Hemophilia Market Size, Share, Trends and Forecast by Type, Treatment, Therapy, and Region, 2026-2034

Hemophilia Market Size and Share:

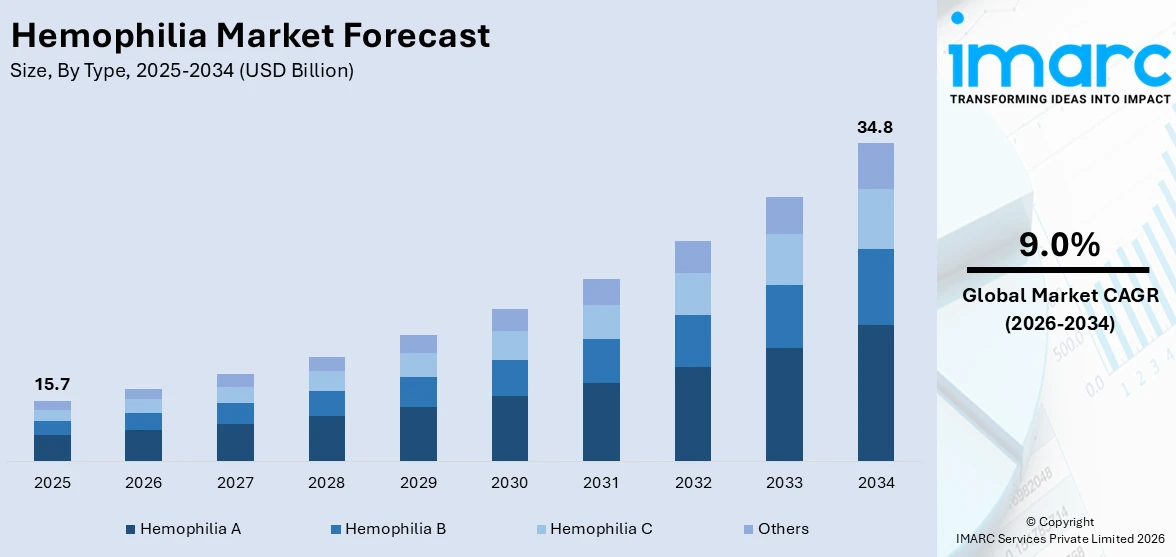

The global hemophilia market size was valued at USD 15.7 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 34.8 Billion by 2034, exhibiting a CAGR of 9.0% during 2026-2034. North America currently dominates the market, holding a significant market share of over 49.7% in 2025.The market is expanding due to increased investment in innovative therapies, including gene therapy and treatments with extended half-lives. At the same time, rising patient awareness and advancements in personalized medicine continue to drive the market, further supporting the hemophilia market share in both developed and emerging regions.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 15.7 Billion |

|

Market Forecast in 2034

|

USD 34.8 Billion |

| Market Growth Rate (2026-2034) | 9.0% |

The market has undergone tremendous evolution on account of being subject to high R&D spending. The funding bestowed innovations in therapies such as gene therapies which purport to give solutions that would last such patients. Efforts have gone into enhancing treatments in an attempt to cut down factor replacement therapy rate as hemophilia cases are on the rise globally. With longer half-life treatment being one such treatment, in fact, it decreases the infusion rate for the patients to elevate their quality of life. Another aspect has been the personalized treatment methods that have been under development with growing inclination toward personalized medicine, ensuring that treatment cater more toward the particular needs of an individual patient. In the U.S., demand for advanced hemophilia treatment has picked up well, driven largely by the demand for better and easy methods of treatments.

To get more information on this market Request Sample

As the population of individuals with hemophilia increases, there is a rising focus on therapies that offer improved efficacy and fewer infusions, ultimately enhancing patients' quality of life. Gene therapies, which offer the potential for long-term or permanent treatment solutions, have garnered significant attention, with several clinical trials underway in the country. The US government and healthcare centers have also expressed greater interest in opening up access to these new treatments, promoting treatments to become more accessible and affordable. This has been particularly significant as patients look for alternatives to conventional factor replacement treatments that take place regularly through infusions. Additionally, the approval of new clotting factor concentrates, and non-factor therapies has provided better management options for patients, allowing for fewer bleeding episodes and reducing the need for hospital visits.

Hemophilia Market Trends:

Increasing Hemophilia Cases and Advancements

The increasing worldwide incidence of hemophilia and genetic disorders are key drivers fuelling the global hemophilia market growth. In 2023, almost 219,000 individuals globally were diagnosed with hemophilia. The increasing number of diagnoses, combined with the growing adoption of prophylactic therapy, represents a huge opportunity for market growth. Additionally, various governmental bodies are conducting campaigns to raise awareness about the importance of early diagnosis and neonatal screening, which is fostering positive growth prospects for the industry. Furthermore, increased investment in research and development (R&D) is being driven by the limited treatment options available. Leading companies in the sector are focusing on developing advanced diagnostic tools and therapies that aim to improve treatment effectiveness and precision, boosting the market's potential. Moreover, substantial investments in the creation of specialized hemophilia treatment centers (HTCs) worldwide are expected to drive market growth further. For example, in 2023, the HTC Funding Program provided support to 20 centers across 12 countries, strengthening data collection and enhancing patient care.

Advancements in Gene Therapy for Hemophilia

The global hemophilia market is undergoing significant transformation as new and innovative therapies emerge to address longstanding challenges in treatment. Traditional approaches, such as frequent factor replacement infusions, often come with high costs and compliance issues for patients. This has led to an increasing demand for alternative therapies that not only improve patient outcomes but also provide long-term solutions. One of the most promising advancements is the rise of gene therapy, offering the potential to eliminate the need for regular infusions and provide a more sustainable treatment model for hemophilia patients worldwide. For instance, in December 2024, India's first human gene therapy for severe Hemophilia A was successfully conducted using a lentiviral vector. This groundbreaking treatment resulted in zero bleeding episodes, demonstrating its effectiveness in providing long-term protection against bleeding. The therapy also eliminated the need for repeated infusions, reducing both the cost and burden on patients. This success highlights the future potential of gene therapies in the hemophilia market, making them a strong contender in transforming the treatment landscape. As gene therapies gain traction, they are expected to significantly expand the market, offering an innovative, cost-effective, and long-term solution for hemophilia patients globally. With this shift, the hemophilia market trends are set to align with the growing demand for advanced, sustainable treatment options.

Convenience and Personalization in Hemophilia Treatments

As the global hemophilia market continues to grow, there is an increasing emphasis on treatments that offer greater convenience and personalization. Many current therapies, particularly intravenous infusions, are time-consuming, require frequent hospital visits, and can be inconvenient for patients. As patient-centric care becomes more important, the demand for therapies that improve quality of life through ease of administration and personalized treatment regimens is on the rise. This has spurred the development of more accessible and patient-friendly treatment options, further driving innovation in the hemophilia market. For instance, in January 2025, the FDA approved Concizumab-mtci (Alhemo), the first subcutaneous prophylactic treatment for Hemophilia A and B with inhibitors. This novel treatment, based on phase 3 clinical trial data, offers patients a more convenient option by providing a subcutaneous injection, eliminating the need for intravenous infusions. The approval of Alhemo is a game-changer for patients with inhibitors, providing a much-needed alternative to existing treatments and increasing the flexibility and convenience of managing hemophilia. With this new approval, the hemophilia market is witnessing a shift toward therapies that are not only more effective but also tailored to the individual needs of patients, making treatment more accessible. As a result, this market is expanding rapidly, with greater opportunities for personalized care solutions to address the diverse needs of hemophilia patients worldwide.

Hemophilia Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global hemophilia market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, treatment, and therapy.

Analysis by Type:

- Hemophilia A

- Hemophilia B

- Hemophilia C

- Others

As per the hemophilia market outlook, in 2025, the hemophilia A segment led the market, accounting for 75.3% of the total market share driven by higher prevalence of Hemophilia A compared to Hemophilia B, with more patients diagnosed with Factor VIII deficiency. Additionally, advancements in therapies specifically targeting Hemophilia A, such as gene therapy and improved clotting factor products, have contributed to this growth. The increasing diagnosis rate and the popularity of prophylactic treatments that prevent bleeding episodes have also played a critical role in driving the demand for Hemophilia A treatments. With the continued focus on developing more effective, long-lasting therapies, the Hemophilia A segment is expected to maintain its leading position in the global market.

Analysis by Treatment:

Access the comprehensive market breakdown Request Sample

- On-Demand

- Prophylaxis

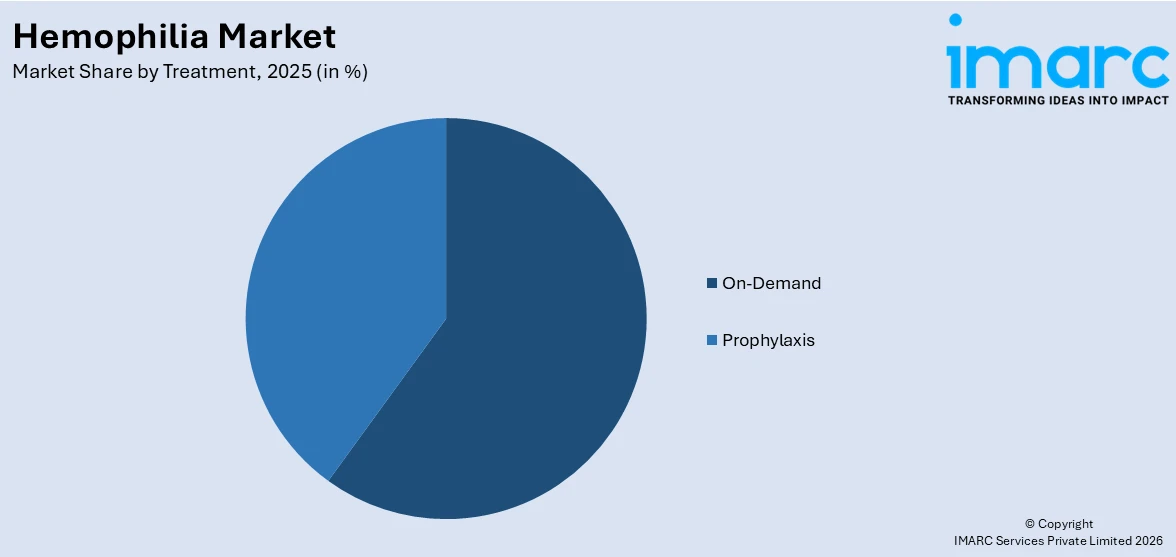

In 2025, the on-demand segment led the hemophilia market, driven by the preference for immediate intervention to manage bleeding episodes. On-demand therapy is primarily used to treat spontaneous bleeds and trauma, offering patients quick access to treatment when needed. This segment has gained traction due to its flexible and responsive nature, particularly for patients who experience occasional bleeding episodes. Additionally, the development of more advanced and easier-to-administer on-demand treatments, such as subcutaneous injections and extended-acting factor therapies, has enhanced patient compliance and convenience. As these therapies continue to improve in terms of effectiveness and ease of use, the on-demand treatment segment remains a crucial player in the Hemophilia market.

Analysis by Therapy:

- Replacement Therapy

- ITI Therapy

- Gene Therapy

In 2025, the replacement therapy segment led the hemophilia market, accounting for 61.7% of the total market share, driven by the effectiveness of replacement therapies in treating both Hemophilia A and B. These therapies involve replacing the missing clotting factors (Factor VIII for Hemophilia A and Factor IX for Hemophilia B), directly addressing the root cause of bleeding episodes. With continuous advancements in the half-life of clotting factors, extended-acting therapies have gained preference, providing longer protection against bleeding episodes and reducing the frequency of infusions. The widespread use of prophylactic replacement therapy has also contributed to the segment’s leading position, as it helps patients maintain better overall health and quality of life.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

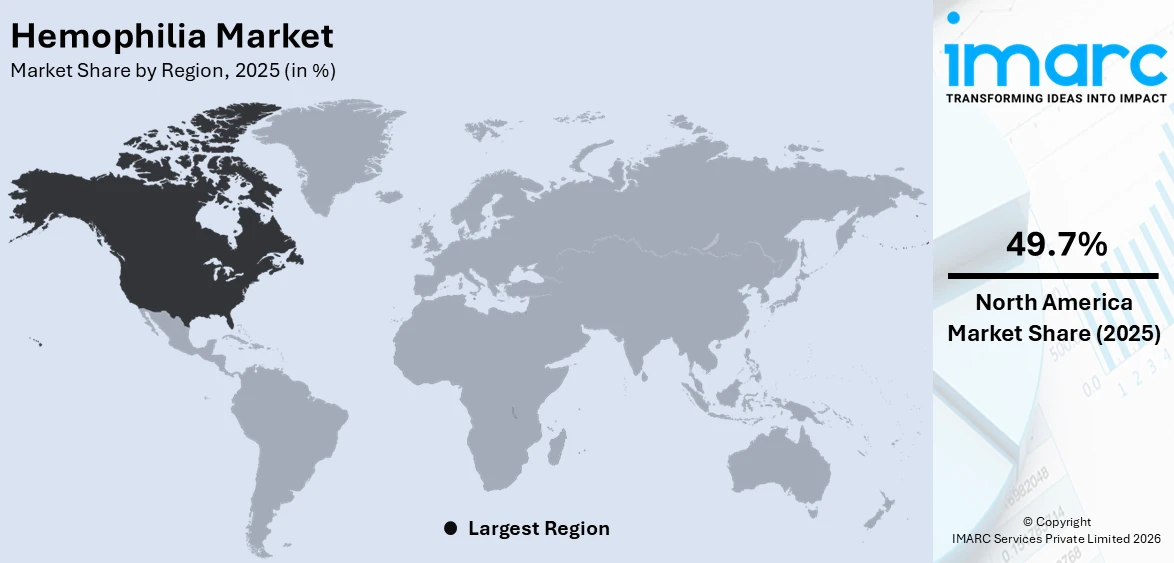

In 2025, the North America segment led the hemophilia market, accounting for 49.7% of the total market share, driven by its high healthcare expenditure, advanced healthcare infrastructure, and extensive access to innovative therapies. North America also benefits from a well-established network of specialized hemophilia treatment centers (HTCs) and significant government support for healthcare research and development. Furthermore, the presence of leading pharmaceutical companies developing innovative hemophilia treatments has contributed to the rapid adoption of novel therapies. The increased diagnosis rates, patient awareness, and access to newer treatments like gene therapy and extended-acting clotting factors have significantly boosted the demand for hemophilia care in North America, solidifying its position as the largest market.

Key Regional Takeaways:

United States Hemophilia Market Analysis

In 2025, the United States accounted for 93.50% of the hemophilia market in North America, driven by multiple factors. United States is a significant contributor to this market share owing to the increase in specialized hemophilia treatment centers (HTCs) across the country. As per the National Bleeding Disorders Foundation, approximately 141 federally funded treatment centers and programs are active in the US. These centers are integral in delivering comprehensive care, improving early diagnosis, and enhancing patient outcomes. The rise in public and private sector funding has led to the expansion of HTCs, ensuring more widespread access to advanced treatments. With continued investments in healthcare infrastructure and specialized care models, adoption rates of hemophilia therapies are steadily increasing. The growing presence of HTCs, combined with strategic collaborations between healthcare providers and pharmaceutical companies, strengthens the market by offering patients more reliable diagnosis and treatment options. This development continues to foster greater patient engagement and boosts the overall growth of the market.

Asia Pacific Hemophilia Market Analysis

The Asia-Pacific region is experiencing a notable rise in hemophilia adoption, largely driven by the increasing prevalence of genetic disorders in the area. According to the Tata Institute for Genetics and Society, there are 5000-8000 rare genetic diseases identified globally, with 450 cases reported in India. Hemophilia, particularly its genetic transmission through inherited X-linked recessive mutations, plays a significant role in the increasing patient population. Public health initiatives focusing on early detection, genetic counseling, and awareness campaigns have improved the identification of hemophilia patients. Advances in diagnostic technologies further contribute to the quicker identification of genetic markers related to the disease. Additionally, better healthcare frameworks and government support are promoting the management of hemophilia across the region. These factors combined with the growing attention to rare genetic conditions create a positive environment for expanding hemophilia care and interventions in Asia-Pacific.

Europe Hemophilia Market Analysis

Europe's aging population is influencing the growing demand for specialized hemophilia care, as more individuals are living longer with the condition. By the beginning of 2024, Europe's population was estimated at 449.3 Million, with over 20% aged 65 or older. As life expectancy rises, patients diagnosed with hemophilia in their early years continue to require lifelong treatment, leading to an increased demand for healthcare resources. This demographic shift is placing greater focus on managing age-related complications in hemophilia, such as joint damage and associated comorbidities. Healthcare systems are adapting to this change by refining long-term therapy plans and mobility support services. The rise in geriatric patients with hemophilia is prompting healthcare providers to tailor treatment approaches to meet the needs of elderly patients, ensuring consistent access to replacement therapies and rehabilitation, driving the demand for specialized services in the region.

Latin America Hemophilia Market Analysis

In Latin America, the adoption of hemophilia treatments is on the rise due to the growing number of diagnosed cases in the region. Government data from Colombia in 2021 reported a prevalence of hemophilia A of 4.29 cases per 100,000 people. The increasing number of diagnoses, along with better access to healthcare services, is helping to raise awareness of the disease burden. Population screening programs have been instrumental in identifying more individuals affected by hemophilia, which in turn has heightened the demand for consistent and comprehensive treatment plans. As more patients are diagnosed and healthcare access improves, the need for ongoing therapy and specialized care is driving the market's expansion in Latin America.

Middle East and Africa Hemophilia Market Analysis

In the Middle East and Africa, hemophilia treatment adoption is rising as regional healthcare infrastructure continues to expand. The prevalence of hemophilia in countries across the Middle East and North Africa (MENA) region—such as Iraq, Iran, Turkey, Egypt, Jordan, Syria, and Saudi Arabia—ranges from 1.4 to 8.1 per 100,000 people. Strengthening healthcare systems and the introduction of new therapy and diagnostic centers are improving access to specialized services and early detection. Advances in diagnostic capabilities and treatment options have contributed to greater hemophilia care availability in underserved regions. As healthcare infrastructure continues to improve, more patients are gaining access to effective treatments, resulting in increased adoption of hemophilia care across the Middle East and Africa.

Competitive Landscape:

As per the hemophilia market forecast, leading companies in the market are focusing on R&D to develop advanced formulations with better efficacy and fewer side effects, reflecting the shift toward safer and more effective treatments. Expansions through acquisitions, partnerships, and global collaborations are driving the market, enabling companies to access new markets and technologies. Regulatory compliance and sustainable manufacturing remain key priorities, underscoring their commitment to quality, safety, and environmental responsibility.

The report provides a comprehensive analysis of the competitive landscape in the hemophilia market with detailed profiles of all major companies, including:

- Baxter International Inc.

- Bayer AG

- BioMarin Pharmaceutical Inc.

- CSL Behring (CSL Limited)

- F. Hoffmann-La Roche AG

- Grifols S.A.

- Kedrion S.p.A.

- Novo Nordisk A/S

- Octapharma AG

- Pfizer Inc.

- Sanofi S.A.

- Takeda Pharmaceutical Company Limited

Latest News and Developments:

- May 2025: The US FDA approved Bayer’s Jivi for pediatric patients aged 7 to under 12 years with hemophilia A, expanding its prior indication. The decision followed positive results from the Alfa-PROTECT and PROTECT Kids studies, which confirmed Jivi’s safety and efficacy in treating hemophilia in this age group.

- April 2025: The FDA approved Sanofi’s Qfitlia (fitusiran) as the first prophylactic therapy for hemophilia A or B, with or without inhibitors, for patients aged 12 and older in the US Qfitlia targeted antithrombin to rebalance hemostasis and showed improved bleed protection in individuals with hemophilia.

- March 2025: The FDA approved Qfitlia (fitusiran) as a new treatment for hemophilia A or B in patients aged 12 and older, with or without factor inhibitors. The medication, which targeted antithrombin to boost thrombin levels for clotting, had been administered subcutaneously as infrequently as once every two months. Hemophilia patients had gained a less burdensome prophylactic option, monitored through the FDA-cleared INNOVANCE Antithrombin test.

- January 2025: The FDA approved Novo Nordisk’s Alhemo as the first subcutaneous injection for hemophilia A or B with inhibitors in patients aged 12 and older. This daily prophylactic marked a major step for those with limited options and has also received global marketing authorizations.

- October 2024: The FDA approved Pfizer's HYMPAVZI (marstacimab-hncq) for routine prophylaxis in Hemophilia A and B patients, aged 12 and older. This approval marked a significant advancement in hemophilia treatment, enhancing market growth by offering a novel, effective therapy for reducing bleeding episodes.

- June 2024: Sanofi presented new data at the ISTH Congress for ALTUVIIIO and fitusiran. The interim results from the XTEND-ed and ATLAS phase 3 studies demonstrated effective bleed protection and long-term safety, enhancing the hemophilia market with innovative treatment options.

Hemophilia Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Hemophilia A, Hemophilia B, Hemophilia C, Others |

| Treatments Covered | On-Demand, Prophylaxis |

| Therapies Covered | Replacement Therapy, ITI Therapy, Gene Therapy |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Baxter International Inc., Bayer AG, BioMarin Pharmaceutical Inc., CSL Behring (CSL Limited), F. Hoffmann-La Roche AG, Grifols S.A., Kedrion S.p.A., Novo Nordisk A/S, Octapharma AG, Pfizer Inc., Sanofi S.A. and Takeda Pharmaceutical Company Limited |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the hemophilia market from 2020-2034.

- The hemophilia market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the hemophilia industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Hemophilia Market Report

The hemophilia market was valued at USD 15.7 Billion in 2025.

The hemophilia market is projected to exhibit a CAGR of 9.0% during 2026-2034, reaching a value of USD 34.8 Billion by 2034.

Key factors driving the hemophilia market include increasing prevalence of genetic disorders, advancements in gene therapies, growing healthcare investments, improved early diagnosis, and better access to specialized treatment centers. Additionally, increased awareness and patient education are fueling the demand for better treatment options.

In 2025, North America dominated the hemophilia market accounting for 49.7% of the total market share, driven by extensive investments in specialized hemophilia treatment centers, improved healthcare infrastructure, advancements in treatment options, and ongoing efforts in research and development aimed at better patient outcomes and accessibility.

Some of the major players in the global hemophilia market include Baxter International Inc., Bayer AG, BioMarin Pharmaceutical Inc., CSL Behring (CSL Limited), F. Hoffmann-La Roche AG, Grifols S.A., Kedrion S.p.A., Novo Nordisk A/S, Octapharma AG, Pfizer Inc., Sanofi S.A. and Takeda Pharmaceutical Company Limited.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)