Handheld Surgical Instruments Market Report by Product (Forceps, Retractors, Dilators, Graspers, Scalpels, Cannulas, Dermatome, Trocars, and Others), Application (Orthopedic Surgery, Cardiology, Ophthalmology, Wound Care, Audiology, Thoracic Surgery, Urology and Gynecology Surgery, Plastic Surgery, Neurosurgery, and Others), End User (Hospitals, Clinics, Ambulatory Surgical Centers, and Others), and Region 2026-2034

Handheld Surgical Instruments Market Size:

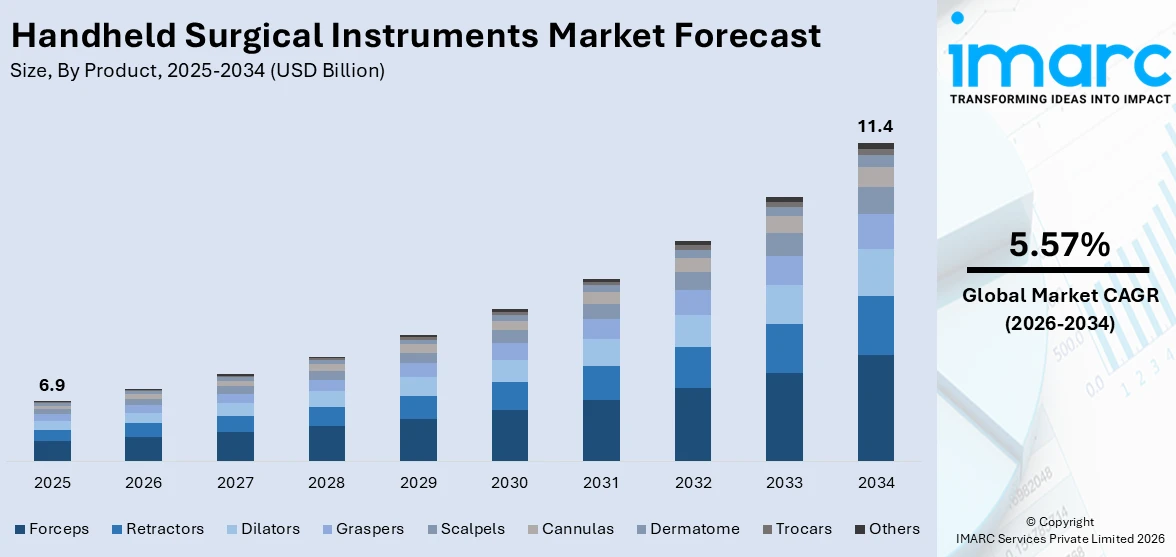

The global handheld surgical instruments market size reached USD 6.9 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 11.4 Billion by 2034, exhibiting a growth rate (CAGR) of 5.57% during 2026-2034. The market is growing rapidly driven by rapid advancements in surgical techniques, rising incidence of chronic diseases, such as cancer and obesity, increasing geriatric population across the globe, significant technological innovations, and escalating healthcare expenditures.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 6.9 Billion |

|

Market Forecast in 2034

|

USD 11.4 Billion |

| Market Growth Rate 2026-2034 | 5.57% |

Handheld Surgical Instruments Market Analysis:

- Market Growth and Size: The market is witnessing stable growth, driven by the increasing demand for surgical procedures globally, rising geriatric population, and growing healthcare expenditure.

- Major Market Drivers: Key drivers influencing the market growth include advancements in surgical techniques, rising number of chronic diseases requiring surgical intervention, significant technological advancements, and growing geriatric population necessitating more surgical procedures.

- Technological Advancements: Recent innovations in material science and design, leading to more ergonomic, precise, and durable instruments, are propelling the market growth. Additionally, the integration of advanced technologies like robotics and sensor-based instruments are favoring the market growth.

- Industry Applications: The market is experiencing high product demand in a wide range of medical fields, including orthopedics, cardiology, and neurosurgery, with orthopedic surgery being the largest application segment.

- Key Market Trends: The key market trends involve the ongoing shift towards personalized and custom-made surgical instruments, rise in healthcare standards, and increasing patient-specific needs. Furthermore, sustainability in manufacturing processes and introduction of eco-friendly products are fueling the market growth.

- Geographical Trends: North America leads the market due to its advanced healthcare infrastructure and high medical spending. Other regions are also showing significant growth, fueled by improving healthcare facilities and rising medical tourism.

- Competitive Landscape: The market is characterized by the presence of both established players and emerging companies that are engaging in mergers, acquisitions, and global expansion to strengthen their market positions.

- Challenges and Opportunities: The market faces various challenges, such as stringent regulatory standards and the need for high capital investments. However, the growing demand or advanced surgical tools in emerging economies and the development of instruments for new surgical techniques are creating new opportunities for the market growth.

To get more information on this market Request Sample

Handheld Surgical Instruments Market Trends:

Rapid advancements in surgical techniques

The shifting trend towards minimally invasive surgeries (MIS) known for their reduced recovery times and lower risk of complications, necessitating precise and advanced tools, is propelling the market growth. Furthermore, the growing demand for handheld surgical instruments in laparoscopic surgeries, allowing surgeons to operate through small incisions, is contributing to the market growth. Besides this, the development of robotic surgery, which has created a demand for instruments compatible with robotic systems, is positively impacting the market growth. These advancements not only enhance the efficacy and safety of surgical procedures but also extend the scope of surgeries that can be performed. Additionally, manufacturers are investing in research and development (R&D) to create more ergonomic, durable, and efficient tools, aligning with the latest surgical practices.

Rising incidences of chronic diseases

The increasing prevalence of chronic conditions, such as cardiovascular diseases (CVDs), cancer, orthopedic disorders, and obesity, which often require surgical interventions, necessitating a wide range of surgical instruments, is boosting the market growth. In line with this, the escalating demand for cardiovascular surgeries, leading to an increased need for specialized surgical tools like scissors, forceps, and clamps, is contributing to the market growth. Additionally, the surge in cancer cases across the globe, which requires more surgical procedures for tumor removal and biopsies, is catalyzing the market growth. Furthermore, the significant growth in orthopedic surgeries due to conditions like osteoarthritis and rheumatoid arthritis is acting as another growth-inducing factor. Moreover, the growing obesity epidemic across the globe, leading to bariatric surgeries, is strengthening the market growth.

Increasing geriatric population across the globe

The escalating geriatric population, which is more susceptible to a variety of medical conditions that may require surgical intervention, is contributing to the market growth. Furthermore, age-related diseases such as cataracts, osteoporosis, and certain types of cancer are becoming more prevalent, increasing the demand for surgeries and, consequently, for surgical instruments. Besides this, the rise in age-related cataract cases, leading to a higher number of cataract surgeries, is favoring the market growth. Moreover, the increasing number of orthopedic surgeries like hip and knee replacements among the geriatric population is boosting the market growth. Apart from this, the geriatric population requires more frequent medical attention and surgical care, which places a continuous demand on the healthcare system, including the need for various surgical instruments.

Significant technological innovations

The continuous development of new and improved instruments that offer greater precision, efficiency, and safety is bolstering the market growth. Additionally, the integration of advanced materials like carbon fiber and titanium, leading to lighter, more durable instruments that reduce surgeon fatigue and enhance performance, is contributing to the market growth. Furthermore, the emergence of smart instruments equipped with sensors and connectivity capabilities, which allow for real-time feedback during surgeries, improving outcomes, is positively impacting the market growth. Besides this, recent innovations in instrument design, such as ergonomic handles and enhanced gripping surfaces, which reduce the risk of errors and increase comfort for surgeons, are favoring the market growth. Moreover, the ongoing miniaturization of surgical tools to suit minimally invasive (MI) procedures is fueling the market growth.

Escalating healthcare expenditure

Governments across the globe are allocating more resources to their healthcare systems, leading to an increase in the availability and quality of medical services, including surgeries. Furthermore, these investments translate into the procurement of better and more advanced surgical tools. Additionally, the rapid improvement in healthcare infrastructure, which includes modernizing hospitals and clinics and equipping them with the latest surgical instruments, is contributing to the market growth. This expansion not only increases the accessibility of surgical care but also boosts the demand for a wide range of surgical tools. Besides this, the escalating support for research and development (R&D) in medical technologies, including the innovation of new surgical instruments, is bolstering the market growth.

Handheld Surgical Instruments Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product, application, and end user.

Breakup by Product:

- Forceps

- Retractors

- Dilators

- Graspers

- Scalpels

- Cannulas

- Dermatome

- Trocars

- Others

Forceps accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the product. This includes forceps, retractors, dilators, graspers, scalpels, cannulas, dermatome, trocars, and others. According to the report, forceps represented the largest segment.

Forceps hold the largest market segment as they are essential for grasping, holding, and manipulating tissues during surgical procedures. They are available in a wide range of designs, such as Allis, Babcock, and hemostatic forceps, catering to various surgical needs, from delicate tissue handling in microsurgeries to firm gripping in general surgeries. Additionally, the heightened awareness about the versatility of forceps, coupled with their critical role in almost every surgical discipline, is strengthening the market growth. Besides this, continuous innovation in forceps design, aimed at improving precision and reducing tissue trauma, is further bolstering the market growth.

Retractors are available in various forms, including handheld and self-retaining retractors, each designed for specific surgical contexts. Additionally, the growing demand for retractors is driven by their indispensable role in a wide array of surgeries, from abdominal procedures to orthopedic surgeries. Innovations focusing on ergonomic design and reduced tissue trauma are key trends influencing this segment's growth in the handheld surgical instruments market.

Dilators are used to enlarge or stretch a body orifice or passage, commonly employed in urological, gynecological, and cardiovascular procedures. Additionally, the increasing number of surgeries involving stent placements and procedures addressing strictures in various body channels. Besides this, the development of dilators that minimize patient discomfort and enhance procedural efficiency is driving the market growth.

Graspers are designed for holding and manipulating tissues, especially in minimally invasive surgeries. It includes a variety of designs like biopsy graspers, tissue manipulators, and organ holders. Additionally, the integration of enhanced grip to improve control and minimal tissue trauma, is bolstering the market growth. Moreover, the rising trend of minimally invasive surgical approaches is favoring the market growth.

The scalpel segment is driven by the need for precision and control in surgical cuts. It includes traditional stainless steel scalpels as well as disposable and safe scalpels designed to reduce infection risks and prevent injuries. Furthermore, the ongoing refinement of blade materials and ergonomic handles is positively impacting the market growth.

Cannulas are tubes inserted into the body to administer or remove fluids. Furthermore, the increasing number of procedures requiring fluid administration or aspiration, such as liposuction and various orthopedic and cardiovascular surgeries, is contributing to the market growth. Moreover, the recent innovations in cannula design, reducing tissue trauma and improving procedural efficacy, are strengthening the market growth.

Dermatomes are specialized instruments used in skin grafting procedures. Additionally, the growing need for effective wound management and reconstructive surgeries, particularly for burn victims, is bolstering the market growth. Moreover, the ability of dermatomes to precisely cut thin and uniform skin grafts, which is a critical factor in successful grafting procedures, is favoring the market growth.

Trocars are used to create entry points for surgical instruments in laparoscopic surgeries. They are pivotal in minimally invasive procedures, allowing access with minimal tissue damage. Furthermore, recent innovations in trocar design, focusing on patient safety, ease of insertion, and reduction of postoperative complications, are bolstering the market growth. Additionally, the increasing preference for minimally invasive procedures is fueling the market growth.

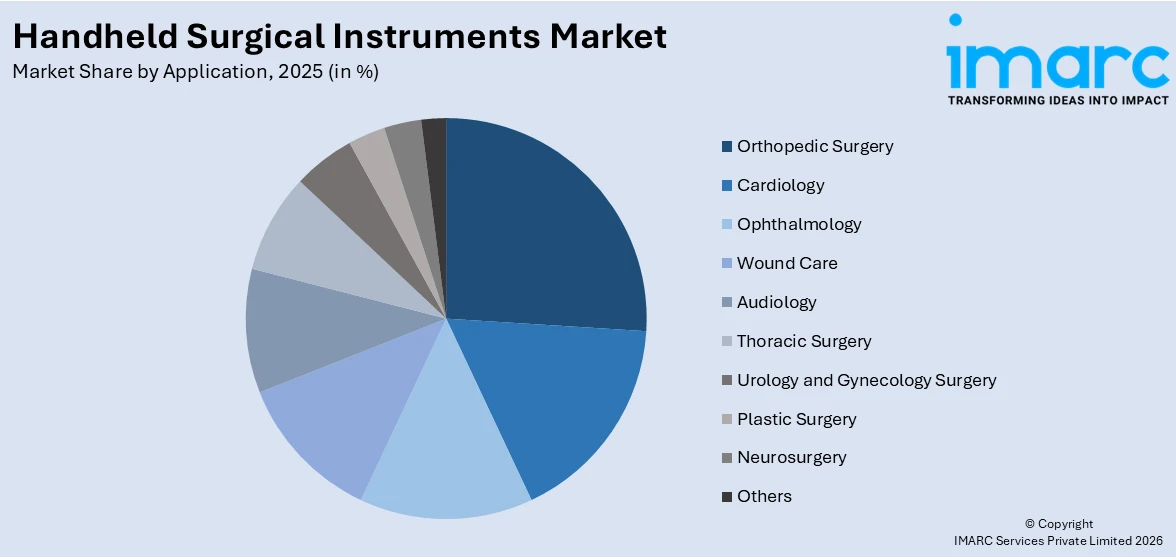

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Orthopedic Surgery

- Cardiology

- Ophthalmology

- Wound Care

- Audiology

- Thoracic Surgery

- Urology and Gynecology Surgery

- Plastic Surgery

- Neurosurgery

- Others

Orthopedic surgery holds the largest share in the industry

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes orthopedic surgery, cardiology, ophthalmology, wound care, audiology, thoracic surgery, urology and gynecology surgery, plastic surgery, neurosurgery, and others. According to the report, orthopedic surgery accounted for the largest market share.

Orthopedic surgery holds the largest market segment, reflecting the high volume of musculoskeletal procedures performed across the globe. This segment includes instruments used in joint replacement, fracture management, and spinal surgeries, among others. Additionally, the rising incidence of osteoporosis, sports injuries, and a geriatric population, which contributes to the growing demand for orthopedic surgeries, is favoring the market growth. Moreover, recent advances in surgical techniques and the development of specialized instruments for bone cutting, drilling, and fixing are further bolstering the market growth.

The cardiology segment encompasses instruments used in heart-related surgical procedures, including coronary artery bypass grafting, heart valve repair or replacement, and other cardiac surgeries. Furthermore, the increasing prevalence of heart diseases, driven by factors such as aging populations and lifestyle-related issues, is contributing to the market growth.

The ophthalmology segment focuses on surgical instruments for eye-related procedures like cataract removal, glaucoma treatment, and refractive surgeries. Additionally, the rising incidence of eye diseases, particularly among the geriatric population, is driving the market growth. Moreover, recent innovations in instruments that enhance precision and safety, such as microsurgical tools, are fueling the market growth.

The wound care segment includes instruments used in the management and closure of wounds, such as suturing tools and staplers. Additionally, the growing need for efficient wound healing in surgeries, trauma, and burn care is fueling the market growth. Besides this, the heightened focus on reducing infection risks and enhancing healing times is contributing to the market growth.

Audiology encompasses surgical instruments used in ear surgeries, such as cochlear implantation and tympanoplasty. Additionally, the increasing prevalence of hearing disorders and advancements in ear surgery techniques are catalyzing the market growth. Besides this, the introduction of precision instruments that cater to the delicate nature of ear structures is positively impacting the market growth.

Thoracic surgery involves procedures on the chest organs, including the lungs and heart. It involves specialized instruments for lung resections, thoracotomies, and other chest surgeries. Furthermore, the rising incidence of lung diseases and technological advancements in thoracic surgery are contributing to the market growth.

The urology and gynecology surgery segment covers instruments such as for treating urinary tract disorders and performing hysterectomies. Furthermore, the growing prevalence of related health conditions, coupled with advancements in surgical techniques, is acting as another growth-inducing factor.

The plastic surgery segment includes instruments used in cosmetic and reconstructive procedures. Furthermore, the increasing demand for aesthetic surgeries and reconstructive procedures following trauma or cancer treatment is favoring the market growth. Moreover, the development of precision tools that cater to the specific requirements of plastic surgery is fueling the market growth.

Neurosurgery involves complex procedures on the brain and spinal cord. It demands high-precision instruments for delicate surgeries, such as tumor removal and aneurysm repair. Furthermore, the increasing incidence of neurological disorders and advancements in neurosurgical techniques are positively impacting the market growth.

Breakup by End User:

- Hospitals

- Clinics

- Ambulatory Surgical Centers

- Others

Hospitals represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the end user. This includes hospitals, clinics, ambulatory surgical centers, and others. According to the report, hospitals represented the largest segment.

Hospitals represent the largest market segment due to their comprehensive surgical capabilities and the wide range of procedures they accommodate. Hospitals are typically equipped with extensive and diverse sets of surgical instruments to cater to various specialties, from emergency surgeries to elective procedures. Additionally, their large patient base, coupled with the need for advanced and specialized surgical tools for complex surgeries, is bolstering the market growth. Besides this, hospitals' ongoing efforts to update and expand their surgical equipment to keep pace with technological advancements and evolving medical standards are favoring the market growth.

Clinics handle less complex procedures compared to hospitals, their role in performing minor surgeries, outpatient procedures, and diagnostic interventions is contributing to the market growth. Furthermore, the increasing number of specialty clinics, the rising preference for outpatient surgical procedures due to cost-effectiveness, and the growing accessibility to healthcare services are favoring the market growth.

Ambulatory surgical centers (ASCs) specialize in providing same-day surgical care, including diagnostic and preventive procedures. They are known for their lower costs compared to hospitals, shorter wait times, convenience, and the increasing capability to perform a wider range of surgeries with advancements in surgical and anesthesia techniques. Additionally, the introduction of favorable healthcare policies and a focus on cost-effective healthcare delivery is supporting the market growth.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest handheld surgical instruments market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America holds the largest market share due to its advanced healthcare infrastructure, high healthcare spending, and the presence of leading medical device companies. Additionally, the increasing prevalence of surgical procedures due to the geriatric population, escalating chronic diseases, and a strong focus on healthcare innovation are contributing to the market growth. Furthermore, the rising adoption of technologically advanced surgical instruments and a robust regulatory framework ensuring quality and safety, is positively influencing the market growth. Moreover, increasing investments in research and development (R&D), coupled with favorable healthcare policies, are strengthening the market growth.

Europe is a significant market for handheld surgical instruments, driven by advanced healthcare systems, high healthcare expenditure, and a strong focus on surgical research and innovation. Additionally, the rising geriatric population, increasing prevalence of chronic diseases, and a well-established medical device industry in the region are contributing to the market growth.

The Asia Pacific region is rapidly growing in the handheld surgical instruments market, driven by improving healthcare infrastructure, increasing healthcare spending, and a growing population. Additionally, the region is witnessing an increasing number of surgical procedures due to rising chronic diseases and the geriatric population, which is bolstering the market growth. Besides this, the increasing local manufacturing and the presence of emerging medical device companies are supporting the market growth.

Latin America represents a growing market for handheld surgical instruments, fueled by improving healthcare infrastructure, increasing medical expenditure, and rising awareness about advanced surgical procedures. Additionally, the imposition of various government initiatives to improve healthcare services, increase accessibility, and escalate investments in hospital infrastructure are acting as another growth-inducing factor.

The Middle East and Africa region is experiencing growth in the handheld surgical instruments market due to the increasing investments in healthcare infrastructure, rising medical tourism in the region, and growing awareness about surgical care. Additionally, the growing private sector investment and government initiatives in healthcare are fueling the market growth.

Leading Key Players in the Handheld Surgical Instruments Industry:

Top companies are heavily investing in research and development (R&D) to innovate and improve their product offerings. It includes creating more ergonomic designs, utilizing advanced materials for durability and precision, and developing instruments suited for emerging surgical techniques like MIS. Furthermore, several leading players are expanding their market presence and product portfolio through strategic mergers and acquisitions. Besides this, they are continuously looking to expand their geographic footprint to establish new distribution channels and partnerships with local firms. Moreover, companies are adopting eco-friendly practices in their manufacturing processes and are working on developing sustainable products.

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Aspen Surgical

- B. Braun Melsungen AG

- Becton Dickinson and Company

- CooperSurgical Inc. (The Cooper Companies Inc.)

- Integra LifeSciences

- Johnson & Johnson

- Medtronic plc

- Thompson Surgical Instruments Inc.

- Zimmer Biomet

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Latest News:

- In October 2022, Aspen Surgical acquired Symmetry Surgical, a leading manufacturer of high-quality surgical and specialty instruments.

- In May 2022, Johnson & Johnson received FDA approval for its Monarch robotic surgery system that can be used in kidney stone removal treatment.

- In June 2023, Becton Dickinson and Company signed an agreement with STERIS to sell its Surgical Instrumentation platform, in a move to simplify its portfolio.

Handheld Surgical Instruments Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Forceps, Retractors, Dilators, Graspers, Scalpels, Cannulas, Dermatome, Trocars, Others |

| Applications Covered | Orthopedic Surgery, Cardiology, Ophthalmology, Wound Care, Audiology, Thoracic Surgery, Urology and Gynecology Surgery, Plastic Surgery, Neurosurgery, Others |

| End Users Covered | Hospitals, Clinics, Ambulatory Surgical Centers, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Aspen Surgical, B. Braun Melsungen AG, Becton Dickinson and Company, CooperSurgical Inc. (The Cooper Companies Inc.), Integra LifeSciences, Johnson & Johnson, Medtronic plc, Thompson Surgical Instruments Inc., Zimmer Biomet, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global handheld surgical instruments market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global handheld surgical instruments market?

- What is the impact of each driver, restraint, and opportunity on the global handheld surgical instruments market?

- What are the key regional markets?

- Which countries represent the most attractive handheld surgical instruments market?

- What is the breakup of the market based on the product?

- Which is the most attractive product in the handheld surgical instruments market?

- What is the breakup of the market based on the application?

- Which is the most attractive application in the handheld surgical instruments market?

- What is the breakup of the market based on the end user?

- Which is the most attractive end user in the handheld surgical instruments market?

- What is the competitive structure of the market?

- Who are the key players/companies in the global handheld surgical instruments market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the handheld surgical instruments market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global handheld surgical instruments market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the handheld surgical instruments industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)