Homeland Security Market Size, Share, Trends and Forecast by Type, System, End-User, and Region, 2026-2034

Homeland Security Market Size and Share:

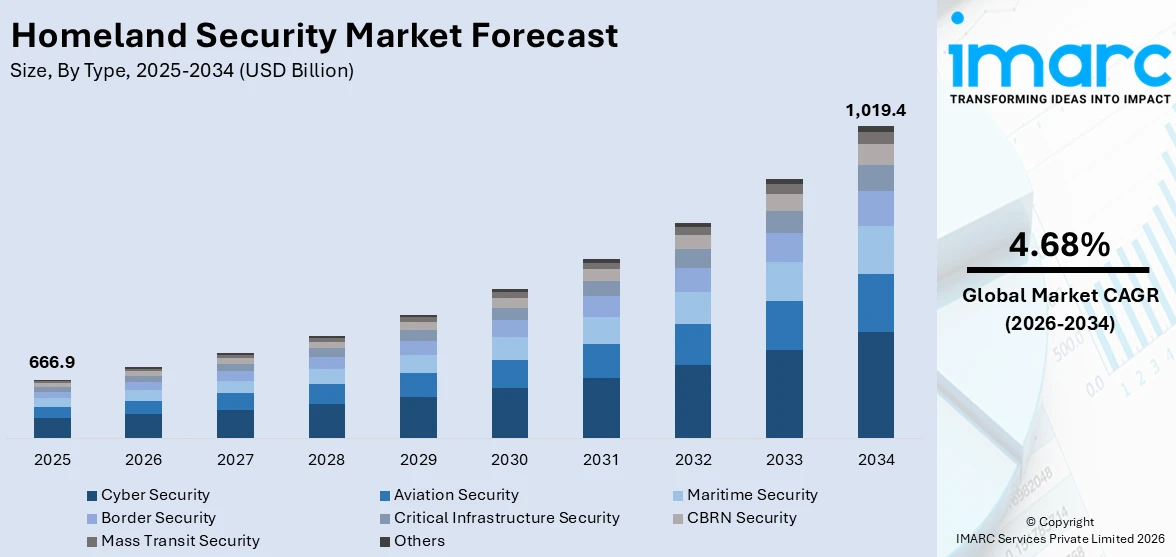

The global homeland security market size was valued at USD 666.9 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 1,019.4 Billion by 2034, exhibiting a CAGR of 4.68% from 2026-2034. North America currently dominates the market, holding a market share of 30.6% in 2025. The growing threats and sophistication of cyber attacks against critical infrastructure, government networks, and private sector networks, increasing efforts to secure national borders and effectively control immigration, and rising number and severity of natural disasters is influencing the homeland security market share positively.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 666.9 Billion |

|

Market Forecast in 2034

|

USD 1,019.4 Billion |

| Market Growth Rate 2026-2034 | 4.68% |

Due to the increasing complexity and diversity of global threats, the homeland security sector is undergoing significant change. To combat threats to national security, governments and the business sector around the world are constantly investing in cutting-edge infrastructure and technologies. The industry is seeing a rise in demand for emergency response systems, cyber defense mechanisms, and surveillance systems, which is a sign of both new and classic roles becoming more important. By using biometric systems, drone surveillance, and intelligent fencing technology, countries are progressively enhancing border security. While lowering the need for human intervention, these technologies are helping authorities keep a closer eye on cross-border activity. Additionally, the market is seeing an increase in the application of machine learning (ML) and artificial intelligence (AI) to improve real-time threat detection and data analysis capabilities.

To get more information on this market Request Sample

The United States homeland security market is rapidly evolving as federal, state, and local authorities are constantly reacting to a wide range of threats such as terrorism, cyberattacks, natural disasters, and pandemics. The Department of Homeland Security (DHS) and related organizations are actively investing in advanced technologies and integrated solutions to boost national preparedness and resilience. The market is becoming more cybersecurity-focused, with the agencies using enhanced threat detection systems and making the key infrastructure cyber-secure. The federal and state governments are embracing cloud platforms and real-time monitoring solutions to tackle digital risks. Public and private sector players are collaborating to exchange threat intelligence and enhance response mechanisms, mirroring a collective orientation towards national cybersecurity. The IMARC Group predicts that the United States cybersecurity market size is expected to reach USD 167.9 Billion by 2033.

Homeland Security Market Trends:

Rising Cybersecurity Threats

The homeland security industry is being driven by increasing threats and sophistication of cyber attacks against critical infrastructure, government networks, and private sector networks. Threat actors such as nation-states and organized cybercrime groups are progressively using advanced tools to cause disruptions, steal confidential data, and destabilize national security. In turn, federal and state governments are incessantly investing in new-generation cybersecurity technology like AI-based threat detection, end-point security, and enhanced encryption protocols. Cybersecurity frameworks are being revised to incorporate real-time monitoring, incident response automatization, and data resiliency tactics. Organizations are also augmenting their cybersecurity staffs, while forming public-private partnerships to maintain a cohesive front against changing cyber threats. The government is proactively introducing solutions like zero-trust architecture and supply chain hardening, thus strengthening the cyber perimeter. With these cyber threats ongoing and rising, cybersecurity is emerging as a key pillar in homeland security policy, driving sustained market growth. The FY 2025 President's Budget request of $150 million for the Cybersecurity Enhancement Account (CEA) was developed to assist the Department in its continued efforts aimed at operational risk reduction. The request contains $6 million for bureau-specific investments for mission-critical requirements that need to be met to align with Treasury's enterprise cybersecurity services.

Increasing Border and Immigration Security Measures

The global homeland security market is driven by increased efforts to secure national borders and effectively control immigration, thereby impelling the homeland security market growth. In February 2025, the USBP apprehended 8,347 illegal aliens at the southwest border between ports of entry. This is a 71% drop from January 2025 when USBP apprehended 29,101 aliens, and a 94% drop from February 2024 when USBP apprehended 140,641 aliens. With illegal immigration, trafficking, and cross-border crime concerns increasing, homeland security organizations are deploying advanced technologies to boost surveillance and operational control. These include the installation of biometric identification systems, artificial intelligence (AI)-driven surveillance cameras, ground sensors, and drone technology to track extensive border areas in real time. Governments are incorporating data analysis platforms that assist in the identification of patterns of illegal entry and coordination of responses across jurisdictions. Mobile screening stations and automated passport verification systems are being used at points of entry to speed up security checks without sacrificing efficiency. In addition, policy initiatives like tighter visa controls and asylum processing overhauls are complementing investments in technology, supporting the nation's capacity to control migration while maintaining national security. These combined efforts are continually enhancing border integrity.

Growing Threat of Natural Disasters and Public Health Emergencies

The growing number and severity of natural disasters and public health emergencies is offering a favorable homeland security market outlook. There were 27 separate weather and climate disasters with at least $1 billion in damages in 2024. The disasters resulted in at least 568 direct or indirect deaths, the eighth-highest for these billion-dollar disasters in the past 45 years (1980-2024). The cost was around $182.7 billion. Disasters like hurricanes, wildfires, earthquakes, and pandemics are putting huge strain on emergency response systems and infrastructure resistance. Governments are constantly adding investments in early warning systems, emergency communications networks, and disaster logistics platforms in order to improve preparedness and response capabilities. Agencies are also implementing AI and geospatial analysis software to forecast the effects of disasters and prioritize the distribution of resources. Public health readiness is receiving the same attention, with governments bolstering caches of medical equipment, enhancing the surge capacity of hospitals, and deploying mobile medical facilities. Federal, state, and local coordination of response planning is given priority so that quick and coordinated action can be undertaken during disasters. According to the homeland security market analysis, as such occurrences become more frequent and widespread with climate change and globalization, emergency and disaster management investments are becoming an integral part of homeland security, thus maintaining market growth.

Homeland Security Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global homeland security market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, system, and end-user.

Analysis by Type:

- Aviation Security

- Maritime Security

- Border Security

- Critical Infrastructure Security

- Cyber Security

- CBRN Security

- Mass Transit Security

- Others

Cyber security represents the largest segment. The cybersecurity segment is continuously expanding and diversifying, with various solution types addressing evolving digital threats, thereby driving the homeland security market demand. Network security is playing a crucial role, as organizations are deploying firewalls, intrusion detection systems, and secure access protocols to safeguard data transmission and prevent unauthorized access. Simultaneously, endpoint security is gaining momentum, with antivirus software, encryption tools, and mobile threat management solutions being implemented to protect individual devices from malware and phishing attacks. Cloud security is also witnessing rapid adoption as government agencies and enterprises are migrating operations to cloud environments. Providers are offering identity and access management (IAM), data loss prevention (DLP), and multi-factor authentication (MFA) solutions to secure virtualized infrastructures. Application security is being reinforced by integrating secure coding practices and vulnerability assessment tools during development lifecycles.

Analysis by System:

- Intelligence and Surveillance System

- Detection and Monitoring System

- Weapon System

- Access Control System

- Modelling and Simulation

- Communication System

- Platforms

- Rescue and Recovery System

- Command and Control System

- Countermeasure System

- Others

Intelligence and surveillance system lead the market. The intelligence and surveillance systems are constantly advancing as homeland security organizations are improving their abilities to observe, identify, and react to threats in real time. Ground-based monitoring systems are being extensively utilized, including radar technologies, unattended ground sensors, and vehicle-mounted devices, which are aiding in the protection of borders, military facilities, and essential infrastructure. These systems offer ongoing surveillance of high-risk zones and enable rapid reactions to intrusions or unusual activities. Aerial monitoring systems are also becoming more important, as drones and unmanned aerial vehicles (UAVs) are utilized more frequently for reconnaissance and situational awareness. These platforms are acquiring high-definition images and sending real-time information to command centers, thus enhancing decision-making in intricate settings.

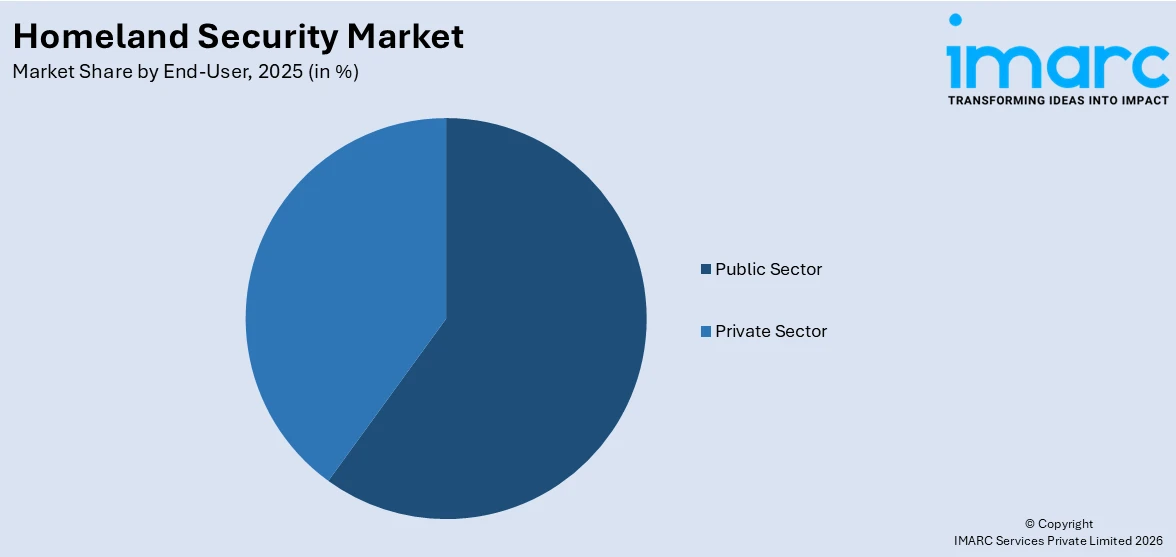

Analysis by End-User:

Access the comprehensive market breakdown Request Sample

- Public Sector

- Private Sector

Public sector leads the market with 60.2% of market share in 2025. The public sector consistently serves as a key end-user, generating significant demand for sophisticated technologies and comprehensive security solutions. Government entities at federal, state, and local tiers are significantly investing in systems that improve national security, emergency readiness, and public safety. Agencies including defense, border security, transportation, and law enforcement are utilizing advanced surveillance technologies, cyber protection systems, and data analysis platforms to address changing security challenges. Public sector organizations are increasingly utilizing command and control centers, real-time communication networks, and situational awareness systems to manage responses to both human-induced and natural disasters. Moreover, as per the homeland security market forecasts, these agencies are likewise incorporating geospatial intelligence, biometric systems, and AI-based decision-support tools to enhance operations and accelerate incident response times.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of 30.6%. The North America market is growing steadily as governments in the region are confronting an intricate environment of threats encompassing terrorism and cyberattacks to natural disasters and public health crises. Both the US and Canada are actively strengthening their homeland security architectures by investing in state-of-the-art technologies, multi-agency collaboration tools, and active threat mitigation strategies. Cybersecurity is also one of the most important fields that is being focused on by government agencies, public institutions, and private businesses alike, who are adopting strong security architectures to thwart advanced cyber threats. Zero-trust frameworks, real-time network monitoring tools, and endpoint detection systems are being used by authorities to bolster digital resilience. Cloud security and secure data-sharing protocols are being embraced across industries to safeguard sensitive information and infrastructure from breaches. The IMARC Group predicts that the US cloud security market size is expected to reach USD 31.2 Billion by 2033.

Key Regional Takeaways:

United States Homeland Security Market Analysis

The United States hold 87.20% share in the North America. The United States market is primarily driven by increasing cyberattacks, including ransomware and critical infrastructure breaches. According to CISA, cyberattacks on critical infrastructure increased by 30% globally last year, while ransomware incidents increased over 70% from 2022 to 2023, with government agencies ranking as the third-most targeted sector. Furthermore, rising investments in biometric identification and facial recognition technology strengthening border security and law enforcement efforts is propelling market growth. The expansion of unmanned aerial systems (UAS) for surveillance and threat detection improving situational awareness in high-risk areas is fostering market development. Additionally, growing concerns over domestic terrorism and mass shootings leading to increased deployment of AI-powered threat detection in public spaces is supporting market demand. The favorable smart city initiatives integrating surveillance, emergency response, and communication systems to enhance urban security are expanding the market scope. Similarly, the rise in climate-related disasters driving demand for disaster preparedness and emergency response technologies is augmenting market expansion. Moreover, continual advancements in artificial intelligence (AI) and predictive analytics enhancing risk assessment and real-time threat monitoring, is providing an impetus to the market.

Europe Homeland Security Market Analysis

The Europe market is expanding due to the rise of hybrid warfare tactics, including cyber espionage and disinformation campaigns. In line with this, growing concerns over cross-border terrorism and organized crime prompting governments to enhance surveillance, intelligence-sharing, and counterterrorism initiatives is bolstering the market. Similarly, stricter EU data protection and cybersecurity regulations accelerating investments in compliance-driven security solutions to safeguard sensitive information is propelling market growth. The increasing migration flows and intense border security challenges necessitating the deployment of biometric screening, automated border control systems, and AI-powered threat detection is fostering market expansion. IMF states that, in 2022, EU immigration of non-EU citizens reached 1.4% of its population, the highest level recorded, with 4 million Ukrainian refugees under the EU’s Temporary Protection Scheme significantly influencing migration trends, particularly in Central and Eastern Europe and Germany. Furthermore, the rise in extremist activities and lone-wolf attacks increasing the need for enhanced public space protection and emergency response measures is supporting market demand. Likewise, the expanding critical infrastructure protection, particularly in energy and transportation, remains a priority to mitigate potential threats, thereby creating lucrative opportunities in the market.

Asia Pacific Homeland Security Market Analysis

The market in Asia-Pacific is being propelled by the rising territorial disputes in the South China Sea and Indo-Pacific region. In addition to this, the rapid digital transformation across industries intensifying cyber threats, prompting significant investments in advanced cybersecurity infrastructure is propelling the market growth. The increase in transnational organized crime, including drug trafficking and human smuggling, leading to strengthened law enforcement cooperation and intelligence-sharing initiatives is augmenting market demand. According to the 2023 UNODC report, Myanmar became the world's largest opium producer, with cultivation reaching 116,000 acres, escalating drug trafficking risks in the NER, where contraband worth over USD 267 Million was seized in FY 2022-23. Furthermore, heightened investments in early warning systems and emergency response technologies strengthening disaster resilience are encouraging the higher uptake of the product. Moreover, the expansion of biometric identification, including facial recognition and iris scanning, improving security measures at airports, government facilities, and border checkpoints, is positively influencing the market.

Latin America Homeland Security Market Analysis

In Latin America, the market is expanding as governments address rising security threats through increased investments in surveillance, intelligence, and defense capabilities. In accordance with this, the growing influence of drug cartels and organized crime syndicates heightening the demand for advanced border security and intelligence-sharing initiatives is impelling the market. Furthermore, escalating urban crime rates and gang violence driving the deployment of AI-powered surveillance and real-time crime monitoring systems in major cities is expanding the market scope. According to an industry report, in 2023, over 40 of the world’s 50 most violent cities were in Latin America and the Caribbean (LAC), with Durán, Ecuador recording the highest homicide rate. Ecuador’s national homicide rate rose from 5.7 per 100,000 (2018) to 45.1 (2023), making it the most violent country. Apart from this, rising geopolitical instability accelerating military modernization efforts and defense strategies is providing an impetus to the market.

Middle East and Africa Homeland Security Market Analysis

The Middle East and Africa market is expanding attributed to the persistent risk of insurgencies and extremist groups prompting governments to enhance counterterrorism operations and border security infrastructure. In 2024, the Middle East witnessed a significant surge in cyberattacks, with nearly 25% of all reported incidents targeting government entities. These attacks predominantly involved ransomware and wiper malware, such as the notorious "BiBi Wiper," aimed at destabilizing critical operations in Israel. This growing threat landscape underscores the increasing vulnerability of governmental systems to sophisticated cyber warfare tactics, prompting heightened cybersecurity measures across the region. As cyber threats continue to evolve, governments are focusing on enhancing their defense strategies, investing in advanced security technologies to safeguard national infrastructure and mitigate risks associated with digital disruptions.

Competitive Landscape:

Market participants in the homeland security industry are constantly involved in strategic initiatives to reinforce their market position and respond to changing threats. Organizations are spending on research and development to develop sophisticated surveillance systems, cybersecurity tools, and biometric solutions. They are entering into partnerships with government departments and technology companies to co-create converged security platforms and broaden their solution offerings. Mergers and acquisitions (M&A) are also occurring, allowing companies to expand their competencies and reach new markets. Further, the players are competing aggressively in government tenders and contracts, primarily for infrastructure security, emergency response, and border control initiatives. By emphasizing innovation, collaboration, and growth, these companies are leading the drive in the homeland security market.

The report provides a comprehensive analysis of the competitive landscape in the homeland security market with detailed profiles of all major companies, including:

- Accenture PLC

- The Boeing Company

- Booz Allen Hamilton Inc.

- General Dynamics Corporation

- The General Electric Company

- International Business Machines (IBM) Corporation

- L3Harris Technologies, Inc.

- Lockheed Martin Corporation

- SAIC Motor Corporation Limited

- Unisys Corporation

Latest News and Developments:

- March 2025: Skylark Labs launched the Scout MK II AI Tower, an advanced mobile surveillance system for border security. Featuring Kepler AI, it enables real-time, autonomous threat detection with a 3-mile range, adaptive learning, and all-terrain deployment. It enhances border surveillance against changing threats like smuggling and trafficking.

- February 2025: ADASI, a leader in UAV system manufacturing, announced the adoption of Perceptra (GPS-less navigation) and Saluki (secure flight control) to enhance aviation security. These technologies prevent GPS jamming and spoofing, ensuring precise, AI-powered autonomous navigation for UAVs. Unveiled at IDEX 2025, they strengthen defense, commercial aviation, and urban drone operations in complex airspaces.

- December 2024: Rakuten Symphony introduced Rakuten Maritime, a cybersecurity service for autonomous vessels and smart ships. Developed with CYTUR, it integrates IoT, cloud, and zero-trust security, ensuring compliance with IACS regulations. It enhances threat detection, operational efficiency, and risk management, revolutionizing maritime cybersecurity and digital transformation.

- September 2024: SITA launched Managed Network Access Control (NAC) to enhance cyber security for airport and airline networks. The solution strengthens LAN and Wireless LAN security, segments networks, and ensures compliance with industry standards. Built on Cisco’s ISE platform, it follows a zero-trust model for secure access control.

- March 2024: Garuda Aerospace, unveiled Trishul, a border patrol surveillance drone equipped with high-definition cameras, infrared, and radar. Designed for security, disaster monitoring, and traffic assessment, it ensures real-time data access and enhances decision-making in a sustainable drone ecosystem.

Homeland Security Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Aviation Security, Maritime Security, Border Security, Critical Infrastructure Security, Cyber Security, CBRN Security, Mass Transit Security, Others |

| Systems Covered | Intelligence and Surveillance System, Detection and Monitoring System, Weapon System, Access Control System, Modelling and Simulation, Communication System, Platforms, Rescue and Recovery System, Command and Control System, Countermeasure System, Others |

| End-Users Covered | Public Sector, Private Sector |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Accenture PLC, The Boeing Company, Booz Allen Hamilton Inc., General Dynamics Corporation, The General Electric Company, International Business Machines (IBM) Corporation, L3Harris Technologies, Inc., Lockheed Martin Corporation, SAIC Motor Corporation Limited, Unisys Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the homeland security market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global homeland security market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the homeland security industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Homeland Security Market Report Report

The homeland security market was valued at USD 666.9 Billion in 2025.

The homeland security market is projected to exhibit a CAGR of 4.68% during 2026-2034, reaching a value of USD 1,019.4 Billion by 2034.

The homeland security market is being driven by increasing cyber threats targeting critical infrastructure, growing efforts to secure borders and manage immigration, and rising incidences of natural disasters and public health emergencies, prompting sustained investment in advanced surveillance, cybersecurity, and emergency response technologies.

North America currently dominates the homeland security market, accounting for a share of 30.6%. This is due to heightened investments in cybersecurity infrastructure, advanced surveillance systems, and disaster preparedness technologies, primarily driven by the United States and Canada.

Some of the major players in the homeland security market include Accenture PLC, The Boeing Company, Booz Allen Hamilton Inc., General Dynamics Corporation, The General Electric Company, International Business Machines (IBM) Corporation, L3Harris Technologies, Inc., Lockheed Martin Corporation, SAIC Motor Corporation Limited, Unisys Corporation, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)