Healthy Snacks Market Size, Share, Trends, and Forecast by Product, Distribution Channel, and Region, 2026-2034

Global Healthy Snacks Market Size, Share, Trends & Forecast (2026-2034)

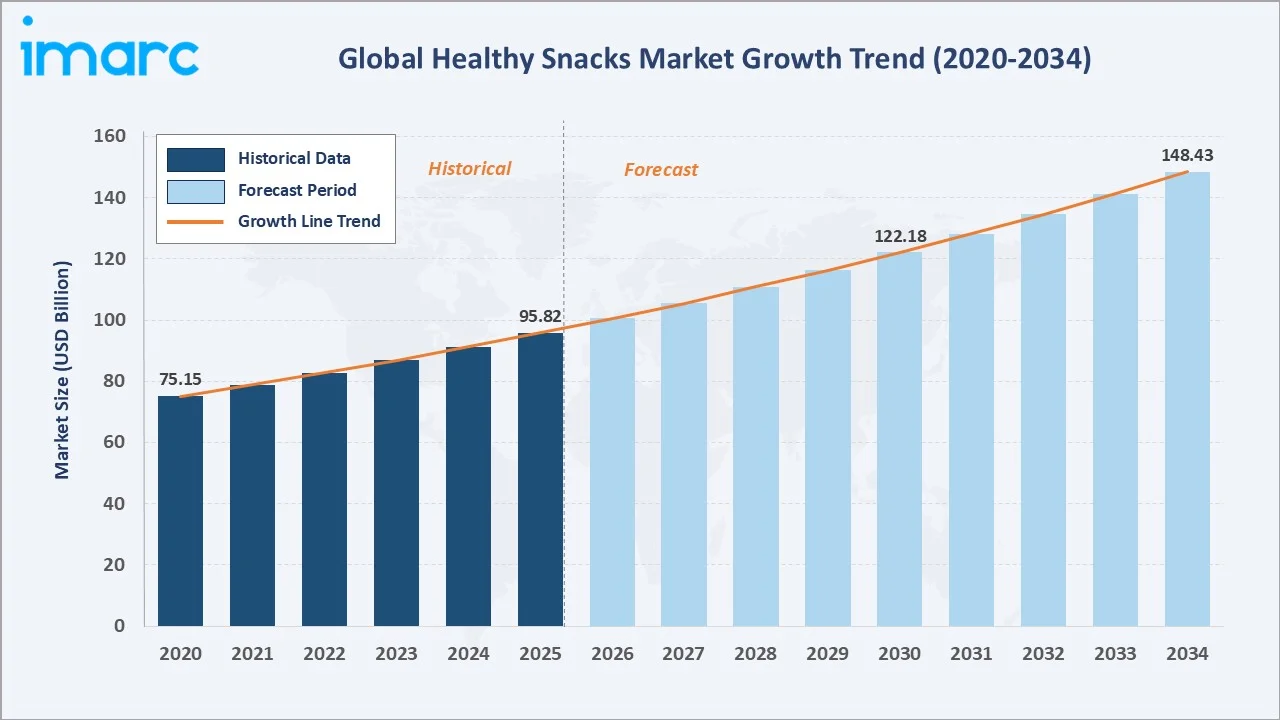

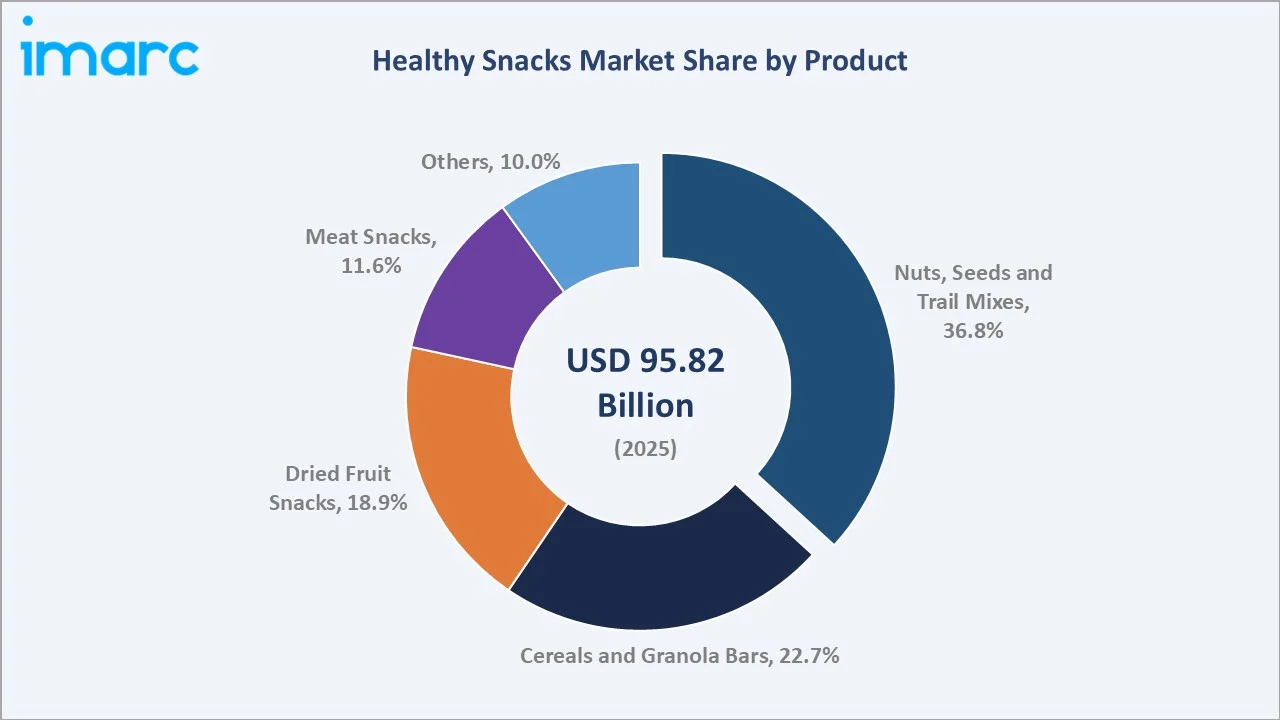

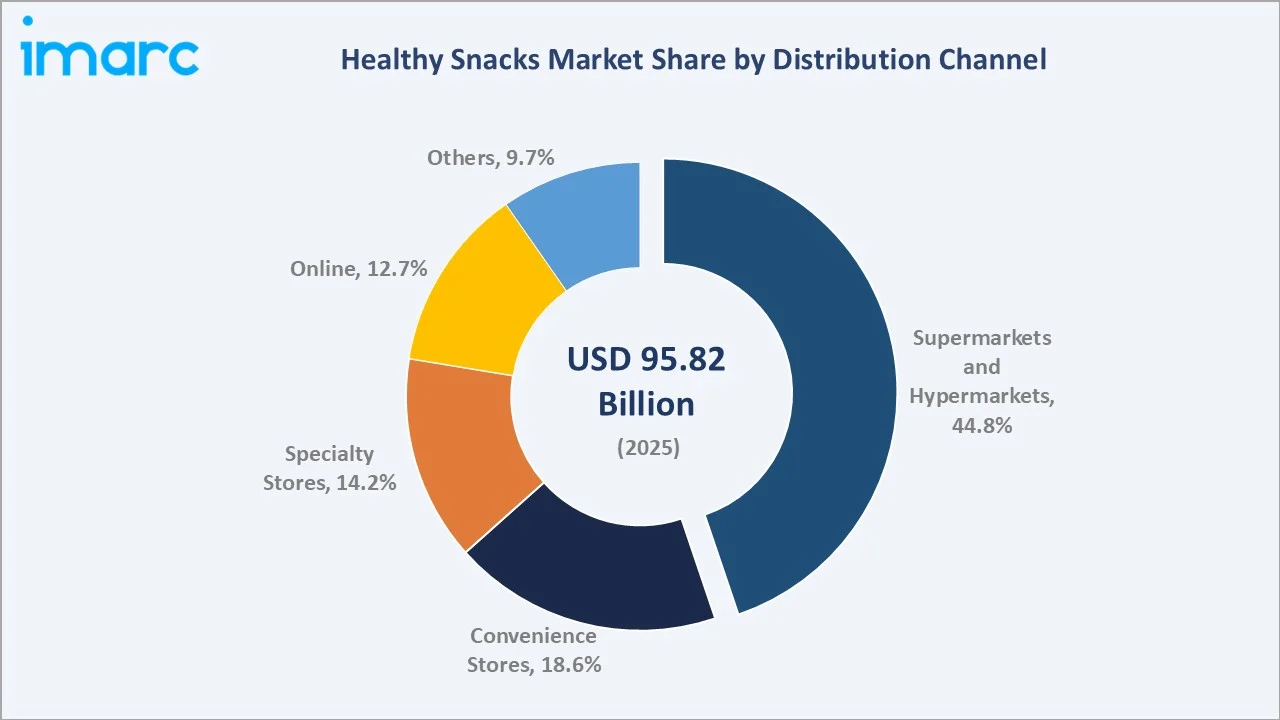

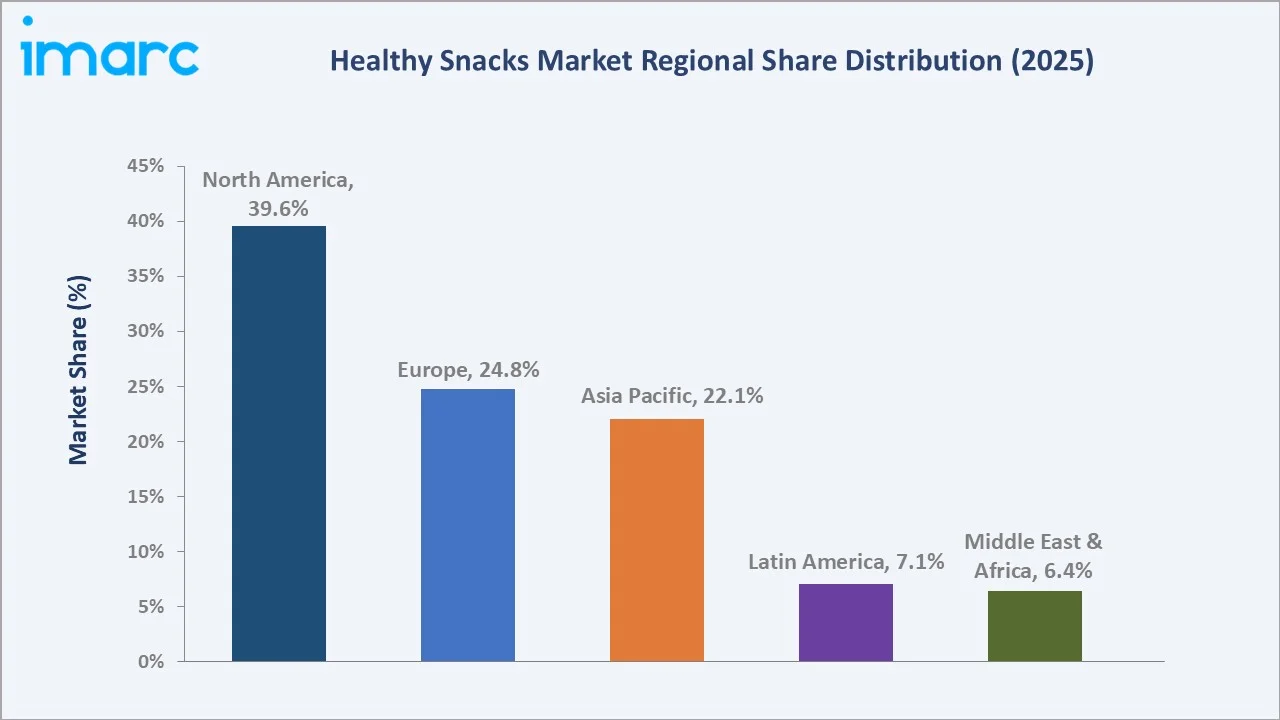

The global healthy snacks market size reached USD 95.82 Billion in 2025 and is projected to reach USD 148.43 Billion by 2034, exhibiting a CAGR of 4.98% during 2026-2034. Rising health consciousness, growing prevalence of chronic diseases, and surging demand for convenient, nutritious, and clean-label products are the primary forces driving market growth.

Nuts, Seeds and Trail Mixes dominate the product mix at 36.8% in 2025, while Supermarkets and Hypermarkets lead distribution at 44.8%. North America commands a dominant 39.6% regional share in 2025, reflecting its mature health-food culture and strong retail infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 95.82 Billion |

|

Forecast Market Size (2034) |

USD 148.43 Billion |

|

CAGR (2026-2034) |

4.98% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (39.6% share, 2025) |

|

Second Largest Region |

Europe (24.8% share, 2025) |

|

Leading Product |

Nuts, Seeds & Trail Mixes (36.8%, 2025) |

|

Leading Distribution Channel |

Supermarkets & Hypermarkets (44.8%, 2025) |

The global healthy snacks market growth trajectory from 2020 through 2034, with the historical expansion to USD 95.82 Billion in 2025, reflects consistent health-awareness-driven demand, while the forecast to USD 148.43 Billion captures accelerating plant-based innovation, functional food adoption, and emerging-market growth.

To get more information on this market, Request Sample

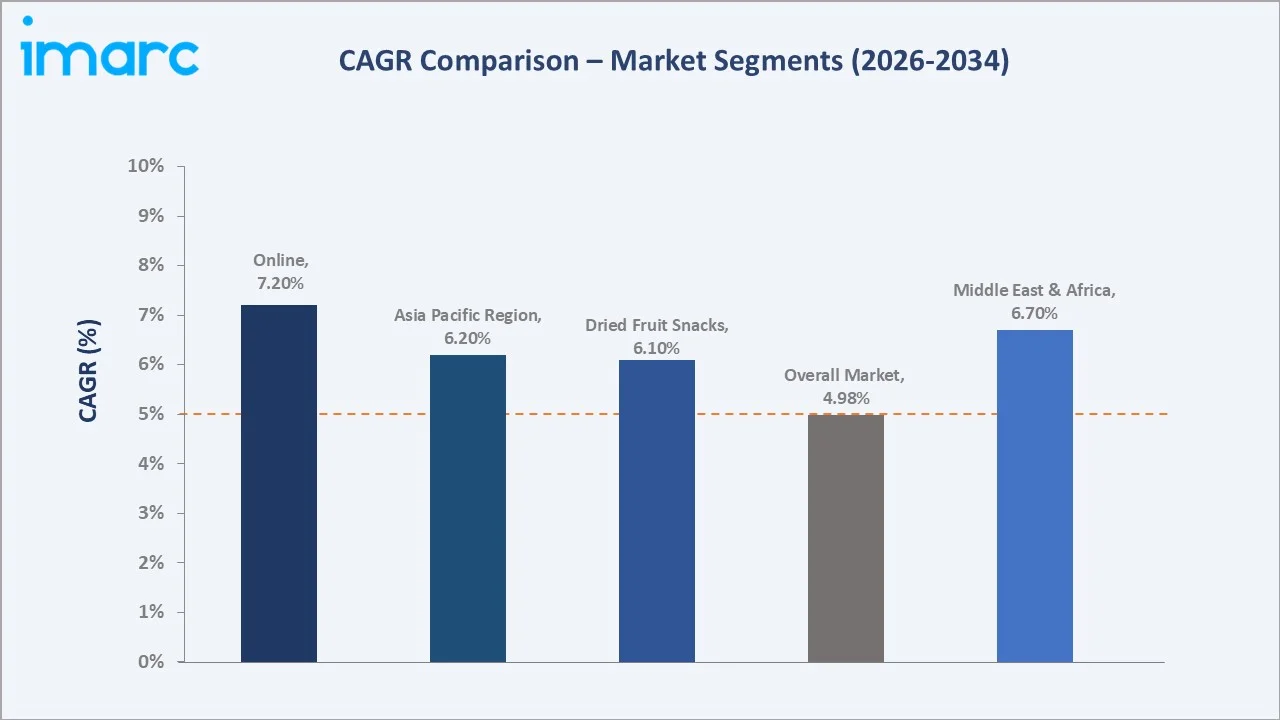

The CAGR trajectories across key product, distribution channel, and regional sub-segments, with Online at ~7.2% CAGR and Dried Fruit Snacks at ~6.1% CAGR, are among the fastest-growing categories within the global healthy snacks industry analysis through 2034.

Executive Summary

The global healthy snacks market is on a sustained growth trajectory from USD 95.82 Billion in 2025 to USD 148.43 Billion by 2034. Healthy snacks positioned across nuts, seeds, dried fruits, granola bars, and meat-based alternatives benefit from non-discretionary health-driven purchasing across all major demographics worldwide.

Nuts, Seeds and Trail Mixes dominate product type at 36.8% in 2025, valued for their nutrient density, portability, and shelf stability. Cereals and Granola Bars (22.7%) hold strong positioning as morning-meal replacements and active-lifestyle snacks. Dried Fruit Snacks (18.9%) are the fastest-growing product segment at ~6.1% CAGR through 2034.

Supermarkets and Hypermarkets lead distribution at 44.8% in 2025, driven by broad shelf visibility and promotional placement. Online channels (12.7%) represent the fastest-growing distribution path at ~7.2% CAGR, enabled by direct-to-consumer subscription models and digital-native brand expansion strategies.

North America's 39.6% dominance in 2025 reflects the region's mature health-food market, high per-capita health spending, and the presence of global snack innovators. Asia Pacific (22.1%) represents the fastest-growing region, driven by urbanization and rising disposable incomes across China, India, and Southeast Asian markets.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Nuts, Seeds & Trail Mixes – 36.8% share (2025) |

|

Fastest-Growing Product |

Dried Fruit Snacks – ~6.1% CAGR (2026-2034) |

|

Leading Distribution |

Supermarkets & Hypermarkets – 44.8% share (2025) |

|

Fastest Distribution Channel |

Online – ~7.2% CAGR (2026-2034) |

|

Leading Region |

North America – 39.6% share (2025) |

|

Second Largest Region |

Europe – 24.8% share (2025) |

|

Top Companies |

B&G Foods, Inc., Calbee, Danone, General Mills Inc., Mondelēz International |

Key Analytical Observations Expanding on the Above Data:

- Nuts, Seeds and Trail Mixes, with 36.8% in 2025, dominate because of their superior nutritional profile combining healthy fats, proteins, and fiber, making them the default specification for health-conscious on-the-go consumption across all major retail formats globally.

- Supermarkets and Hypermarkets, with 44.8% in 2025, lead because they provide the broadest product assortment, impulse-purchase placement, and promotional mechanics that drive trial and repeat purchase for mainstream healthy snack brands at scale.

- North America's 39.6% dominance in 2025 reflects entrenched consumer health culture, high average transaction values, and the presence of leading global healthy snack brands headquartered in the United States generating both domestic and international export volume.

- Europe, with 24.8% in 2025, benefits from strong regulatory frameworks supporting clean-label claims, a sophisticated consumer base with high nutritional awareness, and premiumization trends supporting higher average selling prices compared with other regions.

Global Healthy Snacks Market Overview

Healthy snacks are food products consumed between meals that deliver meaningful nutritional value including proteins, healthy fats, dietary fiber, vitamins, and minerals, while minimising artificial additives, excessive sugar, refined carbohydrates, and trans fats. Product categories span nuts, seeds, trail mixes, dried fruits, granola bars, meat snacks, and plant-based alternatives across multiple packaging formats.

The global ecosystem integrates agricultural commodity producers, specialty ingredient suppliers, food manufacturers, contract packers, co-manufacturers, specialty and mainstream retailers, e-commerce platforms, and diverse end-use consumer segments spanning children, athletes, office workers, seniors, and diet-specific communities.

Market Dynamics

To evaluate market opportunities, Request Sample

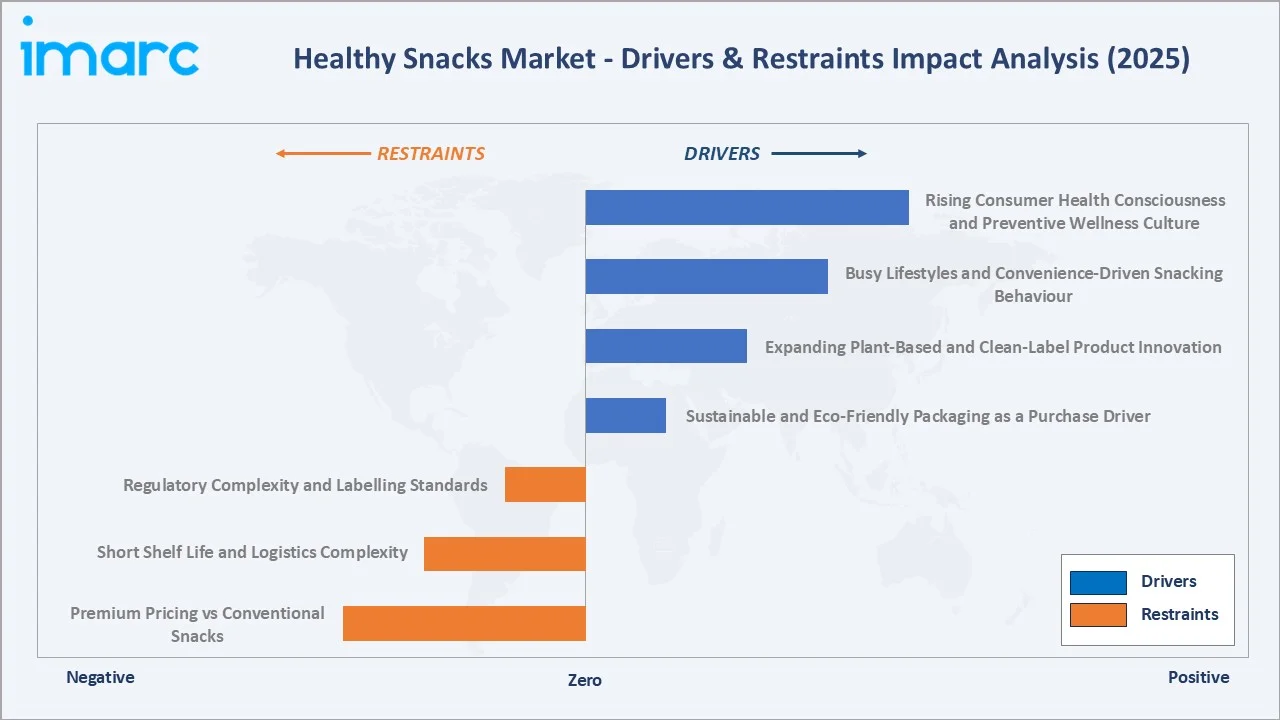

Market Drivers

- Rising Consumer Health Consciousness and Preventive Wellness Culture: The escalating global awareness of diet-related chronic diseases, including cardiovascular conditions, diabetes, and obesity, is compelling consumers to scrutinise nutritional labels and prioritise snacks with functional benefits. This is translating into increased consumption of nutritious snack products that offer multiple health benefits, including enhanced bone health, regulated blood sugar levels, and reduced risk of long-term lifestyle diseases.

- Busy Lifestyles and Convenience-Driven Snacking Behaviour: Rapid urbanisation and increasingly demanding work schedules have transformed eating patterns globally, with snacking replacing traditional meals for a significant proportion of consumers. Portable, individually portioned healthy snacks with resealable packaging addresses the need for convenient, on-the-go nutrition without any preparation requirements.

- Expanding Plant-Based and Clean-Label Product Innovation: The global plant-based food market expansion has catalysed significant innovation in healthy snack formulations, with manufacturers deploying chickpeas, lentils, quinoa, and pea protein as functional ingredients that deliver satiety alongside clean nutritional profiles acceptable to vegan, vegetarian, and flexitarian consumer segments worldwide.

- Sustainable and Eco-Friendly Packaging as a Purchase Driver: Environmentally conscious consumers, particularly Millennials and Generation Z, actively prefer healthy snack brands utilising compostable, recyclable, or minimal-plastic packaging. Brands investing in sustainable packaging report measurable improvements in brand equity, consumer loyalty, and repeat purchase rates across premium retail channels.

Market Restraints

- Premium Pricing vs. Conventional Snack Alternatives: Healthy snacks command significant price premiums over conventional alternatives, with organic and clean-label products typically priced 30-60% higher than standard equivalents. Price sensitivity among lower-income consumer segments and in developing markets constrains market penetration beyond premium and upper-middle-income consumer cohorts.

- Short Shelf Life and Logistics Complexity: Natural, minimally processed healthy snacks, particularly those containing nuts, seeds, and dried fruits without preservatives, face accelerated rancidity and oxidation challenges that limit shelf life versus conventional snacks, increasing inventory management complexity and overall distribution cost structures for manufacturers and retailers.

- Regulatory Complexity and Evolving Labelling Standards: Divergent national and regional regulatory frameworks governing health claims, organic certification, and nutritional labelling create significant compliance overhead for manufacturers seeking to operate across multiple markets, particularly where regulatory requirements differ substantially between major trading blocks.

Market Opportunities

- Functional Snacks with Immune and Gut-Health Benefits: Consumer focus on immunity, gut health, and mental wellness has created substantial opportunity for snacks fortified with probiotics, prebiotics, adaptogens, and botanical extracts. Brands delivering clinically substantiated functional benefits command meaningful price premiums and stronger consumer loyalty compared with mainstream healthy snack alternatives.

- Emerging Market Expansion in Asia Pacific and Latin America: Rising middle-class populations in India, China, Brazil, and Southeast Asian markets are exhibiting accelerating healthy snack adoption, supported by expanding modern retail infrastructure, growing health consciousness, and improving logistics networks that enable efficient distribution of premium healthy snack products.

Market Challenges

- Ingredient Cost Volatility and Supply Chain Disruptions: Key healthy snack ingredients including tree nuts, chia seeds, quinoa, and cacao face significant price volatility driven by climate variability, crop failures, and geopolitical disruptions. This directly impacts cost structures for manufacturers and can compress margins or require consumer price increases that weaken volume demand.

- Consumer Scepticism Regarding Health Claim Authenticity: Growing consumer awareness of greenwashing and health-washing practices has increased scrutiny of product claims, requiring manufacturers to provide transparent, scientifically substantiated evidence for nutritional benefits. Products failing authenticity scrutiny face significant reputational and commercial consequences in social media-amplified markets.

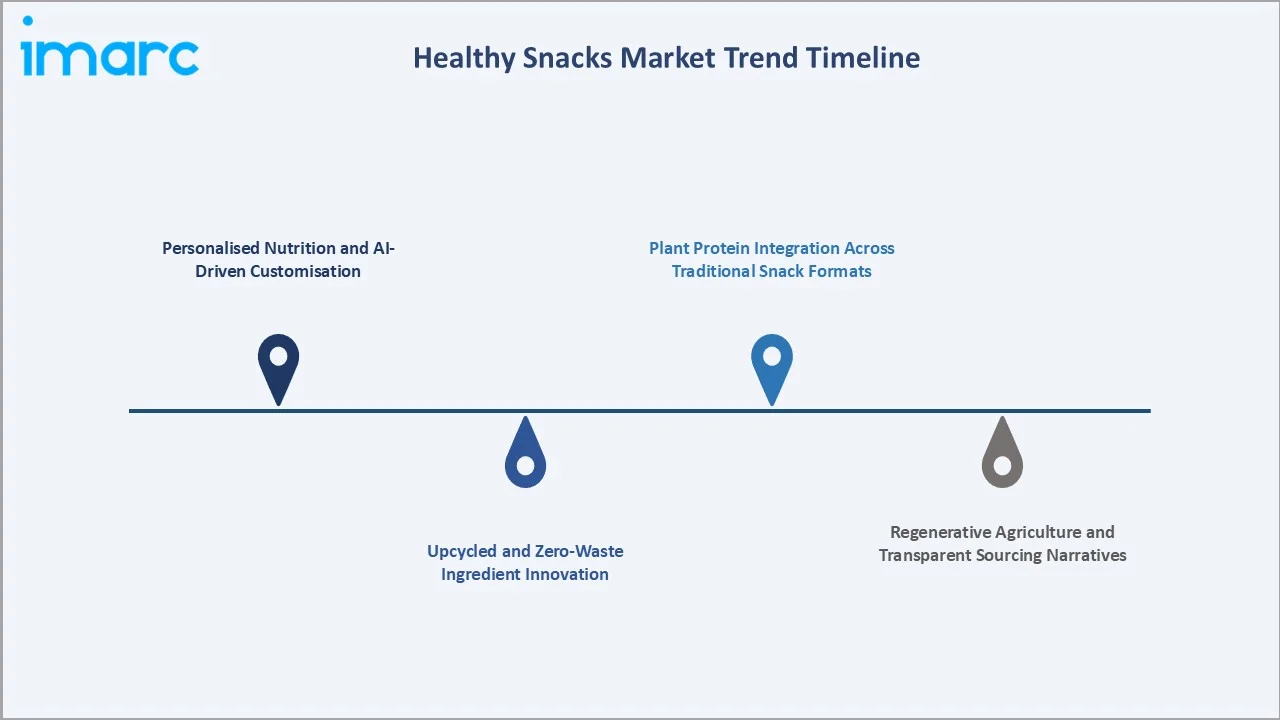

Emerging Market Trends

1. Personalised Nutrition and AI-Driven Product Customisation

Advances in nutrigenomics, microbiome analysis, and AI-powered dietary profiling are enabling brands to offer personalised healthy snack formulations matched to individual health goals, dietary restrictions, and metabolic profiles. Subscription platforms leveraging consumer health data are achieving retention rates significantly above category averages.

2. Plant Protein Integration Across Traditional Snack Formats

Plant-based protein ingredients including pea protein, fava bean, hemp seed, and watermelon seed are being integrated into traditionally indulgent snack formats including crackers, cookies, and chips, enabling brands to capture both health-conscious and mainstream consumer segments simultaneously within existing retail fixture positions.

3. Regenerative Agriculture and Transparent Sourcing Narratives

Consumer demand for supply chain transparency and positive environmental impact is driving leading healthy snack brands to adopt regenerative agriculture sourcing commitments and blockchain-enabled ingredient traceability that converts sourcing practices into compelling brand differentiation narratives at point of sale.

4. Upcycled and Zero-Waste Ingredient Innovation

Regulatory support for upcycled food certification and growing consumer receptivity to snacks made from rescued agricultural by-products is creating a nascent but rapidly expanding market segment aligned with circular economy principles, attracting both venture capital investment and strategic interest from established CPG companies.

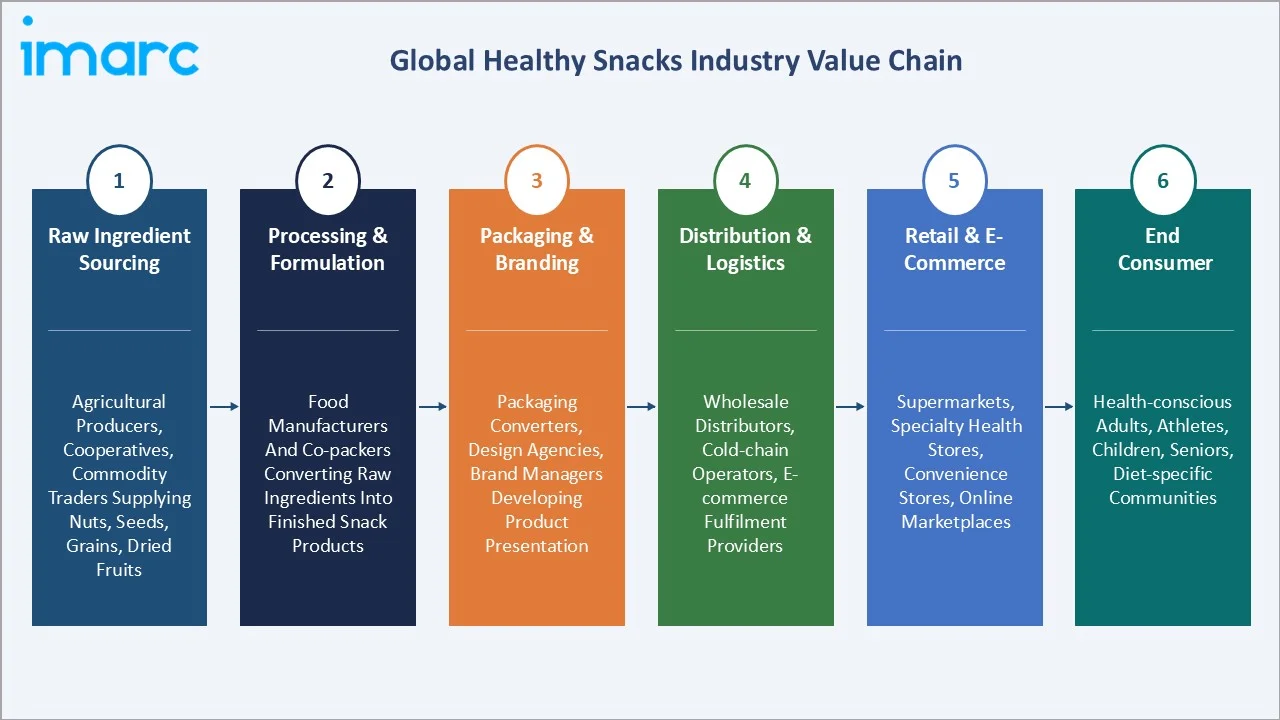

Industry Value Chain Analysis

The healthy snacks value chain spans six stages from raw ingredient sourcing through end-consumer delivery. Processing, formulation, and branding capture the highest value-add margins, while distribution logistics and retailer margin structures represent the most significant cost-management challenges for branded manufacturers.

|

Stage |

Description |

|

Raw Ingredient Sourcing |

Agricultural producers, cooperatives, and commodity traders supplying nuts, seeds, grains, and dried fruits |

|

Processing & Formulation |

Food manufacturers and co-packers converting raw ingredients into finished snack products |

|

Packaging & Branding |

Packaging converters, design agencies, and brand managers developing consumer-facing product presentation |

|

Distribution & Logistics |

Wholesale distributors, cold-chain operators, and e-commerce fulfilment providers |

|

Retail & E-Commerce |

Supermarkets, specialty health stores, convenience stores, and online marketplaces |

|

End Consumer |

Health-conscious adults, athletes, children, seniors, and diet-specific consumer communities |

Technology Landscape in the Healthy Snacks Industry

Advanced Food Processing: Air Frying, Extrusion, and Freeze-Drying

Modern processing technologies enable manufacturers to produce healthy snacks with optimised textural profiles and preserved nutritional content. Air-frying reduces fat content significantly versus traditional oil-frying while maintaining crunch. Freeze-drying preserves the vast majority of original nutritional value in fruit and vegetable snacks, enabling premium-priced positioning across specialty retail channels.

Functional Ingredient Innovation: Probiotics, Adaptogens, and Superfoods

Microencapsulation technology enables stable incorporation of heat-sensitive probiotics into baked and extruded snack formats with guaranteed viable cell counts at point of consumption. Adaptogen standardisation advances allow consistent inclusion of ashwagandha, lion's mane, and rhodiola extracts with defined bioactive compound concentrations supporting on-pack claims.

Sustainable Packaging Technology: Compostable and Active Barrier Solutions

Compostable flexible packaging utilising bio-based materials and cellulose-based barrier coatings is achieving commercially viable oxygen transmission rates for nut and seed snack applications. Active packaging incorporating oxygen scavengers and moisture management systems is extending shelf life without preservative additions, addressing both sustainability and quality objectives.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Nuts, Seeds and Trail Mixes |

36.8% |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

44.8% |

2025 |

|

Region |

North America |

39.6% |

2025 |

By Product

Nuts, Seeds and Trail Mixes commands a 36.8% majority share in 2025 owing to their exceptional nutritional density, natural protein and healthy fat content, versatile snacking occasions from office consumption to athletic recovery, and a strong scientific evidence base supporting cardiovascular and metabolic health benefits across consumer demographics.

To access detailed market analysis, Request Sample

Cereals and Granola Bars at 22.7% in 2025 serve the breakfast replacement and active lifestyle snacking occasion, with formulation innovations incorporating whole grains, seeds, and plant proteins commanding premium positioning. Dried Fruit Snacks (18.9%) is the fastest-growing segment at ~6.1% CAGR, driven by clean-label appeal and natural sugar messaging.

By Distribution Channel

Supermarkets and Hypermarkets dominate the distribution segment at 44.8% in 2025, representing the most critical retailer relationship for healthy snack brands. Shelf placement, in-store promotional support, and nutritional end-cap positioning within this channel drive the majority of trial and repeat purchase for mainstream healthy snack brands globally.

Convenience Stores (18.6%) serve the impulse and on-the-go consumption occasion, with single-serve packaging formats optimised for this channel generating premium per-unit pricing. Specialty Stores (14.2%) including health food chains and organic retailers provide the critical innovation incubation environment for premium healthy snack brands.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

39.6% |

Mature health-food culture; high disposable income; strong premium brand ecosystem; developed retail infrastructure |

|

Europe |

24.8% |

Clean-label regulatory framework; organic certification demand; premiumisation trend; strong private-label growth |

|

Asia Pacific |

22.1% |

Rising middle class; urbanisation; expanding modern retail; growing health and wellness awareness |

|

Latin America |

7.1% |

Expanding urban middle class; modern retail development; natural ingredient tradition; growing health awareness |

|

Middle East & Africa |

6.4% |

Young health-conscious population; premium retail expansion; urbanisation; rising disposable incomes |

North America's 39.6% market dominance in 2025 reflects the most advanced healthy snack consumer culture globally. The region benefits from a highly developed specialty retail network, a robust functional food regulatory framework, and world-leading healthy snack brand portfolios that continuously drive category innovation and consumer adoption.

Europe, with 24.8% in 2025, benefits from stringent food safety regulations that reinforce consumer trust in labelled health claims, a sophisticated retail market with advanced private-label healthy snack programmes, and strong organic certification infrastructure that supports premium pricing across the region's diverse consumer markets.

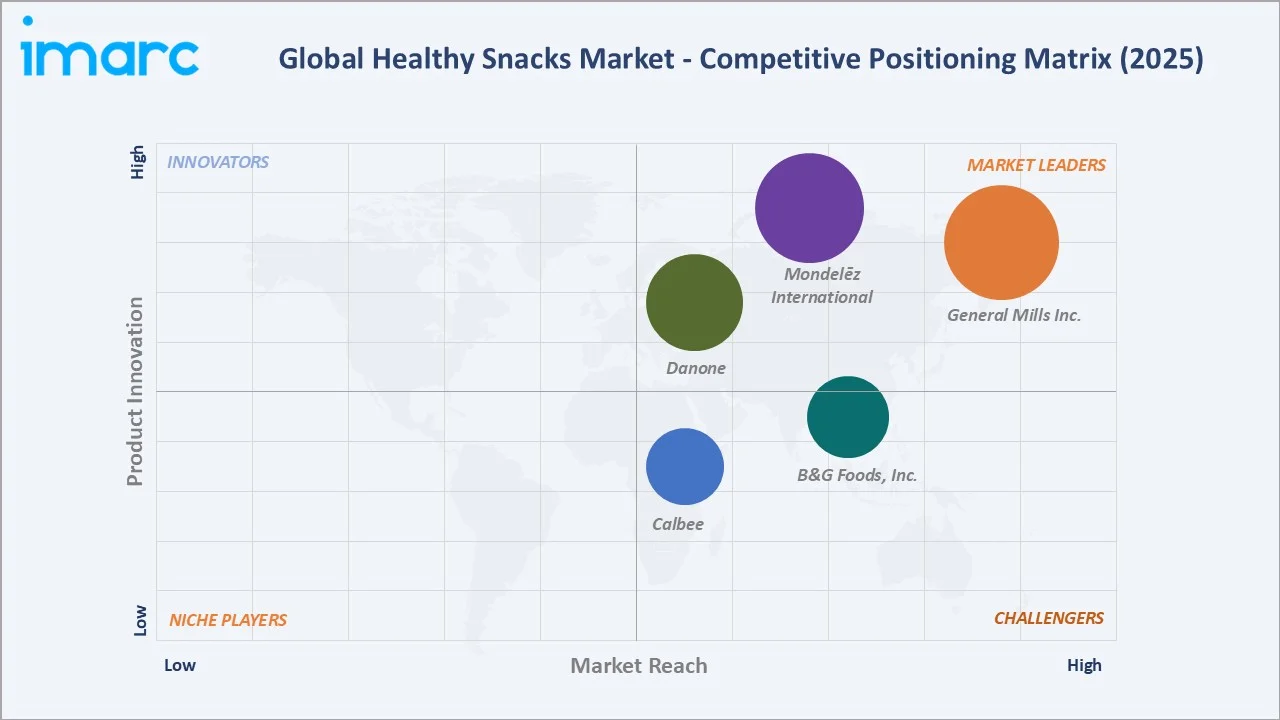

Competitive Landscape

The global healthy snacks market is moderately concentrated at the upper tier, with large multinational food corporations holding dominant positions through extensive brand portfolios, global distribution networks, and significant R&D investment capacity. A fragmented mid-tier of regional and niche brands competes on ingredient specificity, certification credentials, and direct-to-consumer digital engagement.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

B&G Foods, Inc. |

Pirate's Booty, Old London |

Challenger |

US market; better-for-you mainstream; portfolio diversification |

|

Calbee |

Harvest Snaps |

Challenger |

Japan and APAC leader; vegetable-based; better-for-you crisps |

|

Danone |

Activia, Oikos Pro |

Leader |

Gut-health and protein snack positioning; global nutrition focus |

|

General Mills Inc. |

Nature Valley, LARABAR, Fiber One |

Leader |

US and global granola bar leader; brand portfolio breadth |

|

Mondelēz International |

BelVita, Good Thins, Clif Bar |

Leader |

Global better-for-you biscuit and bar leader; emerging markets |

Key players include B&G Foods, Inc., Calbee, Danone, General Mills Inc., Mondelēz International, and others.

Key Company Profiles

General Mills Inc.

General Mills, Inc. is one of the world's leading food companies, headquartered in Golden Valley, Minneapolis, Minnesota, USA. The company operates a comprehensive portfolio of healthy snack brands including Nature Valley granola bars, energy bars, and Fiber One snack bars.

- Product Portfolio: Offers nature valley, larabar, fiber one, and others.

- Recent Developments: In December 2024, General Mills expanded its protein-focused breakfast portfolio with the launch of Cheerios Protein, introducing a new cereal range aimed at consumers seeking convenient, high-protein food options. The new offering delivers added protein content while maintaining the brand’s signature taste and texture.

- Strategic Focus: General Mills' healthy snacks strategy leverages its unmatched retail distribution infrastructure to scale better-for-you brands nationally and internationally, while investing in emerging functional ingredient platforms aligned with evolving consumer wellness priorities.

Mondelēz International

Mondelēz International is a global snacking powerhouse headquartered in Chicago, Illinois, USA. Mondelēz has assembled one of the broadest better-for-you snacking portfolios among global CPG companies.

- Product Portfolio: Offers belvita, good thins, clif bar, and others.

- Recent Developments: In January 2025, Mondelēz International expanded its belVita portfolio with the launch of belVita Energy Snack Bites, introducing a new range of soft-baked, bite-sized snacks designed for mid-morning consumption. The new product line aims to cater to consumers seeking convenient and wholesome snacking options during busy routines.

- Strategic Focus: Mondelēz’s strategy focuses on building its better-for-you snacking portfolio through organic growth of Clif Bar, BelVita, and Good Thins, supported by global distribution advantages that accelerate international expansion of brands proven in the North American market.

Market Concentration Analysis

The global healthy snacks market is moderately concentrated at the global level, with the top five multinational companies collectively holding approximately 25-30% of total global revenue. The remaining market share is distributed across hundreds of regional, national, and niche brands operating in specific product categories or geographies.

Consolidation through mergers and acquisitions is a defining feature of the competitive landscape, with large CPG companies systematically acquiring innovative healthy snack brands once they achieve sufficient scale. This established acquisition path creates clear value creation incentives for healthy snack entrepreneurs and venture investors targeting the category.

Investment & Growth Opportunities

Fastest-Growing Segments

Dried Fruit Snacks at ~6.1% CAGR through 2034 represent the highest-growth product segment, driven by clean-label positioning, no-added-sugar formulation, and portability characteristics matching modern on-the-go consumption patterns. Online distribution at ~7.2% CAGR is the fastest-growing channel, enabling direct-to-consumer economics and subscription-based growth.

Emerging Markets

Asia Pacific at ~6.2% CAGR is the fastest-growing region for healthy snacks through 2034. India's expanding urban middle class, Southeast Asia's modern retail infrastructure development, and China's premium food market maturation are creating collectively significant incremental market volume from a rapidly growing consumer base.

Venture & Investment Trends

Venture capital investment in healthy snack start-ups remains robust globally, targeting brands with demonstrated direct-to-consumer traction in functional, plant-based, and personalised nutrition categories. Strategic acquirers from large CPG companies continue to prioritise healthy snack bolt-on acquisitions with strong brand equity and differentiated positioning.

Future Market Outlook (2026-2034)

The global healthy snacks market is forecast to expand from USD 95.82 Billion in 2025 to USD 148.43 Billion by 2034 at a CAGR of 4.98%, adding USD 52.61 Billion in incremental annual market value over the forecast period. This consistent, sustained growth reflects the market's health-awareness-driven, structurally supported demand characteristics globally.

Three technological forces will most significantly shape the healthy snacks landscape through 2034: AI-powered personalised nutrition enabling mass-customised snack subscription services; precision fermentation delivering next-generation protein and fat ingredients with superior nutritional profiles; and blockchain-enabled supply chain transparency converting ethical sourcing into verifiable consumer-facing claims and competitive brand differentiation.

Research Methodology

Primary Research

Primary research encompassed over 60 structured interviews in 2024-2025 with healthy snack industry stakeholders, including senior brand managers, retail buyers, nutritionists, ingredient suppliers, and e-commerce platform operators. Primary data validated market sizing, product and distribution channel segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include USDA Economic Research Service food consumption data, IRI and Nielsen retail scan data, Mintel Global New Products Database, Euromonitor International packaged food market reports, FAO commodity production statistics, and trade publications including Food Business News, Food Navigator, and Progressive Grocer.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating consumer expenditure data, retail channel dynamics, demographic health trend indices, and historical market evolution patterns with scenario analysis covering base, optimistic, and conservative cases.

Healthy Snacks Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Nuts, Seeds and Trail Mixes, Dried Fruit Snacks, Cereals and Granola Bars, Meat Snacks, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | B&G Foods Inc., Calbee, Danone, General Mills Inc., Mondelēz International, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the healthy snacks market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global healthy snacks market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the healthy snacks industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Healthy Snacks Market Report

The global healthy snacks market reached USD 95.82 Billion in 2025, reflecting consistent demand driven by rising health consciousness, busy lifestyles, and growing chronic disease prevalence worldwide.

The market is projected to reach USD 148.43 Billion by 2034, growing at a CAGR of 4.98% during 2026-2034, driven by plant-based innovation, online channel expansion, and emerging market growth.

Nuts, Seeds and Trail Mixes leads with a 36.8% product share in 2025, valued for their superior nutritional density, natural ingredient profiles, and broad consumption occasion applicability globally.

Supermarkets and Hypermarkets lead at 44.8% in 2025, providing the broadest product assortment, promotional support, and consumer traffic for healthy snack brand building at scale.

North America commands a dominant 39.6% market share in 2025, driven by the world's most mature health-food consumer culture, high per-capita health spending, and a leading branded innovation ecosystem.

Online is the fastest-growing distribution channel at ~7.2% CAGR through 2034, driven by direct-to-consumer subscription platforms, marketplace listings, and digital-native healthy snack brand expansion.

Leading companies include B&G Foods, Inc., Calbee, Danone, General Mills Inc., Mondelēz International, among others.

Key benefits include enhanced cardiovascular health, improved blood sugar regulation, weight management support, gut microbiome improvement, and reduced risk of chronic diseases including diabetes, obesity, and cancer.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)