Hyperloop Technology Market Size, Share, Trends and Forecast by Component Type, Speed, Carriage Type, and Region 2026-2034

Hyperloop Technology Market Size, Share, Trends & Forecast (2026-2034)

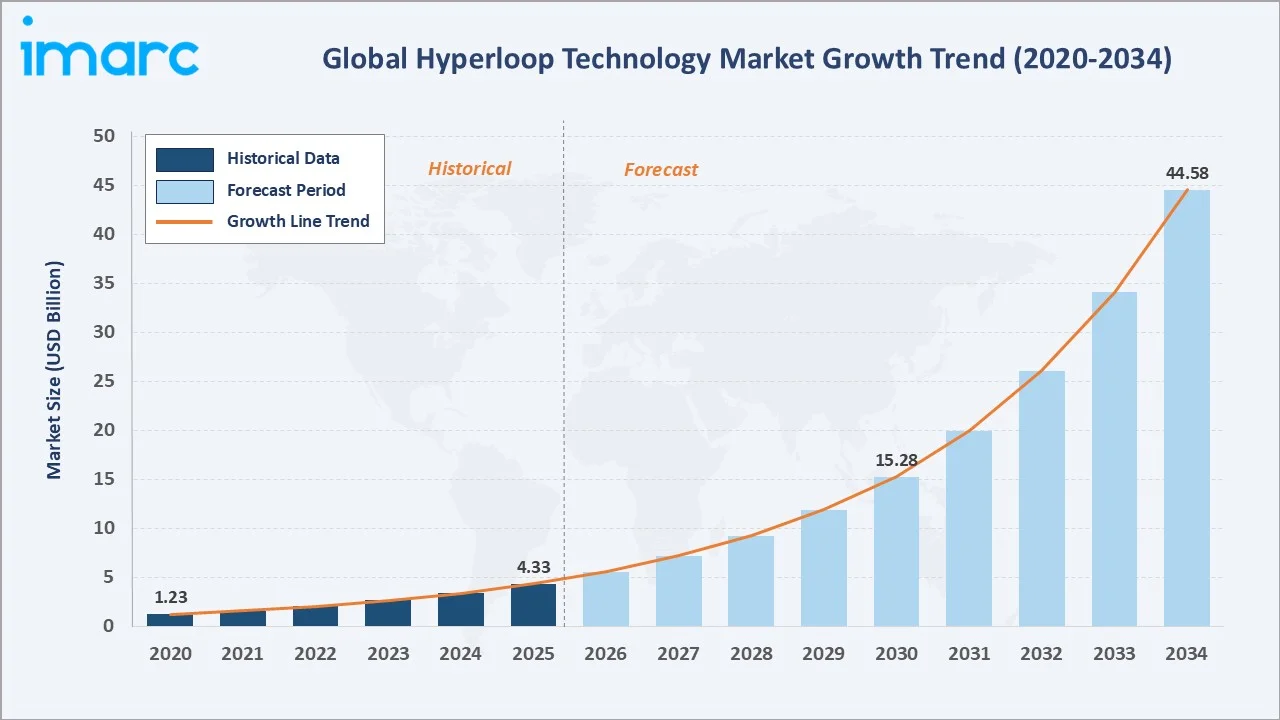

The global hyperloop technology market size reached USD 4.33 Billion in 2025 and is projected to reach USD 44.58 Billion by 2034, exhibiting a CAGR of 28.69% during 2026-2034. Strong government investment, climate-driven transit policy, and technological advances in magnetic levitation and propulsion are the primary growth forces shaping this market.

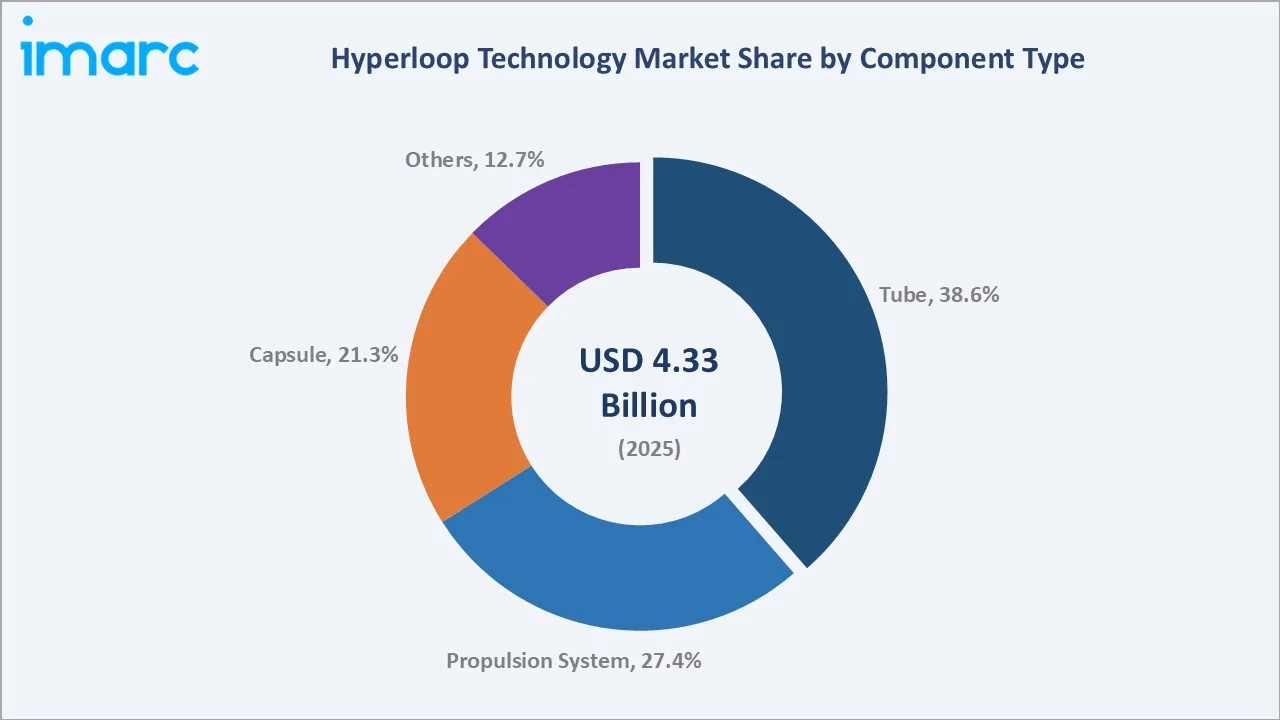

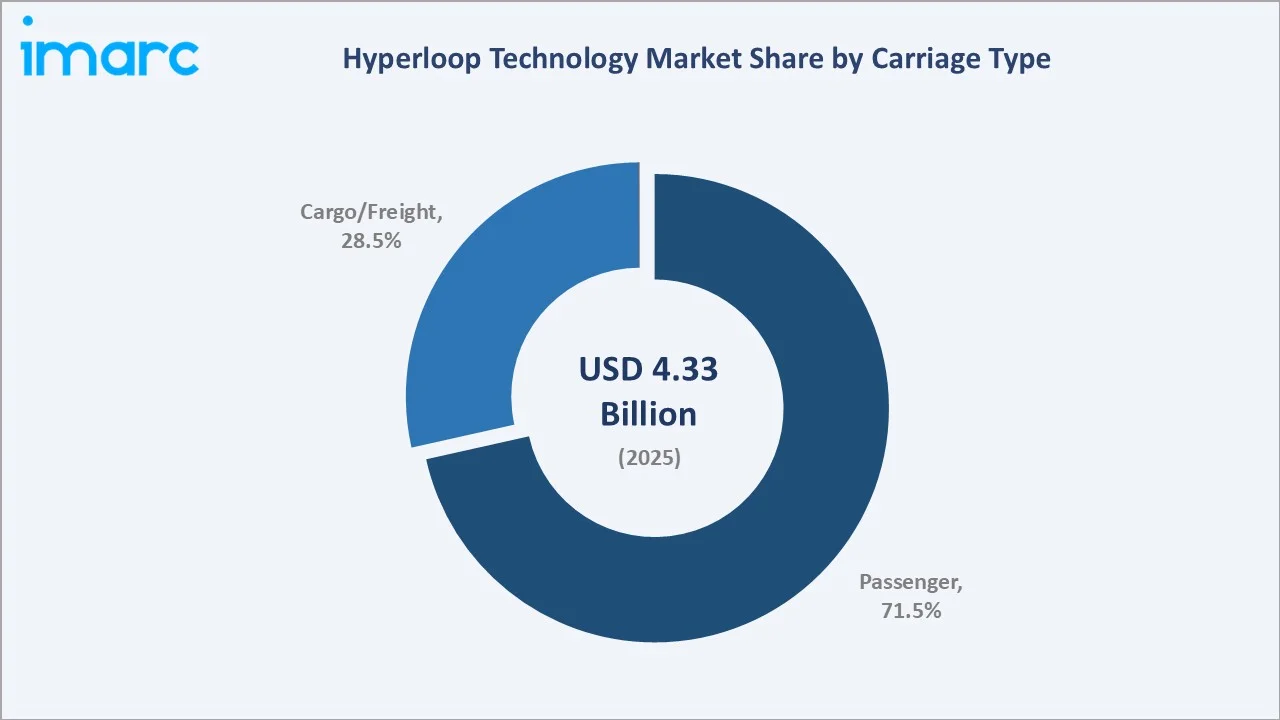

Tube leads component type segmentation at 38.6% in 2025, driven by large-scale infrastructure contracts globally. Passenger commands 71.5% carriage type share.

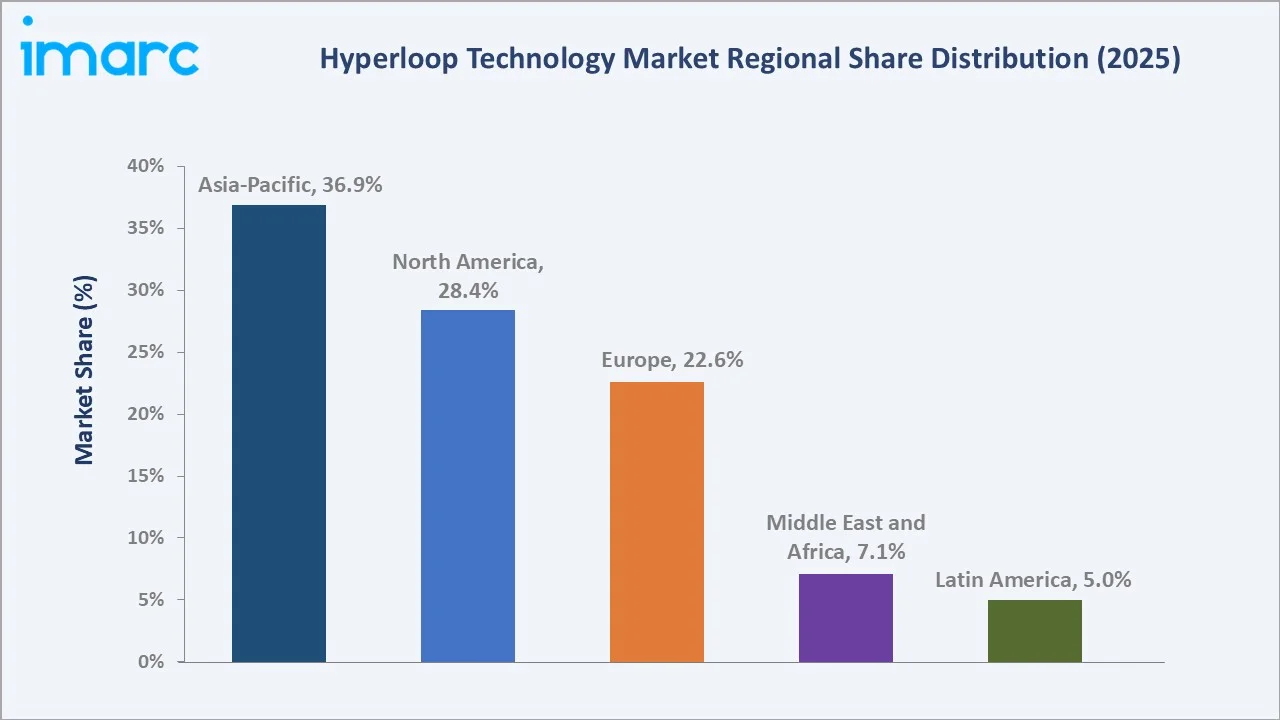

Asia-Pacific dominates the regional landscape with a 36.9% share underpinned by strong government-led transit infrastructure investment across China, India, and Southeast Asia.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.33 Billion |

|

Forecast Market Size (2034) |

USD 44.58 Billion |

|

CAGR (2026-2034) |

28.69% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Component Type |

Tube (38.6% share, 2025) |

|

Leading Carriage Type |

Passenger (71.5% share, 2025) |

|

Leading Region |

Asia-Pacific (36.9% share, 2025) |

The hyperloop technology market growth from 2020 through 2034 reflects sustained demand driven by public and private investment in next-generation transport infrastructure. The forecast to USD 44.58 Billion by 2034 captures accelerating project pipelines, regulatory milestones, and the transition from pilot programmes to commercial deployments across major global economies.

To get more information on this market, Request Sample

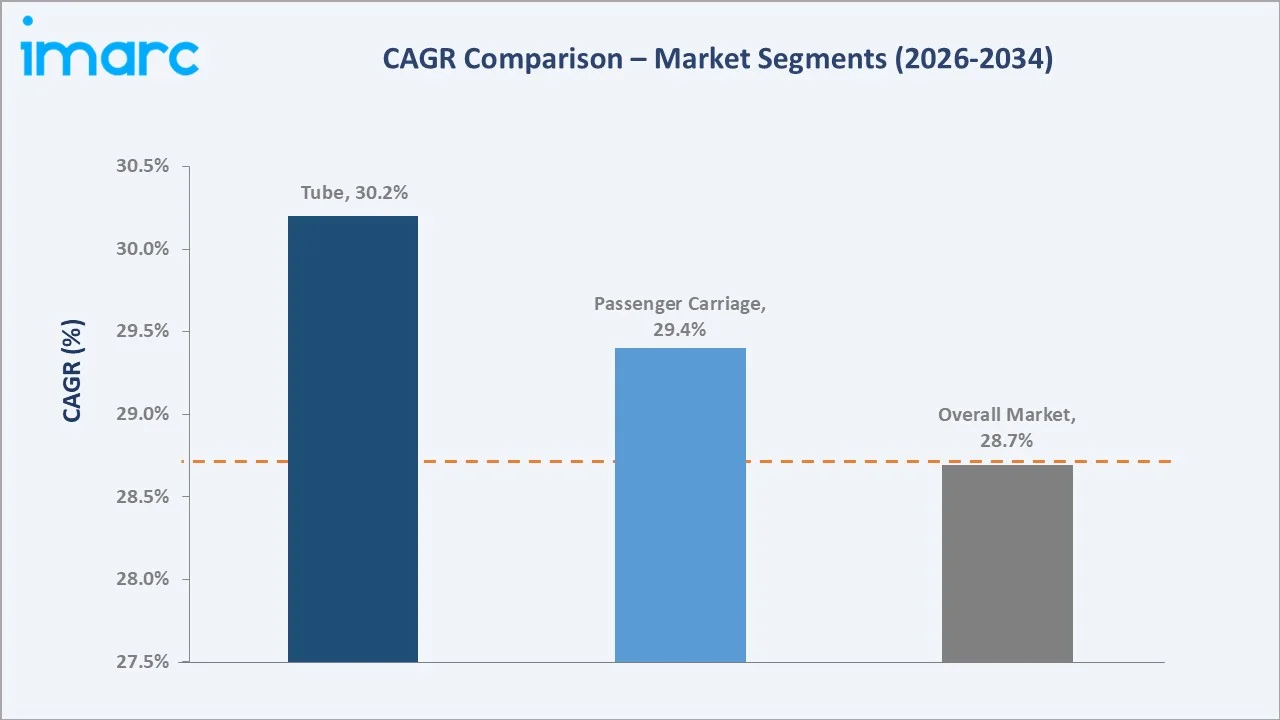

The CAGR trajectories across key component and carriage sub-segments highlight the Tube segment at approximately 30.2% CAGR and Passenger carriage at approximately 29.4% CAGR as the fastest-growing categories within the hyperloop technology market through 2034.

Executive Summary

The hyperloop technology market is on a sustained growth trajectory from USD 4.33 Billion in 2025 to USD 44.58 Billion by 2034. The market encompasses tube infrastructure, propulsion systems, capsule design, and ancillary components deployed across passenger and freight transport applications worldwide.

Tube leads at 38.6% in 2025, owing to its critical role as the primary structural and pressure-containment component in all hyperloop system architectures. Extensive capital allocation toward tube fabrication and installation underpins this dominance across projects in development globally.

Propulsion System (27.4%) supports the electromagnetic and linear motor technologies enabling high-speed transit. Capsule (21.3%) captures demand from vehicle design, passenger comfort fitout, and cargo container engineering across multiple concurrent hyperloop development programmes.

Passenger carriage commands 71.5% share in 2025, driven by the high commercial value of ultra-fast intercity and inter-regional passenger transit. Cargo/Freight (28.5%) captures growing interest in high-value express logistics and time-sensitive supply chain applications globally.

Asia-Pacific dominates at 36.9% in 2025, supported by government-backed transport R&D and infrastructure initiatives across Asia-Pacific.

North America follows at 28.4%, with Europe at 22.6%, driven by sophisticated transport research and climate-focused transit investment.

Key Market Insights

|

Insight |

Data |

|

Largest Component Type |

Tube – 38.6% share (2025) |

|

Second Largest Component |

Propulsion System – 27.4% share (2025) |

|

Leading Carriage Type |

Passenger – 71.5% share (2025) |

|

Leading Region |

Asia-Pacific – 36.9% share (2025) |

|

Top Companies |

AECOM, Hyperloop Transportation Technologies, TransPod |

- Tube at 38.6%: Tube dominates because large-scale infrastructure deployment requires continuous, airtight, low-pressure tube networks as the foundational component. Every hyperloop route requires substantial tube investment, sustaining its majority share across all active and planned projects globally.

- Passenger at 71.5%: Passenger carriage commands majority share because intercity high-speed travel represents the highest commercial return use case. Strong public interest, government support, and fare revenue potential make passenger hyperloop the primary commercial target globally.

- Asia-Pacific at 36.9%: Asia-Pacific's regional dominance reflects unrivalled government-led infrastructure ambition, significant R&D investment, and large population corridors ideally suited to hyperloop's speed advantages. China and India are leading project development globally.

Hyperloop Technology Market Overview

The hyperloop technology market encompasses tube infrastructure, electromagnetic propulsion systems, passenger and cargo capsules, and enabling control technologies. Market structure integrates technology developers, infrastructure contractors, equipment manufacturers, regulatory bodies, and end-user transport operators globally.

The ecosystem integrates global technology developers, civil engineering and construction contractors, component manufacturers, regulatory agencies, project finance institutions, government transport ministries, research institutions, and operational partners enabling commercial hyperloop deployment across passenger and freight transport sectors worldwide.

Market Dynamics

To evaluate market opportunities, Request Sample

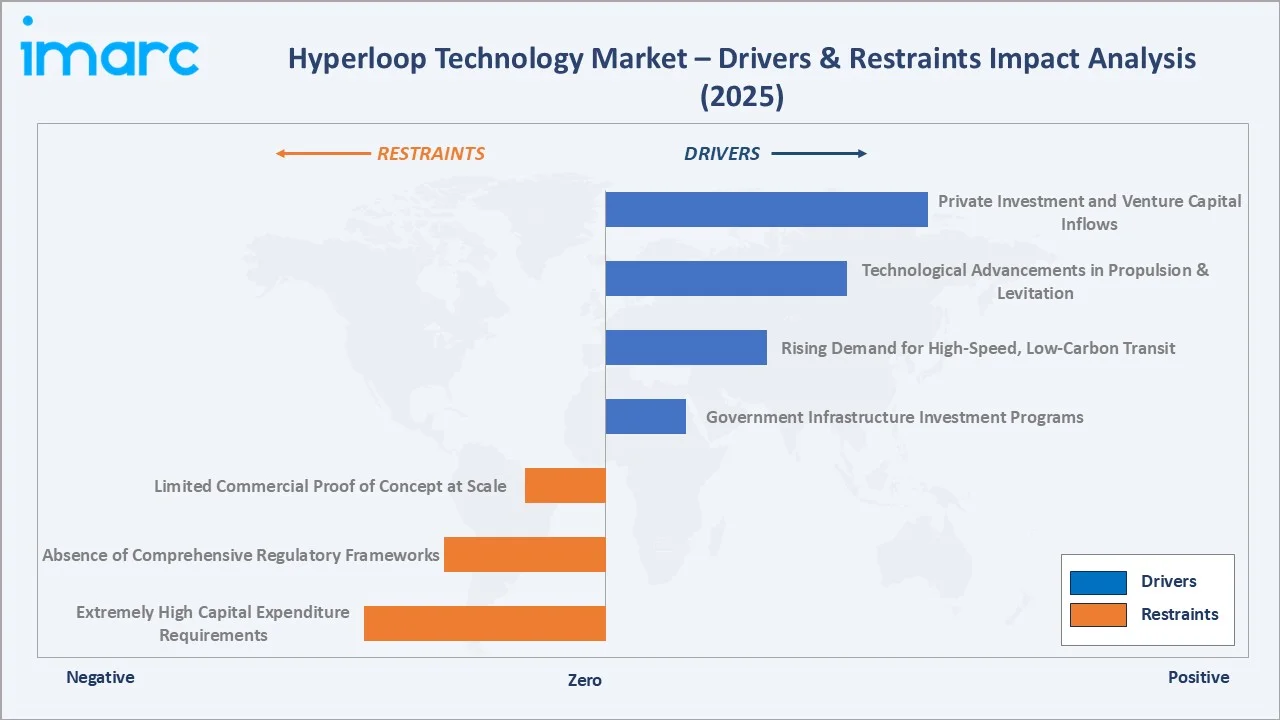

Market Drivers

- Government Infrastructure Investment Programs: Governments across Asia-Pacific, the Middle East, and North America are committing substantial public funding to hyperloop feasibility studies, pilot corridors, and regulatory frameworks. National transport modernisation agendas and stimulus-driven infrastructure packages are accelerating project pipelines globally.

- Rising Demand for High-Speed, Low-Carbon Transit: Escalating urban congestion, expanding megacity populations, and aggressive net-zero transport targets are driving demand for hyperloop as a viable alternative to short-haul aviation and road transport. Decarbonisation policy is elevating hyperloop on national transport agendas globally.

- Technological Advancements in Propulsion and Levitation: Continuous improvements in linear induction motor efficiency, magnetic levitation stability, vacuum pump technology, and capsule aerodynamics are reducing technical risk and improving cost projections. These advances are improving investor confidence and accelerating commercial deployment timelines globally.

- Private Investment and Venture Capital Inflows: Significant private capital from technology investors, infrastructure funds, and strategic corporate partners is funding hyperloop technology development, prototype testing, and route certification programmes. Growing investor confidence in the commercial viability of hyperloop is accelerating development globally.

Market Restraints

- Extremely High Capital Expenditure Requirements: Hyperloop infrastructure demands unprecedented per-kilometre capital investment for tube construction, depressurisation systems, and safety infrastructure. These extraordinary upfront costs create substantial financing barriers, limiting the pace of commercial deployment particularly in emerging markets with constrained public budgets.

- Absence of Comprehensive Regulatory and Safety Frameworks: No country has yet established complete commercial operational regulations for hyperloop systems. Regulatory uncertainty increases project risk, complicates insurance and financing, and extends development timelines across all active hyperloop projects in planning and construction stages globally.

- Limited Commercial Proof of Concept at Scale: The absence of fully operational commercial hyperloop networks constrains institutional investor confidence and public sector procurement decisions. Without demonstrated ridership, revenue, and operational safety records, hyperloop faces scepticism that slows investment and adoption compared to proven high-speed rail alternatives.

Market Opportunities

- High-Value Express Cargo and Cold Chain Logistics: The pharmaceutical, electronics, and perishable goods sectors represent significant untapped demand for hyperloop freight services. Ultra-fast point-to-point cargo delivery with minimal handling offers substantial competitive advantages over existing express logistics options for high-value, time-critical shipments globally.

- Cross-Border Regional Connectivity Projects: Gulf Cooperation Council nations, European corridors, and ASEAN connectivity initiatives present high-potential opportunities for hyperloop as a cross-border transport solution. Government-to-government infrastructure agreements are creating favourable conditions for multi-country hyperloop route development.

Market Challenges

- Engineering Complexity and Safety Certification: Maintaining a stable, low-pressure environment across hundreds of kilometres of tube, ensuring fail-safe emergency evacuation protocols, and certifying novel propulsion systems presents unprecedented engineering and safety certification challenges for hyperloop developers and regulators globally.

- Competition from High-Speed Rail Expansion: Well-established and proven high-speed rail networks are expanding rapidly across Asia, Europe, and the Middle East. These systems offer a commercially validated alternative with established regulatory frameworks and financing models, creating competitive pressure on hyperloop project economics and timelines.

Emerging Market Trends

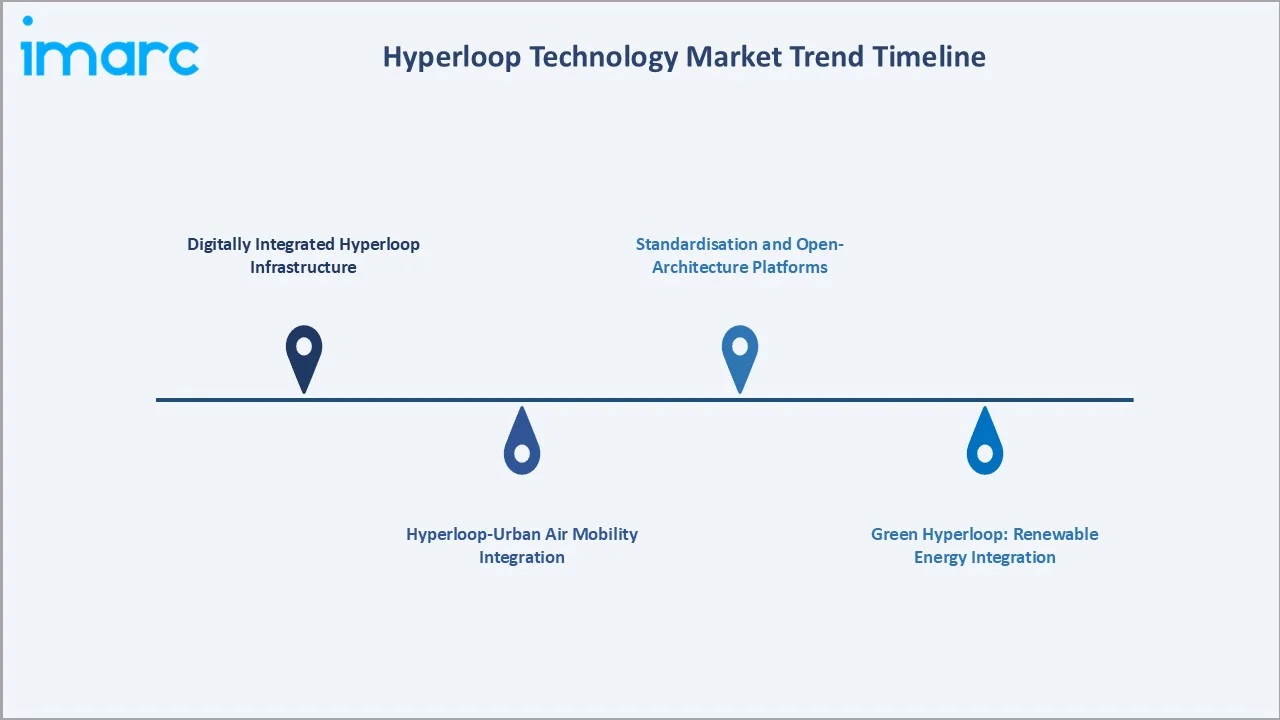

1. Digitally Integrated Hyperloop Infrastructure

Advanced digital twin technology, IoT sensor networks, and AI-based operations management are being integrated into hyperloop system design. Real-time structural monitoring, predictive maintenance, and automated safety systems are becoming core design requirements, reducing operational risk and lifecycle costs significantly across all hyperloop projects.

2. Hyperloop-Urban Air Mobility Integration

Strategic integration of hyperloop terminus design with urban air mobility hubs, last-mile autonomous vehicle networks, and smart city transit systems is emerging as a key planning trend. Multi-modal seamless connectivity is becoming a central value proposition for hyperloop project developers globally.

3. Green Hyperloop: Renewable Energy Integration

Hyperloop developers are designing systems to operate entirely on renewable energy through integrated solar panel arrays on tube surfaces, regenerative braking energy recovery, and direct grid connection to renewable power sources, reinforcing hyperloop's positioning as a zero-emission transport mode globally.

4. Standardisation and Open-Architecture Platforms

Industry consortia and standards bodies are advancing interoperability standards for hyperloop tube dimensions, docking systems, and capsule interfaces. Open-architecture platforms enabling multiple capsule operators to serve common infrastructure are emerging as a commercial model that accelerates investment and route development globally.

Industry Value Chain Analysis

The hyperloop value chain spans five integrated stages from raw material sourcing through end-user transport services. System integrators capture primary value through engineering design and technology, while infrastructure deployment and long-term operations generate significant recurring revenue streams supporting sustained project economics globally.

|

Stage |

Key Activities |

|

Raw Material Procurement |

Sourcing of steel, composites, vacuum components, and control electronics from global supply chains |

|

Component Manufacturing |

Production of tube sections, linear motor assemblies, magnetic levitation rails, and capsule structures |

|

System Integration & Testing |

Full-system assembly, vacuum testing, propulsion commissioning, and safety certification activities |

|

Infrastructure Deployment |

Civil construction, tube installation, station development, and control systems integration |

|

Operations & End-User Services |

Commercial passenger and cargo operations, maintenance, ticketing, and logistics integration |

System integration and testing stages capture the highest value in the hyperloop chain, requiring specialised engineering expertise, regulatory certification knowledge, and sophisticated quality systems. Long-term operations, maintenance, and service contracts represent significant recurring revenue streams supporting project financial viability globally.

Technology Landscape in the Hyperloop Technology Industry

Magnetic Levitation and Linear Motor Propulsion

Advanced passive and active magnetic levitation systems combined with linear synchronous and induction motor propulsion represent the core enabling technologies for hyperloop. Ongoing advances in superconducting magnet efficiency and motor power density are progressively improving speed, energy efficiency, and cost economics globally.

Low-Pressure Tube Vacuum Systems

Maintaining stable near-vacuum conditions across operational tube networks requires advanced vacuum pump technology, airtight tube construction, and real-time pressure management systems. Innovations in vacuum pump energy efficiency and tube sealing technology are addressing the significant operational energy cost of pressure maintenance globally.

AI-Driven Operations and Safety Management

Machine learning platforms are being deployed for real-time structural monitoring, capsule scheduling optimisation, predictive maintenance, and emergency response automation. AI-driven operational systems reduce staffing requirements, improve on-time performance, and enhance passenger safety across hyperloop systems in development globally.

Advanced Composite Tube Manufacturing

Carbon fibre reinforced polymer and advanced high-strength steel tube fabrication technologies are enabling lighter, stronger, and more cost-effective tube sections. Automated manufacturing processes and modular design are reducing construction costs and installation timelines, directly improving hyperloop project financial viability globally.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component Type |

Tube |

38.6% |

2025 |

|

Carriage Type |

Passenger |

71.5% |

2025 |

|

Speed |

🔒 |

🔒 |

2025 |

|

Region |

Asia-Pacific |

36.9% |

2025 |

By Component Type

Tube commands a 38.6% majority share in 2025 owing to its fundamental role as the primary infrastructure element in every hyperloop system. All hyperloop routes require extensive tube networks to create and maintain the controlled low-pressure environment enabling high-speed travel, making tube the single largest cost and investment category globally.

To access detailed market analysis, Request Sample

Propulsion System (27.4%) encompasses linear motor technologies, power electronics, and energy management systems enabling acceleration and sustained high-speed operation. Capsule (21.3%) addresses vehicle design, passenger environment management, and cargo container engineering. Others (12.7%) covers control systems, safety monitoring, station infrastructure, and telecommunications.

By Carriage Type

Passenger dominates at 71.5% in 2025, driven by the compelling commercial case for ultra-fast intercity passenger transit. Reducing travel times between major city pairs from hours to minutes generates strong willingness-to-pay and attracts significant private and government investment into passenger-focused hyperloop corridor development globally.

Cargo/Freight (28.5%) encompasses express package delivery, high-value component logistics, and cold-chain freight applications requiring speed advantages over conventional transport. Growing e-commerce demand and supply chain resilience priorities are driving increasing investment in hyperloop freight-dedicated and mixed-use corridor planning globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

36.9% |

Government-led hyperloop programmes, high-density population corridors, and strong R&D investment across China, India, Japan, and South Korea |

|

North America |

28.4% |

Active private sector hyperloop development, strong venture capital ecosystem, and multiple US corridor feasibility programmes underway |

|

Europe |

22.6% |

EU-funded research programmes, climate transport policy support, and UK regulatory sandbox enabling hyperloop technology certification |

|

Middle East and Africa |

7.1% |

UAE and Saudi Arabia giga-project transport inclusions, Gulf state infrastructure ambition, and sovereign wealth fund investment |

|

Latin America |

5.0% |

Brazil and Mexico feasibility corridor studies and growing interest in sustainable high-speed inter-city transport infrastructure |

Asia-Pacific's 36.9% market dominance in 2025 is driven by ambitious government-sponsored hyperloop programmes in China and India, strategic investment by Gulf nations in futuristic transit infrastructure, and strong regional R&D ecosystems in Japan and South Korea. The region's population density and corridor geography are ideal for high-speed hyperloop deployment.

North America at 28.4% in 2025 is anchored by the United States' active private sector hyperloop development ecosystem, with multiple companies pursuing commercial corridor development between major city pairs. Europe at 22.6% benefits from EU research funding, climate transport policy support, and the UK's leadership in establishing hyperloop regulatory frameworks globally.

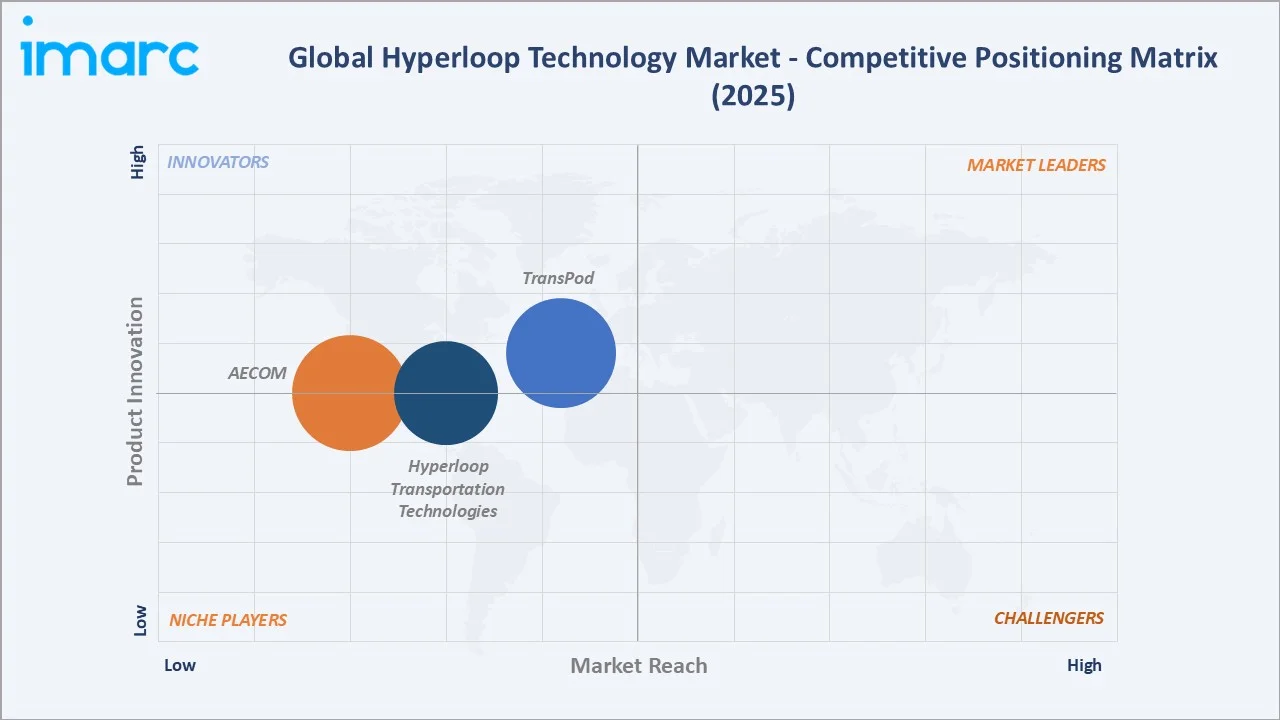

Competitive Landscape

The hyperloop technology market is moderately fragmented, with specialised technology developers and diversified engineering firms competing across technology development, route promotion, and infrastructure contracting roles. First-mover advantage, proprietary technology IP, and government partnerships define competitive positioning across the global hyperloop landscape.

|

Company Name |

Key Products / Operations |

Market Position |

Global Strategic Focus |

|

AECOM |

Hyperloop Texas Project, Hyperloop infrastructure consulting |

Established |

Leveraging global engineering capabilities to lead hyperloop route feasibility and civil design globally |

|

Hyperloop Transportation Technologies |

Hyperloop system projects |

Established |

Advancing commercial licensing model; partnering with governments and developers on corridor projects |

|

TransPod |

Hyperloop projects, FluxJet |

Emerging |

Targeting Canadian inter-city corridors; developing integrated hyperloop-renewable energy financing model |

Key players include AECOM, Hyperloop Transportation Technologies, TransPod, and others.

Key Company Profiles

AECOM

AECOM is a global infrastructure engineering and professional services firm providing planning, design, construction management, and consulting services across transportation, water, environment, and government sectors. AECOM has positioned itself as a leading hyperloop infrastructure consultant providing feasibility and design services on multiple major global hyperloop projects.

- Product Portfolio: Hyperloop Texas Project, Hyperloop infrastructure consulting

- Strategic Focus: AECOM is executing a strategy of establishing itself as the preferred engineering partner for hyperloop infrastructure projects globally, leveraging its relationships with government transport agencies, deep civil engineering capabilities, and international project delivery experience across complex transport infrastructure programmes.

Hyperloop Transportation Technologies

Hyperloop Transportation Technologies is a global technology and transport company developing a full stack hyperloop system including tube infrastructure, capsule design, propulsion technology, and operations management.

- Product Portfolio: Hyperloop system projects

- Recent Developments: In January 2024, Hyperloop Transportation launched Hyper Transfer, a joint venture in Italy aimed at advancing the country’s first commercial hyperloop system. Developed in partnership with Hyperloop Italia, the project will focus on designing and delivering ultra-high-speed transportation infrastructure in the Veneto region. The initiative marks a major step for hyperloop development in Europe, reinforcing Italy’s position as an early leader in next-generation mobility and moving the technology closer to real-world deployment.

- Strategic Focus: HyperloopTT is focused on securing commercial operating licences and government concession agreements across multiple international corridors, building on its technology licensing model and open-innovation platform to accelerate system development while expanding its global partner and government relationship network.

Market Concentration Analysis

The hyperloop technology market is highly fragmented with multiple early-stage technology developers, specialised engineering firms, and diversified industrial conglomerates competing across technology, infrastructure, and services roles. No single company currently commands dominant global market share, reflecting the pre-commercial development stage of the industry.

At the application level, passenger transport programmes receive most investment and commercial development activity, while cargo hyperloop remains primarily at the conceptual and feasibility stage. Geographic concentration of active project pipelines in Asia-Pacific and North America creates regional competitive dynamics distinct from Europe and emerging markets globally.

Investment & Growth Opportunities

Fastest-Growing Segments

Tube infrastructure represents the largest capital investment opportunity through 2034 given its per-kilometre cost intensity and requirement across all hyperloop routes globally. Passenger carriage systems are expected to lead commercial revenue growth at approximately 29.4% CAGR, driven by fare revenue from initial commercial route launches in Asia-Pacific and North America.

Emerging Markets

Asia-Pacific and the Middle East represent the most active investment frontiers. India's National Hyperloop Mission, China's high-speed transport research programmes, and megaproject inclusions are creating substantial near-term project opportunities. Southeast Asian connectivity corridors represent a growing medium-term development pipeline for hyperloop investors globally.

Venture & Investment Trends

Infrastructure funds, sovereign wealth funds, and strategic corporate investors are increasing capital allocation to hyperloop technology companies demonstrating regulatory progress and route concession agreements. Government co-investment frameworks are emerging as the dominant financing model, combining public infrastructure grants with private project finance to manage the unprecedented capital requirements of commercial hyperloop deployment globally.

Future Market Outlook (2026-2034)

The hyperloop technology market is forecast to expand from USD 4.33 Billion in 2025 to USD 44.58 Billion by 2034 at a CAGR of 28.69%, driven by government infrastructure commitment, first-mover commercial route openings, and expanding private investment across passenger and cargo hyperloop segments throughout the global market.

Three structural forces will shape the market through 2034: first commercial route launches in Asia-Pacific and the Middle East will validate hyperloop economics and accelerate global adoption; digital and energy technology integration will progressively reduce operational costs improving project financial viability; and establishment of international regulatory standards will unlock institutional investment at the scale required for broad network deployment globally.

Research Methodology

Primary Research

Primary research encompassed structured interviews with hyperloop technology developers, civil engineering consultants, government transport ministry officials, infrastructure project finance specialists, and safety certification experts. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines across the hyperloop technology market globally.

Secondary Research

Key secondary sources include government transport ministry publications, regulatory agency reports, industry association whitepapers, annual reports from key technology companies, academic research journals on magnetic levitation and vacuum transport, and market intelligence databases covering transportation infrastructure and emerging mobility sectors globally.

Forecasting Models

Market forecasts were derived using bottom-up and top-down modelling approaches, incorporating project pipeline analysis, government investment commitment data, technology readiness assessments, and comparable infrastructure market adoption curves. Scenario analysis captured upside and downside risks associated with regulatory milestones, capital availability, and technology development timelines globally.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Segment Coverage | Component Type, Speed, Carriage Type, Region |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AECOM, Hyperloop Transportation Technologies, TransPod, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, market trends, market forecasts, and dynamics of the hyperloop technology market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global hyperloop technology market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the hyperloop technology industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Hyperloop Technology Market Report

The global hyperloop technology market reached USD 4.33 Billion in 2025, reflecting sustained demand driven by government infrastructure investment, private sector development activity, and growing commercial interest in high-speed low-carbon transport solutions across major global markets.

The market is projected to reach USD 44.58 Billion by 2034, growing at a CAGR of 28.69% during 2026-2034, driven by first commercial route openings, expanded government funding, technology maturation, and increasing private capital deployment into hyperloop corridor development globally.

Tube leads the market with a 38.6% share in 2025, driven by its fundamental role as the primary structural and pressure-containment infrastructure in every hyperloop system. This segment is expected to maintain its leadership through 2034 as global route development accelerates.

Passenger commands the largest carriage type share at 71.5% in 2025. The compelling commercial case for ultra-fast intercity passenger transit, strong government support, and high fare revenue potential are sustaining this segment's market leadership through the forecast period.

Asia-Pacific dominates with a 36.9% share in 2025, underpinned by China's national hyperloop programmes, India's transit infrastructure push, and Gulf state megaproject inclusions. The region is expected to maintain its leadership position through the 2034 forecast horizon globally.

Key market drivers include government infrastructure investment programmes, rising demand for high-speed low-carbon transit, continuous technological advancements in magnetic levitation and propulsion, and growing private investment and venture capital inflows supporting hyperloop technology development globally.

Major challenges include extremely high capital expenditure requirements, absence of comprehensive regulatory and safety frameworks, limited commercial proof of concept at scale, intense competition from established high-speed rail, and complex engineering and safety certification requirements globally.

Leading companies in the hyperloop technology market include AECOM, Hyperloop Transportation Technologies, TransPod, and others.

Key emerging technologies include AI-driven digital twin operations management, IoT-enabled structural monitoring, renewable energy-integrated tube infrastructure, continuous improvement in superconducting magnetic levitation systems, advanced composite tube manufacturing, and open-architecture interoperability platforms enabling multi-operator commercial network deployment globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade