India Commercial Telematics Market Size, Share, Trends and Forecast by Type, System Type, Provider Type, End Use Industry, and Region, 2026-2034

India Commercial Telematics Market Summary:

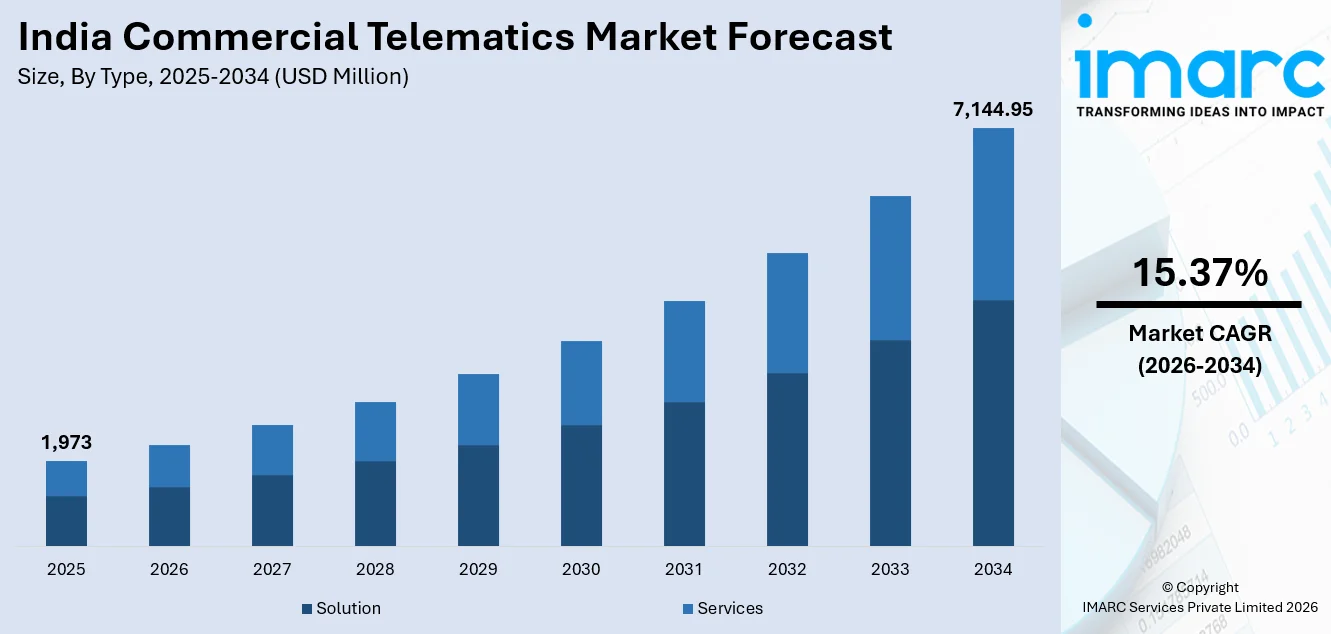

The India commercial telematics market size was valued at USD 1,973 Million in 2025 and is projected to reach USD 7,144.95 Million by 2034, growing at a compound annual growth rate of 15.37% from 2026-2034.

The market is experiencing robust growth as fleet operators and transportation companies increasingly adopt advanced connectivity solutions to enhance operational efficiency and road safety. Strengthening government mandates, rising demand for real-time vehicle tracking, and the integration of intelligent analytics into fleet management are accelerating adoption across industries. The growing emphasis on digital transformation in logistics and the proliferation of smartphone-based telematics platforms are further expanding the India commercial telematics market share.

Key Takeaways and Insights:

- By Type: Solution dominates the market with a share of 62% in 2025, driven by the surging demand for GPS-based fleet tracking, route optimization, and driver management platforms across commercial vehicle fleets in India.

- By System Type: Smartphone integrated leads the market with a share of 45% in 2025, reflecting the high penetration of mobile devices and cost-effective telematics accessibility for fleet operators of varying scales.

- By Provider Type: OEM holds the largest market share at 56% in 2025, as original equipment manufacturers increasingly embed telematics systems directly into commercial vehicles during production.

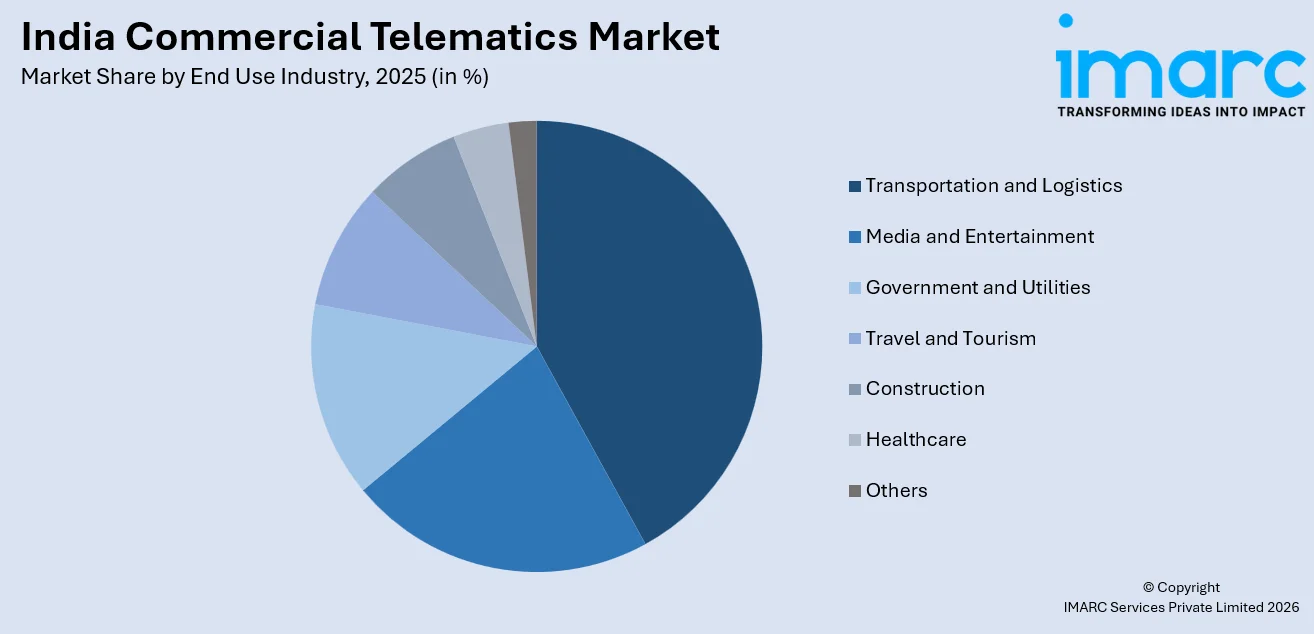

- By End Use Industry: Transportation and logistics accounts for the largest share with 41% in 2025, underscoring the critical role of telematics in enabling real-time shipment tracking, fleet optimization, and route planning.

- By Region: North India represents the largest segment with a 30% market share in 2025, supported by its extensive industrial corridors, high commercial vehicle density, and well-developed logistics infrastructure.

- Key Players: The market features a competitive landscape with domestic telematics start-ups, global technology providers, and leading commercial vehicle OEMs vying for market share through innovation, strategic partnerships, and expanded service offerings.

To get more information on this market Request Sample

The commercial telematics market in India is growing at a rapid pace with the increasing convergence of commercial vehicle regulations, digital revolution in logistics, and the development of connected vehicle technology. The government of India has been actively promoting the development of the commercial vehicle tracking sector through initiatives like the introduction of the AIS 140 standard, which requires all commercial vehicles as well as public transportation vehicles to be enabled with GPS tracking solutions and emergency buttons. Furthermore, the growth of the online shopping and quick commerce industry has led to an increased demand for real-time fleet tracking solutions as well as predictive maintenance tools. In addition, the increasing adoption of artificial intelligence and machine learning in the commercial telematics system enables fleet operators to make informed decisions based on the insights received. For instance, ZF announced the launch of its artificial intelligence-driven fleet orchestration system, SCALAR, in the Bharat Mobility Expo 2025 in New Delhi in January 2025, specifically targeting the commercial vehicle needs of the Indian market.

India Commercial Telematics Market Trends:

Integration of AI and Predictive Analytics in Fleet Platforms

Commercial telematics services available in India are changing rapidly, with many now extending beyond GPS tracking capabilities to include artificial intelligence and machine learning capabilities. Advanced telematics services available in India are empowering fleet operators to not only predict required maintenance for fleet vehicles but also to enhance fuel efficiency and minimize downtime associated with fleet operations. For example, the iPulse platform available from Force Motors includes AI-based analytics for data related to the operation of commercial vehicles, which improves the growth of India’s commercial vehicle telematics market.

Rising Adoption of Usage-Based Insurance Telematics

Telematics-enabled usage-based insurance models are gaining traction in India as insurers partner with technology providers to offer personalized premium structures based on actual driving behavior and mileage. This trend is creating new revenue streams for telematics solution providers while incentivizing safer driving practices among commercial fleet operators. Moreover, various companies are introducing Pay-As-You-Drive car insurance policy, allowing customers to choose kilometer-based coverage plans and pay premiums based on actual vehicle usage, reinforcing the link between telematics data and insurance innovation. IMARC Group predicts that the India insurance telematics market is projected to attain USD 1,022.1 Million by 2033.

Expansion of EV-Specific Telematics Ecosystems

As electric vehicle penetration rises across India’s commercial fleet segment, telematics solutions are being developed specifically for EVs, incorporating battery health monitoring, charging behavior analytics, range optimization, and energy management features. These capabilities are essential for managing fleet electrification and ensuring operational efficiency. In December 2025, Zypp Electric launched FleetEase.ai, an AI-driven fleet management platform built on experience managing over 20,000 electric vehicles, offering predictive maintenance, battery optimization, and driver analytics for logistics and mobility operators.

Market Outlook 2026-2034:

The India commercial telematics market is poised for substantial expansion as the adoption of connected fleet technologies accelerates across transportation, logistics, government, and healthcare sectors. The market generated a revenue of USD 1,973 Million in 2025 and is projected to reach a revenue of USD 7,144.95 Million by 2034, growing at a compound annual growth rate of 15.37% from 2026-2034. Advancements in AI-driven analytics, predictive maintenance, and EV-specific telematics platforms are further creating new avenues for market expansion. Increasing OEM integration of factory-fitted connected vehicle systems, the proliferation of usage-based insurance models, and the growing digital maturity of small and medium fleet operators are expected to broaden the addressable market significantly. Additionally, the ongoing deployment of 5G networks across India will enhance real-time data transmission capabilities, enabling more responsive and reliable telematics solutions for fleet operators managing complex, multi-modal logistics operations.

India Commercial Telematics Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Solution |

62% |

|

System Type |

Smartphone Integrated |

45% |

|

Provider Type |

OEM |

56% |

|

End Use Industry |

Transportation and Logistics |

41% |

|

Region |

North India |

30% |

Type Insights:

- Solution

- Fleet Tracking and Monitoring

- Driver Management

- Insurance Telematics

- Safety and Compliance

- V2X Solutions

- Others

- Services

- Professional Services

- Managed Services

Solution dominates with a market share of 62% of the total India commercial telematics market in 2025.

The solution segment’s commanding position reflects the growing demand among Indian fleet operators for comprehensive software platforms that deliver GPS-based fleet tracking, route optimization, driver behavior monitoring, and compliance management capabilities. As commercial vehicle fleets expand in scale and complexity, operators are prioritizing integrated telematics solutions that consolidate multiple functionalities into unified dashboards, enabling real-time decision-making and operational cost reduction across diverse transportation networks. The increasing sophistication of solution offerings, incorporating features such as geofencing, automated regulatory reporting, and fuel consumption analytics, has significantly enhanced their value proposition for enterprises managing large and geographically dispersed fleets. Cloud-based deployment models have further democratized access to enterprise-grade telematics solutions, allowing operators of all sizes to benefit from scalable, subscription-based platforms without heavy capital expenditure on dedicated infrastructure.

Furthermore, the rising adoption of cloud-hosted telematics platforms and mobile-accessible fleet management applications has made advanced solution offerings accessible to small and medium fleet operators across India. The growing emphasis on predictive maintenance, data-driven fleet optimization, and AI-powered decision support is reinforcing demand for sophisticated software solutions that go beyond basic vehicle tracking to deliver actionable business intelligence. The integration of video telematics, advanced driver assistance notifications, and automated compliance alerts within solution platforms is further expanding their functionality and market appeal.

System Type Insights:

- Embedded

- Tethered

- Smartphone Integrated

Smartphone integrated leads with a share of 45% of the total India commercial telematics market in 2025.

The smartphone integrated segment’s leadership is driven by India’s exceptionally high smartphone penetration and the cost-effectiveness of mobile-based telematics solutions, which eliminate the need for dedicated hardware installations. Fleet operators, particularly small and medium enterprises, prefer smartphone-based platforms that leverage built-in GPS, accelerometers, and cellular connectivity to deliver real-time tracking, route navigation, and driver behavior analytics without significant upfront investment in specialized devices. The accessibility and affordability of smartphone-integrated telematics have been particularly transformative for India’s vast unorganized fleet sector, enabling millions of small fleet owners and independent operators to adopt digital fleet management tools for the first time. These platforms also offer the advantage of rapid deployment and easy scalability, allowing businesses to onboard new vehicles without complex installation procedures or lengthy hardware procurement cycles.

The proliferation of affordable data plans and expanding 4G and 5G network coverage across India has further strengthened the viability of smartphone-integrated telematics systems. Mobile-based platforms also support seamless integration with cloud-hosted fleet management dashboards, enabling operators to access fleet data remotely from any location. The convergence of smartphone telematics with emerging technologies such as AI-powered driver scoring, real-time fuel monitoring, and automated trip logging is enhancing the sophistication and utility of these cost-effective solutions. Additionally, the growing availability of telematics applications that support regional languages and simplified user interfaces is driving adoption among India’s diverse driver workforce. India’s internet user base reached approximately 969 million by March 2025, creating a robust digital foundation for scalable smartphone-based telematics deployment across the commercial vehicle ecosystem and supporting the rapid growth of mobile-first fleet management solutions in both urban and semi-urban markets.

Provider Type Insights:

- OEM

- Aftermarket

OEM exhibits a clear dominance with a 56% share of the total India commercial telematics market in 2025.

The OEM segment’s dominance reflects the strategic shift by India’s leading commercial vehicle manufacturers toward embedding telematics systems directly into vehicles during production. This factory-integrated approach ensures seamless hardware-software compatibility, enhances data reliability, and enables manufacturers to offer connected vehicle services as part of their standard product portfolios, thereby creating stronger customer relationships and recurring revenue streams. The growing preference among large fleet operators for factory-fitted telematics systems is driven by the superior reliability, tamper-proof installation, and warranty-backed support that OEM solutions provide compared to aftermarket alternatives. As commercial vehicle buyers increasingly factor connectivity features into their purchasing decisions, OEMs are leveraging embedded telematics as a key competitive differentiator to attract and retain customers in an increasingly technology-driven market landscape.

Major Indian commercial vehicle OEMs have invested significantly in developing proprietary telematics ecosystems that provide end-to-end fleet intelligence capabilities. Tata Motors has developed its next-generation connected vehicle solution in-house, offering comprehensive fleet visibility and diagnostic services, while Ashok Leyland has connected over 150,000 vehicles on its telematics platform in collaboration with Trimble, which also serves as a leading high-end fleet management solution provider in the aftermarket segment. These factory-fitted telematics systems provide remote diagnostics, predictive maintenance alerts, and compliance monitoring capabilities that appeal to large fleet operators seeking reliable and integrated solutions.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Transportation and Logistics

- Media and Entertainment

- Government and Utilities

- Travel and Tourism

- Construction

- Healthcare

- Others

Transportation and logistics lead with a share of 41% of the total India commercial telematics market in 2025.

The transportation and logistics segment’s leadership is driven by the sector’s critical reliance on real-time fleet tracking, route optimization, fuel management, and delivery scheduling to maintain operational efficiency across India’s expansive supply chain networks. The rapid expansion of e-commerce and quick commerce has intensified the need for telematics-enabled visibility across last-mile and mid-mile delivery operations, making advanced fleet management solutions indispensable for logistics providers. Telematics platforms have become essential tools for managing the increasing complexity of multi-modal transportation networks, enabling operators to monitor shipment status, ensure on-time deliveries, and reduce fuel wastage through intelligent routing algorithms.

The growing adoption of cold chain logistics for pharmaceuticals and perishable goods is further driving demand for specialized telematics solutions that incorporate temperature monitoring, humidity tracking, and real-time cargo condition alerts alongside traditional fleet management functionalities. The ongoing development of dedicated freight corridors, multimodal logistics parks, and warehouse modernization initiatives is heightening operational complexity across the logistics sector, increasing reliance on intelligent telematics platforms for end-to-end supply chain visibility and cost control.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India exhibits a clear dominance with a 30% share of the total India commercial telematics market in 2025.

North India’s leadership in the commercial telematics market is supported by its strategic position as a major logistics and industrial hub, encompassing key commercial corridors connecting Delhi, Haryana, Punjab, Uttar Pradesh, and Rajasthan. The region’s high concentration of manufacturing units, distribution centers, and warehousing facilities generates substantial commercial vehicle traffic, driving demand for advanced fleet tracking, route optimization, and compliance monitoring solutions. The national capital region serves as a primary gateway for the movement of goods across northern and central India, concentrating a disproportionately large share of India’s organized fleet operators and logistics service providers. Additionally, North India’s extensive network of national highways, expressways, and industrial townships creates a strong operational foundation for telematics adoption, as fleet managers seek to optimize vehicle utilization, reduce transit times, and ensure regulatory compliance across high-traffic interstate routes.

The presence of India’s national capital region as a primary logistics gateway, combined with ongoing infrastructure development under programs such as the Delhi-Mumbai Industrial Corridor and the Eastern and Western Dedicated Freight Corridors, has further accelerated telematics adoption across the region. North India’s dense interstate transportation networks and large fleet operator bases create a favorable environment for widespread commercial telematics deployment across transportation, construction, and government sectors. The region also benefits from a relatively higher concentration of organized fleet operators and third-party logistics providers who are more receptive to digital fleet management technologies compared to operators in other regions. State-level initiatives to improve road safety, enforce vehicle fitness standards, and digitize transportation governance are further reinforcing the demand for telematics installations, positioning North India as the most mature and commercially active regional market for commercial telematics solutions in the country.

Market Dynamics:

Growth Drivers:

Why is the India Commercial Telematics Market Growing?

Strengthening Government Mandates and Regulatory Framework

India’s commercial telematics market is experiencing strong growth momentum driven by an expanding regulatory framework that mandates the adoption of intelligent transportation systems across commercial and public transport vehicles. The government’s commitment to improving road safety, reducing emissions, and enhancing transportation efficiency has translated into progressively stricter compliance requirements for fleet operators nationwide. The Automotive Industry Standard 140, originally introduced for public transport buses and school vehicles, has been significantly expanded under updated guidelines enforced in 2025 by the Ministry of Road Transport and Highways. All commercial vehicles including goods carriers, taxis, and tourist buses are now required to install AIS 140-compliant GPS tracking devices with emergency buttons and live data transmission capabilities. Pre-2025 registered vehicles face a compliance deadline of October 31, 2025, with non-compliant vehicles subject to penalties, fitness test failures, or suspension of route permits.

Rapid Expansion of E-Commerce and Logistics Infrastructure

The explosive growth of India’s e-commerce and quick commerce sectors is generating unprecedented demand for telematics-enabled fleet management solutions. As online retail platforms expand their delivery networks and tighten fulfillment timelines, logistics operators are increasingly relying on real-time tracking, route optimization, and predictive analytics to manage fleet operations efficiently. The rising complexity of multi-tier supply chains, combined with the need for greater delivery precision and cost control, is making commercial telematics solutions indispensable for transportation and logistics companies. Government infrastructure programs such as PM Gati Shakti and the National Logistics Policy are further strengthening multimodal connectivity and stimulating demand for advanced fleet intelligence platforms. On the 75th Independence Day, Prime Minister Narendra Modi unveiled the 'PM Gati Shakti' initiative while addressing the country from the Red Fort's ramparts. The project seeks to offer smooth and effective connectivity for the transport of individuals, products, and services across different transportation modes, thus improving last-mile connectivity and cutting down travel duration.

Growing OEM Integration and Connected Vehicle Adoption

India’s leading commercial vehicle manufacturers are increasingly embedding telematics systems directly into their vehicles, transforming connected fleet services from optional aftermarket additions into standard product features. This factory-integrated approach is accelerating telematics penetration by ensuring that new commercial vehicles enter service with built-in tracking, diagnostics, and connectivity capabilities. The shift toward OEM-embedded telematics is driven by manufacturers’ desire to enhance customer relationships, generate recurring service revenues, and differentiate their product offerings in a competitive market. Tata Motors has developed its next-generation connected vehicle solution in-house, while Kia India has exceeded 500,000 connected vehicles on Indian roads, with connected car models now accounting for almost 40% of the firm's domestic wholesale volumes. The Kia Seltos represents approximately 70% of the total connected car sales for the company, with the Sonet and Carens also making important contributions to this success.

Market Restraints:

What Challenges the India Commercial Telematics Market is Facing?

Data Privacy and Cybersecurity Concerns

The extensive collection and transmission of real-time vehicle, driver, and location data by telematics systems raise significant data privacy and cybersecurity concerns among fleet operators and drivers. The absence of comprehensive, standardized data protection frameworks specifically governing telematics data creates uncertainty around data ownership, storage, and usage, potentially slowing adoption among privacy-conscious organizations.

High Initial Costs and Infrastructure Fragmentation

The upfront investment required for telematics hardware, installation, and ongoing subscription services remains a barrier for small and medium fleet operators, who constitute a significant portion of India’s commercial vehicle ecosystem. Additionally, fragmented cellular network coverage in rural and remote regions limits the reliability of real-time data transmission, reducing the effectiveness of telematics solutions in underserved areas.

Inconsistent Regulatory Enforcement Across States

Despite the introduction of national mandates like AIS 140, enforcement of telematics compliance varies significantly across Indian states, creating an uneven regulatory landscape. Patchy implementation and differing state-level interpretations of compliance requirements hinder the creation of a unified telematics ecosystem, discouraging some fleet operators from investing in compliant systems until enforcement becomes more consistent.

Competitive Landscape:

The India commercial telematics market is characterized by a dynamic competitive landscape featuring a diverse mix of domestic start-ups, pan-Indian technology providers, global telematics solution companies, and leading commercial vehicle OEMs. Companies are competing through investments in AI-powered analytics platforms, cloud-based fleet management dashboards, and hardware-agnostic software solutions. Strategic partnerships between telematics providers and vehicle manufacturers are intensifying, enabling deeper integration of connected services into commercial fleet operations. Acquisitions and consolidation activities are reshaping the competitive dynamics as larger players seek to expand their customer bases and technology capabilities. As the market matures, differentiation through value-added services, predictive analytics, and comprehensive compliance management solutions is becoming increasingly critical for sustaining market share.

Recent Developments:

- In October 2025, Sensorise acquired LocoNav’s India fleet management business, integrating over 150,000 active device subscriptions and 10,000 customers including Hero, Mahindra, Kinetic Green, and Dalmia Cements into its ecosystem. Simultaneously, Sensorise unveiled the Eagle.ai AI-powered mobility intelligence platform at India Mobile Congress 2025 in New Delhi.

- In January 2025, ZF launched its next-generation digital fleet management platform SCALAR at the Bharat Mobility Expo 2025 in New Delhi. The platform leverages AI and predictive analytics to optimize routing, vehicle performance monitoring, and maintenance planning for both cargo and passenger commercial fleets operating in India.

India Commercial Telematics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| System Types Covered | Embedded, Tethered, Smartphone Integrated |

| Provider Types Covered | OEM, Aftermarket |

| End Use Industries Covered | Transportation and Logistics, Media and Entertainment, Government and Utilities, Travel and Tourism, Construction, Healthcare, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Commercial Telematics Market Report

The India commercial telematics market size was valued at USD 1,973 Million in 2025.

The market is expected to grow at a compound annual growth rate of 15.37% from 2026-2034 to reach USD 7,144.95 Million by 2034.

Solution, holding the largest revenue share of 62% in 2025, leads the India commercial telematics market, driven by growing demand for GPS-based fleet tracking, route optimization, driver management, and compliance monitoring platforms across commercial vehicle operations.

Key factors driving the India commercial telematics market include strengthening government mandates, rapid expansion of e-commerce and logistics infrastructure, growing OEM integration of connected vehicle systems, and rising adoption of AI-powered fleet analytics platforms.

Major challenges include data privacy and cybersecurity concerns, high initial hardware and subscription costs for small fleet operators, fragmented cellular network coverage in rural areas, and inconsistent regulatory enforcement of telematics mandates across states.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade