Ice Cream Market in India Size, Share, Trends and Forecast by Type, Flavor, Format, End-User, Distribution Channel, and Region, 2026-2034

Ice Cream Market in India Size, Share, Trends & Forecast (2026-2034)

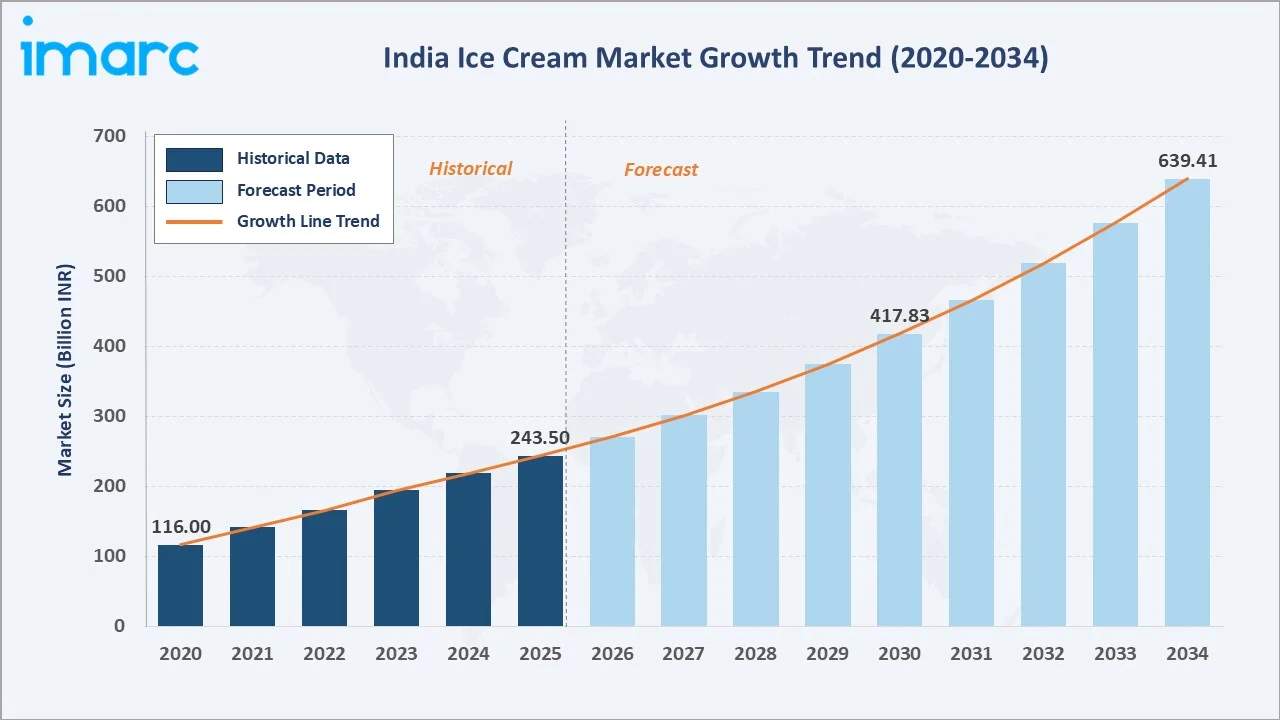

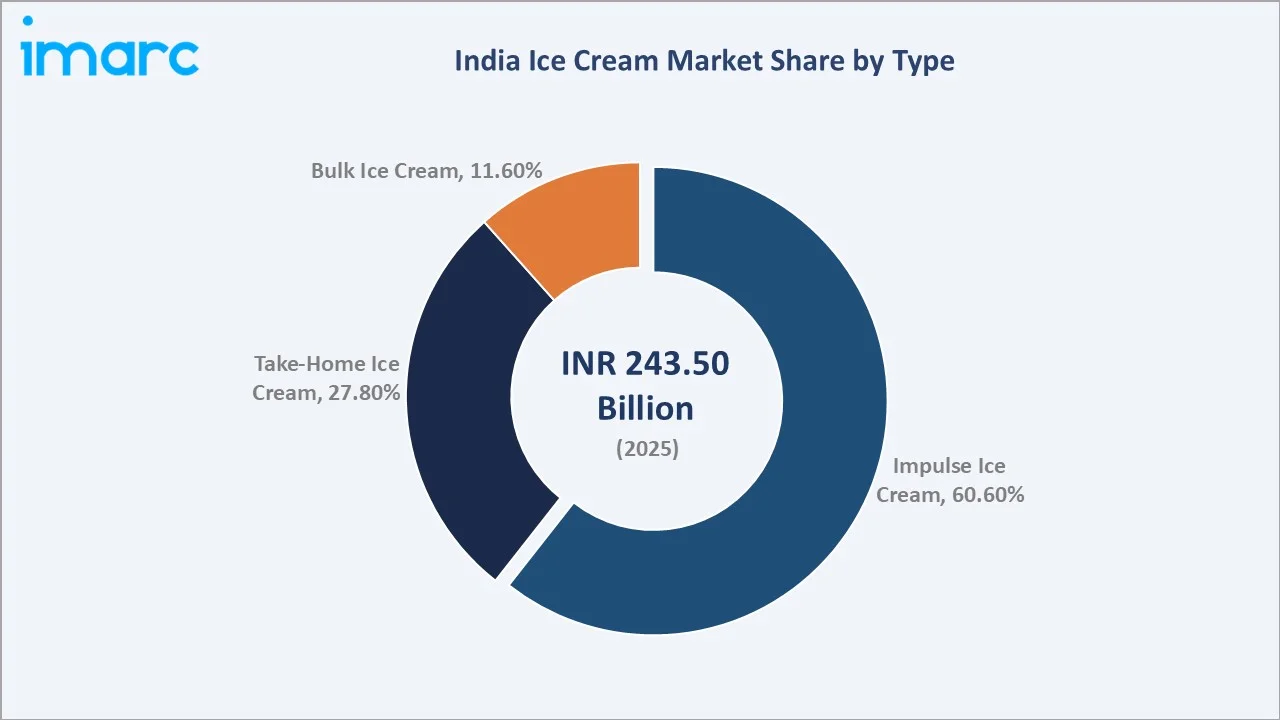

The ice cream market in India was valued at INR 243.50 Billion in 2025 and is estimated to reach INR 271.7 Billion in 2026. The market is further projected to grow INR 639.41 Billion by 2034 , exhibiting at a CAGR of 11.29% during 2026-2034. The market is driven by rising disposable incomes, rapid urbanization, and growing demand for indulgent and premium frozen desserts. India’s per capita ice cream consumption has increased steadily over the last decade, rising from 400 millilitres in 2011 to nearly 1.6 litres in 2023. This growth reflects changing consumer preferences, higher disposable incomes, and rising acceptance of ice cream as a regular dessert rather than an occasional treat. Expanding urban retail, quick-commerce, and foodservice channels are further supporting market growth. Impulse ice cream leads at 60.60%. Cones leads the format at 27.30%. Maharashtra leads regionally at 15.90%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 243.50 Billion |

| Market Size (2026) | INR 271.7 Billion |

|

Forecast Market Size (2034) |

INR 639.41 Billion |

|

CAGR (2026-2034) |

11.29% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Impulse Ice Cream (60.60%, 2025) |

|

Dominant Format |

Cones (27.30%, 2025) |

|

Leading State |

Maharashtra (15.90%, 2025) |

The ice cream market in India grew strongly from INR 116.00 Billion in 2020 to INR 243.50 Billion in 2025, supported by rising incomes, urbanization, and changing dessert preferences. The market is expected to reach INR 417.83 Billion by 2030, indicating rapid expansion in organized retail, foodservice, and online delivery channels. By 2034, it is forecast to touch INR 639.41 Billion, reflecting sustained demand for premium, impulse, and innovative frozen dessert products. This growth highlights ice cream’s shift from an occasional treat to a regular consumption category in India.

To get more information on this market, Request Sample

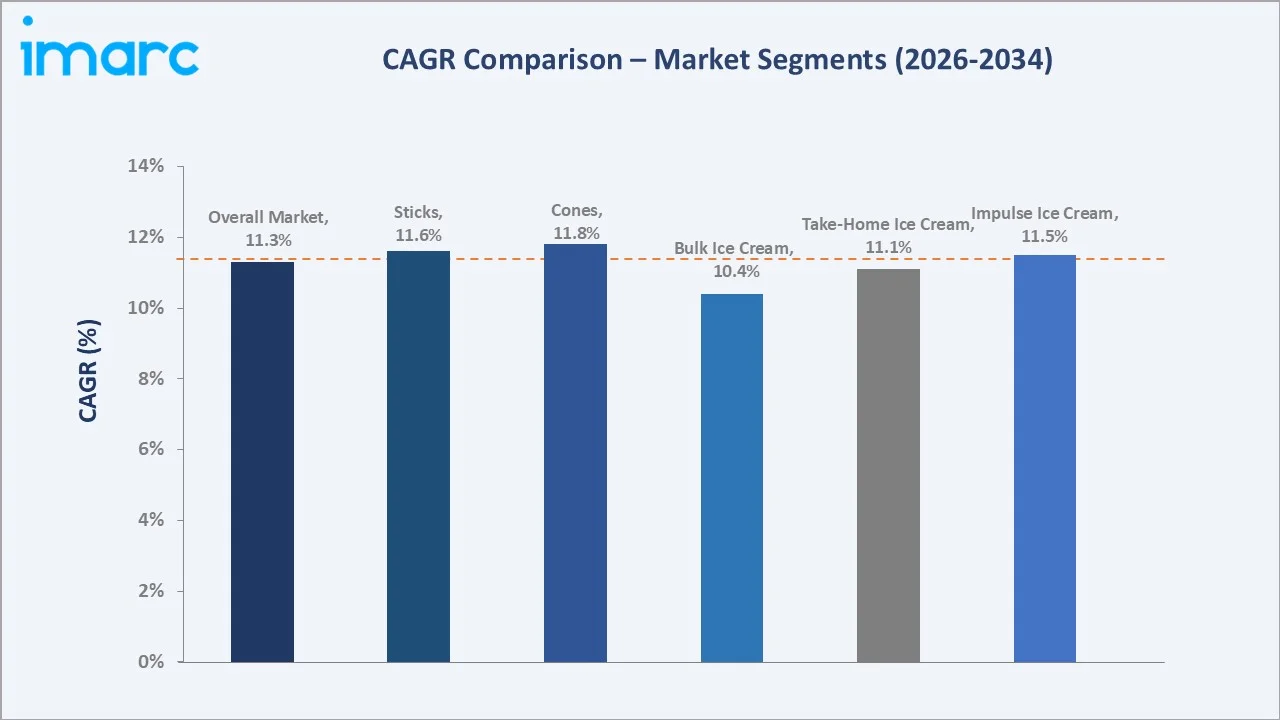

Cones grow fastest among formats at ~11.8% CAGR through artisan waffle cone, QSR soft-serve, and premium gelato cone expansion. Impulse ice cream type grows at ~11.5% CAGR through Q-commerce delivery impulse, affordable mini-stick scale in tier-2/3 cities, and street push-cart penetration in non-metro India.

Executive Summary

The ice cream market in India is expanding rapidly, rising from INR 116.0 Billion in 2020 to INR 243.50 Billion in 2025. It is projected to reach INR 639.41 Billion by 2034, driven by rising disposable incomes, urbanization, and increasing per capita consumption. Growth is supported by premium flavors, impulse products, organized retail, and online delivery. Expanding cold-chain infrastructure and wider availability across Tier-2 and Tier-3 cities are further strengthening demand. Impulse ice cream at 60.60% leads through street vending volume. Cones at 27.30% lead format. Maharashtra leads at 15.90%.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Impulse Ice Cream - 60.60% share (2025) |

|

Dominant Format |

Cones - 27.30% market share (2025) |

|

Leading State |

Maharashtra - 15.90% share (2025) |

|

Market Opportunity |

Vegan and plant-based ice cream; millet and functional health ice cream; gelato and artisan premium; tier-2/3 Q-commerce; franchise parlor; private label modern trade |

Key Analytical Observations Supporting the Above Data:

- Impulse Ice Cream at 60.60%: The impulse ice cream segment is dominant due to strong demand for single-serve products such as cones, cups, sticks, and bars. Its affordability, convenience, and wide availability through retail stores, kiosks, and quick-commerce channels support frequent consumption.

- Cones at 27.30%: The cones segment is dominant due to its strong appeal as a convenient, portable, and affordable ice cream format. Wide availability through retail outlets, parlours, kiosks, and impulse purchase channels supports its leading position.

- Maharashtra at 15.90%: Maharashtra is a dominant state due to its large urban consumer base and high disposable income. Well-developed retail, foodservice, cold-chain, and quick-commerce networks further support ice cream consumption.

Ice Cream Market in India Overview

The ice cream market in India encompasses impulse ice creams, take-home packs, artisanal products, premium variants, and frozen desserts sold through retail, foodservice, and online delivery channels. Demand is supported by rising urban consumption, young demographics, higher disposable incomes, and growing preference for indulgent desserts. The market also includes cones, cups, sticks, tubs, sundaes, and innovative flavors tailored to regional tastes. Cold-chain expansion and quick-commerce platforms are further widening product availability across urban and semi-urban India. Macroeconomic factors include rising disposable incomes, rapid urbanization, and expanding middle-class consumption.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

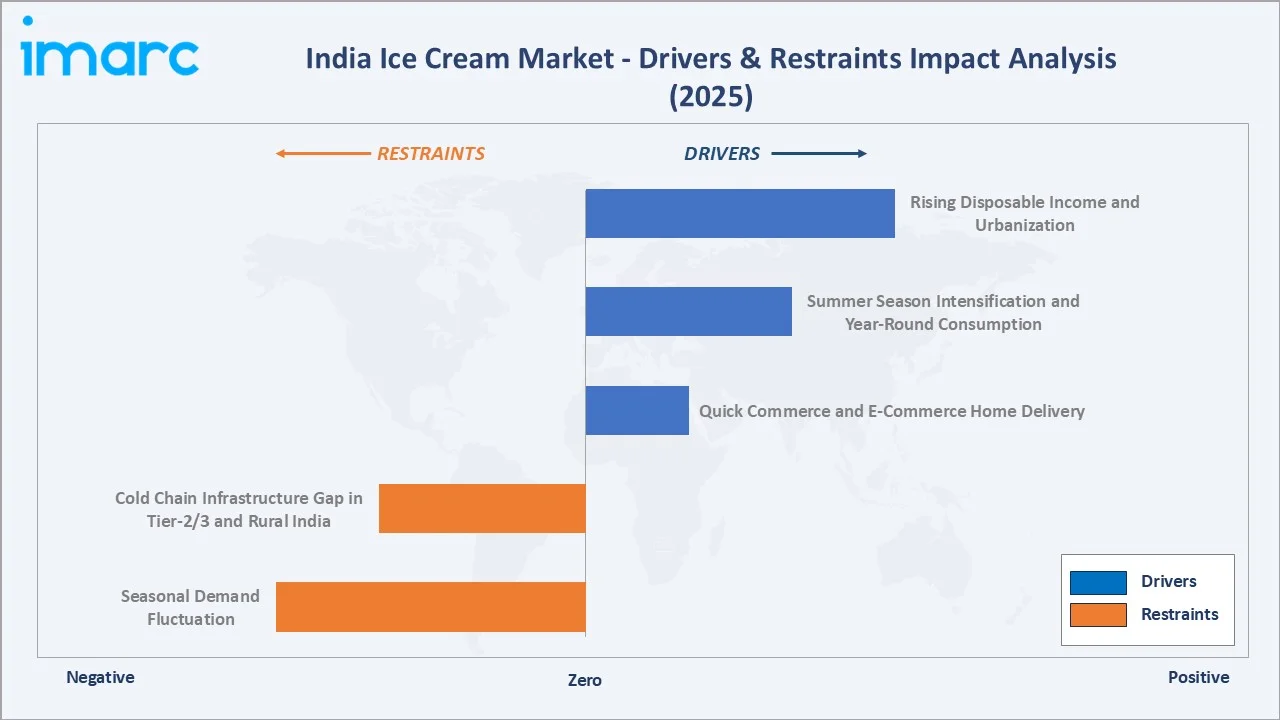

- Rising Disposable Income and Urbanization: The Economic Survey noted that the World Bank expects India’s urban population to reach 600 million by 2036, accounting for 40% of the total population, compared to 31% in 2011. Urban areas are also projected to contribute nearly 70% of India’s GDP. Growing urban populations have greater access to modern retail stores, ice cream parlours, and food delivery platforms, boosting product availability and consumption. Higher household incomes are also encouraging demand for premium, artisanal, and innovative ice cream offerings. As lifestyles become more fast-paced and consumption-driven, ice cream is increasingly viewed as an everyday treat rather than a seasonal luxury.

- Summer Season Intensification and Year-Round Consumption: Summer season intensification and year-round consumption are driving the market as hotter and longer summers increase demand for cooling and indulgent products. Rising temperatures encourage frequent purchases of cones, cups, sticks, and family packs. At the same time, ice cream consumption is expanding beyond summer due to malls, cafés, food delivery, and quick-commerce platforms. This shift from seasonal demand to regular dessert consumption supports stronger year-round market growth.

- Quick Commerce and E-Commerce Home Delivery: Quick commerce and e-commerce home delivery are driving the market by making frozen products more accessible for instant and planned consumption. Platforms offering rapid delivery help consumers buy cones, tubs, bars, and premium packs without visiting stores. Improved cold-chain packaging and last-mile delivery are reducing melting risks and expanding online sales. This is increasing impulse purchases, family consumption, and year-round demand across urban markets.

Market Restraints

- Cold Chain Infrastructure Gap in Tier-2/3 and Rural India: Frozen products require uninterrupted temperature-controlled storage and transport. Limited freezer availability, unreliable power supply, and weak last-mile cold logistics increase melting, spoilage, and product quality risks. This restricts distribution beyond major cities and raises operating costs for manufacturers and retailers. As a result, market penetration remains slower in semi-urban and rural areas despite rising consumer demand.

- Seasonal Demand Fluctuation: Consumption remains highly dependent on summer months and hot weather conditions. Demand often weakens during the monsoon and winter seasons, affecting sales consistency for manufacturers, retailers, and distributors. This creates challenges in production planning, inventory management, and freezer-space utilization. Seasonal variation also increases pressure on brands to develop year-round consumption formats, premium desserts, and delivery-led demand.

Market Opportunities

- Vegan and Millet-Based Functional Ice Creams: Vegan and millet-based functional ice creams present an opportunity in India as consumers increasingly seek healthier, plant-based, and locally inspired dessert options. Millet-based formulations can benefit from rising interest in nutrition-rich traditional grains, while vegan variants appeal to lactose-intolerant and health-conscious consumers. These products allow brands to differentiate through clean-label, high-fiber, protein-enriched, and premium offerings. As demand grows for functional and guilt-free indulgence, this segment can support innovation and higher-margin growth in the ice cream market in India.

- Artisanal Ice Cream Brand Expansion: Artisanal ice cream brand expansion presents a significant opportunity as consumers increasingly seek premium, unique, and locally inspired dessert experiences. In September 2025, Indulge Creamery, a new artisanal ice cream brand launched in India by hospitality professional Pawan Saluja, focuses on premium slow-churned ice creams made with quality ingredients and curated flavours. Its portfolio includes classic and modern options such as Belgian Chocolate, Cookies Cheesecake, Cream Biscotti, Vegan Dark Chocolate, and Vegan Mango Sorbet. The brand is also expanding into ice cream sticks with Espresso, Vanilla, and Dark Chocolate variants. Artisanal brands can differentiate through regional flavors, healthier formulations, and premium positioning, enabling higher margins.

Market Challenges

- Rising Milk, Sugar, and Packaging Material Costs: Rising milk, sugar, and packaging material costs are increasing production and operating expenses for manufacturers. Since milk is a primary ingredient, fluctuations in dairy prices can significantly impact profit margins. Higher sugar, cocoa, flavoring, and packaging costs further add to overall product expenses. These cost pressures make it difficult for companies to maintain competitive pricing in a price-sensitive market, often forcing them to absorb costs or reduce margins.

- Product Spoilage and Temperature-Control Risks: Product spoilage and temperature-control risks are a significant challenge as ice cream requires a continuous cold chain from manufacturing to consumption. Any interruption in refrigeration during storage, transportation, or retail display can lead to melting, texture deterioration, and product wastage. These risks are particularly pronounced in regions with inadequate cold-storage infrastructure and unreliable power supply. As a result, manufacturers and distributors face higher logistics costs, inventory losses, and quality-control challenges.

Emerging Market Trends

1. Quick Commerce 10-Minute Ice Cream Delivery

Quick commerce 10-minute ice cream delivery is making frozen desserts instantly accessible to urban consumers. Platforms such as Blinkit, Zepto, and Swiggy Instamart are enabling rapid delivery of cones, tubs, sticks, and premium packs with improved cold-chain handling. This supports impulse purchases, late-night consumption, and year-round demand beyond traditional retail stores. As brands optimize packaging and last-mile freezer logistics, quick commerce is becoming an important growth channel for ice cream sales.

2. Health-Conscious and Functional Formulations

Health-conscious and functional formulations are emerging as consumers seek indulgence with added nutritional value. Brands are introducing low-sugar, high-protein, probiotic, vegan, millet-based, and natural-ingredient variants to appeal to wellness-focused buyers. In October 2024, Iceberg, India’s first organic ice cream brand and a decade-old homegrown brand from the Telugu states, introduced its premium label, Organic Creamery, along with plans for major expansion across the market. These products help reduce guilt around dessert consumption while supporting premium positioning. Rising demand for clean-label and better-for-you snacks is encouraging innovation across the ice cream category.

3. Sustainability and Eco-Friendly Packaging

Sustainability and eco-friendly packaging are emerging as brands respond to rising consumer and regulatory focus on plastic reduction. Companies are exploring recyclable cups, paper-based packs, biodegradable spoons, and lower-waste packaging formats. This helps improve brand image while appealing to environmentally conscious urban consumers. Sustainable packaging also supports premium positioning and differentiation in a competitive frozen dessert market.

4. Franchise Parlor Expansion in Tier-2/3 Cities

Franchise parlor expansion in Tier-2 and Tier-3 cities is emerging as brands move beyond metros to capture rising demand in smaller urban centers. Growing disposable incomes, mall culture, and changing dessert habits are supporting franchise-based ice cream outlets. These parlors help brands build local visibility, offer premium flavors, and improve consumer access. Expansion into underserved cities also supports faster market penetration and stronger regional growth.

Industry Value Chain Analysis

India's ice cream value chain integrates raw material sourcing, processing & manufacturing, freezing, packaging & quality control, cold chain storage & logistics, distribution & sales channels, and end-use consumption.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Dairy farmers, milk cooperatives, sugar suppliers, fruit and flavor suppliers, stabilizer and ingredient providers |

|

Processing & Manufacturing |

Pasteurization facilities, homogenization plants, ice cream producers, contract manufacturers |

|

Freezing, Packaging & Quality Control |

Packaging companies, cold-processing facilities, QA/testing laboratories, food safety compliance providers |

|

Cold Chain Storage & Logistics |

Refrigerated warehousing providers, cold-chain logistics operators, freezer equipment suppliers |

|

Distribution & Sales Channels |

Distributors, wholesalers, supermarkets, convenience stores, ice cream parlors, quick-commerce and e-commerce platforms |

|

End-Use Consumption |

Consumers, cafés, restaurants, hotels, QSR chains, institutional buyers, and online delivery customers |

The processing & manufacturing stage is the most value-added stage. This is where raw milk, sugar, flavors, and ingredients are transformed into finished ice cream through pasteurization, homogenization, formulation, freezing, and product innovation. Manufacturers create value through recipe development, quality control, premium ingredients, and brand differentiation, making this stage the primary driver of margins and competitive advantage in the ice cream market in India.

Technology Landscape in the India Ice Cream Industry

Advanced Pasteurization and Homogenization Technology

Advanced pasteurization and homogenization technology improve product safety, texture, and consistency. Modern pasteurization systems enhance microbial control and extend shelf life, while advanced homogenization creates a smoother mouthfeel and uniform fat distribution. These technologies enable manufacturers to produce premium, low-fat, functional, and innovative ice cream variants at scale. As consumer expectations for quality rise, investments in automated processing systems are becoming increasingly important across the industry.

Cold Chain and Refrigerated Logistics Technology

Cold chain and refrigerated logistics technology ensure consistent temperature control from production to consumption. Advanced refrigerated transportation, cold storage facilities, and IoT-enabled temperature monitoring systems help reduce spoilage and maintain product quality. These technologies are critical for expanding distribution into Tier-2 and Tier-3 cities while supporting the growth of quick-commerce and home delivery channels. Improved cold-chain efficiency also enables manufacturers to offer premium and innovative ice cream products across wider geographic markets.

Low-Sugar and Sugar-Free Sweetening Technologies

Low-sugar and sugar-free sweetening technologies enable manufacturers to develop healthier dessert options without compromising taste and texture. Companies are increasingly using natural and alternative sweeteners such as stevia, monk fruit, erythritol, and other sugar substitutes to meet growing health-conscious consumer demand. In February 2026, Ice Cream Works launched its Zero Sugar Added range, entering the fast-growing better-for-you dessert category. Introduced under The House of Ice Cream Works, the new range targets health-conscious millennials, Gen Z consumers, fitness-focused buyers, and people managing dietary needs such as diabetes. These technologies support the development of diabetic-friendly, low-calorie, and functional ice cream products.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Impulse Ice Cream |

60.60% |

2025 |

|

Flavor |

🔒 |

🔒 |

2025 |

|

Format |

Cones |

27.30% |

2025 |

|

End-User |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Price Point |

🔒 |

🔒 |

2025 |

|

State |

Maharashtra |

15.90% |

2025 |

By Type

Impulse ice cream leads at 60.60% (2025), due to strong demand for convenient, single-serve formats such as cones, cups, sticks, and bars. These products are affordable, easy to consume on the go, and widely available through retail stores, kiosks, parlours, and quick-commerce platforms. Rising urban lifestyles, youth consumption, and frequent impulse purchases further support the segment’s dominance.

To access detailed market analysis, Request Sample

Take-home ice cream at 27.80% reflects growing modern trade and Q-commerce home delivery. Bulk ice cream at 11.60% reflects institutional catering, QSR, and wedding catering bulk ice creams.

By Format

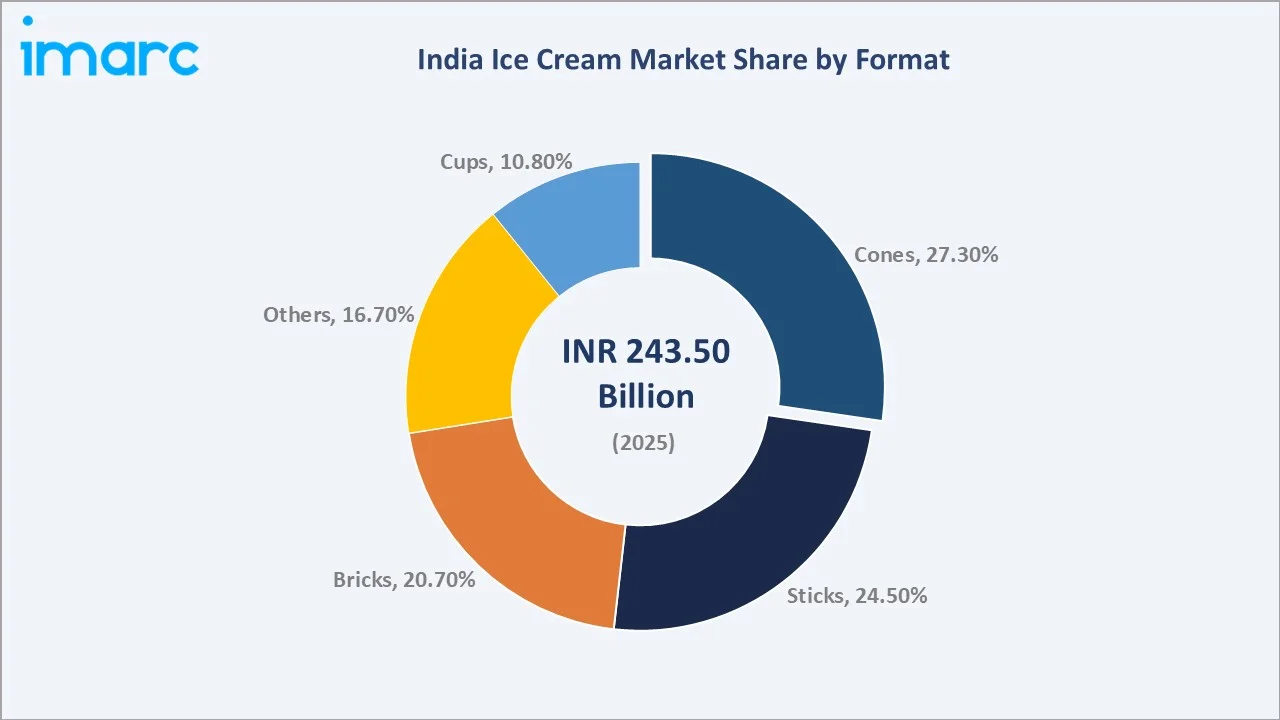

Cones lead at 27.30% (2025), due to their convenience, portability, and strong appeal as an on-the-go dessert format. Their affordable pricing and wide availability across kiosks, retail outlets, parlours, and quick-commerce platforms support frequent impulse purchases. Product innovation in waffle cones, chocolate-filled cones, and premium flavors further strengthens demand.

Sticks at 24.50% supported by their convenience, affordability, and popularity among younger consumers. Bricks at 20.70% driven by family consumption and take-home purchases, making them a preferred format for households. Cups at 10.80% benefiting from portion control, premium offerings, and easy consumption. Others at 16.80% includes sundaes, tubs, sandwiches, rolls, and specialty products that cater to evolving consumer preferences.

Regional Market Insights

|

State |

Share (2025) |

Key Ice Cream Market in India Drivers & Characteristics |

|

Maharashtra |

15.90% |

Driven by its large urban population, high disposable incomes, strong retail presence, and robust demand |

|

Uttar Pradesh |

9.50% |

Benefits from its large consumer base, expanding urbanization, growing middle-class population, and increasing penetration of organized retail and food delivery platforms. |

|

Karnataka |

7.90% |

Supported by rising premium ice cream consumption, strong café culture, technology-driven urban centers, and growing quick-commerce adoption. |

|

Gujarat |

7.60% |

Experiences strong demand due to its preference for dairy-based products, expanding retail infrastructure, and increasing consumption of premium and family-pack ice creams. |

|

Andhra Pradesh & Telangana |

7.10% |

Driven by urban growth, rising incomes, expanding cold-chain infrastructure, and increasing demand from Hyderabad and other major cities. |

|

Tamil Nadu |

6.60% |

Benefits from strong foodservice demand, a growing youth population, rising disposable incomes, and widespread availability of branded ice cream products. |

|

West Bengal |

6.20% |

Supported by dense urban centers, growing organized retail, and increasing consumer preference for packaged frozen desserts and premium offerings. |

|

Delhi |

5.90% |

Driven by high per-capita spending, premium product adoption, extensive food delivery networks, and a large concentration of modern retail outlets. |

|

Rajasthan |

4.00% |

Supported by hot climate conditions, rising urban consumption, and expanding retail reach in Jaipur and other cities. |

|

Kerala |

3.80% |

Driven by high consumer spending, tourism, foodservice demand, and growing premium dessert consumption. |

|

Bihar |

3.70% |

Benefits from a large population base, rising disposable incomes, and increasing branded ice cream penetration. |

|

Haryana |

3.50% |

Supported by urban growth, proximity to NCR, modern retail expansion, and rising impulse purchases. |

|

Madhya Pradesh |

3.40% |

Driven by growing Tier-2 city demand, improving cold-chain access, and rising packaged dessert consumption. |

|

Punjab |

3.20% |

Supported by a strong dairy consumption culture, high household spending, and demand for family-pack ice creams. |

|

Odisha |

1.90% |

Driven by urbanization, improving retail infrastructure, and the gradual expansion of branded ice cream availability. |

|

Others |

9.70% |

Remaining states contribute through expanding cold-chain networks, increasing urbanization, rising disposable incomes, and growing penetration of branded ice cream products across Tier-2 and Tier-3 cities. |

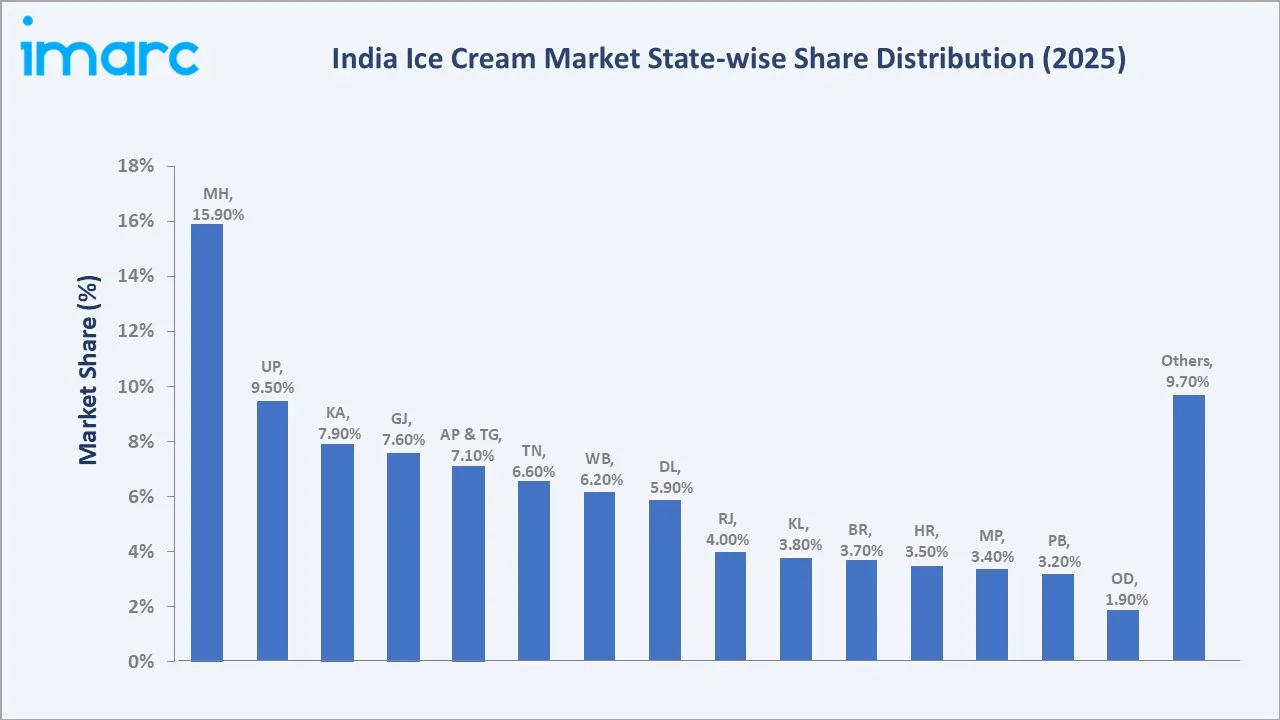

Maharashtra's 15.90% market dominance is supported by high urban consumption, strong retail penetration, and demand from cities such as Mumbai and Pune. Uttar Pradesh's 9.50% benefits from its large population base, rising middle-class income, and expanding organized retail. Karnataka's 7.90% driven by premium consumption, café culture, and quick-commerce adoption in Bengaluru.

Gujarat's 7.60% shows strong demand due to its dairy-rich consumption culture and family-pack purchases. Andhra Pradesh and Telangana's 7.10% supported by Hyderabad-led urban growth and improving cold-chain infrastructure. Tamil Nadu’s 6.60% and West Bengal’s 6.20% benefit from strong foodservice demand, branded product availability, and rising youth consumption. Delhi's 5.90% reflects high disposable incomes and strong delivery-platform penetration.

Competitive Landscape

The ice cream market in India is highly competitive, with a mix of national brands, regional dairy players, premium artisanal manufacturers, and emerging direct-to-consumer brands. Competition is driven by product innovation, flavor diversification, pricing strategies, distribution reach, and brand recognition.

|

Company |

Key Brands |

Market Position |

Core Strength |

|

The Magnum Ice Cream Company |

Kwality Wall’s, Cornetto, Magnum |

Market Leader |

The Magnum Ice Cream Company is reshaping the Indian dairy landscape by taking majority control of Kwality Wall's (India) Limited. |

|

GCMMF |

Amul |

Market Leader |

GCMMF acts as the apex marketing body for Amul, driving the democratization of ice cream across India. It transformed the dessert from a premium luxury into an affordable, mass-market staple by replacing vegetable fat "frozen desserts" with 100% real milk ice cream at highly competitive price points. |

|

Vadilal Group |

Vadilal |

Niche Player |

Vadilal Group is one of India’s largest ice cream brands. Originating as a small soda fountain, it acts as a pioneer in cold-chain distribution, extensive flavor innovation, and premiumization within the country's frozen dessert sector. |

|

LOTTE |

Havmor, LOTTE |

Strong Challenger |

LOTTE has transformed the Indian ice cream landscape by scaling Havmor Ice Cream into a pan-Indian powerhouse through aggressive infrastructure investments, advanced manufacturing technology, and the introduction of innovative Korean frozen snacks. |

|

Dinshaw’s Dairy Foods Pvt. Ltd. |

Dinshaw’s |

Strong Challenger |

Dinshaw’s Dairy Foods Pvt. Ltd. operates as a major legacy brand in the Indian ice cream market, combining traditional roots with massive, automated manufacturing capabilities. |

Leading companies are expanding their presence through quick-commerce partnerships, franchise parlors, premium product launches, and health-focused offerings such as low-sugar and plant-based ice creams. Regional players maintain strong positions through localized flavors and extensive retail networks. Investments in cold-chain infrastructure, digital channels, and sustainable packaging are further shaping the competitive landscape.

Key Company Profiles

The Magnum Ice Cream Company

The Magnum Ice Cream Company is a leading premium ice cream brand operating in India, known for its indulgent chocolate-coated ice cream bars and luxury positioning. The brand offers a portfolio of premium products featuring high-quality ingredients, Belgian chocolate coatings, and innovative flavor combinations targeted at affluent and urban consumers. Magnum has established a strong presence in major Indian cities through modern retail outlets, supermarkets, convenience stores, and quick-commerce platforms.

- Key Brands: Kwality Wall's, Cornetto, Magnum.

- Recent Developments: In April 2026, Magnum launched Magnum Caramel Pop in India, a bold new innovation that brings a playful twist to indulgence, while reinforcing the brand’s leadership in the premium ice cream segment.

- Strategic Focus: Strengthening its presence in India’s premium and indulgence ice cream segment through continuous flavor innovation, luxury positioning, and high-quality ingredients.

GCMMF

GCMMF, through its flagship brand Amul, is one of the leading players in the Ice Cream Market in India. Leveraging one of the largest dairy cooperative networks, the company offers a broad portfolio of ice creams, frozen desserts, cones, cups, sticks, family packs, and premium variants. Amul benefits from extensive milk procurement capabilities, strong brand recognition, and a vast distribution network spanning urban and rural India.

- Key Brands: Amul.

- Strategic Focus: Expanding its leadership in the ice cream market in India through a combination of mass-market reach, product innovation, and distribution strength.

Market Concentration Analysis

The ice cream market in India is moderately concentrated, with a few large national players holding significant market share alongside numerous regional and local brands. Major companies benefit from strong brand recognition, extensive cold-chain infrastructure, broad distribution networks, and diversified product portfolios. Regional manufacturers remain competitive through localized flavors, competitive pricing, and strong presence in specific states. The market is also witnessing the emergence of premium, artisanal, vegan, and health-focused brands that are targeting niche consumer segments. While entry barriers related to cold-chain investment and distribution are substantial, growing demand and evolving consumer preferences continue to create opportunities for new entrants and category innovation.

Investment & Growth Opportunities

Highest Growth Segments

Q-commerce digital impulse (above-15% CAGR from a smaller base), vegan and plant-based (above-20% CAGR emerging), artisan gelato premium (above-14% CAGR), tier-2/3 franchise parlor (above-12% CAGR), millet and functional ice cream (above-15% CAGR), and take-home modern trade (above-12% CAGR through D-Mart and Reliance) represent India ice cream highest-growth investment vectors through 2034.

Investment Themes

- Quick commerce digital impulse ice cream: This is an attractive investment theme as platforms such as Blinkit, Zepto, and Swiggy Instamart are transforming ice cream into an on-demand purchase category. Investments in cold-chain-enabled last-mile delivery, digital merchandising, and exclusive online SKUs can drive higher impulse consumption and urban market penetration.

- Vegan and millet-based functional ice cream: Growing health awareness, lactose intolerance concerns, and demand for better-for-you desserts are creating opportunities for plant-based and millet-enriched ice creams. Brands investing in functional formulations, clean-label ingredients, and premium health-focused products can benefit from higher margins and differentiated positioning.

- Tier-2/3 city franchise parlor expansion: Expanding franchise networks into Tier-2 and Tier-3 cities offers access to large, underserved consumer markets with rising disposable incomes and changing consumption habits. Investments in branded parlors, localized product offerings, and cold-chain infrastructure can accelerate market penetration and long-term revenue growth.

Future Market Outlook (2026-2034)

The ice cream market in India is projected to grow from INR 243.50 Billion in 2025 to INR 639.41 Billion by 2034, registering a strong 11.29% CAGR. Growth is supported by rising disposable incomes, urbanization, quick-commerce delivery, premiumization, and expanding cold-chain infrastructure. The INR 417.83 Billion anchor value in 2030 reflects a key inflection point where ice cream becomes more mainstream across metro and Tier-2/3 markets. This growth also highlights rising demand for impulse formats, premium products, vegan variants, and functional ice creams.

Three structural forces define ice cream market in India through 2034: rising urban incomes, expanding cold-chain and quick-commerce networks, and strong product innovation. Growing demand for impulse formats, premium desserts, and year-round consumption is shifting ice cream from a seasonal treat to a regular indulgence. At the same time, vegan, millet-based, low-sugar, and functional formulations are widening the consumer base. Expansion into Tier-2 and Tier-3 cities will further strengthen long-term market growth.

Research Methodology

Primary Research

Primary research comprised interviews and discussions with ice cream manufacturers, dairy processors, distributors, cold-chain operators, retailers, franchise owners, and industry experts across India. Insights were also gathered from consumers, foodservice operators, and quick-commerce platforms to understand purchasing behavior, flavor preferences, pricing trends, and distribution dynamics.

Secondary Research

Secondary research encompassed company reports, industry publications, government data, trade sources, food safety regulations, and dairy sector statistics. It also included reviewing retail trends, cold-chain infrastructure, quick-commerce growth, consumer spending patterns, and product launch information. These sources helped benchmark market sizing, regional demand, competitive landscape, and long-term growth assumptions.

Forecasting Models

Forecasting models combined historical market performance, per capita consumption trends, demographic shifts, and macroeconomic indicators to project demand through 2034. The analysis incorporated factors such as disposable income growth, urbanization, cold-chain expansion, quick-commerce penetration, and evolving consumer preferences. Both top-down and bottom-up approaches were used, with scenario analysis applied to assess the impact of seasonality, premiumization, and health-focused product adoption on future market growth.

India Ice Cream Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Billion, Million Litres |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Impulse Ice Cream, Take-Home Ice Cream, Artisanal Ice Cream |

| Flavors Covered | Chocolate, Fruit, Vanilla, Others |

| Formats Covered | Cup, Stick, Cone, Brick Others |

| End-Users Covered | Retail, Institutional |

| Distribution Channels Covered | General Trade, Supermarkets/Hypermarkets, Ice Cream Parlors, Convenience Stores, Online, Others |

| States Covered | Karnataka, Maharashtra, Tamil Nadu, Delhi, Gujarat, Andhra Pradesh and Telangana, Uttar Pradesh, West Bengal, Kerala, Haryana, Punjab, Rajasthan, Madhya Pradesh, Bihar, Odisha |

| Companies Covered | The Magnum Ice Cream Company, GCMMF, Vadilal Group, LOTTE, Dinshaw’s Dairy Foods Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Ice cream market in India from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Ice cream market in India.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Ice cream market in India industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Ice Cream Market in India Report

The ice cream market in India reached INR 243.50 Billion in 2025, driven by rising disposable incomes, urbanization, higher per capita consumption, and growing demand for impulse and premium frozen desserts. Quick-commerce delivery, cold-chain expansion, and product innovation in vegan, low-sugar, and functional ice creams further support market growth.

The ice cream market in India grows at 11.29% CAGR during 2026-2034, reaching INR 639.41 Billion by 2034. The CAGR reflects young population, rising income, Q-commerce digital impulse, premiumization trade-up, tier-2/3 city franchise expansion, and vegan functional ice cream growth.

Impulse leads at 60.60% due to strong demand for convenient, single-serve products such as cones, cups, and sticks. Its affordability, portability, and wide availability through retail outlets, kiosks, parlours, and quick-commerce platforms drive frequent purchases and high consumption volumes.

Cones lead at 27.30% due to their convenience, affordability, and strong appeal as an on-the-go dessert format. Wide availability across kiosks, retail stores, parlours, and quick-commerce platforms supports frequent impulse purchases.

Maharashtra leads at 15.90% due to its large urban consumer base, high disposable incomes, and strong demand from Mumbai, Pune, and Nagpur. Well-developed retail, foodservice, cold-chain, and quick-commerce networks further support higher ice cream consumption.

Leading companies include The Magnum Ice Cream Company, GCMMF, Vadilal Group, LOTTE, and Dinshaw’s Dairy Foods Pvt. Ltd., among others.

The market is projected to reach approximately INR 417.83 Billion by 2030, reflecting strong mid-term expansion. Growth will be supported by rising per capita consumption, quick-commerce delivery, premiumization, and wider cold-chain penetration. This milestone represents a key inflection point as ice cream shifts from seasonal indulgence to regular dessert consumption across India.

Three priority investment opportunities in the ice cream market in India include quick-commerce-enabled impulse ice cream sales, vegan and millet-based functional ice creams, and franchise parlor expansion across Tier-2 and Tier-3 cities. These segments are benefiting from changing consumer preferences, rising health awareness, digital delivery growth, and increasing demand from underserved regional markets, creating strong potential for long-term revenue expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)