Aquaculture Market Size, Share, Trends and Forecast by Fish Type, Environment, Distribution Channel, and Region, 2026-2034

Aquaculture Market Size, Share, Trends & Forecast (2026-2034)

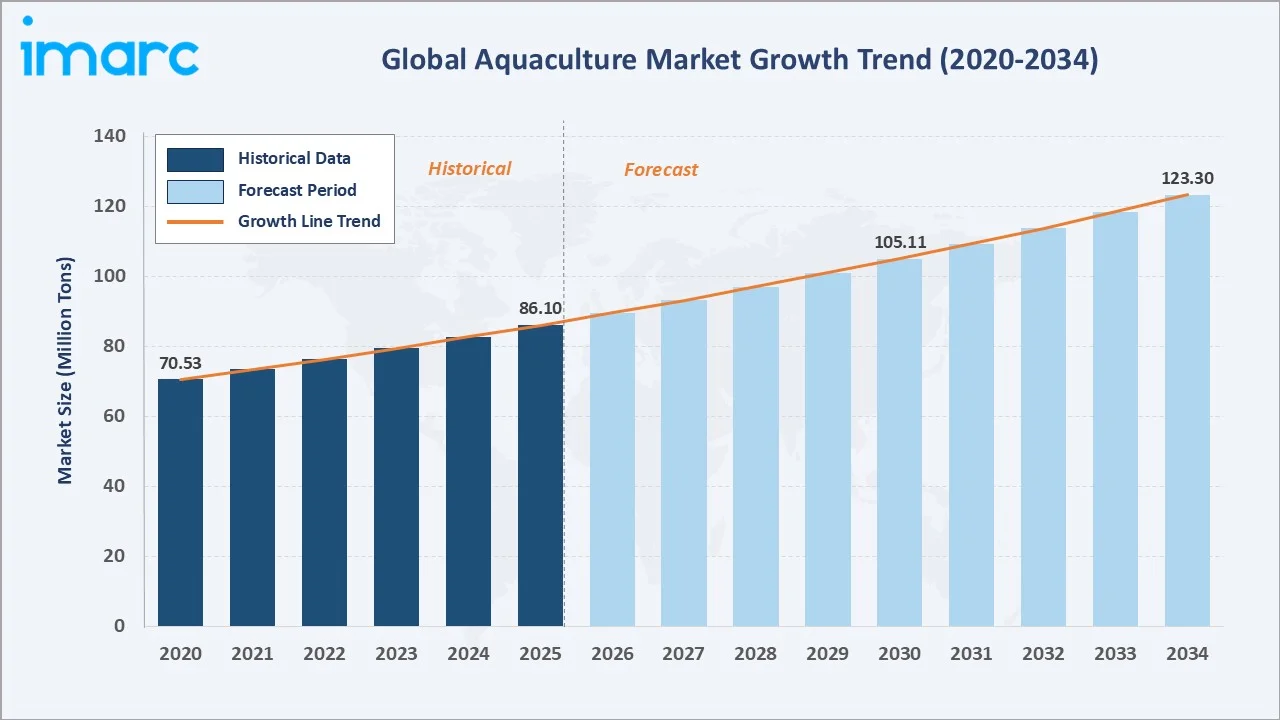

The global aquaculture market reached 86.10 Million Tons in 2025 and is projected to reach 123.30 Million Tons by 2034, growing at a CAGR of 4.07% during 2026-2034. Market growth is driven by rising global seafood demand amid declining wild capture fisheries, strong government support programs, and accelerating adoption of advanced farming technologies including recirculating aquaculture systems (RAS), AI-powered feeding management, and precision genetics.

Market Snapshot

|

Metric |

Value |

|

Market Volume (2025) |

86.10 Million Tons |

|

Forecast Market Volume (2034) |

123.30 Million Tons |

|

CAGR (2026-2034) |

4.07% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

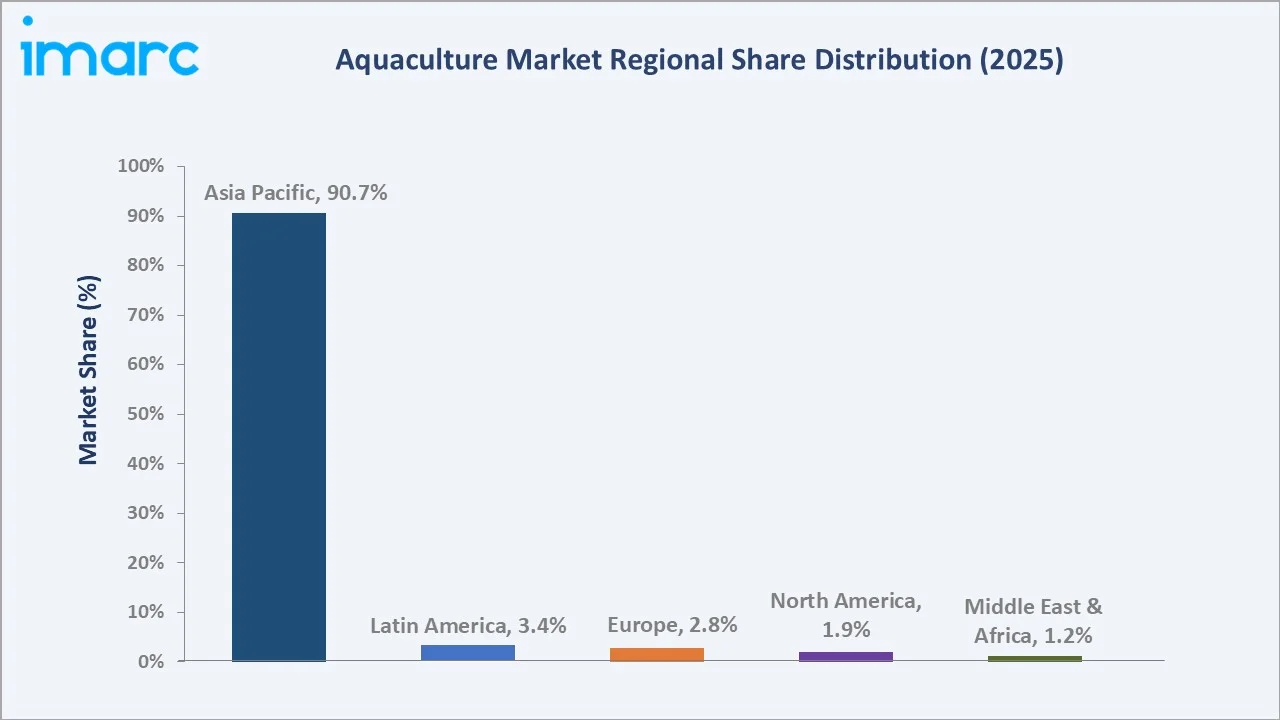

Asia Pacific's extraordinary 90.7% dominance reflects China's position as the world's largest aquaculture producer, contributing approximately 60% of global production, followed by India, Indonesia, Vietnam, Bangladesh, and the Philippines. In 2024, China retained its position as the world’s largest seafood producer, with output estimated at 74.1 million metric tons (MMT), leveraging millennia of aquaculture tradition alongside modern intensive farming techniques that achieve yields unmatched in other regions.

To get more information on this market, Request Sample

The market's 4.07% CAGR is anchored by the structural necessity of aquaculture in meeting global seafood demand. With wild fisheries production plateaued at approximately 90 Million Tons annually since the 1990s, the additional seafood required to feed a population projected to reach 10 Billion by 2050 must come almost entirely from aquaculture expansion and productivity improvement, creating a non-discretionary long-term demand driver.

Executive Summary

The global aquaculture market is the world's fastest-growing food production sector, supplying over 50% of global seafood consumption and playing an irreplaceable role in global food security and nutrition. From 86.10 Million Tons in 2025, the market is forecast to reach 123.30 Million Tons by 2034, adding 37.20 Million Tons of incremental production at a 4.07% CAGR.

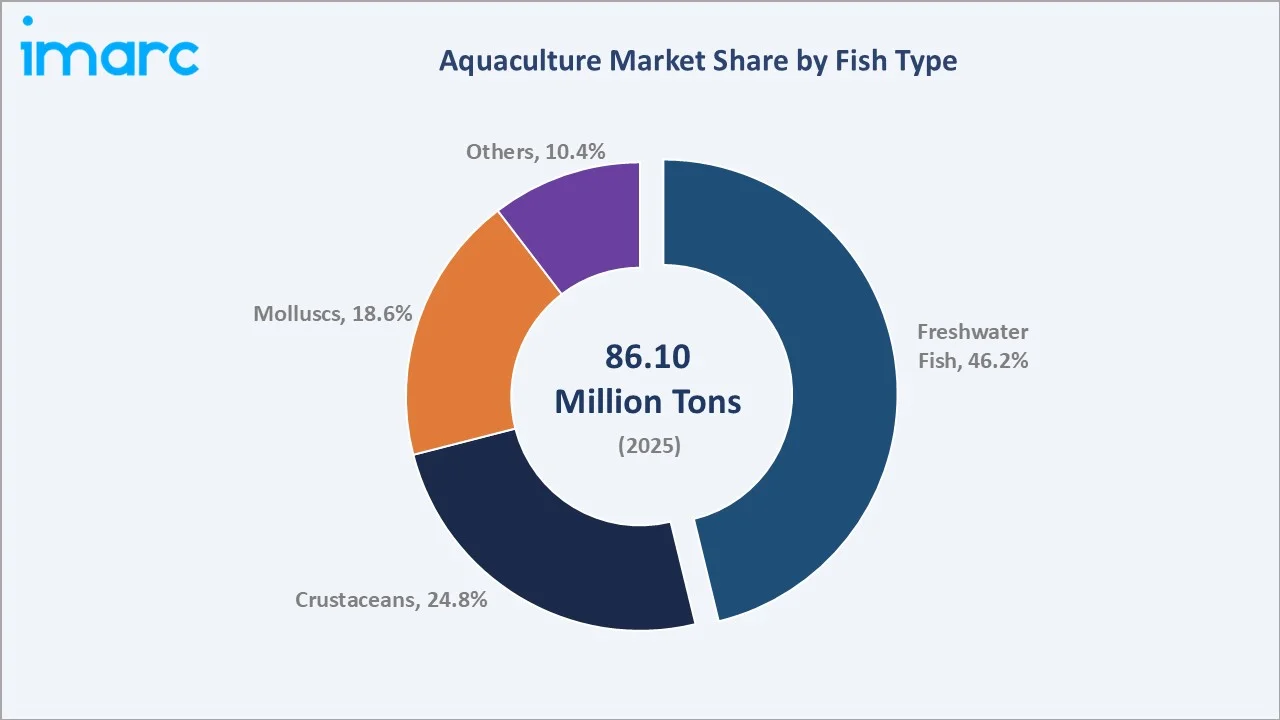

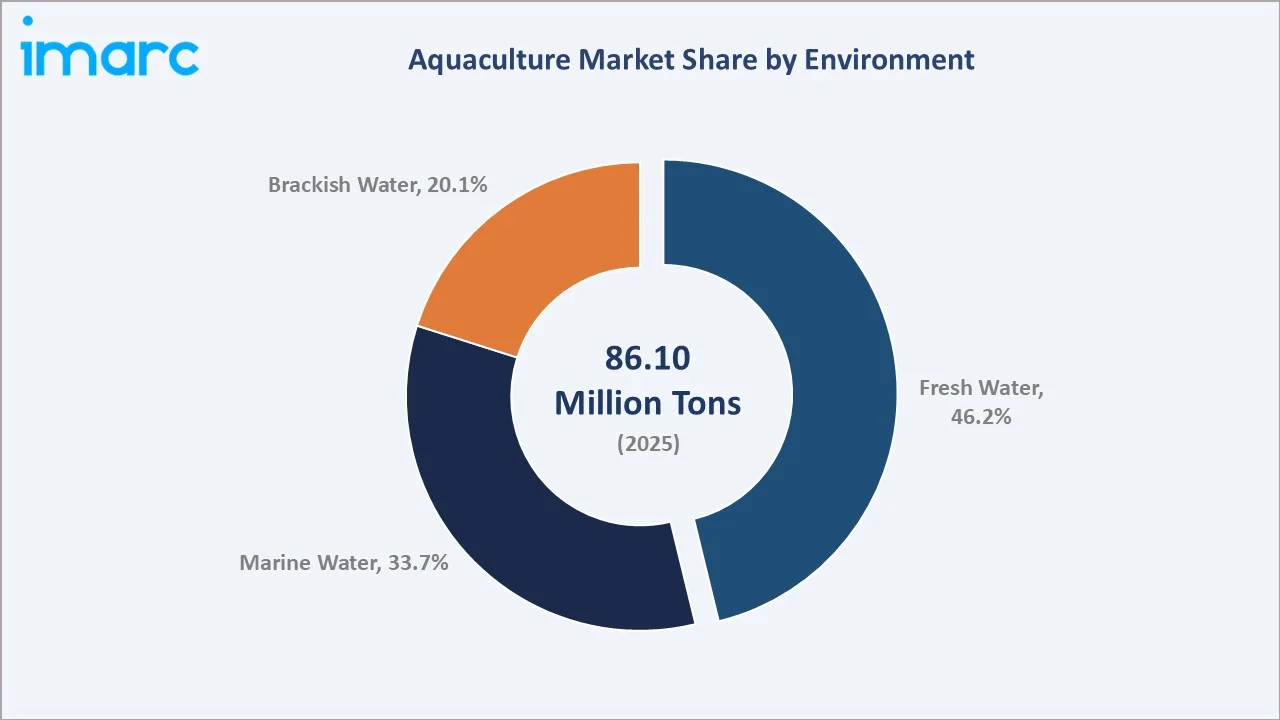

Freshwater fish leads the fish type segment at 46.2% in 2025, dominated by carp species (grass carp, silver carp, common carp) that collectively represent the largest volume of any cultured species globally, followed by tilapia and catfish. The fresh water environment at 46.2% reflects the dominance of inland fish pond and reservoir-based aquaculture across Asia.

Key players, including Mowi, Charoen Pokphand Group, Umios Corporation, SalMar ASA, and Austevoll Seafood ASA, compete through species specialization, geographic market breadth, farm technology investment, and sustainability certification programs that are increasingly demanded by European and North American seafood retail buyers.

Key Market Insights

|

Insight |

Data |

|

Largest Fish Type |

Freshwater Fish – 46.2% share (2025) |

|

Fastest Growing Fish Type |

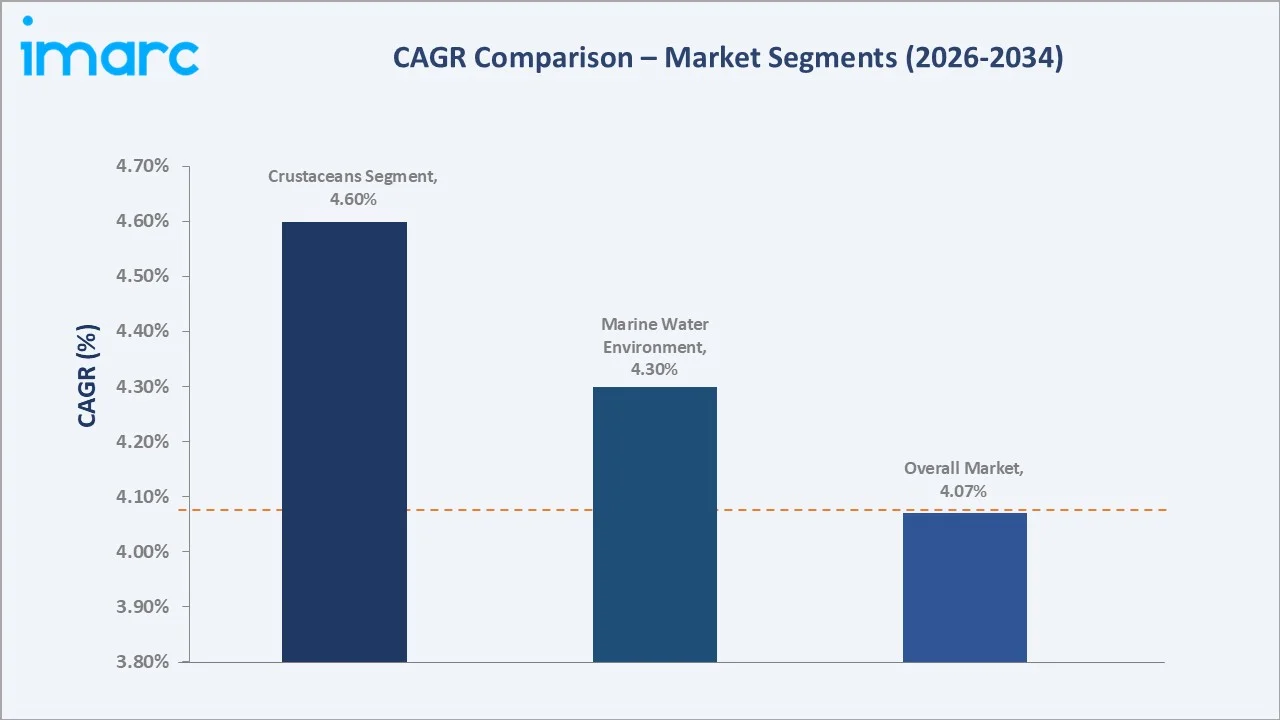

Crustaceans – ~4.60% CAGR (2026-2034) |

|

Largest Environment Segment |

Fresh Water – 46.2% share (2025) |

|

Second Largest Environment |

Marine Water – 33.7% (seaweed, salmon, bivalves) |

|

Leading Region |

Asia Pacific – 90.7% share (2025) |

|

Top Companies |

Mowi, Charoen Pokphand Group, Umios Corporation, SalMar ASA, and Austevoll Seafood ASA |

Key Analytical Observations:

- Freshwater fish at 46.2% (2025) represents the foundation of global aquaculture, dominated by carps, tilapia, catfish, and freshwater shrimp cultivated in ponds, reservoirs, rice paddies, and cages across river systems in China, India, Bangladesh, and Southeast Asia.

- Crustaceans at 24.8% (2025), primarily vannamei shrimp, tiger shrimp, and freshwater prawns, are growing fastest at approximately 4.60% CAGR. In January 2026, Ecuador’s shrimp exports reached 125,215 metric tons, registering a 23% year-on-year increase.

- Marine water aquaculture at 33.7% (2025) encompasses Atlantic salmon farming, seaweed cultivation, bivalve mollusk farming, and marine fish species including sea bass, sea bream, and grouper.

- Brackish water aquaculture at 20.1% (2025) covers coastal shrimp farming, milkfish, and estuarine species farming in coastal ponds and enclosed lagoons across Southeast Asia, the Indian subcontinent, and the Pacific Islands.

Aquaculture Market Overview

Aquaculture is the controlled cultivation of aquatic organisms, fish, crustaceans, molluscs, seaweed, and other aquatic plants, in fresh, brackish, or marine water environments for food production, aquarium trade, bait, and industrial applications.

It encompasses a vast range of farming systems from simple subsistence fish ponds to highly engineered recirculating aquaculture systems (RAS), offshore cage farms, and shellfish longline operations. Aquaculture now accounts for over 50% of global seafood supply, having doubled from approximately 25% in the year 2000, and is projected to supply 65%+ of global seafood consumption by 2034.

The market spans a diverse range of farming environments and production intensities, from traditional extensive pond culture at 1–5 tons per hectare, through semi-intensive managed pond systems at 5–20 tons per hectare, to intensive cage and RAS operations exceeding 100 kg/m³.

Aquaculture species range from low-trophic-level filter-feeding bivalves and herbivorous carp that require minimal feed inputs, to high-value carnivorous species such as Atlantic salmon, sea bass, and shrimp that depend on formulated compound feed with fishmeal and fish oil components.

Market Dynamics

To evaluate market opportunities, Request Sample

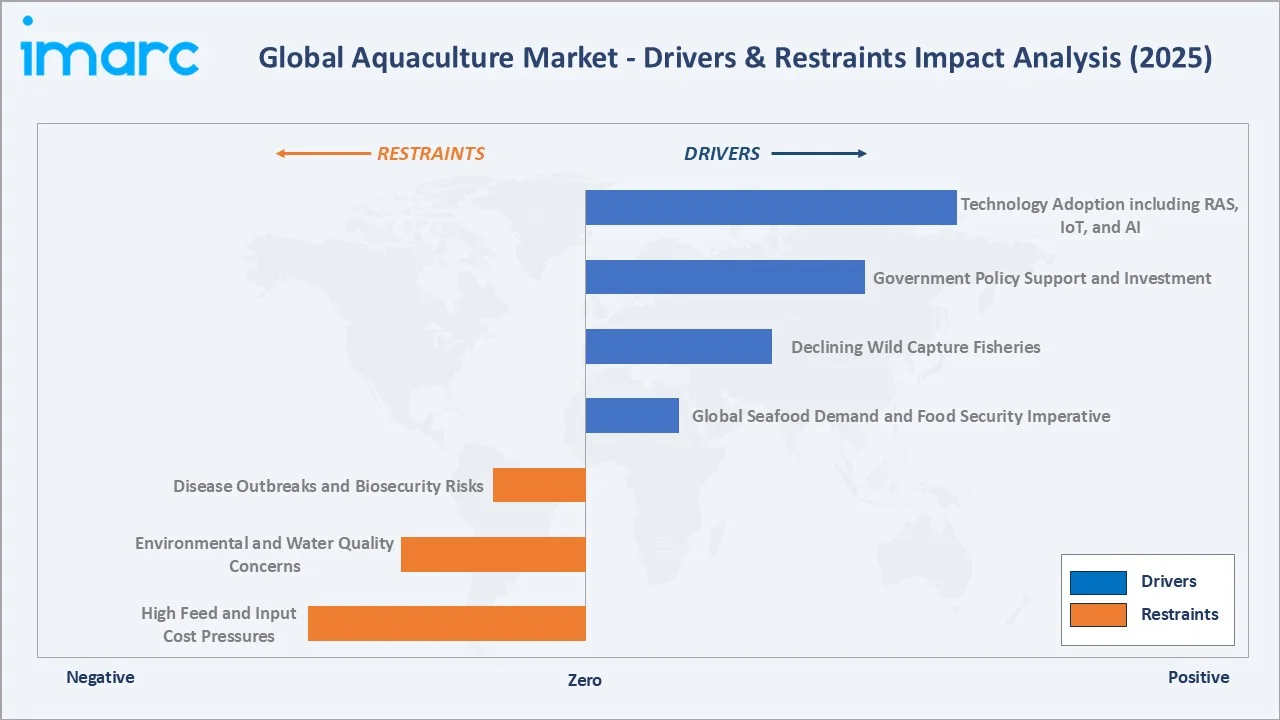

Market Drivers

- Global Seafood Demand and Food Security Imperative: Over the past 60 years, global seafood consumption has grown nearly fivefold, with per capita consumption increasing at an average annual rate of 3.0%. As the global population grows and as rising incomes in developing countries increase protein demand, FAO estimates that global food production must increase by 50–70% by 2050.

- Declining Wild Capture Fisheries: The FAO estimates that approximately 35% of global marine fish stocks are now overfished or depleted, compared to 10% in 1974. Wild capture fisheries production has been essentially flat since the mid-1990s, while global seafood demand has continued to grow.

- Government Policy Support and Investment: China's 14th Five-Year Plan includes specific aquaculture production targets and subsidies feed, equipment, and insurance for aquaculture farmers. India's Pradhan Mantri Matsya Sampada Yojana (PMMSY) program committed INR 20,050 Crore to fisheries and aquaculture development over 2020–2025.

- Technology Adoption including RAS, IoT, and AI: Recirculating Aquaculture Systems (RAS) enable land-based salmon and trout farming independent of ocean access, with water recycling rates of 95–99% and precise environmental control. IoT sensor networks monitor dissolved oxygen, temperature, pH, ammonia, and feed utilization in real time, reducing mortality rates and feed waste.

Market Restraints

- Disease Outbreaks and Biosecurity Risks: Sea lice infestations cost the Atlantic salmon farming industry an estimated between USD 600 million and USD 1 billion annually in treatment costs and production losses. Early Mortality Syndrome (EMS/AHPND) bacterial disease has devastated shrimp production in China, Vietnam, Thailand, and Malaysia since 2010–2012.

- Environmental and Water Quality Concerns: Intensive aquaculture operations generate nutrient-rich effluents that can cause eutrophication of receiving water bodies. Coastal shrimp pond expansion has been linked to mangrove deforestation across Southeast Asia.

- High Feed and Input Cost Pressures: Formulated aquaculture feeds represent 50–70% of total production costs. Fishmeal and fish oil prices have increased significantly since 2020 due to anchovy catch restrictions in Peru and El Niño climate impacts on Peruvian fisheries.

Market Opportunities

- Offshore Aquaculture Development: Moving aquaculture operations beyond the 3-nautical-mile coastal zone to exposed offshore environments with stronger currents and reduced disease pressure is a major growth frontier.

- Recirculating Aquaculture Systems (RAS) Market Expansion: Land-based RAS technology is enabling salmon and high-value fish farming in proximity to major urban consumer markets, eliminating freight logistics and enabling year-round production.

Market Challenges

- Skilled Workforce and Technical Knowledge Gaps: As aquaculture intensifies and adopts complex technologies, the demand for trained aquaculture technicians, farm managers, and veterinary specialists exceeds the supply in most producing countries.

- Regulatory Approval Timelines and Siting Constraints: New aquaculture farm permits in many markets require environmental impact assessments, coastal zone approvals, water body allocation permits, and community consultation processes that can extend to 5–10 years in Norway, Canada, and Australia.

Emerging Market Trends

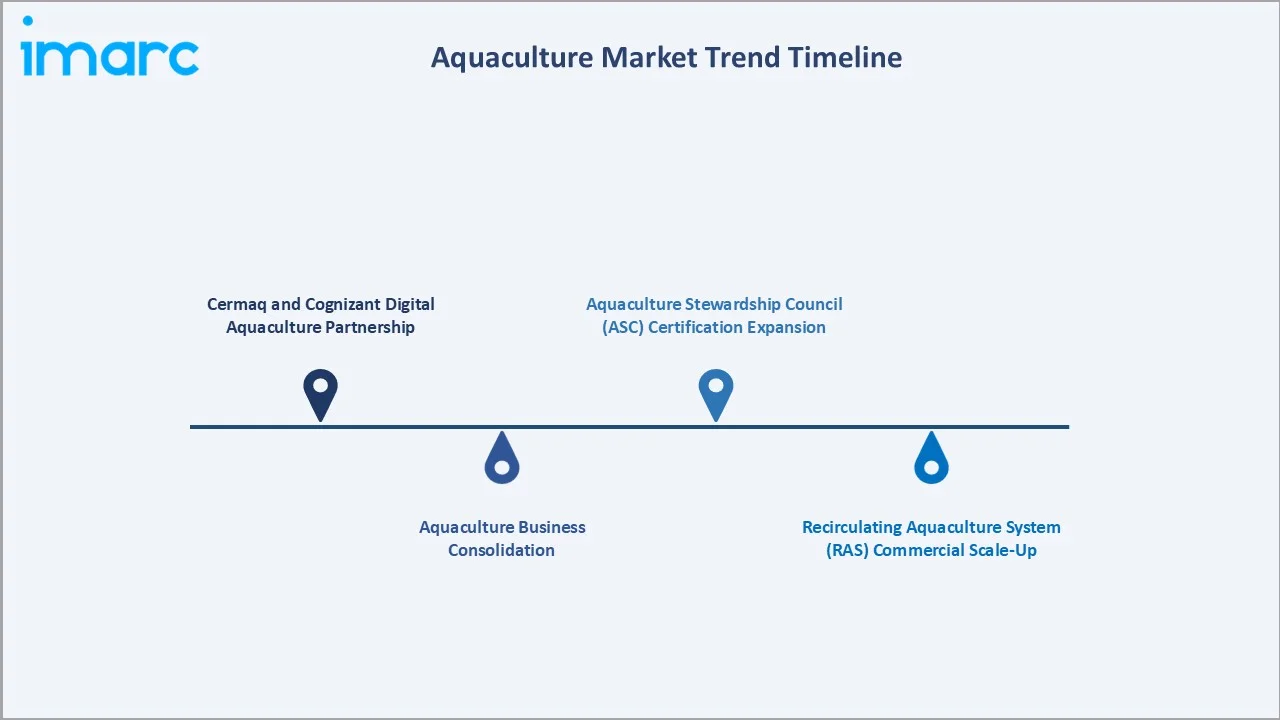

1. Cermaq and Cognizant Digital Aquaculture Partnership

In March 2024, Cognizant announced a new technology partnership with Cermaq Group AS, a global salmon producer, to develop AI-based digital monitoring systems. The partnership focuses on deploying computer vision and machine learning to automate fish welfare assessment, feed optimization, sea lice counting, and biomass estimation across Cermaq's Norwegian and Canadian farm operations.

2. Aquaculture Business Consolidation

Hampidjan consolidated its global aquaculture operations under the new brand ELDI, which will begin operations on January 1, 2026, with 10 companies, 14 service centers, and over 500 employees worldwide. The restructuring aims to strengthen product development, service coordination, and cost-efficient fish farming net production, building on aquaculture sales expected to approach EUR 113 million in 2025.

3. Recirculating Aquaculture System (RAS) Commercial Scale-Up

Land-based RAS is transitioning from pilot-scale to commercial-scale operations, with major projects including Mowi’s aim to increase its annual salmon harvest to 600,000 tons by 2029, Nordic Aquafarms' US East Coast developments, and multiple large-scale RAS projects across the US, Denmark, and Singapore.

4. Aquaculture Stewardship Council (ASC) Certification Expansion

The Aquaculture Stewardship Council's certification program, the global benchmark for responsible aquaculture, surpassed 2 Million Tons of certified production in 2024. European and North American retail buyers including Sainsbury's, Tesco, Walmart, and Costco are mandating ASC or equivalent certification for all seafood procurement, creating commercial pressure for global producers to achieve sustainability certification as a market access requirement rather than a voluntary differentiator.

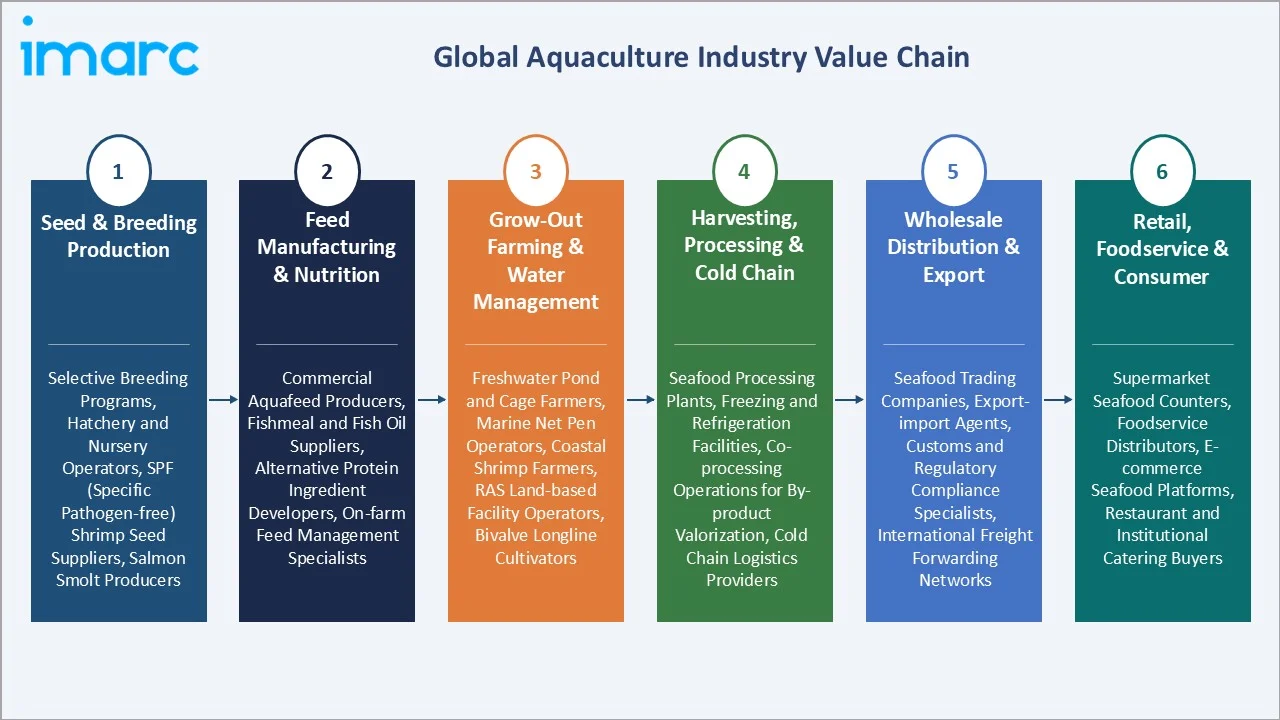

Industry Value Chain Analysis

The aquaculture value chain extends from genetic broodstock development through grow-out farm operations, processing, cold chain logistics, and final seafood consumption, with high complexity and geographic dispersion across the global supply chain.

|

Stage |

Key Players / Examples |

|

Seed & Breeding Production |

Selective breeding programs, hatchery and nursery operators, SPF (specific pathogen-free) shrimp seed suppliers, salmon smolt producers |

|

Feed Manufacturing & Nutrition |

Commercial aquafeed producers, fishmeal and fish oil suppliers, alternative protein ingredient developers, on-farm feed management specialists |

|

Grow-Out Farming & Water Management |

Freshwater pond and cage farmers, marine net pen operators, coastal shrimp farmers, RAS land-based facility operators, bivalve longline cultivators |

|

Harvesting, Processing & Cold Chain |

Seafood processing plants, freezing and refrigeration facilities, co-processing operations for by-product valorization, cold chain logistics providers |

|

Wholesale Distribution & Export |

Seafood trading companies, export-import agents, customs and regulatory compliance specialists, international freight forwarding networks |

|

Retail, Foodservice & Consumer |

Supermarket seafood counters, foodservice distributors, e-commerce seafood platforms, restaurant and institutional catering buyers |

Technology Landscape in the Aquaculture Industry

Recirculating Aquaculture Systems (RAS)

RAS technology enables high-density fish production in land-based facilities by continuously filtering and recycling water, maintaining optimal temperature, oxygen, pH, and ammonia levels with 95–99% water reuse efficiency. Modern commercial RAS systems achieve salmon densities of ~80 kg/m³, compared to 10–25 kg/m³ in traditional sea cages.

AI and Digital Aquaculture Management

Computer vision systems mounted in underwater cameras around sea cages and RAS tanks now provide continuous biomass estimation, individual fish growth tracking, feed detection and waste monitoring, and automated sea lice counting. Mowi's 4.0 Smart Farming and Cermaq's Cognizant AI partnership represent the leading edge of digital aquaculture deployment at commercial scale.

Selective Breeding and Precision Genetics

Selective breeding for Atlantic salmon has achieved 10–15% growth improvement per generation since the 1970s. Next-generation genomic selection (SNP panels) enables selection for disease resistance, feed conversion, and fillet quality traits, further accelerating genetic gain to 15–20% per generation in leading programs.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Fish Type |

Freshwater Fish |

46.2% |

2025 |

|

Environment |

Fresh Water |

46.2% |

2025 |

|

Distribution Channel |

Traditional Retail |

32.0% |

2025 |

|

Region |

Asia Pacific |

90.7% |

2025 |

By Fish Type

Freshwater fish leads at 46.2% in 2025. This segment is dominated by Asia's carp polyculture systems, and tilapia growing operations across China, Indonesia, Egypt, and the Americas. Freshwater fish's volume dominance reflects its role as the primary protein source for low-to-middle-income populations across Asia and sub-Saharan Africa.

To access detailed market analysis, Request Sample

Crustaceans at 24.8% are growing fastest, led by global shrimp farming's expansion into new geographies including Ecuador's large-scale Pacific coast operations and India's Andhra Pradesh vannamei shrimp farming clusters. Molluscs at 18.6% include oysters, mussels, clams, and scallops, primarily farmed in Europe, Japan, China, and North America on longlines and in natural estuaries.

By Environment

Fresh water leads at 46.2% in 2025, reflecting the dominance of inland aquaculture across Asia. China's Hubei, Guangdong, and Jiangsu provinces concentrate the world's most intensive freshwater fish pond systems, with aquaculture integrated into rice paddy systems, river cage networks, and purpose-built reservoir impoundments.

Marine water at 33.7% encompasses Atlantic salmon farming in Norway, Chile, and Scotland, seaweed cultivation across East Asia, and bivalve longline farming in Europe and North America. Brackish water at 20.1% covers coastal shrimp pond farming and milkfish cultivation in Southeast Asia and India, where tidal exchange in coastal environments supports high-productivity aquaculture.

Regional Market Insights

Asia Pacific commands an extraordinary 90.7% of global aquaculture production in 2025. This unparalleled dominance reflects millennia of aquaculture tradition, the world's largest inland water surface area for freshwater fish farming, and extensive coastal resources for shrimp and marine fish production.

Latin America's 3.4% share represents significant absolute production volumes, particularly Ecuador's emergence as the world's largest shrimp exporter in recent years. Chile's Atlantic salmon industry is projected to grow at a rate of 1-4% annually through 2030, making it the world's second-largest salmon producer and the dominant exporter to US and Asian markets.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

90.7% |

China's dominant freshwater carp, shrimp, and seaweed production; India's shrimp farming expansion; Vietnam's pangasius and shrimp export industry; Indonesia's seaweed and shrimp sectors; Bangladesh's prawn aquaculture. |

|

Latin America |

3.4% |

Ecuador's rapid vannamei shrimp expansion; Chile's Atlantic salmon industry; Brazil's tilapia farming growth; Peru's trout aquaculture in Andean lake systems. |

|

Europe |

2.8% |

Norway and Scotland's Atlantic salmon industry; Mediterranean sea bass and sea bream farming in Spain, Greece, and Turkey; mussel and oyster cultivation in France, Ireland, and the Netherlands. |

|

North America |

1.9% |

US catfish, oyster, and salmon farming; Canada's British Columbia and New Brunswick salmon operations; growing RAS land-based salmon and tilapia investment. |

|

Middle East & Africa |

1.2% |

Egypt's rapidly growing tilapia farming sector; Saudi Arabia's food security aquaculture investment; Sub-Saharan Africa's nascent pond fish farming development. |

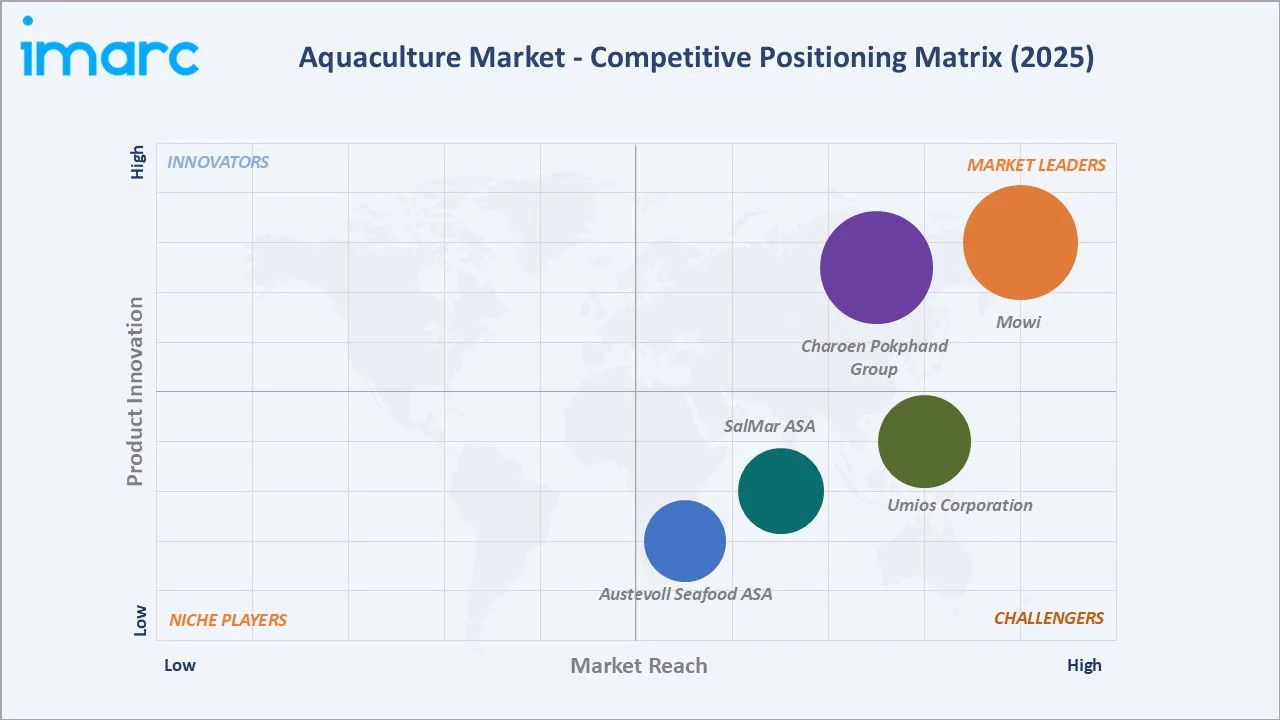

Competitive Landscape

The global aquaculture market is highly fragmented at the farm level, with millions of small-scale farmers in Asia dominating volume production. At the commercial company level, the market is moderately concentrated among listed and private aquaculture companies that collectively represent a minority of total global production but a majority of the highest-value species output.

|

Company Name |

Brands/Products |

Market Position |

Core Strength |

|

Mowi |

Ducktrap, MOWI, Supreme Salmon |

Market Leader |

One of the world's largest salmon producers, AI-powered farming system, ASC certified, 6-continent operations |

|

Charoen Pokphand Group |

CPF |

Market Leader |

Vertically integrated shrimp and aquafeed operations in Thailand, India, and globally; largest shrimp farming company |

|

Umios Corporation |

Umios |

Strong Challenger |

Japanese seafood processing and aquaculture leader; tuna, salmon, and flatfish species; global processing network |

|

SalMar ASA |

SalMar |

Challenger |

Norwegian salmon farming leader, SalMar Ocean offshore aquaculture innovation |

|

Austevoll Seafood ASA |

Norway Seafoods, mǽr, Aurora Salmon, Fjord Trout, Arctic Supreme, Sea Eagle, Fossen |

Challenger |

Norwegian salmon and trout farming, seafood processing and distribution, pan-European market coverage |

Mowi is one of the world’s largest seafood companies and the leading producer of Atlantic salmon, with harvest volumes reaching 559,000 tons in 2025, representing approximately 20% of the global market.

Key Company Profiles

Mowi

Mowi is one of the world's largest Atlantic salmon farming and seafood companies. With worldwide operations, the company farms, processes, and markets over 500,000 tons of salmon products annually.

- Product Portfolio: Ducktrap, MOWI, Supreme Salmon, and others.

- Recent Developments: In May 2024, Mowi Canada East proposed expanding its Indian Head Hatchery in Stephenville, Newfoundland, to improve salmon smolt quality and increase aquaculture production capacity. The company scheduled public meetings in Gander, Harbour Breton, and Stephenville to discuss potential impacts, mitigation measures, benefits, and gather community feedback.

- Strategic Focus: Land-based RAS market development, ASC sustainability certification leadership, consumer brand premium positioning, and sea lice treatment cost reduction through biological control programs.

Charoen Pokphand Group

Charoen Pokphand Group operates Charoen Pokphand Foods PCL, which is Asia's largest integrated shrimp and aquaculture company, operating across the full shrimp value chain from broodstock and feed production through farm operations, processing, and global distribution.

- Product Portfolio: Vannamei and black tiger shrimp (fresh, frozen, cooked, and value-added), shrimp broodstock and SPF larvae, aquafeed for shrimp and fish species.

- Recent Developments: In March 2024, Charoen Pokphand Foods PCL’s seven shrimp farms in Thailand received Antibiotic-Free Product Certification from SGS, demonstrating compliance with stringent food safety and responsible aquaculture standards. The farms use biosafety measures and probiotic farming techniques to produce antibiotic-free shrimp.

- Strategic Focus: SPF shrimp health leadership, India and global shrimp farming expansion, sustainable feed ingredient development (algae, black soldier fly), carbon footprint reduction across shrimp supply chain, and premium retail brand development in European and Japanese markets.

Market Concentration Analysis

The global aquaculture market is highly fragmented in volume terms. The top companies collectively produce approximately 3–5 Million Tons annually, representing only 3–6% of global production. The vast majority comes from millions of small-scale and family farmers in China, Bangladesh, India, and Vietnam.

Shrimp farming is more fragmented, with CPF, Thai Union, and Indian integrated processors collectively representing approximately 10–15% of global shrimp production. Technology consolidation is occurring as large companies acquire RAS technology startups and digital monitoring companies to build proprietary farm management competitive advantages.

Investment & Growth Opportunities

Fastest Growing Segments

Crustaceans (~4.60% CAGR), RAS land-based salmon (~15%+ CAGR), marine water seaweed (~6%+ CAGR), and Africa tilapia farming (~8%+ CAGR from a low base) represent the highest-growth investment vectors through 2034. The combined incremental addressable volume from these high-growth sub-segments is estimated at approximately 20 Million Tons by 2034.

Emerging Market Expansion

Sub-Saharan Africa represents the largest underexploited aquaculture opportunity globally. Africa has abundant freshwater resources (Lake Victoria, Congo River system, Niger River), suitable climate conditions for tilapia year-round production, and rapidly growing protein demand from a population projected to reach 2 Billion by 2050.

Venture and Institutional Investment Trends

- Sovereign wealth funds, including Norway's Government Pension Fund and GCC funds, are investing in aquaculture as part of national food security strategies, providing patient capital suited to aquaculture's long investment timescales.

- Carbon credit markets are an emerging revenue stream for seaweed aquaculture, as macroalgae cultivation sequesters CO₂ and qualifies under voluntary carbon standards, potentially generating USD 20–50 per ton of seaweed produced.

Future Market Outlook (2026-2034)

The global aquaculture market is positioned for consistent, non-cyclical growth through 2034. From 86.10 Million Tons in 2025, production will reach 123.30 Million Tons by 2034, adding 37.20 Million Tons at a 4.07% CAGR. Asia Pacific will retain its structural dominance, while Latin American shrimp and salmon expansion will modestly increase their relative shares. Technology-enabled productivity improvement will deliver a growing share of production growth from existing farm footprints.

RAS land-based aquaculture will grow to an estimated 5–8% of global salmon production by 2034 as costs decline. Sustainability-certified seafood will gain retail shelf share, and the aquaculture-wild fisheries production ratio will shift to approximately 65:35 by 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 95 industry participants in 2024–2025, including aquaculture farm operators, feed company representatives, seafood processors, export traders, technology providers, and aquaculture policy specialists across Asia Pacific, Europe, Latin America, and North America.

Secondary Research

Secondary research encompassed FAO Global Fishery Statistics, Norwegian Directorate of Fisheries, company annual reports, Aquaculture Stewardship Council certification data, industry publications including Fish Farming International, Hatchery International, and IntraFish, and peer-reviewed journals including Aquaculture and Reviews in Aquaculture.

Forecasting Models

Market volume estimations used bottom-up forecasting incorporating production data by species, country, and farming environment, overlaid with capacity expansion pipeline data from major producers, government aquaculture development program targets, and productivity improvement assumptions based on technology adoption rates.

Aquaculture Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Fish Types Covered | Freshwater Fish, Molluscs, Crustaceans, Others |

| Environments Covered | Fresh Water, Marine Water, Brackish Water |

| Distribution Channels Covered | Traditional Retail, Supermarkets and Hypermarkets, Specialized Retailers, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | China, Indonesia, India, Vietnam, Philippines, South Korea, Japan, Thailand, Malaysia, Australia, Chile, Brazil, Ecuador, Mexico, Norway, Spain, Russia, United Kingdom, France, Italy, Greece, Netherlands, Ireland, Denmark, Germany, Egypt, Turkey, Saudi Arabia, United States, Canada |

| Companies Covered | Mowi, Charoen Pokphand Group, Umios Corporation, SalMar ASA, Austevoll Seafood ASA, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the aquaculture market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global aquaculture market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the aquaculture industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Aquaculture Market Report

The market reached 86.10 Million Tons in 2025 and is projected to grow to 123.30 Million Tons by 2034 at a 4.07% CAGR.

Asia Pacific dominates with a 90.7% share in 2025, led by China's massive freshwater fish, shrimp, and seaweed production and India's growing shrimp farming sector.

Freshwater fish leads at 46.2% in 2025, dominated by carp polyculture in Asia and tilapia farming globally, producing approximately 40 Million Tons annually.

Fresh water leads at 46.2%, reflecting the dominance of inland pond and cage fish farming across China, India, and Southeast Asia.

Mowi, Charoen Pokphand Group, Umios Corporation, SalMar ASA, and Austevoll Seafood ASA are some of the leading companies in the market.

Rising global seafood demand, declining wild catch fisheries, government policy support, and technology adoption, including RAS, IoT, and AI, are the primary drivers.

Disease outbreaks, environmental concerns, high feed costs, regulatory approval timelines, and the skilled workforce shortage are key challenges.

Crustaceans are growing fastest at approximately 4.60% CAGR, driven by global shrimp farming expansion in Asia and Latin America.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)