Healthcare Claims Management Market Size, Share, Trends and Forecast by Product, Component, Solution Type, Delivery Mode, End User, and Region, 2026-2034

Healthcare Claims Management Market Size and Share:

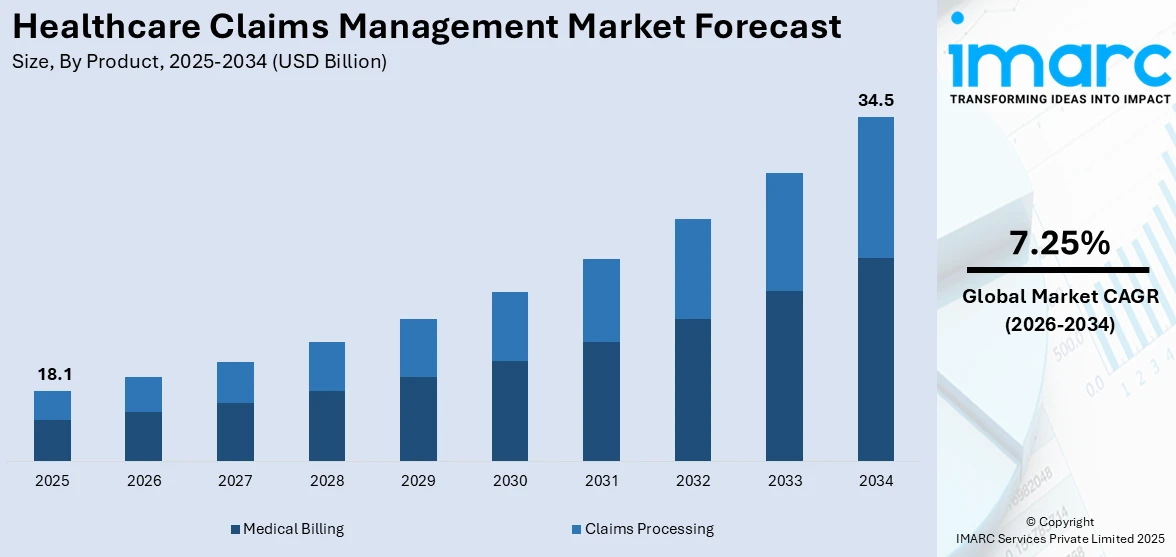

The global healthcare claims management market size was valued at USD 18.1 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 34.5 Billion by 2034, exhibiting a CAGR of 7.25% from 2026-2034. North America currently dominates the market, holding a market share of 42% in 2025. The region benefits from a mature healthcare infrastructure, high private and public insurance penetration, stringent regulatory mandates driving claims digitization, and widespread adoption of electronic health records, all of which reinforce its leading Healthcare Claims Management market share.

The global market for healthcare claims management is growing steadily due to the interlinked factors that are transforming the management of the global healthcare industry. The increasing complexity of billing codes and processing claims is forcing organizations to turn to sophisticated solutions that can simplify processes and minimize the chances of errors. The increasing volume of patient data and the widespread use of electronic health record systems are creating a need for comprehensive solutions that can process large volumes of claims. The changes in regulations in various international nations to ensure transparency in healthcare payments are forcing organizations to turn to automation solutions.

The United States has emerged as a major region in the healthcare claims management market owing to many factors. The country operates one of the world's most intricate healthcare billing ecosystems, involving Medicare, Medicaid, and private insurance structures requiring specialized claims management capabilities. Federal mandates including the Health Insurance Portability and Accountability Act and ICD code transitions have created enduring demand for compliant, regularly updated solutions. In September 2025, AGS Health was recognized with the UiPath AI25 Award for its use of agentic automation to help U.S. providers reduce costly claim denials and improve clean claim rates, reinforcing how automation is reshaping claims workflows. Widespread electronic health record adoption across hospitals and physician practices provides a strong foundation for digital claims adjudication. The sustained emphasis on reducing administrative costs is further motivating investment in automation tools, reinforcing the Healthcare Claims Management market outlook across the United States.

To get more information on this market Request Sample

Healthcare Claims Management Market Trends:

Accelerating Adoption of Artificial Intelligence

Artificial intelligence is fundamentally reshaping how healthcare organizations manage and process claims. Machine learning algorithms automate the identification of claim errors, predict likely denials before submission, and recommend corrective actions that improve first-pass acceptance rates. Natural language processing tools assist in extracting relevant clinical documentation to support medical necessity determinations, reducing manual review time considerably. In 2025, Optum launched its AI‑driven platform Optum Real, enabling real‑time claims verification and adjudication that helps providers and payers detect issues before submission and reduce administrative errors, showcasing real‑world application of AI in claims workflows. AI-driven platforms enable continuous learning systems that adapt to evolving payer policies and coding guidelines automatically. By analyzing historical claims patterns, these systems flag billing inconsistencies and compliance risks proactively, improving operational accuracy and lowering administrative costs, making it one of the defining Healthcare Claims Management market trends.

Shift Toward Cloud-Based Delivery Platforms

Cloud computing has emerged as a transformative force within the Healthcare Claims Management market, enabling organizations of all sizes to access sophisticated claims management capabilities without maintaining costly on-premises infrastructure. Cloud-based platforms offer scalability that allows providers and payers to manage fluctuating claims volumes efficiently across varied operational conditions. In January 2026, Wipro expanded its PayerAI platform, automating claims inventory and reconciliation workflows to boost accuracy, efficiency, and scalability. These platforms facilitate real-time data exchange between providers, payers, and clearinghouses, accelerating adjudication timelines and improving revenue cycle transparency. Enhanced security protocols embedded in modern cloud architectures are encouraging broader adoption among risk-averse healthcare entities, while seamless integration with electronic health records supports end-to-end visibility, contributing to the evolving Healthcare Claims Management market forecast landscape.

Growing Focus on Interoperability Standards

Interoperability has become a strategic priority for healthcare systems globally, with profound implications for claims management. The ability of disparate systems to exchange and interpret claims data accurately is critical for minimizing processing delays, reducing duplicate submissions, and improving adjudication efficiency. In July 2025, the U.S. Centers for Medicare & Medicaid Services (CMS) launched a new Interoperability Framework alongside a patient‑centric digital health ecosystem, with over 60 tech and health companies pledging to enable standards‑based data exchange across payers, providers, and apps, thereby accelerating seamless claims and clinical data sharing. Interoperable claims management platforms reduce friction in multi-payer environments by enabling consistent data formatting and transmission standards across provider networks and payer systems. This harmonization supports more accurate analytics and reporting, empowering administrators to identify denial patterns and optimize submission strategies effectively. The pursuit of interoperability remains a key driver behind investment in advanced Healthcare Claims Management market growth solutions across all geographic segments.

Healthcare Claims Management Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global healthcare claims management market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product, component, solution type, delivery mode, and end user.

Analysis by Product:

- Medical Billing

- Professional

- Institutional

- Claims Processing

Medical billing holds 54% of the market share. Medical billing encompasses the translation of healthcare services rendered by providers into standardized billing codes that are submitted to payers for reimbursement. This process involves patient registration, charge capture, coding, claim submission, and payment posting, forming the backbone of healthcare revenue cycle management. The dominance of medical billing within the Healthcare Claims Management landscape reflects the sheer complexity and volume of billing transactions generated across hospital systems, physician practices, outpatient facilities, and specialty care centers. Rising patient volumes, driven by aging populations and growing chronic disease prevalence, are expanding the quantity of billing events requiring accurate and timely processing. The transition to value-based reimbursement models has further elevated the importance of precise billing that accurately reflects clinical outcomes and service complexity. Additionally, increasing regulatory scrutiny around billing accuracy and compliance has incentivized organizations to invest in advanced medical billing platforms that minimize claim errors and optimize reimbursement capture.

Analysis by Component:

- Services

- Software

Software leads the market with a share of 65%. Software solutions form the technological core of modern healthcare claims management operations, providing the automation, integration, and analytical capabilities that organizations require to handle complex billing and adjudication processes at scale. In October 2025, NYX Health launched its AI‑powered denial management platform, automating claim denials and helping hospitals accelerate revenue recovery. Claims management software encompasses a broad spectrum of functionalities including eligibility verification, code scrubbing, electronic claim submission, denial management, remittance processing, and real-time reporting. The dominance of the software segment reflects the ongoing digital transformation of healthcare administrative functions, where manual processes are progressively replaced by intelligent automated workflows. Organizations are increasingly selecting feature-rich software platforms that integrate with existing electronic health record and practice management systems, enabling seamless data flow across the revenue cycle. The growing emphasis on analytics-driven decision-making is further boosting investment in software that provides actionable insights into claim performance, denial trends, and payer behavior patterns.

Analysis by Solution Type:

- Integrated Solutions

- Standalone Solutions

Integrated solutions dominate the market, with a share of 67%. Integrated claims management solutions deliver comprehensive, end-to-end capabilities that unify billing, coding, submission, adjudication, and analytics within a single cohesive platform. This holistic approach eliminates the operational fragmentation associated with deploying multiple point solutions, enabling healthcare organizations to achieve greater workflow continuity and data consistency across the revenue cycle. The preference for integrated solutions is driven by the recognition that disconnected systems create information silos that slow processing speeds and increase the risk of claim errors and denials. Healthcare payers and providers alike are prioritizing integrated platforms that offer real-time visibility into claim status, automated follow-up workflows, and unified reporting dashboards. The scalability inherent in integrated architectures also makes them suitable for large hospital systems and multi-specialty practices managing high claims volumes. Furthermore, integrated solutions facilitate compliance with evolving regulatory requirements by enabling centralized policy management and standardized coding protocols.

Analysis by Delivery Mode:

- On-premises

- Cloud-based

- Web-based

Cloud-based represents the leading segment, with a market share of 40%. Cloud-based delivery of healthcare claims management solutions has gained substantial traction as organizations seek flexible, scalable, and cost-effective alternatives to traditional on-premises deployments. By hosting applications and data on remote servers managed by specialized providers, cloud platforms relieve healthcare organizations of the capital expenditure and ongoing maintenance responsibilities associated with in-house infrastructure. This shift is particularly advantageous for small and mid-sized practices that may lack the IT resources to manage complex on-premises systems effectively. Cloud architectures enable automatic software updates that incorporate the latest coding guidelines and regulatory changes, ensuring continuous compliance without manual intervention. Real-time access to claims data from any location supports distributed care teams and remote administrative staff, enhancing operational flexibility. The growing confidence in cloud security frameworks and expanding compliance certifications relevant to healthcare data protection continue to accelerate adoption of cloud-based claims management platforms globally.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Healthcare Payers

- Healthcare Providers

- Others

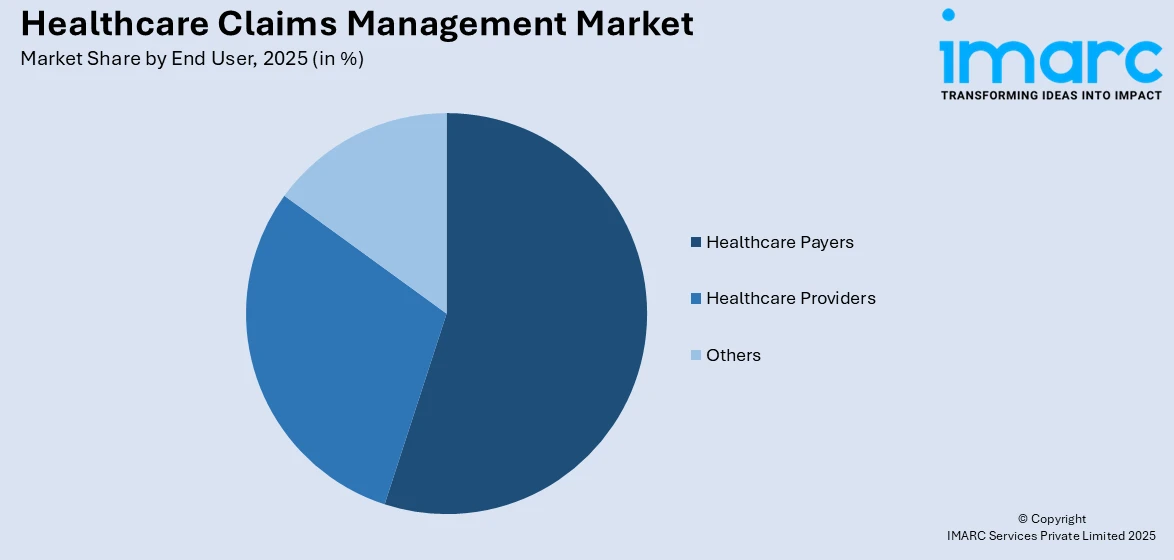

Healthcare Payers account for the leading position in the market, with a share of 46%. Healthcare payers, including insurance companies, managed care organizations, and government health programs, represent the largest end-user segment within the Healthcare Claims Management market due to their central role in processing and adjudicating the vast majority of healthcare claims. Payers rely heavily on sophisticated claims management systems to evaluate, validate, and reimburse claims submitted by providers, making accurate and efficient processing critical to their financial performance and member satisfaction. The complexity of managing claims across diverse plan types, benefit structures, and provider networks necessitates robust software platforms capable of handling high transaction volumes with precision. Payers are increasingly investing in advanced analytics and automation capabilities within their claims operations to detect fraudulent billing patterns, reduce administrative overhead, and accelerate payment cycles. Regulatory compliance requirements governing claims processing timelines and accuracy standards further drive payer investment in comprehensive claims management infrastructure.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 42% of the share, enjoys the leading position in the market. The region's commanding position is attributable to its highly developed healthcare ecosystem, characterized by complex multi-payer reimbursement structures that generate substantial volumes of claims requiring professional management. The United States, in particular, drives regional dominance through its expansive private health insurance market, federally administered programs, and an extensive network of hospitals, physician groups, and ancillary care providers, all of which depend on efficient claims processing to sustain financial operations. Comprehensive regulatory frameworks governing claims accuracy, payment timelines, and coding standards create continuous demand for compliant, sophisticated management solutions. Canada contributes to regional strength through its universal healthcare model, where administrative efficiency in claims handling supports broader health system sustainability objectives. Ongoing investment in healthcare information technology infrastructure across North America is expected to further reinforce the region's leadership in the Healthcare Claims Management market throughout the forecast period.

Key Regional Takeaways:

United States Healthcare Claims Management Market Analysis

The United States represents the most sophisticated and mature Healthcare Claims Management market globally, underpinned by an extraordinarily complex healthcare billing environment involving thousands of payers, multiple reimbursement programs, and continuously evolving coding requirements. The coexistence of Medicare, Medicaid, commercial insurance plans, and managed care organizations creates a multifaceted reimbursement landscape that demands advanced, adaptable claims management capabilities. Federal legislative initiatives aimed at reducing administrative friction and promoting electronic claims submission have accelerated the transition from paper-based processes to digital platforms across healthcare organizations of all sizes. The emphasis on reducing claim denials and improving first-pass resolution rates is driving adoption of predictive analytics tools and automated denial management workflows. The growing complexity of value-based care contracts and alternative payment models requires claims systems capable of processing outcomes-linked billing with precision. These factors collectively sustain robust demand for advanced claims management solutions throughout the United States, supporting the country's preeminent position in the Healthcare Claims Management market forecast.

Europe Healthcare Claims Management Market Analysis

Europe represents a significant and evolving market for healthcare claims management, shaped by the distinctive characteristics of its predominantly public healthcare financing systems alongside growing private sector participation. Countries such as Germany, France, and the United Kingdom are advancing digital health transformation agendas that include modernizing administrative processes for health reimbursement and claims adjudication. In March 2025, the European Health Data Space (EHDS) Regulation entered its implementation phase, setting common standards to enable secure, interoperable health data exchange across EU member states, serving as a key enabler for harmonized claims workflows across borders. The fragmented nature of European healthcare systems, with country-specific billing standards and reimbursement frameworks, creates demand for flexible claims management solutions adaptable to multiple regulatory environments. Cross-border care agreements within the European Union are generating additional complexity in claims processing, incentivizing investment in interoperable platforms capable of managing multi-jurisdictional billing scenarios. The increasing prevalence of private supplemental insurance in several European markets is expanding the claims processing ecosystem beyond public payers.

Asia Pacific Healthcare Claims Management Market Analysis

The Asia-Pacific region is emerging as a high-growth market for healthcare claims management, driven by rapid expansion in healthcare infrastructure, rising health insurance enrollment, and increasing government commitment to digital health transformation. Countries including China, India, Japan, and South Korea are investing substantially in modernizing their health reimbursement systems, creating favorable conditions for adoption of advanced claims processing solutions. The expansion of private health insurance coverage across developing economies in the region is generating growing volumes of complex claims requiring efficient management platforms. Government initiatives promoting paperless healthcare administration and electronic health record adoption are creating a supportive regulatory environment for digital claims solutions. The large and growing patient populations across the region, coupled with an expanding middle class seeking quality healthcare services, are expected to sustain strong demand for scalable claims management infrastructure throughout the forecast period.

Latin America Healthcare Claims Management Market Analysis

Latin America presents a developing opportunity within the global Healthcare Claims Management landscape, supported by expanding healthcare coverage programs and growing private insurance penetration in key economies such as Brazil and Mexico. Governments across the region are progressively investing in healthcare administration modernization, including the digitization of claims submission and reimbursement processes. The dual-payer structure present in many Latin American countries, combining public social security systems with private insurance, requires flexible claims management solutions capable of navigating distinct regulatory requirements. While infrastructure gaps and digital literacy variations across the region moderate the pace of adoption, sustained investment in healthcare information technology is expected to strengthen market development progressively.

Middle East and Africa Healthcare Claims Management Market Analysis

The Middle East and Africa region represents an emerging frontier for healthcare claims management, characterized by divergent market maturity levels across its constituent countries. Gulf Cooperation Council nations, particularly Saudi Arabia and the United Arab Emirates, are investing aggressively in healthcare infrastructure modernization and mandatory health insurance schemes that are generating substantial claims management requirements. National health transformation programs in these economies are creating demand for sophisticated digital claims processing platforms aligned with international standards. In Africa, expanding health insurance coverage through government and employer-sponsored programs is gradually increasing the volume and complexity of claims requiring professional management solutions, laying the groundwork for longer-term market development.

Competitive Landscape:

The global Healthcare Claims Management market is characterized by intense competition among established technology firms, specialized revenue cycle management companies, and healthcare IT conglomerates, all vying for market share through continuous product innovation and strategic partnerships. Leading players are investing significantly in artificial intelligence and machine learning capabilities to enhance denial prediction, automate adjudication workflows, and deliver actionable analytics to customers. The competitive environment is further shaped by merger and acquisition activity, as larger entities seek to broaden their solution portfolios and expand geographic reach. Vendors are increasingly differentiating through cloud-native architectures, interoperability capabilities, and seamless integration with electronic health record ecosystems. Regulatory compliance expertise and the ability to adapt rapidly to changing coding standards represent critical competitive advantages. Smaller specialized vendors are carving niches by focusing on specific care settings or payer segments, intensifying overall competitive dynamics across the landscape.

The report provides a comprehensive analysis of the competitive landscape in the healthcare claims management market with detailed profiles of all major companies, including:

- Accenture Plc

- Allscripts Healthcare Solutions Inc.

- Athenahealth

- Carecloud Inc.

- Cognizant

- Conifer Health Solutions (Tenet Healthcare Corporation)

- Mckesson Corporation

- Optum Inc. (UnitedHealth Group Incorporated)

- Oracle Corporation

- Plexis Healthcare Systems

- Quest Diagnostics

- The SSI Group LLC.

Latest News and Developments:

- In February 2026, Healthee announced the upcoming launch of AI-powered Claims Analytics within its Healthee Pulse platform. The solution transforms static claims reports into real-time conversational analytics using an AI assistant. It helps employers and health plans identify cost drivers, utilization trends, and savings opportunities, improving decision-making and claims cost optimization.

- In February 2026, LexisNexis Risk Solutions launched an AI-powered Healthcare Identity Platform for providers and payers. The platform automates patient identity verification, reduces fraud risks, and enhances claims workflow accuracy with enriched data profiles, streamlining processing and improving operational efficiency.

Healthcare Claims Management Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered |

|

| Components covered | Services, Software |

| Solution Types covered | Integrated Solutions, Standalone Solutions |

| Delivery Modes covered | On-Premises, Cloud-Based, Web-Based |

| End Users Covered | PHealthcare Players, Healthcare Providers, Others |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Accenture plc, Allscripts Healthcare Solutions Inc., Athenahealth, Carecloud Inc., Cognizant, Conifer Health Solutions (Tenet Healthcare Corporation), Mckesson Corporation, Optum Inc. (UnitedHealth Group Incorporated), Oracle Corporation, Plexis Healthcare Systems, Quest Diagnostics, The SSI Group LLC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the healthcare claims management market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global healthcare claims management market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the healthcare claims management industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Healthcare Claims Management Market Report

The healthcare claims management market was valued at USD 18.1 Billion in 2025.

The healthcare claims management market is projected to exhibit a CAGR of 7.25% during 2026-2034, reaching a value of USD 34.5 Billion by 2034.

Key drivers include increasing complexity in healthcare billing and reimbursement processes, growing adoption of electronic health records, regulatory mandates promoting claims digitization, the shift toward value-based care models, rising demand for interoperable platforms, and expanding health insurance coverage across both developed and emerging markets worldwide.

North America currently dominates the healthcare claims management market, accounting for a share of 42%. The region benefits from a mature healthcare infrastructure, complex multi-payer reimbursement structures, strong regulatory frameworks promoting claims digitization, and broad adoption of electronic health record systems that support efficient digital claims processing.

Some of the major players in the healthcare claims management market include Accenture plc, Allscripts Healthcare Solutions Inc., Athenahealth, Carecloud Inc., Cognizant, Conifer Health Solutions (Tenet Healthcare Corporation), Mckesson Corporation, Optum Inc. (UnitedHealth Group Incorporated), Oracle Corporation, Plexis Healthcare Systems, Quest Diagnostics, The SSI Group LLC, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)