistance, rust protection, and extreme-pressure wear protection for heavy-duty mining applications.

2. EV-Grade Synthetic Grease Specification Development

The transition to electric vehicles is driving specification development for a new category of high-performance synthetic greases suited to EV-specific operating conditions, higher motor shaft speeds, lower noise requirements, wider operating temperature ranges, and electrical insulation requirements for motor bearing greases. Leading OEMs, including Toyota, BMW, and Volkswagen, are developing EV-specific grease specifications that are creating premium product categories for synthetic grease formulators with the technical capability to meet these new requirements.

3. Automated Lubrication System Integration

The growing deployment of automatic lubrication systems (ALS) in industrial machinery, construction equipment, and wind turbines is changing grease application patterns from manual re-greasing to continuous micro-dosing through centralized distribution systems. ALS compatibility requirements, including specific grease pumpability, thixotropic recovery, and consistency grade characteristics, are influencing grease product development and creating a preference for formulations with validated ALS compatibility from major system manufacturers.

4. Sustainable and Circular Lubricant Programs

In May 2026, HPCL and Tata Motors signed an MoU to pilot a scalable circular economy model for the responsible collection and recycling of used automotive lubricants. The initiative will channel used lubricants to registered recyclers and convert them into high-quality re-refined base oil. These circular economy initiatives are driven by both regulatory requirements and corporate sustainability targets, and are creating new business model opportunities around grease lifecycle management services.

Industry Value Chain Analysis

The grease value chain spans from raw material supply through formulation, manufacturing, packaging, distribution, and end-use application across automotive, industrial, and infrastructure sectors. The formulation manufacturing tier is dominated by integrated oil majors and specialty lubricant manufacturers, while the distribution tier operates through both direct OEM channels for premium synthetic greases and independent industrial distributor networks for standard mineral oil formulations.

|

Stage |

Key Players / Examples |

|

Raw Material Suppliers |

Base oil refiners, metallic soap producers, synthetic oil manufacturers, thickener suppliers, and performance additive developers |

|

Grease Manufacturers |

Integrated oil majors, specialty lubricant manufacturers, and independent grease formulators |

|

Packaging & Labelling |

Drum and cartridge manufacturers, industrial packaging suppliers, and private-label packaging service providers |

|

Distributors & Wholesalers |

Industrial lubricant distributors, OEM-approved channel partners, MRO distributors, and specialty lubrication retailers |

|

End-Use Industries |

Automotive manufacturers, construction equipment OEMs, steel mills, mining operators, and general manufacturing facilities |

|

After-Sales & Service Providers |

Lubrication analysis laboratories, condition monitoring service providers, and MRO maintenance contractors |

Technology Landscape in the Grease Industry

Metallic Soap Thickener Technology

Metallic soap thickeners, produced by the saponification of fatty acids with metal hydroxides, remain the dominant grease thickener technology at 64.8% market share. Lithium and lithium complex soaps provide superior multipurpose performance across a −30°C to +150°C service temperature range, combining water resistance, mechanical stability, and compatibility with most additive packages. Calcium sulphonate complex soaps are gaining share as a lithium alternative, offering natural extreme pressure performance, excellent water resistance, and compatibility with both mineral and synthetic base oils.

Synthetic and Non-Soap Thickener Systems

Polyurea thickeners, produced by the reaction of diisocyanates with amines, deliver exceptional high-temperature performance and are the preferred thickener for electric motor bearing greases due to their superior oxidation stability and long re-lubrication intervals. Organobentonite and fumed silica inorganic thickeners are used in specialty high-temperature and solvent-resistant applications. The non-soap thickener category is the fastest growing within the thickener type segment, driven by automotive OEM adoption of polyurea greases for sealed-for-life motor bearings.

Bio-Based Formulation Technology

Bio-based greases using renewable base stocks, including sunflower, rapeseed, and synthetic ester oils derived from vegetable feedstocks, are the focus of significant formulation investment. Additive technology advances, including antioxidant systems optimized for vegetable oil oxidation mechanisms, biostabilizers to prevent microbial degradation, and pour point depressants to address bio-based oil cold flow limitations, are progressively closing the performance gap between bio-based and mineral oil greases across a wider range of application temperatures and conditions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Base Oil |

Mineral Oil |

69.3% |

2025 |

|

Thickener Type |

Metallic-Soap Thickener |

64.8% |

2025 |

|

End User |

Automotive |

🔒 |

2025 |

|

Region |

Asia-Pacific |

41.2% |

2025 |

By Base Oil

Mineral oil leads with a 69.3% share of the global grease market in 2025. Petroleum-derived mineral base oils provide the viscosity range, film strength, and additive compatibility required for standard-duty automotive and industrial grease applications at a cost competitive with no alternative base oil type. The extensive global refinery infrastructure for mineral-based oil production ensures a reliable supply and stable pricing relative to synthetic alternatives, reinforcing mineral oil’s dominant position in volume-driven commodity grease markets.

To access detailed market analysis, Request Sample

Synthetic oil represents 21.5% of the market in 2025, driven by OEM extended-drain specifications, high-temperature industrial applications, and the growing EV-grade grease requirement. Bio-based oil at 9.2% is the fastest-growing segment, driven by regulatory requirements in environmentally sensitive applications and corporate sustainability commitments from major manufacturers and fleet operators.

By Thickener Type

Metallic-soap thickener dominates with a 64.8% share in 2025. Within this category, lithium and lithium complex soaps collectively account for the majority of volume, reflecting their universal adoption across automotive wheel bearing grease, industrial rolling bearing grease, and multipurpose chassis grease applications.

Non-soap thickener at 18.7% is the fastest-growing thickener category, driven primarily by polyurea grease adoption in electric motor bearings and high-speed bearing applications requiring extended re-lubrication intervals and high-temperature stability. Inorganic thickener at 10.6% serves specialized high-temperature, solvent-resistant, and clean-room applications.

Regional Market Insights

Asia-Pacific’s dominant position (41.2%, 2025) reflects the region’s unparalleled scale in automotive production, heavy industry, and infrastructure construction. China alone accounts for the majority of the Asia-Pacific grease market, driven by its position as the world’s largest vehicle producer, largest steel producer, and the dominant global construction equipment market, both in domestic use and export manufacturing.

Europe, at 24.3%, is characterized by premium synthetic grease demand from the automotive and industrial sectors, high regulatory pressure for biodegradable formulations, and a mature market with strong replacement demand cycle characteristics.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

41.2% |

Rapid industrialization, a large automotive manufacturing base, expanding construction and infrastructure activity, and growing steel and mining sectors across China, India, and Southeast Asia |

|

Europe |

24.3% |

Mature automotive and industrial manufacturing sector, stringent lubrication standards, high demand for premium synthetic greases, and strong regulatory push for bio-based and biodegradable formulations |

|

North America |

22.1% |

Large automotive fleet, established heavy manufacturing and mining sectors, high adoption of high-performance synthetic greases, and strong MRO lubrication market across industrial facilities |

|

Latin America |

7.0% |

Growing automotive production, expanding construction and mining activity, increasing industrialization, and rising adoption of quality lubricants in Brazil and Mexico |

|

Middle East and Africa |

5.4% |

Oil and gas sector maintenance and machinery lubrication demand, expanding construction activity, growing automotive market, and increasing industrial capacity investment |

North America accounts for 22.1% (2025), driven by a large automotive fleet, heavy manufacturing, and mining sectors with high penetration of synthetic and semi-synthetic premium greases. Latin America at 7.0% and the Middle East and Africa at 5.4% represent smaller but growing markets, with automotive, mining, and oil and gas sector maintenance demand as the primary growth drivers in their respective regions.

Competitive Landscape

The global grease market exhibits moderate-to-high concentration among the integrated oil majors and high-volume lubricant manufacturers, with the top players collectively accounting for approximately 45–55% of global market revenues in 2025.

|

Company Name |

Brands/Products |

Market Position |

Core Strength |

|

Shell plc |

Shell Gadus |

Market Leader |

Broadest global grease portfolio, strong automotive and industrial brand recognition, and extensive distribution network |

|

Exxon Mobil Corporation |

Mobil SHC Aware Grease Series, Mobilith SHC Series, Mobilgrease XHP series, among others |

Market Leader |

Premium performance formulations, global OEM approvals, and a strong synthetic grease portfolio for extreme conditions |

|

Chevron Corporation |

Delo Grease |

Strong Challenger |

Competitive mineral and synthetic portfolio, strong North American presence, and well-established MRO channel relationships |

|

FUCHS SE |

Renolit, Urethyn, Stabyl, Cassida |

Challenger |

Specialty and high-performance grease expertise, strong European industrial sector relationships, and a growing bio-based formulation portfolio |

The integrated oil majors compete primarily on product breadth, global availability, OEM approval portfolios, and brand trust built through decades of automotive and industrial channel presence. Specialty manufacturers compete on formulation expertise, custom solution capability, and technical service depth in demanding applications requiring non-standard grease specifications.

Key Company Profiles

Shell plc

Shell plc is one of the world’s leading lubricant suppliers and one of the top two grease market leaders globally. Its Shell Gadus grease series spans automotive, industrial, construction, and specialty applications, covering mineral, synthetic, and bio-based formulations across a global manufacturing and distribution network.

- Product Portfolio: Shell Gadus S1, S2, S3, S5 series covering multipurpose, high-temperature, heavy-duty, and specialty grease applications; Shell Gadus Bio series for environmentally acceptable applications.

- Recent Developments: In March 2024, Shell plc announced plans to build its first grease manufacturing plant in Indonesia at the Marunda Lubricants Oil Blending Plant complex in Bekasi. The facility will produce up to 12 kilotons of Shell Gadus grease annually for industries such as manufacturing, steel, construction, fleet, and mining.

- Strategic Focus: Sustainable and circular lubricant portfolio expansion; EV-grade grease specification development for automotive OEM channels; digital lubrication management service platform deployment across industrial customer base.

Exxon Mobil Corporation

Exxon Mobil Corporation is one of the world's leading global integrated energy companies and one of the world’s largest lubricant producers. Its Mobilgrease grease series is widely recognized for premium synthetic performance across automotive OEM, industrial, and specialty applications.

- Product Portfolio: Mobil SHC Aware Grease Series. Mobilith SHC Series, Mobilgrease XHP, Mobilgrease XHP 460 Series, and Mobilgrease XHP Mine Series, among others.

- Strategic Focus: Premium synthetic grease market leadership; EV-specific formulation development; expansion of Mobil SHC synthetic lubricant portfolio into high-value industrial bearing applications.

FUCHS SE

FUCHS SE is one of the world’s largest independent lubricant manufacturers and one of the leading specialty grease producers globally. The company differentiates through its formulation expertise in specialty and high-performance grease applications, with a particularly strong position in European automotive OEM channels and industrial specialty lubrication markets.

- Product Portfolio: Renolit, Urethyn, Stabyl, and Cassida (food-grade) grease series.

- Recent Developments: In May 2024, FUCHS China inaugurated its high-performance grease plant in Yingkou to strengthen grease production for China and the Asia-Pacific market. The plant features advanced automation, strict quality control, and supports applications such as new energy vehicles, wind power, semiconductors, aerospace, and robotics.

- Strategic Focus: Specialty and high-performance grease market differentiation; bio-based and re-refined lubricant portfolio expansion; digital lubrication service offering development through FUCHS’ LUBRICATION EXCELLENCE program.

Market Concentration Analysis

The global grease market exhibits moderate-to-high concentration at the premium and mainstream segments, with the integrated oil majors holding the largest individual market revenue shares through their global distribution infrastructure and broad OEM approval portfolios. The specialty segment is served by a more fragmented competitive landscape, which competes on formulation expertise and technical service in high-value niche applications.

Regional concentration patterns reflect the underlying industrial structure of each geography. Asia-Pacific’s market is more fragmented than Western markets, with regional Asian manufacturers holding significant domestic shares alongside global majors. Europe’s market includes strong positions for regional specialists in industrial specialty segments where formulation expertise and technical service depth matter more than brand scale and distribution breadth.

Investment & Growth Opportunities

Fastest Growing Segments

Bio-based grease (~5.2% CAGR), non-soap thickener (~4.1% CAGR), and EV-grade high-speed motor bearing greases represent the highest-growth investment vectors within the grease market through 2034. Specialty segments, including food-grade, extreme-pressure mining, and wind turbine main bearing greases, offer premium pricing opportunities above market CAGR due to stringent specification requirements limiting competitive pressure.

Emerging Market Expansion

India, Vietnam, Indonesia, and sub-Saharan Africa represent significant greenfield growth opportunities as automotive production, construction, and industrial capacity expand at above-average rates. Local grease manufacturing investment in these markets to avoid import tariffs and logistics costs, combined with technical service capability development to support industrial customers, is the primary market entry strategy for global grease manufacturers targeting these high-growth geographies.

Technology Investment Trends

- Lithium alternative thickener development is attracting significant R&D investment from all major grease manufacturers, with calcium sulphonate complex and polyurea formulations receiving the largest development resources as the most commercially viable lithium alternatives across the widest range of application conditions.

- Bio-based base oil formulation technology investment is growing, driven by regulatory requirements and sustainability commitments, with bio-lubricant specialists and major oil companies investing in vegetable-oil-derived synthetic ester base stocks that overcome the thermal and oxidative limitations of conventional vegetable oils.

- Digital lubrication management platforms combining automated lubrication system integration, grease condition monitoring, and IoT-enabled re-lubrication scheduling are attracting investment from both grease manufacturers seeking service revenue expansion and industrial automation companies seeking to integrate lubrication into predictive maintenance programs.

Future Market Outlook (2026-2034)

The global grease market is positioned for moderate, sustained growth through 2034. From USD 3.98 Billion in 2025, the market is projected to reach USD 5.12 Billion by 2034, representing total incremental value creation of USD 1.14 Billion at a CAGR of 2.71%. This growth is structurally supported by the continued indispensability of grease across automotive, industrial, and infrastructure applications, partially moderated by the structural headwind of EV powertrain adoption, reducing conventional automotive grease application points.

The market’s compositional evolution will be significant even as overall CAGR remains moderate. Synthetic and bio-based formulations will grow their combined share from approximately 30.7% in 2025 toward 40% by 2034, as OEM specification evolution, environmental regulation, and sustainability commitments progressively shift product mix toward higher-value premium formulations. The thickener type distribution will evolve similarly, with non-soap and inorganic thickeners gaining share from metallic soaps as EV-grade polyurea and calcium sulphonate complex greases grow their automotive and industrial penetration.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 65 industry participants in 2024–2025, including grease manufacturers, base oil and additive suppliers, automotive OEM lubrication engineers, industrial equipment MRO managers, and lubricant distributors across Asia-Pacific, Europe, and North America. Expert input validated market sizing, segment growth rates, and regional penetration estimates.

Secondary Research

Secondary research encompassed lubricant company annual reports and investor presentations, NLGI (National Lubricating Grease Institute) grease consumption statistics, ATIEL European lubricant production data, automotive production statistics from OICA, IEA industrial energy and manufacturing output data, and industry publications including Lubes’n’Greases, Tribology Transactions, and F+L Asia.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating global grease consumption volume data by end-use sector, price trend analysis by base oil and thickener type, and market value modelling based on regional product mix evolution. The base-case CAGR of 2.71% reflects consensus estimates validated against lubricant company revenue guidance and automotive production and industrial output projections for 2026–2034.

Grease Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Thickener Types Covered | Metallic-Soap Thickener, Non-Soap Thickener, Inorganic Thickener, Others |

| Base Oils Covered | Mineral Oil, Synthetic Oil, Bio-based Oil |

| End Users Covered | Automotive, Construction and Off-Highways, General Manufacturing, Steel, Mining, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered |

Shell plc, Exxon Mobil Corporation, Chevron Corporation, FUCHS SE, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the grease market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global grease market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the grease industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Grease Market Report

The global grease market reached USD 3.98 Billion in 2025 and is projected to reach USD 5.12 Billion by 2034.

The market is expected to grow at a CAGR of 2.71% during 2026-2034, driven by automotive fleet maintenance, industrial machinery, and construction sector expansion, and progressive adoption of premium synthetic and bio-based formulations.

Asia-Pacific leads with a 41.2% share in 2025, driven by the region’s dominance in automotive production, heavy industrial machinery, steel production, construction activity, and mining operations across China, India, and Southeast Asia.

Mineral oil dominates with a 69.3% share in 2025, reflecting its cost competitiveness and performance adequacy across the majority of standard automotive and industrial grease applications served by conventional mineral base oil formulations.

Metallic-soap thickener leads with a 64.8% share in 2025, with lithium and lithium complex soaps accounting for the majority, reflecting their multipurpose performance across automotive, industrial, and construction equipment grease applications.

Some of the key players include Shell plc, Exxon Mobil Corporation, Chevron Corporation, and FUCHS SE.

Some of the key drivers include global automotive production and fleet maintenance demand, industrial machinery and manufacturing growth, construction and infrastructure investment, and the premiumization trend toward synthetic and bio-based formulations commanding higher unit values.

Some of the key opportunities include bio-based and biodegradable grease formulation development, EV-grade synthetic grease specifications for motor bearing applications, and digital lubrication management service platforms combining automated re-lubrication systems with condition monitoring analytics.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)