India Adhesives Market Size, Share, Trends and Forecast by Technology, Resin, End User Industry, and Region, 2026-2034

India Adhesives Market Size, Share, Trends & Forecast (2026-2034)

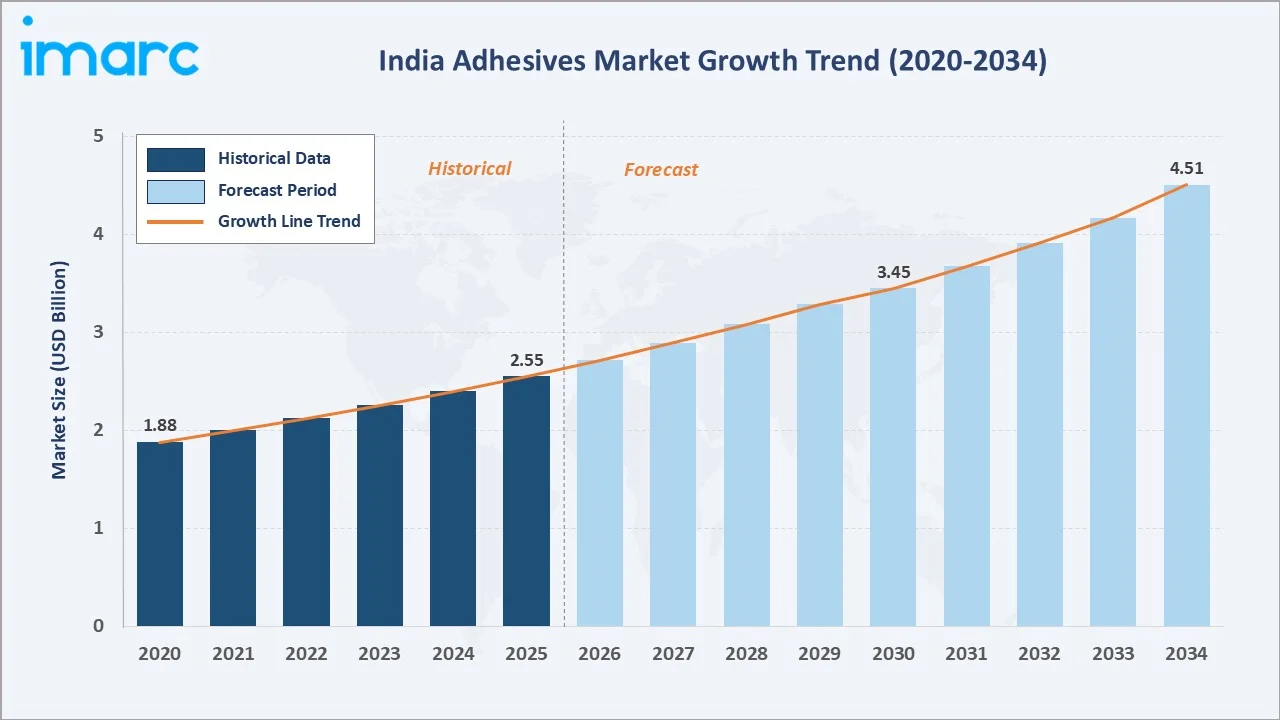

The India adhesives market size reached USD 2.55 Billion in 2025 and is projected to reach USD 4.51 Billion by 2034, exhibiting a CAGR of 6.22% during 2026-2034. Rising demand from the automobile, construction, packaging, and electronics sectors, the shift toward eco-friendly high-performance adhesives, and tighter environmental regulations are the primary forces driving market growth.

Water-borne adhesives lead technology at 32.6% in 2025, acrylic resin dominates at 26.4%, and West India commands the largest regional share at 34.1%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.55 Billion |

|

Forecast Market Size (2034) |

USD 4.51 Billion |

|

CAGR (2026-2034) |

6.22% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West India (34.1% share, 2025) |

|

Leading Technology |

Water-borne Adhesives (32.6%, 2025) |

|

Leading Resin |

Acrylic Resin (26.4%, 2025) |

The India adhesives market growth trajectory from 2020 through 2034, with historical expansion to USD 2.55 Billion in 2025, reflects consistent multi-sector industrial demand, while the forecast to USD 4.51 Billion captures accelerating EV adoption, national infrastructure investment, and packaging-driven bonding needs.

To get more information on this market, Request Sample

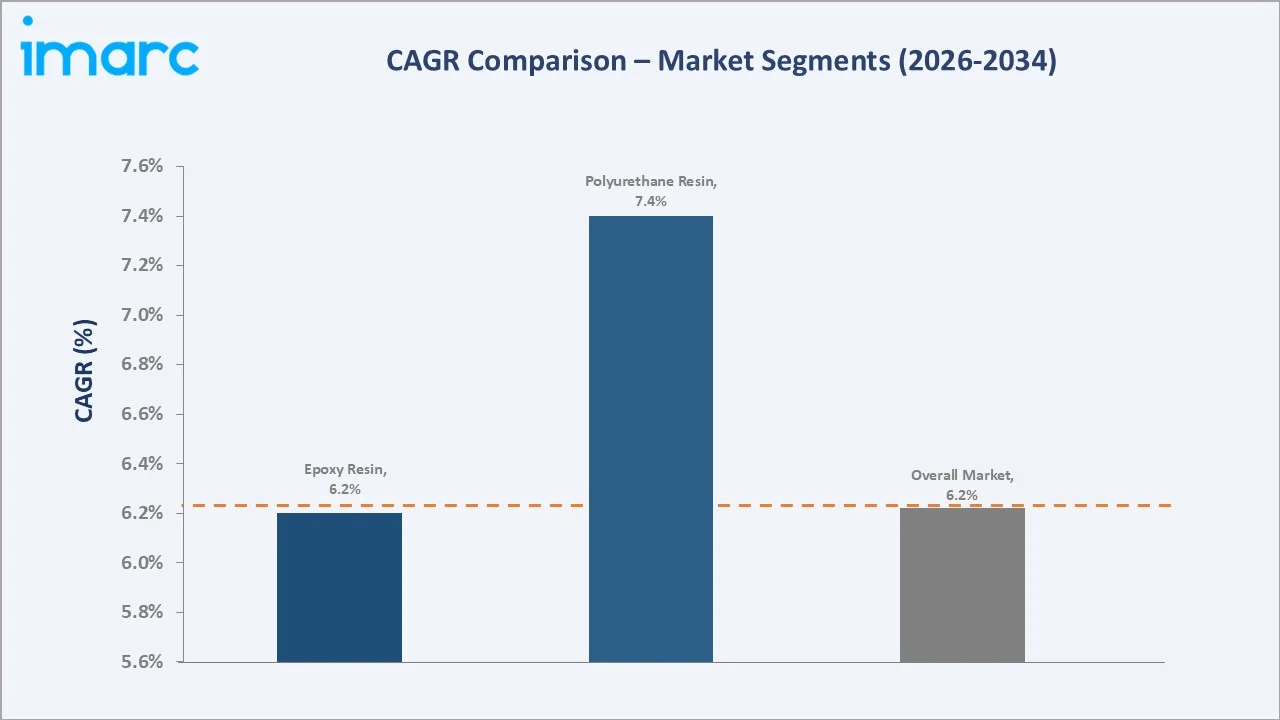

The CAGR trajectories across technology, resin, and regional sub-segments, with UV-cured adhesives at approximately 7.5% CAGR and polyurethane resin at approximately 7.4% CAGR, are the fastest-growing categories within the India adhesives industry analysis through 2034.

Executive Summary

The India adhesives market is on a sustained growth trajectory from USD 2.55 Billion in 2025 to USD 4.51 Billion by 2034. Adhesives are essential bonding agents deployed across automotive assembly, construction, flexible packaging, electronics, footwear, and woodworking, benefiting from multi-sector demand that insulates the market from single-industry cycles.

Water-borne adhesives dominate technology at 32.6% in 2025, driven by environmental regulations restricting VOC emissions and growing adoption across packaging and construction applications. Hot melt adhesives (24.8%) lead in packaging and woodworking due to fast cure cycles and solvent-free application chemistry. Acrylic resin leads at 26.4% owing to excellent multi-substrate bonding versatility.

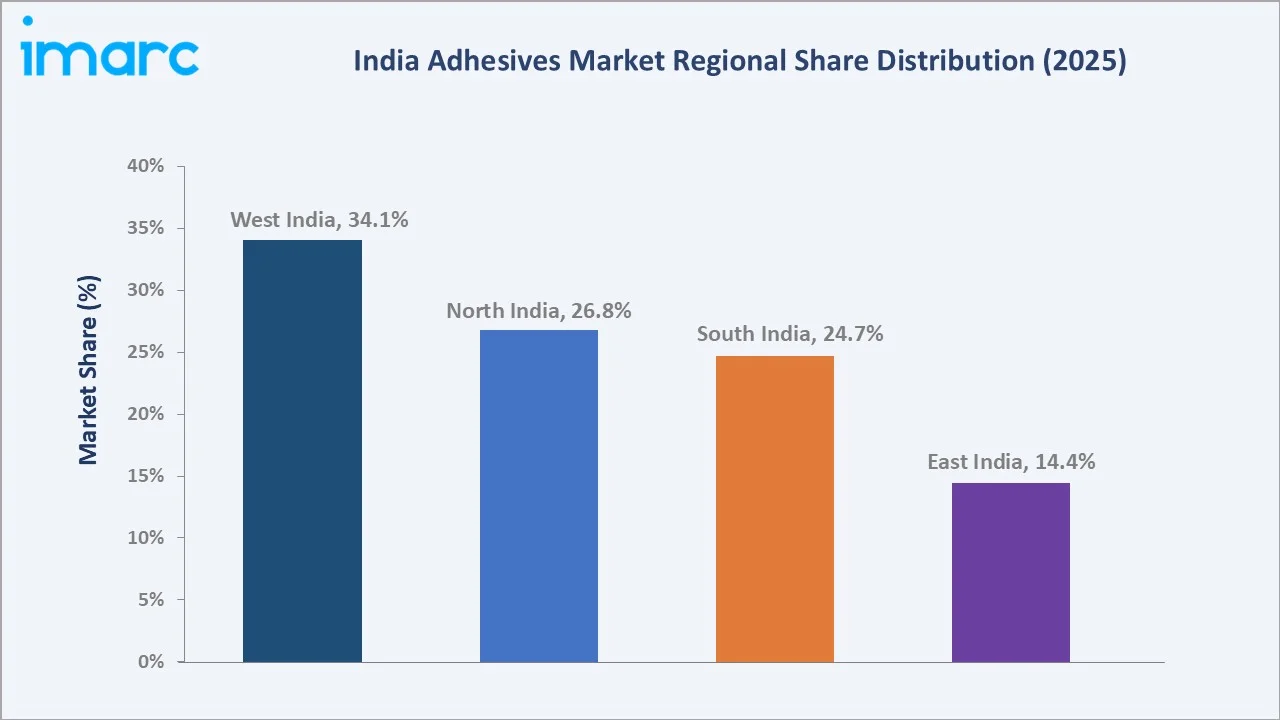

West India commands 34.1% regional share in 2025, anchored by Maharashtra's automotive OEM clusters and Gujarat's chemical manufacturing base. North India (26.8%) follows, driven by auto component manufacturing and footwear industries. South India (24.7%) benefits from growing electronics and EV supply chain expansion in Tamil Nadu and Karnataka.

Key Market Insights

|

Insight |

Data |

|

Largest Technology Segment |

Water-borne – 32.6% share (2025) |

|

Fastest-Growing Technology |

UV Cured Adhesives (~7.5% CAGR, 2026-2034) |

|

Largest Resin Segment |

Acrylic – 26.4% share (2025) |

|

Fastest-Growing Resin |

Polyurethane (~7.4% CAGR, 2026-2034) |

|

Leading Region |

West India – 34.1% share (2025) |

|

Second Largest Region |

North India – 26.8% share (2025) |

|

Top Companies |

Pidilite Industries Ltd., Henkel Adhesives Technologies India Private Limited, 3M, H.B. Fuller Company, Arkema, Jubilant Bhartia Group, Astral Adhesives |

Key Analytical Observations Expanding on the Above Data:

- Water-borne adhesives, with 32.6% in 2025, dominate because CPCB environmental mandates are accelerating the shift from solvent-borne to low-VOC formulations in packaging, construction, and consumer applications across India.

- Acrylic resin, at 26.4% in 2025, leads due to superior UV resistance, adhesion to diverse substrates, and broad applicability across pressure-sensitive, structural, and sealant adhesive formulations.

- West India's 34.1% dominance in 2025 reflects Maharashtra's concentration of automotive OEMs and Tier-1 suppliers alongside Gujarat's chemical manufacturing corridor and dense packaging industry base.

- South India at 24.7% is the fastest-growing region, driven by semiconductor and electronics manufacturing expansion in Chennai, Bengaluru, and Mysuru, creating demand for high-performance UV-cured and thermally conductive adhesive systems.

India Adhesives Market Overview

Adhesives are chemical substances that bond two surfaces together through surface attachment, enabling structural joining, sealing, and laminating across industrial and consumer applications. The India adhesives ecosystem integrates petrochemical raw material producers, specialty resin and polymer manufacturers, adhesive formulators, surface treatment providers, and end-use industries spanning automotive, construction, packaging, electronics, footwear, and healthcare.

.webp)

India's adhesives industry is one of the fastest-growing segments within the broader specialty chemicals sector. Government initiatives including the Production Linked Incentive scheme for automobiles, the National Infrastructure Pipeline, and the Smart Cities Mission are generating sustained structural demand for advanced bonding solutions across construction, transportation, and industrial manufacturing verticals.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

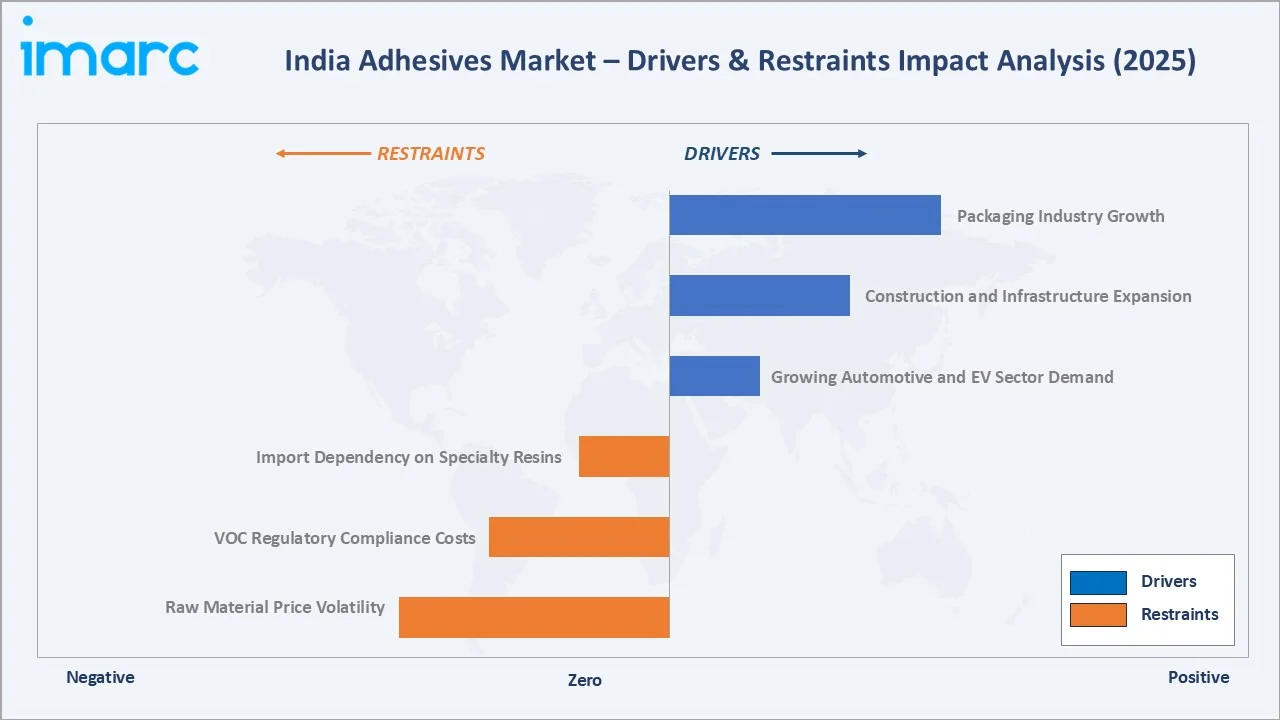

- Growing Automotive and EV Sector Demand: India's EV market crossed 2 million units in 2024, a 24% year-on-year increase, driving structural bonding adhesives for battery pack assembly, lightweight body panels, and thermal management systems that replace conventional welding, reducing vehicle weight by 8-12%.

- Construction and Infrastructure Expansion: India's National Infrastructure Pipeline targets USD 1.4 Trillion in investments, generating demand for tile adhesives, waterproofing compounds, sealants, and construction-grade epoxies. The Smart Cities Mission and Housing for All scheme are major catalysts sustaining multi-year adhesive demand.

- Packaging Industry Growth: India's packaging market is expanding at approximately 8% annually, driven by e-commerce, FMCG, and food delivery sectors. Hot melt, pressure-sensitive, and water-based adhesives are critical for carton sealing, labeling, and flexible packaging lamination applications.

Market Restraints

- Raw Material Price Volatility: Adhesive formulations rely on petroleum-derived chemicals including acrylates, polyurethane polyols, and epoxy resins. Global crude oil price fluctuations directly impact raw material costs, creating margin pressure for formulators unable to pass increases to price-sensitive customers.

- VOC Regulatory Compliance Costs: Stricter CPCB guidelines on volatile organic compound emissions require reformulation investments from solvent-borne adhesive manufacturers, with conversion to water-borne or reactive systems involving capital expenditure that strains smaller domestic formulators.

Market Opportunities

- Smart Adhesives and Industry 4.0 Integration: Adhesives responding to temperature, humidity, or pressure are gaining traction in aerospace, electronics, and healthcare. New Application Engineering Centers deploying Industry 4.0 smart manufacturing for high-performance adhesives signal the opportunity in intelligent bonding systems.

- Bio-based and Sustainable Adhesive Development: EPR mandates on packaging waste and green building certifications are driving demand for bio-based adhesives derived from starch, soy protein, and lignin. Solvent-free and recyclable-compatible formulations are attracting growing investment from domestic and multinational formulators.

Market Challenges

- Counterfeiting and Unorganised Sector Competition: India's construction and consumer adhesive segments face significant pressure from unbranded sub-standard products in price-sensitive tier-2 and tier-3 markets, eroding revenue and brand trust for organised market participants.

- Import Dependency on Specialty Resin Systems: High-performance reactive, UV-cured, and silicone adhesive systems rely heavily on imported specialty monomers and photoinitiators, creating supply chain disruption risk and cost uncertainty for premium application segment manufacturers.

Emerging Market Trends

1. Shift to Water-borne and Low-VOC Adhesives Driven by Environmental Regulations

India's CPCB has tightened VOC emission norms for adhesive applications. Water-borne adhesives, growing at approximately 7.1% CAGR, are the fastest-growing technology segment, replacing solvent-borne formulations in woodworking, packaging, and textile lamination across compliance-driven industries.

2. EV Battery and Structural Bonding Demand Transforming Automotive Adhesives

India's EV push under FAME II and EMPS 2024 is driving structural adhesive demand for battery cell fixation, thermal interface bonding, and lightweight body panel assembly. Automotive adhesives command a premium CAGR within the broader market through 2034.

3. Growth of UV-Cured Adhesives in Electronics and Medical Device Assembly

UV-cured adhesives at 10.0% share in 2025 are growing at the fastest CAGR of approximately 7.5%, driven by rapid cure cycles, solvent-free composition, and growing electronics manufacturing in India. Semiconductor assembly, PCB bonding, and medical device encapsulation are key demand segments.

4. Capacity Expansion and Localisation by Global Players

Global adhesive companies are rapidly localising Indian production to compete on price and lead time. Multiple capacity expansions through 2024-2025 target solvent-based adhesives for packaging, smart manufacturing for automotive and electronics, and bio-based formulations for sustainable packaging converters.

Industry Value Chain Analysis

The India adhesives value chain spans five stages from raw material supply through end-use application. Adhesive formulation captures the highest value-added margins, while distribution logistics and brand equity are critical competitive differentiators for market participants at each stage.

|

Stage |

Description |

|

Raw Material Supply |

Petrochemical derivatives, specialty monomers, resins, and solvents sourced from domestic and international chemical producers |

|

Resin & Chemical Manufacturing |

Conversion of raw chemicals into polymer resins including acrylic, polyurethane, epoxy, VAE/EVA, silicone, and cyanoacrylate systems |

|

Adhesive Formulation |

Blending, compounding, and packaging of finished adhesive products across water-borne, hot melt, solvent-borne, reactive, and UV-cured technologies |

|

Packaging & Distribution |

Bulk and packaged products distributed through specialty chemical stockists, industrial distributors, and direct OEM supply channels |

|

End-Use Industries |

Automotive, building & construction, packaging, electronics, footwear & leather, woodworking, healthcare, and aerospace applications |

Integrated adhesive manufacturers with captive resin sourcing achieve lower material cost structures than pure-play formulators. Global players leverage R&D capabilities and certified formulations to command premium pricing in automotive and electronics segments relative to domestic commodity producers.

Technology Landscape in the India Adhesives Industry

Water-borne and Bio-based Adhesive Formulation Technology

Water-borne adhesive technology uses polymer dispersions including acrylic, VAE, and polyurethane in aqueous media, eliminating organic solvent emissions. Advanced cross-linking chemistry enables water-borne formulations to match solvent-borne bond strength in wood, paper, and textile applications, driving conversion across regulated and export-oriented industries.

Reactive Adhesive and Structural Bonding Systems

Two-component epoxy and polyurethane reactive systems provide the highest structural bond strengths, critical for automotive crash-resistant joints and construction panel bonding. High-speed two-component metering and mixing systems enable automated reactive adhesive dispensing on EV assembly lines and modular construction platforms.

UV-Cured and Radiation-Cured Adhesive Technology

UV-cured acrylate adhesives cure instantly on light exposure, enabling high-speed electronics assembly and medical device manufacturing. Dual-cure UV and moisture systems are gaining specification for shadow-area bonding in complex geometries. India's growing electronics manufacturing ecosystem is accelerating UV adhesive adoption significantly.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Technology | Water-borne | 32.6% | 2025 |

| Resin | Acrylic | 26.4% | 2025 |

| End User Industry | 🔒 | 🔒 | 2025 |

| Region | West India | 34.1% | 2025 |

By Technology

Water-borne adhesives command a 32.6% majority share in 2025, driven by environmental compliance mandates and growing adoption in packaging and construction sectors. The technology's low-VOC profile aligns with CPCB regulations and green building certifications, making it the default specification for sustainable building and consumer adhesive applications.

.webp)

To access detailed market analysis, Request Sample

Hot melt adhesives at 24.8% in 2025 lead in packaging and woodworking due to zero-solvent application and instant bonding at high line speeds. Solvent-borne adhesives (18.7%) retain specification in footwear, automotive interior, and industrial applications. Reactive adhesives (13.9%) dominate structural engineering. UV-cured adhesives (10.0%) are the fastest-growing segment.

By Resin

Acrylic resin commands a 26.4% majority share in 2025 owing to outstanding UV stability, adhesion to diverse substrates including plastics, glass, and metals, and versatile application in both pressure-sensitive and structural adhesive formulations across all key end-use industries in India.

.webp)

Polyurethane resin at 18.7% in 2025, growing fastest at approximately 7.4% CAGR, is essential in automotive structural bonding, footwear, and construction waterproofing. Epoxy (16.2%) leads industrial structural applications. VAE/EVA (14.8%) serves woodworking and packaging. Silicone (10.6%) commands premium pricing in electronics and healthcare. Cyanoacrylate (7.9%) leads consumer instant adhesives.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West India |

34.1% |

Largest chemical manufacturing base; major automotive OEM and packaging clusters; high construction activity in urban agglomerations |

|

North India |

26.8% |

Auto component manufacturing corridors; footwear and leather industries; rapid urbanisation driving construction adhesive demand |

|

South India |

24.7% |

Growing electronics and semiconductor manufacturing; EV supply chain development; pharmaceutical and medical device assembly |

|

East India |

14.4% |

Rising construction activity and infrastructure projects; expanding packaging demand from consumer goods and FMCG sectors |

West India's 34.1% market dominance in 2025 is driven by Maharashtra's concentration of automotive OEM and Tier-1 supplier plants, Gujarat's chemical manufacturing corridor, and a dense packaging industry in the Mumbai Metropolitan Region. The region benefits from established distribution networks and proximity to the country's largest port infrastructure.

North India with 26.8% in 2025 benefits from the NCR auto component cluster, footwear and leather manufacturing, and industrial corridor development. South India at 24.7% is the fastest-growing region, underpinned by electronics and semiconductor manufacturing expansion creating demand for UV-cured and thermally conductive adhesive systems.

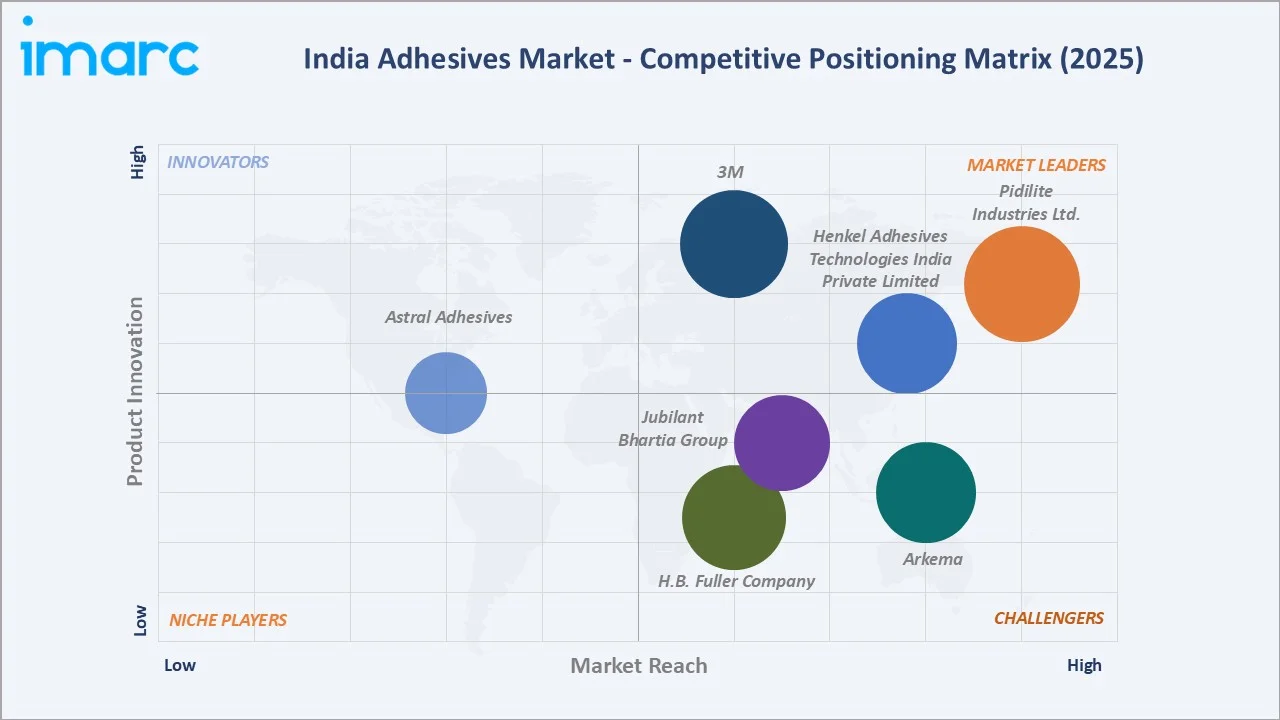

Competitive Landscape

The India adhesives market is moderately fragmented, with a domestic leader commanding strong brand equity in consumer and carpentry channels, while global multinationals compete in industrial, automotive, and high-performance segments through technical application expertise and R&D-driven differentiation across formulation platforms.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Pidilite Industries Ltd. |

Fevicol, Fevicol MR, Fevistick, Fevikwik, Fevibond, Fevigum, Falcofix |

Leader |

Dominant domestic brand; consumer & construction adhesives |

|

Henkel Adhesives Technologies India Private Limited |

Aquence, Loctite, Technomelt, Teroson |

Leader |

Industrial & automotive; Industry 4.0 smart manufacturing |

|

3M |

Scotch-Weld, VHB Tape |

Leader |

Diversified portfolio; electronics & automotive specialty |

|

H.B. Fuller Company |

Tuskbond, Fullabond, Fullamelt |

Challenger |

Packaging & woodworking; hot melt technology leadership |

|

Arkema |

Bostik |

Challenger |

Specialty & construction adhesives; sustainable formulations |

|

Jubilant Bhartia Group |

Jivanjor, Vamicol, Polystic, Hero |

Challenger |

PVAc (Polyvinyl Acetate) and VP (Vinyl Pyridine) Latex; building & woodworking adhesives |

|

Astral Adhesives |

Bondtite, Resimet |

Emerging |

Epoxy and industrial adhesives; dealer channel distribution |

Key players include Pidilite Industries Ltd., Henkel Adhesives Technologies India Private Limited, 3M, H.B. Fuller Company, Arkema, Jubilant Bhartia Group, Astral Adhesives, and others.

Key Company Profiles

Pidilite Industries Ltd.

Pidilite Industries is India's largest adhesive manufacturer, headquartered in Mumbai. The company commands dominant domestic brand equity through Fevicol, FeviKwik, Dr. Fixit, and Roff product families, serving carpenter, construction, and consumer segments through a 680,000-outlet dealer network.

- Product Portfolio: Fevicol, Fevicol MR, Fevistick, Fevikwik, Fevibond, Fevigum, Falcofix

- Recent Developments: In April 2024, Pidilite launched Fevikwik Precision Pro, Fevikwik Gel, Fevikwik Advanced, and Fevikwik Craft, enhancing cyanoacrylate product performance for consumer repair and crafting applications.

- Strategic Focus: Pidilite's strategy leverages its unmatched distribution depth and brand trust to defend consumer segment leadership while expanding into construction chemicals and waterproofing where margins are structurally higher and competitive intensity from global players is lower.

Henkel Adhesives Technologies India Private Limited

Henkel India is a subsidiary of Henkel AG & Co. KGaA, operating the Adhesive Technologies division serving automotive, electronics, packaging, and industrial maintenance markets through Loctite, Technomelt, and Bonderite brand portfolios.

- Product Portfolio: Aquence, Loctite, Technomelt, Teroson

- Recent Developments: In July 2024, Henkel announced the completion of Phase 3 of its adhesive materials manufacturing facility at its Kurkumbh site near Pune, reinforcing its commitment to expanding local production capabilities.

- Strategic Focus: Henkel's India strategy focuses on localised manufacturing to reduce import dependence, application engineering to create customer preference, and expansion in EV battery and electronics assembly adhesives where India's manufacturing growth creates significant long-term volume opportunity.

3M

3M Company operates across industrial adhesives and tapes, electronics assembly, automotive, and consumer segments with a highly diversified product portfolio spanning structural bonding, VHB foam tapes, and specialty adhesive systems.

- Product Portfolio: Scotch-Weld, VHB Tape

- Strategic Focus: 3M's India strategy prioritises diversification across electronics, automotive, and industrial end markets, leveraging global technology transfer to introduce high-margin specialty adhesive solutions where domestic manufacturing is deepening under PLI schemes.

Market Concentration Analysis

The India adhesives market is moderately fragmented at the national level, with the domestic market leader holding an estimated 20-25% overall share anchored by consumer and carpenter channel dominance. Industrial and high-performance segments are served by global players who collectively hold significant organised sector share across technology-intensive applications.

Consolidation is occurring through capacity expansion and product line extension rather than mergers and acquisitions. Global players are localising manufacturing to compete on price and delivery in growing mid-market segments, while domestic leaders are moving upmarket into construction chemicals where premium pricing supports stronger returns on capital.

Investment & Growth Opportunities

Fastest-Growing Segments

UV-cured adhesives at approximately 7.5% CAGR through 2034 represent the highest-growth technology segment, driven by electronics and medical device manufacturing expansion. Polyurethane resin at approximately 7.4% CAGR is the fastest-growing resin type, fuelled by EV structural bonding and construction waterproofing demand.

Emerging Markets

The electronics manufacturing segment, anchored by India's PLI scheme, is creating high-growth demand for UV-cured, thermally conductive, and electrically insulating adhesives. EV battery pack assembly adhesives represent an incremental opportunity growing from near-zero to significant scale by 2034.

Venture & Investment Trends

Domestic adhesive manufacturers are attracting private equity interest, supported by import substitution tailwinds and PLI-linked demand growth. Global specialty chemical companies are expanding India manufacturing through greenfield plants and partnership structures. Sustainable adhesive formulation R&D is attracting startup activity in bio-based and recyclable adhesive systems.

Future Market Outlook (2026-2034)

The India adhesives market is forecast to expand from USD 2.55 Billion in 2025 to USD 4.51 Billion by 2034 at a CAGR of 6.22%, adding USD 1.96 Billion in incremental annual market value. This sustained growth reflects India's multi-sector industrial expansion, large-scale infrastructure investment, and accelerating shift toward premium high-performance adhesive systems.

Three structural forces will most significantly shape the India adhesives industry through 2034. First, the EV transition will create the largest new demand vertical in automotive adhesives, with battery pack bonding and thermal management adhesives growing at approximately 9% CAGR. Second, the National Infrastructure Pipeline construction boom will sustain high-volume demand for tile, waterproofing, and structural adhesives. Third, electronics and semiconductor manufacturing localisation under PLI schemes will drive adoption of advanced UV-cured and thermally conductive adhesive systems currently sourced through imports.

Research Methodology

Primary Research

Primary research encompassed structured interviews with adhesives industry stakeholders including senior commercial managers at domestic formulators, purchasing managers at automotive OEMs, EPC procurement specialists, and technical managers at global adhesive multinationals operating in India, validating market sizing, technology shares, and regional demand estimates.

Secondary Research

Key secondary sources include Ministry of Chemicals and Fertilizers production data, CPCB VOC regulation documents, Automotive Component Manufacturers Association data, National Infrastructure Pipeline database, BIS adhesive product standards, Chemical Weekly, and Adhesives and Sealants Industry trade publications.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models incorporating GDP growth rates, industrial production indices, end-use sector growth trajectories, and historical adhesives consumption intensity ratios. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty.

India Adhesives Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Hot Melt, Reactive, Solvent-borne, UV Cured Adhesives, Water-borne |

| Resins Covered | Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA, Others |

| End User Industries Covered | Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Pidilite Industries Ltd., Henkel Adhesives Technologies India Private Limited, 3M, H.B. Fuller Company, Arkema, Jubilant Bhartia Group, Astral Adhesives, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India adhesives market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India adhesives market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India adhesives industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Adhesives Market Report

The India adhesives market reached USD 2.55 Billion in 2025, reflecting consistent demand from automotive, construction, packaging, and electronics sectors alongside a structural shift toward eco-friendly, high-performance, and smart adhesive formulations.

The India adhesives market is projected to reach USD 4.51 Billion by 2034, growing at a CAGR of 6.22% during 2026-2034, supported by multi-sector industrial expansion and growing adoption of specialty adhesive systems.

Water-borne adhesives lead the technology segment with a 32.6% share in 2025, driven by environmental compliance requirements and growing adoption in packaging, construction, and consumer applications across India.

Acrylic resin holds the largest share at 26.4% in 2025, owing to its excellent UV resistance, multi-substrate adhesion capability, and broad applicability across pressure-sensitive, structural, and sealant adhesive formulations.

West India leads the market with a 34.1% share in 2025, anchored by Maharashtra's automotive and pharmaceutical industries and Gujarat's large-scale chemical manufacturing base and packaging industry.

Key players include Pidilite Industries Ltd., Henkel Adhesives Technologies India Private Limited, 3M, H.B. Fuller Company, Arkema, Jubilant Bhartia Group, Astral Adhesives, and others.

Primary growth drivers include rising EV and automotive sector demand, large-scale construction and infrastructure investment, packaging industry expansion driven by e-commerce, and the increasing adoption of eco-friendly and high-performance adhesive formulations across regulated industries.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade