High-performance Computing (HPC) Market Size, Share, Trends and Forecast by Component, Deployment Type, End Use, and Region, 2026-2034

High-performance Computing (HPC) Market Size and Share:

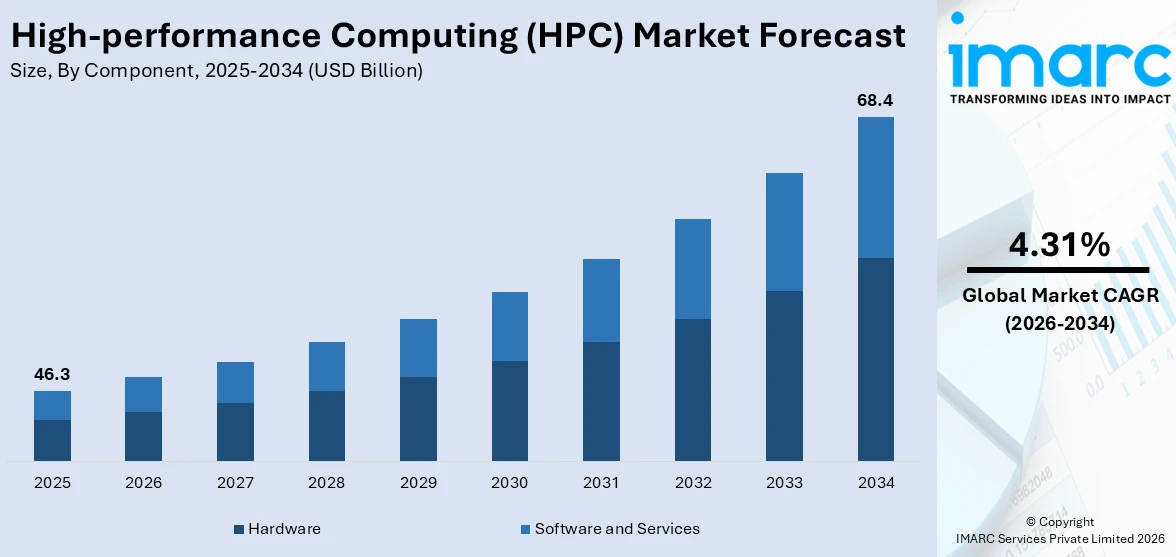

The global high-performance computing (HPC) market size was valued at USD 46.3 Billion in 2025. Looking forward, the market is forecasted to reach USD 68.4 Billion by 2034, exhibiting a CAGR of 4.31% from 2026-2034. North America currently dominates the market, holding a market share of over 40.3% in 2025. The market demand is experiencing steady growth driven by rapid digitization, increasing demand for high-performance computing solutions, and extensive research and development (R&D) activities.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 46.3 Billion |

|

Market Forecast in 2034

|

USD 68.4 Billion |

| Market Growth Rate (2026-2034) | 4.31% |

Government and corporate investments are pivotal in propelling the high-performance computing (HPC) market's expansion. In the United States, the National Strategic Computing Initiative (NSCI), established in 2015, underscores a commitment to advancing HPC capabilities. This initiative has led to the development of exascale supercomputers, such as Frontier and Aurora, which became operational in 2022 and 2024, respectively. These systems, each exceeding one exaFLOP in performance, represent significant milestones in computational power. Internationally, countries like Australia are making substantial investments to enhance their HPC infrastructure. In April 2024, the Australian government announced a nearly $1 billion investment in collaboration with PsiQuantum to build a quantum computer in Brisbane. This initiative aims to position Australia at the forefront of quantum computing technology, fostering advancements in materials science and drug development. These strategic investments by governments and corporations are instrumental in advancing HPC technologies, thereby driving market growth and enabling breakthroughs across various scientific and industrial domains.

To get more information on this market Request Sample

The U.S. HPC market is emerging as a major disruptor, holding 76.80% of the total share. A significant contributor is the escalating demand for advanced computational power across various industries, including engineering simulations, scientific research, and big data analytics. This surge is attributed to the increasing complexity of tasks such as weather forecasting, drug discovery, and financial modeling, which require sophisticated computing capabilities. The proliferation of data centers and cloud services is another pivotal factor propelling the HPC market. Organizations are increasingly adopting hybrid HPC solutions, combining on-premises and cloud resources to achieve flexibility and cost-effectiveness. This trend is evident in the substantial growth of data center construction; for instance, in the first half of 2024, over 500 megawatts of new data center capacity were added in the United States and Canada, reflecting a 70% increase compared to the previous year.

High-performance Computing (HPC) Market Trends:

Rapid Digitization

The high-performance computing (HPC) market price is being propelled by ongoing digitization across various sectors. When organizations are adopting digital transformation initiatives, they require computer systems that can handle large amounts of data and perform intensive tasks at high speeds. In 2018–2022, there were 1.5 billion new internet users worldwide, according to the World Bank's Digital Progress and Trends Report 2023. In 2022, there were 5.3 billion internet users worldwide, or two-thirds of the world's population. In middle-income nations, the already rapid increase in internet users was accelerated by the COVID-19 pandemic. But in 2022, only one in four people in low-income nations had access to the internet. As a result, HPC systems provide the computational capacity required to process large data sets, perform sophisticated simulations, and effectively execute complicated algorithms. It is true that the healthcare, banking, manufacturing, and research industries rely on this type of technology to speed up innovation, boost productivity, and give them an edge over competitors. Rapid digitization has raised demand for HPC solutions, promoting industry growth and innovation across industries.

Increasing Research and Development Activities

According to the high-performance computing (HPC) market overview, the market is being driven ahead by increased research and development (R&D) activities. Companies are increasing R&D investments to be competitive in the face of rapid technology breakthroughs and dynamic innovation trends. The Global Innovation Index (GII) is based on data from the European Commission's Joint Research Centre's 2023 EU Industrial R&D Investment Scoreboard, which analyzes the world's top 2,500 corporate R&D spenders, who account for 90% of total R&D investment. The findings were clear: since 2003, R&D investments by these top companies have steadily risen, surpassing Euro 1.3 Trillion (USD 1.37 Trillion) in 2022, marking a 13% increase over the previous year. The need for computing systems that can deal with intricate simulations, data analysis, and modeling exercises is increasing as industries become more competitive and innovative. HPC solutions are useful in advancing R&D operations in different sectors like pharmaceuticals, automotive, aerospace, and energy, through providing the computational power necessary. For this reason, HPC technologies have been adopted in these sectors to hasten product development cycles, optimize designs, and enhance decision-making processes. Continuous R&D activities across the globe is giving the market the required push. For instance, the EuroHPC Joint Undertaking has launched its first quantum computing initiative, aiming to integrate quantum systems into high-performance computing infrastructures. This project focuses on developing cutting-edge quantum computing technologies and fostering collaboration among European researchers, industries, and institutions. Additionally, Georgia Tech researchers are working hard to create useful software and algorithms that push the boundaries of HPC speed and scale. Their work covers a wide range of applications, such as biological simulations, material discoveries, and climate modelling. Furthermore, Illinois Tech is carrying out significant research in the area. Therefore, market growth is driven by intensified R&D coupled with the need for faster and more efficient computing.

Rising volume of data generated

One of the key drivers of the high-performance computing (HPC) market is rising data volume from sectors. With the digital technology explosion, organizations generate huge amounts of data on a daily basis. According to the data by International Data Corporation, Global datasphere will grow from 33 Zettabytes in 2018 to 175 Zettabytes in 2025. China's datasphere is predicted to develop by 30% on average over the next seven years, making it the largest datasphere globally by 2025 owing to connected population increases and its video surveillance infrastructure spreads. It calls for HPC systems to process, analyze, and draw insights from this data at the real time. Big data analytics, predictive modeling, and machine learning algorithms are some elements in the healthcare finance and telecommunications industry where HPC solutions are used for big data handling. Additionally, emerging technologies like artificial intelligence and deep learning require massive computational power, further driving the demand for HPC solutions.

High-performance Computing (HPC) Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global high-performance computing (HPC) market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on component, deployment type, and end use.

Analysis by Component:

- Hardware

- Software and Services

The hardware segment dominates the market, with its growth primarily fueled by continuous advancements in hardware technology. As technology continues to develop, various components of the systems such as processors, memory, and interconnects become more powerful and efficient. The development of specialized accelerators such as GPUs and FPGAs further enhances computational capabilities. These advances allow HPC systems to execute complex calculations and analyze huge datasets at unprecedented speeds. Hardware vendors are also always striving to provide solutions tailored for HPC applications that have unique requirements. As a result, sustained improvements in hardware form an important aspect of shaping the HPC market.

Analysis by Deployment Type:

- On-premises

- Cloud-based

On-premises leads the market with around 61.75% of market share in 2025. Many organizations prefer on-premises deployments because they handle sensitive data or want to have full control over their computing infrastructure. This type of deployment allows for security, customization, and dedicated resources required for HPC workloads. On the other hand, on-premises deployments also offer higher flexibility when it comes to scaling resources according to specific requirements as well as workload demands. The demand for on-premises deployments is expected to grow as industries demand higher for HPC.

Analysis by End Use:

Access the comprehensive market breakdown Request Sample

- Aerospace and Defense

- Energy and Utilities

- BFSI

- Media and Entertainment

- Manufacturing

- Life Science and Healthcare

- Others

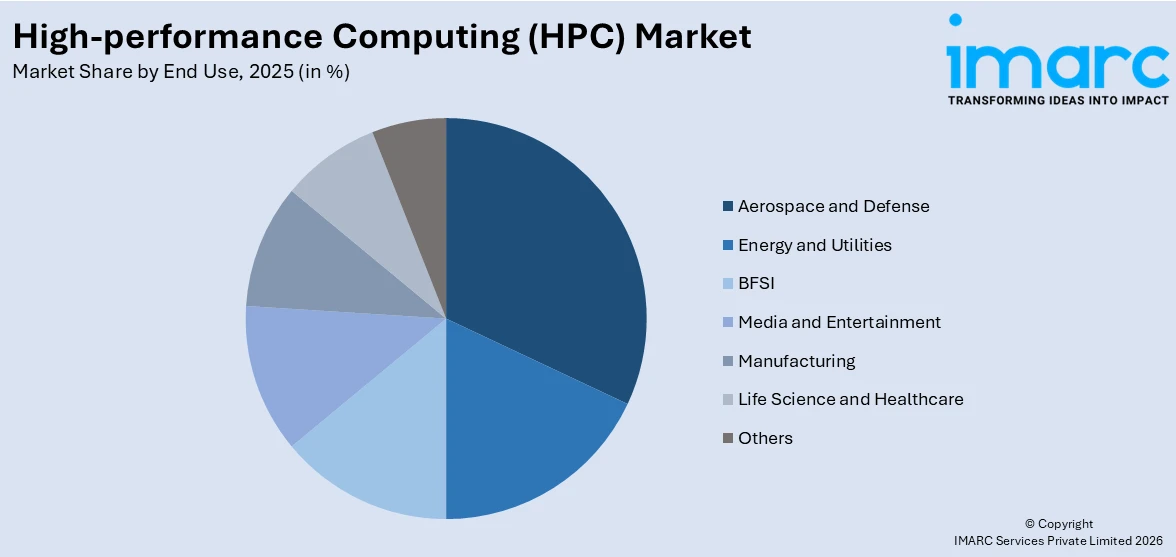

Aerospace and defense lead the market with approx. 32.0% market share in 2025. The aerospace and defense sector dominates the market, due to its critical reliance on advanced computational capabilities for innovation and security. HPC systems are integral to designing next-generation aircraft, spacecraft, and defense technologies by enabling the simulation of complex aerodynamic phenomena and advanced material behavior. For instance, designing supersonic jets and spacecraft involves processing enormous datasets and performing intricate calculations, which HPC systems efficiently manage. Furthermore, in defense, HPC is vital for real-time data processing and analysis in areas like missile guidance, radar system optimization, and cyber defense strategies.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

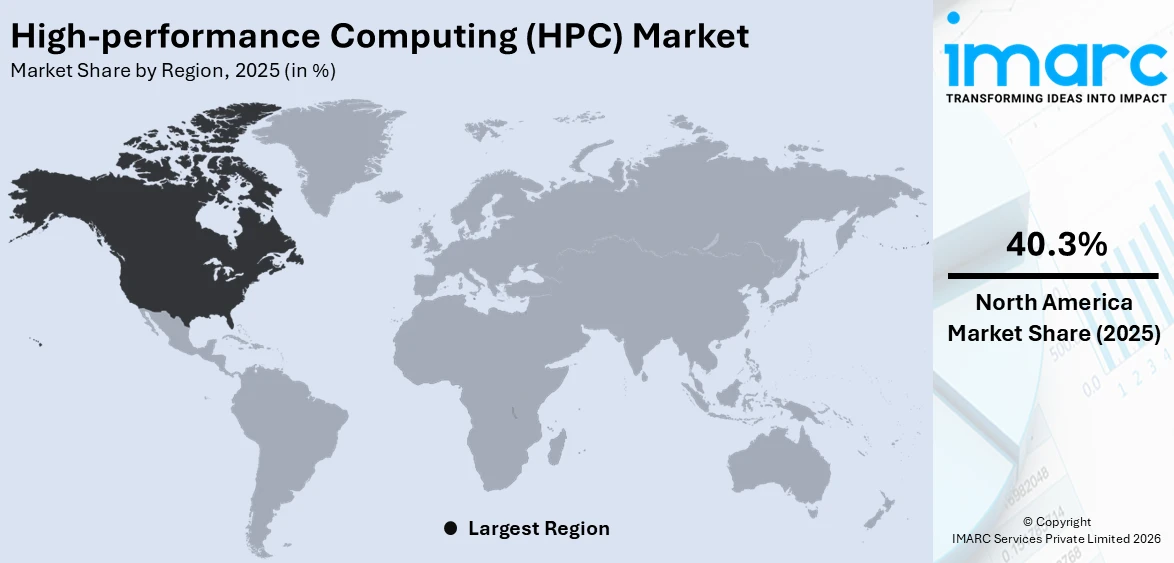

In 2025, North America accounted for the largest market share of over 40.3%. North America is leading the market for several reasons. This region has a vibrant ecosystem of tech companies, research centers, and universities that promote creativity in HPC technologies. North America has made huge investments in R&D, infrastructure, and labor force competence, thus nurturing the growth and acceptance of progressive HPC solutions. Furthermore, their strong presence in significant sectors like healthcare, finance, and aerospace creates demand for HPC applications. Moreover, North American favorable government policies as well as initiatives supporting technological innovation help it to lead in the HPC marketplace. Through an innovative program, the U.S. Department of Energy (DOE) is granting U.S. companies access to its exceptional computing resources and technical proficiency. This initiative utilizes high-performance computing (HPC) to address urgent manufacturing and materials development challenges faced by industries.

Key Regional Takeaways:

United States High-performance Computing (HPC) Market Analysis

The market for high-performance computing (HPC) is dominated by the US due to substantial investments in supercomputing infrastructure and technological breakthroughs. Defence, energy, and climate research are just a few of the industries that rely on the nation's strong research and development (R&D) ecosystem, which is bolstered by government programs like the Exascale Computing Project (ECP) of the U.S. Department of Energy. The ECP, which was overseen by the US Department of Energy (DOE) from 2016 to 2024, was the largest software research, development, and deployment project to date. The National Nuclear Security Administration and the DOE Office of Science collaborated on the USD 1.8 Billion initiative, which provided funding to about 2,800 interdisciplinary professionals over its duration. Moreover, the need for HPC solutions to effectively process massive datasets is fuelled by the growth of big data analytics in sectors like healthcare, finance, and retail.

The ongoing innovation in HPC hardware and software by major tech companies like IBM, Hewlett Packard Enterprise, and NVIDIA makes it possible for larger industry applications like AI and machine learning. Another major factor is the growing demand for cloud based HPC solutions, which is driven by businesses looking for scalable and affordable solutions. The market is also supported by the rising demand for sophisticated automotive simulations, real-time financial modelling, and precision medicine. The United States is well-positioned to continue leading the HPC market because to continuous efforts to strengthen semiconductor supply chains and manufacturing.

Europe High-performance Computing (HPC) Market Analysis

Growing investments in industrial digitisation and scientific research are driving the expansion of the HPC industry in Europe. One important motivator is the European Union's EuroHPC Joint Undertaking, which plans to invest more than Euro 8 Billion (USD 8.4 Billion) in supercomputing infrastructure and research and development by 2030 in order to create a world-class HPC environment. Leading nations like Germany, France, and the UK are at the forefront of using HPC for advanced manufacturing, genomics, and climate modelling applications. JUPITER, the first exascale supercomputer in Europe, is now being deployed in the second half of 2024. Jupiter, one of the world's most potent AI supercomputers, is anticipated to be the first European supercomputer to perform more than one quintillion (a "1" followed by eighteen zeros) calculations per second. Applications of artificial intelligence in science and industry, as well as the creation of high-precision models of complex systems, will be facilitated by this unparalleled processing power.

HPC is used extensively in the automobile industry, especially in Germany, for simulations in the development of autonomous vehicles and the optimisation of aerodynamics. Furthermore, HPC adoption for smart grid management and renewable energy research is fuelled by Europe's emphasis on sustainability. As SMEs use HPC without having to pay large upfront fees, cloud-based HPC services—made possible by companies like Atos and Dassault Systèmes—are growing quickly.

Asia Pacific High-performance Computing (HPC) Market Analysis

The increasing digitisation, government efforts, and growth of data-intensive businesses have made Asia-Pacific the HPC market's fastest-growing area. Leading the area, China is home to some of the most potent supercomputers in the world, such as Sunway TaihuLight, which are used in biosciences, artificial intelligence, and weather forecasting. The Chinese government has demonstrated its dedication to technical leadership by investing in exascale computing. China emphasised its commitment to improving HPC capabilities in 2022 when it announced plans to construct ten national data-center clusters and eight national computing centres. Similar to this, the Ministry of Science and ICT of South Korea announced a national strategy in 2023 to enhance HPC capabilities, which included the creation of a new supercomputer that is anticipated to reach exaflop performance by 2025. Furthermore, in 2022, OneAsia introduced OAsis, Hong Kong's first HPC solution, with the goal of revolutionising data processing for scholarly research and business innovation. Japan is also an important participant. Japan's top-performing supercomputer, Fugaku, aids in disaster relief, medical development, and climate research.

The need for HPC has increased in industries including e-governance, healthcare, and education because of India's emphasis on digital transformation and AI adoption. SMEs and startups are using HPC more and more for scalable computing solutions as cloud based HPC services expand. Additionally supporting HPC growth is the region's growing semiconductor manufacturing base, which serves AI, big data, and analytics needs.

Latin America High-performance Computing (HPC) Market Analysis

The growing digitisation of sectors including healthcare, energy, and agriculture is propelling the adoption of high-performance computing throughout Latin America. Very few countries in the region are employing and investing in Supercomputers. For example, Brazil has a good computing capacity with 88,175 TFlops – the vast majority of which is in the hands of the oil industry and only about 3,000 TFlops are used for basic research. Another factor is the expansion of AI and machine learning in industries like logistics and retail. Although HPC adoption is still in its early phases, cloud-based solutions and regional partnerships are opening up HPC to a wider audience. Infrastructure is being improved by international players working with regional businesses. The region's need for affordable, scalable HPC solutions is expected to increase as sectors modernise.

Middle East and Africa High-performance Computing (HPC) Market Analysis

Improvements in the energy, healthcare, and finance sectors are driving growth in the Middle East and Africa (MEA) HPC industry. Saudi Aramco and other Gulf oil and gas firms employ HPC for reservoir exploration and modelling. The UAE's emphasis on renewable energy initiatives and AI-powered smart cities encourages the use of HPC even more. HPC systems are being used more and more in Africa for genomics research and weather forecasting. Cloud-based HPC services make the technology available to smaller businesses, while government programs and global alliances are encouraging investments in HPC equipment. According to an industrial report, globally, by the end of 2030, it is expected that 5G networks will carry around 80 percent of total mobile data traffic while as on the end of 2024, the same stood at 34 percent. The Gulf Cooperation Council (GCC) countries are poised to achieve 47% fifth-generation (5G) subscription penetration by 2024. These factors will likely infuse the industry demand.

Competitive Landscape:

The market is driven by key players who are innovating through strategic partnerships and investments. Companies are always coming up with state-of-the-art HPC hardware, software, and services aimed at serving the ever-rising industries’ demands. These players spend heavily on research and development in order to improve their computational capabilities, lower energy consumption costs, and increase scalability. Furthermore, strategic collaborations with research institutions, government agencies, and industry partners allow key players to extend their market footprint by developing niche-targeted solutions for specific usages only. By staying at the forefront of technological advancements and addressing customer needs, key players play an important role in driving the high-performance computing (HPC) market recent developments.

The report provides a comprehensive analysis of the competitive landscape in the high-performance computing (HPC) market with detailed profiles of all major companies, including:

- Advanced Micro Devices Inc.

- Atos SE

- Cisco Systems Inc.

- Dell Technologies Inc.

- Fujitsu Limited

- Hewlett Packard Enterprise Development LP

- Intel Corporation

- International Business Machines Corporation

- Lenovo Group Limited

- Microsoft Corporation

- NetApp Inc.

- Nvidia Corporation

Latest News and Developments:

- August 2024: RIKEN has launched a virtual platform replicating the capabilities of Fugaku, one of the world's fastest supercomputers, to expand accessibility for researchers globally. This initiative allows users to harness Fugaku's computational power remotely for diverse scientific applications, such as climate modeling, medical research, and AI development.

- August 2024: The National Renewable Energy Laboratory (NREL) has launched its Kestrel supercomputer to support advanced renewable energy research. The system, housed at NREL’s Energy Systems Integration Facility, offers 44 petaflops of computational power, enabling detailed simulations and analyses to optimize energy systems, develop new materials, and advance grid technologies. Kestrel is pivotal in achieving U.S. energy transition goals, supporting initiatives in wind, solar, and hydrogen energy research.

- March 2024: Advanced Micro Devices Inc. announced the AMD Spartan™ UltraScale+™ FPGA family. It is the latest addition to AMD's vast array of cost-optimized FPGAs and adaptive SoCs.

- March 2024: Cisco Systems Inc. unveiled new purpose-built, multifunctional devices that provide modernized collaborative experiences to today's hybrid workforce.

- December 2023: Atos SE revealed that it is expanding its partner network. It has entered into a collaboration arrangement with Onepoint, a consulting firm that specializes in big corporate and government transitions.

High-performance Computing (HPC) Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Hardware, Software and Services |

| Deployment Type Covered | On-premises, Cloud-based |

| End Uses Covered | Aerospace and Defense, Energy and Utilities, BFSI, Media and Entertainment, Manufacturing, Life Science and Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Advanced Micro Devices Inc., Atos SE, Cisco Systems Inc., Dell Technologies Inc., Fujitsu Limited, Hewlett Packard Enterprise Development LP, Intel Corporation, International Business Machines Corporation, Lenovo Group Limited, Microsoft Corporation, NetApp Inc., Nvidia Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the high-performance computing (HPC) market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global high-performance computing (HPC) market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the high-performance computing (HPC) industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the High-performance Computing (HPC) Market Report

High-Performance Computing (HPC) is the use of supercomputers and parallel processing techniques to solve complex computational problems in a very high speed with high efficiency. It combines hardware, software, and networking to perform massive calculations that would take conventional computers an impractically long time to complete. HPC systems are often measured in terms of their ability to execute floating-point operations per second (FLOPS), with modern systems capable of reaching petascale or even exascale performance levels.

The high-performance computing (HPC) market was valued at USD 46.3 Billion in 2025.

IMARC estimates the global high-performance computing (HPC) market to exhibit a CAGR of 4.31% during 2026-2034.

The market is expanding due to increasing government and corporate investment, rapid digitization, increasing research and development (R&D) activities, and rising volume of data generated.

In 2025, hardware represented the largest segment by component, driven by rapid technological advancements in various components, such as processors, memory, and interconnects.

On-premises leads the market by deployment type as many organizations prefer to have full control over their computing infrastructure.

The aerospace and defense are the leading segment by end use due to its critical reliance on advanced computational capabilities for innovation and security.

In 2025, North America accounted for the largest market share of over 40.3%.

Some of the major players in the global high-performance computing (HPC) market include Advanced Micro Devices Inc., Atos SE, Cisco Systems Inc., Dell Technologies Inc., Fujitsu Limited, Hewlett Packard Enterprise Development LP, Intel Corporation, International Business Machines Corporation, Lenovo Group Limited, Microsoft Corporation, NetApp Inc., Nvidia Corporation, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade