Hospital Beds Market Size, Share, Trends and Forecast by Technology, Bed Type, Usage, End User, and Region, 2026-2034

Global Hospital Beds Market Size, Share, Trends & Forecast (2026-2034)

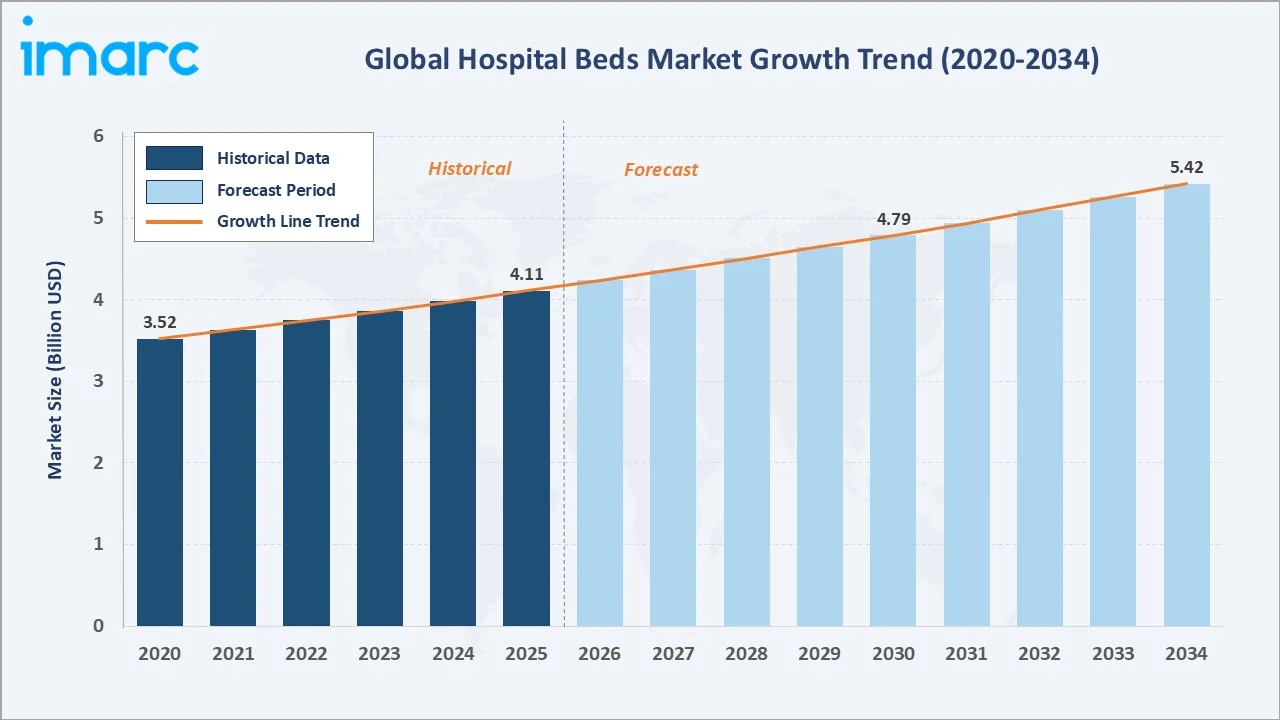

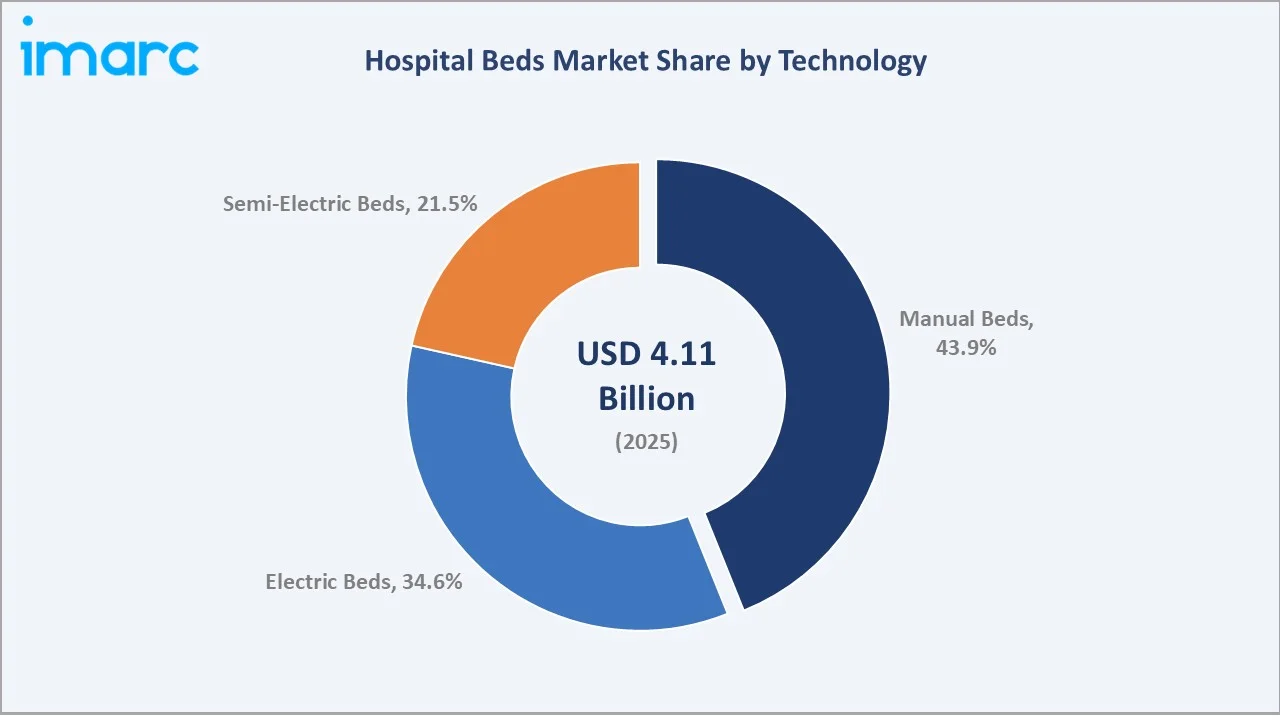

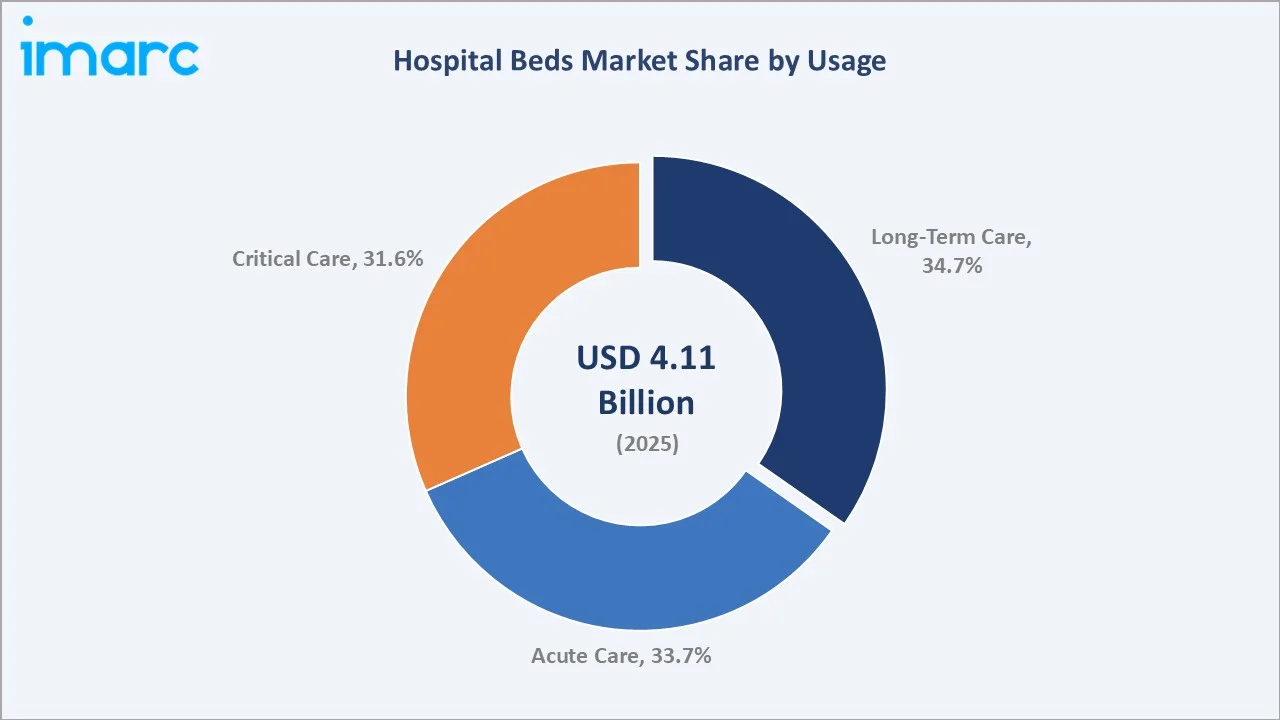

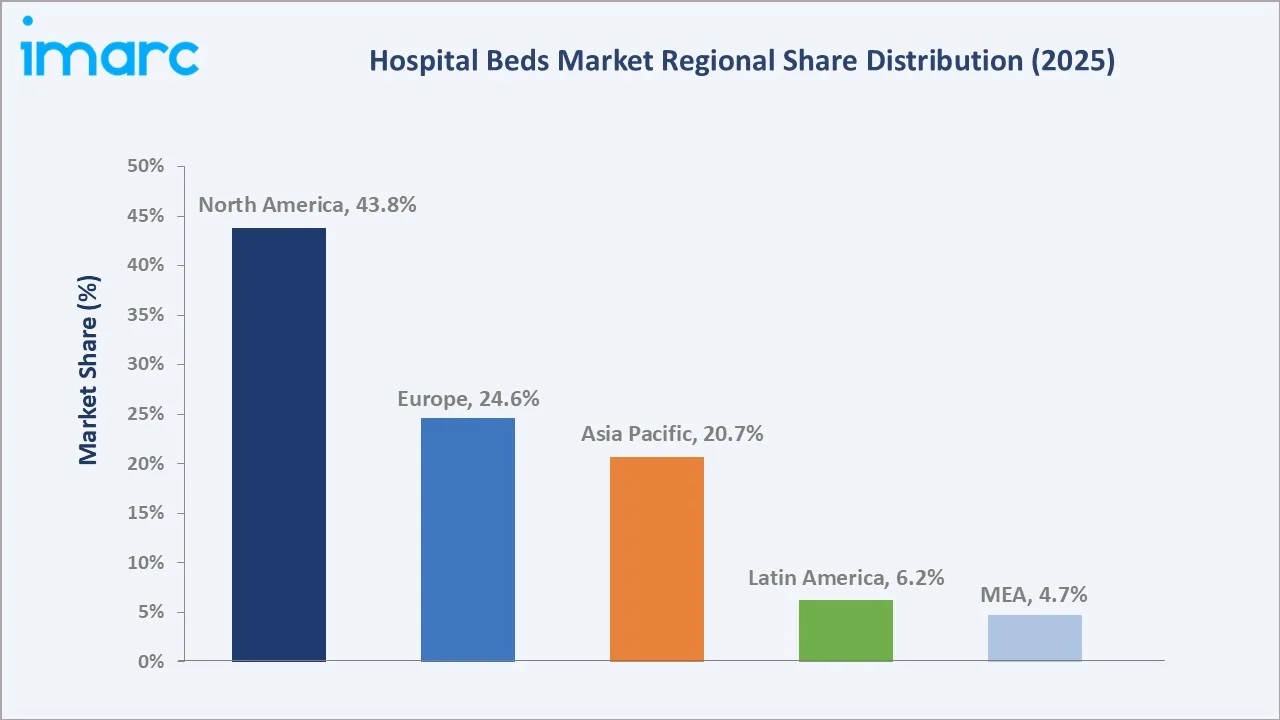

The global hospital beds market size was valued at USD 4.11 Billion in 2025 and is projected to reach USD 5.42 Billion by 2034, exhibiting a CAGR of 3.12% during 2026-2034. Rapid expansion of healthcare infrastructure, rising geriatric population, escalating burden of chronic diseases, and accelerating adoption of electric and smart hospital beds are collectively driving hospital beds market growth. Long-term care leads by usage with a 34.7% share in 2025, while manual beds dominate by technology with a 43.9% share. North America commands global leadership with a 43.8% revenue share in 2025, supported by mature hospital networks, high Medicare reimbursement, and technology-led bed modernization programs.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.11 Billion |

|

Forecast Market Size (2034) |

USD 5.42 Billion |

|

CAGR (2026-2034) |

3.12% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (43.8% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Usage Segment |

Long-Term Care (34.7%, 2025) |

|

Leading Technology Segment |

Manual Beds (43.9%, 2025) |

The chart below illustrates hospital beds market expansion from 2020-2034, with steady post-pandemic recovery shaping historical growth and rising demand for chronic-care beds supporting the forecast.

To get more information on this market, Request Sample

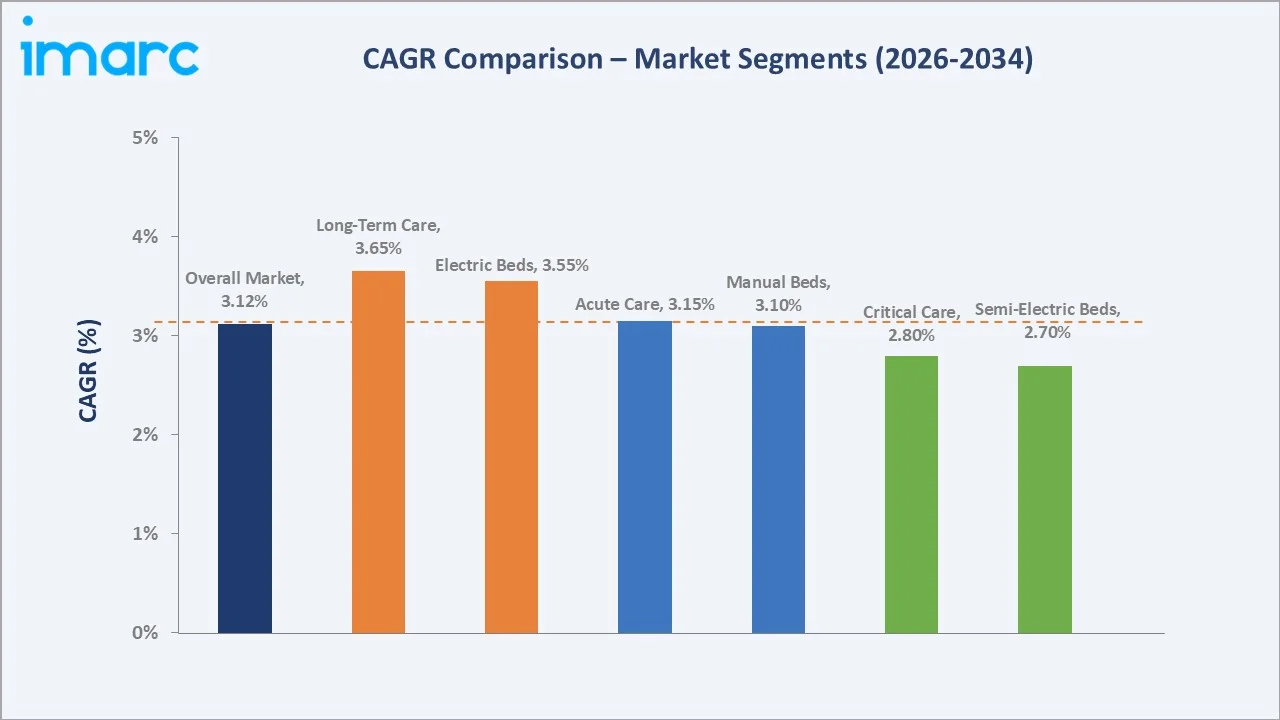

CAGR analysis highlights long-term care and electric beds as the fastest-growing sub-segments, reflecting the shift toward extended care and smart bed adoption across global hospital networks.

Executive Summary

The global hospital beds market is evolving steadily, shaped by aging demographics, chronic disease growth, and rising investment in hospital modernization. Valued at USD 4.11 billion in 2025, the market is expected to reach USD 5.42 billion by 2034, expanding at a 3.12% CAGR. Post-pandemic capacity expansion and bed replacement cycles continue to anchor demand across developed and emerging healthcare systems.

Manual beds lead by technology with a 43.9% share in 2025, supported by affordability and reliability across lower-tier hospitals and long-term care facilities. Long-term care holds a 34.7% share by usage, driven by senior care expansion in the U.S., Japan, and Europe. Key trends include adoption of IoT-enabled smart beds, pressure-ulcer prevention systems, and integration with electronic health records for real-time monitoring.

North America commands a 43.8% global revenue share in 2025, reinforced by high healthcare spending, advanced hospital networks, and strong presence of Hill-Rom (Baxter), Stryker, and Invacare. Europe follows at 24.6%, supported by Germany, France, and the UK. Asia Pacific, at 20.7%, is the fastest-growing region, fueled by rapid hospital construction and government-led healthcare programs across China and India.

Key Market Insights

|

Insight |

Data |

|

Largest Technology Segment |

Manual Beds - 43.9% share (2025) |

|

Second Technology Segment |

Electric Beds - 34.6% share (2025) |

|

Leading Usage Segment |

Long-Term Care - 34.7% share (2025) |

|

Leading Region |

North America - 43.8% revenue share (2025) |

|

Second Region |

Europe - 24.6% revenue share (2025) |

|

Top Companies |

Hill-Rom (Baxter), Stryker, Paramount Bed, Invacare |

Key Analytical Observations Supporting the Above Data:

- Manual beds' 43.9% share in 2025 reflects continued demand across mid-tier hospitals, rural facilities, and long-term care centers where cost efficiency and durability outweigh motorized functionality requirements.

- Electric beds at 34.6% in 2025 are gaining faster traction in tertiary hospitals, ICUs, and premium care settings where clinician workload reduction and patient safety justify the higher per-unit price point.

- Long-term care's 34.7% share in 2025 is supported by aging populations, with the global 65+ population expected to nearly double to 1.6 billion by 2050, driving sustained demand for specialized senior-care beds.

- North America's 43.8% global dominance in 2025 reflects high per-capita healthcare spending of over USD 14,000, extensive ICU capacity, and strong Medicare reimbursement supporting hospital bed procurement and replacement cycles.

- Asia Pacific's position as the fastest-growing region is underpinned by large hospital construction pipelines in China and India, with India adding more than 100,000 hospital beds annually across public and private systems.

- Baxter (including Hillrom) and Stryker are leading players in the hospital beds and patient support systems segment, with combined total company revenues exceeding USD 30 billion in 2024. However, only a portion of this revenue is directly attributable to hospital bed-related products.

Global Hospital Beds Market Overview

The hospital beds market includes specialized beds used in critical, acute, and long-term care, ranging from manual to advanced electric models with monitoring and safety features. It involves a broad ecosystem of suppliers, manufacturers, distributors, regulators, and healthcare providers enabling continuous patient care.

Hospital beds are deployed across tertiary hospitals, community clinics, ASCs, long-term care facilities, and home care environments. Growth is supported by rising chronic disease prevalence, aging populations, expanding hospital capacity in Asia Pacific, and stricter patient-safety regulations that drive upgrades from older manual beds to modern electric and semi-electric platforms.

Market Dynamics

To evaluate market opportunities, Request Sample

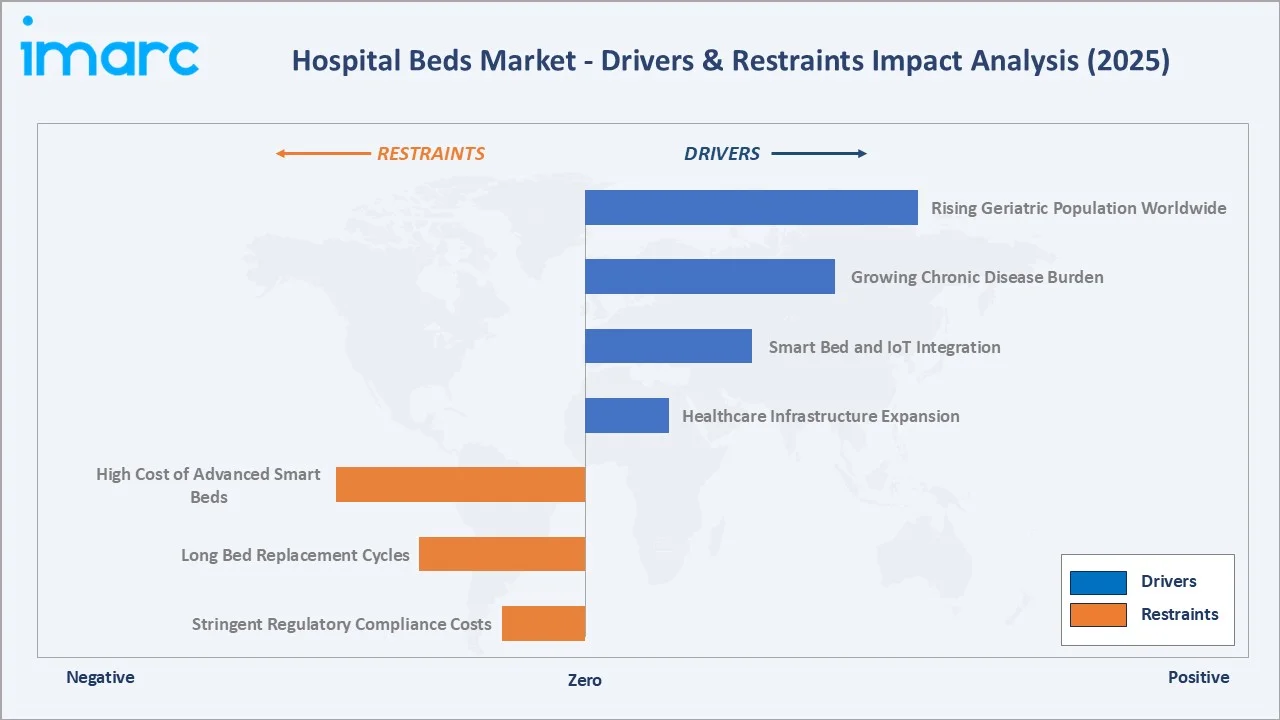

Market Drivers

- Rising Geriatric Population Worldwide: The share of people aged 65 and above is projected to reach 16% of the global population by 2050, according to the United Nations, creating sustained demand for long-term care beds, pressure-relief systems, and senior-friendly adjustable designs across global healthcare systems.

- Growing Chronic Disease Burden: Noncommunicable diseases cause about 74% of global deaths, according to the World Health Organization. Increasing prevalence of cardiovascular diseases, diabetes, cancer, and respiratory disorders is driving higher hospital admissions, supporting sustained demand for ICU, acute care, and rehabilitation beds globally.

- Smart Bed and IoT Integration: Hospitals are rapidly upgrading to beds with integrated sensors, EHR connectivity, and bed-exit alarms. Hill-Rom's Centrella and Stryker's ProCuity platforms are accelerating replacement cycles across U.S. and European hospital networks.

- Healthcare Infrastructure Expansion: Rising global healthcare spending and infrastructure expansion are supporting new hospital construction, capacity additions, and modernization of facilities, driving demand for hospital beds across emerging and developed markets worldwide.

Market Restraints

- High Cost of Advanced Electric and Smart Beds: Advanced electric and smart hospital beds are significantly more expensive than manual models, limiting adoption in price-sensitive public healthcare systems across emerging regions, where cost constraints favor basic bed procurement.

- Long Bed Replacement Cycles: Hospital beds typically remain in use for over a decade, leading to slow replacement cycles and uneven procurement demand, particularly in mature healthcare markets with established infrastructure and budget constraints.

- Stringent Regulatory Compliance Costs: Medical beds must comply with strict regulatory standards such as FDA 510(k), CE marking, and IEC safety norms, increasing development costs and delaying product approvals, especially for smaller manufacturers.

Market Opportunities

- Emerging Market Hospital Expansion: Government-led healthcare expansion programs such as Ayushman Bharat are increasing hospital infrastructure and bed capacity across India and China, driving sustained demand for hospital beds in Asia Pacific.

- Home Healthcare Bed Segment Growth: Rising preference for home-based care across North America and Europe is increasing demand for home-use hospital beds, including electric and specialty beds, supported by aging populations and chronic disease prevalence.

- AI-Enabled Smart Bed Platforms: Beds integrating AI fall detection, automatic repositioning, and real-time vital-sign monitoring are gaining adoption in ICU and critical-care settings, with Stryker, Hill-Rom, and Getinge actively investing in this category.

Market Challenges

- Supply Chain Disruptions and Component Costs: Rising raw material and component costs, along with supply chain disruptions during and after the COVID-19 pandemic, increased manufacturing expenses and pressured margins for medical equipment producers.

- Skilled Service Technician Shortages: Smart and electric beds require trained field service technicians for calibration and repair. Technician shortages across emerging markets limit after-sales support and slow electric bed adoption in Tier-2 and Tier-3 cities.

- Hospital Capital Budget Constraints: Fiscal pressures on public healthcare systems, particularly across Europe, are leading hospitals to defer capital expenditures and extend equipment lifecycles, reducing short-term demand for hospital bed replacement and upgrades.

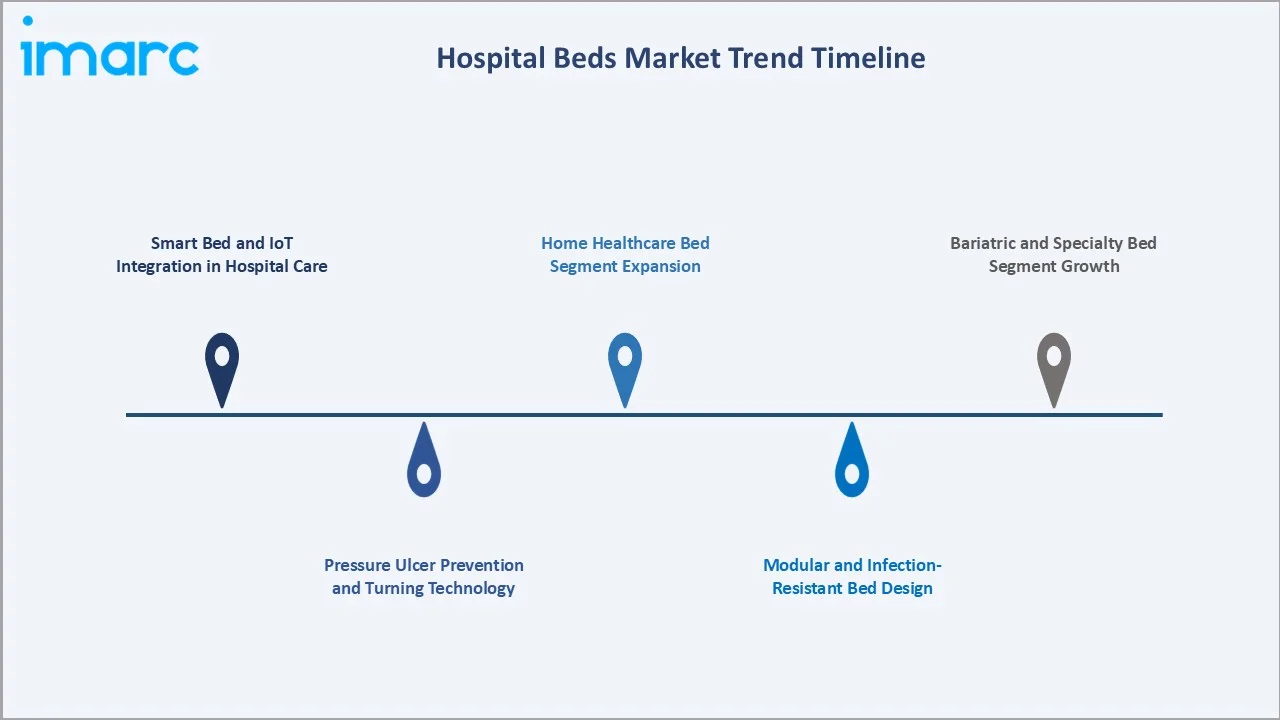

Emerging Market Trends

1. Smart Bed and IoT Integration in Hospital Care

IoT-enabled beds with built-in sensors for weight, heart rate, and patient movement are being adopted in ICU and acute care units. Hill-Rom's Centrella Smart+ Bed and Stryker's ProCuity RC beds use real-time data to reduce falls and improve nurse workflows.

2. Pressure Ulcer Prevention and Turning Technology

Advanced pressure redistribution and lateral rotation systems are increasingly used in critical and long-term care beds, helping reduce pressure ulcer risk and improving patient outcomes, though reduction rates vary across clinical settings.

3. Home Healthcare Bed Segment Expansion

Demand for home-use electric beds is rising sharply as more chronic and post-acute care shifts out of hospitals. Invacare and Drive DeVilbilt lead home-care bed distribution across North America, serving Medicare and insurance-covered segments.

4. Modular and Infection-Resistant Bed Design

Post-COVID-19 pandemic, demand has increased for hospital beds with antimicrobial materials and easy-clean designs, supporting infection prevention protocols and improving operational efficiency in healthcare facilities.

5. Bariatric and Specialty Bed Segment Growth

Rising obesity prevalence in regions like North America and Europe is increasing demand for bariatric hospital beds with higher weight capacities, with companies such as Stryker Corporation expanding specialty portfolios.

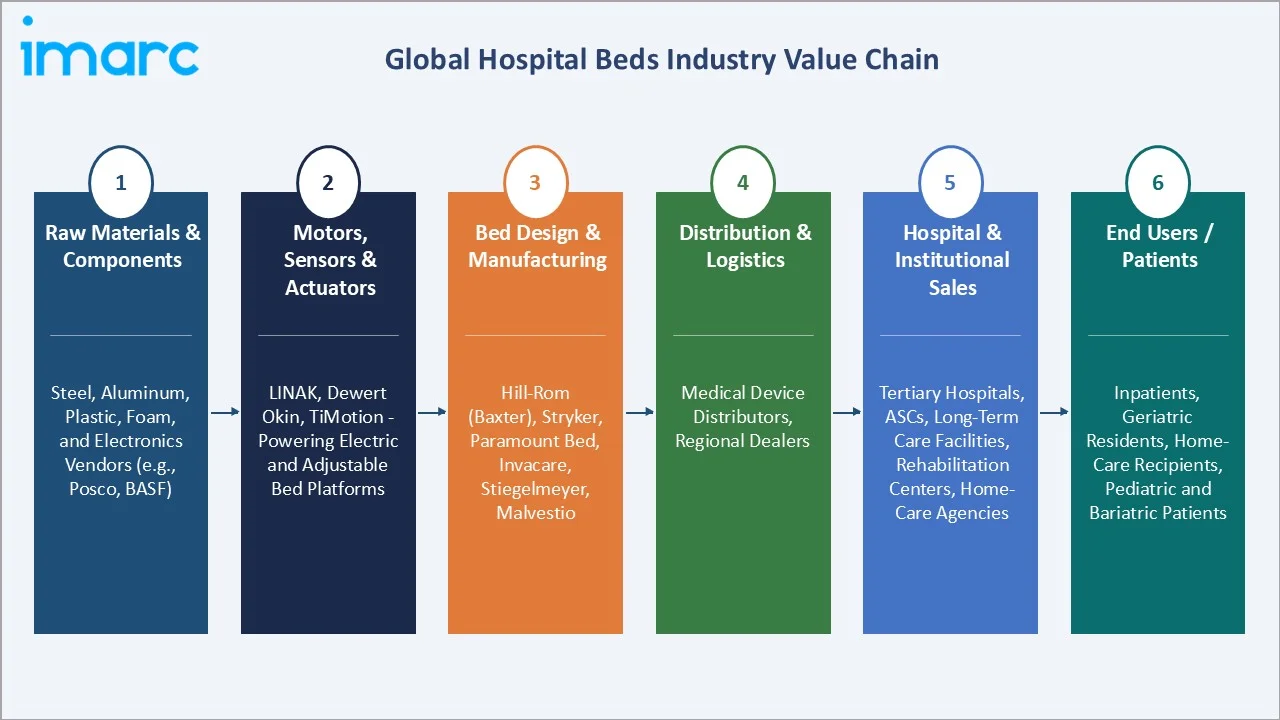

Industry Value Chain Analysis

The hospital beds value chain spans five stages, from raw material sourcing to end-user care delivery, each with distinct economics, supplier structures, and margin profiles that influence competitive dynamics.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Steel, aluminum, plastic, foam, and electronics vendors (e.g., Posco, BASF) |

|

Motors, Sensors & Actuators |

LINAK, Dewert Okin, TiMotion - powering electric and adjustable bed platforms |

|

Bed Design & Manufacturing |

Hill-Rom (Baxter), Stryker, Paramount Bed, Invacare, Stiegelmeyer, Malvestio |

|

Distribution & Logistics |

Medical device distributors, regional dealers |

|

Hospital & Institutional Sales |

Tertiary hospitals, ASCs, long-term care facilities, rehabilitation centers, home-care agencies |

|

End Users / Patients |

Inpatients, geriatric residents, home-care recipients, pediatric and bariatric patients |

Tier-1 global manufacturers capture the highest value by combining design, manufacturing, and service contracts, while raw material and component vendors operate on thinner, commodity-like margins.

Technology Landscape in the Hospital Beds Industry

Smart Bed Connectivity and Sensor Integration

Modern hospital beds now integrate pressure sensors, weight scales, bed-exit alarms, and wireless connectivity to hospital electronic health records, enabling real-time patient monitoring and reducing nursing workloads across ICUs and acute care wards.

Electric Actuation and Motor Technology

LINAK and TiMotion supply compact, quiet-drive actuators that support multi-position adjustment of head, knee, and trendelenburg positions. Electric beds now offer up to five adjustment axes, enabling improved clinical ergonomics and patient comfort.

Materials Innovation and Infection Control

Antimicrobial coatings, copper-alloy surfaces, and seamless bed designs are increasingly used to reduce microbial contamination and support infection control, with studies showing significant bacterial reduction on treated hospital surfaces.

Automation and Robotic Assistance

Emerging technologies include automatic patient turning, AI-assisted fall detection, and integrated weighing without repositioning. Stryker's ProCuity RC beds offer fully wireless architectures that streamline maintenance and enable future-ready software updates.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

Manual Beds |

43.9% |

2025 |

|

Bed Type |

🔒 |

🔒 |

2025 |

|

Usage |

Acute Care |

33.7% |

2025 |

|

End User |

Hospitals and Clinics |

52.2% |

2025 |

|

Region |

North America |

43.8% |

2025 |

By Technology

Manual beds dominate with a 43.9% share in 2025, driven by strong adoption in price-sensitive public hospitals, long-term care facilities, and Tier-2/Tier-3 cities across emerging markets. Their simple mechanical architecture ensures low maintenance and long useful life.

To access detailed market analysis, Request Sample

Electric beds account for 34.6% in 2025, with strong growth in tertiary hospitals, ICUs, and premium private-care settings where patient safety, clinician ergonomics, and advanced monitoring justify the higher per-unit investment cost. Semi-electric beds hold 21.5% in 2025, serving as a transitional option balancing affordability and functionality. These beds are widely used in community hospitals, step-down care units, and home-healthcare across North America and Europe.

By Usage

Long-term care leads with a 34.7% share in 2025, supported by aging populations, rising dementia and rehabilitation demand, and growing senior living capacity across the U.S., Japan, Germany, and the UK. This segment grows faster than overall market average.

Acute care holds 33.7% in 2025, anchored by general hospital wards that handle post-surgical recovery, short-stay admissions, and emergency overflow. Regular and pressure-relief beds dominate procurement in this segment across global hospital systems. Critical care accounts for 31.6% in 2025, driven by ICU expansion, cardiac and respiratory care units, and high-acuity trauma centers. ICU-specific beds with advanced monitoring, integrated scales, and pressure therapy command premium per-unit pricing.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

43.8% |

Large Medicare reimbursement base, advanced hospital networks, premium electric bed adoption, ICU expansion |

|

Europe |

24.6% |

Aging population in Germany, UK, France; strong regulatory standards; hospital modernization programs |

|

Asia Pacific |

20.7% |

Rapid hospital construction in India and China, rising healthcare spending, public health infrastructure investment |

|

Latin America |

6.2% |

Brazil and Mexico hospital network expansion, rising chronic disease burden, private hospital investment |

|

Middle East & Africa |

4.7% |

GCC healthcare city projects, Saudi Vision 2030, growing medical tourism, new hospital construction |

North America commands 43.8% of the global hospital beds market in 2025, anchored by high per-capita healthcare spending and rapid adoption of electric and smart beds. The United States alone operates over 900,000 staffed hospital beds, with consistent annual replacement and modernization activity.

Europe holds 24.6% in 2025, supported by mature hospital networks in Germany, France, the UK, and Italy. Aging populations, public health system investment, and stringent safety standards continue to drive steady demand for premium electric and semi-electric beds. Asia Pacific, at 20.7% in 2025, is the fastest-growing regional market, fueled by rapid hospital capacity expansion in China and India, along with strong growth in Southeast Asia and Japan's sustained long-term care investment. The region will close the gap on North America through 2034.

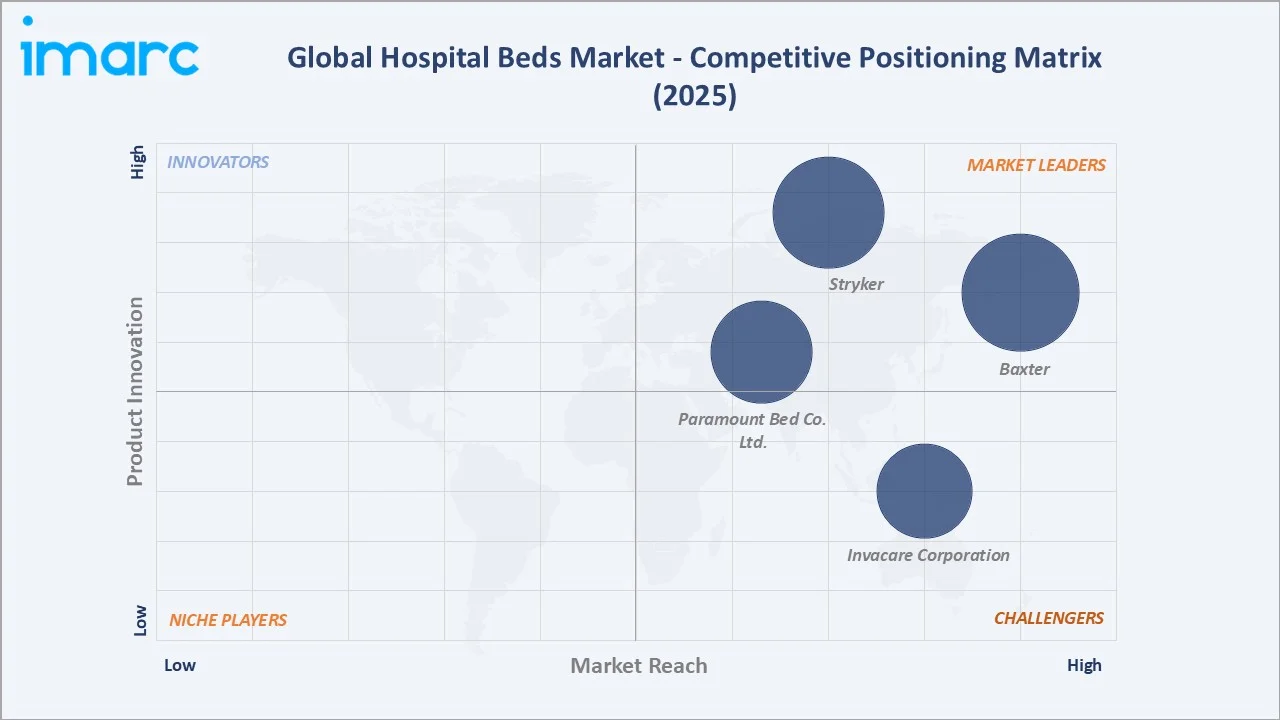

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Baxter |

Centrella / Progressa / VersaCare |

Leader |

Smart beds, connected bed platforms, global scale |

|

Stryker |

ProCuity / InTouch |

Leader |

U.S. hospital leadership, wireless bed innovation |

|

Paramount Bed Co. Ltd. |

A5 / A6 / KK-810A Series |

Leader |

Japan & APAC dominance, senior care specialization |

|

Invacare Corporation |

Medley / CS7 |

Challenger |

Home-care beds, North America, long-term care |

The hospital beds market is moderately concentrated, with Baxter (Hill-Rom), Stryker, and Paramount Bed Co. Ltd. leading premium and ICU segments, while regional specialists such as Invacare Corporation dominate their home markets. Baxter’s 2024 revenue from continuing operations was approximately USD 10.6 billion. While Hill-Rom-derived products contribute within its Healthcare Systems segment.

Key Company Profiles

Baxter

Baxter, headquartered in Deerfield, Illinois, acquired Hillrom in 2021 for $12.5 billion, strengthening its hospital bed portfolio. The company reported about $11.24 billion revenue (2025) and is refocusing on medtech after divesting its Kidney Care (Vantive) business.

- Product & Service Portfolio: Baxter (via Hillrom) offers smart hospital beds (Centrella, Progressa, VersaCare, CareAssist), patient support surfaces, monitoring-integrated beds, and connected care platforms such as Voalte for clinical communication and digital patient management.

- Recent Developments: In 2024, Baxter announced the sale of its Kidney Care unit (Vantive) to Carlyle for $3.8 billion to enhance strategic focus and reduce debt, sharpening emphasis on medical devices including hospital beds and connected care.

- Strategic Focus: Baxter focuses on connected bed platforms, ICU and acute-care bed leadership, and expanding smart hospital solutions integrating EHR connectivity, fall prevention, and patient mobility capabilities across global healthcare networks.

Stryker

Stryker, headquartered in Michigan, is a leading global medical technology company, reporting $22.6 billion revenue in 2024 and $25.1 billion in 2025, driven by MedSurg and Neurotechnology segments, including hospital beds, stretchers, and patient handling solutions.

- Product & Service Portfolio: Stryker offers hospital beds (ProCuity, InTouch, S3), stretchers (SecureFit), support surfaces, and integrated patient handling and emergency care solutions within its MedSurg portfolio.

- Recent Developments: In January 2026, Stryker reported FY2025 revenue of $25.1 billion, with strong growth in its MedSurg and Neurotechnology segment (including beds), supported by product innovation and increased hospital demand.

- Strategic Focus: Stryker focuses on advancing connected and wireless hospital bed ecosystems, integrating patient safety, fall prevention, and digital connectivity across acute care, emergency, and surgical workflows to strengthen its MedSurg leadership.

Paramount Bed Co. Ltd.

Paramount Bed Co., Ltd., headquartered in Tokyo, Japan, is a leading manufacturer of hospital and nursing care beds, specializing in electric and smart beds. The company operates globally, particularly in Asia, and is recognized for advanced patient care and rehabilitation solutions.

- Product & Service Portfolio: Paramount Bed offers hospital and long-term care beds (electric, ICU, and nursing beds), mattresses, patient transfer aids, and smart care solutions, including product lines such as A5 Series and Qualitas beds designed for acute and elderly care settings.

- Recent Developments: In 2025, Paramount Bed continues to promote advanced models such as the A5 Series and Qualitas beds, focusing on improved patient safety, ergonomics, and smart monitoring capabilities aligned with evolving hospital and eldercare needs.

- Strategic Focus:Paramount Bed focuses on expanding its global presence in acute and long-term care by developing smart, ergonomic hospital beds integrated with patient monitoring, mobility support, and aging-care solutions, particularly targeting Asia’s rapidly growing elderly population.

Market Concentration Analysis

The global hospital beds market is moderately concentrated. Baxter (Hill-Rom), Stryker, and Paramount Bed collectively account for approximately 35-40% of global revenue in 2025, supported by strong brand equity, global distribution, and broad product portfolios spanning ICU, acute care, and long-term care.

Fragmentation increases at the regional level, with companies such as Stiegelmeyer (Germany), Malvestio (Italy), Savion, and Span-America focusing on specific geographies or product niches. Manual and semi-electric bed segments in emerging markets remain especially fragmented, with local Chinese and Indian manufacturers supplying public hospitals at lower price points.

Consolidation activity is gradually accelerating. Baxter's USD 12.5 billion acquisition of Hill-Rom in 2021 was a transformative deal, and larger OEMs continue to evaluate bolt-on acquisitions in pressure-relief surfaces, home-care beds, and digital care platforms to strengthen connected care offerings.

Investment & Growth Opportunities

Fastest-Growing Segments

Long-term care and geriatric beds are among the fastest-growing segments, driven by aging populations. According to the World Health Organization, the global population aged 60+ will reach ~2.1 billion by 2050, supporting demand for senior-care beds and pressure-relief solutions.

Electric and smart hospital beds are expected to grow faster than the overall market due to hospital modernization and replacement of outdated manual beds, particularly across advanced healthcare systems.

Emerging Market Expansion

Asia Pacific, currently at 20.7% of the global market, offers major growth potential through hospital infrastructure expansion in India, China, Indonesia, and Vietnam. India’s hospital capacity expansion under Ayushman Bharat – PMJAY and related healthcare initiatives is driving gradual increases in bed capacity.

The Middle East and Africa, at 4.7% in 2025, is growing steadily through Saudi Arabia's Vision 2030 healthcare investments, UAE hospital expansion, and GCC medical tourism programs. Specialty ICU and bariatric beds are emerging as premium procurement categories in this region.

Venture & Strategic Investment Trends

Investment in smart hospital technologies - including AI-driven patient monitoring, remote care platforms, and predictive-maintenance bed software - is increasing. Strategic acquirers including Baxter, Stryker, and Getinge continue to evaluate bolt-on deals in digital health, sensor integration, and pressure-relief surface innovation.

Future Market Outlook (2026-2034)

The global hospital beds market forecast projects value expansion from USD 4.11 billion in 2025 to USD 5.42 billion by 2034 at a CAGR of 3.12%, representing a USD 1.31 billion expansion through the forecast period. Growth will be driven by aging populations, hospital modernization, electric bed adoption, and Asia Pacific infrastructure build-out.

Three transformational shifts will reshape the industry through 2034. First, smart beds integrating AI fall detection and continuous monitoring will become standard in ICU and tertiary care. Second, home-healthcare bed demand will accelerate as post-acute and chronic care continues shifting out of hospitals. Third, modular, infection-resistant, and sustainable bed designs will redefine sourcing and procurement standards across global hospital systems.

By 2034, hospital beds are expected to evolve from static furniture into active care delivery platforms, integrating clinical monitoring, data analytics, and patient workflow tools. Manufacturers investing in digital connectivity, fall-prevention technology, and sustainability will capture disproportionate share of premium hospital procurement budgets.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with hospital procurement officers, biomedical engineering directors, senior-care facility operators, distributor executives, and bed manufacturer product managers across North America, Europe, Asia Pacific, and select emerging markets.

Secondary Research

Secondary sources include company annual reports (Baxter, Stryker, Paramount Bed Co. Ltd., and Invacare Corporation), regulatory disclosures (FDA 510(k), CE database), industry trade bodies (AdvaMed, MedTech Europe), WHO healthcare infrastructure reports, and hospital capacity databases maintained by AHA, OECD, and national health ministries.

Forecasting Models

Market size and growth projections were built using a combined top-down and bottom-up approach, integrating hospital bed stock estimates, annual replacement cycle assumptions, new hospital construction pipelines, per-capita healthcare spending trends, and scenario analysis under base, optimistic, and conservative assumptions.

Hospital Beds Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Electric Beds, Semi-Electric Beds, Manual Beds |

| Bed Types Covered | Regular Beds, Pediatrics Bed, Respiratory Beds, ICU Beds, Bariatric Beds, Birthing Beds, Pressure Relief Beds, Others |

| Usages Covered | Critical Care, Acute Care, Long-Term Care |

| End Users Covered | Hospitals and Clinics, Ambulatory Surgery Centers (ASCs), Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Baxter, Stryker, Paramount Bed Co. Ltd., Invacare Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the hospital beds market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global hospital beds market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the hospital beds industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Hospital Beds Market Report

The global hospital beds market was valued at USD 4.11 Billion in 2025, supported by rising chronic disease prevalence, aging populations, and ongoing hospital bed replacement and modernization programs globally.

The market is projected to reach USD 5.42 Billion by 2034, growing at a CAGR of 3.12% during 2026-2034, driven by electric bed adoption, senior care expansion, and Asia Pacific infrastructure investment.

Manual beds lead with a 43.9% share in 2025, supported by affordability, durability, and strong demand across public hospitals, long-term care facilities, and emerging market healthcare infrastructure.

Long-term care leads with a 34.7% share in 2025, fueled by aging populations, chronic disease prevalence, senior living expansion, and rehabilitation demand across the U.S., Europe, and Japan.

North America leads with a 43.8% share in 2025, anchored by high healthcare spending, advanced hospital networks, Medicare reimbursement, and early adoption of smart and electric hospital beds.

Key drivers include rising geriatric populations, chronic disease growth, hospital infrastructure expansion, smart bed and IoT adoption, and increasing government healthcare spending across developed and emerging markets.

Asia Pacific is the fastest-growing region, driven by rapid hospital construction, aging populations in Japan and China, India's healthcare expansion, and government-led public health infrastructure investment through 2034.

Leading companies include Baxter, Stryker, Paramount Bed Co. Ltd., and Invacare Corporation.

Electric beds hold a 34.6% share in 2025, with rising adoption in ICUs, tertiary hospitals, and premium care settings due to clinician ergonomics, patient safety, and advanced monitoring features.

Smart bed adoption is driven by patient safety improvements, fall prevention, EHR integration, nurse workflow efficiency, and the ability to collect continuous clinical data for better decision-making.

AI fall detection, wireless bed platforms, pressure-ulcer prevention surfaces, and connected monitoring are improving clinical outcomes, reducing hospital-acquired complications, and accelerating replacement of legacy manual beds.

Hospitals and clinics represent the largest application for hospital beds, supported by inpatient admissions, ICU capacity, acute care wards, and ongoing replacement cycles across tertiary and community hospitals worldwide.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade