India Air Fryer Market Size, Share, Trends and Forecast by Product Type, Technology, Sales Channel, End Use, and Region, 2026-2034

India Air Fryer Market Size, Share, Trends & Forecast (2026-2034)

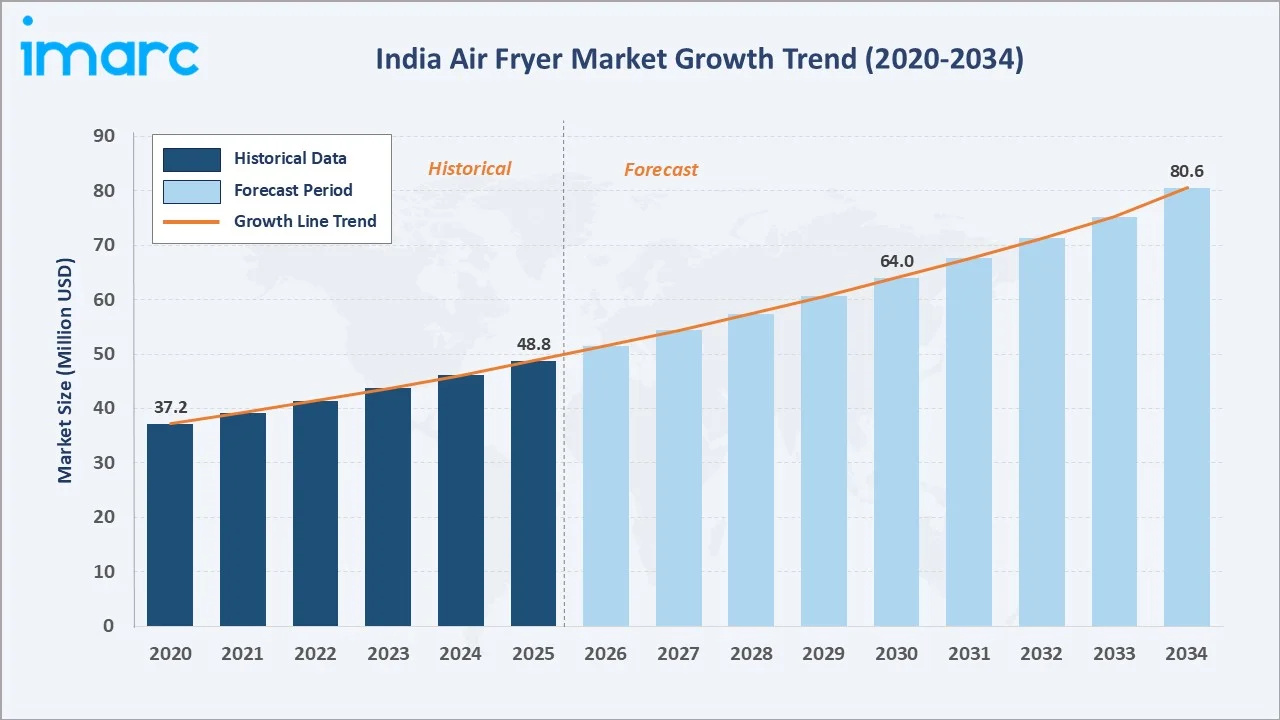

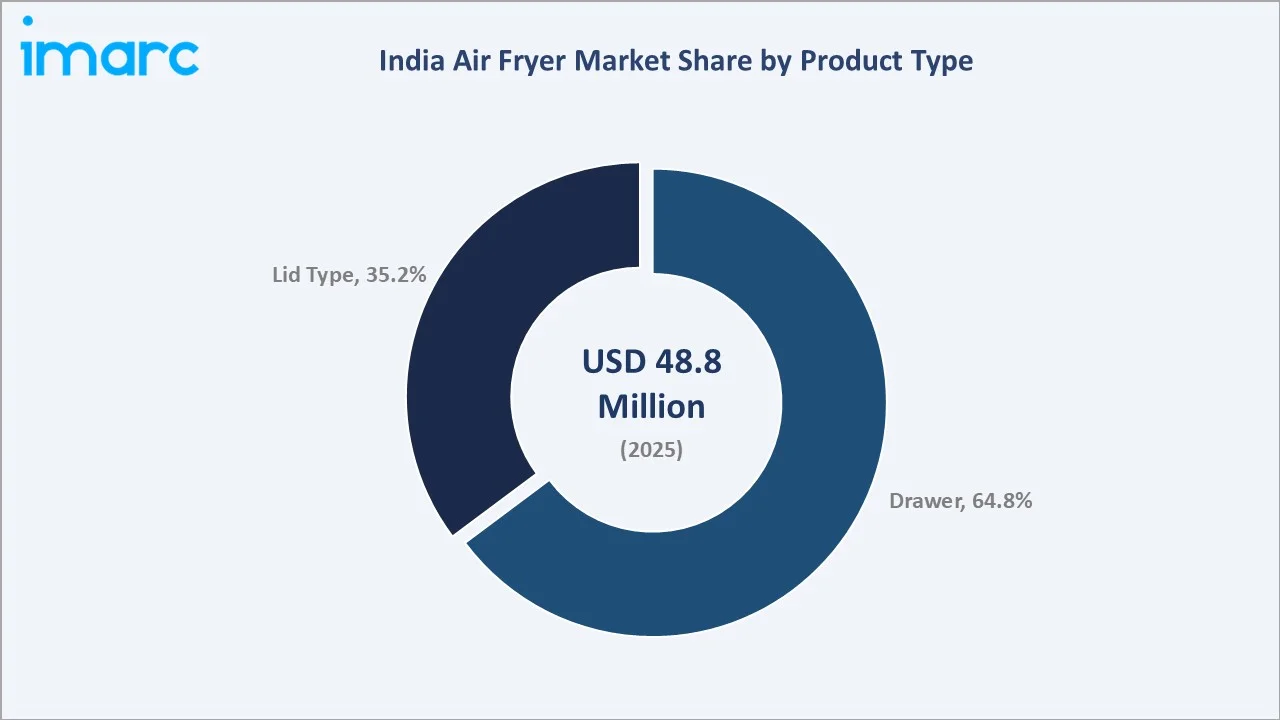

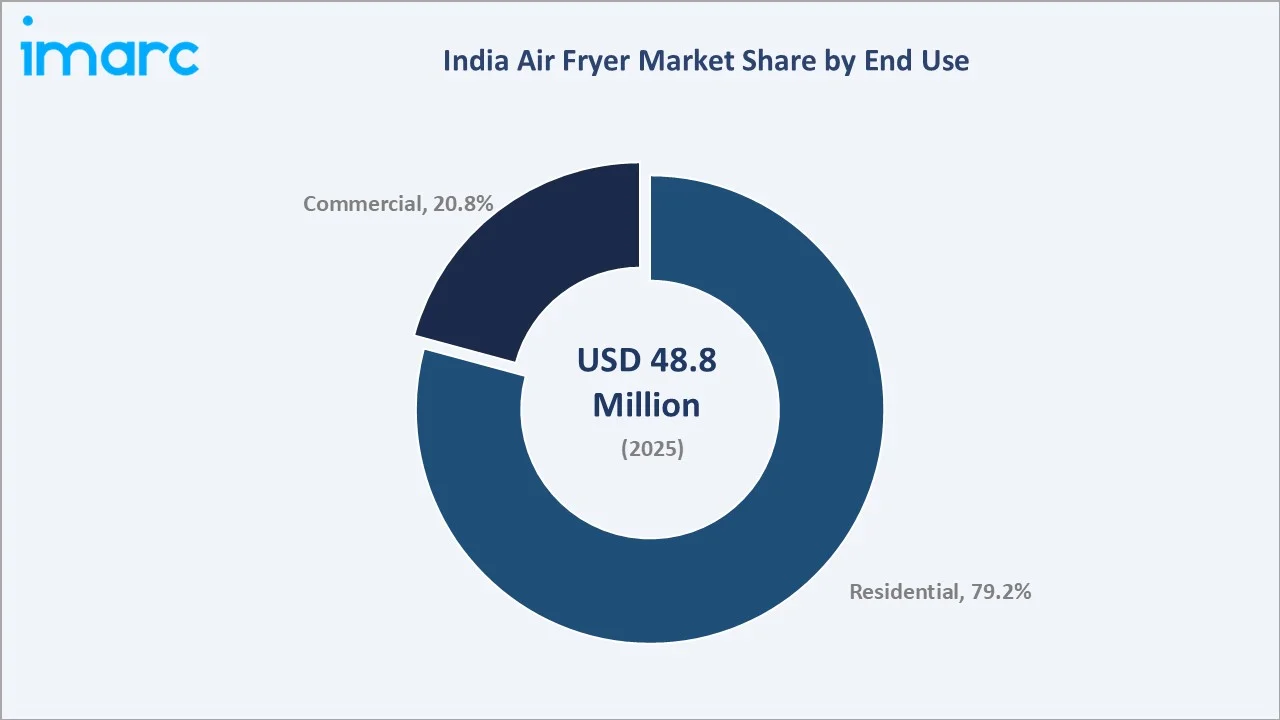

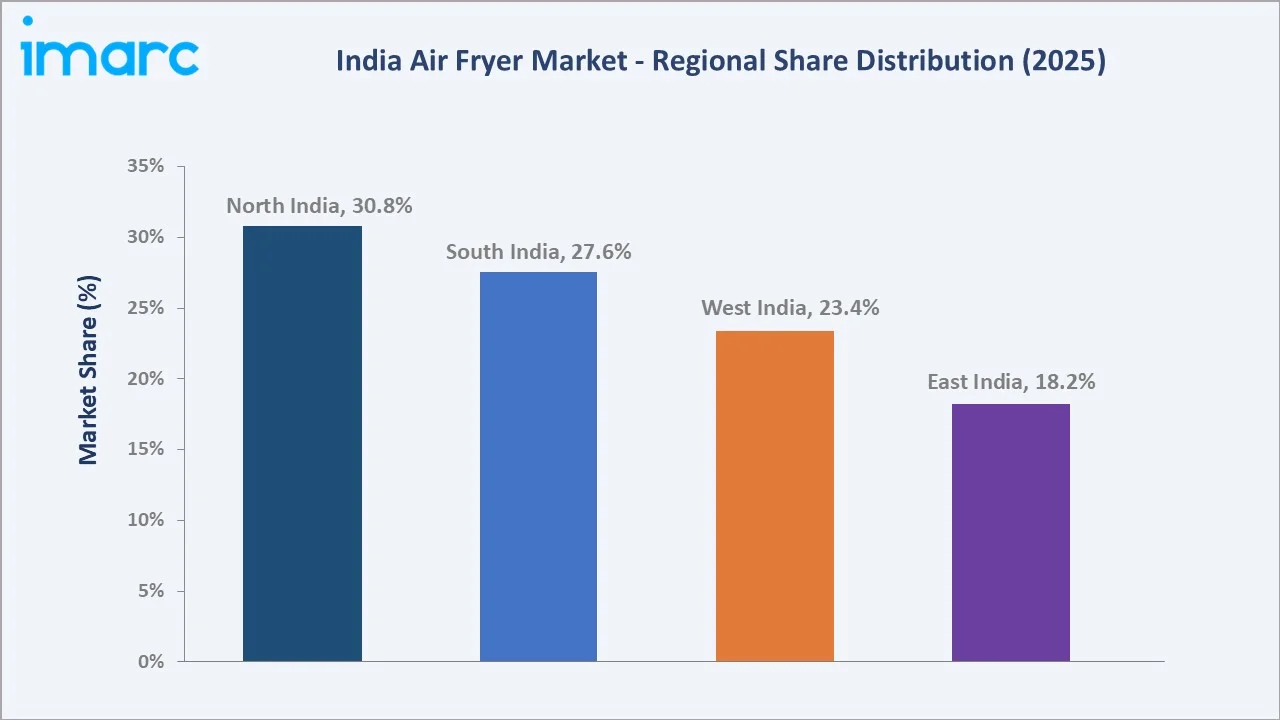

The India air fryer market reached USD 48.8 Million in 2025 and is projected to reach USD 80.6 Million by 2034, growing at a CAGR of 5.57% during 2026-2034. The market is driven by rising health consciousness, growing preference for low-oil cooking, and increasing adoption of smart kitchen appliances among urban households. PM Modi urged Indians to reduce their cooking oil consumption by 10% to benefit both personal health and the nation. Air fryers allow frying, roasting, and grilling with minimal oil, making them a suitable choice for health-conscious households aiming to reduce oil intake. Drawer type dominates at 64.8%. Residential leads end use at 79.2%. North India commands 30.8% of the national market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 48.8 Million |

|

Forecast Market Size (2034) |

USD 80.6 Million |

|

CAGR (2026-2034) |

5.57% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Drawer (64.8%, 2025) |

|

Dominant End Use |

Residential (79.2%, 2025) |

|

Leading Region |

North India (30.8%, 2025) |

India air fryer market expanded from USD 37.2 Million in 2020 to USD 48.8 Million in 2025, anchored at USD 64.0 Million in 2030, and forecast to reach USD 80.6 Million by 2034. The COVID-19 pandemic (2020-2021) was the most significant single demand catalyst in India air fryer market history. Post-COVID, sustained health consciousness, the fast-food culture revolution, and BIS mandatory certification improving product quality perception collectively sustained above-trend market growth.

To get more information on this market, Request Sample

Lid-type air fryers grow fastest at ~6.1% CAGR through their price advantage, the familiarity of the lid mechanism among Indian consumers from traditional pressure cooker usage, and the compact form factor appealing to smaller urban apartment kitchens. Commercial end-use grows at ~5.9% CAGR through India's rapidly expanding cloud kitchen sector and QSR adoption of air fryers for healthier snack preparation.

Executive Summary

India air fryer market reached USD 48.8 Million in 2025, representing one of the fastest-growing premium small kitchen appliance categories in India's consumer electronics market. An air fryer is a countertop cooking appliance that circulates hot air at high velocity around food using rapid air technology or an equivalent mechanism, cooking food with less oil than conventional deep frying while achieving similar crispness and texture. In the Indian market context, the air fryer's primary commercial appeal is the ability to prepare traditional Indian oil-intensive snacks and dishes with dramatically reduced oil consumption. The market is projected to reach USD 80.6 Million by 2034.

Drawer-type air fryers at 64.8% lead through ergonomic pull-out basket design that allows continuous food monitoring without removing the basket, compatibility with a wider range of cooking vessel shapes. Residential end-use at 79.2% dominates through the product's primary positioning as a home cooking health appliance. North India at 30.8% leads through Delhi-NCR's affluent urban consumer concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Drawer - 64.8% share (2025) |

|

Dominant End Use |

Residential - 79.2% market share (2025) |

|

Leading Region |

North India - 30.8% share |

|

Market Opportunity |

BIS certification driving quality compliance; cloud kitchen commercial adoption; D2C health-food brand bundling; smart connected air fryer IoT features; Tier-2 and Tier-3 city first-time buyer penetration |

Key Analytical Observations Supporting the Above Data:

- Drawer type at 64.8%: The drawer type is dominant due to its compact design, easy handling, quick cleaning, and suitability for everyday household cooking. Its affordability and convenience make it highly preferred among urban consumers.

- Residential end-use at 79.2%: The residential segment dominates due to the growing adoption of healthy cooking practices and increasing demand for convenient kitchen appliances among households. Rising disposable incomes, urbanization, and the popularity of home-cooked meals further support segment growth.

- North India at 30.8%: North India is dominant in the market due to higher urban household penetration, rising disposable incomes, and strong demand for modern kitchen appliances in cities such as Delhi-NCR, Chandigarh, Jaipur, and Lucknow. Growing health awareness and preference for low-oil cooking further support regional demand.

India Air Fryer Market Overview

India air fryer market occupies a distinctive commercial position within India's small kitchen appliance sector, the air fryer being simultaneously a health appliance, a cooking appliance, a technology appliance, and an aspirational lifestyle appliance in the Indian consumer's perception.

The air fryer ecosystem in India integrates component importers and domestic manufacturers, brand owners, Indian distribution channels, and India-specific content creators whose organic content drives the majority of first-time air fryer purchase intent in India's urban middle-class market. Macroeconomic factors include rising disposable incomes, rapid urbanization, expanding middle-class households, and growing e-commerce penetration.

Market Dynamics

To evaluate market opportunities, Request Sample

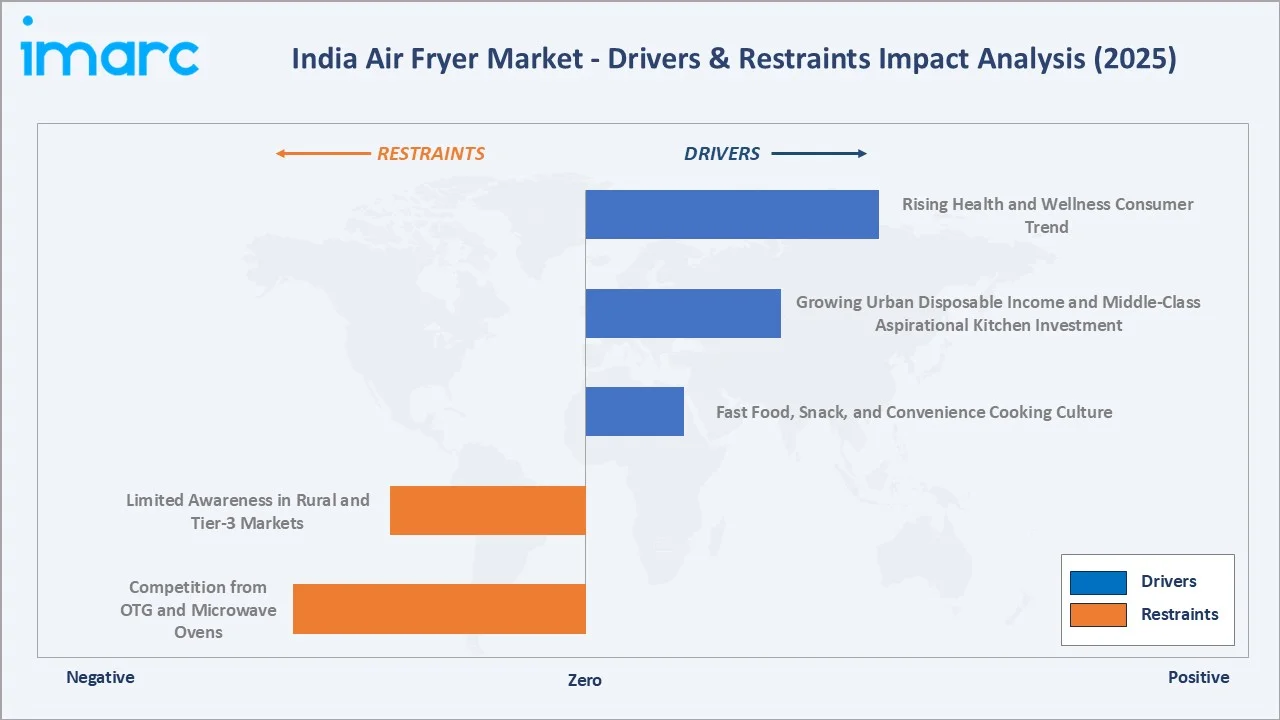

Market Drivers

- Rising Health and Wellness Consumer Trend: The rising health and wellness trend is increasingly reducing oil intake and shifting toward healthier cooking methods. Air fryers use hot air circulation to prepare fried-style foods with little to no oil, making them attractive for health-conscious households. In India, 89.8 million adults (20–79 years) have diabetes, in India and it is expected to reach 156.7 million adults by 2050. Additionally, 40% of women and 12% of men are abdominally obese in India. These rising concerns over obesity, diabetes, and lifestyle diseases are further encouraging adoption. This trend is especially strong among urban consumers seeking convenient yet healthier cooking appliances.

- Growing Urban Disposable Income and Middle-Class Aspirational Kitchen Investment: Growing urban disposable income is enabling Indian households to spend more on premium and convenience-based kitchen appliances. By 2030, India is expected to add about 75 million middle-class and 25 million rich households. This expanding middle class is increasingly investing in modern, aspirational products that improve cooking efficiency and lifestyle quality. Air fryers appeal to these consumers as they combine health, convenience, and smart kitchen functionality. Rising nuclear families and busy urban lifestyles further support their adoption.

- Fast Food, Snack, and Convenience Cooking Culture: Fast food, snack, and convenience cooking culture is driving the market as consumers seek quick ways to prepare fries, nuggets, cutlets, samosas, and other snacks at home. Air fryers offer faster cooking with less oil, making them suitable for busy urban households. The growing preference for ready-to-cook and frozen snacks further supports demand. This makes air fryers popular among families looking for convenient yet healthier snack preparation.

Market Restraints

- Limited Awareness in Rural and Tier-3 Markets: Limited awareness in rural and tier-3 markets is hampering the market, as many consumers are unfamiliar with its usage, benefits, and cooking applications. Traditional cooking habits and lower exposure to modern kitchen appliances reduce adoption. Higher upfront costs also make air fryers less attractive in price-sensitive markets. As a result, demand remains concentrated mainly in urban and semi-urban households.

- Competition from OTG and Microwave Ovens: Competition from oven, toaster, and grill (OTG) and microwave ovens is hampering the market as many households already use these appliances for baking, grilling, reheating, and snack preparation. Since microwaves and OTGs offer multi-purpose cooking functions, consumers may delay or avoid purchasing a separate air fryer. Price-sensitive buyers often prefer appliances with broader utility. This limits air fryer adoption, especially among first-time modern kitchen appliance buyers.

Market Opportunities

- Cloud Kitchen and Dark Kitchen Commercial Sector: Cloud kitchens and dark kitchens are increasing demand for compact, fast, and efficient cooking equipment. Air fryers help these kitchens prepare snacks, fries, and appetizers with lower oil usage and consistent quality. Their small footprint suits space-constrained commercial kitchens. Growing online food delivery further supports adoption among small foodservice operators.

- Smart Connected Air Fryer with IoT Features and App Integration: Smart connected air fryers with IoT features and app integration are appealing to tech-savvy urban consumers. These appliances allow remote control, preset cooking modes, recipe guidance, and cooking notifications through smartphones. Voice assistant compatibility and energy-monitoring features further enhance convenience. This supports premiumization and encourages consumers to upgrade from basic air fryer models.

Market Challenges

- Consumer Preference for Traditional Deep-Fried Food Taste: Consumer preference for traditional deep-fried food taste is a key challenge, as many consumers believe air-fried foods do not fully replicate the texture, aroma, and richness of conventionally fried dishes. Popular Indian snacks such as samosas, pakoras, and puris are often associated with deep frying. This perception can discourage first-time buyers and limit repeat usage. As a result, adoption remains slower among consumers who prioritize authentic taste over health benefits.

- Dependence on Electricity and Concerns Over Power Consumption: Dependence on electricity is challenging, as the appliance cannot be used during power cuts or in areas with unreliable electricity supply. Consumers may also worry about higher power consumption compared to gas-based cooking. In price-sensitive households, concerns over monthly electricity bills can reduce purchase interest. This limits adoption, especially in rural, semi-urban, and low-income consumer segments.

Emerging Market Trends

1. Indian Recipe Adaptation Creating a Country-Specific Air Fryer Usage Culture

Indian recipe adaptation is emerging as consumers use air fryers to prepare samosas, pakoras, tikkis, kebabs, roasted makhana, and paneer snacks with less oil. Brands and influencers are also promoting India-specific recipes and preset cooking modes. This is helping consumers see air fryers as suitable for everyday Indian cooking, not just Western snacks. As a result, air fryer usage is becoming more localized and culturally relevant in Indian households.

2. D2C Brand Disruption Challenging Established Appliance Brand Hierarchy

D2C brand disruption is emerging as digital-first brands offer affordable, stylish, and feature-rich models directly through online channels. These brands use social media, influencer marketing, discounts, and customer reviews to quickly build visibility. This is challenging established appliance brands that traditionally relied on offline retail strength. As a result, competition is intensifying, especially in the mid-range and value-for-money air fryer segments.

3. Premiumization and Multi-Function Convergence in Urban Premium Segment

Premiumization and multi-function convergence are emerging as urban consumers prefer air fryers with baking, roasting, grilling, reheating, dehydrating, and smart preset functions. Premium models offer larger capacity, digital controls, app connectivity, advanced air circulation technology, and sleek designs. In December 2025, Crompton expanded its appliances portfolio with the launch of the Ameo Air Fryer series in India. The new range is designed to prepare crispy and flavourful meals with less oil, reduced mess, and greater convenience for busy households. Its advanced air circulation technology supports healthier snacking and family cooking while retaining taste and nutrition with quiet operation. This allows air fryers to compete with OTGs and microwaves as versatile kitchen appliances. The trend is stronger among affluent urban households seeking convenience, health, and modern kitchen aesthetics.

4. Regional Cuisine Expansion Driving Category Penetration Beyond North Indian Snack Applications

Regional cuisine expansion is emerging as consumers are using air fryers beyond North Indian snacks like samosas, pakoras, and tikkis. Air fryers are increasingly being adapted for South Indian, western, eastern, and coastal recipes such as cutlets, kebabs, roasted snacks, fish, and vegetable dishes. This broadens usage occasions across Indian households. As a result, the category is gaining relevance beyond a limited snack-focused appliance.

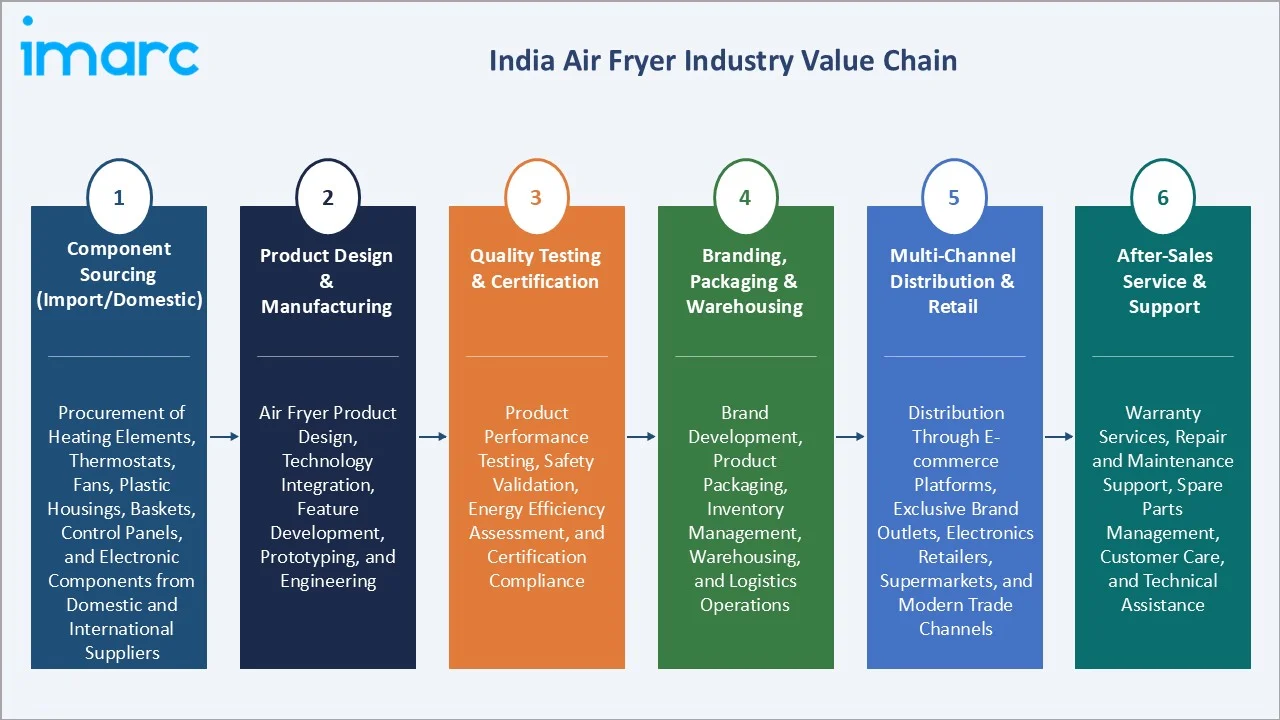

Industry Value Chain Analysis

India air fryer value chain operates primarily through import-dependent assembly and branding. An estimated 75-85% of India air fryer component value is imported, with India contributing primarily to final assembly, branding, quality testing, distribution, and after-sales service as the domestically created value chain stages.

|

Stage |

Key Participants |

|

Component Sourcing (Import/Domestic) |

Procurement of heating elements, thermostats, fans, plastic housings, baskets, control panels, and electronic components from domestic and international suppliers |

|

Product Design & Manufacturing |

Air fryer product design, technology integration, feature development, prototyping, and engineering |

|

Quality Testing & Certification |

Product performance testing, safety validation, energy efficiency assessment, and certification compliance |

|

Branding, Packaging & Warehousing |

Brand development, product packaging, inventory management, warehousing, and logistics operations |

|

Multi-Channel Distribution & Retail |

Distribution through e-commerce platforms, exclusive brand outlets, electronics retailers, supermarkets, and modern trade channels |

|

After-Sales Service & Support |

Warranty services, repair and maintenance support, spare parts management, customer care, and technical assistance |

The distribution stage is the India air fryer value chain's most commercially contested phase, e-commerce versus modern trade retail versus general trade, creating three simultaneous distribution battlegrounds where different brands have different competitive strengths and market access effectiveness.

Technology Landscape in the India Air Fryer Industry

Rapid Air Circulation Technology

Rapid air circulation technology enables faster and more even cooking with minimal oil. It uses high-speed hot air movement to create crispy textures similar to deep frying while reducing oil consumption. In November 2025, Nuuk launched its latest product lineup in collaboration with filmmaker Karan Johar, featuring the Nuuk BRĪSK Air Fryer. Designed for modern Indian kitchens, it uses proprietary 360° Rapid Air Circulation technology to cook food evenly and up to 30% faster. This technology improves cooking efficiency, taste consistency, and convenience for Indian snacks and daily meals.

Smart Connectivity and AI Recipe Technology

Smart connectivity and AI recipe technology enable app-based control, remote monitoring, and personalized cooking experiences. AI-powered systems can recommend recipes, automatically adjust cooking settings, and provide real-time cooking guidance based on the selected dish. Integration with smartphones and voice assistants enhances user convenience and accessibility. These features are driving demand for premium air fryers among tech-savvy urban consumers seeking smarter kitchen solutions.

Non-Stick Coating and Food Safety Technology

Non-stick coating and food safety technology are improving the ease of cooking, cleaning, and product durability. Manufacturers are increasingly using food-grade coating materials to address consumer concerns regarding health and safety. Advanced coatings also prevent food from sticking and reduce the need for additional oil. These innovations enhance user experience and support the growing demand for healthier and safer cooking appliances.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Drawer |

64.8% |

2025 |

|

Technology |

🔒 |

🔒 |

2025 |

|

Sales Channel |

🔒 |

🔒 |

2025 |

|

End Use |

Residential |

79.2% |

2025 |

|

Region |

North India |

30.8% |

2025 |

By Product Type

Drawer leads at 64.8% (2025). The drawer type segment encompasses the full price range from entry-level through mainstream to premium, capturing India's widest consumer income range in air fryers. Drawer type's ~5.2% CAGR reflects mature category establishment with growth driven by premium dual-zone and large-capacity innovation.

To access detailed market analysis, Request Sample

Lid type at 35.2% grows fastest at ~6.1% CAGR through the budget segment's above-market growth as Tier-2 and Tier-3 city e-commerce penetration expands India's addressable air fryer market below the price threshold, where drawer type's lowest-priced models compete.

By End Use

Residential leads at 79.2% (2025). India residential air fryer market is predominantly driven by urban households. Residential's ~5.4% CAGR reflects broad-based urban middle-class income growth driving upgrade and first-time purchase.

Commercial at 20.8% grows at ~5.9% CAGR through cloud kitchen expansion and QSR chain modernization. India's cloud kitchens, corporate cafeteria health food program adoption, and hospital and healthcare food service dietary management collectively create structured above-residential commercial growth.

Regional Market Insights

|

Region |

Share (2025) |

Key India Air Fryer Market Drivers & Characteristics |

|

North India |

30.8% |

Driven by high urbanization, rising disposable incomes, and strong adoption of modern kitchen appliances. |

|

South India |

27.6% |

Driven by strong consumer spending power, high penetration of premium home appliances, and increasing preference for healthy cooking alternatives. |

|

West India |

23.4% |

Supported by affluent urban consumers, expanding middle-class households, and a well-developed retail ecosystem. |

|

East India |

18.2% |

Supported by improving household incomes, expanding urban centers, and growing awareness of healthy cooking methods. |

North India's 30.8% market leadership reflects Delhi-NCR's status as India's most affluent and most health-conscious urban consumer market. South India, at 27.6%, is powered by Bengaluru's tech professional consumer base and Kerala's NRI-influenced premium appliance adoption.

West India, at 23.4%, is anchored by Mumbai's food culture diversity and Gujarat's health-conscious traditional snack adaptation. East India, at 18.2%, represents India's highest-potential growth region with the lowest current penetration, creating the most commercially compelling untapped opportunity.

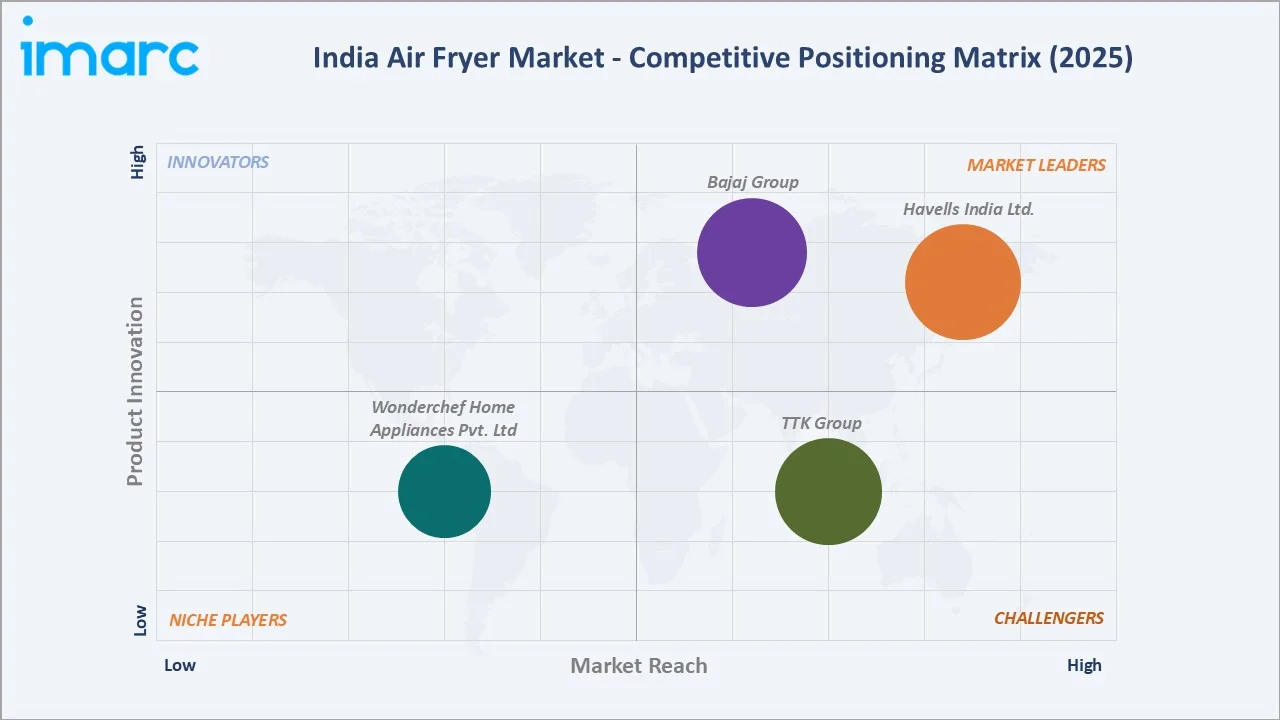

Competitive Landscape

India air fryer market competitive landscape is transitioning from a two-brand premium market toward a multi-tier competitive structure encompassing international premium brands, domestic established appliance brands, and India-specific D2C e-commerce brands competing across distinct price tiers with different distribution models and marketing approaches.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Havells India Ltd. |

Prolife Vista Digital Air fryer, Prolife Stellar Chef Digital Air fryer, Prolife Vista Air Fryer, Prolife Neo Air Fryer |

Market Leader |

Havells India Ltd plays a significant role in the India air fryer market, positioning itself as a premium yet accessible brand focusing on healthy cooking technology and user convenience. |

|

Bajaj Group |

Morphy Richards 5L Classic Air Fryer BL, Morphy Richards 5L Crisp Pro Digital Blue Air Fryer, Morphy Richards DuoCrisp 9L Air Fryer |

Market Leader |

The Bajaj Group, specifically through its consumer electrical arm Bajaj Electricals Ltd, plays a significant role in the India air fryer market by manufacturing, selling, and distributing affordable, durable, and energy-efficient kitchen appliances tailored for Indian cooking habits. |

|

TTK Group |

Prestige Nutrifry Electric Air Fryer, Prestige PAF 6.0 Electric Air Fryer, Prestige Air Fryer PAF 4.0, Prestige Crysta Digital Electric Air Fryer |

Strong Challenger |

TTK Group, primarily through its flagship brand TTK Prestige, plays a significant role in the India air fryer market by focusing on healthy cooking, innovative design, and family-sized capacities tailored for Indian cuisine. |

|

Wonderchef Home Appliances Pvt. Ltd |

Neo Pro Digital Air Fryer, Platinum Digital Air Fryer, Regalia Digital Air Fryer, Swift Digital Air Fryer with Window |

Niche Player |

Wonderchef Home Appliances Pvt. Ltd is a major player in the India air fryer market, specializing in accessible, healthy-cooking appliances with Rapid Air Technology that use less oil. |

The competitive landscape's most commercially significant dynamics are the D2C brand challenge to established brands' market share. International brand aspiration is creating a distinct premium import segment that domestic brands cannot address through price competition alone, requiring Indian brands to invest in product innovation and design quality to compete above the international prestige differential.

Key Company Profiles

Havells India Ltd.

Havells India Ltd. is a leading Indian consumer electrical and home appliance company with a strong presence in the India air fryer market. The company offers a range of air fryer models featuring technologies such as Aero Crisp air circulation, digital controls, and large-capacity cooking baskets to cater to health-conscious consumers.

- Key Products: Prolife Vista Digital Air fryer, Prolife Stellar Chef Digital Air fryer, Prolife Vista Air Fryer, Prolife Neo Air Fryer.

- Strategic Focus: Focuses on innovative, energy-efficient air fryers with smart controls and rapid air circulation technology to meet India’s rising demand for healthy and convenient cooking appliances.

Bajaj Group

Bajaj Group, through its consumer appliances business, Bajaj Electricals, is a prominent player in the India air fryer market, offering a range of air fryers designed for healthy and convenient cooking. The company provides products with features such as rapid air technology, digital controls, multiple cooking presets, and energy-efficient operation to cater to evolving consumer preferences.

- Key Products: Morphy Richards 5L Classic Air Fryer BL, Morphy Richards 5L Crisp Pro Digital Blue Air Fryer, Morphy Richards Duocrisp 9L Air Fryer.

- Recent Developments: In March 2026, Bajaj Electricals signed a definitive agreement to acquire the intellectual property rights of Morphy Richards in India and select South Asian markets for ₹141.4 crore.

- Strategic Focus: Offering affordable, feature-rich air fryers with rapid air technology and user-friendly designs, while leveraging its extensive distribution network to expand penetration among health-conscious and value-driven consumers across India.

Market Concentration Analysis

India air fryer market is moderately concentrated. Market concentration is increasing at the premium tier, while the mid-market is becoming more fragmented through D2C brand proliferation. BIS mandatory certification has created a quality barrier, reducing the extremely low-end segment, while the brand middle has expanded through new market entrants. Geographic concentration is the most commercially distinctive feature of India air fryer market structure. The e-commerce channel's progressive geographic expansion is the primary mechanism by which air fryer market geographic concentration will reduce through 2034, as first-time buyers in smaller cities access product range and pricing that physical retail availability had previously withheld.

Investment & Growth Opportunities

Highest Growth Segments

Lid type (~6.1% CAGR), commercial end-use (~5.9% CAGR through cloud kitchen and QSR adoption), smart connected premium segment (~8-10% CAGR from small base), East India regional market (~7-8% CAGR from low penetration base), Gujarat-specific health snack segment (~7% CAGR through vegetarian traditional snack adaptation), and large-capacity dual-zone premium segment (~8% CAGR through urban premium household kitchen upgrade) represent India highest-growth air fryer investment vectors through 2034.

Emerging Investment Opportunities

India's cloud kitchen sector expansion represents the most commercially concentrated air fryer growth opportunity. Commercial air fryer product development targeting India's cloud kitchen operators through Swiggy and Zomato platform partner programs creates structured commercial channel access that residential retail distribution cannot serve.

Investment Themes

- Make in India air fryer component manufacturing, reducing import dependency and creating domestic value creation: India's import duty on finished air fryer products creates a price cost disadvantage for imported product brands versus domestic assembly that domestic manufacturers exploit through lower landed cost.

- Regional language content and Tier-2/3 city marketing creating below-metro market penetration above national advertising: India's Tier-2 and Tier-3 cities collectively represent urban consumers with below-national air fryer penetration but above-average growth in disposable income and e-commerce adoption. Regional language air fryer recipe content reaches regional language-dominant consumers, where Hindi-English air fryer content does not convert, creating above-return-on-investment brand awareness investment for brands willing to create regional content above national language advertising.

Future Market Outlook (2026-2034)

India air fryer market is projected to grow from USD 48.8 Million in 2025 to USD 80.6 Million by 2034, delivering a 5.57% CAGR over the forecast period. The market's anchor value of USD 64.0 Million in 2030 represents the Indian air fryer industry at its most commercially dynamic inflection. Tier-2 and Tier-3 city e-commerce penetration will have created first-time air fryer access for millions of households previously without physical retail access to the product, cloud kitchen commercial adoption will have created India's largest commercial air fryer installed base, and BIS quality market consolidation will have concentrated market growth in certified brands above the grey-import competition that suppressed brand value creation in the pre-2023 market.

Three structural forces define India air fryer market growth through 2034 with confidence. India's demographic dividend's income progression creates the most commercially significant expansion of air fryers' addressable market in any single national market globally, as annual household income growth progressively moves Tier-2 and Tier-3 city households above the air fryer purchase threshold. India's e-commerce infrastructure maturation. India's health consciousness trend's structural permanence.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders (2025), including Product Directors; Category Heads; Founders; retail category managers; cloud kitchen operators; and industry association representatives.

Secondary Research

Secondary research encompassed small appliance certification database; industry data report; India consumer electronics market data; India bestseller rank historical data for air fryer category; Flipkart category insights kitchen appliance report; company annual reports; India air fryer search data; Indian air fryer recipe content analytics. Over 45 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using household penetration model: (i) India urban household count by income segment multiplied by air fryer adoption probability curve at each income bracket; (ii) commercial segment modelled from cloud kitchen count projection multiplied by average air fryer per cloud kitchen; (iii) average revenue per unit calculated from product mix shift applied to product category average selling price trajectory assuming continued moderate price decline from BIS quality market consolidation.

India Air Fryer Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Drawer, Lid |

| Technologies Covered | Digital, Manual |

| Sales Channels Covered | Supermarkets/Hypermarkets, Multi-Branded Stores, Exclusive Stores, Online, Others |

| End Uses Covered | Residential, Commercial |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Havells India Ltd., Bajaj Group, TTK Group, Wonderchef Home Appliances Pvt. Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India air fryer market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India air fryer market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India air fryer industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Air Fryer Market Report

India air fryer market reached USD 48.8 Million in 2025, driven by rising health awareness, growing demand for low-oil cooking, and increasing adoption of modern kitchen appliances. Urbanization, higher disposable incomes, busy lifestyles, and expanding e-commerce channels are further boosting product demand.

India air fryer market grows at 5.57% CAGR during 2026-2034, reaching USD 80.6 Million by 2034. The overall market growth is sustained by India's rising urban middle-class income, e-commerce geographic penetration reaching Tier-2/3 cities, post-COVID sustained health consciousness, and a BIS quality market, creating consumer confidence in certified products.

Drawer leads at 64.8% through ergonomic pull-out basket design aligned with international brand product range standards, superior Indian cooking application compatibility requiring constant food monitoring and shaking, and the complete price range premium capturing India's widest appliance buyer spectrum.

Residential leads at 79.2% through the air fryer's primary positioning as a personal health appliance for urban household cooking oil reduction and Indian snack healthification.

North India leads at 30.8% through Delhi-NCR's status as India's most affluent urban consumer market with the highest concentration of SEC-A and SEC-B households, Punjab's above-national income and strong home cooking culture, and North India's high social media engagement, driving the fastest health appliance trend adoption.

Leading companies include Havells India Ltd., Bajaj Group, TTK Group, and Wonderchef Home Appliances Pvt. Ltd., among others.

India air fryer market is projected to reach approximately USD 64.0 Million by 2030, with Tier-2 and Tier-3 city household penetration growth through e-commerce maturation, commercial cloud kitchen segment growth, smart connected air fryer mainstream availability, and India-specific Make in India air fryer assembly.

India's cloud kitchen sector is the most commercially significant emerging driver of India's commercial air fryer segment. Cloud kitchen operators use an air fryer as the primary cooking equipment for appetiser, starter, and snack menu items, where the air fryer's compact footprint, fast heating, and oil-free cooking align with cloud kitchen's small-space, health-positioning, and high-throughput operational requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)