India Carbon Black Market Size, Share, Trends and Forecast by Type, Grade Wise Application, and Region, 2026-2034

India Carbon Black Market Summary:

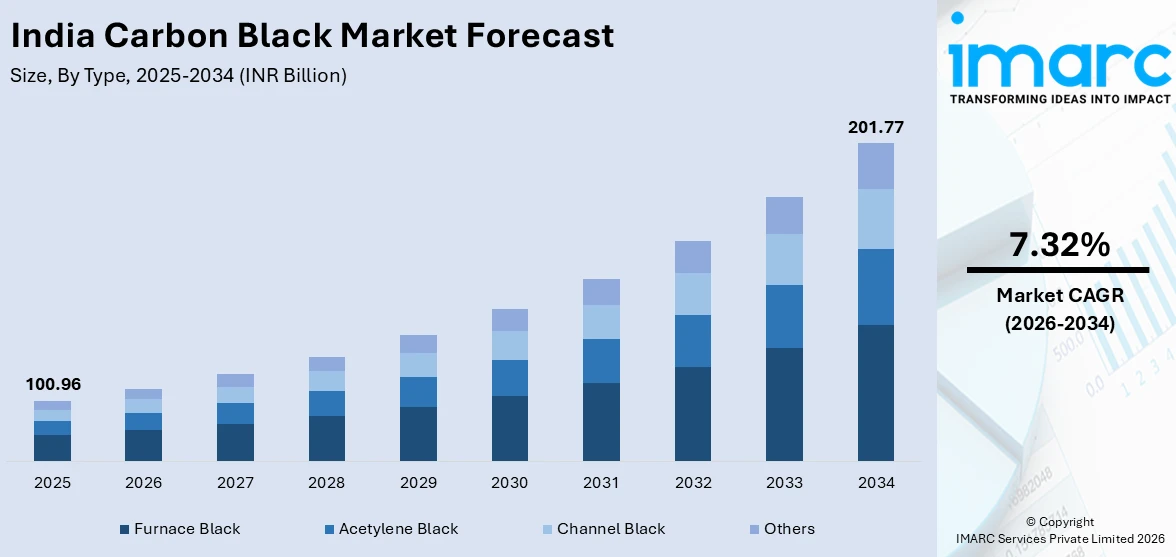

The India carbon black market size was valued at INR 100.96 Billion in 2025 and is projected to reach INR 201.77 Billion by 2034, growing at a compound annual growth rate of 7.32% during 2026-2034.

The India carbon black market is driven by robust growth in the automotive and tire manufacturing sectors, accelerating infrastructure development, and rising demand across plastics, specialty chemicals, and rubber goods industries. The growing adoption of high-performance specialty grades for conductive and ultraviolet (UV)-protective applications, alongside significant capacity investments by domestic producers, is reshaping the competitive landscape. Favorable government policies supporting industrial growth and electric vehicle (EV) adoption further contribute to the India carbon black market share.

Key Takeaways and Insights:

- By Type: Furnace black dominates the market with a share of 81.4% in 2025, owing to its cost-efficient, scalable production process and widespread use across tire manufacturing, rubber goods, and specialty applications.

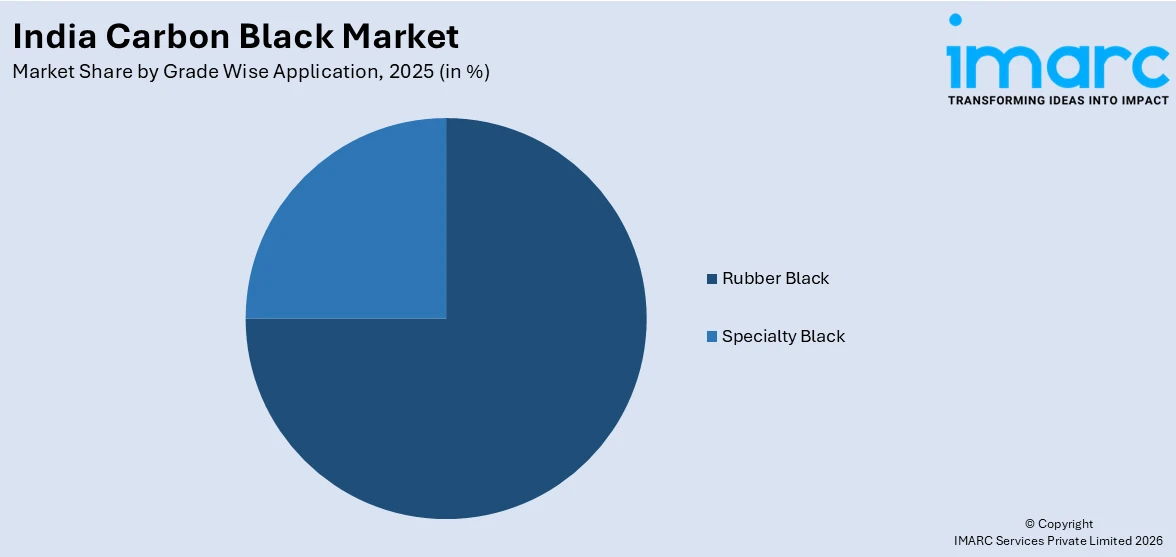

- By Grade Wise Application: Rubber black leads the market with a share of 72.9% in 2025, driven by India's extensive tire production base, growing two-wheeler and passenger vehicle sales, and heavy demand from conveyor belt, hose, and rubber goods manufacturers.

- By Region: South India represents the largest segment with a market share of 31.2% in 2025, anchored by major tire manufacturing hubs in Chennai and a dense concentration of rubber goods and automotive component plants across Tamil Nadu, Andhra Pradesh, and Karnataka.

- Key Players: The India carbon black market is moderately consolidated, with a few large domestic producers commanding significant capacity alongside global specialty players, competing on grade quality, production scale, sustainability credentials, and customer proximity. Some of the key players in the market include Phillips Carbon Black Limited (PCBL), Birla Carbon India Pvt. Ltd., Balkrishna Industries Limited (BKT), Himadri Specialty Chemical Ltd., Continental Carbon India Private Limited, Ralson Shine Carbon Ltd., Epsilon Carbon Private Limited, Cabot Corporation, and Selective Minerals and Color Industries Pvt. Ltd.

To get more information on this market Request Sample

The carbon black market in India is experiencing steady expansion as industries adopt more sustainable and performance-oriented materials across manufacturing sectors. Strong demand from the automotive and tire industries, combined with increasing infrastructure development, is contributing to higher usage of carbon black in rubber reinforcement and industrial applications. Manufacturers are also focusing on environmentally responsible production practices and the use of recycled raw materials to reduce environmental impact. This shift is encouraging innovation in recovered and sustainable carbon black solutions that maintain performance while supporting circular economy goals. In 2025, JK Tyre introduced India’s first ISCC Plus certified sustainable passenger car tire, UX Royale Green, produced using 80% sustainable, recycled, and renewable materials, including recovered carbon black. Such developments highlight the growing integration of sustainable carbon black in tire manufacturing as companies work toward reducing emissions and improving resource efficiency.

India Carbon Black Market Trends:

Shift Toward Sustainable and Low-Emission Supply Chains

Environmental sustainability is becoming a central priority for carbon black manufacturers and their downstream users. Companies are increasingly adopting cleaner transportation systems and energy-efficient logistics to reduce emissions associated with raw material and product movement. These initiatives help manufacturers align with global decarbonization goals while supporting companies in lowering their emissions. Cleaner freight solutions also improve fuel efficiency and reduce regulatory risks related to environmental compliance. As sustainability expectations grow across industrial supply chains, manufacturers are investing in alternative fuel vehicles and greener logistics operations. Reflecting this trend, in 2025, Epsilon Carbon introduced a fleet of six LNG-powered container trucks to transport carbon black, reducing carbon dioxide emissions by 20–25% and significantly lowering nitrogen oxide and particulate emissions compared with diesel vehicles.

Rising Demand for High-Performance Materials in Tire Manufacturing

The increasing production of premium and high-performance tires is driving the demand for advanced grades of carbon black with enhanced reinforcement properties. Tire manufacturers require materials that improve abrasion resistance, durability, and traction while maintaining performance under varying road conditions. Advanced carbon black grades enable stronger rubber compounds that enhance tire lifespan and safety. Domestic production of specialized carbon black also strengthens supply security and reduces dependence on imports, supporting the competitiveness of the local tire industry. Supporting this development, in 2025, Epsilon Carbon launched N134 grade hard carbon black for premium tire manufacturing, with planned production at its expanded Vijayanagar carbon complex. The development aimed to reduce India’s reliance on imports while enabling exports to high-end tire markets in the United States and Europe.

Expansion of Carbon Black Production Capacity

Increasing demand from automotive, industrial rubber, and specialty chemical sectors is encouraging carbon black manufacturers to expand their production capacity. Larger manufacturing facilities allow producers to supply growing domestic markets while supporting export opportunities. Capacity expansion also enables companies to produce specialized carbon black grades tailored to different industrial applications. Investments in new production lines and infrastructure strengthen supply reliability and improve operational efficiency across the value chain. Supporting this trend, in 2025, BKT announced a strategic investment plan of INR 3,500 crore aimed at increasing its carbon black production capacity from 200,000 to 360,000 metric tons annually.

Market Outlook 2026-2034:

The India carbon black market is projected to grow steadily, supported by increasing demand from the automotive, tire manufacturing, and industrial rubber sectors. Rising automobile production and replacement tire demand are contributing significantly to the market growth. Expanding industrial activities and investments in manufacturing are expected to sustain demand for carbon black across multiple end-use applications in India. The market generated a revenue of INR 100.96 Billion in 2025 and is projected to reach a revenue of INR 201.77 Billion by 2034, growing at a compound annual growth rate of 7.32% from 2026-2034.

India Carbon Black Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Furnace Black |

81.4% |

|

Grade Wise Application |

Rubber Black |

72.9% |

|

Region |

South India |

31.2% |

Type Insights:

- Furnace Black

- Acetylene Black

- Channel Black

- Others

Furnace black dominates with a market share of 81.4% of the total India carbon black market in 2025.

Furnace black holds the biggest market share due to its large-scale use in tire manufacturing and rubber processing industries. This type of carbon black is produced through the furnace process, which allows manufacturers to generate high volumes with consistent particle size and performance characteristics. Tire manufacturers prefer furnace black because it improves rubber strength, abrasion resistance, and durability, all of which are critical for vehicle tire performance. With India witnessing steady growth in automobile production and replacement tire demand, furnace black continues to be widely used. Its ability to enhance rubber reinforcement makes it a primary material used in tire treads and other rubber components.

Another factor supporting the dominance of furnace black is its versatility across multiple industrial applications. Apart from tires, furnace black is used in rubber goods like conveyor belts, hoses, gaskets, seals, and molded rubber products. The material also finds applications in plastics, coatings, and inks where color strength and UV protection are required. Manufacturers prefer furnace black because it can be produced in various grades suited for different performance requirements. As India’s automotive, construction, and industrial manufacturing sectors continue to expand, the demand for furnace black remains strong owing to its reliable performance and cost-effective production process.

Grade Wise Application Insights:

Access the comprehensive market breakdown Request Sample

- Rubber Black

- Tire Treads

- Inner Liner and Tubes

- Conveyor Belts

- Hoses

- Others

- Specialty Black

- Plastics

- Ink and Toners

- Paint and Coatings

- Wires and Cables

- Others

Rubber black leads with a market share of 72.9% of the total India carbon black market in 2025.

Rubber black represents the largest segment because of its extensive use in the tire and rubber manufacturing industries. Carbon black acts as a reinforcing filler that enhances the strength, durability, and abrasion resistance of rubber products. Tire manufacturers rely heavily on rubber-grade carbon black to improve tread performance, heat resistance, and overall product lifespan. With India experiencing consistent growth in vehicle production and replacement tire demand, the use of rubber-grade carbon black continues to rise. Automotive manufacturers, tire producers, and rubber component suppliers increasingly depend on this material to meet performance standards, making rubber black the most widely used grade in the market.

Another factor influencing the dominance of rubber black is the widespread production of industrial and consumer rubber goods across the country. Products, such as conveyor belts, hoses, seals, gaskets, footwear soles, and molded rubber components require rubber-grade carbon black to improve elasticity and mechanical strength. Manufacturing clusters supplying automotive, construction, and industrial equipment sectors rely on rubber black to maintain product quality and durability. Expanding infrastructure development and industrial activity further drive the demand for rubber-based products. In 2025: PCBL Chemical Ltd. selected a site for its sixth carbon black manufacturing facility in India, expanding its production footprint in the country. The project supported the company’s strategy to increase capacity and strengthen supply for rubber and specialty carbon black applications.

Regional Insights:

- South India

- West and Central India

- North India

- East India

South India exhibits a clear dominance with a 31.2% share of the total India carbon black market in 2025.

South India leads the market owing to the strong presence of tire manufacturing and automotive component industries across states, such as Tamil Nadu, Karnataka, and Andhra Pradesh. Carbon black is widely used as a reinforcing agent in tire production, making regions with established automotive manufacturing hubs key centers of demand. Cities, including Chennai and Bengaluru, host large automobile assembly plants and tire manufacturing facilities, which require consistent supplies of carbon black for production. The region’s well-developed industrial infrastructure and logistics networks also support efficient raw material distribution, allowing manufacturers to maintain steady production and supply across automotive and rubber product industries.

South India’s leadership in the carbon black market is also supported by the concentration of rubber goods manufacturers and established industrial production clusters across the region. A large number of companies producing conveyor belts, hoses, seals, footwear components, and other rubber-based products operate in states, such as Tamil Nadu and Karnataka, generating consistent demand for carbon black as a reinforcing and coloring agent. Reflecting this growing industrial demand, in 2024, Birla Carbon announced plans to establish new carbon black manufacturing facilities in Naidupet, Andhra Pradesh, with an initial production capacity of 120 kMT and plans to expand to 240 kMT. The region’s skilled workforce and supportive industrial policies continue to encourage manufacturing expansion and sustained consumption of carbon black.

Market Dynamics:

Growth Drivers:

Why is the India Carbon Black Market Growing?

Growing Adoption of Recycled Materials in Carbon Black Production

The increasing focus on circular economy practices is encouraging the development of recovered carbon black derived from recycled tires. Recycling technologies allow manufacturers to extract valuable carbonaceous materials from end-of-life tires and reuse them in new rubber products, coatings, and industrial applications. Recovered carbon black helps reduce dependence on fossil-based raw materials and lowers the environmental footprint of production. Many companies are investing in tire recycling infrastructure to support sustainable material recovery while addressing the global challenge of tire waste management. In line with this trend, in 2025, Epsilon Carbon launched its Terrablack recovered carbon black product line and began constructing a tire recycling facility in Karnataka to process large volumes of discarded tires.

Growth of Plastics and Polymer Manufacturing

Carbon black is widely used as a pigment and reinforcing agent in plastics and polymer-based materials. It provides ultraviolet protection, improves durability, and enhances electrical conductivity in certain polymer applications. Industries such as packaging, agriculture, construction, and consumer goods rely heavily on plastic products that incorporate carbon black to improve performance characteristics. As plastic production expands to support the growing industrial and individual demand, the use of carbon black in polymer compounds continues to increase. The expansion of plastic manufacturing facilities and polymer processing industries in India is contributing to the steady rise in carbon black usage across non-rubber applications.

Increasing Demand from Packaging Industry

The robust packaging sector in India is catalyzing the demand for carbon black in plastic and polymer applications. Carbon black is widely used in packaging materials to provide ultraviolet protection, color stability, and improved durability. Black polymer compounds are commonly used in industrial packaging, agricultural films, and protective plastic components where resistance to sunlight and environmental exposure is essential. The growth of organized retail, e-commerce distribution, and food processing industries is increasing demand for reliable packaging materials. Carbon black helps improve the strength and performance of plastic products used in these applications. As packaging demand continues to expand alongside consumer markets, there is a rise in the demand for carbon black in polymer applications.

Market Restraints:

What Challenges the India Carbon Black Market is Facing?

Volatility in Carbon Black Feedstock Prices

Carbon black production is highly dependent on carbon black feedstock, a heavy petroleum derivative whose price is closely correlated with crude oil market dynamics. Frequent swings in crude oil prices create significant cost volatility for producers, compressing margins when price increases cannot be fully passed through to customers with multi-year supply agreements.

Stringent Environmental Compliance Requirements Raising Operating Costs

Carbon black manufacturing generates particulate matter, sulfur dioxide, and other emissions requiring substantial investment in pollution control infrastructure. India's tightening environmental regulations, including mandates from the Central Pollution Control Board for enhanced emission monitoring and reductions in industrial pollutants, impose significant capital expenditure requirements on both existing and new production facilities.

Competition from Imported Carbon Black Grades in Specialty Segments

India's specialty carbon black market faces sustained competition from imported grades, particularly high-purity conductive blacks and specialty pigment-grade products manufactured in Europe, Japan, and the United States, where established technology advantages allow international producers to offer grades not yet produced domestically at commercial scale. Import competition limits the pricing power of domestic manufacturers in specialty applications and delays the development of a fully self-sufficient specialty carbon black value chain within India.

Competitive Landscape:

The India carbon black market is moderately consolidated, with a small number of large-scale domestic producers accounting for the majority of production capacity, while global specialty carbon black companies maintain targeted presence in high-margin application segments. The competitive environment is defined by ongoing capacity expansion, product portfolio diversification toward specialty grades, investment in sustainability and recovered carbon black technologies, and efforts to enhance export market penetration. Producers are differentiating through investments in specialty chemical capacity, post-treatment plant technologies, and strategic site selection near major port infrastructure to optimize supply chain efficiency. The market is increasingly shaped by customer requirements for sustainability certifications, low-PAH grade compliance, and circular economy credentials, prompting leading manufacturers to pursue recovered carbon black programs and expand conductive grade offerings to address battery and electronics applications.

Some of the key players in the market include:

- Phillips Carbon Black Limited (PCBL)

- Birla Carbon India Pvt. Ltd.

- Balkrishna Industries Limited (BKT)

- Himadri Specialty Chemical Ltd.

- Continental Carbon India Private Limited

- Ralson Shine Carbon Ltd.

- Epsilon Carbon Private Limited

- Cabot Corporation

- Selective Minerals and Color Industries Pvt. Ltd.

Recent Developments:

- December 2025: Birla Carbon highlighted its efforts to make carbon black production more circular through its Continua Sustainable Carbonaceous Materials (SCM) made from recovered carbon black sourced from end-of-life tires. The initiative supports sustainability in the tire, rubber, and automotive industries by providing alternatives to conventional carbon black. Birla Carbon aims to repurpose 300,000 tons of end-of-life tires annually by 2030, supporting circular material use and decarbonization goals.

- February 2026: Himadri Speciality Chemical Ltd began commercial production at a 70,000 MTPA specialty carbon black line at its Mahistikry facility in West Bengal. The expansion raised the plant’s specialty carbon black capacity to 130,000 MTPA, making it the world’s largest single-location facility for this product. The additional capacity supported rising demand for advanced carbon materials used in plastics, inks, paints, coatings, and other industrial applications.

- September 2025: PCBL Chemical Ltd, India’s largest carbon black manufacturer, unveiled the next phase of its carbon black innovation, highlighting sustainable solutions, such as ecozen®, a circular carbon black derived from recycled raw materials. The company also planned to expand R&D efforts in specialty carbon blacks for applications in EVs, plastics, coatings, and conductive polymers. These initiatives aimed to support sustainability goals while strengthening PCBL’s position in advanced materials and emerging automotive technologies.

India Carbon Black Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion INR |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Furnace Black, Acetylene Black, Channel Black, Others |

| Grade Wise Applications Covered |

|

| Regions Covered | South India, West and Central India, North India, East India |

| Companies Covered | Phillips Carbon Black Limited (PCBL), Birla Carbon India Pvt. Ltd., Balkrishna Industries Limited (BKT), Himadri Specialty Chemical Ltd., Continental Carbon India Private Limited, Ralson Shine Carbon Ltd., Epsilon Carbon Private Limited, Cabot Corporation, Selective Minerals and Color Industries Pvt. Ltd. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Carbon Black Market Report

The India carbon black market size was valued at INR 100.96 Billion in 2025.

The India carbon black market market is expected to grow at a compound annual growth rate of 7.32% during 2026-2034 to reach INR 201.77 Billion by 2034.

Furnace black dominates the India carbon black market with an 81.4% revenue share in 2025, owing to its cost-efficient production process, high scalability, and widespread application across tire, rubber goods, and specialty grade manufacturing.

Key factors driving the India carbon black market include the rising demand from automotive, industrial rubber, and specialty chemical sectors, encouraging manufacturers to expand capacity. Reflecting this trend, in 2025 BKT announced an investment of INR 3,500 crore to increase carbon black production from 200,000 to 360,000 metric tons annually.

Major challenges include volatility in carbon black feedstock prices linked to crude oil market dynamics, stringent environmental compliance requirements increasing operating costs, and competition from imported specialty grades in high-value application segments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade