India Bottled Water Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

India Bottled Water Market Size, Share, Trends & Forecast (2026-2034)

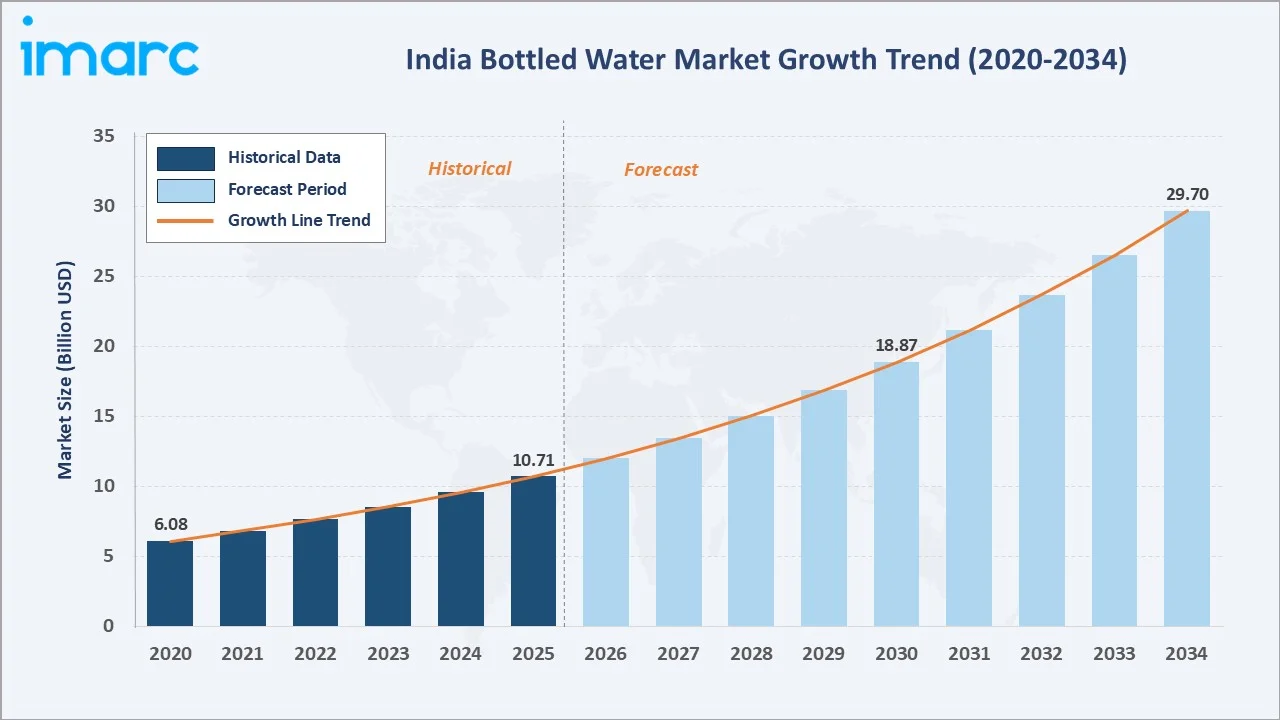

The India bottled water market reached USD 10.71 Billion in 2025 and is projected to reach USD 29.70 Billion by 2034, growing at a CAGR of 12.00% during 2026-2034. Rising consumer health consciousness, expanding urban infrastructure gaps, surging tourism and hospitality demand, and the proliferation of quick commerce and e-commerce distribution channels are driving consistent double-digit growth across all product and distribution segments.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 10.71 Billion |

|

Forecast Market Size (2034) |

USD 29.70 Billion |

|

CAGR (2026-2034) |

12.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

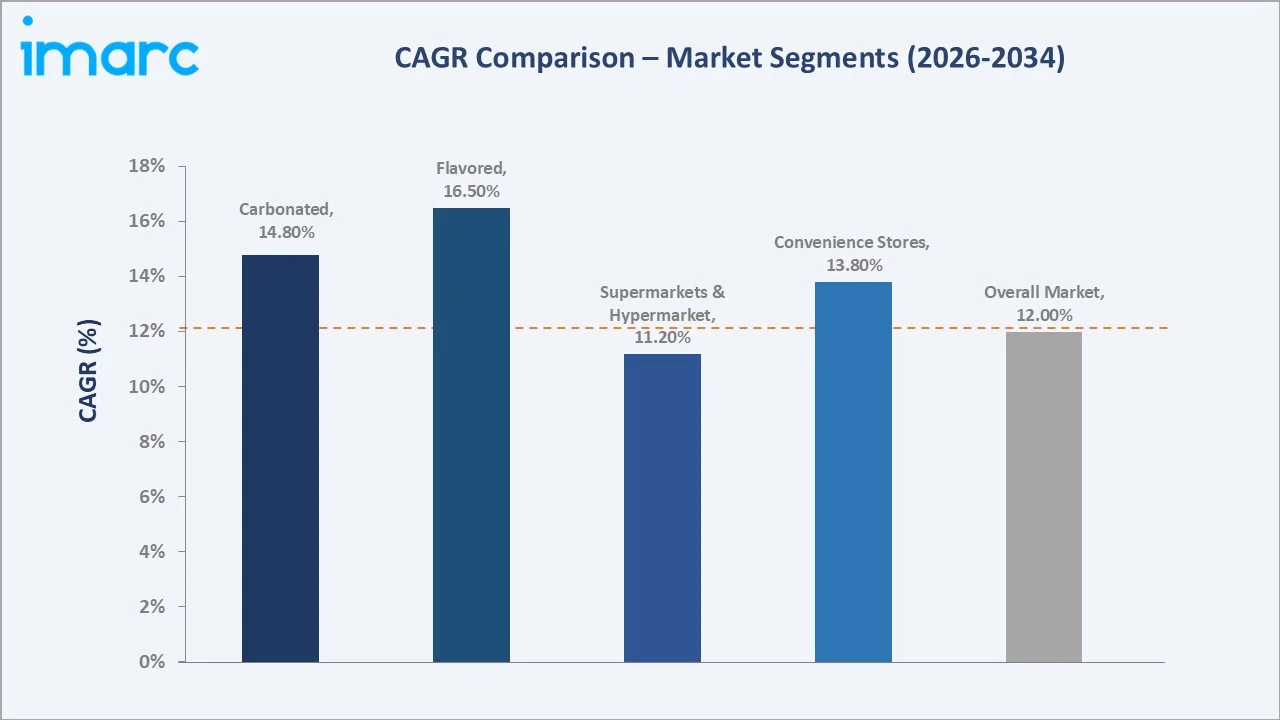

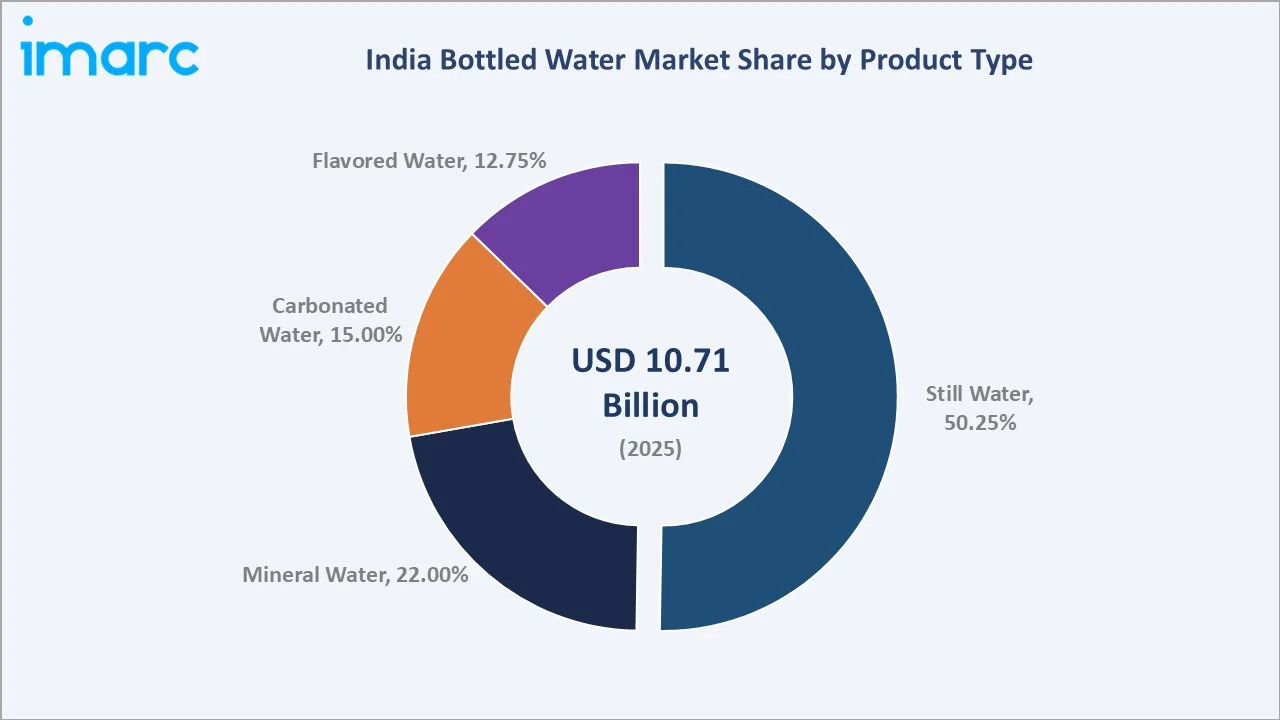

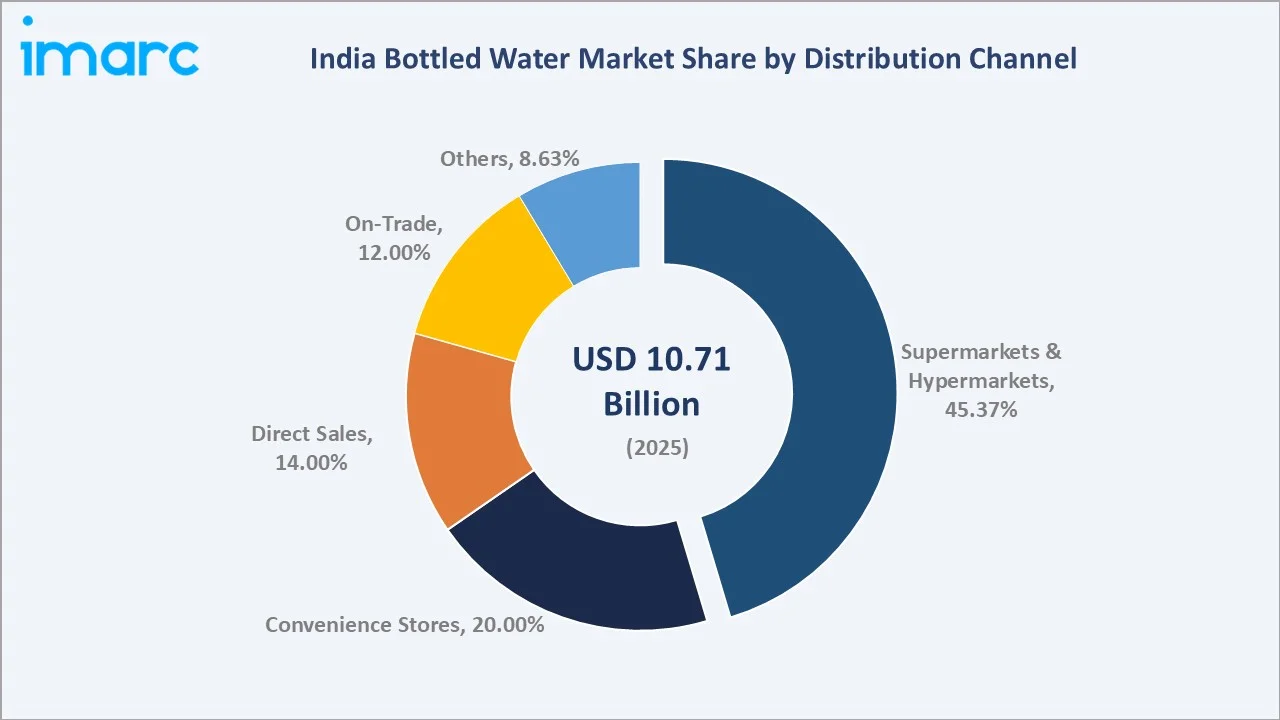

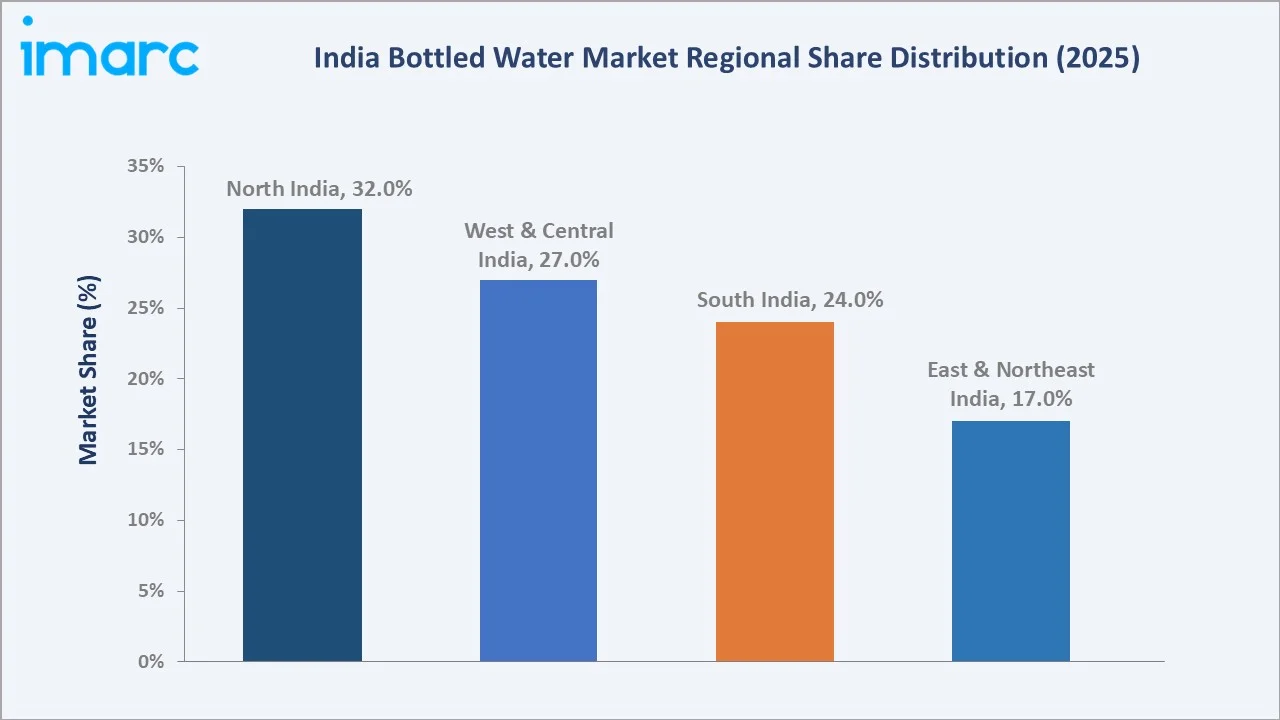

North India leads regionally with a 32.0% market share in 2025, anchored by Delhi-NCR's high-density urban population and tourism demand. Still water commands a dominant product share at 50.25%, while supermarkets and hypermarkets control 45.37% of distribution. Flavored water is the fastest-growing product type at ~16.5% CAGR, driven by health-flavored and functional water adoption among urban consumers.

To get more information on this market, Request Sample

India's bottled water market has grown from USD 6.08 Billion in 2020 to USD 10.71 Billion in 2025, underpinned by three structural forces: the post-COVID hygiene-driven consumption shift, India's expanding tourism infrastructure requiring safe portable hydration, and the rapid proliferation of e-commerce and quick commerce platforms extending bottled water accessibility to 800+ Tier-2 and Tier-3 cities.

Executive Summary

India's bottled water market is expanding at a robust 12.00% CAGR, driven by rising per-capita water consumption, increasing health awareness, and deep structural gaps in urban tap water quality. The market grew from USD 6.08 Billion in 2020 to USD 10.71 Billion in 2025 and is forecast to reach USD 29.70 Billion by 2034, representing an incremental opportunity of USD 18.99 Billion over the forecast period.

Still water retains the leading product share at 50.25% in 2025, serving everyday hydration needs across mass and premium segments. Mineral water at 22.0% benefits from the premiumization of packaged water as urban consumers upgrade from purified to natural mineral sources. Flavored water at 12.75% is the fastest-growing product type at ~16.5% CAGR, as functional hydration and zero-calorie flavored water appeal to health-conscious millennials replacing carbonated soft drinks.

Supermarkets and hypermarkets command 45.37% of distribution, while convenience stores (20.0%) and direct sales (14.0%) reflect the multi-channel distribution complexity of India's diverse retail landscape. Key players, including Bisleri International Private Limited, The Coca‑Cola Company, PepsiCo, and Parle Agro, are investing in premium formats, eco-packaging, and digital distribution to capture India's fast-growing premium and functional hydration segments.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Still Water – 50.25% share (2025) |

|

Fastest Growing Product Type |

Flavored Water – ~16.5% CAGR (2026-2034) |

|

Largest Distribution Channel |

Supermarkets & Hypermarkets – 45.37% share (2025) |

|

Fastest Growing Channel |

Convenience Stores – ~13.8% CAGR (2026-2034) |

|

Leading Region |

North India – 32.0% share (2025) |

|

Top Companies |

Bisleri International Private Limited, The Coca‑Cola Company, PepsiCo, Parle Agro |

Key Analytical Observations Supporting the Above Data:

- Still water at 50.25% (2025) dominates as the workhorse product serving everyday hydration across all price tiers. The 500ml PET bottle format accounts for over 60% of still water volumes, driven by its portability in commuter, office, and retail environments.

- Supermarkets & hypermarkets at 45.37% (2025) reflect the organized retail penetration of bottled water as a planned purchase category. Modern trade's cold chain infrastructure, pack-size variety, and promotional intensity sustain its dominance, while multi-pack deals drive per-basket revenue for leading brands.

- North India's 32.0% (2025) regional share reflects Delhi-NCR's status as India's highest per-capita bottled water consuming urban cluster, driven by tap water quality concerns, extreme summer temperatures, and the highest concentration of hotels, restaurants, and corporate campuses among all Indian regions.

- Flavored water at ~16.5% CAGR is the fastest-growing product type as brands, including Ocean Beverages, introduce zero-sugar, vitamin-infused, and fruit-flavored variants targeting the active lifestyle segment.

- The overall 12.00% CAGR through 2034 is structurally supported by India's per-capita bottled water consumption of 15-18 liters annually versus the global average of 50-60 liters, a 2.3x penetration gap that represents the primary structural growth engine as income levels rise and urban infrastructure gaps persist.

India Bottled Water Market Overview

Bottled water encompasses packaged drinking water, including still, mineral, carbonated, and flavored variants distributed through organized retail, foodservice, institutional, and direct delivery channels. India's market spans mass-market PET purified water, premium natural mineral water, carbonated sparkling variants, and the emerging functional flavored hydration segment serving 1.4 billion consumers.

India's bottled water market has evolved from a niche urban product in the 1990s to a mass-market essential following Bisleri's modern packaging revolution and the BIS IS 14543 packaged drinking water standard enforcement from 2002. FSSAI Regulations 2011 (amended 2020) and the Bureau of Indian Standards' mandatory BIS certification framework now govern registered packaged water units.

Market Dynamics

To evaluate market opportunities, Request Sample

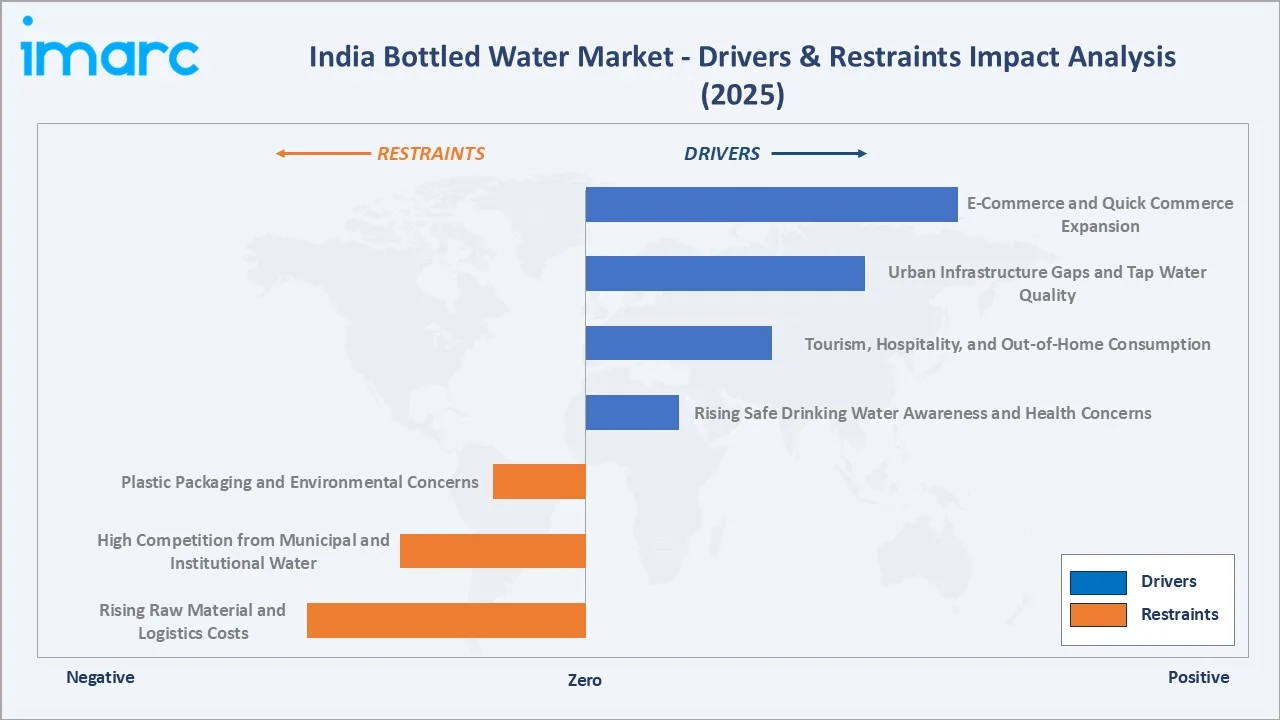

Market Drivers

- Rising Safe Drinking Water Awareness and Health Concerns: India's tap water quality deficits, with CPCB estimates suggesting over 70% of surface water is polluted, sustain structural bottled water demand.

- Tourism, Hospitality, and Out-of-Home Consumption: India welcomed 56 lakh foreign tourist arrivals till August 2025, each generating an estimated 1.5 liters/day bottled water demand. The HoReCa (hotels, restaurants, cafes) channel accounts for approximately 18% of organized bottled water revenue, driving glass-bottle premium and branded mineral water adoption.

- Urban Infrastructure Gaps and Tap Water Quality: Between January 2025 and January 7, 2026, over 5,500 people in 26 cities, including 16 state capitals across 22 states and Union Territories, fell ill after consuming sewage-contaminated piped drinking water. This has driven the growing adoption of household bottled water subscription models.

- E-Commerce and Quick Commerce Expansion: Zepto, Blinkit, and Swiggy Instamart have made bottled water a sub-10-minute delivery category. Amazon Fresh and Flipkart Grocery's subscription models for 10-litre and 20-litre bulk water are capturing the urban household repeat purchase share.

Market Restraints

- Plastic Packaging and Environmental Concerns: India generates an estimated 3.4 million tons of plastic waste annually, of which single-use water bottles constitute a significant share. NGT regulations on single-use plastics below 75 microns, consumer backlash, and ESG pressure on brands are accelerating investment in rPET packaging and refillable formats.

- High Competition from Municipal and Institutional Water: In tier-1 cities with improving municipal water quality, tap water remains a zero-cost substitute that constrains premium pricing power. NDMC and Mumbai's BMC water quality improvements in select zones reduce household bottled water conversion in these micro-markets.

- Rising Raw Material and Logistics Costs: PET resin prices, linked to global crude oil cycles, increased 18–22% between 2022 and 2024, compressing manufacturer margins. Last-mile logistics costs for 20-litre bulk delivery in dense urban markets, including Bengaluru and Pune, have risen 25% over the same period.

Market Opportunities

- Functional and Enhanced Water Premiumization: Electrolyte-infused recovery water, alkaline water, and vitamin-enriched variants are growing at around 20%+ CAGR. The functional water segment, currently below 3% of market value, represents a USD 5+ Billion opportunity by 2034 as sports nutrition and wellness trends drive trial among urban consumers.

- Sustainable Packaging and Refillable Models: Bisleri's Bottles for Change program, Coca-Cola's PlantBottle PET initiative, and startup entrants including Infuse Water are pioneering deposit-return and subscription refill models.

Market Challenges

- Regulatory Compliance and Quality Enforcement Inconsistency: India's bottled water sector has over 6,000 registered units with inconsistent BIS/FSSAI enforcement across states. Counterfeit and adulterated packaged water, estimated at 8–12% of rural market volumes, creates brand safety risks and erodes consumer trust in smaller regional markets.

- Price Elasticity in Mass-Market Segments: The INR 10–15 price point for 500ml still water represents a near-commodity market where an INR 2–3 price increase triggers significant volume loss in price-sensitive tier-2 and tier-3 markets. Rising input costs without commensurate pricing power constrain mass-market brand profitability.

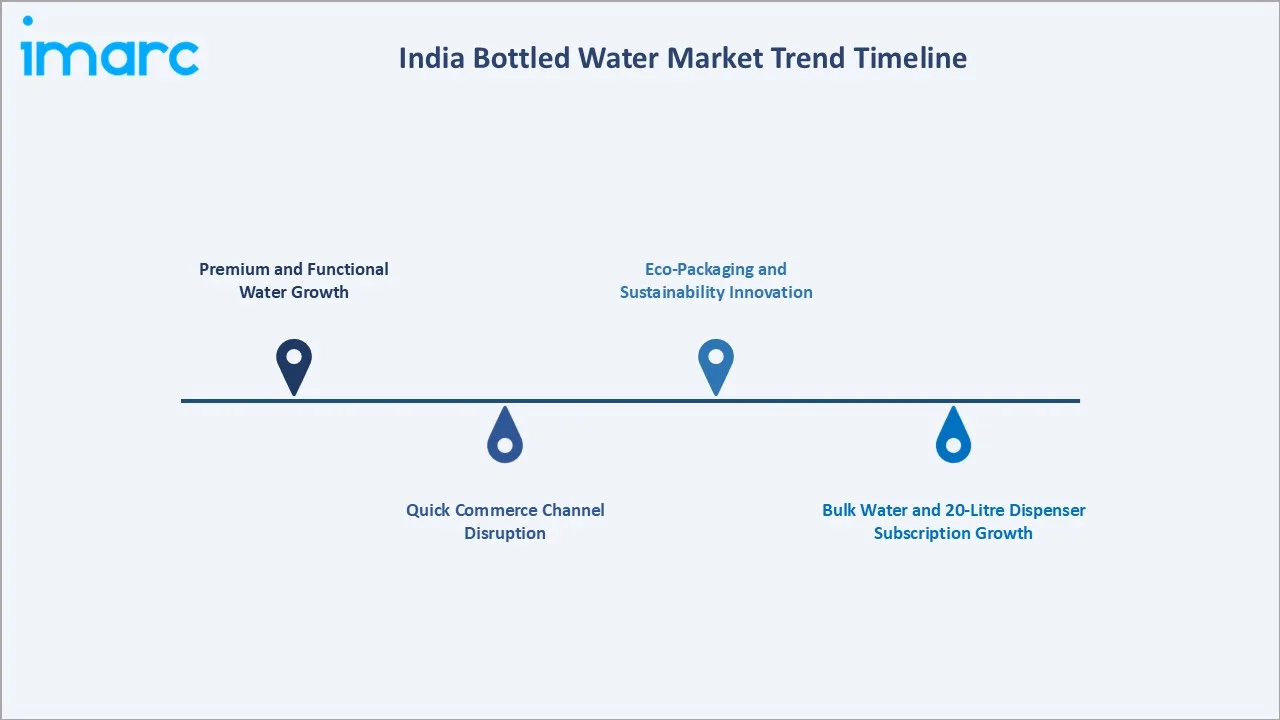

Emerging Market Trends

1. Premium and Functional Water Growth

India's premium bottled water segment is growing at 18% CAGR, led by Evian and Evocus alkaline water. In October 2023, Bisleri expanded its premium Vedica Himalayan Spring Water line with the launch of Vedica Himalayan Sparkling Water, a 300 ml premium sparkling drink sourced from the Himalayas and aimed at health‑conscious, luxury‑oriented consumers.

2. Quick Commerce Channel Disruption

In June 2025, CLEAR Premium Water expanded into both e‑commerce and quick‑commerce channels, making its products available for instant purchase on major platforms like Amazon, Swiggy Instamart, Blinkit, Zepto, BigBasket, and Flipkart Minutes, to boost convenience and strengthen its digital reach.

3. Bulk Water and 20-Litre Dispenser Subscription Growth

In April 2024, demand for 20‑litre packaged water cans surged in Pune as residents faced water shortages and irregular or poor‑quality municipal supply, prompting many housing societies and individuals to buy more bottled water. Distributors reported demand rising by about 40–50% compared to last year.

4. Eco-Packaging and Sustainability Innovation

In June 2023, Coca‑Cola India introduced Kinley bottles made from 100 % recycled PET (rPET), becoming one of the first in the Indian beverage sector to use entirely recycled food‑grade plastic for water packaging. This move supports the company’s sustainability push toward a circular economy and reduces reliance on virgin plastic while aligning with its “World Without Waste” goals.

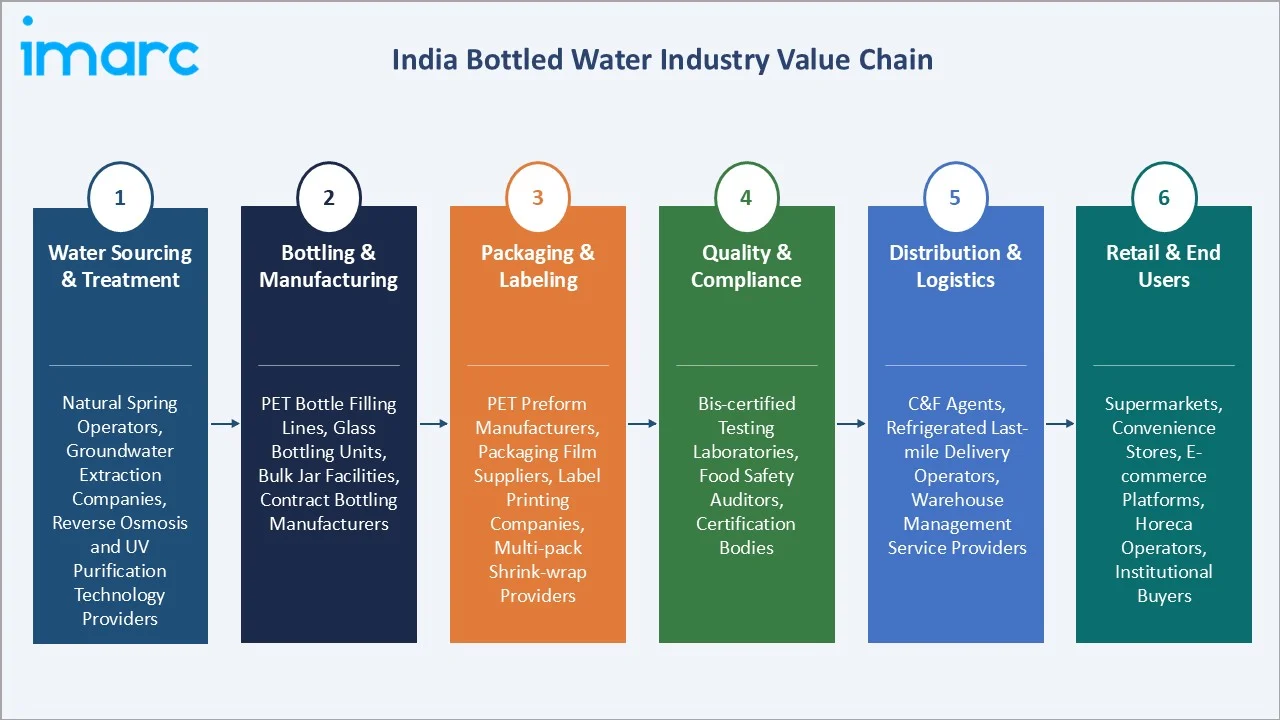

Industry Value Chain Analysis

India's bottled water value chain spans natural water sourcing and purification through multi-channel retail delivery, with each stage subject to BIS/FSSAI quality compliance requirements that define minimum standards for product safety and label accuracy.

|

Stage |

Key Players / Examples |

|

Water Sourcing & Treatment |

Natural spring operators, groundwater extraction companies, reverse osmosis and UV purification technology providers |

|

Bottling & Manufacturing |

PET bottle filling lines, glass bottling units, bulk jar facilities, contract bottling manufacturers |

|

Packaging & Labeling |

PET preform manufacturers, packaging film suppliers, label printing companies, multi-pack shrink-wrap providers |

|

Quality & Compliance |

BIS-certified testing laboratories, food safety auditors, certification bodies |

|

Distribution & Logistics |

C&F agents, refrigerated last-mile delivery operators, warehouse management service providers |

|

Retail & End Users |

Supermarkets, convenience stores, e-commerce platforms, HoReCa operators, institutional buyers |

Technology Landscape in the India Bottled Water Industry

Advanced Water Purification Technology

Reverse osmosis (RO), ultraviolet (UV) sterilization, and ozone treatment systems form the backbone of India's packaged drinking water production infrastructure. Leading manufacturers, including Bisleri, operate multi-stage purification with 8–14 filtration steps, including activated carbon filtration, micron filtration, and post-ozonation. The adoption of nano-filtration membranes for mineral-retaining purification is enabling the production of natural-mineral-equivalent water from groundwater sources.

Smart Packaging and QR Traceability

BIS-mandated batch traceability and the Food Safety and Standards Authority of India's FOSCOS platform are driving the adoption of QR code-enabled packaging that allows consumers to verify water quality test results, source location, and certification validity. In May 2024, plastic refund vending machines were installed along the Kedarnath yatra route to encourage pilgrims to return plastic bottles by offering refunds, aiming to reduce litter and improve waste management.

IoT-Enabled Production and Quality Monitoring

Leading bottling plants are deploying IoT-connected quality sensors that provide continuous total dissolved solids, pH, and microbial count monitoring throughout the filling line. Bisleri's flagship Rudrapur plant operates zero-defect automated quality assurance using computer vision for seal integrity inspection, reducing quality rejections by 40% versus manual inspection baselines and enabling real-time FSSAI compliance documentation.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Still Water |

50.25% |

2025 |

|

Distribution Channel |

Supermarkets & Hypermarkets |

45.37% |

2025 |

|

Region |

North India |

32.00% |

2025 |

By Product Type

Still water commands a 50.25% share in 2025. This leadership reflects the dominance of everyday purified drinking water consumed across household, office, travel, and institutional settings. The 500ml and 1L PET formats account for the bulk of still water volumes, with the 20-litre bulk format growing rapidly as urban household subscription delivery expands.

To access detailed market analysis, Request Sample

Mineral water at 22.0% benefits from the growing premiumization of hydration among urban consumers. Carbonated water at 15.0% is driven by sparkling water's substitution of carbonated soft drinks in health-conscious consumption occasions. Flavored water at 12.75% is the fastest-growing segment at ~16.5% CAGR, as electrolyte-infused, vitamin-fortified, and zero-sugar fruit-flavored variants capture the active lifestyle and fitness hydration segment.

By Distribution Channel

Supermarkets and hypermarkets dominate at 45.37% in 2025. Modern trade's cold storage infrastructure, extensive SKU range, multi-pack promotional offerings, and high footfall frequency sustain its dominance as a planned purchase channel. Reliance Fresh and DMart drive the bulk of organized retail bottled water volumes.

Convenience stores at 20.0% serve the impulse and on-the-go hydration occasion at transit hubs, petrol stations, and neighborhood kirana-format convenience outlets. Direct sales at 14.0% encompass bulk 20-litre jar home delivery subscriptions and corporate water dispensing contracts. On-trade at 12.0% covers the hotel, restaurant, airline, and hospitality channel, where branded mineral water commands a significant premium over retail pricing.

Regional Market Insights

North India's market leadership (32.0%, 2025) is driven by Delhi-NCR's status as India's largest single urban water market. Delhi's tap water quality issues, with CPCB flagging Yamuna-sourced water for coliform contamination, sustain structural bottled water dependence across all income segments.

West and Central India, at 27.0% (2025), benefits from Mumbai's premium bottled water demand and Maharashtra's strong HoReCa channel. South India, at 24.0%, is the fastest-growing region, as Bengaluru and Chennai's tech corridor millennial workforce drives functional and premium water adoption.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

32.0% |

Highest urban population density; Delhi-NCR tourism and hospitality demand; strong modern trade penetration; rising health awareness among middle-class consumers |

|

West and Central India |

27.0% |

Mumbai and Pune premium bottled water demand; Maharashtra strong HoReCa channel; Gujarat industrial and commercial belt demand; rapid Tier-2 city modern retail expansion |

|

South India |

24.0% |

Bengaluru and Chennai tech-corridor on-the-go consumption; Tamil Nadu strong tourist inflow; Kerala and AP hospitality sector; growing convenience store network |

|

East and Northeast India |

17.0% |

Expanding urban middle class in Kolkata and Guwahati; growing tourism in Northeast states; rising e-commerce penetration; government infrastructure investment improving distribution |

East and Northeast India at 17.0% represents the highest upside geography as Kolkata's growing middle class and Northeast India's expanding tourism infrastructure convert home-filtered and public-source users to commercial packaged water.

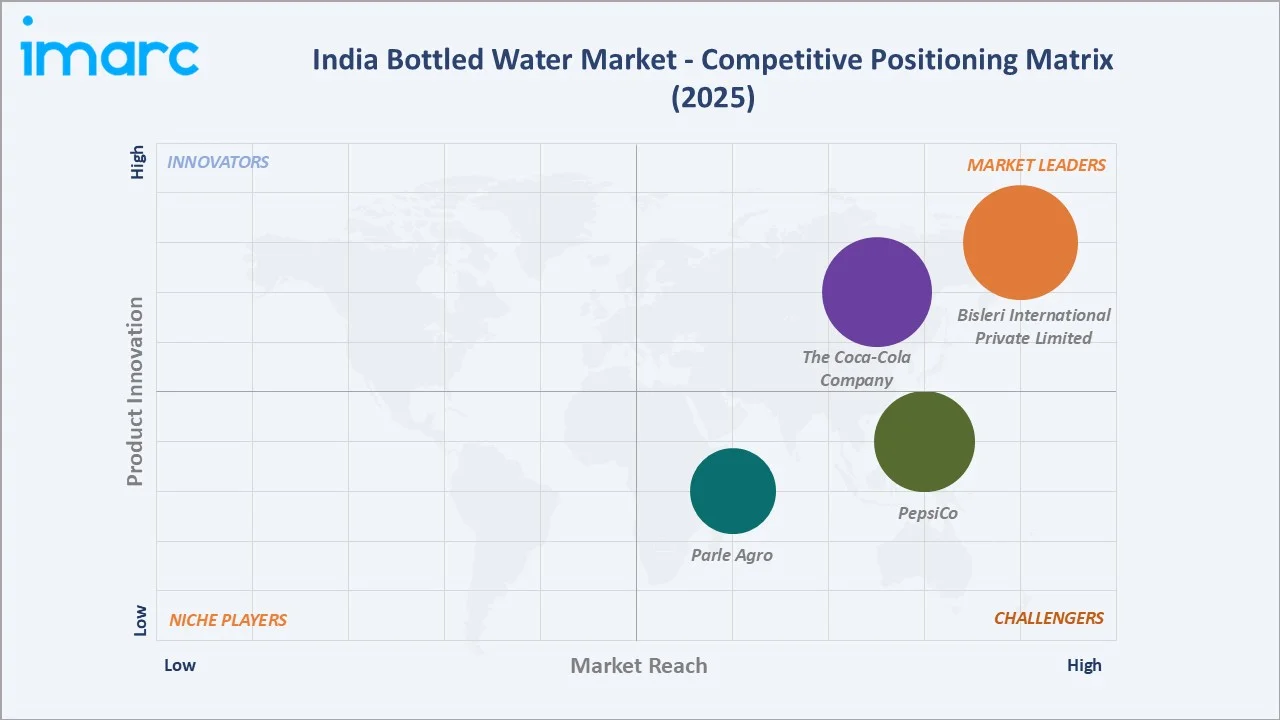

Competitive Landscape

India's bottled water market is moderately concentrated, with Bisleri International Private Limited, The Coca‑Cola Company, and PepsiCo collectively holding approximately 55–65% of organized market volume in 2025.

|

Company Name |

Brand / Products |

Market Position |

Core Strength |

|

Bisleri International Private Limited |

Bisleri, Vedica, Bisleri subscription |

Market Leader |

Pan-India distribution; largest retail footprint; strong brand recall; multiple price tiers; dominant bulk and institutional segment |

|

The Coca-Cola Company |

Kinley, still and sparkling water, Schweppes, smartwater, vitaminwater |

Market Leader |

Global brand; mass-market reach via Coca-Cola distribution network; strong HoReCa channel |

|

PepsiCo |

Aquafina purified water |

Strong Challenger |

Wide retail network; co-distribution with PepsiCo beverages; strong convenience store and quick commerce channel presence |

|

Parle Agro |

Bailley still water |

Challenger |

Cost-competitive pricing; wide distributor base in Tier-2 and Tier-3 cities; strong rural market penetration strategy |

The premium segment is contested by Danone (Evian) and domestic new entrants, while regional players, including Parle Agro, and hundreds of state-level BIS-certified units dominate tier-2 and tier-3 geographies.

Key Company Profiles

Bisleri International Private Limited

Bisleri International Private Limited is India's most recognized bottled water brand. The company commands unrivalled distribution depth across urban and semi-urban India.

- Product Portfolio: Bisleri Still, Vedica Himalayan Spring Water, and Bisleri subscription service.

- Recent Developments: In November 2025, Bisleri International Private Limited signed a two‑year deal to be the Official Beverage Partner of the Tata Women’s Premier League, supporting India’s top women’s cricket tournament with branded hydration and promotional activations.

- Strategic Focus: Quick commerce channel expansion via Blinkit, Zepto, and Swiggy Instamart partnerships; rPET packaging transition; Bisleri digital subscription scaling; Vedica premium brand investment.

The Coca-Cola Company

The Coca-Cola Company is one of India's leading bottled water players, operating through its Kinley, Schweppes, smartwater, vitaminwater, and DASANI packaged drinking water brands.

- Product Portfolio: Kinley still and sparkling water, Schweppes, smartwater, and vitaminwater.

- Recent Developments: In June 2026, The Coca‑Cola Company announced a potential public listing in India in 2027 for Hindustan Coca‑Cola Holdings Pvt. Ltd. (HCCH), the parent of its largest bottler, which could include the sale of a portion of its shareholding.

- Strategic Focus: rPET packaging roll-out; Kinley quick commerce channel scaling via Blinkit, Zepto, and Swiggy Instamart; smartwater premium segment investment; and franchise bottling partner model.

Market Concentration Analysis

India's bottled water market exhibits moderate concentration at the national level, with Bisleri International Private Limited, The Coca‑Cola Company, and PepsiCo controlling the mass-market volume segment. Below the top three, a competitive mid-market of 15–20 branded regional players serves tier-2 and tier-3 geographies. The long tail includes 6,000+ BIS-registered small units that collectively hold significant rural market volume through ultra-low pricing.

Market consolidation is emerging through the premiumization shift: as consumers upgrade from INR 10–15 mass-market water to INR 25–100 premium and functional variants, brand investment by Bisleri and Tata Consumer Products is diverting wallet share from unbranded regional players to nationally marketed premium formats.

Investment & Growth Opportunities

Fastest Growing Segments

Flavored water (~16.5% CAGR), alkaline and functional water (~20% CAGR), convenience store channel (~13.8% CAGR), and direct sales and subscription delivery (~15% CAGR) represent the highest-return investment vectors through 2034. Together, these sub-categories address an incremental market of approximately USD 12+ Billion by 2034, above 2025 levels, as health premiumization and channel diversification converge.

Emerging Market Expansion

East and Northeast India's 17.0% regional share represents the highest upside geography, with per-capita bottled water consumption at less than 40% of North India levels despite comparable population size. PM-Jal Jeevan Mission's piped water investment paradoxically creates a quality awareness catalyst that converts households from unverified water sources to packaged alternatives as income levels rise.

Venture and Institutional Investment Trends

- India's functional and premium water segment attracted USD 45+ Million in venture capital in 2023–2025, with Startups including Evocus (INR 10 crore in debt funding from Red Fort Capital) and WaterScience (INR 1.4 crore from Velocity) are scaling premium urban positioning through D2C and quick commerce.

- Established FMCG groups, including Dabur and ITC, are evaluating bottled water entries leveraging their existing distribution infrastructure to capture the 12% CAGR market.

Future Market Outlook (2026-2034)

India's bottled water market will expand from USD 10.71 Billion in 2025 to USD 29.70 Billion by 2034 at a 12.00% CAGR. Still water will retain volume dominance, but flavored and functional water will grow from 12.75% to approximately 20% of market value by 2034. The premium segment will more than double as India's per-capita income growth and tourism expansion accelerate the shift from economy to premium hydration.

By 2034, India's bottled water market will be defined by three converging trends: sustainability mandates, digital subscription and quick commerce delivery displacing traditional retail for household formats, and functional premiumization capturing the health and wellness consumer who no longer views water as a commodity. India's position as a top-5 global bottled water market by volume by 2030 will attract global premium brands and accelerate MNC investment in India-specific manufacturing and brand building.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 80 industry participants in 2024–2025, including bottled water brand managers, FSSAI and BIS regulatory consultants, modern trade category managers, quick commerce category heads, and institutional procurement officers across Delhi, Mumbai, Bengaluru, and Hyderabad.

Secondary Research

Secondary research covered BIS IS 14543 certification databases, FSSAI Food Safety Compliance System (FOSCOS) registration data, Ministry of Commerce packaged water export statistics, CPCB water quality reports, venture capital transaction records, and publications including FoodTech India, Business of Water, and Beverage Business Worldwide.

Forecasting Models

Market size estimations used bottom-up and top-down forecasting incorporating per-capita consumption data, urban household penetration benchmarks, distribution channel revenue disclosures, and expert panel validation. A CAGR of 12.00% reflects consensus estimates cross-validated against BIS registration growth trends and IMARC's primary research interviews through 2034.

India Bottled Water Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Still, Carbonated, Flavored, Mineral |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Direct Sales, On-Trade, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Bisleri International Private Limited, The Coca-Cola Company, PepsiCo, Parle Agro, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Bottled Water Market Report

The market reached USD 10.71 Billion in 2025 and is forecast to reach USD 29.70 Billion by 2034 at a 12.00% CAGR.

Still water leads at 50.25% in 2025, driven by everyday hydration demand across mass-market PET formats and the bulk 20-litre jar subscription channel.

Supermarkets and hypermarkets dominate at 45.37% in 2025, reflecting modern trade's cold storage infrastructure, pack-size variety, and high-footfall retail environment for planned bottled water purchases.

North India leads at 32.0% in 2025, anchored by Delhi-NCR's urban population density, tap water quality concerns, tourism demand, and the highest concentration of HoReCa operators among all Indian regions.

Key players include Bisleri International Private Limited, The Coca‑Cola Company, PepsiCo, and Parle Agro, competing through distribution depth, brand investment, and premium portfolio development.

Flavored water is the fastest-growing product type at ~16.5% CAGR, driven by zero-sugar fruit-flavored and vitamin-infused variants appealing to health-conscious urban millennials replacing carbonated soft drinks.

Rising safe drinking water awareness, urban infrastructure and tap water quality gaps, tourism and hospitality sector growth, e-commerce and quick commerce distribution expansion, and per-capita bottled water consumption growth are the primary market catalysts.

Plastic packaging environmental concerns and EPR compliance costs, competition from improving municipal water in select urban areas, rising PET resin and logistics costs, counterfeit products in rural markets, and mass-market price elasticity constraining premium pricing power are the primary challenges.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)