Hematology Analyzers and Reagents Market Report by Product (Haematology, Haemostasis, Immunohaematology), Usage Type (Standalone, Point-of-Care), Price Range (Low Range, Mid-Range, High Range), Application (Haemorrhagic Conditions, Infection-Related Conditions, Immune System-Related Conditions, Blood Cancer, Anaemia), End User (Commercial Service Providers, Hospital Laboratories, Research and Academic Institutes, and Others), and Region 2026-2034

Hematology Analyzers and Reagents Market Size:

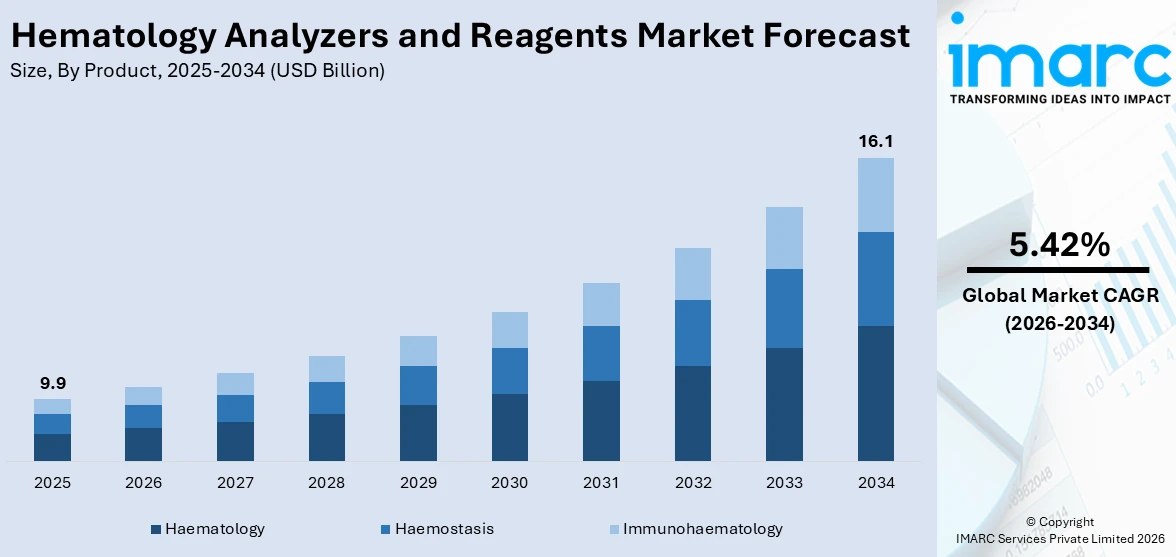

The global hematology analyzers and reagents market size reached USD 9.9 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 16.1 Billion by 2034, exhibiting a growth rate (CAGR) of 5.42% during 2026-2034. The market is propelled by the rising incidence of blood disorders and chronic illnesses, significant technological advancements in hematology analyzers, rising geriatric population globally, significantly rising demand for point-of-care (POC) diagnostics, and integration of artificial intelligence (AI) and machine learning (ML) in the diagnostics.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 9.9 Billion |

|

Market Forecast in 2034

|

USD 16.1 Billion |

| Market Growth Rate 2026-2034 | 5.42% |

Hematology Analyzers and Reagents Market Analysis:

- Major Market Drivers: Some of the major market drivers include the rising number of individuals diagnosed with blood disorders and chronic diseases, significant technological developments, and growing demand for point-of-care testing.

- Key Market Trends: The inclusion of artificial intelligence (AI) and machine learning (ML) in the diagnostics, increasing demand for automated and point-of-care testing, and rapid growth of customized medicine and personalized therapies, are some of the key market trends.

- Geographical Trends: North America leads the industry on account of the rising incidence of non-communicable diseases, robust healthcare infrastructure, and strong competitive presence within the industry.

- Competitive Landscape: Abbott Laboratories, Bio-Rad Laboratories Inc., Boule Diagnostics, Danaher Corporation, Diatron MI PLC (Stratec SE), EKF Diagnostics Holdings plc, Heska Corporation, Horiba Ltd., Mindray Medical International Limited, Nihon Kohden Corporation, Siemens, Sinnowa Medical Science & Technology Co. Ltd., are among some of the key players in the hematology analyzers and reagents industry.

- Challenges and Opportunities: Hematology analyzers and reagents market opportunities include entry into new untapped regions and introduction of next-generation analyzers with improves qualities and reduced operational costs. Whereas, challenges of the market include high cost of advanced hematology analyzers and reagents and strict regulatory requirements.

To get more information on this market Request Sample

Hematology Analyzers and Reagents Market Trends:

Rising Incidence of Blood Related Diseases and Chronic Illnesses:

The rising number of individuals diagnosed with blood disorders and chronic illnesses is majorly driving the market. Blood disorders such as lymphoma, leukemia, and hemophilia are highly prevalent on account of numerous factors including aging population, genetic predispositions, and lifestyle changes. For instance, NATIONAL LIBRARY OF MEDICINE, approximately 24.8% individuals are diagnosed with anemia, which translates to 1.62 billion individuals globally. Other than this, the increasing prevalence of chronic illnesses including cardiovascular diseases and diabetes are also propelling the market growth. As per a report published by the INTERNATIONAL DIABETES FOUNDATION, by the year 2045 1 in 8 individuals are expected to suffer from diabetes which translates to 783 million individuals. In order to manage these illnesses precisely, the demand for advanced hematology analyzers and reagents is significantly rising.

Increasing Geriatric Population:

The rising geriatric population globally is further leading to a positive market outlook. Elderly individuals are more prone to a wide range of health conditions, such as chronic diseases, blood disorders which leads to a rising requirement for regular blood testing for diagnosis and monitoring. According to the WORLD HEALTH ORGANIZATION (WHO), between 2016 and 2050, the global population with the age of 60 years and above will approximately double from 12% to 22%. This rising age group is leading to a rise in the demand for healthcare services, such as diagnostic testing. These devices play a major contribution in the early diagnosis and management of age-related health issues, thereby leading to a hematology analyzers and reagents market growth.

Rising Demand for Point-of-Care (POC) Diagnostics:

The increasing demand for point-of-care (POC) diagnostics is a major factor leading to a rise in the hematology analyzers and reagents demand. POC diagnostics is the medical testing conducted at or nearby the site of patient are, offering immediate results that can lead to speedy clinical decisions. The advantages such as convenience and speed offered by the POC are particularly useful in settings including intensive care units, emergency rooms, and remote or resource-limited areas where there is restricted access to central laboratory facilities. According to the IMARC GROUP, the point-of-care (POC) diagnostics market has reached US$ 49.2 Billion in 2023, and is expected to reach US$ 99.5 Billion in 2032, exhibiting a CAGR of 7.9% during 2024-2032.

Hematology Analyzers and Reagents Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product, usage type, price range, application, and end user.

Breakup by Product:

- Haematology

- Haemostasis

- Immunohaematology

Haematology accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the product. This includes haematology, haemostasis, and immunohaematology. According to the report, haematology represented the largest segment.

Hematology represents the largest segment on account of its ability for diagnosing numerous diseases, such as infections, anemia, leukemia, and other blood disorders. These tests are crucial for regular health check-ups, diagnosing diseases, and tracking treatment progress, making them vital in medical care. The rising number of chronic illnesses and the growing elderly population contributed to the hematology analyzers and reagents revenue. As more individuals need these tests for ongoing health issues and routine checks, the importance of haematology and market share continue to grow. As per a report published by the IMARC GROUP, the global hematology analyzers market size has already reached US$ 6.8 Billion in 2023 and is projected to reach US$ 13.1 Billion by 2032, exhibiting a CAGR of 7.3% during 2024-2032.

Breakup by Usage Type:

- Standalone

- Point-of-Care

Standalone holds the largest share in the industry

A detailed breakup and analysis of the market based on the usage type have also been provided in the report. This includes standalone and point-of-care. According to the report, standalone accounted for the largest market share.

Standalone hematology analyzers market holds the largest hematology analyzers and reagents market share as they are versatile, easy to use, and can perform multiple tests without an extra equipment. Hospitals, clinics, and diagnostic labs prefer them for their high accuracy and reliability in routine blood tests, making them essential for daily operations. Additionally, standalone devices are highly economical and possess lower maintenance requirements, which further drives their widespread adoption. Their ability to offer quick and reliable results without the need for additional instruments makes them a preferred choice in numerous medical settings.

Breakup by Price Range:

- Low Range

- Mid-Range

- High Range

Low range represents the leading market segment

The hematology analyzers and reagents market report has provided a detailed breakup and analysis of the market based on the price range. This includes low range, mid-range, and high range. According to the report, low range represented the largest segment.

The low range segment dominates the market as it is one of the most accessible and affordable option for many healthcare facilities, such as small clinics, outpatient centers, and rural hospitals. These medical settings mostly function on tight budgets and need economical yet reliable diagnostic tools. Low-range hematology analyzers are user-friendly and require minimal maintenance, making them ideal for settings with limited technical expertise. This widespread demand ensures that even those with financial constraints can access essential diagnostic services. Moreover, the rising prevalence of hematological malignancies are also creating a positive hematology analyzers and reagents market outlook. By the year 2030, the incidence rates per 100,000 individuals are projected to rise to 0.045 for multiple myeloma, 0.016 for leukemia, and 0.012 for non-Hodgkin lymphoma.

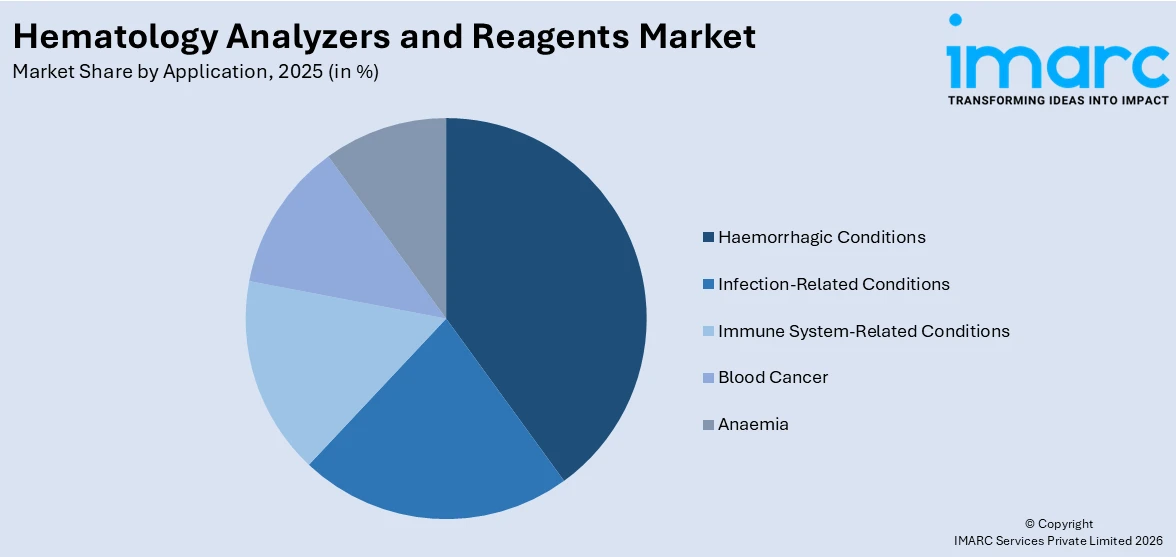

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Haemorrhagic Conditions

- Infection-Related Conditions

- Immune System-Related Conditions

- Blood Cancer

- Anaemia

Haemorrhagic Conditions exhibits a clear dominance in the market

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes haemorrhagic conditions, infection-related conditions, immune system-related conditions, blood cancer, and anaemia. According to the report, haemorrhagic conditions accounted for the largest market share.

Hemorrhagic conditions, such as hemophilia, thrombocytopenia, and other bleeding disorders, dominate the hematology analyzers and reagents industry as they are extremely prevalent and require constant monitoring. Individuals with these conditions need frequent blood tests to check clotting times, platelet counts, and other vital parameters. This necessity drives the demand for advanced hematology analyzers. Moreover, as the population ages, the incidence of these hemorrhagic conditions increases. Older adults are more prone to developing such disorders, on account of which they need regular blood testing in order to regulate their health effectively. This demographic shift is significantly contributing to the growth of the market.

Breakup by End User:

- Commercial Service Providers

- Hospital Laboratories

- Research and Academic Institutes

- Others

Commercial service providers dominate the market

The report has provided a detailed breakup and analysis of the market based on the end user. This includes commercial service providers, hospital laboratories, research and academic institutes, and others. According to the report, commercial service providers represented the largest segment.

Commercial service providers emerged as the largest segment in this market. These providers include independent diagnostic laboratories and large commercial lab chains that offer a wide range of blood testing services. The dominance of commercial service providers can be attributed to several factors such as, these entities often have wide resources to invest in advanced hematology analyzers and reagents, allowing them to provide good-quality and efficient testing services. They cater to a broad consumer base, including individual patients, clinics, and smaller labs that may outsource their complicated testing needs, thereby creating a positive hematology analyzers and reagents market overview.

Breakup by Region:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest hematology and analyzers and reagents market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

The North America hematology analyzers and reagents market is being propelled by several key factors. The rising demand for personalized medicine and companion diagnostics is playing a vital role in the growth of the market. Personalized medicine allows the customization of treatments to individual patients based on their genetic profiles, which needs precise and comprehensive diagnostic tools. Hematology analyzers are essential in this respect as they offer detailed information about the blood of a patient, helping doctors make informed decisions about treatment plans. Moreover, the region possesses a high per capita healthcare spending, thereby leading to significant investments in medical technologies and diagnostics. According to a report, NATIONAL HEALTH EXPENDTIURE (NHE) increased by 4.1% to US$ 4.5 Trillion in 2022, or US$ 13,493 per person, thereby accounting for 17.3% of Gross Domestic Product (GDP).

Competitive Landscape:

- The market research report has also provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the major market players in the hematology analyzers and reagents industry include Abbott Laboratories, Bio-Rad Laboratories Inc., Boule Diagnostics, Danaher Corporation, Diatron MI PLC (Stratec SE), EKF Diagnostics Holdings plc, Heska Corporation, Horiba Ltd., Mindray Medical International Limited, Nihon Kohden Corporation, Siemens, Sinnowa Medical Science & Technology Co. Ltd.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

- Key players in the North America hematology analyzers and reagents market are actively innovating and expanding their product portfolios to meet growing demand. Hematology analyzers and reagents companies such as Abbott Laboratories and Sysmex Corporation are developing advanced, automated hematology analyzers that offer higher accuracy and efficiency. Beckman Coulter is focusing on integrating artificial intelligence and machine learning to enhance diagnostic capabilities. Additionally, these companies are forming strategic partnerships and collaborations to broaden their market reach, invest in research and development to stay ahead of the competition, and make investment decisions according to the hematology analyzers and reagents market forecast. This dynamic activity aims to improve patient care, streamline diagnostic processes, and address the evolving needs of healthcare providers and patients.

Latest News:

- May 2023: Siemens Healthineers launches next-gen hematology analyzers, as one of the hematology analyzers and reagents market recent developments. These analyzers offer two new solutions for high-volume hematology testing, the Atellica HEMA 570 analyzer and the Atellica HEMA 580 analyzer.

Hematology Analyzers and Reagents Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Haematology, Haemostasis, Immunohaematology |

| Usage Types Covered | Standalone, Point-of-Care |

| Price Ranges Covered | Low Range, Mid-Range, High Range |

| Applications Covered | Haemorrhagic Conditions, Infection-Related Conditions, Immune System-Related Conditions, Blood Cancer, Anaemia |

| End Users Covered | Commercial Service Providers, Hospital Laboratories, Research and Academic Institutes, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott Laboratories, Bio-Rad Laboratories Inc., Boule Diagnostics, Danaher Corporation, Diatron MI PLC (Stratec SE), EKF Diagnostics Holdings plc, Heska Corporation, Horiba Ltd., Mindray Medical International Limited, Nihon Kohden Corporation, Siemens, Sinnowa Medical Science & Technology Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global hematology analyzers and reagents market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global hematology analyzers and reagents market?

- What is the impact of each driver, restraint, and opportunity on the global hematology analyzers and reagents market?

- What are the key regional markets?

- Which countries represent the most attractive hematology analyzers and reagents market?

- What is the breakup of the market based on the product?

- Which is the most attractive product in the hematology analyzers and reagents market?

- What is the breakup of the market based on the usage type?

- Which is the most attractive usage type in the hematology analyzers and reagents market?

- What is the breakup of the market based on the price range?

- Which is the most attractive price range in the hematology analyzers and reagents market?

- What is the breakup of the market based on the application?

- Which is the most attractive application in the hematology analyzers and reagents market?

- What is the breakup of the market based on the end user?

- Which is the most attractive end user in the hematology analyzers and reagents market?

- What is the competitive structure of the market?

- Who are the key players/companies in the global hematology analyzers and reagents market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the hematology analyzers and reagents market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global hematology analyzers and reagents market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the hematology analyzers and reagents industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)