India Aquafeed Market Size, Share, Trends and Forecast by Species, Ingredients, Additives, Product Form, and Region, 2026-2034

India Aquafeed Market Summary:

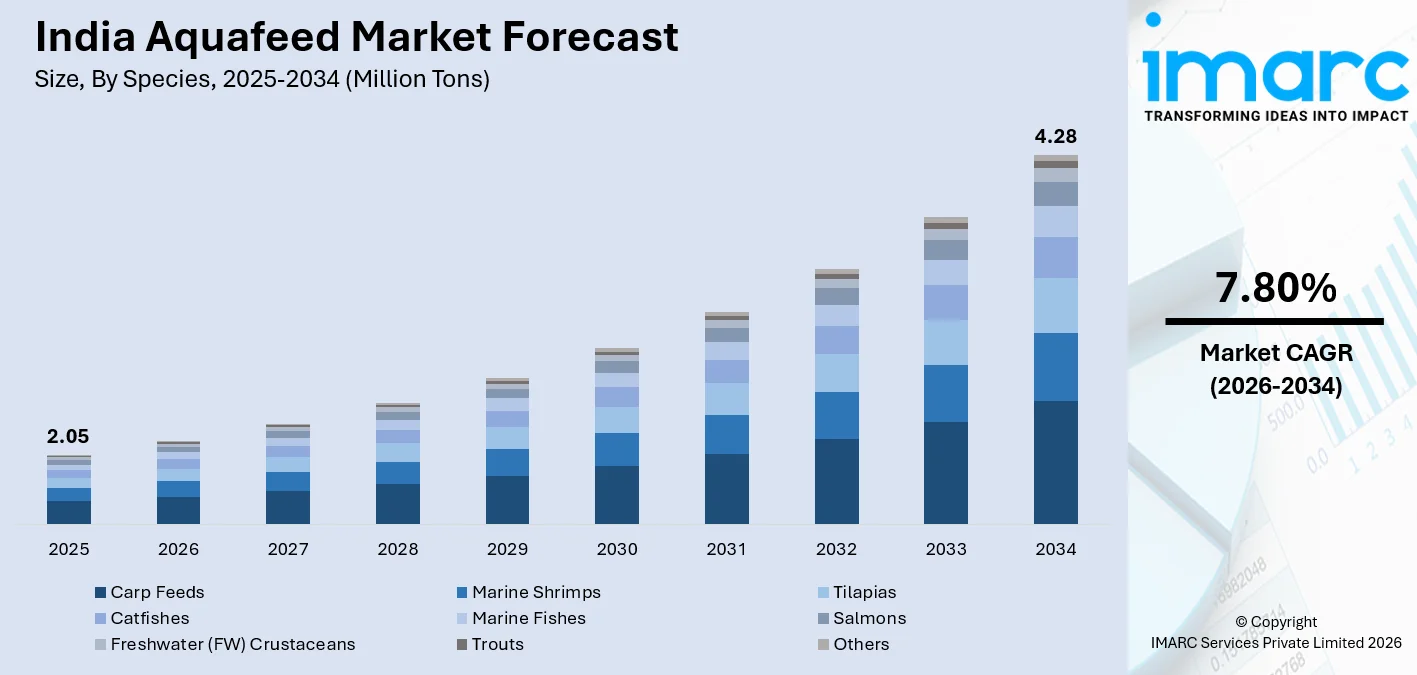

The India aquafeed market size reached 2.05 Million Tons in 2025 and is projected to reach 4.28 Million Tons by 2034, growing at a compound annual growth rate of 7.80% from 2026-2034.

The market is driven by rising demand for high-quality seafood, expanding aquaculture practices, and growing emphasis on sustainable fish farming. Government support for fisheries development and advancements in feed formulation is accelerating adoption nationwide. Increasing farmer awareness about the nutritional benefits of scientifically formulated feeds continues to boost consumption across freshwater and coastal systems. The expanding inland and coastal aquaculture sectors, combined with growing processed seafood exports, continue to reinforce strong momentum across the India aquafeed market share.

Key Takeaways and Insights:

- By Species: Carp feeds dominate the market with a share of 58.5% in 2025, driven by the widespread prevalence of carp aquaculture in freshwater farming systems and strong consumer preference for carp species in domestic food consumption.

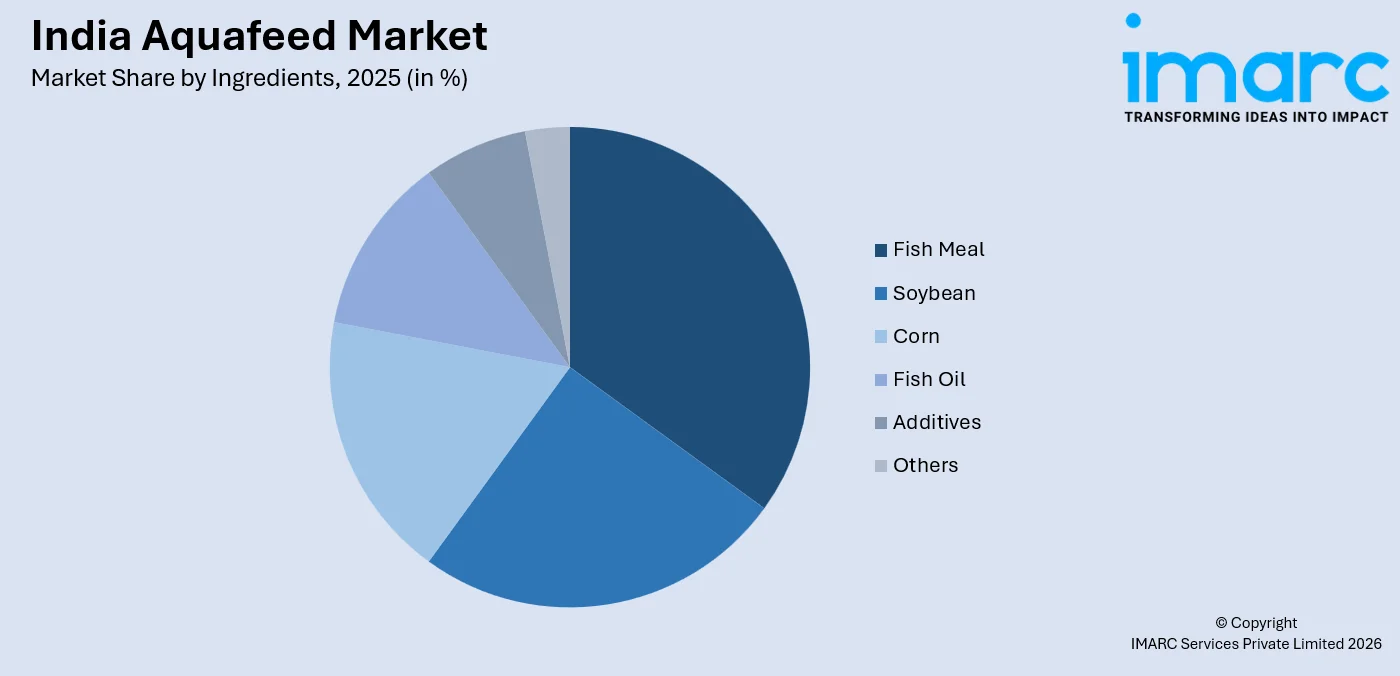

- By Ingredients: Fish meals lead the market with a share of 27.5% in 2025, owing to its superior amino acid profile, high digestibility, and well-established role as a primary protein source in formulated aquafeeds.

- By Additives: Vitamins and minerals represent the largest segment with a market share of 33.0% in 2025, as these micronutrients are essential for immune function, skeletal development, and overall performance optimization across commercially farmed aquatic species.

- By Product Form: Pellets dominate the market with a share of 48.0% in 2025, owing to fish farmers for ease of handling, reduced feed wastage, and compatibility with mechanized feeding systems across freshwater and marine aquaculture operations.

- By Region: East India leads the market with a share of 35.0% in 2025, driven by an extensive network of rivers, ponds, and water bodies, alongside a deeply rooted aquaculture tradition across its key farming states.

- Key Players: The India aquafeed market features a moderately consolidated competitive landscape, with both domestic manufacturers and international feed producers actively expanding their footprint. Players are focusing on product innovation, nutrient optimization, and geographic reach to capture growing farmer demand across freshwater and marine aquaculture segments. Some of the key players operating in the market include Avanti Feeds Limited, Godrej Agrovet Limited, Growel Feeds Pvt. Ltd, Happy Feeds, IB Group, IFB Agro Industries Limited, Skretting India, Sreema’s Feeds, and UNO Feeds.

To get more information on this market Request Sample

India's aquafeed market is experiencing robust expansion, propelled by several converging forces reshaping the aquaculture industry. The country's growing population, with its heightened appetite for protein-rich seafood, is creating sustained downstream demand for commercially farmed fish and shrimp. In February 2025, Aqua Bridge Group launched a new intensive aquaculture farm and research centre in Unnao, Uttar Pradesh, which includes a one‑million‑tonne aquafeed plant aimed at sustainable feed solutions and farmer training, reflecting rising private sector investment in feed infrastructure. Simultaneously, government-backed fisheries development programs are encouraging smallholder farmers to adopt scientifically formulated feeds in place of traditional feeding methods. Advances in feed technology, including improved palatability, digestibility profiles, and nutrient bioavailability, are enabling better feed conversion ratios and faster growth cycles across diverse farmed species. The increasing push toward export competitiveness is compelling producers to consistently upgrade feed quality standards.

India Aquafeed Market Trends:

Shift Toward Nutritionally Optimized and Species-Specific Feeds

Aquafeed manufacturers in India are increasingly moving away from generalized formulations toward species-specific feeds tailored to the unique nutritional requirements of carp, shrimp, tilapia, and other commercially farmed species. This trend reflects a deeper understanding among fish farmers of how targeted nutrition improves growth performance and disease resistance. In February 2025, Insectika Biotech launched insect protein-based feeds YuM ToM and Yum Pro for Asian seabass and aquarium fish at the Shrimp Farmers Conclave in Odisha, engaging over 500 farmers and government officials to promote species-specific, sustainable nutrition. The incorporation of functional ingredients such as probiotics, prebiotics, and immunostimulants into feed formulations is gaining traction, as farmers seek to reduce dependency on antibiotics and enhance fish health outcomes in a more sustainable and commercially viable manner.

Rising Adoption of Sustainable and Alternative Protein Ingredients

With growing pressure on traditional marine-sourced ingredients, aquafeed producers in India are actively exploring alternative protein sources including soy protein concentrates, insect-based meals, and single-cell proteins. In September 2025, Bangalore‑based insect biotech Loopworm secured regulatory approval from the Coastal Aquaculture Authority of India to supply its insect‑derived protein and fat products directly as additives and attractants in aquaculture nutrition, underscoring industry shifts toward sustainable protein alternatives. This shift is being driven by the need to reduce the ecological footprint of aquafeed production while maintaining high nutritional standards. Plant-based and fermented protein ingredients are being increasingly incorporated into feed matrices, particularly for herbivorous and omnivorous species.

Integration of Advanced Feed Technology and Precision Nutrition

Technological advancements in feed manufacturing, including extrusion technology and micro-encapsulation, are enhancing the stability, bioavailability, and palatability of aquafeeds across Indian production facilities. In September 2025, dsm‑firmenich unveiled a state-of-the-art feed additive facility in Jadcherla, Telangana, equipped with advanced technology to produce additives that improve pellet stability, nutrient bioavailability, and overall feed quality for Indian aquaculture producers. Precision nutrition approaches, supported by data on species-specific metabolic requirements, are enabling manufacturers to optimize ingredient inclusion rates and reduce feed waste. There is also a growing focus on water stability of feeds, which is particularly important in Indian pond-based farming systems.

Market Outlook 2026-2034:

The India aquafeed market is poised for sustained growth over the forecast period, underpinned by increasing aquaculture output, expanding domestic seafood consumption, and a favorable policy environment. Revenue is expected to witness consistent upward movement as fish farming transitions toward commercially optimized operations. Rising investments in hatchery infrastructure, expanding cold chain networks, and growing participation of organized players are expected to catalyze market development, positioning the sector for strong revenue performance through the forecast period. The market size was estimated at 2.05 Million Tons in 2025 and is expected to reach 4.28 Million Tons by 2034, reflecting a compound annual growth rate of 7.80% over the forecast period 2026-2034.

India Aquafeed Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Species |

Carp Feeds |

58.5% |

|

Ingredients |

Fish Meal |

27.5% |

|

Additives |

Vitamins and Minerals |

33.0% |

|

Product Form |

Pellets |

48.0% |

|

Region |

East India |

35.0% |

Species Insights:

- Carp Feeds

- Marine Shrimps

- Tilapias

- Catfishes

- Marine Fishes

- Salmons

- Freshwater (FW) Crustaceans

- Trouts

- Others

Carp feeds dominate with a market share of 58.5% of the total India aquafeed market in 2025.

Carp feeds represent the dominant segment within the India aquafeed market, reflecting the deep entrenchment of carp aquaculture across the country's freshwater farming landscape. In February 2025, the ICAR‑Central Institute of Fisheries Education (ICAR‑CIFE) partnered with M.M. Fish Seed Cultivation Pvt. Ltd. to commercialize ‘ICAR‑CIFE‑Pangas‑Shakti’, a specialized grow‑out feed for freshwater catfish, enhancing access to scientifically developed feeds for inland aquaculture farmers. The widespread farming of rohu, catla, and common carp across semi-intensive pond systems has created consistent and large-scale demand for specially formulated carp feeds.

This segment is the backbone of the Indian market due to the presence of conducive factors for the breed’s reproduction and its adaptability to various types of water. Additionally, the Indian market’s demand for the breed is also significant. The accessibility of the carp farming sector to small and marginal farmers has been responsible for the wide geographic distribution of the carp feed market. With the shift of farmers towards scientifically formulated nutrition programs, the the market is still attracting manufacturer investments.

Ingredients Insights:

Access the comprehensive market breakdown Request Sample

- Soybean

- Corn

- Fish Meal

- Fish Oil

- Additives

- Others

Fish meal leads with a share of 27.5% of the total India aquafeed market in 2025.

Fish meal holds the leading position within the ingredients segment of the India aquafeed market, valued for its exceptional nutritional density and well-established efficacy across a wide range of farmed species. Its superior amino acid profile, high digestibility, and rich concentration of essential fatty acids make it the preferred primary protein source in high-performance aquafeed formulations. Shrimp and marine fish producers rely heavily on fish meal inclusion to achieve the growth rates and feed conversion efficiencies demanded by export-oriented aquaculture operations across coastal farming regions.

The consistent demand for fish meals can be attributed to the proven success of fish meals in ensuring productivity gains at the farm level. While the search for new protein sources gains traction, fish meals maintain their competitive edge over other ingredients because of the mouth appeal and bioavailability advantage it provides across a range of species. Fish meal remains a popular choice in premium feed formulations aimed at performance-sensitive aquaculture species. Its essential role in shrimp and marine fish feeds ensures the foundation of the ingredients segment remaining with fish meal.

Additives Insights:

- Vitamins and Minerals

- Antioxidants

- Feed Enzymes

- Others

Vitamins and minerals exhibit a clear dominance with a 33.0% share of the total India aquafeed market in 2025.

Vitamins and minerals represent the leading category within the additives segment, reflecting their foundational and non-negotiable importance in commercially produced aquafeeds. These micronutrients play an essential role in supporting immune defense mechanisms, skeletal formation, enzyme function, and reproductive health across a broad spectrum of farmed aquatic species. As per sources, Alltech launched Bioplex® Aqua Boost, a chelated mineral and trace‑mineral premix designed for Indian aquaculture that enhances solubility and bioavailability of key minerals for fish and shrimp health and performance. Micronutrient inclusion is essential, as deficiencies reduce growth, increase disease susceptibility, and elevate mortality, undermining aquaculture profitability.

Demand for vitamins and minerals within aquafeed formulations is further driven by the need to compensate for micronutrient losses that occur during feed processing, pelleting, and extended storage periods. As aquaculture operations intensify and stocking densities increase, the nutritional demands on individual fish and shrimp also rise, making adequate micronutrient supplementation even more critical. Feed manufacturers are increasingly developing advanced premix solutions that combine targeted vitamin and mineral blends to address species-specific deficiencies, reinforcing the segment's dominant position within the India aquafeed additives landscape.

Product Form Insights:

- Pellets

- Extruded

- Powdered

- Liquid

Pellets leads with a market share of 48.0% of the total India aquafeed market in 2025.

Pellets dominate the segment of the India aquafeed market, representing the most widely adopted feed format across both freshwater pond systems and coastal aquaculture operations. Their structural integrity ensures that feed remains intact in water for adequate durations, significantly reducing nutrient leaching and improving overall feed utilization efficiency. The consistent size and density of pellets make them compatible with mechanized and automated feeding systems, which are increasingly being adopted by organized aquaculture producers seeking to optimize labor efficiency and minimize feed wastage across large-scale farming operations.

The broad adoption of pellets spans the full spectrum of India's aquaculture sector, from smallholder carp farmers in East India to large commercial shrimp producers along the coastal belt. Pellets are available in a wide range of sizes and nutritional specifications, allowing manufacturers to cater to different species, life stages, and production systems within a single product category. Their ease of storage, transport, and on-farm handling further reinforces farmer preference for this format. These combined advantages firmly establish pellets as the leading and most commercially versatile product form within the India aquafeed market.

Regional Insights:

- North India

- West and Central India

- South India

- East India

East India dominates with a market share of 35.0% of the total India aquafeed market in 2025.

East India commands the largest regional share of the India aquafeed market, supported by an extensive network of rivers, floodplains, ponds, and reservoirs that provide ideal conditions for freshwater aquaculture. States within this region have long maintained a deeply rooted culture of fish farming, with carp polyculture systems forming the foundation of rural aquaculture livelihoods. The high density of fish farming households, combined with increasing adoption of commercially formulated feeds over traditional practices, ensures consistently strong and growing aquafeed consumption volumes across the region's diverse farming communities.

Beyond its structural advantages in water resource availability, East India benefits from active government investment in fisheries infrastructure, technical training programs, and input subsidy schemes that are encouraging farmers to upgrade their feeding practices. The region's proximity to major fish consumption markets further incentivizes commercial production, driving demand for performance-enhancing feeds. As organized aquaculture enterprises expand their presence in the region alongside established smallholder operations, the appetite for quality aquafeed products continues to grow, reinforcing

Market Dynamics:

Growth Drivers:

Why is the India Aquafeed Market Growing?

Rising Domestic Seafood Consumption and Protein Demand

India's expanding population and increasingly health-conscious consumer base are driving sustained growth in domestic seafood demand. According to reports, weekly fish consumption in India has climbed significantly, even in inland areas where it wasn’t traditionally a staple, driven by rising incomes, dietary shifts, and improved availability through aquaculture expansion. As dietary preferences shift toward lean, protein-rich food sources, fish and shrimp are gaining prominence across both urban and semi-urban households. This rising consumption appetite is creating consistent downstream pressure on aquaculture producers to scale output, which in turn drives higher volumes of commercially formulated aquafeed.

Government Initiatives and Fisheries Development Support

Sustained government commitment to strengthening India's fisheries and aquaculture sector is serving as a powerful structural growth driver for the aquafeed market. Policy frameworks focused on increasing fish production, enhancing rural farmer incomes, and promoting sustainable aquaculture practices are creating a supportive environment for feed adoption. Subsidies on feed inputs, institutional credit access, and organized technical extension services are reducing barriers for smallholder farmers transitioning to scientifically formulated feeds. Infrastructure investments in hatcheries, processing units, and distribution networks are simultaneously strengthening the supply chain foundations necessary to support expanding aquafeed demand nationwide.

Expansion of Inland and Coastal Aquaculture Operations

Continuous innovation in aquafeed formulation and manufacturing technology is directly expanding the market by improving the performance, efficiency, and accessibility of commercial feeds. Advances in extrusion processing, precision nutrition, and functional ingredient incorporation are enabling manufacturers to develop feeds with superior digestibility, enhanced palatability, and targeted health benefits. In September 2025, at AquaEx India 2025 in Bhimavaram, several Indian aquafeed firms and technology providers showcased next‑generation feed solutions, including species‑specific formulations and enhanced nutrient delivery systems, aimed at improving productivity and sustainability on local farms. These improvements are delivering measurable productivity gains at the farm level, encouraging wider adoption among farmers who previously relied on unformulated feeding practices.

Market Restraints:

What Challenges the India Aquafeed Market is Facing?

Volatility in Raw Material Availability and Pricing

The aquafeed market remains vulnerable to fluctuations in the availability and cost of key raw materials, particularly marine-sourced ingredients that are subject to seasonal supply variability and international market dynamics. These inconsistencies create pricing pressures that compress manufacturer margins and increase cost burdens on farmers, particularly smallholder operators with limited financial resilience, potentially discouraging adoption of commercially formulated feeds.

Limited Awareness and Adoption Among Smallholder Farmers

A significant proportion of India's fish farming community operates at subsistence or small scales, where awareness of scientifically formulated feeds remains limited. Many farmers continue relying on traditional or locally produced feeds that yield suboptimal results. Behavioral inertia, restricted access to technical advisory services, and upfront cost sensitivity collectively slow commercial aquafeed penetration in these segments, constraining overall market growth potential across non-organized farming communities.

Inconsistent Regulatory Standards and Quality Control Gaps

The absence of uniformly enforced quality standards governing aquafeed composition, labeling, and safety creates market distortions that hinder organized sector growth. The presence of substandard and unregistered feed products in local markets undermines farmer confidence and creates unfair competition for compliant manufacturers. Inconsistent regulatory enforcement across different states makes maintaining a level competitive playing field difficult, slowing the overall formalization and quality advancement of India's aquafeed market.

Competitive Landscape:

The India aquafeed market operates within a moderately competitive landscape characterized by the coexistence of large, organized manufacturers, regional feed producers, and emerging specialty players. Competition is driven by product quality, nutritional efficacy, pricing, and distribution reach across diverse geographies. Established players leverage established distribution networks and brand trust built through years of engagement with the aquaculture farming community. Meanwhile, newer entrants are differentiating through innovation in functional feed ingredients and species-specific formulations. The market rewards producers capable of balancing cost efficiency with nutritional performance, and the ability to serve both premium and value-oriented farmer segments is increasingly defining competitive positioning across the India aquafeed market.

Some of the key players include:

- Avanti Feeds Limited

- Godrej Agrovet Limited

- Growel Feeds Pvt. Ltd

- Happy Feeds

- IB Group

- IFB Agro Industries Limited

- Skretting India

- Sreema’s Feeds

- UNO Feeds

Recent Developments:

- In August 2025, IFB Agro Industries acquired Cargill India’s shrimp and freshwater fish feed business for Rs110 crore, including feed formulations, manufacturing units in Vijayawada and Rajahmundry, licenses, and staff. The move consolidates India’s aquafeed sector, expanding IFB’s production capabilities and market presence in the domestic aquaculture industry.

India Aquafeed Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Species Covered | Carp Feeds, Marine Shrimps, Tilapias, Catfishes, Marine Fishes, Salmons, Freshwater (FW) Crustaceans, Trouts, Others |

| Ingredients Covered | Soybean, Corn, Fish Meal, Fish Oil, Additives, Others |

| Additives Covered | Vitamins and Minerals, Antioxidants, Feed Enzymes, Others |

| Product Forms Covered | Pellets, Extruded, Powdered, Liquid |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | Avanti Feeds Limited, Godrej Agrovet Limited, Growel Feeds Pvt. Ltd, Happy Feeds, IB Group, IFB Agro Industries Limited, Skretting India, Sreema’s Feeds, UNO Feeds, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Aquafeed Market Report

The India aquafeed market reached a volume of 2.05 Million Tons in 2025.

The India aquafeed market is expected to grow at a compound annual growth rate of 7.80% from 2026-2034 to reach 4.28 Million Tons by 2034.

Carp feeds held the largest India aquafeed market share, driven by the dominant presence of freshwater carp aquaculture across East and Central India, strong domestic consumption of carp species, and the widespread availability of cost-effective carp-specific feed formulations.

Key factors driving the India aquafeed market include rising domestic seafood consumption, government support for fisheries development, growing adoption of scientific aquaculture practices, advances in feed technology, expanding inland aquaculture operations, and India's increasing role as a global seafood exporter.

Major challenges include raw material price volatility impacting feed affordability, limited commercial feed adoption among small-scale farmers, regulatory inconsistencies in feed quality standards, dependence on imported marine ingredients, and gaps in rural distribution infrastructure across non-traditional aquaculture regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade