Green Coffee Market Size, Share, Trends and Forecast by Type, Product, Distribution Channel, End User, and Region, 2026-2034

Global Green Coffee Market Size, Share, Trends & Forecast (2026-2034)

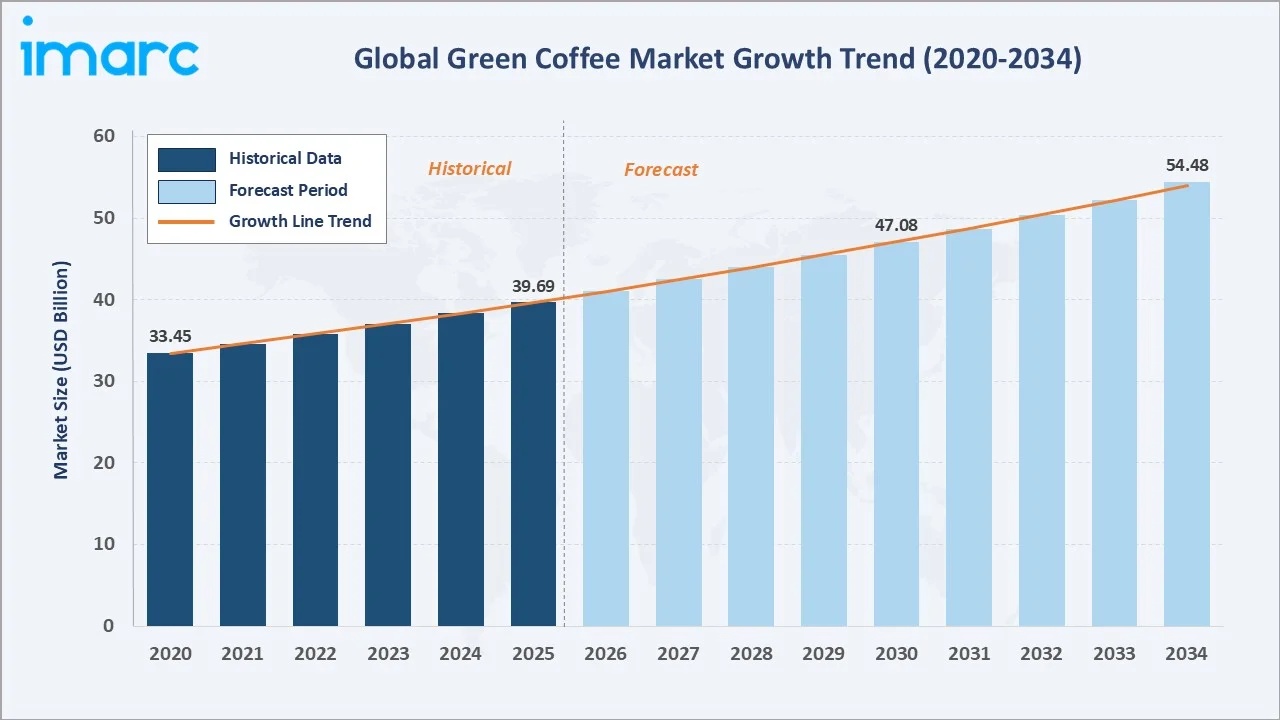

The global green coffee market size reached USD 39.69 Billion in 2025 and is projected to reach USD 54.48 Billion by 2034, exhibiting a CAGR of 3.48% during 2026-2034. Rising global coffee consumption, rapid e-commerce expansion, and growing specialty and sustainable coffee preferences are the primary forces driving green coffee market growth.

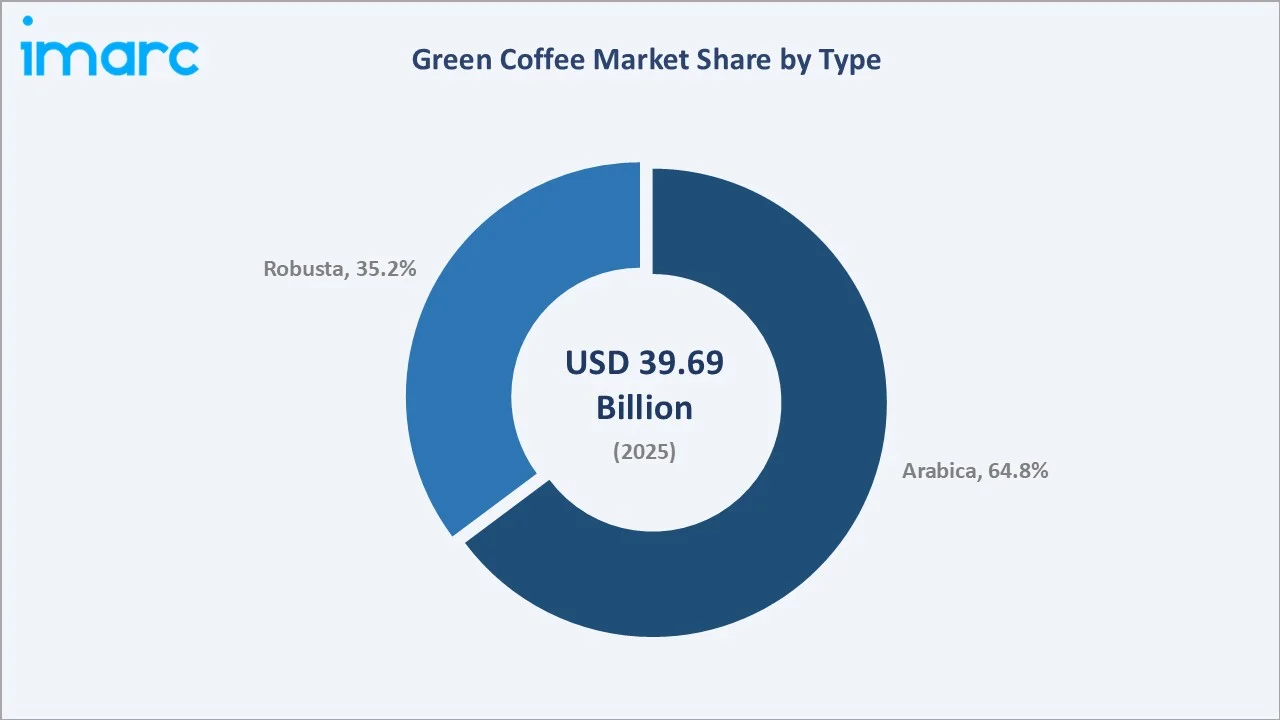

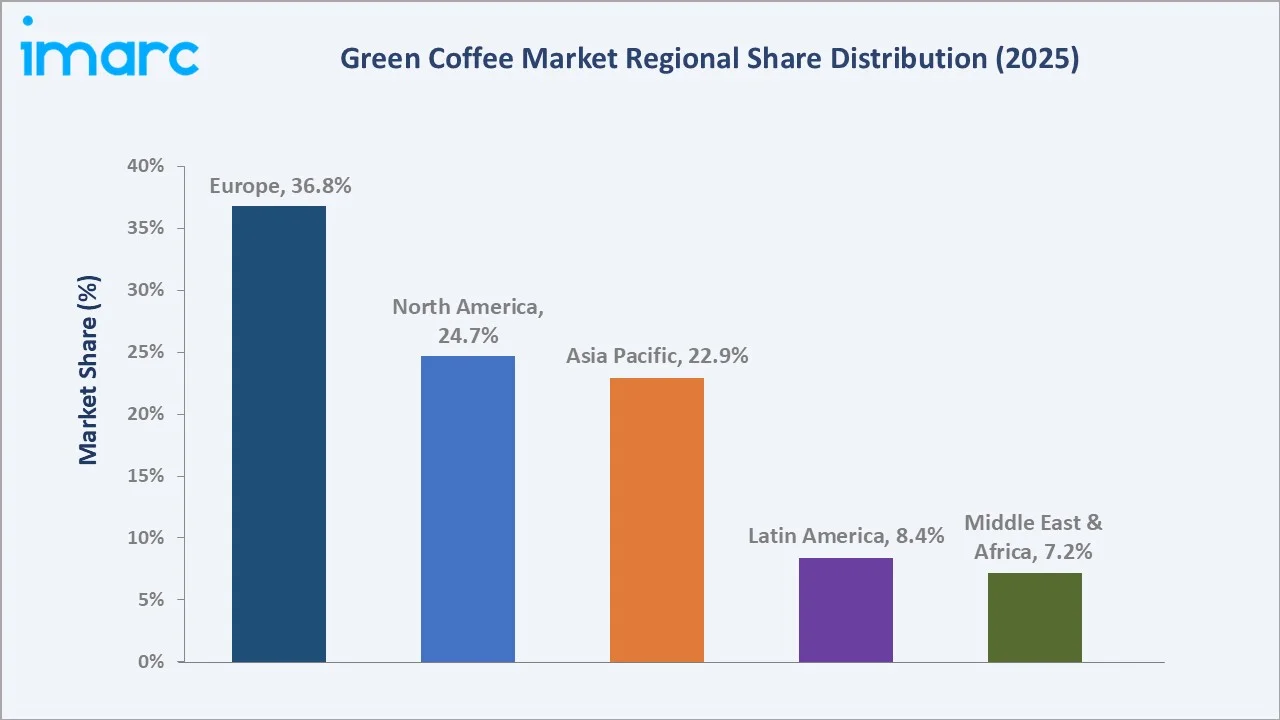

Arabica coffee dominates the type mix at 64.8% in 2025, reflecting its premium flavor profile and broad consumer preference. Roasted coffee leads product segmentation at 46.3% in 2025. Europe commands the largest regional share at 36.8%, underpinned by mature coffee culture, high per-capita consumption, and robust specialty retail infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 39.69 Billion |

|

Forecast Market Size (2034) |

USD 54.48 Billion |

|

CAGR (2026-2034) |

3.48% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (36.8% share, 2025) |

|

Second Largest Region |

North America (24.7% share, 2025) |

|

Leading Type |

Arabica (64.8%, 2025) |

|

Leading Product |

Roasted Coffee (46.3%, 2025) |

The global green coffee market trajectory from 2020 through 2034, with historical expansion to USD 39.69 Billion in 2025, reflects consistent consumer demand growth. The forecast to USD 54.48 Billion captures accelerating specialty coffee adoption, e-commerce channel expansion, and growing health supplement applications for green coffee extracts globally.

To get more information on this market, Request Sample

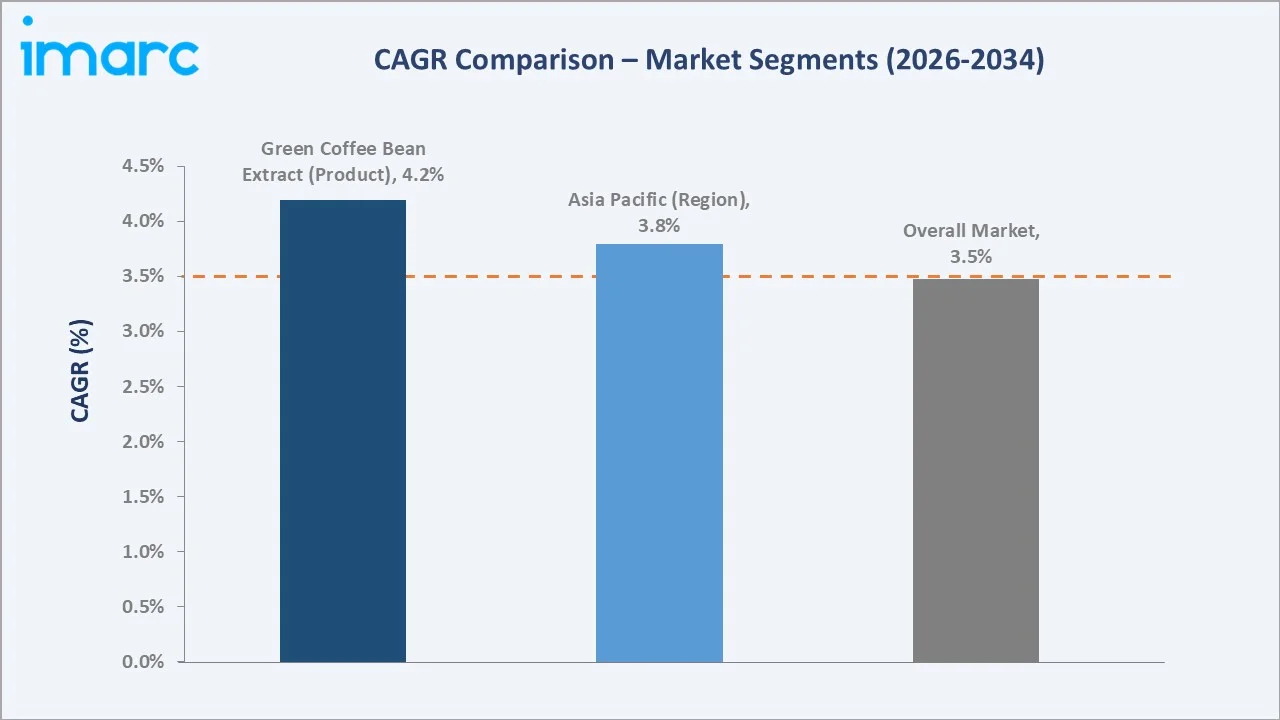

The CAGR trajectories across key type, product, and regional sub-segments, with green coffee bean extract at ~4.2% CAGR and Asia Pacific at ~3.8% CAGR, represent the fastest-growing categories within the global green coffee industry analysis through 2034.

Executive Summary

The global green coffee market is on a sustained growth trajectory from USD 39.69 Billion in 2025 to USD 54.48 Billion by 2034. Green coffee, encompassing unroasted beans, soluble coffee, and botanical extracts, benefits from structural demand driven by global coffee culture expansion and health-conscious consumer behavior.

Arabica coffee beans dominate type at 64.8% in 2025, owing to their premium flavor profile and dominant position across specialty, retail, and gourmet channels globally. Robusta (35.2%) remains critical for espresso blends, mass-market instant coffee, and cost-sensitive commercial applications requiring higher caffeine content and robust flavor intensity.

Roasted coffee leads product at 46.3% in 2025, reflecting broad retail and foodservice applicability. Instant/soluble coffee (34.7%) drives convenience demand in emerging markets. Green coffee bean extract (19.0%) is the fastest-growing product segment at ~4.2% CAGR, driven by nutraceutical and functional food market expansion.

Europe dominates at 36.8% in 2025, supported by highest per-capita coffee consumption, developed specialty retail infrastructure, and strong sustainability certification demand. North America (24.7%) and Asia Pacific (22.9%) are the primary growth engines, with Asia Pacific growing fastest in absolute value terms.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Arabica – 64.8% share (2025) |

|

Second Type |

Robusta – 35.2% share (2025) |

|

Leading Product |

Roasted Coffee – 46.3% share (2025) |

|

Leading Region |

Europe – 36.8% share (2025) |

|

Second Largest Region |

North America – 24.7% share (2025) |

|

Top Companies |

Neumann Gruppe GmbH, Belco, wscafe company limited |

Key Analytical Observations Expanding on the Above Data:

- Arabica, with 64.8% in 2025, dominates because of its superior flavor complexity and premium market positioning. Specialty roasters and artisanal cafes source Arabica as the primary input, commanding price premiums of 30-50% over Robusta varieties in wholesale green coffee markets globally.

- Roasted coffee, with 46.3% in 2025, leads product categories as it represents the most direct value conversion of green beans. Mass-market retail, foodservice, and specialty roasters collectively generate consistent, large-scale green coffee procurement demand across all major consuming regions.

- Europe’s 36.8% dominance in 2025 reflects the highest per-capita coffee consumption globally, deeply embedded specialty coffee culture across Germany, Italy, France, and Scandinavia, and robust retail infrastructure supporting premium product positioning with consistent high-volume procurement.

- North America, with 24.7% in 2025, benefits from expanding specialty coffee culture, direct-trade sourcing trends, and growing subscription-based home roasting markets, generating incremental green coffee demand beyond traditional commercial roaster supply channels.

Global Green Coffee Market Overview

Green coffee refers to raw, unroasted coffee beans sourced from Coffea arabica and Coffea canephora (Robusta) plants. The product spectrum spans whole green beans traded through commodity and specialty markets, soluble and instant coffee intermediates, and botanical extracts for health supplements and functional beverages.

The global ecosystem integrates coffee farmers and cooperatives, green coffee exporters, commodity traders and brokers, specialty importers, commercial roasters, retail distributors, foodservice operators, and health supplement manufacturers across 70+ coffee-producing countries and major consuming markets worldwide.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

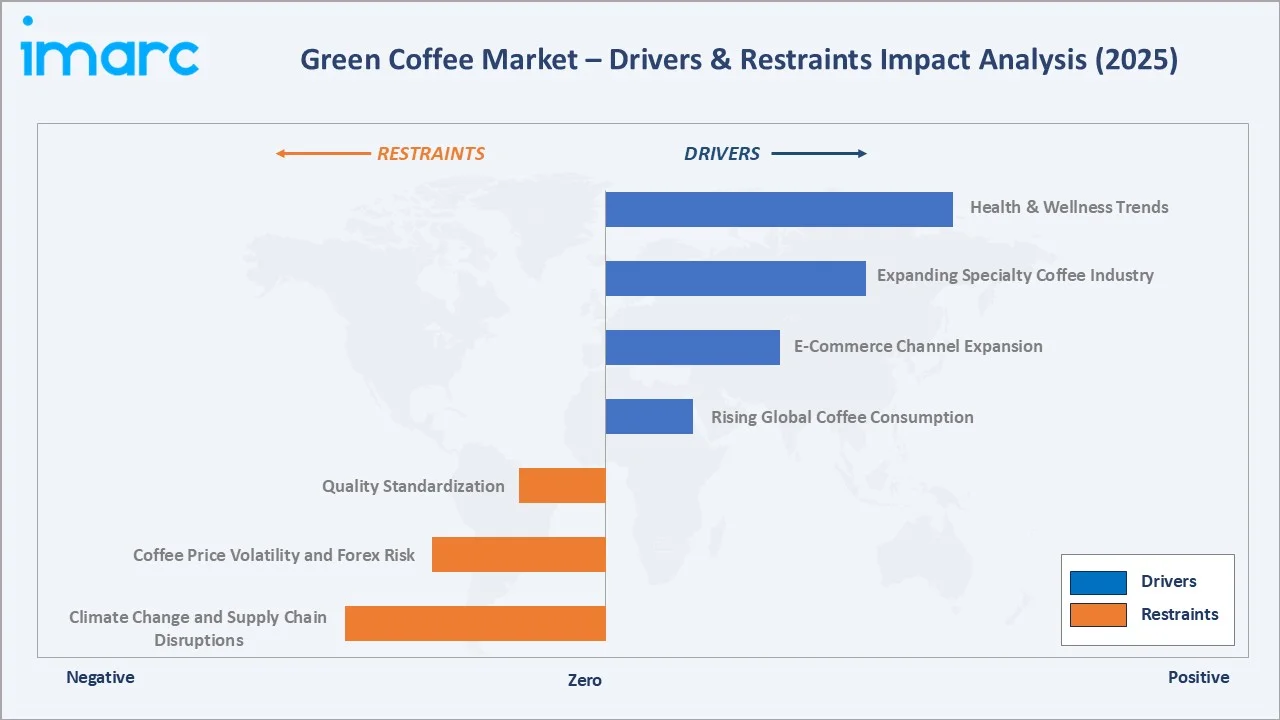

- Rising Global Coffee Consumption: The ICO projects worldwide coffee consumption to increase by over 3.0% in 2023-2024, with total global consumption reaching 177.0 million bags. This consistent demand growth directly translates into sustained green coffee procurement volumes across all product categories and distribution channels.

- E-Commerce Channel Expansion: The rapid expansion of global e-commerce platforms is transforming the way agricultural and specialty products are traded worldwide. Digital marketplaces are enabling direct interaction between producers and buyers, improving pricing transparency, streamlining distribution channels, and widening market reach for premium and specialty coffee varieties, including single-origin and micro-lot offerings.

- Expanding Specialty Coffee Industry: The specialty coffee industry continues to witness strong global growth, supported by evolving consumer preferences toward premium-quality beverages, artisanal roasting, and origin-specific coffee experiences. The increasing popularity of third-wave coffee culture across major markets is encouraging higher demand for high-quality green coffee beans among roasters and retailers in regions such as North America, Europe, and Asia Pacific.

Market Restraints

- Climate Change and Supply Chain Disruptions: Coffee production is highly climate-sensitive, with temperature increases reducing suitable growing areas across Latin America, East Africa, and Southeast Asia. El Niño and La Niña weather cycles create significant annual production volatility, driving supply uncertainty and margin pressure across the green coffee value chain.

- Coffee Price Volatility and Forex Risk: Green coffee commodity prices on the ICE and Euronext exchanges exhibit high volatility driven by harvest projections, currency fluctuations in producing countries, and speculative financial flows.

Market Opportunities

- Ready-to-Drink and Cold Brew Coffee Expansion: The growing popularity of ready-to-drink (RTD) and cold brew coffee products is creating new growth opportunities within the global coffee industry. Changing consumer lifestyles, increasing preference for convenient beverage options, and rising demand for premium café-style experiences are driving innovation across the segment. This trend is encouraging manufacturers to source specialized green coffee varieties tailored for cold extraction and differentiated flavor profiles, thereby expanding procurement requirements beyond conventional roasted coffee applications.

- Health and Wellness Applications of Green Coffee Extract: Growing scientific evidence supporting green coffee bean extract’s chlorogenic acid content as a metabolic health aid is expanding the nutraceutical channel. The global dietary supplements market creates a high-value parallel demand pathway for green coffee beyond traditional beverage applications.

Market Challenges

- Quality Standardization Across Diverse Origins: Specialty coffee market demand for consistent cupping scores, traceability documentation, and certifications (Rainforest Alliance, Fair Trade) creates significant quality management complexity across supply chains spanning dozens of producing countries with highly variable agricultural and processing practices.

- Competition from Alternative Beverages: Tea, energy drinks, plant-based beverages, and functional wellness drinks compete for consumer share-of-stomach in key markets. Younger consumers in North America and Europe are expanding beverage repertoires, requiring continuous coffee industry innovation to maintain consumption frequency and demographic relevance.

Emerging Market Trends

1. Direct Trade and Traceability Transforming Green Coffee Procurement

Direct trade models bypassing commodity brokers and enabling direct financial relationships between roasters and farming cooperatives are accelerating. Digital traceability platforms using blockchain allow end consumers to verify origin, processing method, and farmer compensation, commanding significant retail price premiums and satisfying growing regulatory transparency requirements.

2. Specialty Coffee Subscription Models Expanding Green Bean Demand

Direct-to-consumer subscription platforms for specialty roasted and home-roasting green bean subscriptions are growing at 15-20% annually in North America and Europe. These models generate predictable, recurring green coffee procurement demand outside traditional wholesale channels, improving supply chain planning for origin farmers and specialty exporters.

3. Sustainability Certifications Reshaping Green Coffee Supply Chains

Rainforest Alliance, Fair Trade, and Organic certifications are increasingly mandatory for entry into European supermarket and foodservice buyer programs. The EU Deforestation Regulation (EUDR) effective 2025 requires detailed supply chain documentation for all imported coffee, accelerating investment in traceability technology and sustainable farming practices.

4. Green Coffee Extract Entering Mainstream Health and Wellness Categories

Green coffee bean extract standardized to 45-50% chlorogenic acid content is being incorporated into weight management supplements, metabolic health formulations, and functional beverages. Major supplement brands launching green coffee extract products are creating a high-value parallel demand channel distinct from traditional beverage applications.

Industry Value Chain Analysis

The green coffee value chain spans six stages from cultivation through end-use consumption. Trading and import brokerage capture significant margins through market intelligence and quality selection; while roasting and processing add the highest processing value, and retail and foodservice channels generate consumer-facing premiums.

|

Stage |

Description |

|

Coffee Farming & Production |

Coffee farmers and cooperatives cultivate Arabica and Robusta beans across 70+ producing countries |

|

Green Coffee Export |

Exporters and origin traders prepare, grade, and ship green coffee beans to consuming market importers |

|

Import & Trading |

Importers and brokers manage quality selection, logistics, financing, and risk hedging for buying markets |

|

Roasting & Processing |

Commercial and specialty roasters transform green beans into finished roasted, instant, or extract products |

|

Distribution & Retail |

Supermarkets, specialty retailers, e-commerce platforms, and subscription services reach end consumers |

|

End-Use Consumption |

Home consumers, cafes, foodservice operators, and nutraceutical manufacturers are the final demand sources |

Integrated trading companies combining origin sourcing, quality selection, logistics, and financial hedging capabilities achieve superior supply continuity and quality consistency versus traders relying on spot market procurement, creating meaningful competitive advantages in volume commodity and specialty green coffee segments alike.

Technology Landscape in the Green Coffee Industry

Processing Technology: Wet, Dry, and Honey Processing

Wet (washed) processing, dominant for Arabica coffees, uses water fermentation and washing to remove fruit, producing clean and consistent cup profiles. Dry (natural) processing, traditional in Ethiopia and Brazil, generates complex fruit-forward flavor profiles increasingly prized in specialty markets commanding 20-30% price premiums over washed equivalents.

Quality Assessment: Spectroscopy and AI Grading

Near-infrared (NIR) spectroscopy and hyperspectral imaging enable non-destructive, real-time quality assessment of green coffee moisture content, density, and defect prevalence, reducing reliance on manual cupping and accelerating quality control throughput at origin export stations and importing facilities across major trade hubs.

Supply Chain Technology: Blockchain Traceability

Blockchain platforms including Farmer Connect, bext360, and Origin by Starbucks enable immutable origin-to-cup traceability for specialty green coffee. Farm-level GPS geolocation, harvest date recording, and processing method documentation create verifiable supply chain records satisfying EU Deforestation Regulation compliance requirements for importing companies.

Extraction Technology: Supercritical CO2 and Cold Brew Optimization

Supercritical CO2 extraction for green coffee bean extract production enables selective chlorogenic acid concentration without thermal degradation, producing standardized high-potency extracts for nutraceutical applications. Cold brew process optimization, including nitrogen infusion and high-pressure extraction, creates specialty RTD variants driving premium coffee market growth.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Arabica |

64.8% |

2025 |

|

Product |

Roasted Coffee |

46.3% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Europe |

36.8% |

2025 |

By Type

Arabica coffee commands a 64.8% majority share in 2025 owing to its premium flavor characteristics, broad consumer recognition, and dominant position across specialty and gourmet coffee globally. The smooth taste profile, ranging from sweet and mild to rich and complex depending on origin, makes Arabica the default specification for specialty roasters, premium retail, and upscale foodservice.

To access detailed market analysis, Request Sample

Robusta at 35.2% in 2025 serves critical commercial market functions despite its commodity positioning. Higher caffeine content (1.7-4% vs. Arabica’s 0.8-1.4%), lower production costs, and stronger crema formation make Robusta essential in Italian espresso blends and mass-market instant coffee manufacturing. Vietnam dominates global Robusta production at approximately 40% of world supply.

By Product

Roasted coffee holds a 46.3% share in 2025, representing the primary end-use form for green coffee globally. The roasting process transforms green coffee’s chlorogenic acids, lipids, and carbohydrates into the complex flavor compounds defining finished coffee character, serving specialty roasters, commercial manufacturers, and supermarket private-label programs alike.

Instant/soluble coffee, with 34.7% in 2025, is manufactured through spray-drying and freeze-drying processes converting brewed coffee concentrate into reconstitutable powder. Emerging market demand in Asia Pacific and Africa, where convenience and price accessibility are primary purchase drivers, sustains strong volume demand for soluble coffee as a major green bean end-use channel.

Green coffee bean extract (19.0%) is the fastest-growing segment at ~4.2% CAGR through 2034. Standardized chlorogenic acid extracts are incorporated into weight management supplements and functional beverages. Growing scientific validation and expanding nutraceutical retail distribution are driving sustained premiumization of this category.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

36.8% |

High per-capita consumption; specialty coffee culture; sustainability certifications |

|

North America |

24.7% |

Specialty roaster expansion; RTD coffee growth; direct-trade sourcing trends |

|

Asia Pacific |

22.9% |

Rising coffee adoption in China and SE Asia; growing middle class; urbanization |

|

Latin America |

8.4% |

Domestic consumption growth; specialty expansion in Colombia and Brazil |

|

Middle East & Africa |

7.2% |

Gulf State premium coffee culture; Africa domestic consumption growth |

Europe’s 36.8% market dominance in 2025 is underpinned by the highest per-capita coffee consumption globally, particularly in Scandinavian countries (Finland averages 12 kg/capita/year), Germany, and Italy. The region’s robust specialty coffee infrastructure, stringent certification standards, and consumer willingness to pay premiums for traceable origins sustain consistently strong green coffee demand.

North America, with 24.7% in 2025, is experiencing strong specialty coffee expansion driven by third-wave coffee culture, growing home roasting communities, and direct-to-consumer subscription models.

Asia Pacific, at 22.9%, represents the fastest-growing regional market in absolute value terms, driven by China’s rapid coffee adoption, Southeast Asian urbanization, and Japan’s premium coffee evolution.

Competitive Landscape

The global green coffee market is moderately fragmented, with large commodity trading houses dominating volume flows while specialty importers compete on quality, origin relationships, and traceability. Regional leaders hold strong positions in sourcing networks while several global suppliers operate across multiple geographies and product categories.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Neumann Gruppe GmbH |

Green coffee |

Leader |

Largest global green coffee trader; 25+ origins; logistics integration |

|

Belco |

Green coffee |

Challenger |

Europe-focused specialty importer; direct trade; single origins |

|

wscafe company limited |

Green coffee |

Emerging |

Vietnam based specialist; growing extract channel for nutraceuticals |

Key players include Neumann Gruppe GmbH, Belco, wscafe company limited, and others.

Key Company Profiles

Neumann Gruppe GmbH

Neumann Gruppe GmbH is one of the world’s largest green coffee trading companies, headquartered in Hamburg, Germany, operating across various coffee-producing countries through an integrated network of origin subsidiaries, logistics companies, and risk management services globally.

- Product Portfolio: Green coffee

- Recent Developments: In August 2024, Neumann Kaffee Gruppe (NKG) announced a partnership with osapiens to strengthen compliance with the European Union Deforestation Regulation (EUDR) across its global coffee supply chain. Through this collaboration, NKG aims to enhance transparency, traceability, and sustainability monitoring within its sourcing operations.

- Strategic Focus: NKG’s strategy leverages its unparalleled origin network and logistics integration to deliver consistent large-volume supply to global roasters while expanding specialty and traceable coffee offerings to capture growing premium market demand.

Belco

Belco is a leading European specialty green coffee importer headquartered in France, sourcing directly from farmers and cooperatives, with a strong focus on certified, traceable, and premium quality offerings for European specialty roasters.

- Product Portfolio: Green coffee

- Strategic Focus: Belco focuses on deepening direct origin relationships, investing in farmer technical assistance programs, and expanding its portfolio of certified and traceable specialty lots to reinforce positioning as the preferred quality-focused green coffee partner for European specialty roasters.

Market Concentration Analysis

The global green coffee market is moderately fragmented at the global level, with commodity trading dominated by a small number of large integrated trading houses while specialty importing remains highly fragmented. No single company holds more than 8-10% of total global green coffee trading volume, reflecting the market’s structural diversity.

Consolidation at the commodity trading level is more advanced, with the top five global green coffee trading companies collectively handling a significant share of traded volumes. Specialty importing remains fragmented, with differentiation occurring primarily through direct brand-building, relationship depth, and quality positioning rather than M&A activity.

Investment & Growth Opportunities

Fastest-Growing Segments

Green coffee bean extract at ~4.2% CAGR through 2034 is the highest-growth product segment, driven by health supplement and functional food applications. Asia Pacific at ~3.8% CAGR is the fastest-growing regional market on absolute value terms, driven by China’s rapid coffee adoption and Southeast Asian urbanization dynamics.

Emerging Markets

Asia Pacific represents the largest absolute growth opportunity for green coffee through 2034. China’s coffee consumption is growing at 15%+ annually from a relatively low per-capita base, with Luckin Coffee, Starbucks China, and domestic specialty chains generating significant roasted and instant coffee demand requiring large-scale green bean procurement from origin.

Venture & Investment Trends

Private investment in specialty coffee supply chain technology, including blockchain traceability, precision fermentation for coffee flavor development, and direct-trade digital platforms, is growing. The EU Deforestation Regulation is accelerating capital deployment into supply chain transparency tools that create sustainable competitive advantages for compliant green coffee traders.

Future Market Outlook (2026-2034)

The global green coffee market is forecast to expand from USD 39.69 Billion in 2025 to USD 54.48 Billion by 2034 at a CAGR of 3.48%, adding USD 14.79 Billion in incremental annual market value over the forecast period, reflecting consistent growth linked to structural global coffee consumption expansion and premiumization trends.

Three forces will most significantly shape the green coffee industry through 2034. Climate adaptation investment in producing regions will reshape origin geography, with higher-altitude and climate-resilient varieties gaining share. Digital direct-trade platforms will compress traditional intermediary layers, improving farmer income and buyer quality access. Green coffee extract’s penetration of the global supplements market will create a high-value parallel demand channel growing substantially faster than beverage applications.

Research Methodology

Primary Research

Primary research encompassed structured interviews with green coffee industry stakeholders including senior commercial managers at global trading houses, specialty coffee importers, quality directors at European roasting companies, ICO data specialists, and direct-trade platform executives. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include International Coffee Organization (ICO) Coffee Report and Outlook, USDA Foreign Agricultural Service global coffee reports, Brazilian Coffee Exporters Council (CECAFE) trade statistics, Specialty Coffee Association (SCA) annual market research, European Coffee Federation consumption data, and trade publications including Daily Coffee News and Fresh Cup Magazine.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating per-capita consumption growth rates, urbanization indices, specialty coffee penetration curves, and historical market evolution patterns. Scenario analysis across base, optimistic, and conservative cases was performed to account for climate and macroeconomic uncertainty.

Green Coffee Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Arabica, Robusta |

| Products Covered | Roasted Coffee, Instant/Soluble Coffee, Green Coffee Bean Extract |

| Distribution Channels Covered | Hypermarkets and Supermarkets, Departmental Stores, Specialty Stores, Online, Others |

| End Users Covered | Retail, Coffee cafes, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Neumann Gruppe GmbH, Belco, wscafe company limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the green coffee market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global green coffee market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the green coffee industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Green Coffee Market Report

The global green coffee market reached USD 39.69 Billion in 2025, reflecting consistent demand driven by rising global coffee consumption, expanding specialty coffee culture, and growing health supplement applications for green coffee bean extract in key markets worldwide.

The market is projected to reach USD 54.48 Billion by 2034, growing at a CAGR of 3.48% during 2026-2034, driven by Asia Pacific growth, specialty coffee premiumization, e-commerce channel expansion, and green coffee extract demand in health and wellness categories globally.

Arabica leads with a 64.8% type share in 2025, valued for its premium smooth flavor profile and dominant positioning across third-wave coffee culture, specialty roasting, and gourmet retail segments globally.

Roasted coffee leads at 46.3% in 2025, representing the primary end-use conversion pathway for green coffee beans, serving specialty roasters, commercial manufacturers, supermarket private-label programs, and foodservice operators across all major consuming regions globally.

Europe commands a dominant 36.8% market share in 2025, supported by the highest per-capita coffee consumption globally, well-developed specialty coffee retail infrastructure, and strong consumer demand for premium, traceable, and sustainably sourced green coffee across the region.

Green coffee bean extract is the fastest-growing product at ~4.2% CAGR through 2034, driven by health supplement and functional food applications leveraging chlorogenic acid’s metabolic health benefits and expanding nutraceutical retail distribution across North America, Europe, and Asia Pacific.

Leading companies include Neumann Gruppe GmbH, Belco, wscafe company limited, and others.

Key drivers include rising global coffee consumption, e-commerce channel expansion enabling direct trade, specialty coffee culture growth, health supplement demand for green coffee extracts, and premiumization trends driving consumer willingness to pay for traceable and certified origins across major markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)