India A2 Ghee Market Size, Share, Trends and Forecast by Type, Application, Distribution Channel, and Region, 2026-2034

India A2 Ghee Market Size, Share, Trends & Forecast (2026-2034)

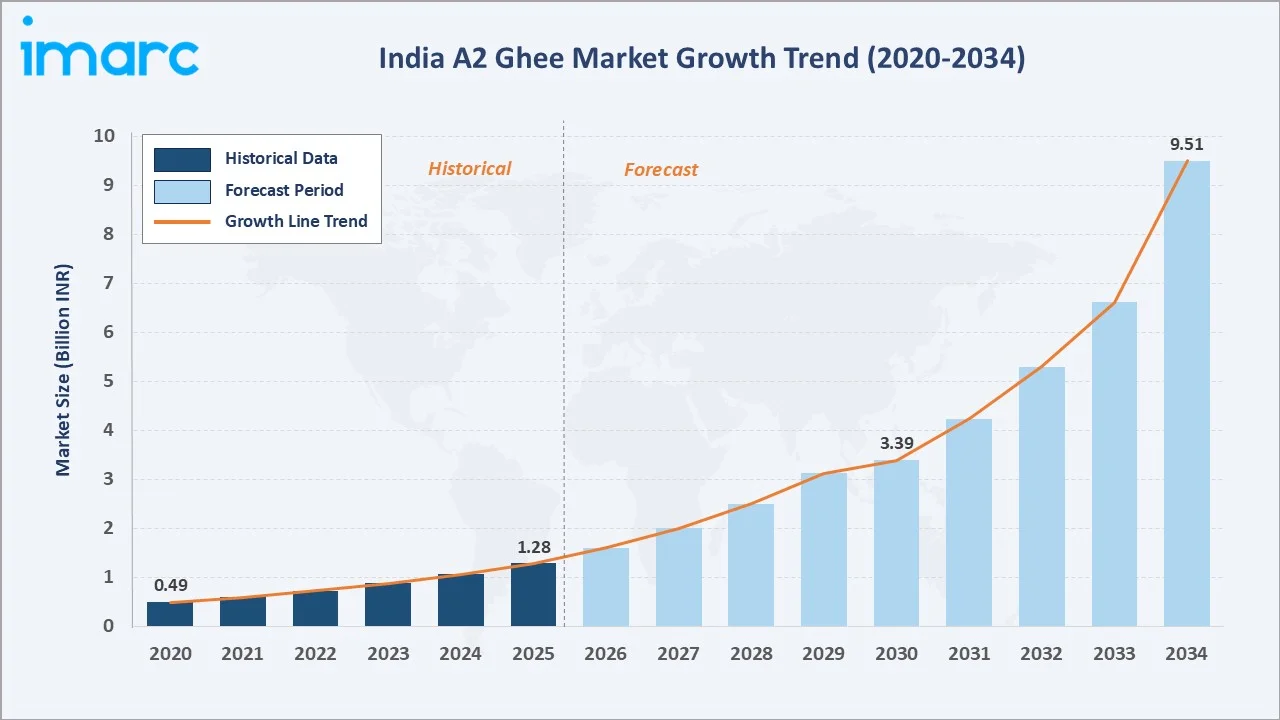

The India A2 ghee market size reached INR 1.28 Billion in 2025 and is projected to reach INR 9.51 Billion by 2034, exhibiting a CAGR of 21.41% during 2026-2034. Rising health consciousness, increasing demand for premium dairy products, and growing awareness of A2 beta-casein protein benefits are the primary growth drivers.

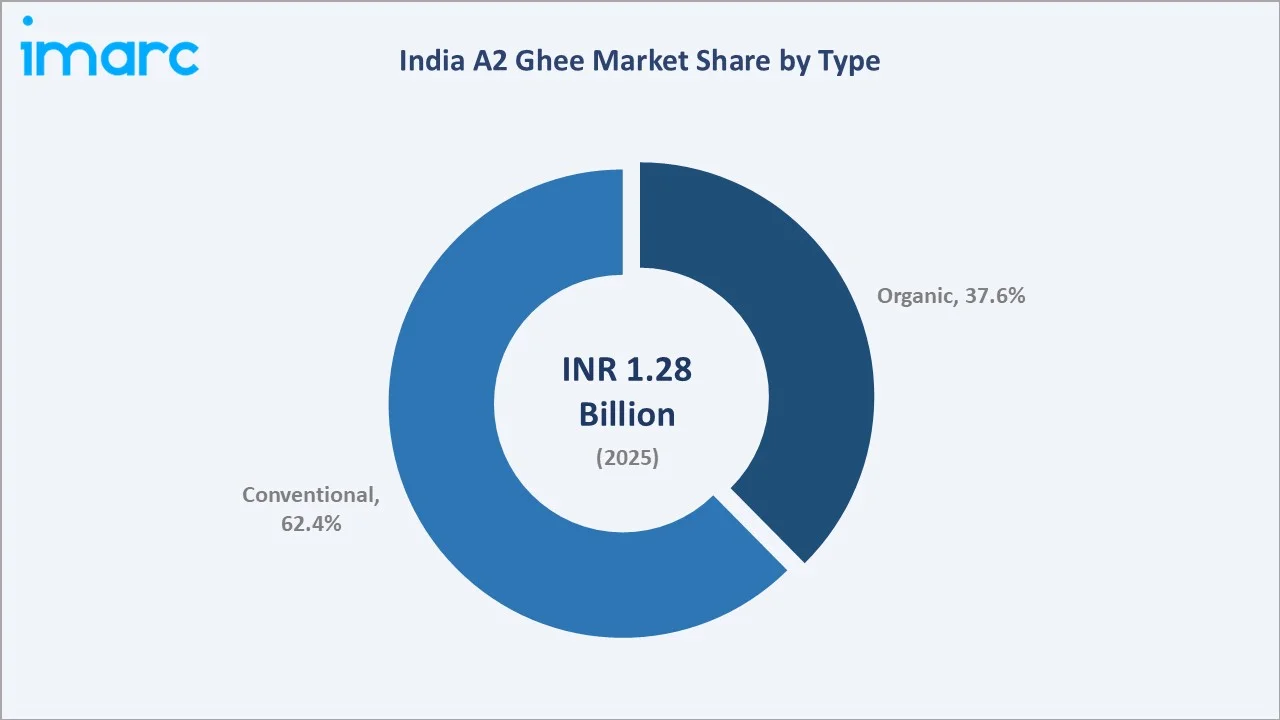

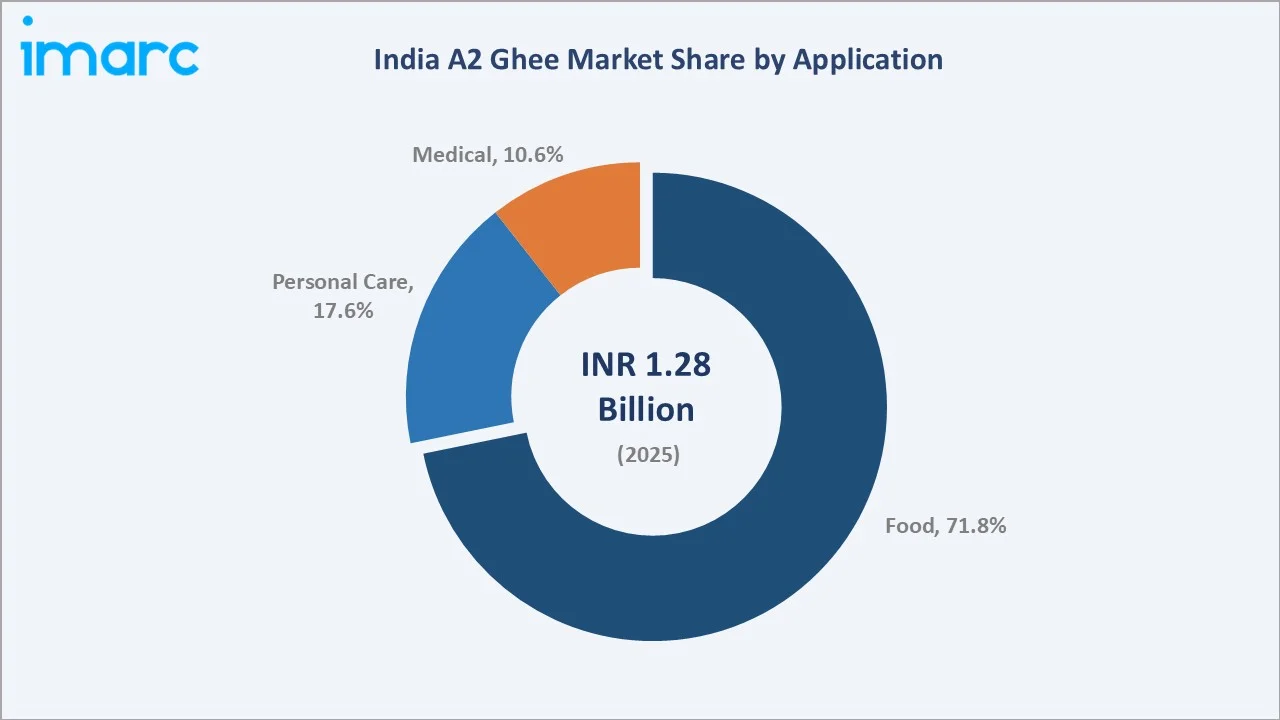

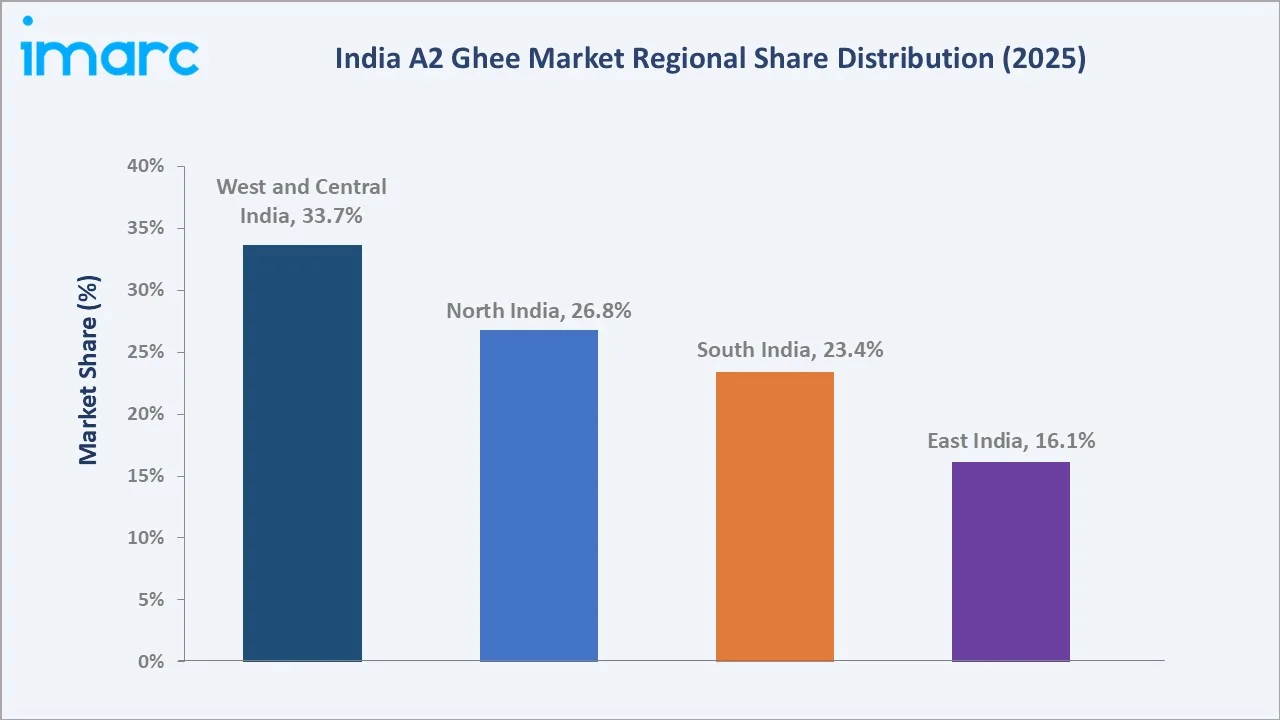

Conventional A2 ghee dominates the type segment at 62.4% in 2025, while the food application leads at 71.8%. West and Central India commands the largest regional share at 33.7% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 1.28 Billion |

|

Forecast Market Size (2034) |

INR 9.51 Billion |

|

CAGR (2026-2034) |

21.41% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West and Central India (33.7% share, 2025) |

|

Second Largest Region |

North India (26.8% share, 2025) |

|

Leading Type |

Conventional A2 Ghee (62.4%, 2025) |

|

Leading Application |

Food (71.8%, 2025) |

The India A2 ghee market growth trajectory from 2020 through 2034 reflects strong health-driven consumer demand. The historical expansion to INR 1.28 Billion in 2025 and forecast to INR 9.51 Billion captures accelerating premiumisation, e-commerce proliferation, and expanding applications across food, personal care, and medical uses.

To get more information on this market, Request Sample

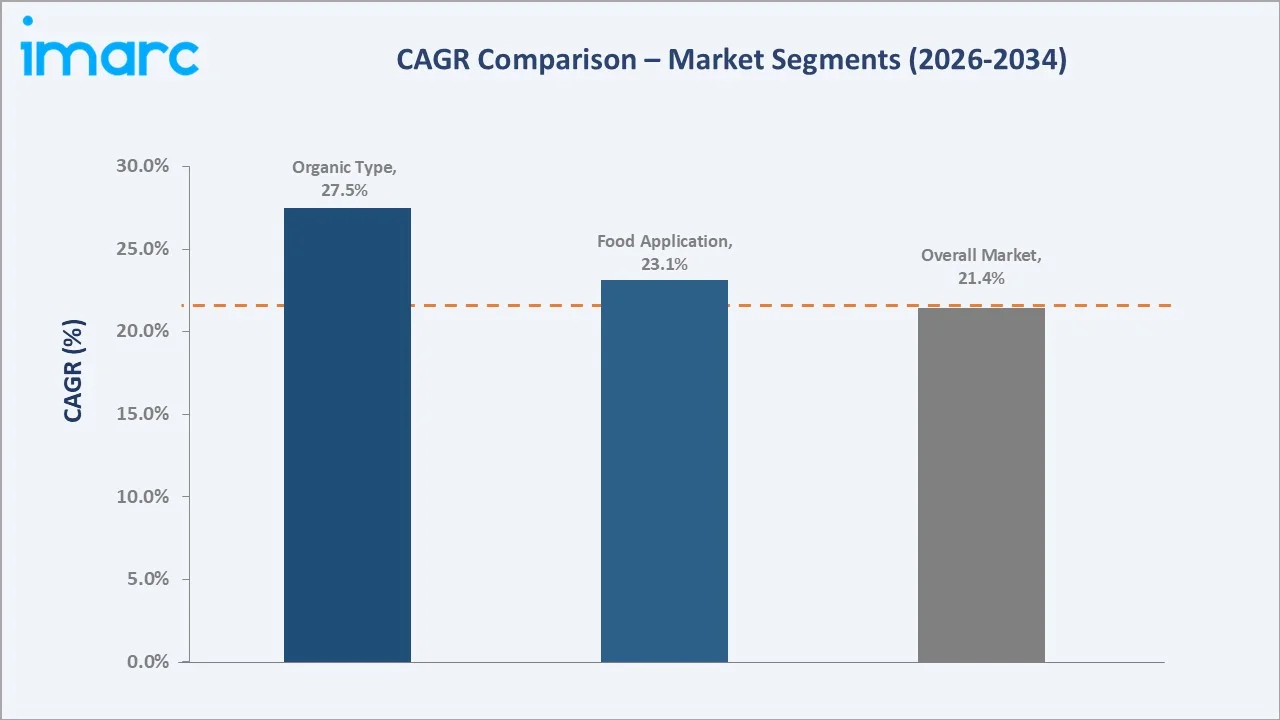

The CAGR trajectories across key type, application, and regional sub-segments, with organic A2 ghee growing at ~27.5% CAGR and food applications at ~23.1% CAGR, are the fastest-growing categories within the India A2 ghee market analysis through 2034.

Executive Summary

The India A2 ghee market is on a sustained high-growth trajectory from INR 1.28 Billion in 2025 to INR 9.51 Billion by 2034. A2 ghee, derived from the milk of indigenous desi cow breeds carrying the A2 beta-casein gene, commands a significant premium over regular ghee owing to its superior digestibility, richer nutrient profile, and Ayurvedic cultural significance.

Conventional A2 ghee dominates the type segment at 62.4% in 2025, benefiting from wider availability and established supply chains. Organic A2 ghee, representing 37.6%, grows faster at ~27.5% CAGR as certification-conscious premium consumers seek chemical-free, bilona-processed variants from farms with traceable indigenous cow breeds.

West and Central India dominates at 33.7% in 2025, driven by Maharashtra and Gujarat's large health-conscious urban consumer base and strong desi cow farming traditions. North India (26.8%) and South India (23.4%) follow, with East India (16.1%) emerging as a growth frontier through organised dairy expansion.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Conventional – 62.4% share (2025) |

|

Fastest Growing Type |

Organic – ~27.5% CAGR (2026-2034) |

|

Leading Application |

Food – 71.8% share (2025) |

|

Leading Region |

West and Central India – 33.7% share (2025) |

|

Top Companies |

Sid's Farm, GirOrganic, Akshayakalpa, Kapiva, Anveshan Farm Technologies Pvt. Ltd., Barosi |

Key Analytical Observations Supporting the Above Data:

- Conventional A2 Ghee: Conventional A2 ghee commands 62.4% in 2025 due to its cost accessibility relative to fully organic variants while still delivering the core A2 protein health benefits. It dominates in tier-2 and tier-3 urban centres and traditional household consumers.

- Food Application: Food application, with 71.8% in 2025, dominates because A2 ghee's high smoke point, rich aroma, and Ayurvedic endorsement make it the preferred cooking medium for health-conscious households, restaurants, and premium packaged food manufacturers.

- West & Central India: West and Central India's 33.7% dominance reflects the dense concentration of indigenous desi cow farms in Gujarat and Rajasthan, strong consumer awareness in Mumbai and Pune, and the region's leadership in organised dairy retail infrastructure.

- North India: North India, with 26.8% in 2025, benefits from deep cultural ties to ghee consumption in Ayurvedic traditions, large indigenous cow populations in Uttar Pradesh and Rajasthan, and expanding D2C premium health food brand penetration across Delhi-NCR.

India A2 Ghee Market Overview

A2 ghee is a premium clarified butter product prepared from the milk of indigenous Indian cattle breeds — including Gir, Sahiwal, Rathi, and Kankrej — that naturally produce only A2 beta-casein protein, in contrast to the A1 protein found in most crossbred and Holstein cows. The traditional bilona churning method, wherein curd is hand-churned to extract butter before clarification, preserves maximum nutritional integrity and is a key quality differentiator in the premium segment.

The India A2 ghee ecosystem integrates indigenous cow breeders and gaushala operators, smallholder and organic farm networks, processing and bilona-method artisan production units, premium branding and packaging companies, offline health stores and modern retail chains, D2C e-commerce platforms, and a growing export market serving Indian diaspora consumers globally.

Market Dynamics

To evaluate market opportunities, Request Sample

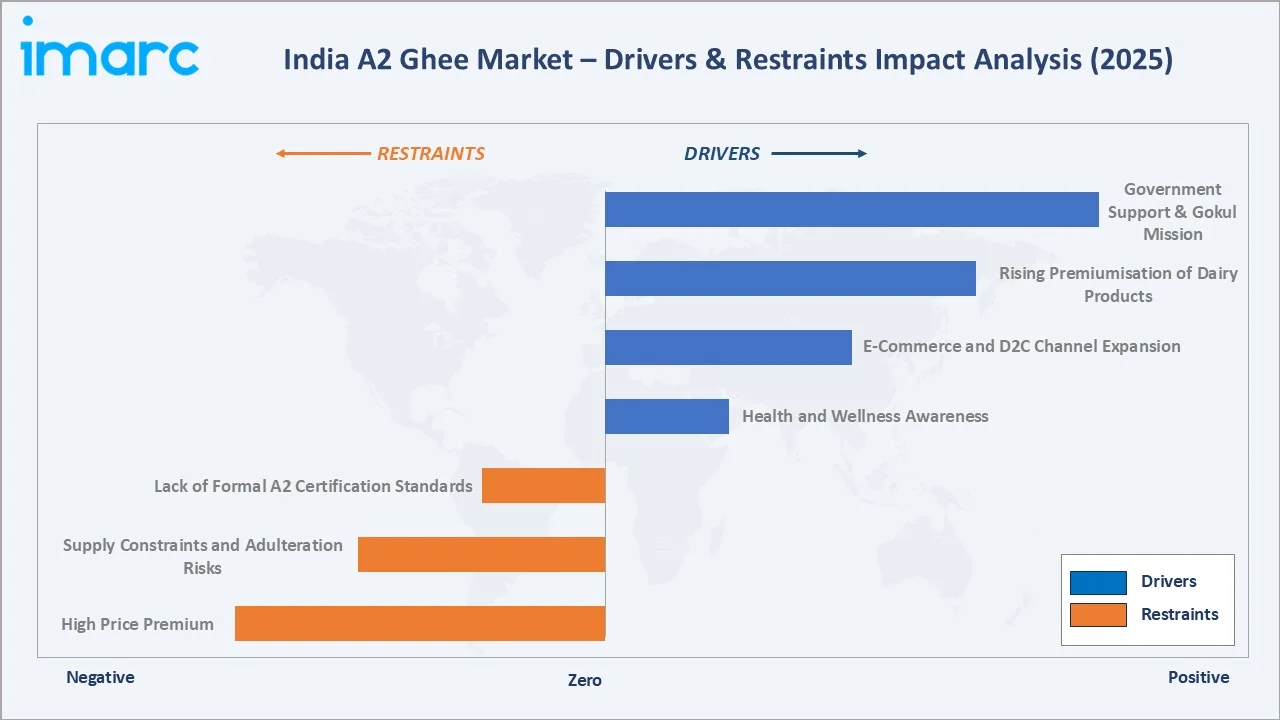

Market Drivers

- Health and Wellness Awareness: The surge in lifestyle diseases such as obesity, irritable bowel syndrome (IBS), and lactose intolerance is propelling consumers toward A2 ghee as a functional food. India's Ayurveda-based food culture aligns naturally with A2 ghee's documented digestive and immunity benefits, creating sustained non-discretionary consumer demand across urban and peri-urban markets.

- E-Commerce and D2C Channel Expansion: India's booming e-commerce and D2C food sector, has dramatically expanded A2 ghee's reach beyond metro markets into tier-2 and tier-3 cities, enabling direct brand-to-consumer premium pricing models with significantly higher net realisations.

- Rising Premiumisation of Dairy Products: Urbanisation, dual-income households, and rising disposable incomes have shifted dietary preferences toward premium, clean-label dairy products. A2 ghee commands 3–5x the price of regular ghee, and affordability barriers are progressively lowering among the growing affluent and upper-middle-class consumer segment.

Market Restraints

- High Price Premium: Higher-priced premium variants compared to conventional alternatives restrict widespread consumption, particularly in price-sensitive markets; as a result, mainstream products continue to dominate household usage, constraining the overall addressable market and slowing broader category penetration, while the category often remains confined to niche, health-conscious or affluent consumer segments, and limited affordability can also hinder repeat purchases and long-term volume growth.

- Supply Constraints and Adulteration Risks: The limited population of certified indigenous A2 cow breeds and long lead times to scale certified organic farm networks create significant supply constraints. Adulteration with regular ghee remains a persistent consumer trust challenge that undermines premium brand positioning in unorganised trade channels.

Market Opportunities

- Personal Care and Medical Applications: A2 ghee's documented anti-inflammatory and skin-nourishing properties are generating growing demand in premium personal care and Ayurvedic medical formulations, creating entirely new revenue streams for producers beyond traditional household food use.

- Export Market Development: Growing Indian diaspora populations in North America, Europe, the UAE, and Southeast Asia represent a substantial premium export opportunity. Indian A2 ghee brands are well-positioned for USD-denominated premium export revenue at significantly higher margins than comparable domestic pricing.

Market Challenges

- Regulatory Standardisation: The absence of standardised FSSAI certification specifically for A2 ghee, distinct from regular ghee, creates regulatory ambiguity. Brands struggle to make legally substantiated health claims, limiting the marketing effectiveness of scientifically documented A2 protein benefits to mainstream consumers.

- Cold Chain Infrastructure Gaps: Bilona-method A2 ghee production is labour-intensive and requires refrigerated supply chains from farm to consumer. Cold chain inadequacies in tier-2 and rural markets constrain organised brand expansion beyond metropolitan centres and restrict shelf-life management for smaller regional producers.

Emerging Market Trends

1. Direct-to-Consumer Digital Brand Building

Premium A2 ghee brands are leveraging Instagram, YouTube, and WhatsApp commerce to build direct consumer relationships, bypassing traditional distributor margins. Social media-driven awareness campaigns highlighting bilona craftsmanship and farm-to-fork traceability are driving premium brand loyalty and repeat subscription purchases.

2. Organic Certification and Traceability Technology

FSSAI organic certification, ECOCERT validation, and emerging blockchain-based milk traceability platforms are differentiating credible premium brands from uncertified operators. QR code-enabled farm story packaging is gaining significant consumer acceptance as a trust-building mechanism in the premium segment.

3. A2 Ghee in Functional and Nutraceutical Food Products

Leading FMCG and health supplement companies are incorporating A2 ghee into protein bars, Ayurvedic health drinks, and immunity-boosting formulations. This extends the A2 ghee ingredient economy well beyond traditional kitchen use into the high-growth functional food and nutraceutical segment.

4. Premium Packaging Innovation Driving Gifting Demand

Festival and corporate gifting of premium A2 ghee in artisan glass jars, copper containers, and handcrafted wooden boxes represents a fast-growing high-value segment. Gifting demand peaks during Diwali, Dussehra, and wedding seasons, creating significant seasonal revenue concentration for organised brands.

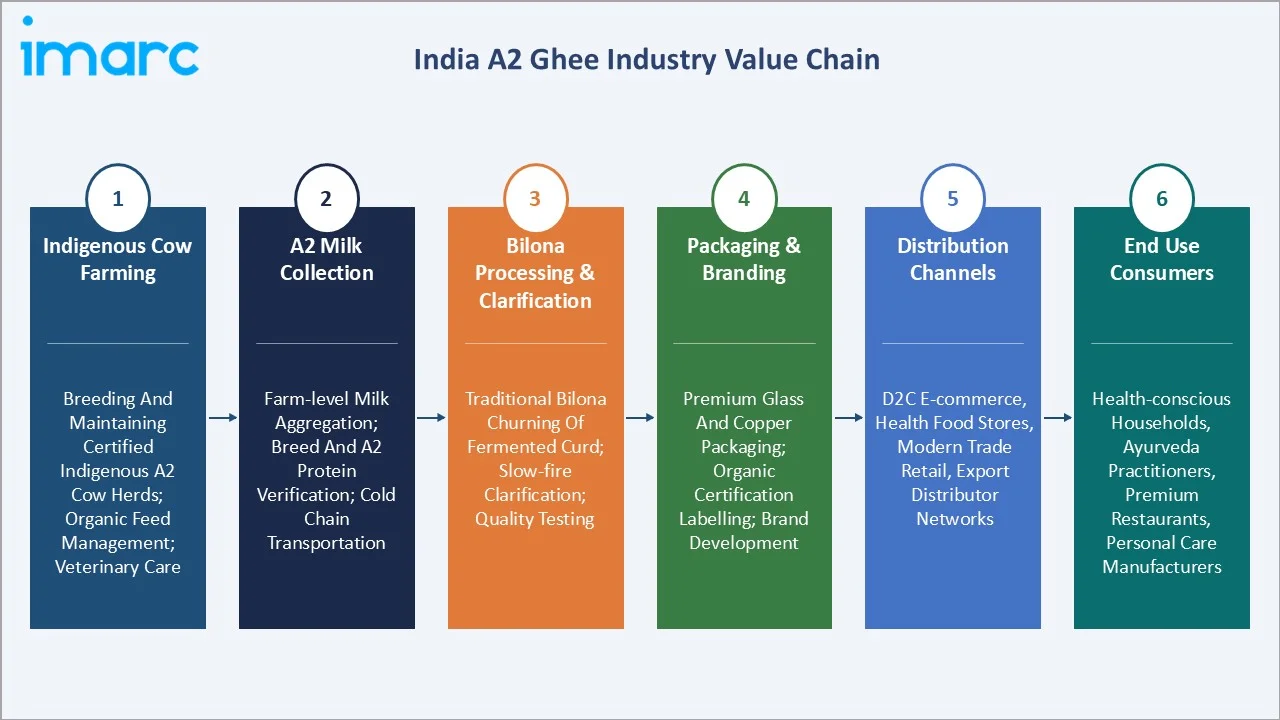

Industry Value Chain Analysis

The India A2 ghee value chain spans six core stages from indigenous cow breeding through end consumer delivery. Bilona processing and premium branding capture the highest value-add margins, while D2C digital platforms are disintermediating traditional distribution and enabling brands to capture 40–60% higher net realisations compared to retail wholesale channels.

|

Stage |

Key Activities |

|

Indigenous Cow Farming |

Breeding and maintaining certified indigenous A2 cow herds; organic feed management; veterinary care |

|

A2 Milk Collection |

Farm-level milk aggregation; breed and A2 protein verification; cold chain transportation |

|

Bilona Processing & Clarification |

Traditional bilona churning of fermented curd; slow-fire clarification; quality testing |

|

Packaging & Branding |

Premium glass and copper packaging; organic certification labelling; brand development |

|

Distribution Channels |

D2C e-commerce, health food stores, modern trade retail, export distributor networks |

|

End Use Consumers |

Health-conscious households, Ayurveda practitioners, premium restaurants, personal care manufacturers |

Technology Landscape in the India A2 Ghee Industry

Traditional Bilona Method and Modern Quality Control Integration

The bilona method, involving curd fermentation of A2 milk, pre-dawn hand-churning of curd to extract makkhan (butter), and slow clarification over wood or cow dung cake fire, preserves CLA, omega-3, fat-soluble vitamins, and probiotic-origin compounds that industrial cream-based ghee processing destroys. Modern brands supplement traditional methods with NABL-accredited laboratory testing for quality assurance and shelf-life validation.

Breed Verification and A2 Milk Authenticity Testing

DNA-based indigenous breed verification and A2 beta-casein protein ELISA testing are emerging technologies enabling brands to substantiate A2 authenticity claims with scientific evidence. These testing capabilities are increasingly demanded by institutional buyers and premium export market counterparties requiring documented provenance and A2 protein concentration certification.

Blockchain-Based Farm-to-Table Traceability

Early-adopter A2 ghee brands are deploying QR-code-linked blockchain platforms allowing consumers to trace their ghee batch back to the specific farm, cow breed, milking date, and bilona processing batch. This traceability infrastructure commands significant consumer trust premium and substantively reduces adulteration risk across the supply chain.

Cold Chain and Smart Packaging Technology

Advanced nitrogen-flushed glass jar sealing, UV-resistant amber glass packaging, and vacuum-sealed copper container technology are extending A2 ghee shelf life from 9–12 months to 18–24 months without preservatives. IoT-enabled cold chain monitoring systems are enabling organised brands to guarantee temperature-controlled delivery integrity from farm to doorstep across Tier-1 and Tier-2 city markets.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Conventional |

62.4% |

2025 |

|

Application |

Food |

71.8% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

West and Central India |

33.7% |

2025 |

By Type

Conventional A2 ghee commands a 62.4% majority share in 2025, reflecting its broader farm base, established supply chains through cooperatives and regional dairies, and pricing accessibility relative to fully certified organic variants. It is the default A2 ghee specification for mainstream health food buyers seeking the A2 protein benefit at a moderate price premium over regular ghee.

To access detailed market analysis, Request Sample

Organic A2 ghee at 37.6% in 2025, growing fastest at ~27.5% CAGR, is irreplaceable for the premium consumer segment that demands FSSAI-organic or international organic certification alongside the A2 protein guarantee. The certification premium commands significantly higher per-unit margins and superior export price realisations.

By Application

Food application dominates at 71.8% in 2025, driven by A2 ghee's use as a premium cooking medium, spread, and taste enhancer in traditional Indian cuisine. Its high smoke point of 250°C makes it superior to most cooking oils for high-temperature applications, and Ayurvedic dietary prescriptions reinforce consistent daily consumption among health-conscious households.

Personal care applications at 17.6% in 2025 include premium skin moisturisation, hair nourishment oils, Ayurvedic beauty formulations, and lip care products. Medical applications (10.6%) encompass Ayurvedic panchakarma treatments, wound healing preparations, and nutraceutical supplement formulations across registered Ayurvedic medicine manufacturers.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West and Central India |

33.7% |

Dense urban health-conscious consumer base; strong indigenous cow farming heritage; organised retail and D2C channel leadership |

|

North India |

26.8% |

Deep Ayurvedic cultural roots; large desi cow population; Delhi-NCR premium D2C platform adoption |

|

South India |

23.4% |

Established organic farming tradition; progressive organic dairy policy; strong Bangalore and Chennai premium food market |

|

East India |

16.1% |

Emerging urban health food market; growing e-commerce penetration; expanding branded dairy infrastructure in metros |

West and Central India's 33.7% market dominance in 2025 is driven by the highest urban health-consciousness in Maharashtra and Gujarat combined with the region's strong indigenous Gir and Kankrej cow farming heritage. Metropolitan consumers in Mumbai, Pune, and Ahmedabad drive premium A2 ghee D2C volumes significantly above national averages.

South India, with 23.4% in 2025, hosts a significant concentration of certified organic A2 ghee producers benefiting from Karnataka's progressive organic farming policies and Telangana's indigenous cow protection programmes. These supply-side growth catalysts are translating into premium brand expansion and national distribution reach.

Competitive Landscape

The India A2 ghee market is highly fragmented, with several hundred local, regional, and national brands competing across quality, organic certification, bilona authenticity, indigenous breed sourcing, and digital brand positioning. No single company holds more than 8–10% of total market revenue, with the top five players collectively accounting for approximately 30–35% of organised market share.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Sid's Farm |

Desi Cow Ghee |

Leader |

South India D2C leader; bilona method; digital brand excellence |

|

GirOrganic |

A2 Gir Cow Ghee |

Leader |

Gujarat-based organic farm; Gir cow sourcing; premium export |

|

Akshayakalpa |

Organic A2 Desi Cow Ghee |

Leader |

Karnataka organic model; certified supply chain; institutional |

|

Kapiva |

A2 Milk Cow Ghee |

Challenger |

Ayurvedic wellness brand; national distribution; functional food |

|

Anveshan Farm Technologies Pvt. Ltd. |

A2 Desi Cow Ghee |

Challenger |

Karnataka and TN indigenous breed focus; batch traceability; urban D2C |

|

Barosi |

Barosi A2 Desi Cow Ghee, Barosi A2 Buffalo Ghee |

Emerging |

North India; Sahiwal/Rathi/Kankrej breed sourcing; clean-label premium |

Key players include Sid's Farm, GirOrganic, Akshayakalpa, Kapiva, Anveshan Farm Technologies Pvt. Ltd., Barosi, and others.

Key Company Profiles

Sid's Farm

Sid's Farm is a leading premium A2 dairy brand headquartered in Hyderabad, Telangana. The company pioneered the direct-to-consumer A2 milk and ghee model in South India, maintaining a certified herd of indigenous desi cows and producing bilona-method A2 ghee with full farm-to-bottle traceability.

- Product Portfolio: Desi Cow Ghee

- Recent Developments: In January 2023, Sid’s Farm expanded its premium dairy portfolio with the launch of A2 Desi Cow Ghee, following strong consumer demand for its A2 milk products. The company aims to strengthen its presence in the premium dairy segment by offering high-quality, unadulterated ghee products through its direct-to-consumer model, while leveraging growing consumer awareness around health, purity, and natural dairy consumption to drive category expansion.

- Strategic Focus: Sid's Farm differentiates on complete supply chain transparency, NABL-certified quality testing, and tech-enabled D2C subscription models delivering farm-fresh A2 ghee with zero intermediary markup.

GirOrganic

GirOrganic is a certified organic farm and brand operating since 1990 from its 500+ acre ECOCERT-certified organic farm in Surat and Chotta Udaipur, Gujarat. Its Gir cow herd produces exclusively A2 milk for processing into organic-certified ghee following traditional bilona methods alongside modern quality control standards.

- Product Portfolio: A2 Gir Cow Ghee

- Strategic Focus: GirOrganic's strategy leverages its long-established organic farm heritage and ECOCERT certification to command the highest price-per-litre realisations in both domestic premium retail and export channels.

Akshayakalpa

Akshayakalpa is India's pioneering organic dairy brand headquartered in Bengaluru, Karnataka. Its unique model partners smallholder farmers across Karnataka, providing organic inputs, veterinary support, and guaranteed milk procurement to build a large certified organic A2 milk supply network at scale.

- Product Portfolio: Organic A2 Desi Cow Ghee

- Recent Developments: In April 2026, Akshayakalpa Organic expanded its footprint in western India with the launch of its organic dairy product range in Mumbai and Pune, strengthening its presence in the premium and health-focused dairy segment. The expansion includes products such as organic milk, curd, paneer, butter, ghee, and other products aimed at meeting the growing consumer demand for clean-label, chemical-free, and sustainably produced dairy products, while reinforcing the company’s focus on organic farming, traceability, and direct farm-to-consumer sourcing.

- Strategic Focus: Akshayakalpa's farmer-first model creates a defensible supply advantage, producing certified organic A2 ghee at scale while maintaining farm-level quality control that single-farm brands cannot replicate at comparable volumes.

Market Concentration Analysis

The India A2 ghee market is highly fragmented, with thousands of local artisan producers, regional dairy brands, and organised D2C players competing simultaneously. The organised premium segment (branded, certified, D2C-enabled) accounts for approximately 35–40% of total market value in 2025, with the remainder comprising unbranded local artisan producers and cooperative dairy ghee labelled as A2 without formal certification.

Consolidation in the organised segment is occurring through D2C platform acquisitions and fund-raised brand expansions. Private equity and venture capital interest is growing, with multiple leading brands having attracted institutional investment rounds. This funding enables national scale-up, decisively defeating smaller local players on brand trust and supply chain consistency.

Investment & Growth Opportunities

Fastest-Growing Segments

Organic A2 ghee at ~27.5% CAGR through 2034 is the highest-growth type segment, driven by premium export markets, FSSAI organic certification alignment, and the fastest-growing urban health-conscious consumer demographic. Personal care applications growing at ~19.8% CAGR represent a high-margin diversification opportunity for existing A2 ghee producers.

Emerging Markets

East India at an estimated ~20% CAGR through 2034 is the fastest-growing region, benefiting from rapidly rising urban health food consumption in Kolkata, Odisha, and West Bengal combined with a low organised market penetration base that creates substantial first-mover advantages for pan-India premium brands entering the region.

Venture & Investment Trends

India's agri-food tech investment ecosystem is channelling significant capital into vertically integrated A2 dairy platforms. The government's Rashtriya Gokul Mission (INR 3,400 Crore approved in March 2025) is expanding certified indigenous cow breed conservation and A2 milk supply infrastructure at scale, directly supporting market supply-side growth.

Future Market Outlook (2026-2034)

The India A2 ghee market is forecast to expand from INR 1.28 Billion in 2025 to INR 9.51 Billion by 2034 at a CAGR of 21.41%, adding INR 8.23 Billion in incremental annual market value over the forecast period. Three structural forces will shape the landscape: rising health premiumisation, digital retail transformation, and export market development.

Government support for indigenous cow conservation and organic farming, combined with FSSAI's evolving A2 dairy regulatory framework, will progressively formalise the market and create clearer brand differentiation for certified players. Export market development targeting the Indian diaspora and premium global health food channels will generate INR-USD arbitrage revenue at 2–4x domestic price realisations for certified organic brands.

Research Methodology

Primary Research

Primary research encompassed structured interviews with India A2 ghee brand founders, organic farm operators, FSSAI regulatory specialists, Ayurvedic practitioners, premium health food retail buyers, and e-commerce platform category managers. Primary data validated market sizing, segmentation shares, and competitive landscape positioning across all major segments and regions.

Secondary Research

Key secondary sources include FSSAI dairy product regulations, National Dairy Development Board (NDDB) annual reports, Rashtriya Gokul Mission scheme documents, APEDA export data, Indian Council of Agricultural Research publications on indigenous cow breeds, premium health food e-commerce platform market data, and trade publications covering the Indian premium dairy sector.

Forecasting Models

Market size estimations and forecasts were derived using bottom-up analysis of organised brand revenues, e-commerce platform sales data, farm-level production estimates, and top-down GDP and health food expenditure growth models. Scenario analysis accounted for regulatory evolution timelines, organic certification scale-up, and export market development trajectories.

India A2 Ghee Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion INR |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Organic, Conventional |

| Applications Covered | Food, Personal Care, Medical |

| Distribution Channels Covered | Online, Offline |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | Sid's Farm, GirOrganic, Akshayakalpa, Kapiva, Anveshan Farm Technologies Pvt. Ltd., Barosi, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India A2 ghee market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India A2 ghee market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India A2 ghee industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India A2 Ghee Market Report

The India A2 ghee market reached INR 1.28 Billion in 2025, reflecting strong demand from health-conscious urban consumers seeking premium indigenous dairy products with documented nutritional advantages over regular ghee.

The market is projected to reach INR 9.51 Billion by 2034, growing at a CAGR of 21.41% during 2026-2034, driven by rising health premiumisation, e-commerce expansion, and growing personal care and medical applications.

Conventional A2 ghee leads with a 62.4% type share in 2025, valued for its broader availability and moderate price premium, serving mainstream health-conscious households across India seeking A2 protein benefits.

Food application dominates at 71.8% in 2025, reflecting A2 ghee's role as a premium cooking medium, spread, and dietary supplement across traditional Indian households, premium restaurants, and health food manufacturers.

West and Central India commands 33.7% market share in 2025, driven by Maharashtra and Gujarat's dense health-conscious urban consumer base and strong indigenous Gir cow farming heritage across the region.

Organic A2 ghee is the fastest-growing type at ~27.5% CAGR through 2034, driven by certification-conscious premium consumers and expanding export demand from international health food and Indian diaspora markets.

Leading companies include Sid's Farm, GirOrganic, Akshayakalpa, Kapiva, Anveshan Farm Technologies Pvt. Ltd., Barosi, and others.

West and Central India hosts India's largest indigenous Gir cow populations in Gujarat and Rajasthan, and its metropolitan consumers in Mumbai, Pune, and Ahmedabad demonstrate the highest premium dairy spend per capita nationally, creating both supply and demand advantages.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)