India Active Pharmaceutical Ingredients Market Size, Share, Trends and Forecast by Drug Type, Manufacturer Type, Synthesis Type, Therapeutic Application, and Region, 2026-2034

India Active Pharmaceutical Ingredients Market Size, Share, Trends & Forecast (2026-2034)

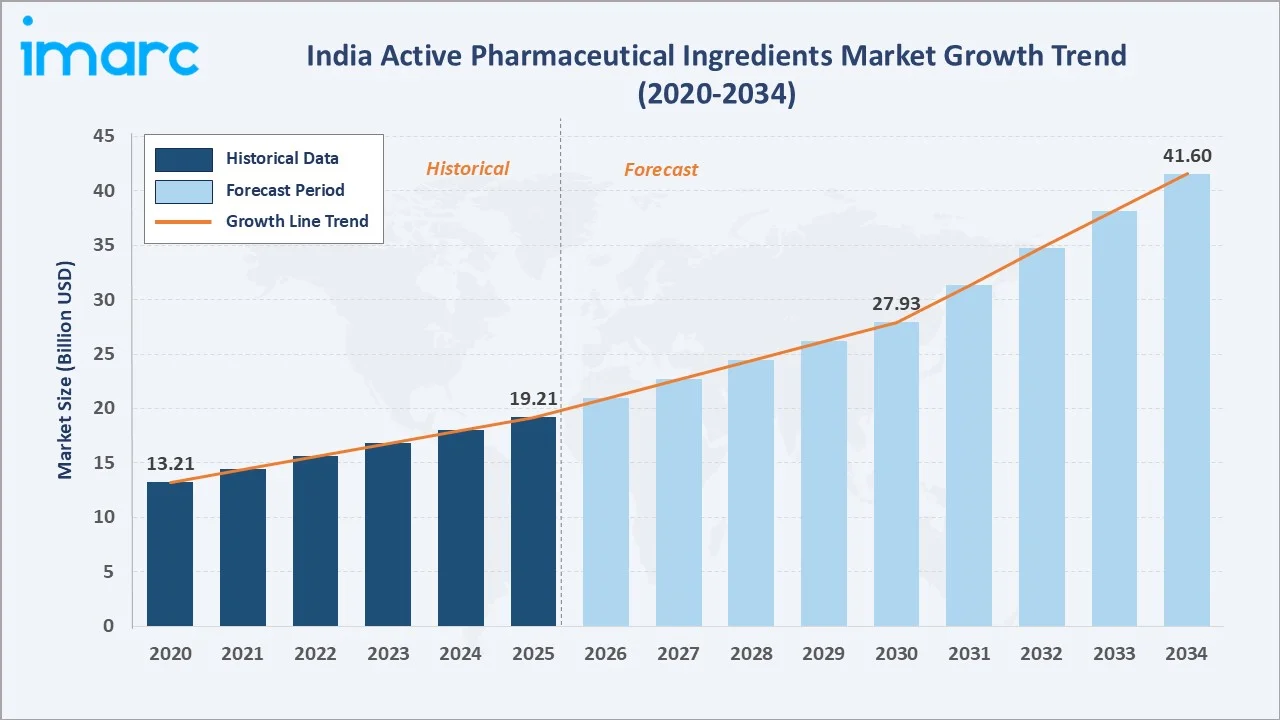

The India active pharmaceutical ingredients market reached USD 19.21 Billion in 2025 and is projected to reach USD 41.60 Billion by 2034, growing at a CAGR of 7.78% during 2026-2034. The market is driven by PLI scheme incentives, rising chronic disease burden, patent expirations, biosimilar expansion, and export growth.

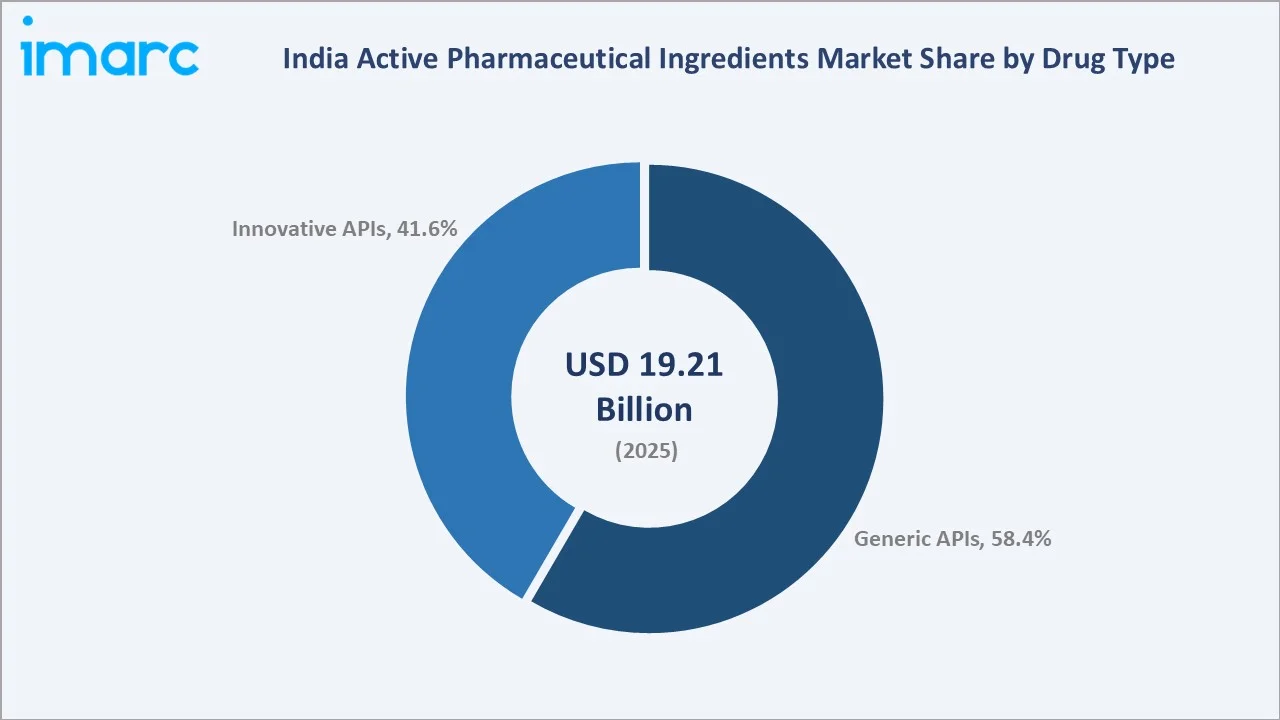

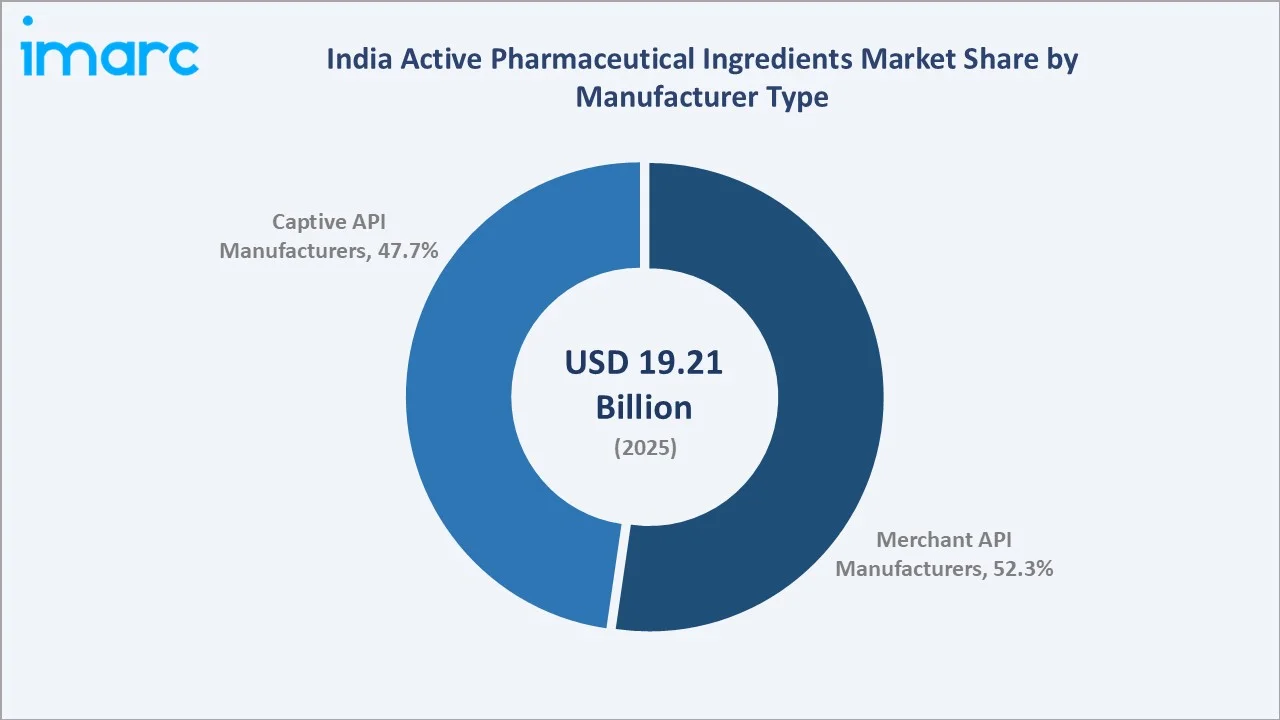

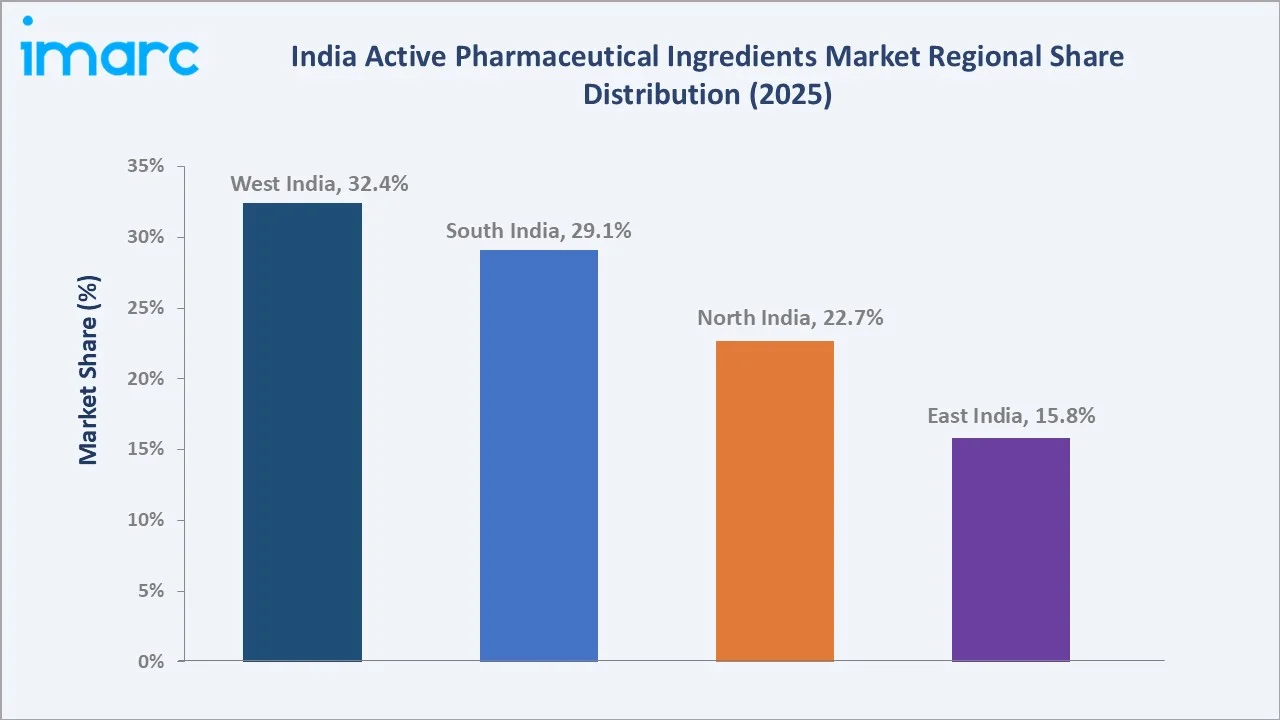

Generic APIs lead at 58.4%. Merchant manufacturers dominate at 52.3%. West India commands 32.4% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 19.21 Billion |

|

Forecast Market Size (2034) |

USD 41.60 Billion |

|

CAGR (2026-2034) |

7.78% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Drug Type |

Generic APIs (58.4%, 2025) |

|

Dominant Manufacturer Type |

Merchant API Manufacturers (52.3%, 2025) |

|

Leading Region |

West India (32.4%, 2025) |

The market expanded from USD 13.21 Billion in 2020 to USD 19.21 Billion in 2025, anchored at USD 27.93 Billion in 2030 and forecast to reach USD 41.60 Billion by 2034. Government PLI initiatives and China+1 sourcing diversification by global pharma companies have significantly accelerated India's API manufacturing capacity expansion across this period.

To get more information on this market, Request Sample

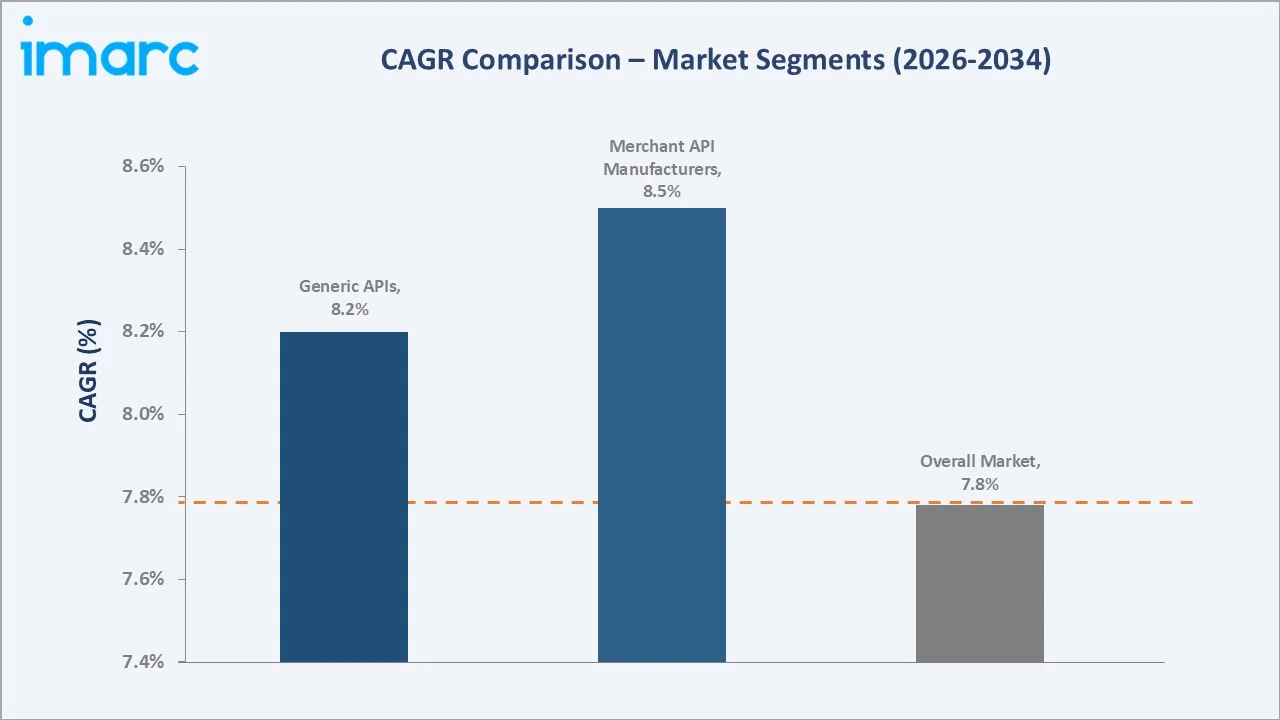

Generic APIs grow at ~8.2% CAGR, underpinned by global demand for affordable medicines and patent cliff opportunities. Merchant API manufacturers grow at ~8.5% CAGR, driven by outsourcing trends and CDMO capacity expansion.

Executive Summary

The India active pharmaceutical ingredients market reached USD 19.21 Billion in 2025, representing one of the world's most strategically significant pharmaceutical manufacturing sectors. The market is projected to reach USD 41.60 Billion by 2034 at a 7.78% CAGR.

Generic APIs at 58.4% dominate through established cost-competitive manufacturing. Merchant API manufacturers at 52.3% reflect the growing outsourcing and CDMO trend. West India at 32.4% leads through Mumbai and Ahmedabad's pharmaceutical clusters.

Key Market Insights

|

Insight |

Data |

|

Dominant Drug Type |

Generic APIs – 58.4% share (2025) |

|

Dominant Manufacturer Type |

Merchant API Manufacturers – 52.3% market share (2025) |

|

Leading Region |

West India – 32.4% market share (2025) |

|

Market Opportunity |

Biosimilars, HPAPI, oncology APIs, contract manufacturing, China+1 diversification |

Key Analytical Observations Supporting the Above Data:

- Generic APIs at 58.4%: India's strength in reverse engineering and process chemistry enables cost-effective production of off-patent APIs, commanding the dominant share and driving global generic drug supply chains.

- Merchant API Manufacturers at 52.3%: Third-party API suppliers benefit from global pharma outsourcing, contract manufacturing agreements, and CDMO investments, capturing most of the India's API market.

- West India at 32.4%: Maharashtra and Gujarat's pharmaceutical clusters, anchored in Ahmedabad, Mumbai, and Vadodara, host India's highest concentration of API manufacturing facilities and export infrastructure.

India Active Pharmaceutical Ingredients Market Overview

The India API market encompasses the development, manufacture, and supply of biologically active pharmaceutical compounds used in drug formulations across generic and innovative categories, serving domestic formulation and global export demand.

The ecosystem integrates raw material and KSM suppliers, API manufacturers, CDMO service providers, regulatory bodies (CDSCO, USFDA, EMA), and formulation companies. Macroeconomic drivers include India's chemistry talent pool, cost advantages, regulatory compliance improvements, and government self-reliance initiatives.

Market Dynamics

To evaluate market opportunities, Request Sample

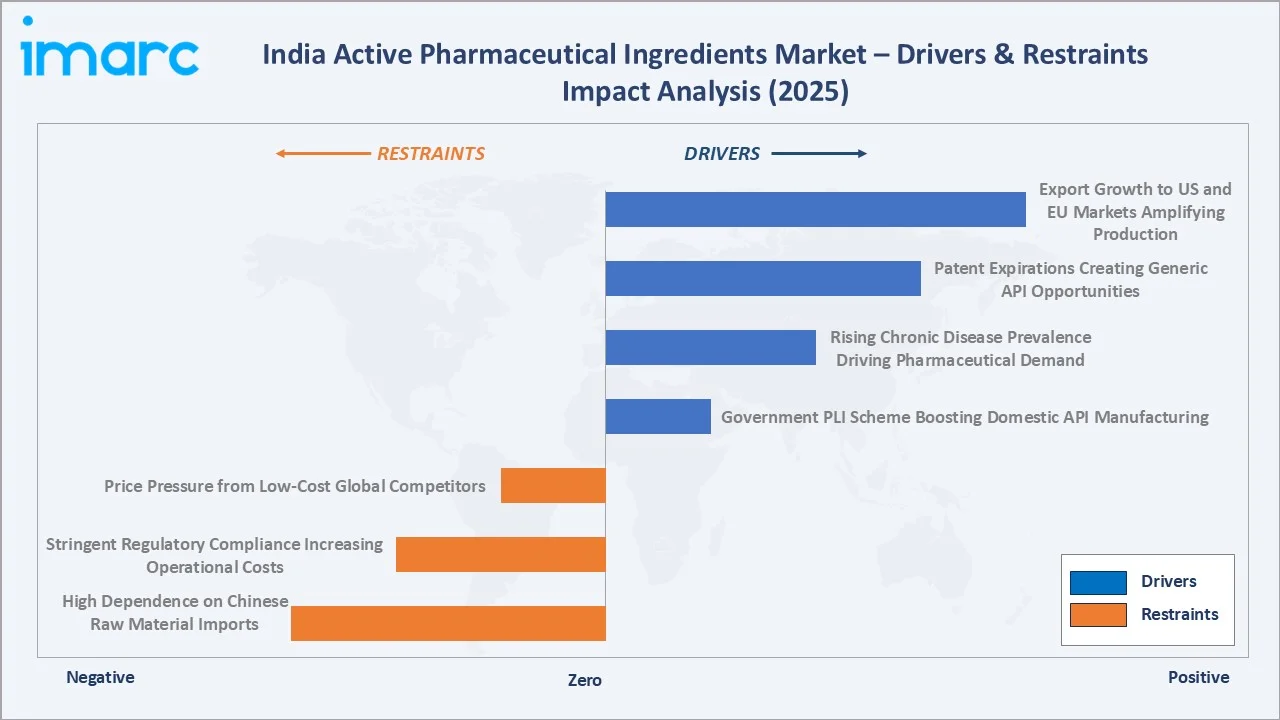

Market Drivers

- Government PLI Scheme Boosting Domestic API Manufacturing: India's Production Linked Incentive scheme, with an allocation of INR 6,940 crore, incentivises domestic production of 41 critical APIs, intermediates, and key starting materials. This policy directly reduces import dependency on China and builds a resilient domestic supply chain.

- Rising Chronic Disease Prevalence Driving Pharmaceutical Demand: India's growing burden of cardiovascular disease, diabetes, oncology, and neurological disorders directly drives demand for APIs targeting these therapeutic areas. With NCDs projected to contribute approximately 75% of India's disease burden by 2030, pharmaceutical manufacturers are expanding API production capacity across critical therapeutic segments.

- Patent Expirations Creating Generic API Opportunities: A significant wave of patent expirations on blockbuster drugs through 2030 is creating substantial market opportunities for Indian generic API manufacturers. India's established capabilities in reverse engineering and process chemistry position it as the primary global beneficiary of the genericisation of major therapeutic molecules.

- Export Growth to US and EU Markets Amplifying Production: India exports approximately 50% of its API production to regulated markets including the US and EU, driven by USFDA and EMA-compliant manufacturing capabilities. Growing global demand for affordable medicines continues to expand Indian API export volumes and manufacturing revenues.

Market Restraints

- High Dependence on Chinese Raw Material Imports: India imports approximately 68% of its key starting materials and chemical intermediates from China, creating supply chain vulnerability. Geopolitical tensions, logistics disruptions, and price volatility in Chinese chemical markets directly impact India's API production costs and supply reliability.

- Stringent Regulatory Compliance Increasing Operational Costs: Meeting USFDA, EMA, and WHO-GMP compliance requirements demands significant capital investment in quality systems, environmental controls, and data integrity infrastructure. Regulatory inspections and import alerts at Indian API facilities have imposed operational disruptions and remediation costs.

- Price Pressure from Low-Cost Global Competitors: Chinese API manufacturers, benefiting from government subsidies and integrated chemical supply chains, exert persistent pricing pressure on Indian API exporters in commodity generic molecules. This competition constrains pricing power and profitability, pushing Indian companies toward complex APIs and biosimilars.

Market Opportunities

- High-Potency API and Oncology Segment Expansion: Growing global demand for oncology treatments is creating significant opportunities in high-potency active pharmaceutical ingredients. India's emerging HPAPI manufacturing capabilities, supported by dedicated containment facilities, position domestic manufacturers to capture premium-priced segments in anti-cancer therapies.

- Biosimilars and Biopharmaceutical API Growth: India's biosimilar regulatory pathway and established biotech manufacturing base create a significant opportunity in biopharmaceutical APIs. With global biologics patent expiries accelerating through 2030, Indian CDMO players are well positioned to supply biosimilar APIs to both domestic and global markets.

Market Challenges

- Infrastructure Gaps in Tier-2 Pharmaceutical Clusters: Emerging pharmaceutical clusters in East India face infrastructure limitations including inadequate utility supply, logistics connectivity, and effluent treatment capacity. These gaps constrain geographic expansion of API manufacturing outside established hubs in West and South India.

- Environmental Compliance and Effluent Management Costs: API manufacturing generates significant chemical waste streams requiring sophisticated effluent treatment systems. Tightening enforcement of pollution norms has increased compliance costs and forced temporary shutdowns at several API manufacturing clusters.

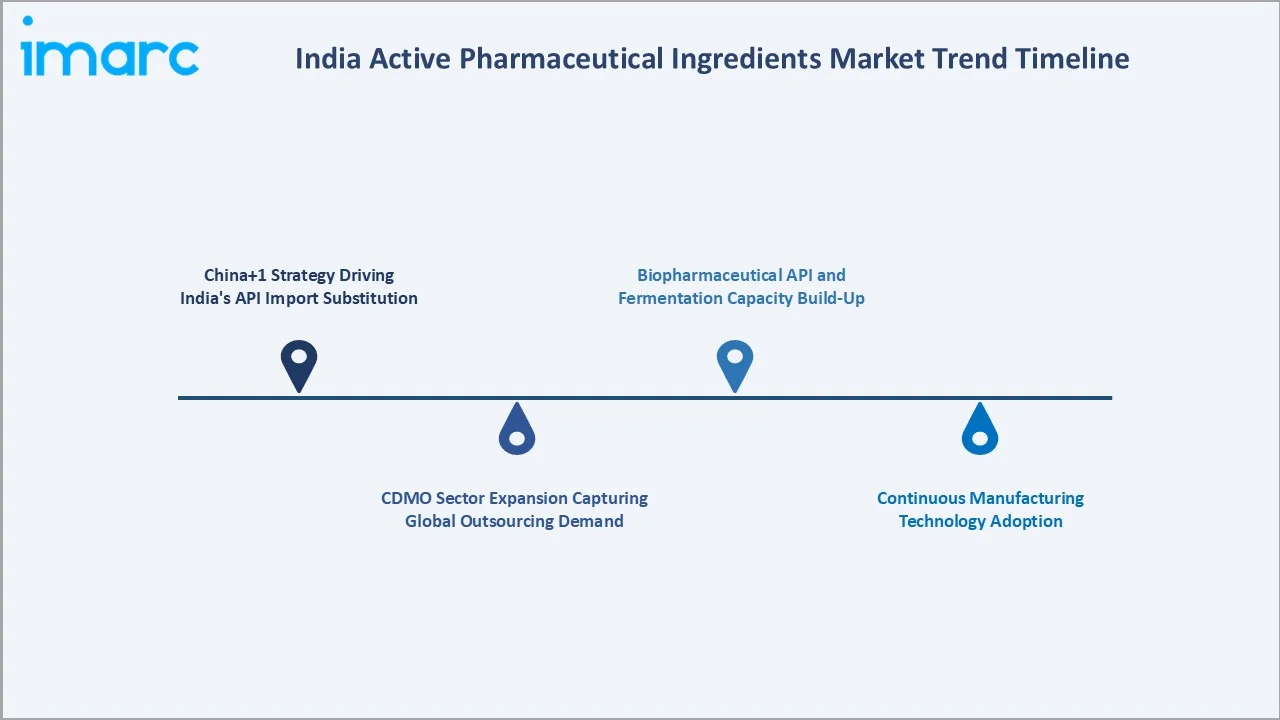

Emerging Market Trends

1. China+1 Strategy Driving India's API Import Substitution

Global pharmaceutical companies are actively diversifying API sourcing away from China to mitigate supply chain concentration risk. India's established chemistry manufacturing base, USFDA-compliant facilities, and government PLI incentives position it as the primary China+1 alternative, attracting long-term API supply agreements from European and North American pharma majors.

2. CDMO Sector Expansion Capturing Global Outsourcing Demand

India's contract development and manufacturing organisation sector is experiencing rapid growth as global pharmaceutical innovators outsource API development and manufacturing to cost-competitive Indian partners. Investment in state-of-the-art synthesis capabilities and analytical services is expanding the value-added service proposition of Indian CDMOs.

3. Continuous Manufacturing Technology Adoption

Indian API manufacturers are investing in continuous flow chemistry and process intensification technologies to improve production efficiency and lower manufacturing costs. Continuous manufacturing enables more consistent API quality, reduced solvent consumption, and faster cycle times, improving competitiveness in both generic and complex specialty API segments.

4. Biopharmaceutical API and Fermentation Capacity Build-Up

India's biosimilar market leadership is driving investment in large-scale biopharmaceutical API manufacturing infrastructure. Expansion of cell culture bioreactor capacity, fermentation facilities, and downstream purification capabilities positions Indian manufacturers to supply both domestic biosimilar formulations and export biopharmaceutical APIs to regulated global markets.

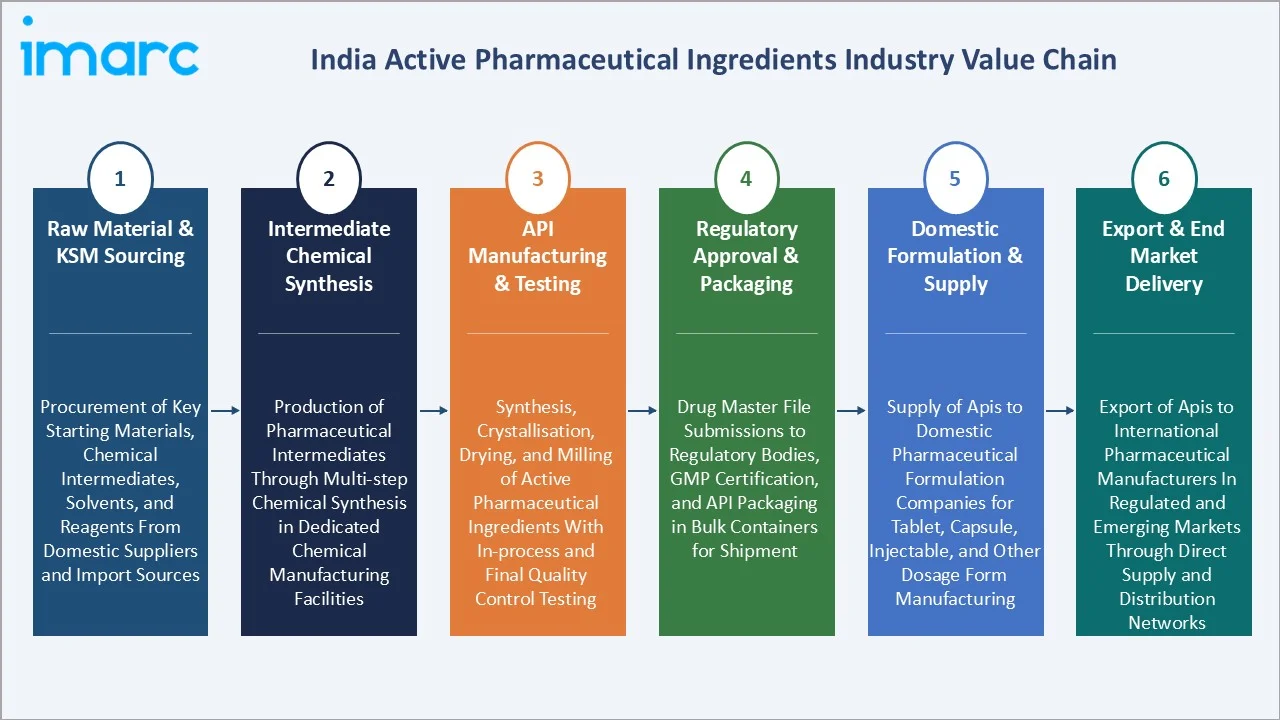

Industry Value Chain Analysis

The India API value chain integrates upstream raw material and KSM sourcing, intermediate chemical synthesis, API manufacturing and quality testing, regulatory approval processes, domestic formulation supply, and global export. The chain's strategic bottleneck remains upstream KSM and intermediate import dependency on China.

|

Stage |

Key Participants |

|

Raw Material & KSM Sourcing |

Procurement of key starting materials, chemical intermediates, solvents, and reagents from domestic suppliers and import sources |

|

Intermediate Chemical Synthesis |

Production of pharmaceutical intermediates through multi-step chemical synthesis in dedicated chemical manufacturing facilities |

|

API Manufacturing & Testing |

Synthesis, crystallisation, drying, and milling of active pharmaceutical ingredients with in-process and final quality control testing |

|

Regulatory Approval & Packaging |

Drug master file submissions to regulatory bodies, GMP certification, and API packaging in bulk containers for shipment |

|

Domestic Formulation & Supply |

Supply of APIs to domestic pharmaceutical formulation companies for tablet, capsule, injectable, and other dosage form manufacturing |

|

Export & End Market Delivery |

Export of APIs to international pharmaceutical manufacturers in regulated and emerging markets through direct supply and distribution networks |

The API manufacturing stage holds the highest value in the chain, requiring sophisticated chemistry capabilities, regulatory compliance, and analytical infrastructure. The export stage is the key revenue multiplier, with regulated market exports commanding significant price premiums over domestic supply.

Technology Landscape in the India API Industry

Continuous Flow Chemistry Technology

Continuous flow chemistry replaces traditional batch synthesis with a steady, controlled reaction process, enabling higher yield, reduced waste, and improved safety for hazardous reactions. Its adoption in Indian API manufacturing improves process consistency, scalability, and regulatory compliance while significantly reducing API production cycle times and solvent consumption.

High-Potency API Containment Technology

High-potency API manufacturing requires specialised containment engineering controls including isolators, closed transfer systems, and continuous air monitoring to protect operators from potent compounds. India's investment in HPAPI containment technology is enabling entry into premium oncology, hormone, and immunosuppressant API segments with superior margin profiles.

Biopharmaceutical Upstream Processing Technology

Mammalian cell culture, microbial fermentation, and yeast expression systems are the primary upstream technologies for biopharmaceutical API production. Indian companies are investing in single-use bioreactor technology and perfusion culture processes to enhance biosimilar API production efficiency and improve the flexibility of biopharmaceutical manufacturing operations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Drug Type |

Generic Active Pharmaceutical Ingredients |

58.4% |

2025 |

|

Manufacturer Type |

Merchant API Manufacturers |

52.3% |

2025 |

|

Synthesis Type |

Synthetic Active Pharmaceutical Ingredients |

62.5% |

2025 |

|

Therapeutic Application |

Cardiovascular and Respiratory |

24.6% |

2025 |

|

Region |

West India |

32.4% |

2025 |

By Drug Type

The Generic APIs segment leads at 58.4% in 2025, reflecting India's core competency as the world's leading generic pharmaceutical supplier. Generic API manufacturers benefit from established process chemistry capabilities, regulatory compliance track records, and cost-efficient large-scale production infrastructure.

To access detailed market analysis, Request Sample

Innovative APIs at 41.6% capture high-value patented drug API supply, biotech API production for innovator companies, and early-phase CDMO services. This segment grows at ~6.9% CAGR as Indian CDMOs secure more innovator API development contracts and biosimilar API manufacturing relationships with global pharmaceutical companies.

By Manufacturer Type

Merchant API Manufacturers lead at 52.3% in 2025, supplying APIs to third-party pharmaceutical formulation companies in domestic and export markets. Merchant manufacturers benefit from economies of scale, specialisation in specific API categories, and growing CDMO service integration.

Captive API Manufacturers at 47.7% produce APIs exclusively for internal formulation use within vertically integrated pharmaceutical companies. This segment supports supply security and quality control advantages for large Indian pharma groups maintaining backward integration in their most critical API supply chains.

Regional Market Insights

|

Region |

Share (2025) |

Key API Market Drivers & Characteristics |

|

West India |

32.4% |

Driven by Maharashtra and Gujarat pharmaceutical clusters, bulk drug manufacturing, port-based export infrastructure, and a high concentration of API manufacturing facilities |

|

South India |

29.1% |

Driven by Hyderabad's API manufacturing hubs, Telangana's pharma city clusters, Andhra Pradesh's bulk drug park, and strong CDMO and biotech API presence |

|

North India |

22.7% |

Driven by pharmaceutical industrial areas in Himachal Pradesh and Uttarakhand, tax-incentive manufacturing zones, and pharmaceutical distribution infrastructure in Delhi NCR |

|

East India |

15.8% |

Emerging with government-supported pharmaceutical clusters, growing manufacturing investment, and expanding API production to serve domestic market demand |

West India at 32.4% leads through Gujarat's and Maharashtra's established bulk drug and chemical manufacturing ecosystems, benefiting from port access, chemical infrastructure, and decades of API production expertise in antibiotic, cardiovascular, and anti-infective molecule categories.

South India at 29.1% reflects Hyderabad's position as India's pharmaceutical capital, hosting major API exporters and CDMO operators. North India at 22.7% benefits from tax-incentive manufacturing zones, while East India at 15.8% represents the fastest-growing region, supported by new bulk drug parks and PLI scheme investments.

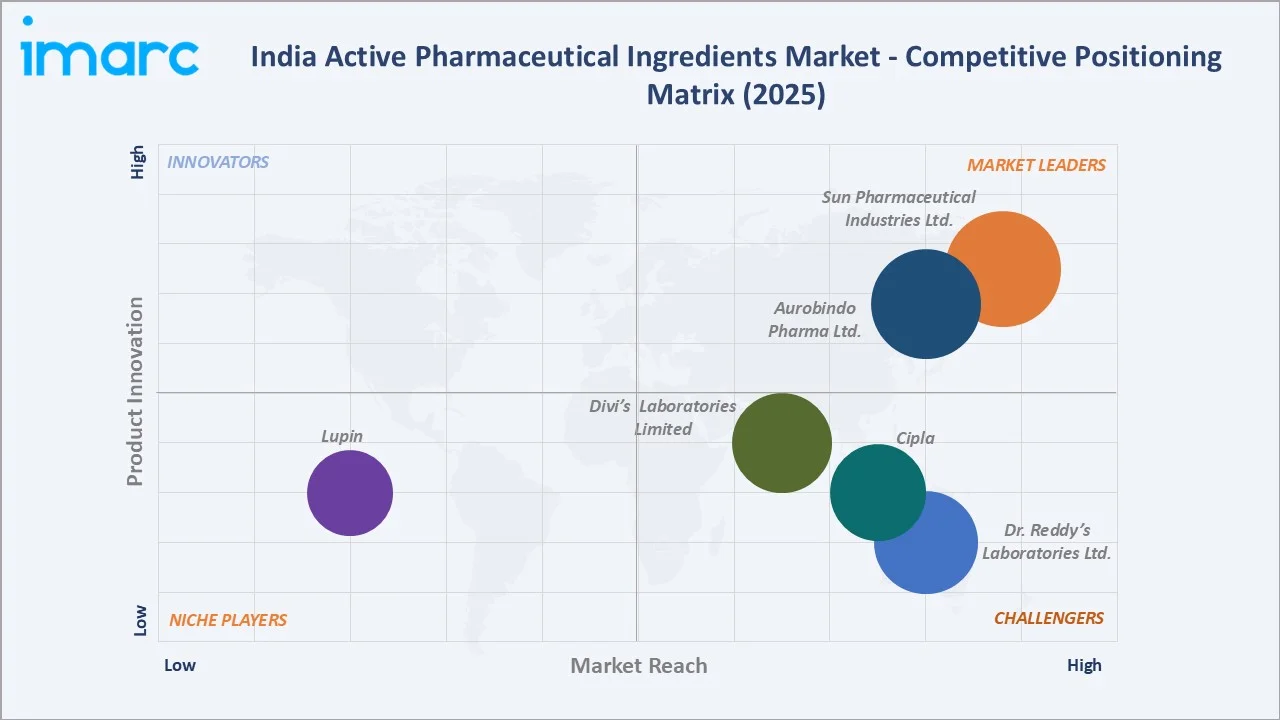

Competitive Landscape

The India API market is moderately concentrated, with major integrated pharmaceutical companies competing alongside specialised API manufacturers and CDMO providers. Competition is driven by regulatory compliance credentials, API portfolio breadth, cost efficiency, and manufacturing capacity scale.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Sun Pharmaceutical Industries Ltd. |

Generic APIs, Specialty APIs, Oncology APIs |

Market Leader |

India's largest pharma company with integrated API manufacturing across generic and specialty segments globally |

|

Aurobindo Pharma Limited |

Antibiotic APIs, Antiviral APIs, ARV APIs |

Market Leader |

One of India's largest API manufacturers with a wide therapeutic API portfolio and strong USFDA compliance |

|

Dr. Reddy's Laboratories Ltd. |

Generic APIs, Active Ingredients for NCEs |

Strong Challenger |

Vertically integrated API manufacturer with strong chemistry capabilities and global regulated market presence |

|

Divi's Laboratories Limited |

Custom Synthesis APIs, Nutraceuticals, Generic APIs |

Strong Challenger |

India's leading API CDMO with deep process chemistry expertise and strong relationships with global innovator pharmaceutical companies |

|

Cipla |

Generic APIs, Respiratory APIs, Oncology APIs |

Strong Challenger |

Strong generic API portfolio across respiratory, oncology, and anti-infective therapeutic areas with significant export reach |

|

Lupin |

Generic APIs, Cardiovascular APIs, CNS APIs |

Niche Player |

Strong generic API portfolio with cardiovascular and CNS focus, supported by significant backward integration and export compliance |

Key players include Sun Pharmaceutical Industries Ltd., Aurobindo Pharma Limited, Dr. Reddy's Laboratories Ltd., Divi's Laboratories Limited, Cipla, Lupin, and others.

Key Company Profiles

Sun Pharmaceutical Industries Ltd.

Sun Pharmaceutical Industries Ltd. is India's largest pharmaceutical company and one of the world's leading generic pharmaceutical manufacturers, with integrated API manufacturing capabilities spanning generic and specialty therapeutic segments globally.

- Key Products: Generic APIs, Specialty APIs, Oncology APIs

- Strategic Focus: Expanding specialty and complex API capabilities, reducing generic API cost base through process innovation, and growing CDMO service revenue from global pharmaceutical partnerships.

Aurobindo Pharma Limited

Aurobindo Pharma Limited is one of India's largest API and generic formulation manufacturers, with a vertically integrated API manufacturing base supplying both internal formulation and third-party global pharmaceutical customers across regulated markets.

- Key Products: Antibiotic APIs (penicillin, cephalosporin), antiviral APIs, antiretroviral APIs, cardiovascular APIs, and CNS APIs across multiple therapeutic categories.

- Strategic Focus: Strengthening backward integration into key starting materials, expanding penicillin and cephalosporin API capacity, and growing the export API business across the US, EU, and emerging markets.

Divi's Laboratories Limited

Divi's Laboratories Limited is India's leading API contract development and manufacturing organisation, specialising in custom synthesis for global innovator pharmaceutical companies and generic API supply for major off-patent molecules.

- Key Products: Custom Synthesis APIs, Nutraceuticals, Generic APIs, and others.

- Strategic Focus: Deepening CDMO relationships with top global pharmaceutical innovators, expanding custom synthesis capabilities into peptides and oligonucleotides, and maintaining cost leadership in high-volume generic API categories.

Market Concentration Analysis

The India API market is moderately fragmented, with the top five companies collectively accounting for approximately 35–45% of domestic API revenue. The remaining market share is distributed across a large base of specialised API manufacturers, CDMO operators, and smaller generic API producers.

Market concentration is expected to increase modestly through consolidation driven by regulatory compliance pressures, capital requirements for specialty API manufacturing, and competitive advantages of scale in cost-intensive commodity API categories.

Investment & Growth Opportunities

Highest Growth Segments

Oncology APIs (~10–12% CAGR), biosimilar and biopharmaceutical APIs (~11% CAGR), high-potency APIs (~9% CAGR from a small base), peptide synthesis APIs (~13% CAGR), and CDMO services (~10% CAGR) represent the highest-growth investment vectors in India's API market through 2034.

Emerging Investment Opportunities

Oligonucleotide and gene therapy API manufacturing represents the API market's most nascent high-value emerging opportunity. As global demand for RNA and DNA-based therapeutics grows, Indian CDMO players with oligonucleotide synthesis and purification capabilities can capture significant per-unit value at premium pricing, supplying both clinical-phase and commercial-stage biopharmaceutical programs.

Investment Themes

- PLI scheme-backed KSM and intermediate manufacturing: Investment in domestically manufactured key starting materials reduces China import dependency, qualifies for government financial incentives, and creates a structurally defensible position in India's API supply chain through 2034.

- Specialty CDMO build-out targeting European and US innovator pipeline: Investment in spray drying, crystallisation engineering, and continuous flow chemistry capabilities captures high-margin CDMO contracts from global pharmaceutical innovators seeking quality-assured Indian manufacturing partners.

Future Market Outlook (2026-2034)

The India API market is projected to grow from USD 19.21 Billion in 2025 to USD 41.60 Billion by 2034, at a 7.78% CAGR. The anchor value of USD 27.93 Billion in 2030 reflects the market's transition from volume-driven generic API supply to a higher-value manufacturing ecosystem encompassing complex generics, biosimilars, and CDMO services.

Three structural forces define India API market growth through 2034. Global pharmaceutical company supply chain diversification away from China creates durable long-term API demand for India. Patent cliff opportunities in oncology, immunology, and CNS through 2030 create massive generic API volume requirements. Government PLI investment in KSM and API self-reliance reduces input cost dependency and strengthens India's competitive position in regulated global markets.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders, including API manufacturing heads, CDMO business development executives, regulatory affairs specialists, export compliance officers, and pharmaceutical procurement managers across India's key manufacturing clusters.

Secondary Research

Secondary research encompassed company annual reports, CDSCO drug master file databases, USFDA establishment inspection reports, India Pharmaceutical Alliance export data, Department of Pharmaceuticals PLI scheme progress reports, and industry association publications. Over 60 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a bottom-up model: (i) API production volume forecast by therapeutic category; (ii) average API realisation per kilogram by drug type and market; (iii) domestic versus export revenue split by manufacturer type; (iv) biosimilar and specialty API premium adjustment for non-commodity segments.

India Active Pharmaceutical Ingredients Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Drug Types Covered | Innovative Active Pharmaceutical Ingredients, Generic Active Pharmaceutical Ingredients |

| Manufacturer Types Covered |

|

| Synthesis Types Covered |

|

| Therapeutic Applications Covered | Oncology, Cardiovascular and Respiratory, Diabetes, Central Nervous System Disorders, Neurological Disorders, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Sun Pharmaceutical Industries Ltd., Aurobindo Pharma Limited, Dr. Reddy's Laboratories Ltd., Divi's Laboratories Limited, Cipla, Lupin, etcx. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India active pharmaceutical ingredients market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India active pharmaceutical ingredients market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India active pharmaceutical ingredients industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Active Pharmaceutical Ingredients Market Report

The India API market reached USD 19.21 Billion in 2025, driven by Generic APIs at 58.4%, Merchant Manufacturer dominance at 52.3%, West India's 32.4% regional leadership, and growing export volumes to regulated markets in the US and EU.

The India API market grows at 7.78% CAGR during 2026-2034, reaching USD 41.60 Billion by 2034, reflecting PLI scheme capacity expansion, patent expirations driving generic API demand, biosimilar scale-up, and China+1 sourcing diversification benefiting Indian manufacturers.

Generic APIs lead at 58.4% in 2025, driven by India's global leadership in generic pharmaceutical manufacturing, established process chemistry capabilities, and USFDA-compliant production scale. Innovative APIs at 41.6% represent the premium-priced complementary segment.

Merchant API Manufacturers lead at 52.3% through third-party supply contracts, CDMO service integration, and export API business with global formulation companies. Captive manufacturers at 47.7% serve internal formulation requirements of vertically integrated pharmaceutical groups.

West India leads at 32.4% through Maharashtra and Gujarat pharmaceutical clusters anchored in Ahmedabad, Mumbai, and Vadodara. South India, at 29.1%, is the second largest region, driven by Hyderabad's established API manufacturing and CDMO sector.

Leading companies include include Sun Pharmaceutical Industries Ltd., Aurobindo Pharma Limited, Dr. Reddy's Laboratories Ltd., Divi's Laboratories Limited, Cipla, Lupin, and others.

The India API market is projected to reach approximately USD 27.93 Billion by 2030, with oncology API capacity expansion, biosimilar manufacturing scale-up, and PLI-backed KSM self-reliance driving above-market growth in specialty and complex API segments.

Oncology and HPAPI manufacturing, biosimilar API capacity, peptide synthesis CDMO services, KSM import substitution under PLI, and specialty CDMO partnerships with global innovators represent the leading investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)