Hybrid Electric Vehicle Market Size, Share, Trends and Forecast by Propulsion Type, Configuration Type, Vehicle Type, Power Source, and Region, 2026-2034

Global Hybrid Electric Vehicle Market Size, Share, Trends & Forecast (2026-2034)

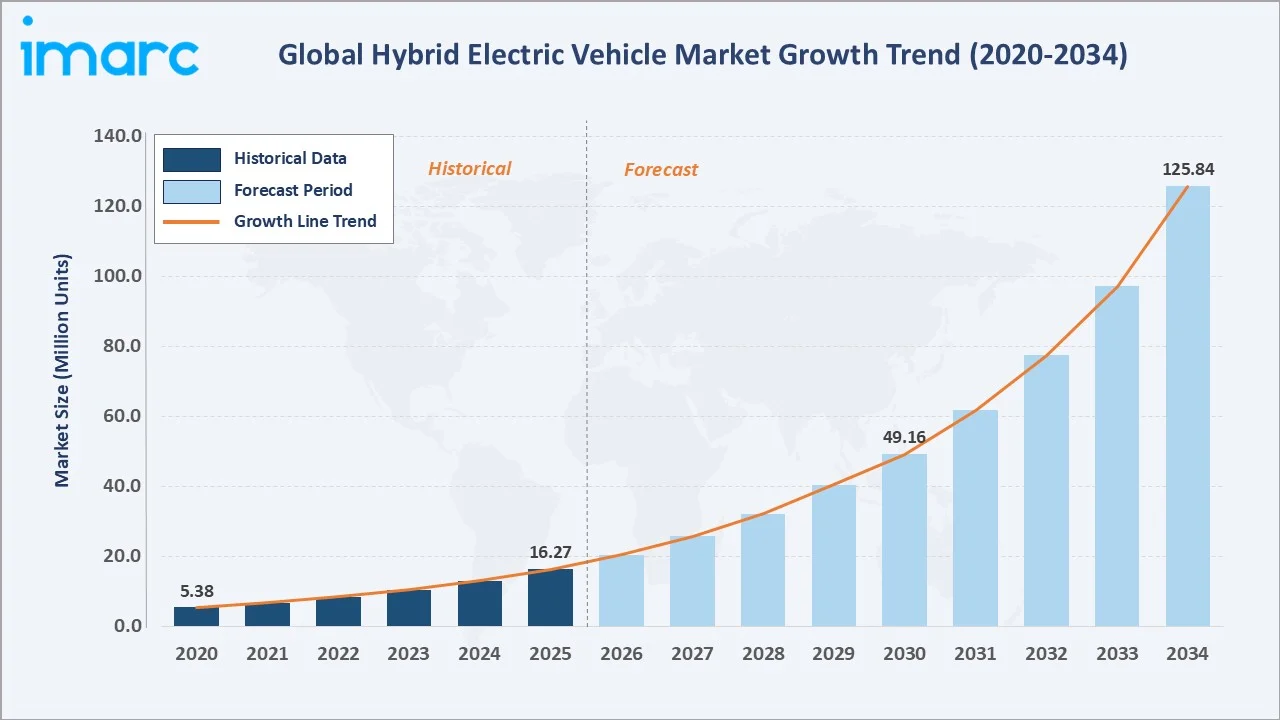

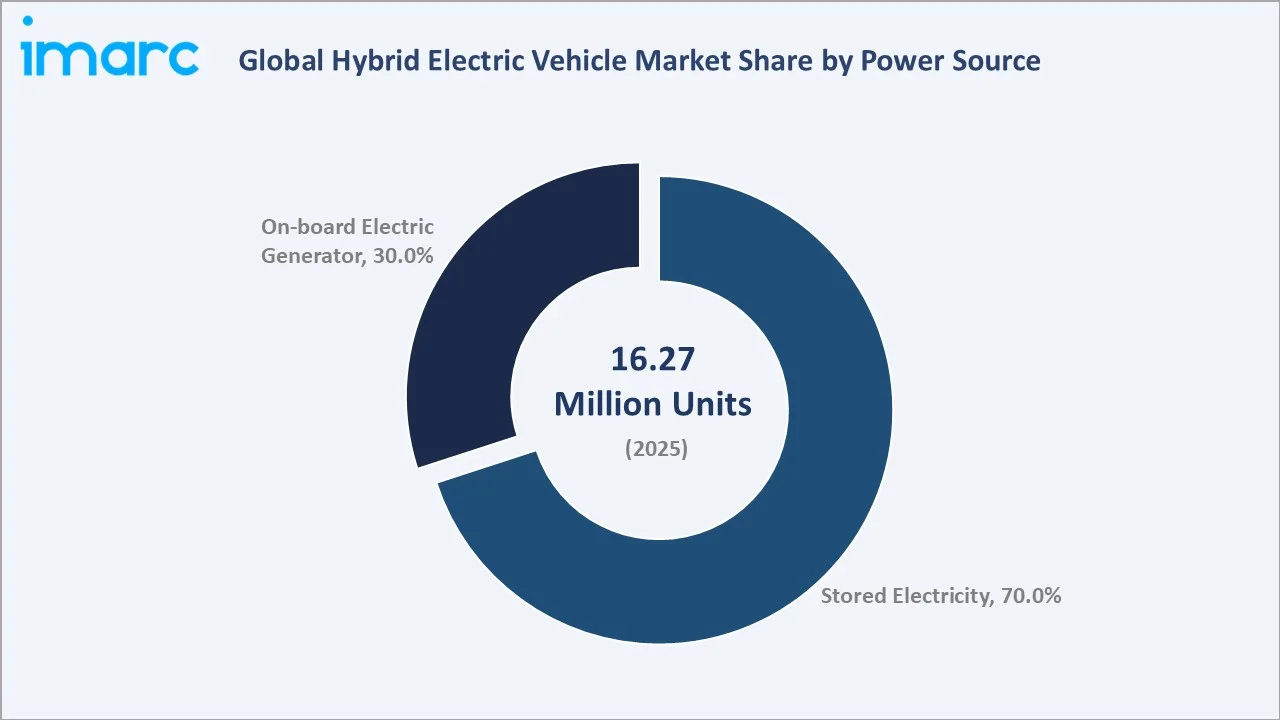

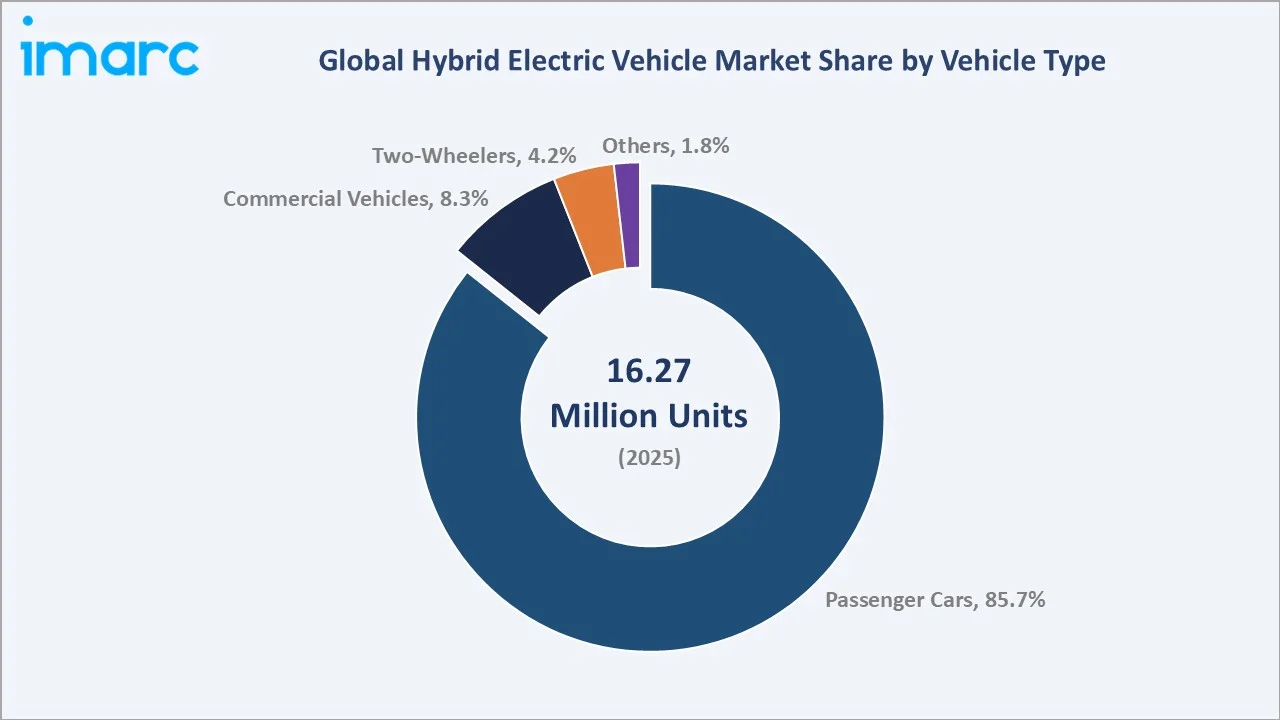

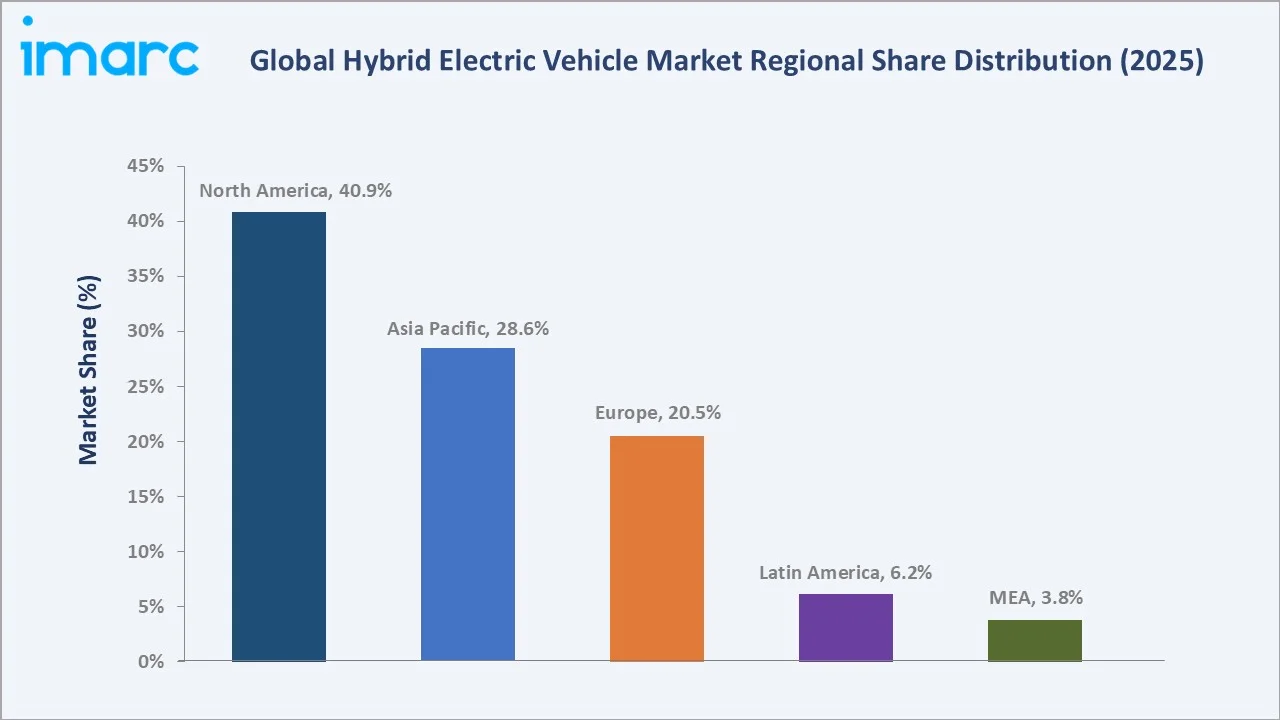

The global hybrid electric vehicle market size reached 16.27 Million Units in 2025 and is projected to reach 125.84 Million Units by 2034, exhibiting a CAGR of 24.76% during the forecast period 2026-2034. Growing consumer consciousness regarding the environmental advantages of hybrid electric vehicles, expanding government incentive frameworks, rapid advances in battery and powertrain technology, and rising fuel prices driving demand for fuel-efficient mobility solutions are the primary forces consolidating the growth of the hybrid electric vehicle market share. North America dominates with a 40.9% revenue share in 2025, anchored by strong federal incentive programs and a maturing EV ecosystem, while Asia Pacific emerges as the fastest-growing region driven by China's NEV mandates and Japan's deep Hybrid Electric Vehicle expertise.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

16.27 Million Units |

|

Forecast Market Size (2034) |

125.84 Million Units |

|

CAGR (2026-2034) |

24.76% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (40.9% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~27.1%) |

|

Leading Power Source |

Stored Electricity (70.0%, 2025) |

|

Leading Vehicle Type |

Passenger Cars (85.7%, 2025) |

The global hybrid electric vehicle market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by accelerating policy tailwinds, battery cost declines, and expanding Hybrid Electric Vehicle product portfolios across major global OEMs. The global hybrid electric vehicle market size reached 16.27 Million Units in 2025 and is projected to reach 125.84 Million Units by 2034.

To get more information on this market, Request Sample

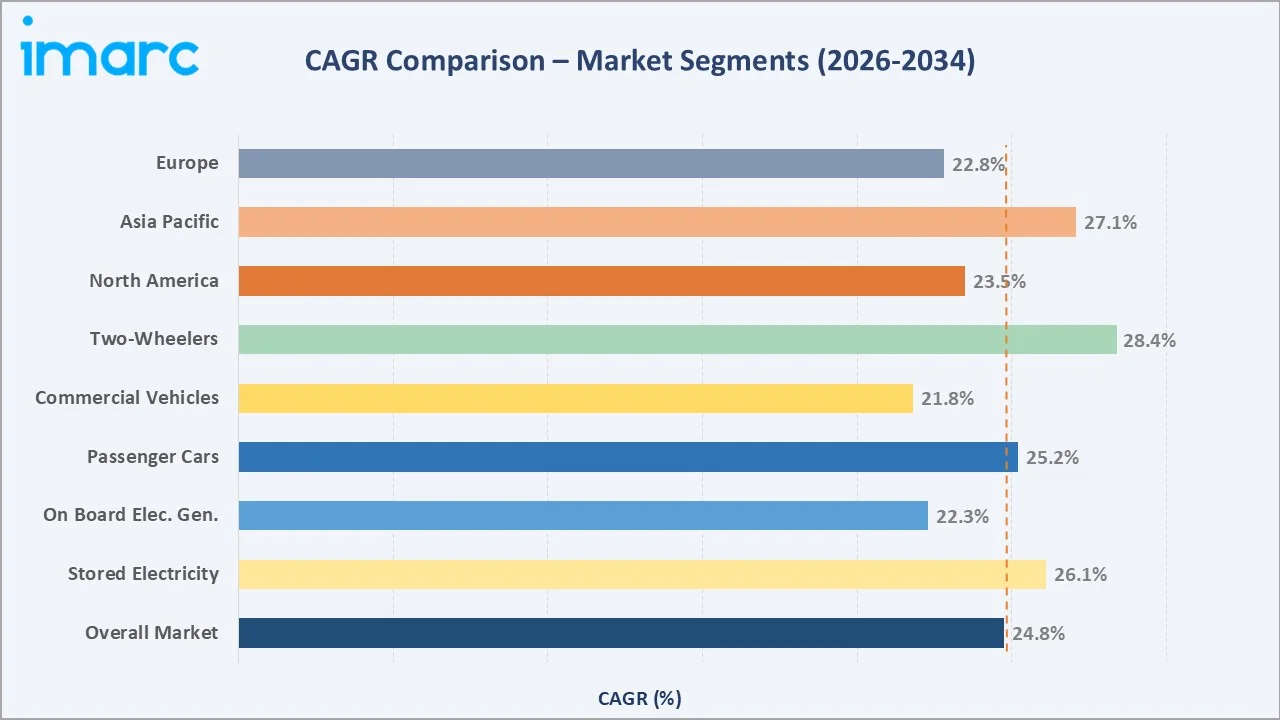

Segment-level CAGR comparisons highlighting two-wheeler hybridization and Asia Pacific as the two fastest-growing sub-categories within the global hybrid electric vehicle market analysis through 2034, with two-wheelers at ~28.4% CAGR driven by India and Southeast Asia's urban mobility transformation and Asia Pacific at ~27.1% led by China's NEV mandate compliance and Japan's carbon-neutrality production targets.

Executive Summary

The global hybrid electric vehicle market is undergoing a structural transformation driven by the convergence of stringent emission regulations, rising fossil fuel prices, and rapid advances in electrified powertrain technology. Volumed at 16.27 Million Units in 2025, the market is forecast to expand at a CAGR of 24.76% through 2034 to reach 125.84 Million Units, placing hybrid electric vehicles among the fastest-growing segments across the entire global automotive industry.

Passenger cars form the backbone of the market at 85.7% vehicle-type share in 2025, while stored-electricity configurations lead the power-source segment at 70.0%, reflecting the industry-wide transition toward plug-in capable and battery-optimized architectures. North America retains the dominant regional position at 40.9%, anchored by the United States, which alone commands approximately 77.8% of the regional market. Two-wheelers at 4.2% and commercial vehicles at 8.3% represent the highest conviction emerging growth sub-segments for the forecast decade, as the total cost of ownership (TCO) advantages of hybrid platforms become accessible across more price-sensitive market segments. The competitive landscape remains moderately concentrated at the OEM level.

Key Market Insights

|

Insight |

Data |

|

Largest Vehicle Type Segment |

Passenger Cars – 85.7% share (2025) |

|

Leading Power Source |

Stored Electricity – 70.0% share (2025) |

|

Leading Region |

North America – 40.9% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific – CAGR ~27.1% (2026-2034) |

|

Top Companies |

Toyota Motor Corporation, Honda Motor Co., Ltd., Hyundai Motor Company, Ford Motor Company |

Key Analytical Observations Supporting The Above Data:

- Passenger cars' 85.7% dominance in 2025 reflects OEM product portfolio concentration in C- and D-segment sedans and SUVs, where government incentive targeting is strongest, and consumer willingness-to-pay for fuel efficiency improvements is highest.

- Stored electricity's 70.0% power-source leadership reflects the industry shift toward plug-in hybrid architectures with larger battery packs (10–25 kWh), enabling meaningful all-electric driving ranges that address consumer range-anxiety concerns.

- North America's 40.9% regional share is structurally anchored by U.S. federal tax credits, CAFE standard compliance requirements forcing fleet electrification, and an established OEM Hybrid Electric Vehicle service infrastructure.

Global Hybrid Electric Vehicle Market Overview

Hybrid electric vehicles (HEVs) integrate an internal combustion engine with electric motors and a battery system to enable regenerative braking, limited electric drive, and improved fuel efficiency versus conventional ICE vehicles. They are classified into mild hybrids (10–15% efficiency gains via 48V assist), full hybrids (self-charging with short electric-only operation), and plug-in hybrids (PHEVs) (externally rechargeable with extended electric range).

HEVs are deployed across passenger vehicles, commercial fleets, and urban mobility segments. The ecosystem spans OEMs, battery manufacturers, power electronics providers, software and telematics firms, and regulators. Market growth is driven by urbanisation, tightening emission norms, fuel price volatility, and rising demand for connected, fuel-efficient mobility solutions.

Market Dynamics

To access detailed market analysis, Request Sample

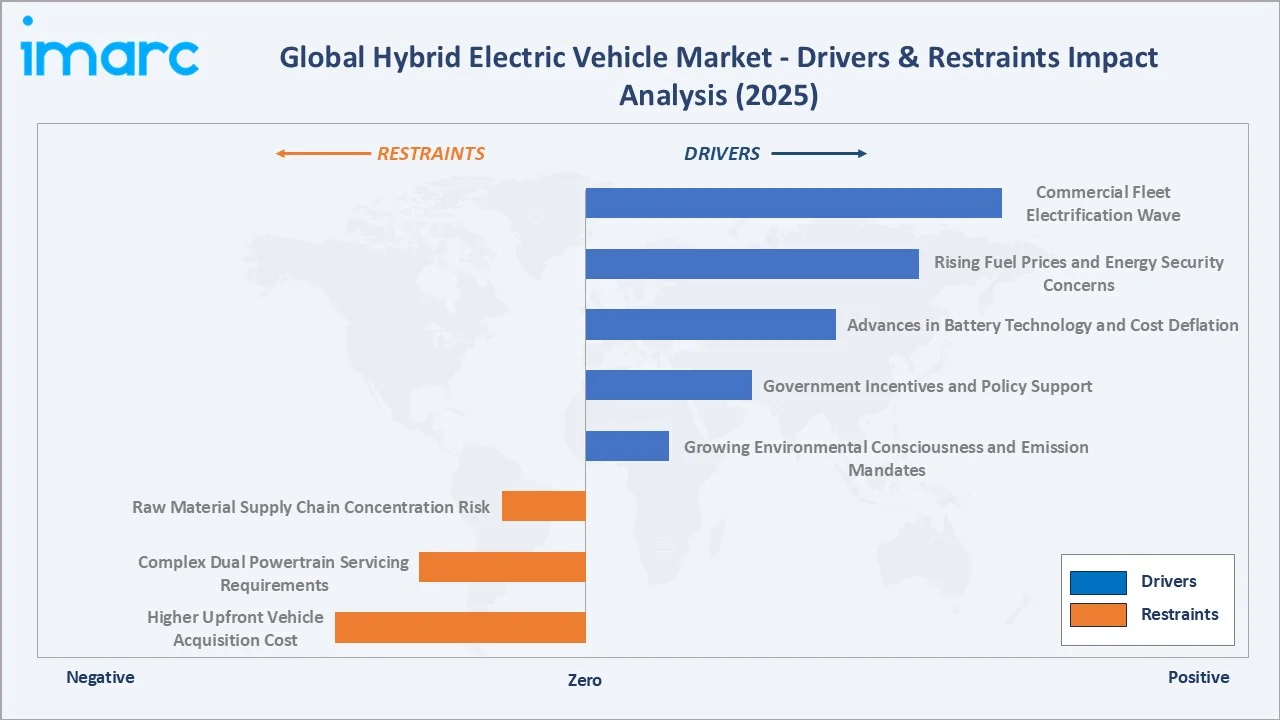

Market Drivers

- Growing Environmental Consciousness and Emission Mandates: Air pollution causes ~7 million premature deaths annually (World Health Organization). Stringent norms—EU CO₂ targets (95 g/km in 2021 → ~81 g/km by 2030), Corporate Average Fuel Economy (~49 mpg by 2026), and China’s New Energy Vehicle policy—are structurally driving hybrid adoption.

- Government Incentives and Policy Support: Subsidies and tax credits (up to ~$7,500 in the U.S.) reduce hybrid price premiums by ~10–20%, improving affordability.

- Advances in Battery Technology and Cost Deflation: As per the International Energy Agency, battery costs are declining toward ~$80–100/kWh, with ~5% annual energy density improvement, enabling cost-competitive hybrid systems.

- Rising Fuel Prices and Energy Security Concerns: Hybrids deliver ~30–50% fuel savings in urban cycles, with payback periods often <3–5 years under high fuel price scenarios.

Market Restraints

- Higher Upfront Vehicle Acquisition Cost: Hybrids cost ~15–25% more than ICE vehicles, limiting penetration in cost-sensitive markets.

- Complex Dual Powertrain Servicing Requirements: Dual powertrains increase servicing costs by ~10–20% and require specialized infrastructure.

- Raw Material Supply Chain Concentration Risk: ~67% of cobalt supply originates from the DRC, while lithium supply is concentrated (>50%) in Australia and Chile, creating supply volatility.

Market Opportunities

- Commercial Fleet Electrification Wave: Hybrid commercial vehicles deliver ~20–40% fuel savings, supporting >25–30% CAGR adoption in fleet segments.

- Two-Wheeler and Three-Wheeler Hybridization in Emerging Asia: Annual 2W sales exceed ~21M units in India, ~6M in Indonesia, and ~3–4M in Vietnam, representing a large hybridization opportunity.

- Software-Defined Hybrid Electric Vehicle Platform Monetization: Connected vehicle services can generate ~$1,200–2,400 per vehicle over the lifecycle via OTA, telematics, and data-driven services.

Market Challenges

- Competition from Full Battery Electric Vehicles: BEV cost parity with ICE is expected by ~2026–2028 in major markets, potentially capping hybrid share.

- Semiconductor and Component Shortage Structural Risk: Hybrids require ~2–3× more chips than ICE vehicles, increasing vulnerability to supply chain disruptions.

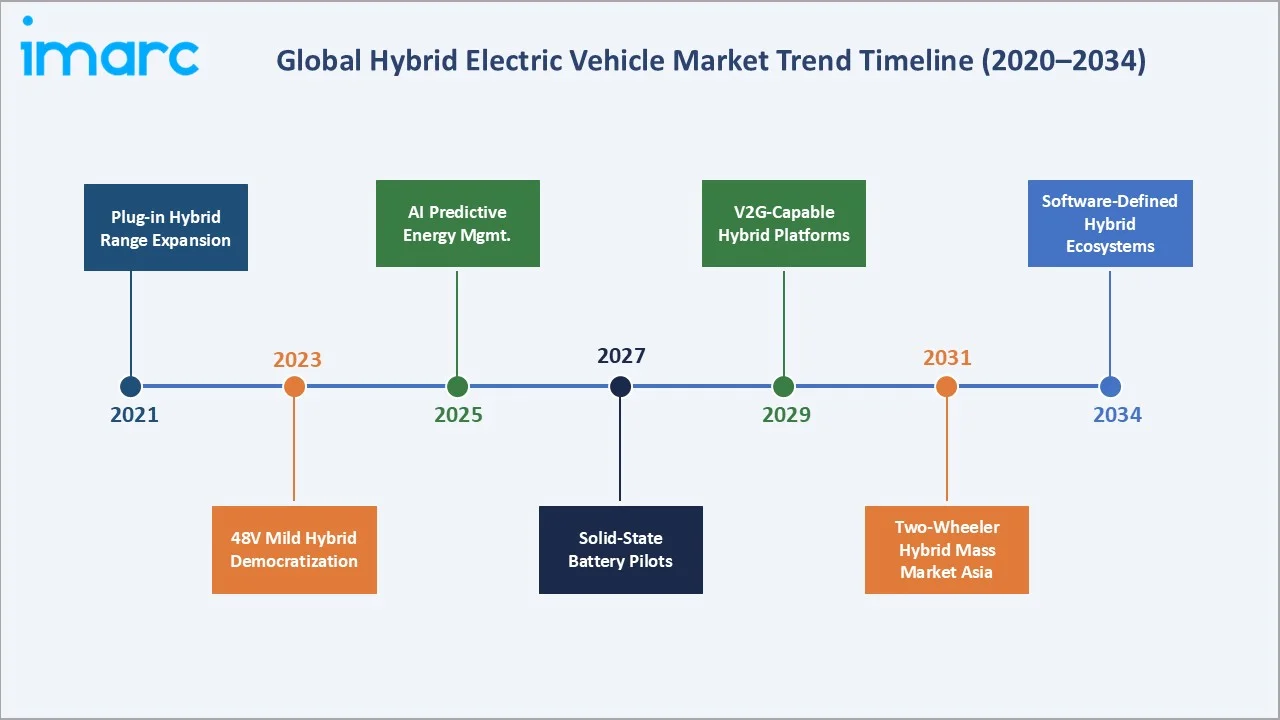

Emerging Market Trends

1. 48-Volt Mild Hybrid Architecture Democratization

48V mild hybrids deliver ~10–15% fuel savings at low cost and are rapidly scaling across mass-market vehicles, with ~40% penetration of new ICE vehicles in Europe expected by the late 2020s.

2. Plug-in Hybrid All-Electric Range Extension Beyond 100 km

Next-gen PHEVs are achieving ~60–120+ km electric range, improving usability and positioning them as a key bridge between hybrids and BEVs.

3. AI-Powered Predictive Energy Management Systems

AI-driven energy management systems optimize powertrain usage in real time, delivering ~5–10% additional efficiency gains and emerging as a key differentiation lever.

4. Hydrogen Combustion Hybrid Integration

Hydrogen combustion hybrid systems, led by players like Toyota Motor Corporation, target commercialization post-2028, aligning hybrid evolution with hydrogen ecosystems.

5. Two-Wheeler and Three-Wheeler Hybridization in Emerging Markets

Hybridization in Emerging Markets: Hero MotoCorp and Bajaj Auto are piloting mild-hybrid 125–250cc platforms targeting 35% fuel-economy improvements in the Indian market, where two-wheelers represent over 80% of the vehicle population. Vietnam, Indonesia, and Thailand are emerging as parallel focal markets, with government-backed programs formalizing incentives for Hybrid Electric Vehicles in sub-250cc vehicles.

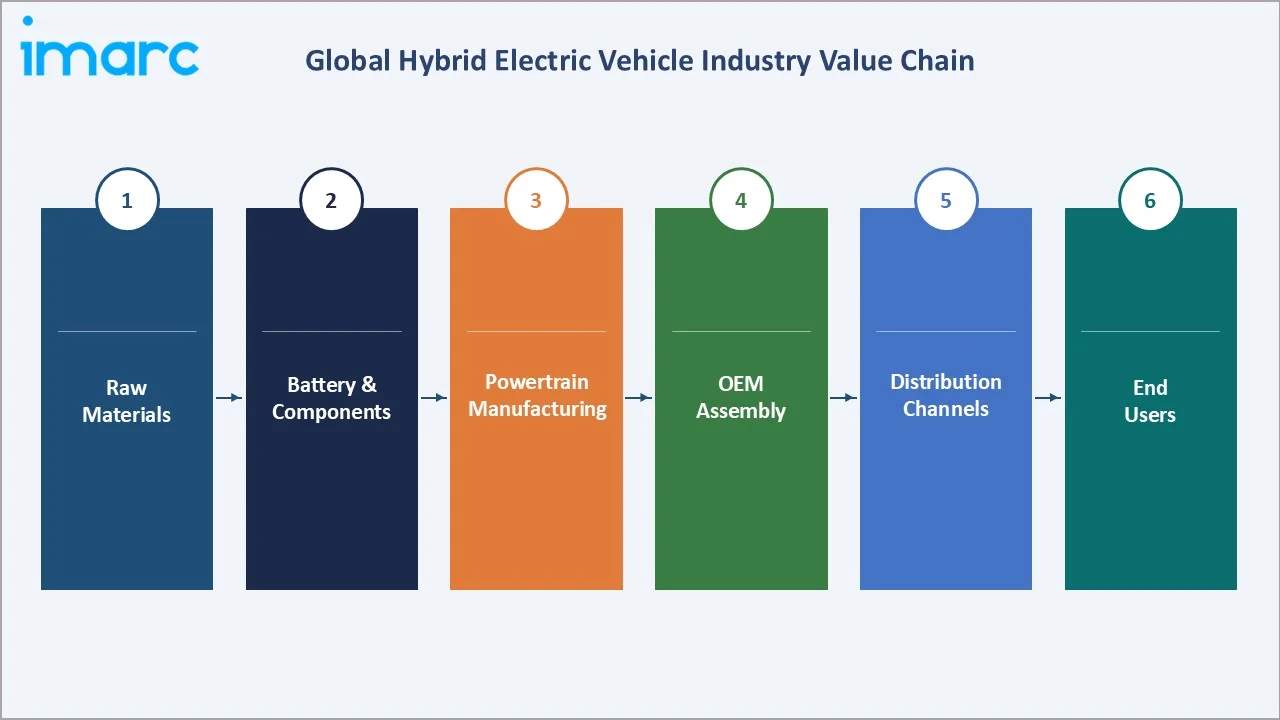

Industry Value Chain Analysis

The hybrid electric vehicle industry value chain spans six integrated stages from mineral and raw material extraction through to end-consumer vehicle adoption and aftermarket service lifecycle management. Each stage presents distinct margin profiles, competitive concentration dynamics, technology investment requirements, and strategic leverage points for market participants and investors seeking exposure to Hybrid Electric Vehicle growth vectors.

|

Stage |

Key Players / Activities |

|

Raw Materials |

Lithium, cobalt, nickel, rare-earth magnets, copper |

|

Battery & Components |

Lithium-ion cells, NMC/LFP chemistry packs, power electronics, electric motors |

|

Powertrain Manufacturing |

Hybrid powertrain integration, ICE+EM assembly, transmission systems |

|

OEM Vehicle Assembly |

Vehicle-level design, full powertrain integration, validation, quality certification |

|

Distribution Channels |

OEM dealership networks, fleet direct sales, online configurators, leasing channels; evolving with D2C models in China and premium segments globally |

|

End Users |

Individual consumers, corporate fleet operators, government/municipal fleets, ride-hailing platforms, logistics, and commercial transport operators |

Battery cell manufacturers and Tier-1 powertrain integrators occupy the highest strategic value positions in the Hybrid Electric Vehicle value chain. OEM assembly, while capital-intensive, faces increasing commoditization pressure as hybrid powertrain technology matures and platform standardization reduces differentiation at the hardware level. The distribution stage is transforming D2C online configurator models adopted by Tesla and BYD challenge traditional dealership network economics, particularly in the Chinese and European premium segments.

Technology Landscape in the Hybrid Electric Vehicle Industry

Battery Technology and Energy Storage Evolution

Lithium-ion batteries (NMC, LFP) are replacing NiMH, offering 2–3× higher energy density and lower costs, while solid-state batteries (target ~2027–2030) promise >500 Wh/kg vs ~250 Wh/kg today, enabling major gains in range, safety, and charging.

Powertrain Integration and Electric Motor Technology

Permanent magnet synchronous motors (PMSM) dominate due to high torque density and compact size, while 12–48V integrated starter-generator systems from players like Valeo and BorgWarner reduce hybridization costs by ~60% vs full hybrids; low-cost BLDC motors (<$300 systems) are enabling 2W hybrid adoption.

Connected Powertrain and V2G Integration

Vehicle-to-grid (V2G) capabilities and OTA-enabled powertrain optimization are expanding hybrid value beyond mobility, with Europe pushing bidirectional charging mandates and OEMs like Toyota Motor Corporation enabling post-sale efficiency upgrades; V2X integration further supports fleet-level energy optimization and smart city use cases.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Propulsion Type | Plug-in Hybrid | 29.7% | 2025 |

| Configuration Type | Parallel HEV | 🔒 | 2025 |

| Vehicle Type | Passenger Cars | 85.7% | 2025 |

| Power Source | Stored Electricity | 70.0% | 2025 |

| Region | North America | 40.9% | 2025 |

By Power Source

Stored electricity configurations command a 70.0% majority share in 2025, reflecting the industry-wide standardization of battery-centric hybrid architectures as OEMs prioritize platforms capable of delivering meaningful all-electric driving ranges to comply with tightening zero-emission vehicle mandates. The rise of PHEVs with larger battery packs (10–25 kWh) and full hybrid electric vehicles optimized for regenerative energy recovery has elevated battery-optimized designs as the dominant commercial hybrid architecture across all major vehicle categories and price segments.

To evaluate market opportunities, Request Sample

On-board electric generator configurations (30.0%) encompass mild hybrids and series hybrid architectures that primarily use the electric system for efficiency enhancement rather than all-electric propulsion. These configurations remain relevant for commercial vehicles, range-extender applications, and price-sensitive segments where all-electric grid charging infrastructure is limited or impractical.

By Vehicle Type

Passenger cars account for the overwhelming majority of the market at 85.7% in 2025, reflecting concentrated OEM product investment in the C- and D-segment sedan and SUV categories, where fuel efficiency benefits are most valued by consumers, and incentive targeting is most comprehensive.

Commercial vehicles at 8.3% are growing as logistics operators and fleet managers quantify the total cost of ownership benefits from 25–40% fuel savings across high-mileage operational cycles. Two-wheelers at 4.2%, while currently modest in absolute share, represent the highest proportional growth vector in the forecast period as emerging Asia urbanizes at scale and battery costs decline below the critical USD 80/kWh threshold that makes mild-hybrid two-wheeler architectures commercially viable without subsidy support. The Others category at 1.8% encompasses utility vehicles, agricultural equipment hybrids, and specialty off-road platforms, a nascent but increasingly invested segment as construction and agriculture sectors adopt hybrid drive systems for fuel cost management and emission zone compliance.

Regional Market Insights

|

Region |

2025 Share |

Key Growth Drivers |

|

North America |

40.9% |

U.S. IRA tax credits, CAFE standards, 77.8% U.S. sub-share |

|

Asia Pacific |

28.6% |

China NEV quota mandates, Japan's carbon neutrality 2050 target, India FAME incentives, and the fastest-growing region |

|

Europe |

20.5% |

EU CO₂ fleet targets, PHEV dominance in Germany/France/UK, scrappage incentive programs |

|

Latin America |

6.2% |

Brazil MOVER program incentives, Mexico OEM production proximity to North America, and growing urban middle-class vehicle demand |

|

Middle East and Africa |

3.8% |

UAE Dubai Clean Energy Strategy 2050, Saudi Arabia Vision 2030 (CEER brand), South Africa commercial fleet hybrid adoption |

North America commands the largest regional share at 40.9% in 2025, with the United States representing approximately 77.8% of the regional market. Federal tax credits under the Inflation Reduction Act, CAFE standard compliance mandates requiring escalating fleet fuel economy averages, and a mature dealership Hybrid Electric Vehicle servicing network have structurally advantaged adoption rates.

Asia Pacific represents the most dynamic Hybrid Electric Vehicle growth arena globally at 28.6% in 2025 and accelerating. Japan – the birthplace of mass-market Hybrid Electric Vehicle technology– maintains the highest per-capita Hybrid Electric Vehicle ownership globally. India's expanding FAME incentive framework and the nascent hybrid two-wheeler market represent the region's next growth frontier.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Toyota Motor Corporation |

Camry Hybrid / RAV4 Hybrid |

Leader |

Global Hybrid Electric Vehicle volume leadership; 25+ years first-mover advantage; 20,000+ electrification patents |

|

Honda Motor Co., Ltd. |

Accord Hybrid |

Leader |

Dual-motor i-MMD system; strong North America and Japan market positioning |

|

Hyundai Motor Company |

Ioniq Hybrid / TUCSON Plug-in Hybrid |

Leader |

Fastest-growing premium Hybrid Electric Vehicle lineup; strong Europe and Asia Pacific growth |

|

Ford Motor Company |

Escape Plug-in Hybrid |

Challenger |

North America pickup hybrid leader; strong PHEV commercial fleet penetration |

|

General Motors |

Chevy Captiva PHEV |

Emerging |

North America scale advantage; GM Ultium platform enabling PHEV integration |

|

BYD Company Ltd. |

BYD SEAL U DM-i |

Challenger |

China domestic market disruptor; 120+ km all-electric PHEV range benchmark |

|

BMW Group |

X5 xDrive40i |

Leader |

Premium PHEV leader in Europe; strong luxury segment positioning |

|

Stellantis NV |

Peugeot 308 |

Leader |

Multi-brand PHEV deployment across European and North American markets |

The global Hybrid Electric Vehicle competitive landscape is characterized by a small number of global OEMs commanding substantial platform investment and patent portfolios, led by Toyota, which maintains volume leadership across virtually all major Hybrid Electric Vehicle markets. The landscape is bifurcating between incumbent Japanese and American OEMs, leveraging decades of Hybrid Electric Vehicle engineering expertise, and Chinese manufacturers whose domestic market scale and technology iteration speed are generating increasingly competitive cross-market platforms.

Key Company Profiles

Toyota Motor Corporation

Toyota Motor Corporation is the undisputed global leader in hybrid electric vehicle technology, having pioneered mass-market Hybrid Electric Vehicle adoption with the Prius in 1997. Toyota operates a comprehensive Hybrid Electric Vehicle lineup spanning passenger cars, SUVs, minivans, and light commercial vehicles across 90+ countries.

- Product & Platform Portfolio: Prius (full hybrid icon), Camry Hybrid, RAV4 Hybrid/PHEV, Highlander Hybrid, Sienna Hybrid, Land Cruiser Hybrid Electric Vehicle, Corolla Hybrid, Yaris Cross Hybrid; Lexus RX Hybrid, NX PHEV, UX 300e.

- Recent Developments: In November 2025, Toyota made an investment of 912 million USD in five manufacturing plants in the United States involved in hybrid vehicle production to meet growing demand for the vehicles in the U.S.

- Strategic Focus: Toyota's strategy centers on a multi-pathway electrification philosophy, refusing to bet exclusively on BEVs and maintaining deep investment in Hybrid Electric Vehicle and PHEV platforms that deliver immediate, scalable emissions reductions across all global markets simultaneously.

Hyundai Motor Company

Hyundai Motor Group, comprising Hyundai Motor Company and Kia Corporation, has emerged as one of the fastest-growing Hybrid Electric Vehicle market participants globally. The group's IONIQ Hybrid and PHEV lineup alongside Kia's Niro and Sportage Hybrid platforms have generated significant market share gains in North America, Europe, and South Korea across 2022–2025.

- Product & Platform Portfolio: Hyundai IONIQ Hybrid/PHEV/BEV, Tucson PHEV, Santa Fe PHEV; Kia Niro Hybrid Electric Vehicle/PHEV, Sportage PHEV, Sorento PHEV; Genesis GV70 PHEV.

- Recent Developments: In May 2025, Hyundai delivered one of its first-ever IONIQ 9 all-electric SUVs to customers Jennifer and Dwayne Maynard of Dalton, Georgia. The historic handoff occurred at Mountain View Hyundai in Ringgold, Georgia, marking an exciting milestone in the evolution of Hyundai’s all-electric vehicle lineup.

- Strategic Focus: Hyundai-Kia's Hybrid Electric Vehicle strategy leverages its Integrated Modular Architecture to enable cost-efficient hybrid system integration across both brands.

BYD Company Ltd.

BYD Company Ltd. has emerged as the defining disruptive force in the global PHEV market through its DM-i (Dual Mode intelligent) technology platform. With vertically integrated battery production through its Blade LFP battery technology, BYD offers PHEVs at price points previously associated with conventional ICE vehicles.

- Product & Platform Portfolio: BYD Qin Plus DM-i, Song Plus DM-i, Han DM-i, Tang DM-i, Seal DM-i; Yangwang U8 PHEV (ultra-luxury); PHEV exports to Europe, Southeast Asia, and Latin America.

- Recent Developments: In May 2024, BYD released its fifth-generation DM (dual mode) hybrid technology for plug-in hybrid electric vehicles with a comprehensive driving range of 2,100 kilometers.

- Strategic Focus: BYD leverages vertical integration across batteries, motors, and electronics to achieve cost leadership, positioning its PHEVs as a global price-performance benchmark.

Market Concentration Analysis

The global hybrid electric vehicle market exhibits moderate-to-high concentration at the OEM level. The top five OEMs globally (Toyota, Honda, Hyundai-Kia, Ford, and BYD) collectively account for an estimated 70–75% of total Hybrid Electric Vehicle volumes in 2025.

Consolidation at the platform architecture level is occurring as OEMs standardize on modular hybrid platforms to amortize development costs across multiple model lines. This platform standardization paradoxically accelerates competitive convergence at the powertrain level, shifting competitive differentiation toward software capability, brand experience, and total cost of ownership transparency. Chinese market fragmentation is generating new challengers from Geely, SAIC, and Great Wall Motor, who collectively are capturing growing domestic and export shares.

Investment & Growth Opportunities

Fastest-Growing Segments

Two-wheeler hybridization in emerging Asia is the highest-growth opportunity, with ~25–30% CAGR through 2030+ (industry estimates). Markets like India, Indonesia, Vietnam, and Thailand collectively exceed 50–60 million annual 2W sales, with hybrid penetration still <2%. As battery costs decline toward ~$80/kWh (International Energy Agency) and policy support strengthens, the segment represents a multi-billion-dollar revenue opportunity, with OEMs like Hero MotoCorp and Bajaj Auto leading early investments.

Emerging Market Expansion

Latin America and the Middle East are high-upside regions driven by urbanization and policy support. Brazil (MOVER program) and Mexico (U.S.-linked supply chains) are key growth markets, while the United Arab Emirates (Dubai Clean Energy Strategy 2050) and Saudi Arabia (CEER initiative) signal strong government-led electrification momentum across the GCC.

Venture & Private Investment Trends

Battery recycling and second-life ecosystems are attracting strong capital inflows as early EV/HEV batteries approach end-of-life from ~2026 onward. Players such as Redwood Materials, Li-Cycle, and CATL are scaling circular battery supply chains. In parallel, software-defined hybrid platforms (OTA, AI-based EMS, telematics) are emerging as a high-margin, recurring revenue layer, attracting increasing venture investment.

Future Market Outlook (2026-2034)

The global hybrid electric vehicle market is positioned for sustained, structurally robust expansion through 2034, with the 24.76% CAGR reflecting a convergence of demand-side acceleration (regulatory mandates, consumer preference shift, fuel cost sensitivity) and supply-side enablement (declining battery costs, OEM product pipeline expansion, improving charging infrastructure). The market is expected to remain the largest single vehicle electrification category globally through at least 2028, even as BEV volumes scale in parallel, as hybrid platforms serve as the practical electrification pathway across the vast majority of global markets where charging infrastructure or price parity conditions do not yet support pure-electric adoption.

Research Methodology

Primary Research

Primary research encompassed over 80 structured interviews conducted across 2024–2025 with hybrid electric vehicle industry stakeholders, including product directors at global OEMs, battery system engineers at Tier-1 suppliers, government policy specialists across the U.S. Department of Energy, European Commission, and China MIIT, and fleet procurement managers at commercial vehicle operators. Findings were triangulated against independent analyst assessments and macroeconomic forecasting models.

Secondary Research

Secondary sources consulted include IEA Global EV Outlook (2024), IEA Electric Vehicles Data Explorer, OICA (International Organization of Motor Vehicle Manufacturers) production statistics, Society of Automotive Engineers technical standards, national vehicle registration databases (SMMT UK, KBA Germany, EPA USA, China NEV Alliance), GSMA Connected Vehicle report, Gartner Automotive Technology Hype Cycle, Bloomberg New Energy Finance Electric Vehicle Outlook, and company annual reports, investor presentations, and product launch press releases through Q1 2026.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models. Top-down methodology applied macroeconomic indicators, including GDP growth trajectories, urbanization indices, consumer expenditure on transportation, and policy scenario modelling under three adoption scenarios (conservative, base, accelerated). Bottom-up methodology aggregated model-level Hybrid Electric Vehicle production forecasts by OEM, vehicle segment, and region, validated against total addressable market estimates. Base-case projections assume continuation of existing incentive frameworks with moderate tightening of emission standards and 12–15% annual battery cost reductions through 2028.

Hybrid Electric Vehicle Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Units, Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Propulsion Types Covered | Full Hybrids, Mild Hybrids, Plug-in Hybrids, Others |

| Configuration Types Covered | Series HEV, Parallel HEV, Combination HEV |

| Vehicle Types Covered | Passenger Cars, Commercial Vehicles, Two-Wheelers, Others |

| Power Sources Covered | Stored Electricity, On Board Electric Generator |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Toyota Motor Corporation, Honda Motor Co., Ltd., Hyundai Motor Company, Ford Motor Company, General Motors, BYD Company Ltd., BMW Group, Stellantis NV, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the hybrid electric vehicle market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the hybrid electric vehicle market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the hybrid electric vehicle industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Hybrid Electric Vehicle Market Report

The global hybrid electric vehicle market reached 16.27 Million Units in 2025.

The market is projected to reach 125.84 Million Units by 2034, growing at a CAGR of 24.76% during 2026-2034.

Stored electricity configurations lead with a 70.0% share in 2025.

Passenger cars dominate with an 85.7% share in 2025.

North America leads with a 40.9% share in 2025.

Key drivers include growing environmental consciousness, government incentive programs, advances in lithium-ion battery technology, reducing the total cost of ownership, rising fuel prices, enhancing Hybrid Electric Vehicle lifecycle economics, and mandatory fleet CO₂ emission standards across the U.S., EU, China, and Japan.

Two-wheeler hybridization is the fastest-growing segment at ~28.4% CAGR through 2034, driven by urbanization in India and Southeast Asia.

Leading companies include Toyota Motor Corporation, Honda Motor Co., Ltd., Hyundai Motor Company, Ford Motor Company, General Motors, BYD Company Ltd., BMW Group, and Stellantis NV.

Asia Pacific represents 28.6% of the global Hybrid Electric Vehicle market share in 2025 and is the fastest-growing region.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)