India Cloud Kitchen Market Size, Share, Trends and Forecast by Type, Product Type, Nature, and Region, 2026-2034

India Cloud Kitchen Market Size, Share, Trends & Forecast (2026-2034)

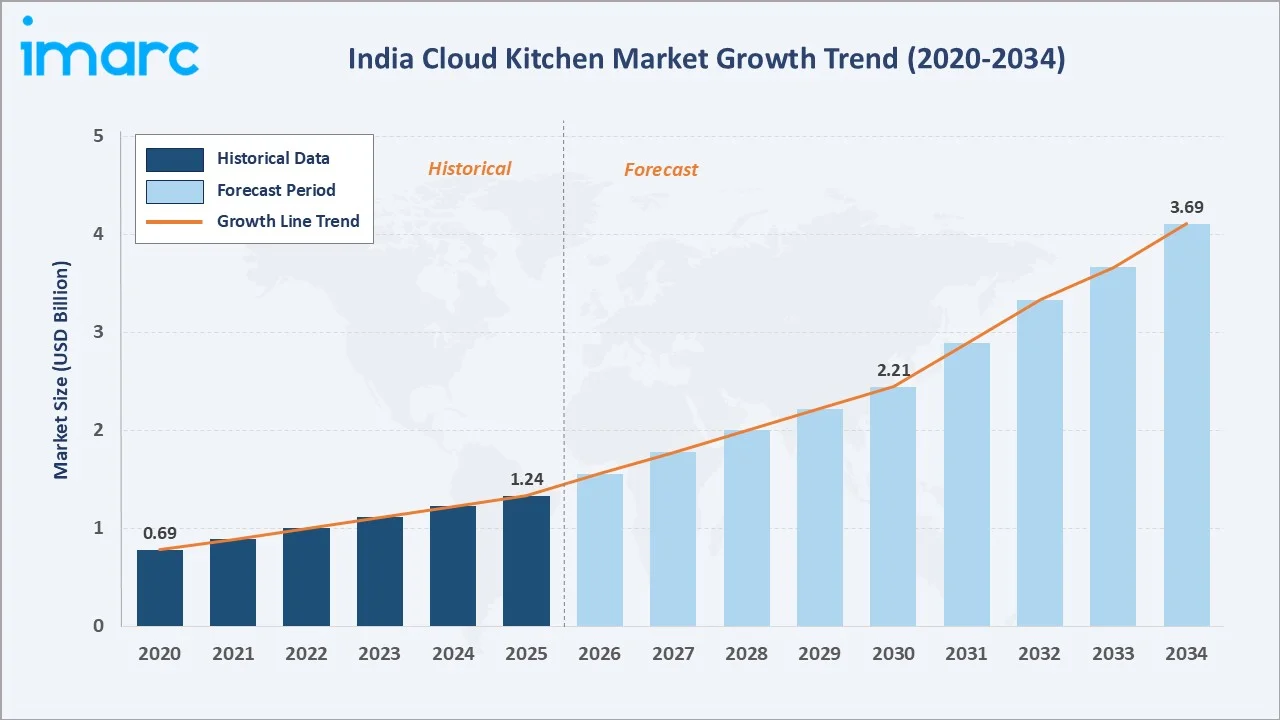

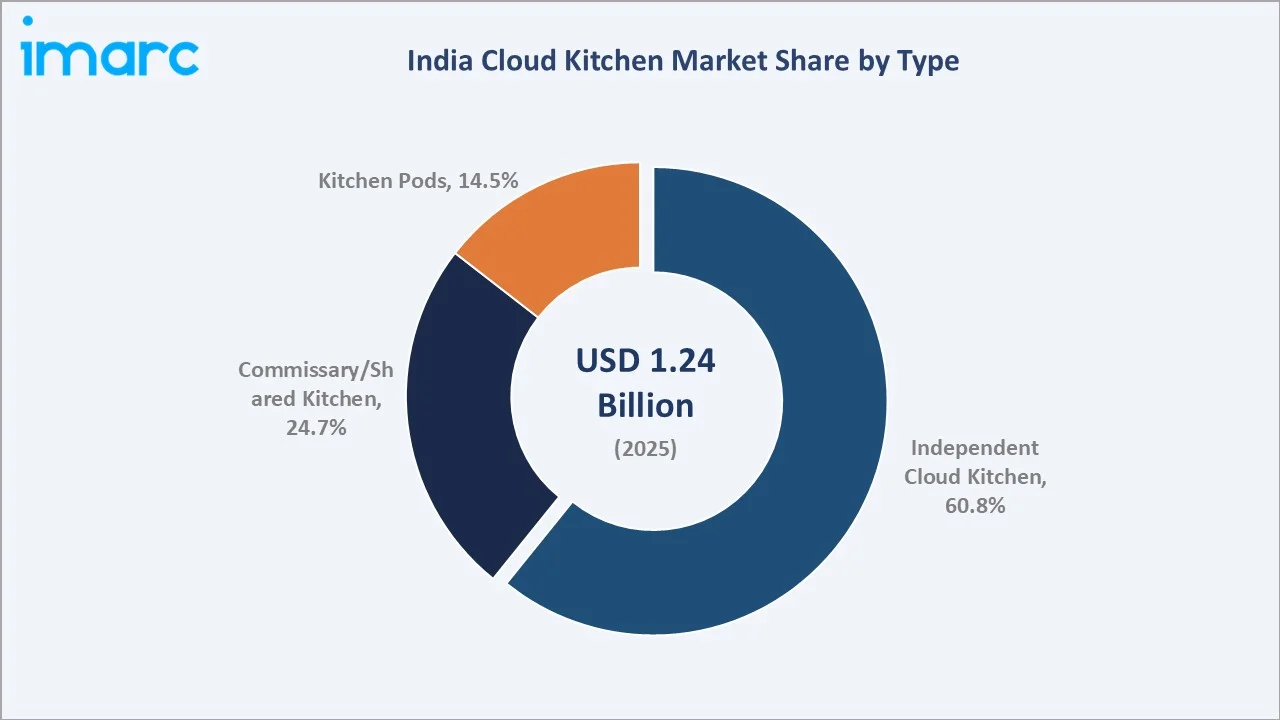

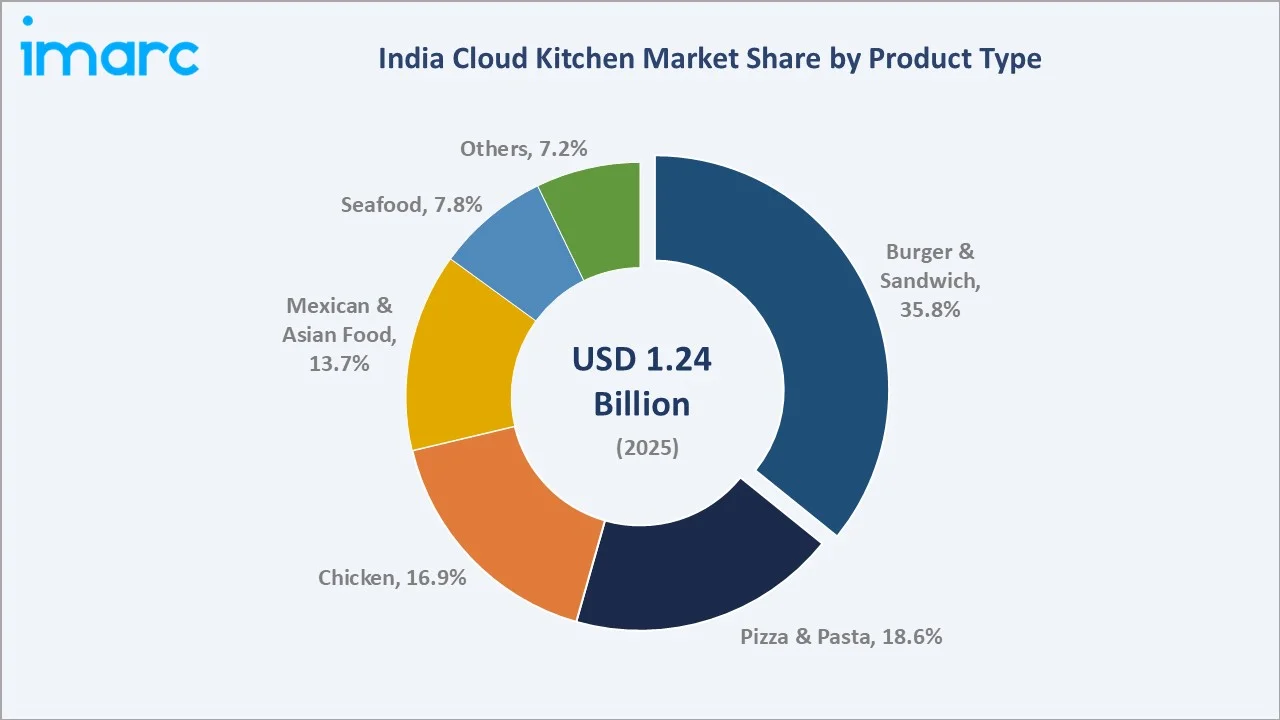

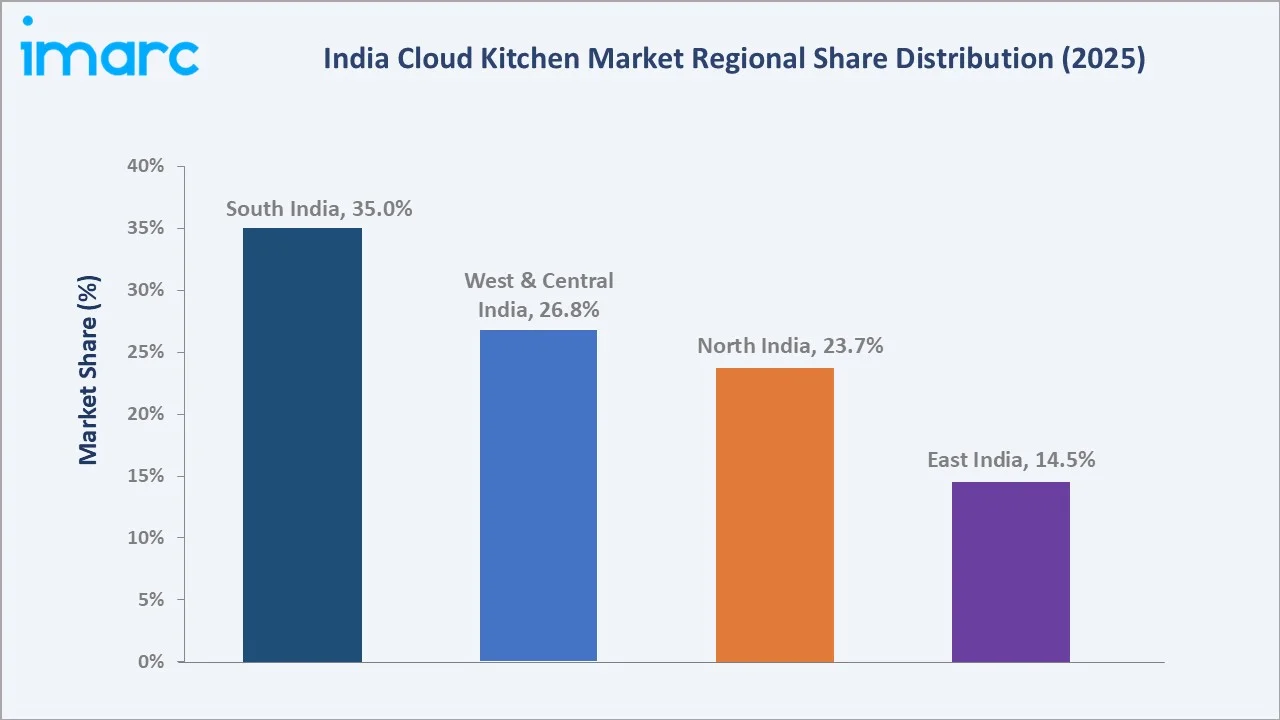

The India cloud kitchen market reached USD 1.24 Billion in 2025 and is projected to reach USD 3.69 Billion by 2034, growing at a CAGR of 12.28% during 2026-2034. The market is driven by rapid growth in online food delivery platforms, rising urbanization with towns and cities will be home to 600 million people, or 40% of the population by 2036, increasing smartphone and internet penetration, changing consumer dining preferences, and growing demand for convenient and affordable food ordering services. Independent cloud kitchen dominates at 60.8%. Burger and sandwich lead product type at 35.8%. South India commands 35.0% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.24 Billion |

|

Forecast Market Size (2034) |

USD 3.69 Billion |

|

CAGR (2026-2034) |

12.28% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Independent Cloud Kitchen (60.8%, 2025) |

|

Dominant Product Type |

Burger and Sandwich (35.8%, 2025) |

|

Leading Region |

South India (35.0%, 2025) |

The market expanded from USD 0.69 Billion in 2020 to USD 1.24 Billion in 2025, anchored at USD 2.21 Billion in 2030, and forecast to reach USD 3.69 Billion by 2034. COVID-19 transformed India's food service industry permanently. Restaurant closures in 2020 forced traditional restaurants to pivot to delivery-only operations while simultaneously accelerating cloud kitchen expansion, as their delivery-native model required zero operating model changes during lockdowns. The pandemic's lasting behavioral shift established the structural demand foundation sustaining the market's 12.28% CAGR.

To get more information on this market, Request Sample

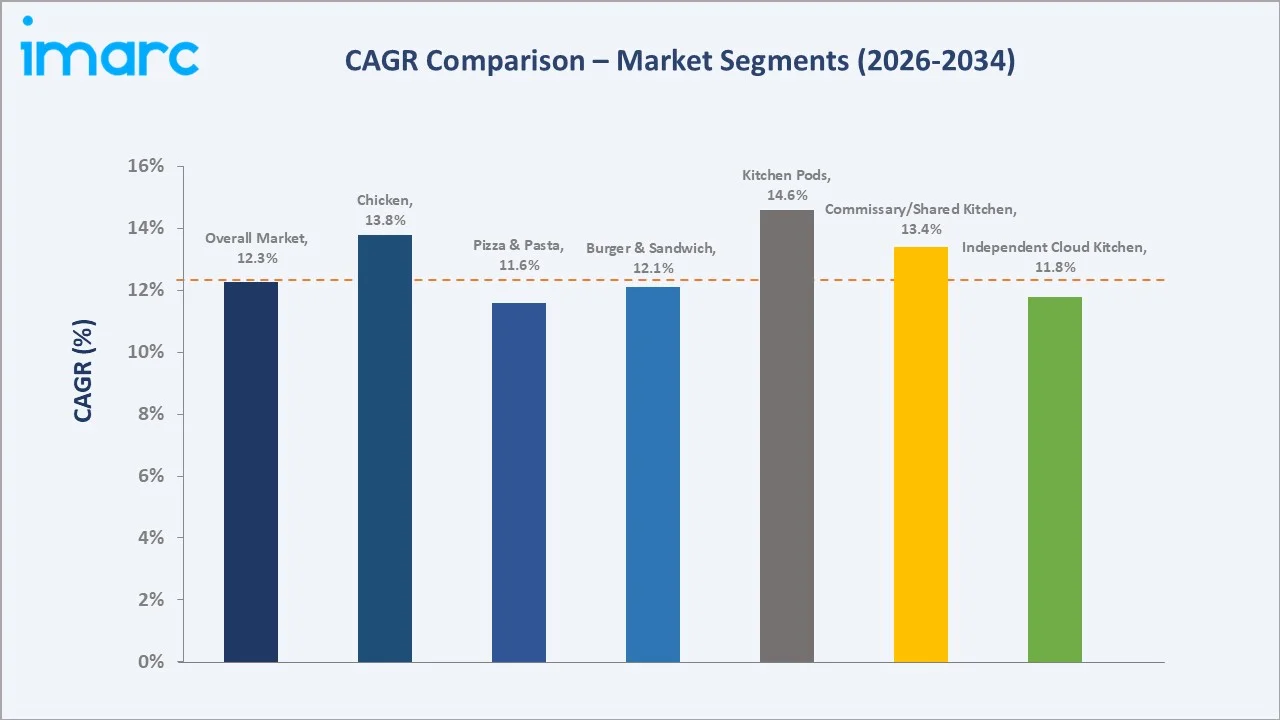

Kitchen pods grow fastest at ~14.6% CAGR (2026-2034) as India's real estate constraints drive innovation toward micro-format cloud kitchens deployable in apartment complex basements, mall food courts, and office park food courts. Chicken grows fastest at ~13.8% CAGR within product types as India's protein consumption evolves, the expanding Andhra and Mughlai chicken brand portfolio on delivery platforms, and chicken's superior unit economics make it the cloud kitchen industry's fastest-growing cuisine category.

Executive Summary

The India cloud kitchen market reached USD 1.24 Billion in 2025, representing the most structurally innovative segment of India's food service industry and one of the world's fastest-growing cloud kitchen markets. India's cloud kitchen ecosystem is uniquely positioned at the intersection of three macro forces: the Swiggy-Zomato food delivery duopoly that has created active food ordering consumers generating high annual food orders; India's urban real estate crisis; and a generation of food entrepreneurs who can now build national food brands from a single rented kitchen without any dining room infrastructure. The market is projected to reach USD 3.69 Billion by 2034 at 12.28% CAGR.

Independent cloud kitchen at 60.8% dominates as the preferred model for both established food brands and individual food entrepreneurs. Burgers and sandwiches dominate at 35.8%. South India at 35.0% leads through Bengaluru's cloud kitchen market maturity and tech workforce food ordering intensity.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Independent Cloud Kitchen - 60.8% share (2025) |

|

Dominant Product Type |

Burger and Sandwich - 35.8% market share (2025) |

|

Leading Region |

South India - 35.0% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Independent Cloud Kitchen at 60.8% driven by India's food entrepreneurship wave and Rebel Foods' multi-brand model validation: The independent cloud kitchen model has proven commercially superior in India for three distinct operator segments: large multi-brand operators, mid-size single-brand operators, and micro-entrepreneurs.

- Burger and Sandwich at 35.8% reflecting Indian youth's QSR cuisine preference and cloud kitchen's operational alignment with assembly-line cooking: Burgers, wraps, and sandwiches represent cloud kitchen's operationally ideal product category, requiring no complex cooking chemistry, highly standardizable preparation procedures enabling consistent quality across multiple kitchen locations, packaging-friendly for delivery, and favorably received by India's 18-35 age demographic that constitutes 70%+ of cloud kitchen order volume.

- South India at 35.0% reflecting Bengaluru-Hyderabad-Chennai's cloud kitchen market maturity and tech workforce ordering intensity: Bengaluru's tech workforce orders food delivery driven by the combination of long working hours, single-occupancy apartment living, high disposable income, and a culinarily adventurous culture that embraces global cuisines delivered locally.

India Cloud Kitchen Market Overview

India's cloud kitchen market encompasses all commercial food preparation and delivery operations without customer-facing dining spaces, delivery-only restaurant brands operating from dedicated cooking facilities (independent cloud kitchens), shared commercial kitchen spaces rented by multiple food brands (commissary/shared kitchens), and ultra-compact kitchen units deployed in high-density residential and commercial locations (kitchen pods). The market serves India's online food ordering consumers through Swiggy and Zomato delivery platforms and emerging direct-ordering channels. Cloud kitchen is distinct from conventional restaurants by its complete absence of dine-in infrastructure, delivery-only business model, and technology-native operations using data analytics for menu optimization, demand forecasting, and kitchen efficiency management.

The ecosystem integrates real estate operators, kitchen equipment suppliers, regulatory compliance infrastructure, food delivery platform aggregators, technology providers, cloud kitchen brands, ingredient suppliers, packaging suppliers, delivery partner networks, and end consumers across India's urban delivery zones. Macroeconomic factors include rising urban population, increasing disposable incomes, expanding digital payment adoption, growing internet and smartphone penetration, and rapid growth of the food delivery ecosystem.

Market Dynamics

To evaluate market opportunities, Request Sample

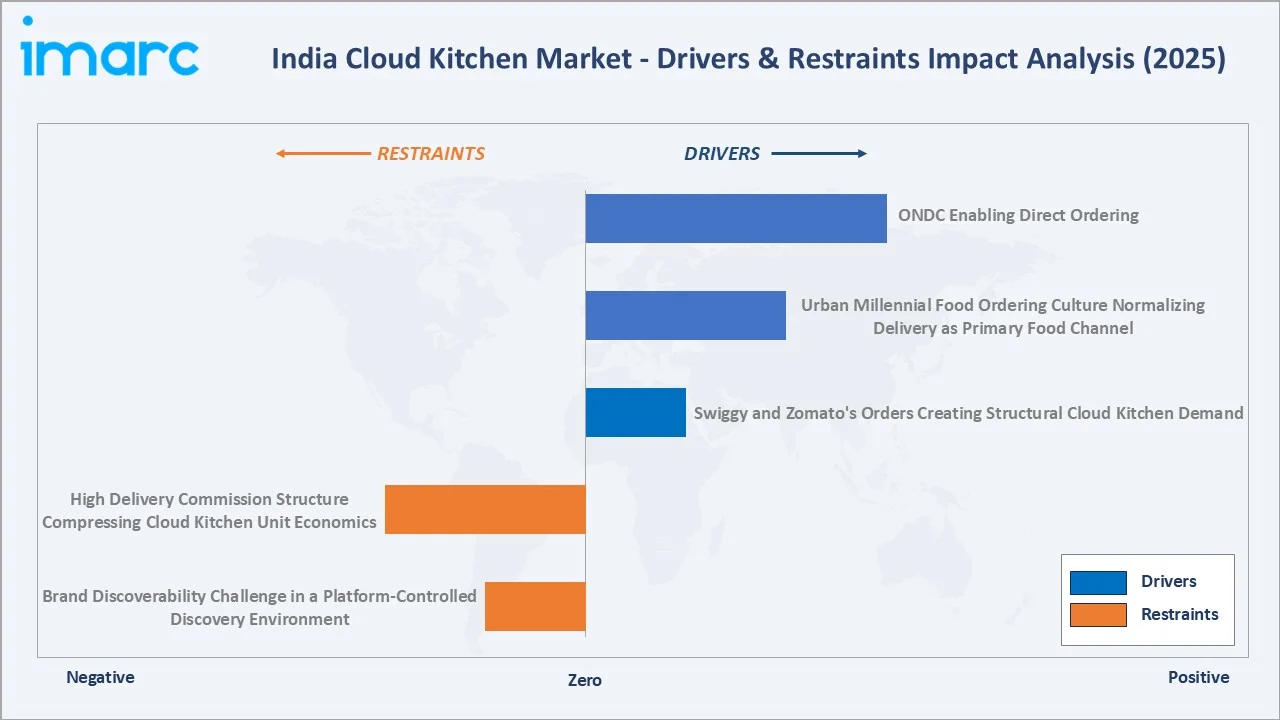

Market Drivers

- Swiggy and Zomato's Orders Creating Structural Cloud Kitchen Demand: India's food delivery market has achieved a scale that creates natural infrastructure demand for delivery-optimized kitchen formats. Swiggy reported that India ordered 93 million biryanis in 2025, including 57.7 million chicken biryanis. Burgers recorded 44.2 million orders, pizzas reached 40.1 million, while veg dosa accounted for 26.2 million orders. Snack-time demand remained strong with 3.42 million samosas and 2.9 million adrak chai orders, whereas white chocolate cake emerged as the top dessert with 6.9 million orders. This order volume creates a demand-guaranteed marketplace where a new cloud kitchen brand listing on Swiggy and Zomato can expect high orders daily within 30 days of launch in any Tier-1 city.

- Urban Millennial Food Ordering Culture Normalizing Delivery as Primary Food Channel: India's 18-35 age group has normalized food delivery as a primary eating occasion rather than an exceptional convenience. The behavioral factors sustaining this pattern are structural rather than cyclical: India's urban nuclear family structure, apartment living in dense urban clusters with a 3-5 km delivery radius, overlap with cloud kitchens, Swiggy and Zomato's gamification, and India's digital payment infrastructure collectively sustain ordering frequency.

- ONDC Enabling Direct Ordering: Government of India's Open Network for Digital Commerce (ONDC) creates an alternative delivery channel where cloud kitchens can receive orders through any ONDC-connected buyer application at 5-10% commission versus Swiggy and Zomato's 25-30% commission.

Market Restraints

- High Delivery Commission Structure Compressing Cloud Kitchen Unit Economics: Swiggy and Zomato's 25-30% commission on cloud kitchen orders significantly compresses cloud kitchen profitability. This commission structure has created an existential economic pressure on cloud kitchens operating at below-optimal volumes, contributing to India's cloud kitchen attrition rate of 30-40% annually as under-scaled operators exit the market.

- Brand Discoverability Challenge in a Platform-Controlled Discovery Environment: Swiggy and Zomato's restaurant ranking algorithms create discovery inequality where well-funded brands with high review counts, premium placement fees, and aggressive discount offers rank prominently while new cloud kitchen brands struggle for visibility.

Market Opportunities

- Corporate Meal Subscription Market as Cloud Kitchen's Highest-Margin Revenue Stream: India's organized sector employs huge workers across IT campuses, manufacturing plants, BPO operations, and corporate offices, each representing a captive meal ordering opportunity for cloud kitchens located within 3-5 km of office clusters.

- Tier-2 City Expansion as Cloud Kitchen's Next Growth Frontier: India's Tier-2 cities represent the cloud kitchen market's largest untapped opportunity. These cities share three characteristics ideal for cloud kitchen growth: rising disposable income, limited organized restaurant infrastructure, and growing Swiggy-Zomato penetration.

Market Challenges

- Regulatory Compliance Complexity and Municipal Licensing for Cloud Kitchen Operations: Regulations require cloud kitchens to obtain separate food business operator licenses for each brand operating from a shared kitchen location, creating administrative complexity where a commissary kitchen housing 15 brands requires 15 separate licenses, periodic inspections, and documentation for each brand. The regulatory burden has pushed organized cloud kitchen operators to invest in dedicated compliance teams while creating a structural barrier to entry that smaller operators navigate with greater difficulty.

- Food Inflation and Ingredient Cost Volatility Compressing Already-Thin Margins: India's food commodity price volatility creates severe margin compression for cloud kitchens operating fixed-price delivery menus. Unlike dine-in restaurants that can adjust portion sizes or quality imperceptibly, cloud kitchen menus are displayed with fixed photographs on Swiggy and Zomato, making unnoticed portion size reduction impossible and visible price increases triggering algorithmic ranking penalties as consumer ratings temporarily decline during price adjustment periods.

Emerging Market Trends

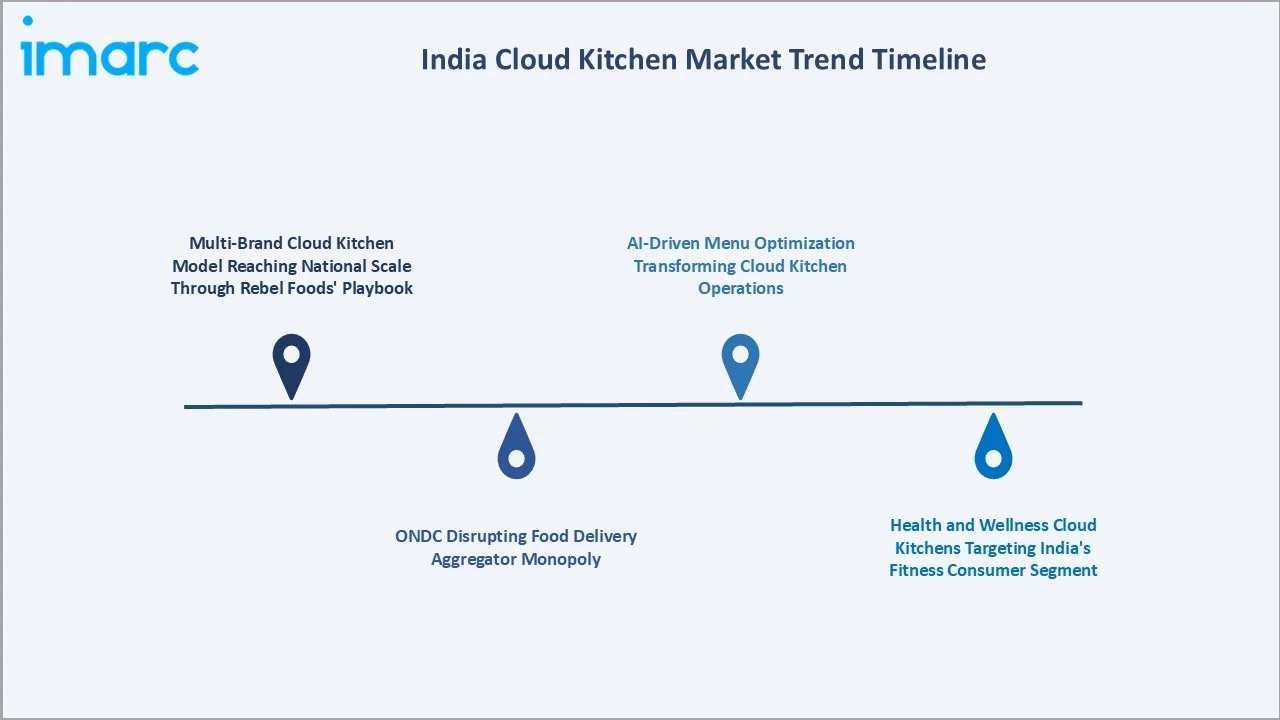

1. Multi-Brand Cloud Kitchen Model Reaching National Scale Through Rebel Foods' Playbook

The multi-brand cloud kitchen model is emerging as operators increasingly manage multiple food brands from shared kitchen infrastructure to improve operational efficiency and profitability. Companies such as Rebel Foods have demonstrated scalable national expansion by leveraging data analytics, delivery-focused menus, centralized supply chains, and asset-light kitchen networks across multiple Indian cities.

2. ONDC Disrupting Food Delivery Aggregator Monopoly

The expansion of the Open Network for Digital Commerce (ONDC) is reducing dependence on dominant food delivery aggregators and enabling more direct digital access to consumers. Cloud kitchens are increasingly leveraging ONDC to lower commission costs, improve profit margins, and gain greater control over pricing, customer relationships, and delivery operations. The open-network model is also encouraging participation from smaller food brands, regional kitchens, and independent restaurant operators across India’s rapidly growing online food delivery ecosystem.

3. Health and Wellness Cloud Kitchens Targeting India's Fitness Consumer Segment

Health and wellness-focused cloud kitchens are emerging as consumers increasingly seek calorie-conscious, protein-rich, organic, and diet-specific meal options. Cloud kitchen operators are expanding offerings such as keto meals, vegan foods, diabetic-friendly diets, and fitness nutrition plans to cater to health-conscious urban consumers and gym-going populations. The rising influence of preventive healthcare, fitness culture, and nutrition-focused digital platforms is further accelerating demand for specialized healthy food delivery services across Indian cities.

4. AI-Driven Menu Optimization Transforming Cloud Kitchen Operations

AI-driven menu optimization helping operators analyze consumer preferences, ordering patterns, pricing behavior, and regional food demand in real time. Cloud kitchens are increasingly using AI and data analytics to refine menus, predict high-demand dishes, reduce food wastage, and improve inventory planning and operational efficiency. The technology is also supporting personalized recommendations, dynamic pricing strategies, and faster product innovation across digital food delivery platforms.

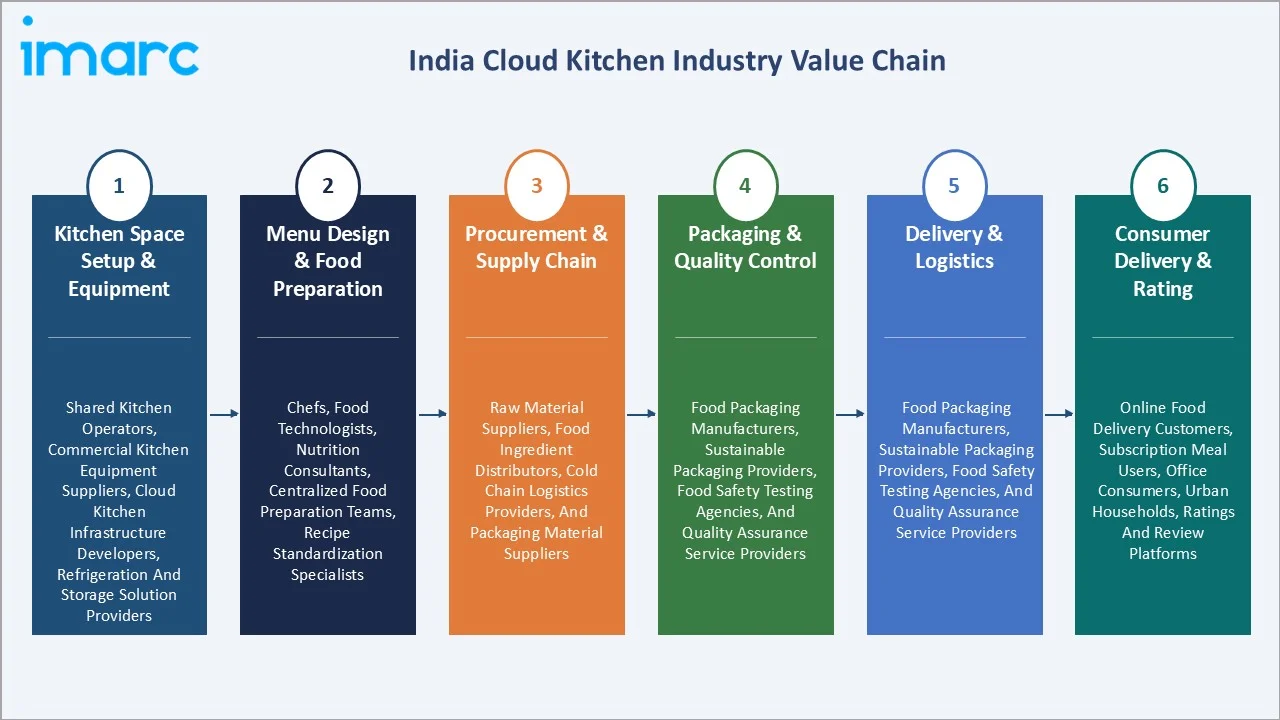

Industry Value Chain Analysis

India's cloud kitchen value chain integrates kitchen space acquisition, food production and quality management, platform listing and order management, delivery logistics, and consumer feedback systems. Cloud kitchen operators retain 70-75% of gross order value after delivery commission (25-30%), generating contribution margins of 15-25% after food cost (28-34%), packaging (3-5%), rent (5-8%), and labor (8-12%). EBITDA margins of 8-15% at mature cloud kitchens compare favorably to dine-in restaurants' 5-12% EBITDA after accounting for front-of-house costs.

|

Stage |

Key Participants |

|

Kitchen Space Setup & Equipment |

Shared kitchen operators, commercial kitchen equipment suppliers, cloud kitchen infrastructure developers, refrigeration and storage solution providers |

|

Menu Design & Food Preparation |

Chefs, food technologists, nutrition consultants, centralized food preparation teams, recipe standardization specialists |

|

Procurement & Supply Chain |

Raw material suppliers, food ingredient distributors, cold chain logistics providers, and packaging material suppliers |

|

Packaging & Quality Control |

Food packaging manufacturers, sustainable packaging providers, food safety testing agencies, and quality assurance service providers |

|

Delivery & Logistics |

Last-mile delivery companies, third-party logistics providers, fleet management firms, and hyperlocal delivery partners |

|

Consumer Delivery & Rating |

Online food delivery customers, subscription meal users, office consumers, urban households, ratings and review platforms |

The delivery partner pickup tier is the value chain's most operationally critical external dependency. Delivery partner availability during peak hours, delivery time consistency, and delivery packaging integrity determine cloud kitchen repeat order rates as much as food quality.

Technology Landscape in the India Cloud Kitchen Industry

Cloud Kitchen Management Software and POS Systems

Cloud kitchen management software and POS systems enabling centralized order management, real-time inventory tracking, kitchen automation, and seamless integration with multiple food delivery platforms. In December 2025, Sapaad entered the Indian market with its cloud-based and AI-driven restaurant technology platform, focusing on organized and technology-oriented foodservice businesses. The company is targeting approximately 5–6 lakh structured food and beverage outlets across segments such as quick service restaurant chains, franchise-led brands, cafés, bakeries, cloud kitchens, and mid-sized restaurant operators.

Demand Forecasting and Inventory Optimization AI

AI-driven demand forecasting and inventory optimization technologies are helping operators predict consumer ordering patterns, peak demand periods, and ingredient requirements with greater accuracy. Cloud kitchens are increasingly using AI analytics to minimize food wastage, streamline procurement planning, optimize stock levels, and improve kitchen efficiency. These technologies also support dynamic menu planning, cost control, and faster operational decision-making across multi-brand cloud kitchen networks.

Packaging Technology for Delivery-Optimized Food Quality

Packaging technology focused on delivery-optimized food quality improves food freshness, temperature retention, spill resistance, and delivery durability. Cloud kitchens are increasingly adopting insulated, tamper-proof, microwave-safe, and sustainable packaging solutions to enhance customer experience during long-distance deliveries. Advanced packaging designs are also helping maintain food texture and presentation quality while supporting branding, hygiene assurance, and eco-friendly delivery practices.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Independent Cloud Kitchen |

60.8% |

2025 |

|

Product Type |

Burger and Sandwich |

35.8% |

2025 |

|

Nature |

🔒 |

🔒 |

2025 |

|

Region |

South India |

35.0% |

2025 |

By Type

Independent cloud kitchen leads at 60.8% market share (2025). This segment encompasses all delivery-only kitchen operations within dedicated, brand-exclusive kitchen spaces. Independent cloud kitchens offer complete operational control (menu flexibility, brand identity management, ingredient sourcing autonomy) that commissary kitchens restrict, justifying higher upfront capital for operators with established brand equity or volume scale.

To access detailed market analysis, Request Sample

Commissary/shared kitchen at 24.7% grows at ~13.4% CAGR as India's cloud kitchen infrastructure matures and shared kitchen operators professionalise and expand. Kitchen pods at 14.5% grow fastest at ~14.6% CAGR through real estate innovation, enabling ultra-compact kitchen deployment in previously untapped locations.

By Product Type

Burger and sandwich leads at 35.8% market share (2025). India's burger and sandwich cloud kitchen segment benefits from QSR culture adoption, youth demographic alignment, and preparation standardization. Pizza and pasta at 18.6% are driven by Domino's ghost kitchen strategy, Oven Story (Rebel Foods), MOJO Pizza, and independent pizza cloud brands.

Chicken at 16.9% grows fastest at ~13.8% CAGR through Andhra-style chicken brands, Mughlai chicken cloud kitchens, and KFC-style delivery-only chicken brands serving India's rising protein consumption. Mexican and Asian food at 13.7% encompasses Chinese cloud kitchens, Thai, Japanese, and Mexican brands. Seafood at 7.8% is concentrated in coastal states, where fresh seafood delivery cloud kitchens achieve premium pricing and high repeat order rates. Others at 7.2% covers Indian regional cuisines, health bowls, desserts, and beverages.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

South India |

35.0% |

Strong urbanization, high online food delivery adoption, large working professional populations, and expanding digital consumer ecosystems across major metropolitan cities. |

|

West and Central India |

26.8% |

Driven by dense urban populations, busy lifestyles, high smartphone penetration, and growing preference for convenient online food ordering services. |

|

North India |

23.7% |

Supported by rising cloud kitchen penetration in metropolitan and tier-2 cities, increasing office-going populations, and expanding food delivery platform usage. |

|

East India |

14.5% |

Increasing digital adoption, expanding food delivery networks, rising young consumer populations, and growing demand for affordable online meal options. |

South India's 35.0% market leadership reflects Bengaluru's position as both the birthplace and most mature market of India's cloud kitchen industry. The South India leadership reflects structural demographic advantages: the region's tech workforce concentration, the highest urban household food delivery frequency in India, and South India's culinary diversity collectively create the optimal cloud kitchen market conditions.

West and Central India's 26.8% reflects Mumbai's commercial-capital food service intensity and Pune's rapidly maturing cloud kitchen ecosystem. North India's 23.7% is driven by Delhi NCR's Gurugram corporate cluster and North India's specific cuisine appetite, creating distinct demand characteristics. East India's 14.5% is growing as Kolkata's tech and professional workforce adopts digital food ordering, and Bhubaneswar-Guwahati emerge as high-growth Tier-2 cloud kitchen markets with limited organized food service competition.

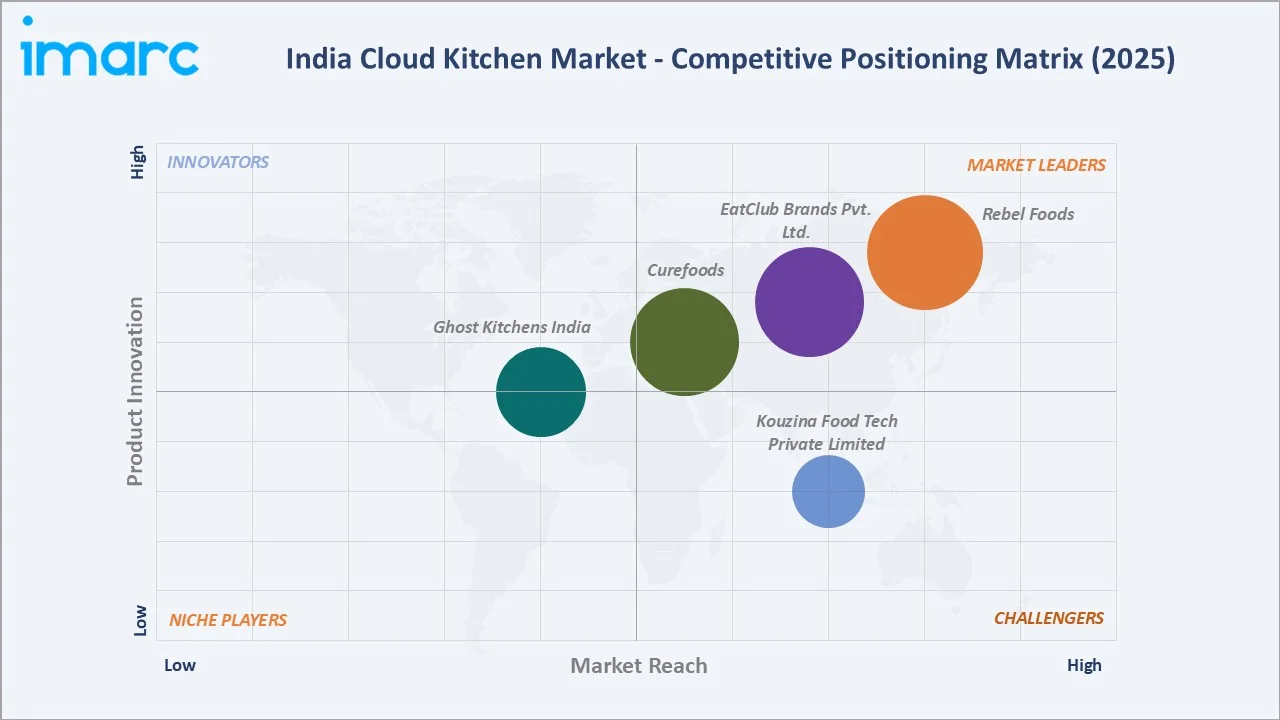

Competitive Landscape

India's cloud kitchen market exhibits moderate concentration with Rebel Foods commanding the largest single-operator market share alongside a highly fragmented long tail of independent cloud kitchen operators. This creates a structural tension where aggregators benefit from cloud kitchen GMV growth while simultaneously extracting 25-30% commission that limits independent cloud kitchen profitability.

|

Company Name |

Brands |

Market Position |

Core Strength |

|

Rebel Foods |

Faasos, Mandarin Oak, Sweet Truth, Behrouz Biryani, Lunch Box, Oven Story, The Good bowl |

Market Leader |

One of India’s leading cloud kitchen companies, operating multiple digital food brands through technology-driven, delivery-focused kitchen networks across major Indian cities and international markets. |

|

EatClub Brands Pvt. Ltd. |

BOX8, Mojo Pizza, LeanCrust Pizza, NH1 Bowls |

Market Leader |

Multi-brand delivery-focused kitchen model with a strong urban customer base and centralized operations. |

|

Curefoods |

EatFit, CakeZone, Arambam, Nomad Pizza, Sharief Bhai Biryani, Krispy Kreme |

Market Leader |

Strong presence in health-focused and multi-cuisine cloud kitchen operations with rapid expansion. |

|

Kouzina Food Tech Private Limited |

WarmOven, KaatiZone, Indiana Burgers, Burger It Up |

Strong Challenger |

Asset-light franchise-led cloud kitchen expansion with technology-enabled operations. |

|

Ghost Kitchens India |

BadBoy Pizza, Speak Burgers, Maa Ki Khichdi |

Emerging Player |

Shared kitchen infrastructure and scalable cloud kitchen management solutions. |

The competitive landscape is being reshaped by ONDC's disruption potential, which eliminates the aggregator commission advantage that large cloud kitchen operators can negotiate through volume but which benefits all operators equally on the ONDC network. The emergence of subscription-first cloud kitchen models, commissary kitchen infrastructure platforms, and health-focused positioning creates competitive differentiation dimensions beyond cuisine category and price, reflecting the market's maturation from a pure delivery-channel play toward genuine food brand building.

Key Company Profiles

Rebel Foods

Rebel Foods is India's first unicorn cloud kitchen company and the world's largest internet restaurant company by brand count.

- Brands: Faasos, Mandarin Oak, Sweet Truth, Behrouz Biryani, Lunch Box, Oven Story, The Good bowl.

- Recent Developments: In February 2026, Rebel Foods, through its Rebel Launcher brand growth platform, partnered with food brand Easybites to accelerate its expansion across major Indian markets. Under the collaboration, Easybites is currently live across 10 Rebel Foods cloud kitchens in Bengaluru & Hyderabad, with plans to scale into additional cities like Chennai and more locations in the coming months.

- Strategic Focus: Expanding its multi-brand cloud kitchen ecosystem through AI-driven operations, rapid delivery models, hybrid dine-in expansion, and technology-enabled food delivery platforms across India and international markets.

Curefoods

Curefoods is one of India’s leading cloud kitchens and digital-first food service companies, operating a diversified portfolio of food brands through technology-enabled delivery and omnichannel kitchen networks.

- Brands: EatFit, CakeZone, Arambam, Nomad Pizza, Sharief Bhai Biryani, Krispy Kreme.

- Recent Developments: In May 2025, Curefoods acquired the pan-India rights for global doughnut and coffee brand Krispy Kreme, strengthening its expansion strategy in the northern region of the country. The acquisition is expected to support wider nationwide growth and accelerate Krispy Kreme’s retail and delivery presence across India.

- Strategic Focus: Expanding its multi-brand cloud kitchen portfolio through acquisitions, omnichannel food delivery expansion, AI-driven operational efficiency, and premium food brand scaling across India.

Market Concentration Analysis

India's cloud kitchen market operates with a two-tier concentration structure: high concentration among platform aggregators alongside extreme fragmentation at the cloud kitchen operator level. Rebel Foods' estimated 8-12% GMV share represents the market's maximum single-operator concentration. The remaining percentage of market GMV is distributed among independent cloud kitchen operators, none of which individually holds more than 0.1% market share.

This concentration structure creates distinct competitive dynamics: the aggregator duopoly exercises market power through commission rate setting and algorithm-driven visibility allocation that is disproportionate to cloud kitchen operators' individual commercial leverage. Only Rebel Foods has sufficient GMV scale to negotiate below-standard commission rates with aggregators, creating a commission advantage unavailable to India's independent cloud kitchen operators who pay full 25-30% platform fees.

Investment & Growth Opportunities

Fastest Growing Segments

Kitchen pods (~14.6% CAGR), commissary/shared kitchen (~13.4% CAGR), chicken product type (~13.8% CAGR), East India region (~12%+ CAGR), Tier-2 city expansion (~18-20% CAGR within Tier-2 cities), and corporate meal subscription (~25%+ CAGR within cloud kitchen revenue streams) represent India's highest-growth cloud kitchen investment vectors through 2034.

Emerging Market Opportunities

India's Tier-2 cloud kitchen market represents the most significant greenfield investment opportunity in food service, where organized food delivery exists but cloud kitchen density remains 10-20% of equivalent Tier-1 city levels. The commissary kitchen model is particularly well-suited for Tier-2 city entry. Commissary kitchen at INR 60,000-120,000 monthly rent can host 8-15 cloud kitchen brands serving a city's entire delivery market, generating INR 30-50 Lakh monthly GMV at investment levels that Tier-1 city real estate economics would prohibit.

Investment Themes

- Commissary kitchen infrastructure development in Tier-2 cities: Building regulatory-compliant commissary kitchens in 20-30 emerging Tier-2 cities at INR 30-80 Lakh per city provides rental income from 10-15 cloud kitchen tenants while capturing a share of the local food delivery market. Real estate private equity firms with commercial real estate expertise are well-positioned to create cloud kitchen real estate investment vehicles analogous to co-working office real estate in scale and investment thesis.

- Health-focused cloud kitchen brand development for gym-adjacent locations: India's gym members, representing a captive meal delivery market adjacent to gyms, are systematically underserved outside Bengaluru and Mumbai. Launching EatFit-equivalent health cloud kitchen brands in 10-15 gym-dense cities, corporate wellness subscription sales to nearby IT campuses, and AI personalization based on fitness app data integration creates a differentiated cloud kitchen concept with sustainable repeat order economics.

Future Market Outlook (2026-2034)

The India cloud kitchen market is projected to grow from USD 1.24 Billion in 2025 to USD 3.69 Billion by 2034, delivering a 12.28% CAGR over the forecast period. The market's anchor value of USD 2.21 Billion in 2030 represents a cloud kitchen industry at structural maturity in Tier-1 cities, while simultaneously experiencing rapid Tier-2 city adoption, where first-mover advantage is available to operators building commissary kitchen infrastructure and corporate meal subscription businesses before market saturation.

Three structural forces define India's cloud kitchen market trajectory with high confidence through 2034: Swiggy and Zomato's user base creates proportional cloud kitchen demand growth as each platform customer generates average INR 2,000-3,000 annual cloud kitchen GMV; ONDC's progressive market share growth systematically improving cloud kitchen economics by reducing commission from 25-30% to an ONDC-blended 15-20% effective commission rate, enabling profitability at lower order volumes and sustaining market entry for new operators; and kitchen pod and commissary kitchen model maturation expanding cloud kitchen beyond the tech-workforce metro demographics that currently constitute 60%+ of the market toward Tier-2 cities, corporate campuses, and residential clusters where kitchen pod economics enable profitable operations at 30-50 daily orders.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including cloud kitchen operations heads; Partner Success and Cloud Kitchen program managers from Swiggy and Zomato; FSSAI and municipal BBMP/BMC food licensing officials; real estate advisors specializing in cloud kitchen space; delivery partner fleet managers for cloud kitchen-dense delivery zones; and 100+ end-consumer interviews with regular cloud kitchen orderers across Bengaluru, Mumbai, Delhi NCR, Hyderabad, and Chennai.

Secondary Research

Secondary research encompassed FSSAI Annual Report 2024-25 (food business operator registration data), Swiggy and Zomato annual reports and investor presentations (FY2023-FY2025), Rebel Foods and company press releases and investor communications, Google India Consumer Food Ordering Survey 2025, RedSeer Consulting India Online Food Delivery Report 2025, NRAI (National Restaurant Association of India) cloud kitchen survey 2024, ONDC Foundation food delivery statistics Q4 2025, NASSCOM India food-tech startup database, Indian Angel Network cloud kitchen investment data 2020-2025, and Razorpay Small Business Cloud Kitchen Report 2025. Over 65 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up cloud kitchen type and product type models calibrated against Swiggy and Zomato platform GMV disclosure data, FSSAI cloud kitchen operator registration count progression, ONDC food delivery monthly order volume data, and per-kitchen average GMV progression models from Rebel Foods' financial disclosures. Key inputs include India smartphone internet user growth projections, Swiggy and Zomato active user base expansion forecasts, ONDC 5-year food delivery market share projections (DPIIT target), Tier-2 city food delivery penetration acceleration curves (based on 2020-2025 Tier-1 city adoption precedent), and corporate meal subscription market addressable base from organized sector employment growth data (MoLE India).

India Cloud Kitchen Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Independent Cloud Kitchen, Commissary/Shared Kitchen, Kitchen Pods |

| Product Types Covered | Burger and Sandwich, Pizza and Pasta, Chicken, Seafood, Mexican and Asian Food, Others |

| Natures Covered | Franchised, Standalone |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Rebel Foods, EatClub Brands Pvt. Ltd., Curefoods, Kouzina Food Tech Private Limited, Ghost Kitchens India, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India cloud kitchen market from 2020-2034.

- The India cloud kitchen market research report provides the latest information on the market drivers, challenges, and opportunities in the regional market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India cloud kitchen industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Cloud Kitchen Market Report

The India cloud kitchen market reached USD 1.24 Billion in 2025, driven by Swiggy-Zomato's annual food orders, Rebel Foods' multi-brand cloud kitchen model validation, COVID-19's permanent behavioral shift toward food delivery, urban millennial food ordering normalization, and ONDC's commission-disruption, creating improved cloud kitchen economics.

The market grows at 12.28% CAGR during 2026-2034, reaching USD 3.69 Billion by 2034, driven by Tier-2 city expansion, ONDC adoption reducing commission costs, kitchen pod innovation enabling new location types, corporate meal subscription growth, health cloud kitchen segment maturation, and India's smartphone food delivery user base.

Independent cloud kitchen leads at 60.8% through Rebel Foods' multi-brand model and independent single-brand operators.

Burger and sandwich leads at 35.8% through QSR cultural adoption and Rebel Foods' Faasos wrap brand. Chicken grows fastest at ~13.8% CAGR driven by Andhra-style chicken cloud brands, Mughlai chicken delivery brands, and India's rising protein consumption, creating the cloud kitchen industry's highest-growth product category through 2034.

South India leads at 35.0%, anchored by Bengaluru's high cloud kitchen locations, tech workforce ordering frequency of 4.8x/week (India's highest), the Rebel Foods innovation cluster, and Hyderabad-Chennai-Bengaluru's combined IT workforce generating India's most digitally native food ordering market.

Leading companies include Rebel Foods, EatClub Brands Pvt. Ltd., Curefoods, Kouzina Food Tech Private Limited, and Ghost Kitchens India, among others.

The market is projected to reach approximately USD 2.21 Billion by 2030, with ONDC capturing 15-20% of food delivery orders, improving cloud kitchen economics, kitchen pods becoming the dominant new kitchen format, Rebel Foods reaching 1,000+ kitchen milestones, EatFit-model health cloud kitchen sub-sector emerging, and commissary kitchen infrastructure operators achieving Series B/C funding, validating national-scale commissary models.

ONDC enables cloud kitchens to receive orders at 5-10% commission through Magicpin, Paytm Food, and PhonePe versus Swiggy-Zomato's 25-30% commission, saving INR 40,000-50,000 monthly for kitchens shifting 40% of orders to ONDC.

Three priority opportunities: Commissary kitchen infrastructure in 20-30 Tier-2 cities generating rental income from 8-15 cloud kitchen tenants per city at INR 30-80 Lakh investment; health-focused corporate meal subscription cloud kitchen in gym-adjacent IT city locations targeting fit-model 35-40% repeat order economics; and ONDC-first cloud kitchen brand building, achieving 15-20 percentage point margin advantage over aggregator-dependent competitors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)