Healthcare Extended Reality Market Size, Share, Trends and Forecast by Component, Application, End User, and Region 2026-2034

Global Healthcare Extended Reality Market Size, Share, Trends & Forecast (2026-2034)

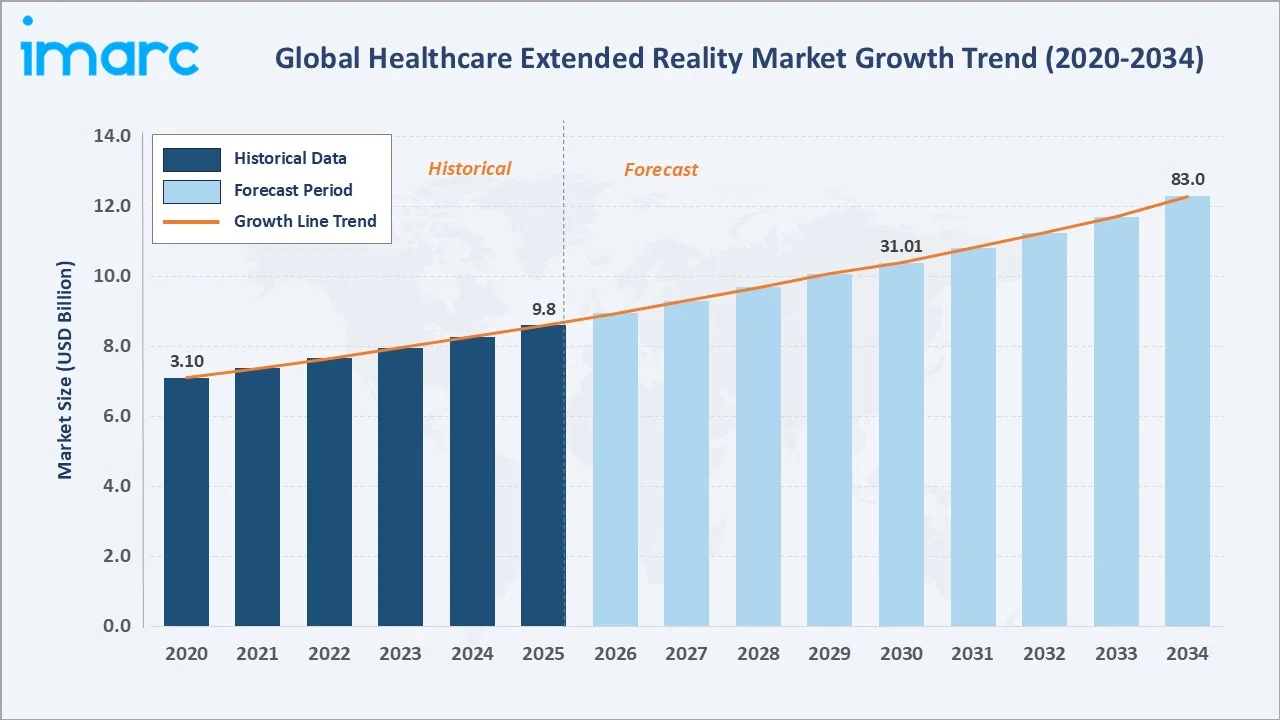

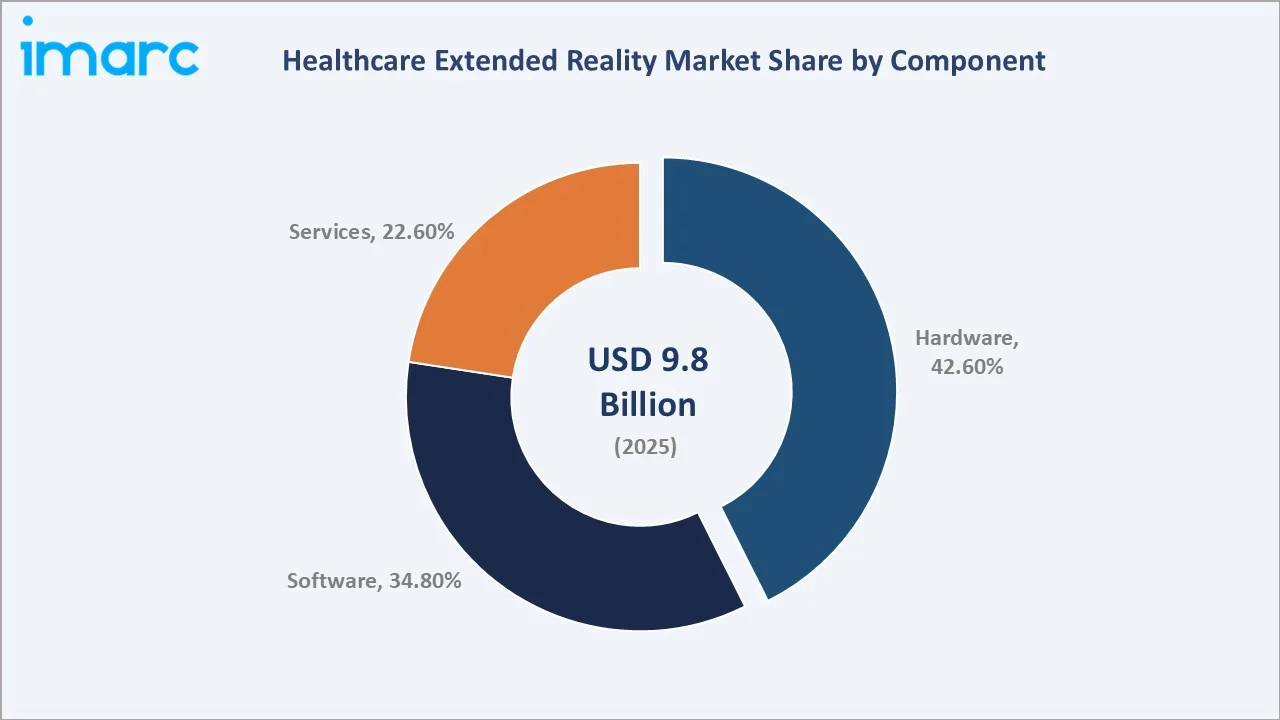

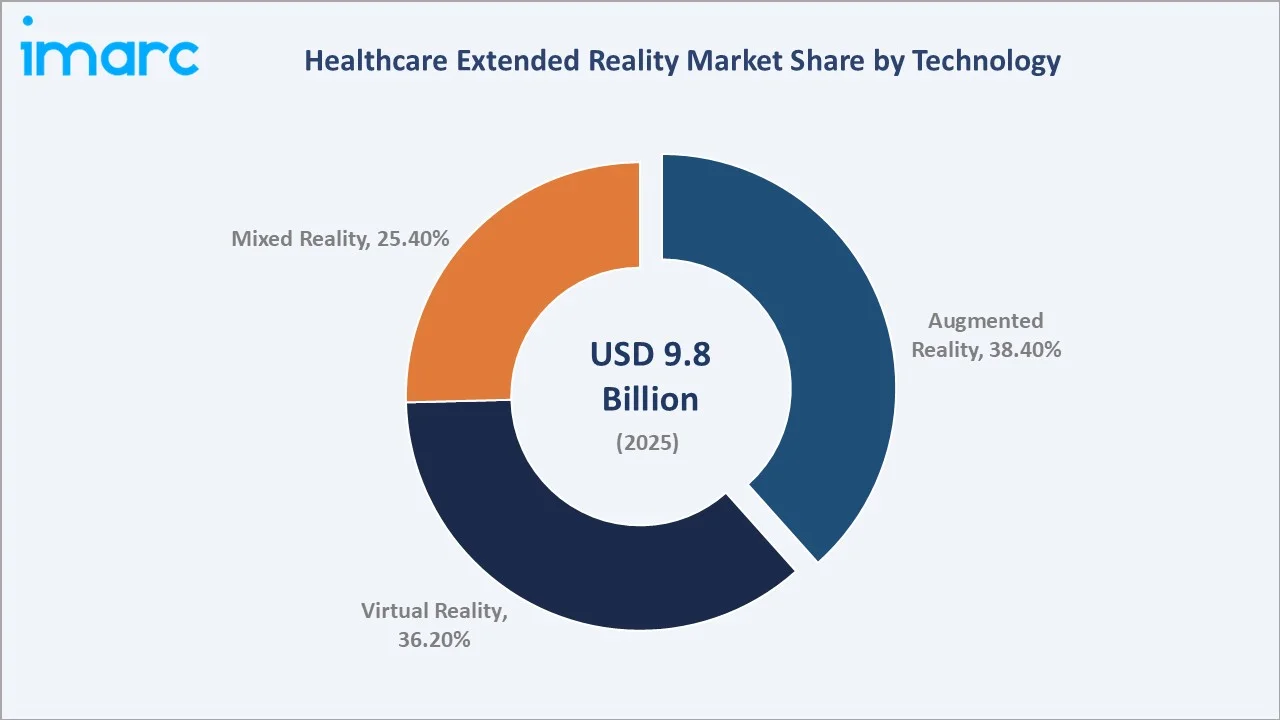

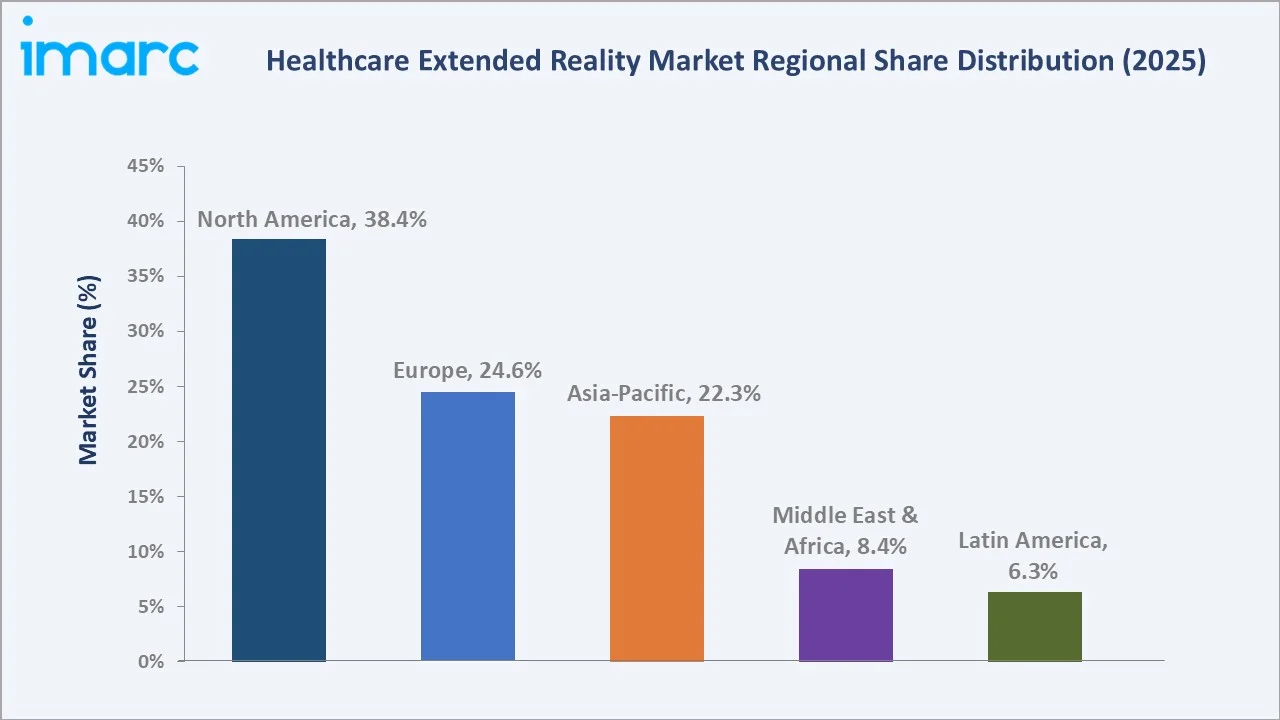

The global healthcare extended reality market size reached USD 9.8 Billion in 2025 and is projected to reach USD 83.0 Billion by 2034, exhibiting a CAGR of 25.91% during 2026-2034. Accelerating adoption of immersive technologies in surgical training and planning, remote medical consultations, patient rehabilitation, and pain management - combined with deepening AI integration, and rising patents with more than 2,000 XR-related patents registered in the United States since 2020 are the primary engines of healthcare XR market growth. Hardware dominates the component mix at 42.6% in 2025, while Augmented Reality leads the technology segment at 38.4%. North America commands the largest regional share at 38.4% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size 2025 |

USD 9.8 Billion |

|

Forecast Market Size 2034 |

USD 83.0 Billion |

|

CAGR 2026-2034 |

25.91% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.4% share, 2025) |

|

Fastest Growing Region |

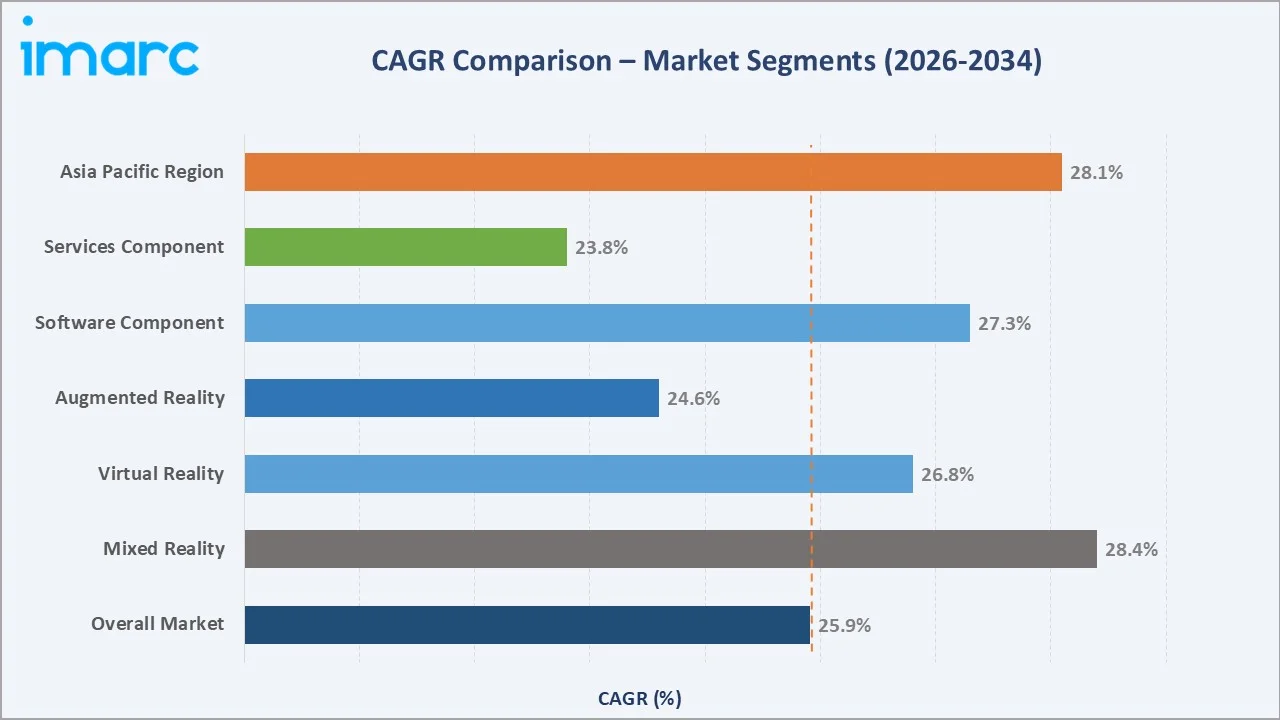

Asia-Pacific (CAGR ~28.1%) |

|

Leading Component |

Hardware (42.6%, 2025) |

|

Leading Technology |

Augmented Reality (38.4%, 2025) |

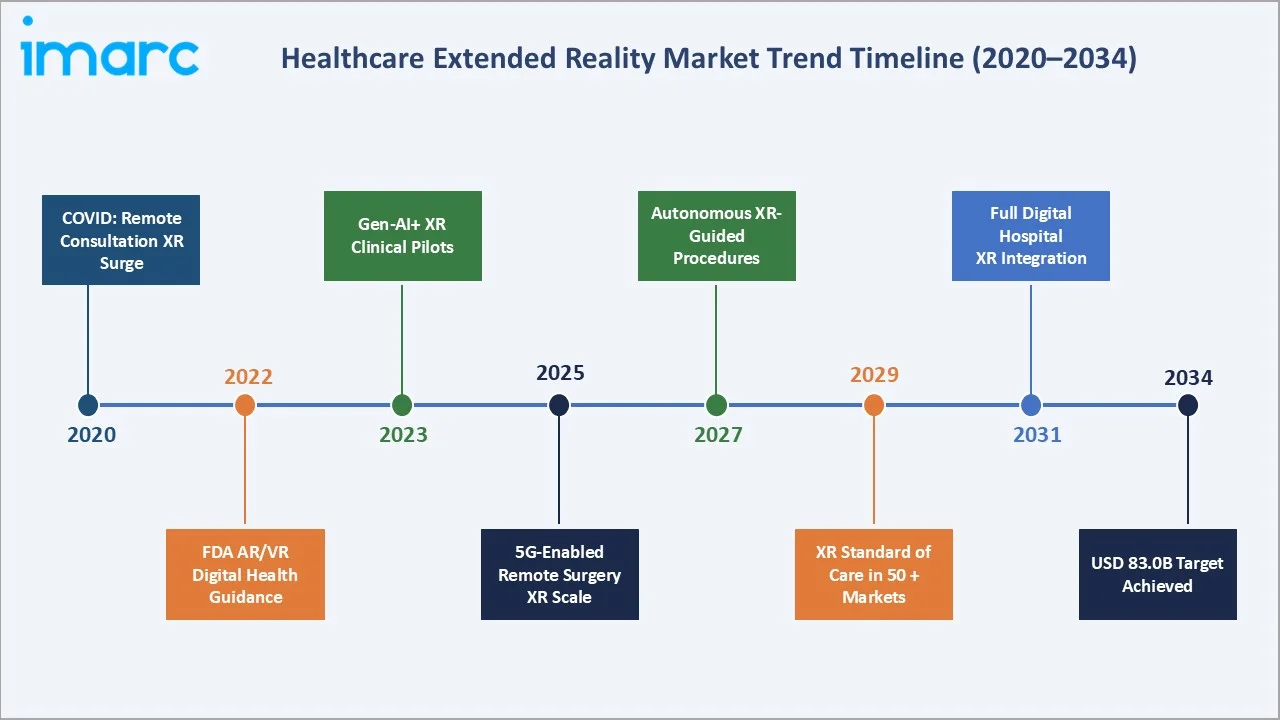

The global healthcare XR market trajectory from 2020 through 2034. Historical CAGR of approximately 36% between 2020 and 2025 reflects pandemic-driven acceleration; the forecast 25.91% CAGR represents sustained expansion driven by clinical adoption maturation and regulatory clearances.

To get more information on this market, Request Sample

Mixed Reality and Software emerge as the fastest-growing sub-categories, growing above the 27% threshold, reflecting the industry's maturation from hardware deployment toward integrated software-driven clinical workflows.

Executive Summary

The global healthcare extended reality (XR) market is one of the fastest-growing segments in the broader digital health industry, expanding from USD 9.8 Billion in 2025 to a projected USD 83.0 Billion by 2034 at a CAGR of 25.91%. XR - encompassing Augmented Reality (AR), Virtual Reality (VR), and Mixed Reality (MR) is reshaping clinical practice across surgery, medical education, rehabilitation, mental health therapy, and pain management.

The COVID-19 pandemic served as a powerful structural catalyst: remote surgical consultations, virtual clinical trials, and telerehabilitation programmes emerged as necessities, establishing XR as core healthcare infrastructure rather than an experimental technology. According to the National Institutes of Health, telemedicine usage grew by over 3,000% during the pandemic peak, with XR-enabled remote consultation tools representing a significant share of new deployments.

Hardware leads component demand at 42.6% in 2025, anchored by head-mounted displays (HMDs) from Microsoft (HoloLens 2), Meta (Quest Pro for clinical use), and Apple (Vision Pro) gaining FDA clearance pathways for specific clinical indications. Software at 34.8% is growing at the highest segment as purpose-built clinical XR applications from companies. Augmented Reality leads technology type at 38.4% in 2025, driven by surgical overlay applications.

North America leads at 38.4% in 2025, supported by a robust FDA digital health framework, NIH digital health investment, and a mature health insurance ecosystem. Europe (24.6%) benefits from EU MDR regulatory support and national digital health programmes. Asia-Pacific (22.3%) is the fastest-growing region, with Japan's Society 5.0 healthcare agenda driving XR adoption.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Hardware - 42.6% share (2025) |

|

Leading Technology |

Augmented Reality - 38.4% share (2025) |

|

Leading Region |

North America - 38.4% revenue share (2025) |

|

Fastest-Growing Region |

Asia-Pacific - CAGR ~28.1% (2026-2034) |

Key Analytical Observations Supporting The Above Data Points:

- Hardware at 42.6% 2025 is driven by rapid deployment of clinical-grade HMDs. Microsoft HoloLens 2 is used in surgical planning in hospitals, targeting surgical visualization and patient education applications.

- Augmented Reality (38.4%, 2025) leads due to its ability to overlay digital information onto real surgical fields without removing surgeons from their physical environment. The FDA has authorized a total of 69 medical products that incorporate AR/VR as of September 2024.

- North America's 38.4% dominance is reinforced by the FDA's Digital Health Center of Excellence - established in 2020, creating the most permissive regulatory environment for healthcare XR commercialization globally.

- Asia-Pacific, with 22.3% in 2025, reflects government support and investments, which are accelerating product commercialization timelines.

Global Healthcare Extended Reality Market Overview

Healthcare Extended Reality (XR) is the collective umbrella term for Augmented Reality (AR), Virtual Reality (VR), and Mixed Reality (MR) technologies applied within clinical, educational, research, and patient-care contexts. AR overlays digital information onto the real world via HMDs or mobile devices; VR creates fully immersive digital environments; and MR blends physical and digital spaces interactively.

The global ecosystem connects semiconductor and display manufacturers, HMD device companies, healthcare-specific software developers, system integration partners, regulatory bodies (FDA, EMA, CDSCO), hospital networks, medical schools, pharmaceutical companies, and research institutions.

Macroeconomic enablers include countries within the OECD, which are estimated to have spent about 9.3% of their GDP on healthcare on average in 2024and the post-pandemic structural shift toward remote and technology-mediated care delivery.

Market Dynamics

To evaluate market opportunities, Request Sample

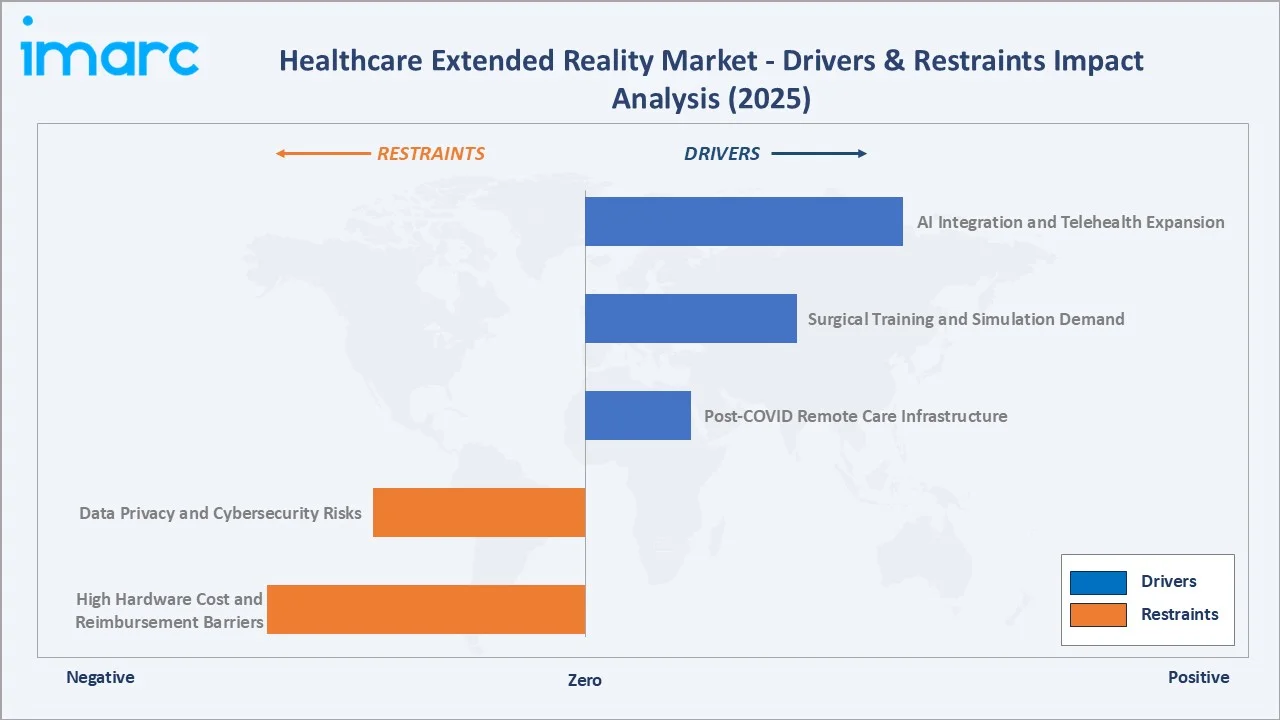

Market Drivers

- AI Integration and Telehealth Expansion: The fusion of Generative AI with XR platforms is creating clinical decision-support systems that were impossible five years ago. Microsoft's Azure AI integrated into HoloLens 2 enables real-time anatomical annotation during surgeries, including pediatric surgical procedures .

- Surgical Training and Simulation Demand: Medical education faces a 11 million healthcare worker shortage projected by WHO by 2030, while regulatory reforms restrict resident surgeon working hours. VR surgical simulation platforms from CAE Healthcare (Vimedix), Surgical Science (LapSim), and 3D Systems (Touch haptic training) offer validated, repeatable training without patient risk.

- Post-COVID Remote Care Infrastructure: The pandemic established XR-enabled remote care as reimbursable and clinically acceptable.

Market Restraints

- High Hardware Cost and Reimbursement Barriers: Clinical-grade HMDs (Microsoft HoloLens 2 at approximately USD 3,500 per unit; Apple Vision Pro at USD 3,499) represent significant capital expenditure for healthcare systems already under financial pressure.

- Data Privacy and Cybersecurity Risks: Healthcare XR systems collect biometric data (eye tracking, gait analysis, physiological responses) in addition to standard patient health information, creating HIPAA (US), GDPR (EU), and national privacy law compliance complexity.

Market Opportunities

- Mental Health and Neurological Rehabilitation: The global mental health treatment gap, with over 1 billion people living with mental health disorder s, is creating an enormous addressable market for scalable, accessible XR-based therapeutic interventions.

- Pharmaceutical XR for Drug Development and Clinical Trials: Pharma companies are deploying XR for clinical trial patient recruitment visualization, drug interaction 3D modelling, and physician detailing (replacing physical sales rep visits).

- Emerging Market Healthcare Capacity Building: Organizations including Jhpiego (Johns Hopkins affiliate) and Living Health Global are deploying VR clinical training platforms in resource-limited settings where high-fidelity simulation mannequins are cost-prohibitive, creating an emerging market entry pathway for XR platform providers with tiered pricing models.

Market Challenges

- Physician Adoption and Workflow Integration: Despite demonstrable clinical benefits, physician adoption of XR tools remains patchy.

- Content Quality and Clinical Accuracy Standards: The proliferation of healthcare XR applications exposed significant variation in clinical content accuracy and pedagogical quality.

Emerging Market Trends

1. Generative AI Integration Enabling Personalized XR Clinical Experiences

Large language models and generative AI are being integrated into XR clinical platforms to create dynamically personalized training scenarios, adaptive rehabilitation programmes, and real-time anatomical annotation. Microsoft's partnership with Epic Systems in May 2023 enabled GPT-4 to electronic health records .

2. VR-Enabled Surgery and Telemedicine XR

Virtual reality is making real-time remote surgical guidance and autonomous surgical robotics viable. A new virtual reality tool named CAPTAiN, created by researchers at Johns Hopkins University, has the potential to transform how beginner surgeons are trained in spinal procedures, offering a safer, more intelligent, and highly personalized learning experience, creating a structural demand vector for XR surgical platforms.

3. XR-Based Mental Health Therapeutics Gaining Clinical Acceptance

The mental health XR therapeutic category is transitioning from research to commercial clinical deployment. The FDA's Breakthrough Device designation for XR-based mental health applications is accelerating the regulatory pathway for this category.

4. Pharmaceutical Company XR Platform Investment

Major pharmaceutical companies are building or acquiring XR capabilities for drug development, physician education, and patient adherence programmes. In June 2023, Medivis, a medical technology firm aiming to make augmented reality the standard for surgical navigation, announced the successful completion of a $20 million Series A funding round, led by Thrive Capital, with additional participation from Initialized Capital and Mayo Clinic .

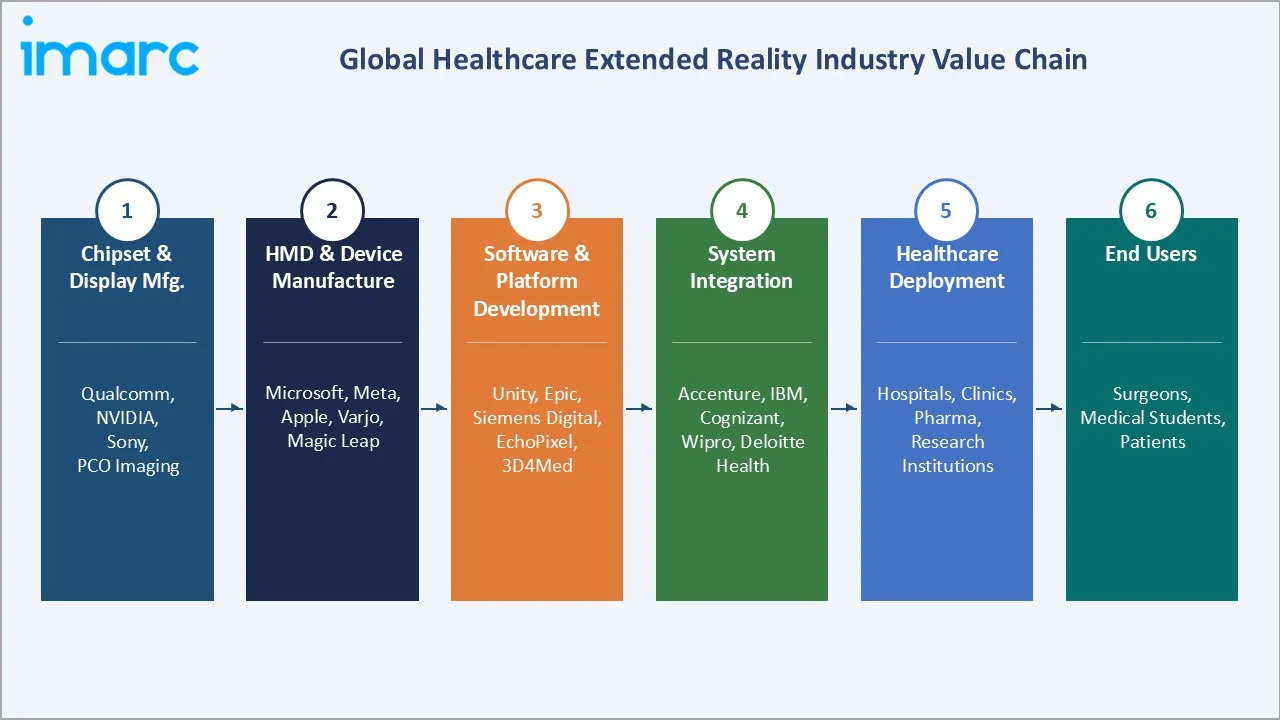

Industry Value Chain Analysis

The healthcare XR value chain spans six stages from semiconductor and display manufacturing through clinical end-use delivery. Each stage carries distinct IP, margin, and regulatory characteristics.

|

Stage |

Key Players / Examples |

|

Chipset & Display Manufacturing |

Qualcomm (Snapdragon XR2), NVIDIA (RTX XR), Sony (OLED Microdisplay), PCO Imaging, BOE Technology |

|

HMD & Device Manufacturing |

Microsoft (HoloLens 2), Meta (Quest Pro), Apple (Vision Pro), Varjo (XR-4), Magic Leap (ML2) |

|

Software & Platform Development |

EchoPixel, ImmersiveTouch, Surgical Science, Unity Technologies, Medivis, 3D Systems, OssoVR |

|

System Integration & Services |

Accenture Health, IBM Watson Health, Cognizant, Wipro Healthcare IT, Deloitte Digital Health |

|

Healthcare System Deployment |

Hospitals (Mayo Clinic, Cleveland Clinic), Medical Schools (Johns Hopkins), Pharma (Pfizer, Roche) |

|

End Users |

Surgeons, medical students, physical therapists, patients (chronic pain, mental health, rehabilitation) |

Clinical software developers and system integrators capture the highest margin positions in the healthcare XR value chain platform software commands 70-80% gross margins versus 20-35% for hardware. Hospital deployment and training services represent a growing recurring revenue stream, with enterprise contracts for large academic medical centers.

Technology Landscape in the Healthcare XR Industry

Head-Mounted Display Hardware Evolution

Field-of-view expansion from 52 degrees (HoloLens 2 ) to 50 degrees (Magic Leap 2) is reducing the 'tunnel vision' effect that previously limited surgical XR utility. Next-generation optics using Pancake lens technology (Meta Quest Pro) and microLED arrays are targeting sub-100g clinical XR displays in future.

Computer Vision and AI-Powered Anatomical Recognition

Real-time anatomical recognition using computer vision and deep learning models is the enabling technology for surgical AR overlay accuracy. Augmedics' Xvision system uses AI to register pre-operative CT and intraoperative 3D images to intraoperative anatomy , enabling FDA-cleared augmented reality spine surgery navigation.

Cloud-Enabled XR and Streaming Rendering

Cloud rendering is enabling high-fidelity XR clinical applications to run on lightweight hardware by offloading compute-intensive 3D rendering to cloud servers. This decoupling of rendering performance from device hardware is a critical enabler for healthcare XR democratization, allowing high-fidelity clinical XR on affordable hardware.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Hardware |

42.6% |

2025 |

|

Technology |

Augmented Reality |

38.4% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End User |

Hospitals, Clinics and Surgical Centers |

🔒 |

2025 |

|

Region |

North America |

38.4% |

2025 |

By Component

Hardware commands a 42.6% component share in 2025, reflecting the initial infrastructure investment phase of the healthcare XR adoption cycle. Microsoft's enterprise agreement with the US Army (USD 21.88 Billion for tactical HoloLens units) and equivalent healthcare enterprise agreements demonstrate the magnitude of institutional hardware procurement.

To access detailed market analysis, Request Sample

As the installed base matures, Software's 34.8% share is growing at the fastest rate as per-procedure subscription revenues compound on top of the expanding hardware deployment base. Services at 22.6% encompasses implementation, integration, training, and managed services contracts.

By Technology

Augmented Reality leads at 38.4% in 2025, driven by surgical navigation applications where overlaying digital anatomical information onto the patient's physical body provides immediate clinical value without removing clinicians from their real-world operating environment. FDA clearances for AR surgical devices have accelerated: in November 2025, Augmedics announced that its next-generation AR headset, X2, received FDA 510(k) clearance for use with the xvision Spine System.

Virtual Reality, with 36.2% in 2025, dominates in application areas requiring complete environmental control: pain management, mental health therapy, phobia treatment, and surgical simulation. Mixed Reality (25.4%, 2025) is growing fastest, blending real and virtual seamlessly.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.4% |

FDA Digital Health Center of Excellence; NIH funding; CMS XR reimbursement expansion; mature hospital tech budgets |

|

Europe |

24.6% |

EU MDR digital health track; NHS digital transformation; Germany Digital Healthcare Act; EMA harmonization |

|

Asia-Pacific |

22.3% |

China 14th Five-Year Plan USD 20B digital health; South Korea XR investment; Japan Society 5.0 healthcare |

|

Middle East & Africa |

8.4% |

Saudi Vision 2030 smart hospital programme; UAE SEHA digital health; South Africa telehealth infrastructure |

|

Latin America |

6.3% |

Brazil SUS digital health modernization; Mexico IMSS digital transformation; Colombia telemedicine expansion |

North America commands 38.4% of global healthcare XR revenue in 2025, anchored by the United States' regulatory leadership. The FDA cleared more XR medical devices than any other regulatory body globally. The US healthcare spending rose by 7.2% to $5.3 trillion in 2024 from $4.9 trillion in 2023, creating significant capital capacity for technology adoption.

Asia-Pacific, with 22.3% in 2025, is the fastest-growing region. A joint report by the World Bank and the Chinese government projected that, without healthcare reforms, China’s health expenditure could rise from $543.5 billion in 2014 to $2.5 trillion by 2035.This rapid cost escalation is driving APAC healthcare XR adoption, as providers turn to XR for cost-efficient training, remote care, and improved clinical outcomes.

Competitive Landscape

The global healthcare XR competitive landscape is led by major technology conglomerates leveraging their hardware and cloud platforms alongside specialized healthcare XR software companies developing clinical-application-specific solutions.

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

AppliedVR |

RelieVRx |

Leader |

VR-based pain management, mental health therapy, digital therapeutics |

|

BioflightVR |

BioflightVR |

Emerging |

Medical training, VR simulations for clinical education |

|

CareAR (Xerox Holdings Corporation) |

CareAR Platform |

Challenger |

AR-assisted remote support, healthcare workflow optimization |

|

FundamentalVR |

Fundamental XR |

Leader |

Surgical training simulations, haptics-enabled VR learning |

|

Fusion VR |

Fusion VR Platform |

Emerging |

Medical education, immersive healthcare training |

|

GigXR |

GigXR Platform / HoloScenarios |

Challenger |

Holographic medical training, mixed reality education |

|

Medicalholodeck AG |

Medicalholodeck |

Challenger |

Surgical planning, 3D visualization, collaborative VR |

|

Microsoft Corporation |

HoloLens |

Leader |

Surgical planning, remote collaboration, medical education |

|

Osso VR Inc. |

Osso VR Platform |

Leader |

Orthopedic surgical training, VR simulation, skill assessment |

|

PrecisionOS |

PrecisionOS Platform |

Challenger |

Orthopedic training, VR surgical simulations |

|

XRHealth |

VR-based Therapy solutions |

Leader |

Leverages virtual reality to deliver healthcare treatments remotely |

The competitive positioning across market presence and strategic investment dimensions for key healthcare XR participants in 2025.

Key Company Profiles

Microsoft Corporation

Microsoft is the global leader in enterprise mixed reality hardware and platform software for healthcare applications. Its HoloLens 2 - priced at USD 3,500 per device with enterprise support packages is deployed across hospital systems for surgical planning, medical education, and remote surgical consultation.

- Product Portfolio: HoloLens 2 , Microsoft Mesh , Azure Remote Rendering.

- Recent Developments: In August 2023, Epic broadened its collaboration with Microsoft to scale the use of artificial intelligence in healthcare by integrating conversational, ambient, and generative AI capabilities into clinical workflows .

- Strategic Focus: Microsoft's healthcare XR strategy centers on becoming the enterprise OS for the connected hospital: integrating HoloLens hardware with Azure cloud infrastructure, Teams communication platforms, and Epic/Cerner EHR systems to position the company as the comprehensive digital healthcare operating environment.

Osso VR Inc.

Osso VR Inc. is a leading virtual reality company focused on transforming surgical training, particularly in orthopedics. The platform enables surgeons and medical professionals to practice procedures in a realistic, immersive environment.

- Product Portfolio: Offers VR-based surgical training modules covering orthopedic procedures, skill assessments, and certification programs .

- Recent Developments: In October 2025, Osso VR announced early access to its new virtual reality solution, Osso Nurse Training, aimed at improving how health systems onboard newly graduated nurses .

- Strategic Focus: Focuses on improving surgical outcomes through standardized, scalable training while integrating performance analytics and validation tools.

XRHealth

XRHealth is a digital therapeutics company that leverages virtual reality to deliver healthcare treatments remotely. It combines XR technology with telehealth services to provide accessible care.

- Product Portfolio: Includes VR-based therapy solutions for physical rehabilitation, cognitive therapy, and mental health treatment .

- Recent Developments: In September 2025, XRHealth launched XR CareCart, a versatile virtual reality rehabilitation station designed to deliver advanced therapy directly within clinics, hospitals, and community healthcare settings .

- Strategic Focus: Aims to make healthcare more accessible and cost-effective by integrating XR with remote care and personalized treatment programs.

Market Concentration Analysis

The global healthcare XR market exhibits moderate concentration at the hardware and platform level, with the top 5 technology providers. The clinical software and specialized application layer are highly fragmented, with FDA-registered XR medical device applications from a diverse ecosystem of companies.

The market's high growth rate (25.91% CAGR) is attracting significant new entrant activity. Apple's Vision Pro entry into the healthcare market represents the most significant new competitive entry since Microsoft HoloLens 2's launch.

Investment & Growth Opportunities

Fastest-Growing Segments

Mixed Reality is the fastest-growing technology. The ability to overlay digital surgical guidance onto real anatomical structures without complete immersion makes MR the preferred technology for intraoperative applications, where complete VR immersion is clinically impractical. Software is the highest-growth component category and captures 70-80% gross margins versus 20-35% for hardware. SaaS-delivered clinical XR applications with per-procedure or per-seat subscription pricing create predictable recurring revenue streams increasingly valued by healthcare system investors.

Emerging Market Expansion

Mental health XR therapeutics represent the highest-potential emerging sub-market. FDA Breakthrough Device designations granted to 4 XR mental health companies in 2023-2024 are compressing regulatory pathways. Early-stage investment in this category carries significant de-risking advantages: validated clinical evidence is accumulating, regulatory pathways are clarifying, and unmet clinical need is structurally permanent.

Venture and Strategic Investment Trends

Global health XR venture investment includes Rock Health Digital Health Funding Database, with mental health XR, surgical simulation, and AI-integrated XR as the primary recipient categories. Strategic corporate investment is accelerating: Apple's Vision Pro healthcare partnerships signal that non-traditional healthcare companies are entering the space.

Future Market Outlook (2026-2034)

The global healthcare XR market is forecast to expand from USD 9.8 Billion in 2025 to USD 83.0 Billion by 2034 at a CAGR of 25.91%, an 8.5x market multiplication representing one of the highest-growth opportunities in the entire digital health landscape.

Three discontinuities are most likely to reshape the healthcare XR market through 2034. AI-autonomous surgical XR, where AI models provide real-time intraoperative decision support overlaid via AR without surgeon manual input, will transition from proof-of-concept to regulated clinical deployment. Brain-computer interface (BCI) integration with XR clinical platforms will enable motor-impaired patients to interact with XR rehabilitation environments through neural signals.

Research Methodology

Primary Research

Primary research included 65+ structured interviews with healthcare CIOs and digital health directors at US and European hospital systems, clinical XR product managers at Microsoft Healthcare, Siemens Healthineers, CAE Healthcare, and GE Healthcare, FDA Digital Health Center of Excellence representatives, surgical simulation educators, and XR-focused venture capital fund managers. Primary data validated market sizing, segmentation shares, technology adoption timelines, and reimbursement landscape assessments.

Secondary Research

Key secondary sources include FDA Digital Health Dashboard (510(k) and De Novo clearance database, 2020-2025), NIH Reporter clinical grant database (XR healthcare grants), Rock Health Digital Health Funding Database (2023-2024), CMS telehealth reimbursement data, WHO Global Strategy on Digital Health 2020-2025, NEJM Catalyst Innovations in Care Delivery surveys, Grand View Research digital health market data, and peer-reviewed literature from JAMA, Lancet Digital Health, Journal of the American College of Surgeons, and NPJ Digital Medicine.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Healthcare Extended Reality Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Hardware, Software, Services |

| Technologies Covered | Augmented Reality, Virtual Reality, Mixed Reality |

| Applications Covered | Surgery, Therapy, Education and Training, Rehabilitation, Pain Management, Others |

| End Users Covered | Hospitals, Clinics and Surgical Centers, Pharma Companies, Research Organizations and Diagnostic Laboratories, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AppliedVR, BioflightVR, CareAR (Xerox Holdings Corporation), FundamentalVR, Fusion VR, GigXR, Medicalholodeck AG, Microsoft Corporation, Osso VR Inc., PrecisionOS, XRHealth, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the healthcare extended reality market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global healthcare extended reality market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the healthcare extended reality industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Healthcare Extended Reality Market Report

The global healthcare XR market reached USD 9.8 Billion in 2025, driven by clinical adoption, regulatory clearances, and telehealth expansion.

The market is projected to reach USD 83.0 Billion by 2034, growing at a CAGR of 25.91% during 2026-2034, driven by AI integration, 5G-enabled remote surgery, mental health therapeutics, and expanding payer reimbursement.

Hardware leads with a 42.6% share in 2025, driven by enterprise HMD deployments from Microsoft HoloLens 2, Meta Quest Pro, and Apple Vision Pro in surgical planning, medical education, and rehabilitation applications.

Augmented Reality leads at 38.4% in 2025, driven by FDA-cleared surgical overlay applications including Augmedics Xvision, AccuVein, and Proprio Vision surgical navigation systems.

North America leads with 38.4% in 2025, supported by FDA Digital Health Center of Excellence regulatory leadership, NIH clinical research funding, and CMS telehealth reimbursement expansion.

Mixed Reality is the fastest-growing technology at ~28.4% CAGR through 2034, driven by surgical navigation platforms (Surgical Theater, Medivis SurgicalAR) combining real-world surgical fields with digital anatomical overlays.

Primary drivers include AI-XR integration for surgical decision support, VR therapeutic FDA clearances (AppliedVR RelieVRx), 5G-enabled remote surgery, post-COVID telehealth infrastructure, and government digital health investment exceeding USD 50 Billion globally.

Leading companies include AppliedVR, BioflightVR, CareAR (Xerox Holdings Corporation), FundamentalVR, Fusion VR, GigXR, Medicalholodeck AG, Microsoft Corporation, Osso VR Inc., PrecisionOS, and XRHealth.

FDA's Digital Health Center of Excellence (established 2020) has cleared 50+ XR medical devices and issued 200+ pre-submission meetings. AppliedVR's RelieVRx received the landmark first FDA authorization for a VR therapeutic in 2021.

Asia-Pacific (22.3%, 2025) is the fastest-growing region at ~28.1% CAGR, driven by China's USD 20 Billion digital health investment in its 14th Five-Year Plan, South Korea's USD 200 Million XR programme, and Japan's Society 5.0 healthcare strategy.

Key applications include surgical navigation and planning (AR), medical education simulation (VR), physical rehabilitation (MR), mental health therapy (VR), pain management (VR), and pharmaceutical training and clinical trials (AR/VR/MR).

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)