India Consumer Electronics Market Size, Share, Trends and Forecast by Product Type, Category, Distribution Channel, End-Use, and Region, 2026-2034

India Consumer Electronics Market Size, Share, Trends & Forecast (2026-2034)

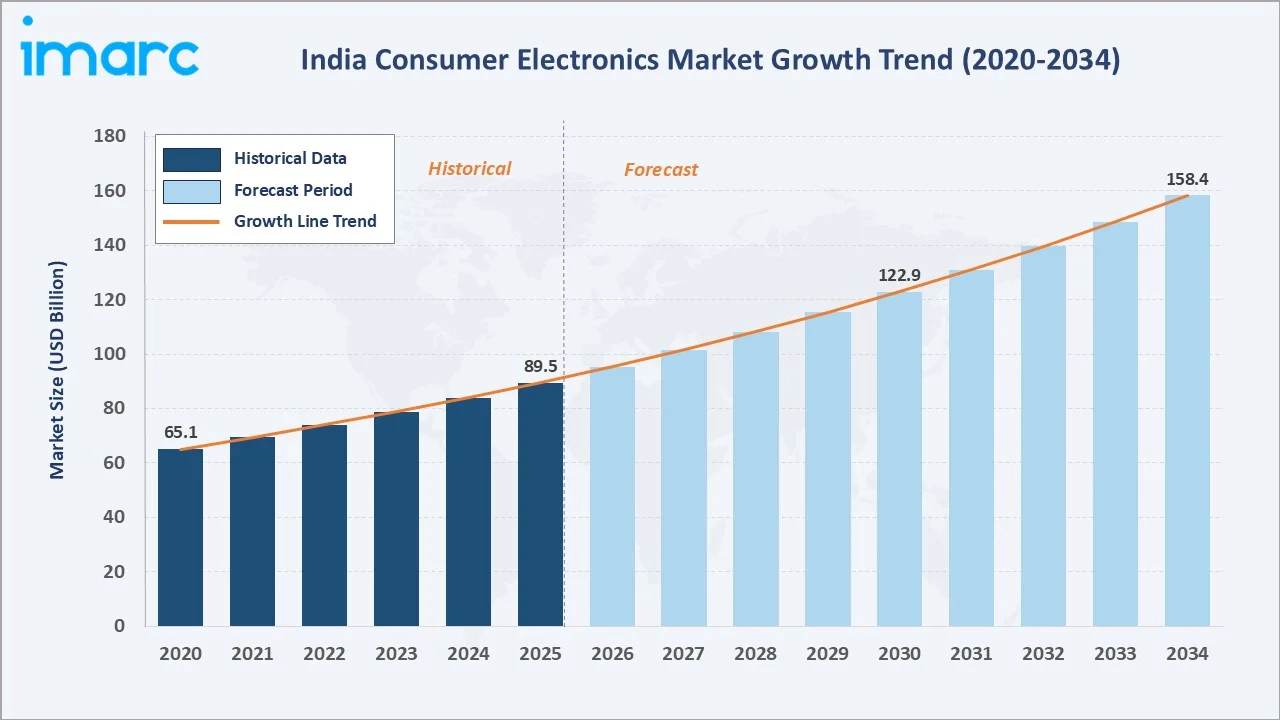

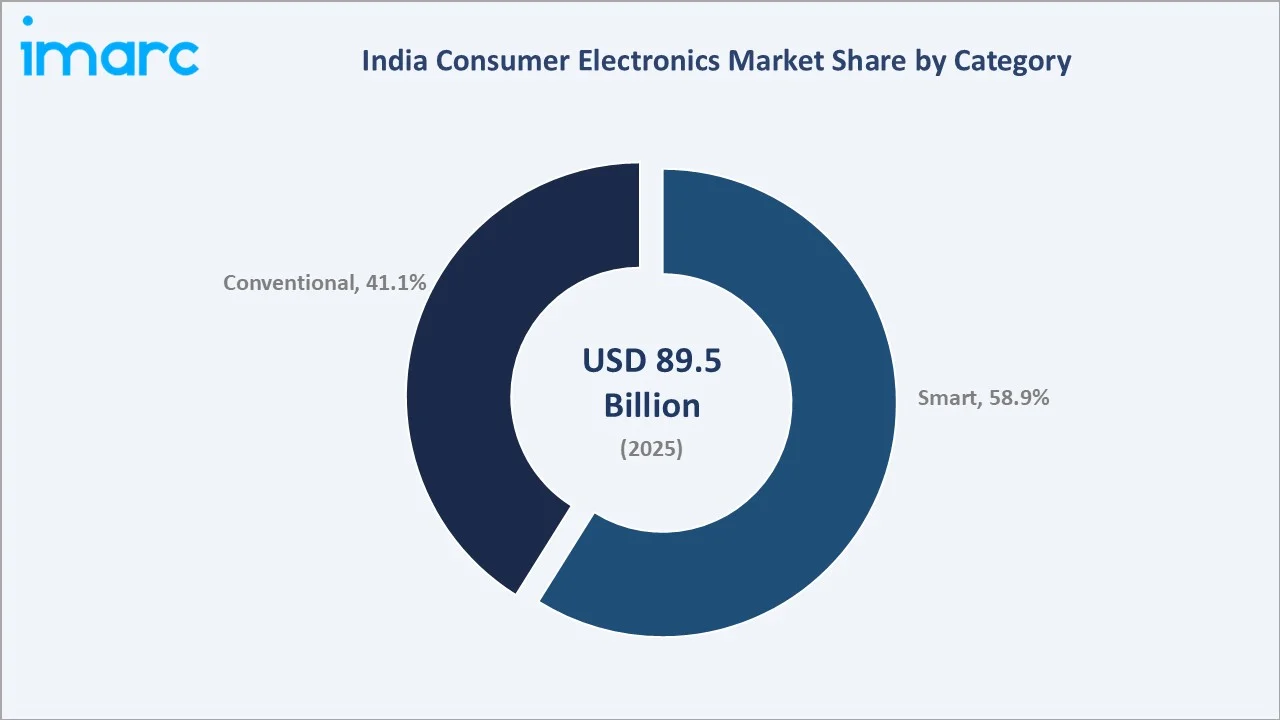

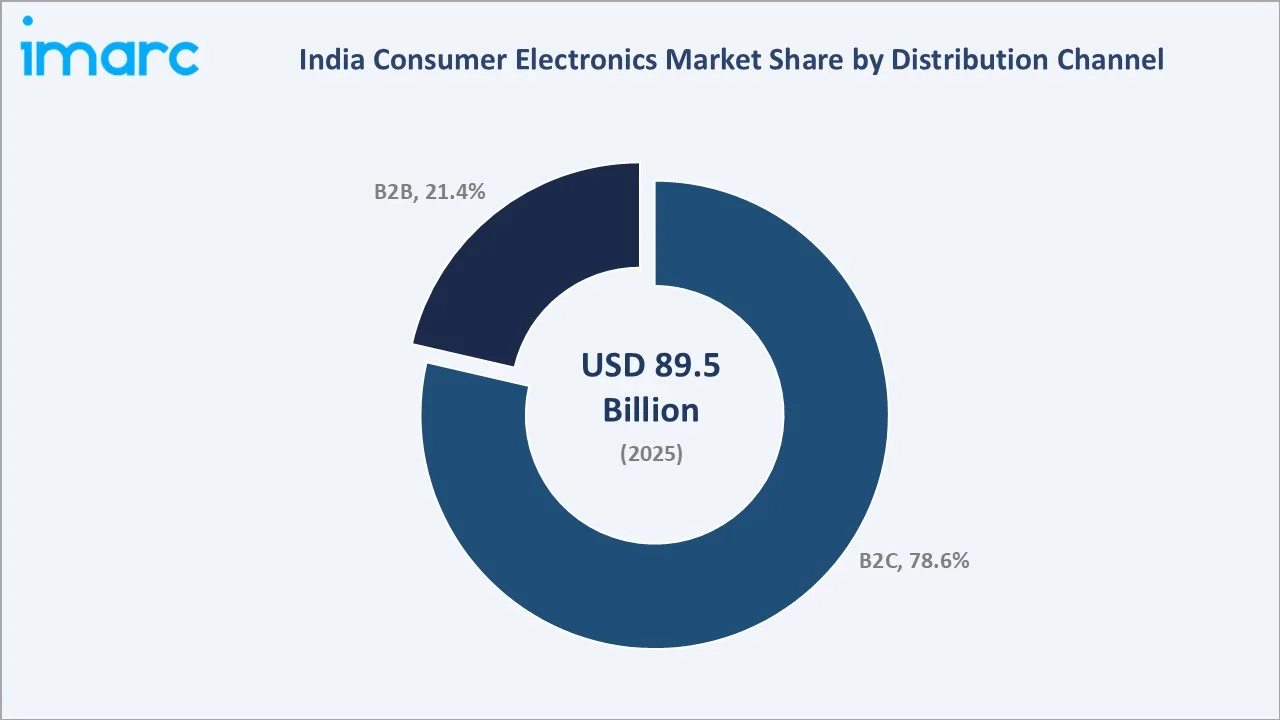

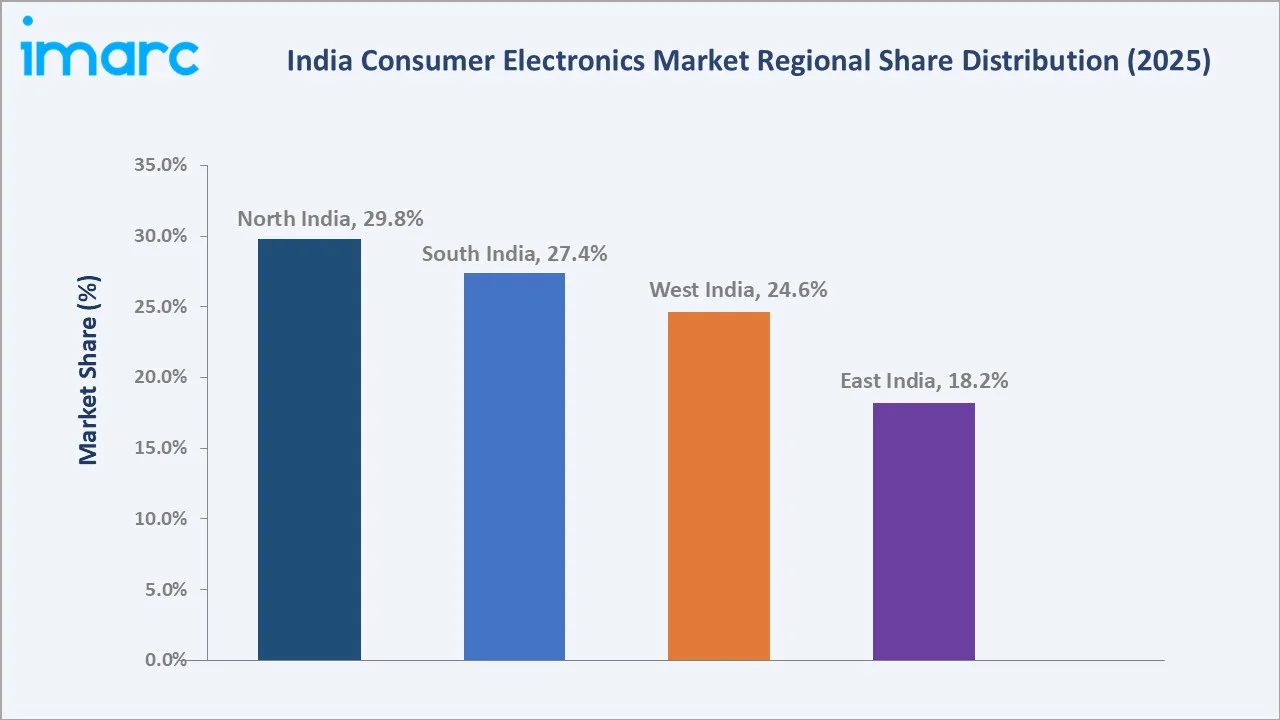

The India consumer electronics market size was valued at USD 89.48 Billion in 2025 and is projected to reach USD 158.44 Billion by2034, exhibiting a CAGR of 6.56% during the forecast period 2026-2034. Rising disposable incomes, accelerating digital infrastructure rollout, the Production-Linked Incentive (PLI) scheme, and rapid urbanization are powering India consumer electronics market growth. Smart devices commanded 58.9% category share in 2025, while B2C accounts for 78.6% of distribution. North India leads regionally with 29.8% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 89.48 Billion |

|

Forecast Market Size (2034) |

USD 158.44 Billion |

|

CAGR (2026-2034) |

6.56% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (29.8% share, 2025) |

|

Leading Category |

Smart (58.9%, 2025) |

|

Leading Distribution Channel |

B2C (78.6%, 2025) |

The India consumer electronics market growth trajectory from 2020 through 2034 contrasts historical recovery with a forecast curve powered by rising household incomes, smart-home adoption, and PLI-led domestic manufacturing scale-up.

To get more information on this market, Request Sample

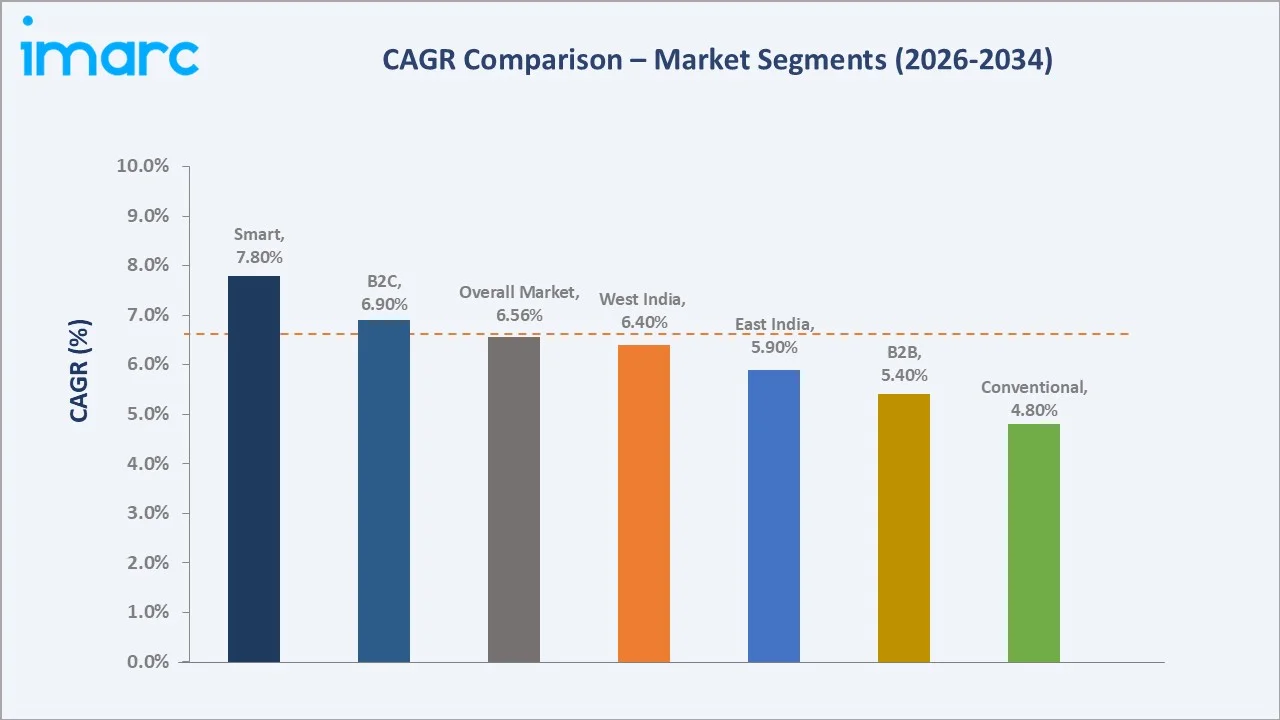

Segment-level CAGR comparisons highlight smart devices and B2C distribution channels as the fastest-growing sub-categories within the India consumer electronics market forecast through 2034.

Executive Summary

The India consumer electronics market is undergoing a structural shift. It is propelled by rising urbanization, expanding middle-class consumption, and accelerating digital adoption. Valued at USD 89.48 Billion in 2025, the market is projected to reach USD 158.44 Billion by 2034 at a CAGR of 6.56%.

Smart products dominate with a 58.9% share in 2025, fueled by smartphone replacement cycles, smart TVs, and connected wearables. The conventional category retains 41.1% on the back of entry-level appliances. B2C distribution leads with 78.6% share as e-commerce and modern retail consolidate consumer purchasing pathways.

North India commands the regional lead at 29.8% share in 2025, followed by South India at 27.4%, West India at 24.6%, and East India at 18.2%. The India consumer electronics market outlook remains positive as PLI incentives, 5G rollout, and AI-enabled feature integration converge across categories.

Key Market Insights

|

Insight |

Data |

|

Largest Category |

Smart - 58.9% share (2025) |

|

Second Category |

Conventional - 41.1% share (2025) |

|

Largest Distribution Channel |

B2C - 78.6% share (2025) |

|

Fastest Growing Channel |

B2C (e-commerce-led, ~6.9% CAGR) |

|

Leading Region |

North India - 29.8% share (2025) |

|

Top Companies |

Samsung India Electronics Private Limited, LG Electronics India Limited, Sony India Private Limited, Apple India Private Limited, Xiaomi Technology India Private Limited, Whirlpool of India Limited. |

|

Smart Device Demand (2025) |

USD 52.7 Billion |

Key Analytical Observations Supporting The Data Above:

- Smart category dominance (58.9%) in 2025 reflects deep smartphone penetration, with India crossing 750 million smartphone users in 2024 and smart TV shipments reaching 16 million units the same year.

- Conventional category share of 41.1% is sustained by Tier-3 and rural demand for entry-level air conditioners, refrigerators, and washing machines as electrification deepens across 600,000 plus Indian villages.

- B2C channel leadership at 78.6% is anchored by e-commerce platforms such as Amazon, Flipkart, and Reliance Digital, which collectively crossed USD 35 Billion in electronics GMV in 2024.

- B2B share of 21.4% is driven by enterprise IT refresh cycles, hospitality renovations, and government procurement, with central PSU electronics spending crossing USD 30 Billion in 2025.

- North India leadership at 29.8% is powered by Delhi-NCR purchasing power, Punjab-Haryana rural consumption, and Uttar Pradesh state programs, where smartphone density rose 14% year-over-year in 2024.

- PLI-backed manufacturing momentum has lifted electronics exports to USD 29.1 Billion in FY2024, a 23.6% jump versus FY2023, per the Ministry of Electronics and IT (MeitY).

India Consumer Electronics Market Overview

Consumer electronics in India span smartphones, televisions, audio equipment, personal computing, wearables, and major and small home appliances. The market includes both smart, connected products and conventional, single-function devices serving households and enterprises.

The industry sits at the intersection of digital adoption, manufacturing policy, and rising household consumption. Growth is shaped by macroeconomic factors such as 7.4% projected GDP expansion in 2025, an expanding 432 million-strong middle class, deeper internet penetration past 900 million users in 2024, and the PLI scheme that has unlocked over USD 17 Billion in committed electronics investment.

Market Dynamics

To evaluate market opportunities, Request Sample

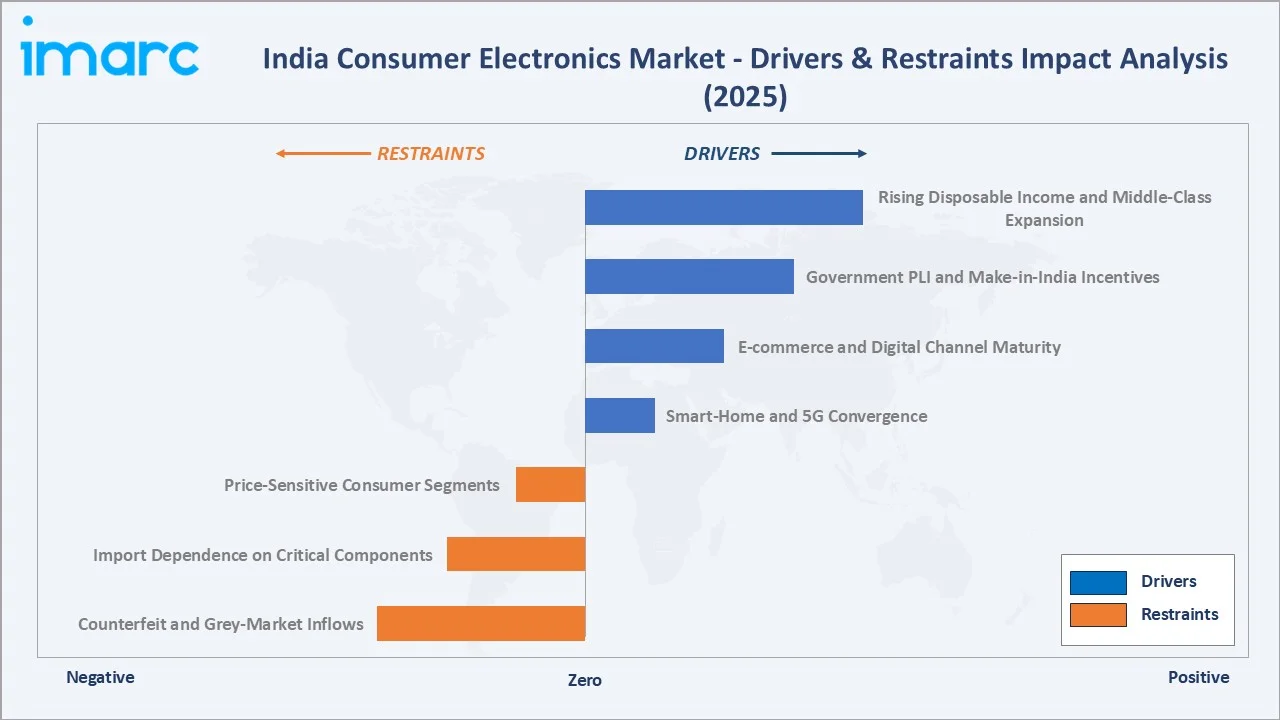

Market Drivers

- Rising Disposable Income and Middle-Class Expansion: India’s per capita income crossed USD 2,730 in FY2024, lifting affordability for premium electronics. The middle class is projected to reach 540 million by 2030, expanding addressable demand for smart TVs, premium smartphones, and connected appliances.

- Government PLI and Make-in-India Incentives: The PLI scheme for IT hardware, mobile phones, and white goods has attracted USD 17 Billion in committed investment by 2024. Domestic mobile phone production crossed USD 49 Billion in FY2024, reducing import dependence and supporting price competitiveness.

- E-commerce and Digital Channel Maturity: India’s e-commerce market crossed USD 300 Billion in 2025. Festive sales events, no-cost EMI penetration above 28%, and same-day delivery in 100 plus cities are accelerating online consumer electronics purchases beyond Tier-1 metros.

- Smart-Home and 5G Convergence: India’s 5G subscriber base crossed 350 million by mid-2025, the world’s second largest. This is unlocking demand for IoT-enabled appliances, AI-powered TVs, and connected wearables, particularly across urban households.

Market Restraints

- Price-Sensitive Consumer Segments: Mass-market shoppers, especially in Tier-3 and rural India, anchor purchasing decisions on entry-level price points, limiting premium product penetration outside metros.

- Import Dependence on Critical Components: India still imports over 60% of semiconductors, display panels, and lithium-ion cells, exposing manufacturers to forex volatility and supply-chain disruption from China and East Asia.

- Counterfeit and Grey-Market Inflows: Counterfeit accessories and unbranded appliances erode roughly 8% to 10% of brand revenue in segments such as audio, mobile chargers, and small kitchen appliances.

Market Opportunities

- Tier-2 and Tier-3 Premium Penetration: Cities such as Lucknow, Coimbatore, Indore, and Bhubaneswar are showing 18% to 22% annual growth in premium electronics sales, supported by aspirational consumption and improving last-mile logistics.

- Local AI and IoT Product Innovation: India-specific design innovations such as voice assistants in regional languages, ultra-low-power IoT devices, and inverter-driven appliances are unlocking incremental volume in price-sensitive segments.

- Export-Oriented Manufacturing Hubs: India’s consumer electronics exports crossed USD 29.1 Billion in FY2024. PLI-backed plants in Tamil Nadu, Karnataka, and Uttar Pradesh are scaling toward serving the U.S., Middle East, and Africa markets.

Market Challenges

- Skill Gap in Advanced Electronics Manufacturing: India faces a shortfall of nearly 300,000 skilled engineers in semiconductor design, PCB assembly, and ATMP, slowing the move toward higher-value local production.

- Regulatory Compliance Complexity: BIS certification, e-waste management rules, and energy-efficiency star ratings impose multi-layered compliance costs that disproportionately affect smaller domestic brands.

- After-Sales Service Coverage in Tier-3 and Rural Markets: Limited authorized service centres outside metros lead to longer repair cycles, repeated warranty claims, and brand dissatisfaction among small-town buyers.

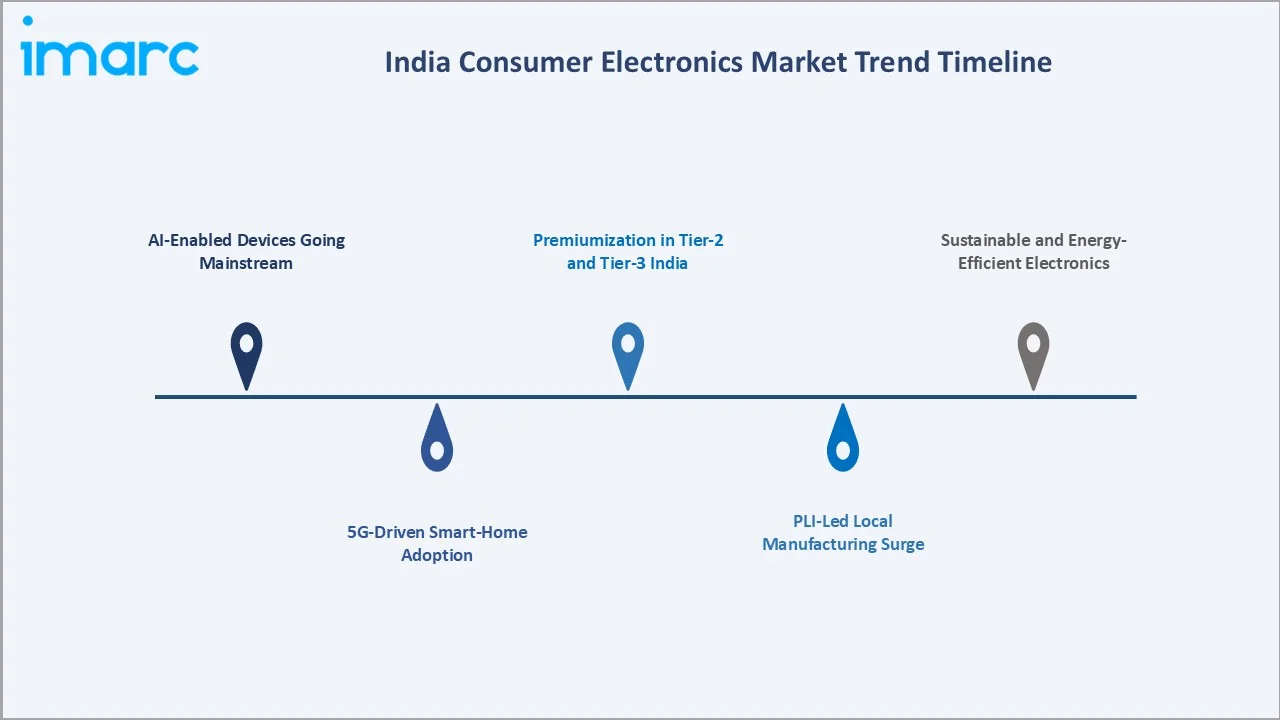

Emerging Market Trends

1. AI-Enabled Devices Going Mainstream

AI features such as on-device translation, generative photography, and ambient computing are now appearing in smartphones priced below USD 250 in India. Smart TV brands are integrating AI for upscaling, content discovery, and energy optimization, drivilng 19% year-over-year volume growth in 2024.

2. 5G-Driven Smart-Home Adoption

With 5G covering all 28 states by 2025, smart speakers, AI security cameras, and connected appliances are gaining adoption in urban India. Smart-home device shipments crossed 30 million units in 2024, up 24% over 2023.

3. PLI-Led Local Manufacturing Surge

Domestic value addition in mobile phone manufacturing rose from 18% in 2020 to 23% in 2024 and is targeted to cross 35% by 2027. Apple now manufactures 14% of its global iPhone output in India, signalling a structural supply-chain shift.

4. Premiumization in Tier-2 and Tier-3 India

Premium smartphones priced above USD 600 grew 31% year-over-year in 2024, with non-metro cities contributing incremental volume. Consumers are upgrading from entry-level products to feature-rich, design-led variants.

5. Sustainable and Energy-Efficient Electronics

5-star Bureau of Energy Efficiency rated air conditioners and refrigerators now account for most of new appliance sales. India’s e-waste recycling capacity expanded to 1.6 million tonnes in 2024, supporting circular-economy positioning by major brands.

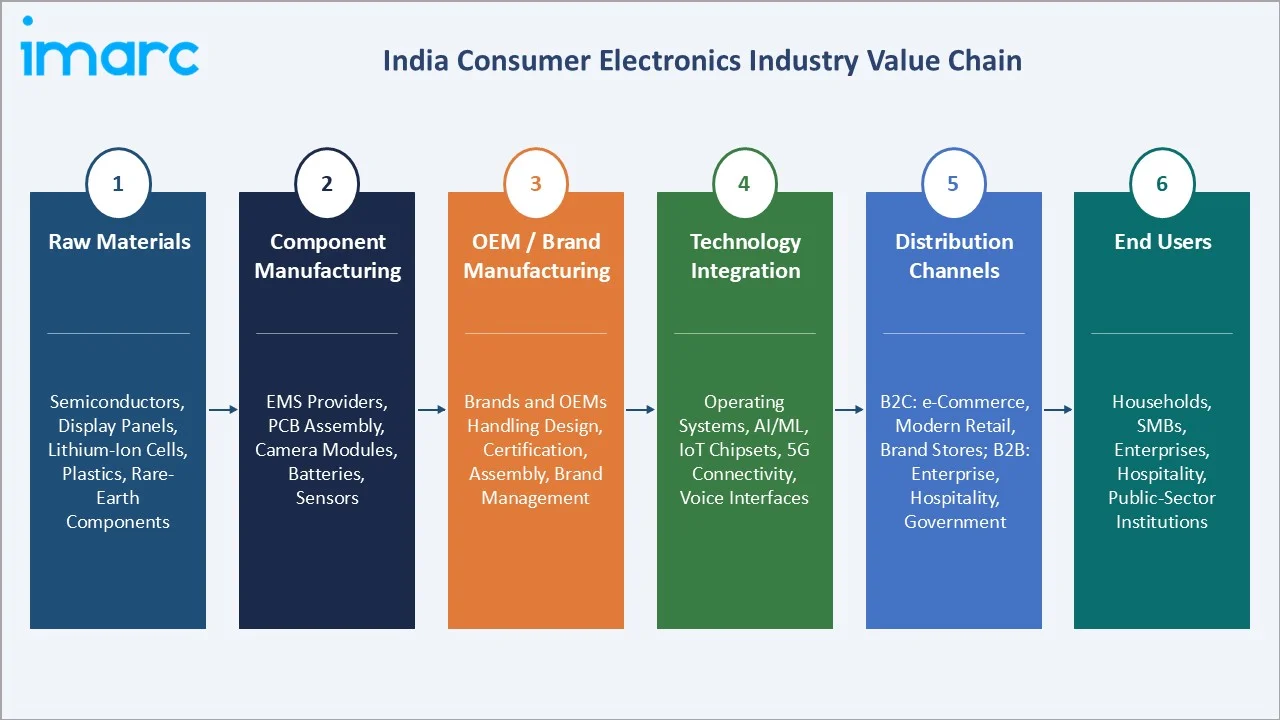

Industry Value Chain Analysis

The India consumer electronics value chain spans six integrated stages from raw-material sourcing through end-consumer purchase. Each stage has distinct margin profiles, technology investment intensity, and competitive dynamics relevant to the India consumer electronics market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Suppliers of semiconductors, display panels, lithium-ion cells, plastics, and rare-earth components, with a significant share sourced through imports |

|

Component Manufacturing |

Electronics manufacturing services (EMS) providers and Tier-2 clusters producing PCB assemblies, camera modules, batteries, and sensors |

|

OEM / Brand Manufacturing |

Consumer electronics brands and OEMs responsible for product design, certification, assembly, and brand management |

|

Technology Integration |

Providers of operating systems, AI/ML capabilities, IoT chipsets, 5G connectivity, and voice-enabled interfaces tailored to local markets |

|

Distribution Channels |

Business-to-consumer channels including e-commerce, modern retail, brand stores, and multi-brand outlets; and business-to-business channels serving enterprise, hospitality, and government clients |

|

End Users |

Households, small and medium businesses, enterprises, hospitality operators, and public-sector institutions across regions |

OEMs hold the strongest strategic position by combining design, certification, and brand. E-commerce and modern retail are reshaping distribution, allowing brands to bypass intermediaries and capture richer margins, while local component manufacturers gain leverage from PLI-led volume.

Technology Landscape in the Consumer Electronics Industry

Battery and Power Technology

Lithium-ion remains the dominant battery chemistry across smartphones, laptops, and wearables. India’s ACC PLI scheme is aimed at building significant domestic cell manufacturing capacity to reduce import dependence. Fast-charging technologies above ultra-high wattage levels are increasingly penetrating mid-tier smartphones, although adoption is still uneven across brands.

Materials and Display Innovation

OLED and QLED displays are gaining share in televisions and premium smartphones, driven by colour fidelity and energy savings. Brands such as Samsung and LG account for over 78% of OLED supply globally. India is positioning to host display fab capacity through state-level incentives in Telangana and Gujarat.

Smart Connectivity and IoT Integration

Wi-Fi 6, Bluetooth LE, and Matter protocols are becoming default across smart-home devices. Integration with Amazon Alexa, Google Home, and Apple HomeKit, combined with regional language voice assistants, is expanding accessibility. India’s smart-home ecosystem is still at an early adoption stage, with a relatively small but rapidly growing user base driven by increasing IoT penetration and rising disposable incomes.

Automation and AI-Driven Features

AI-driven personalization is moving from premium tiers into mid-segment electronics. On-device AI processors in smartphones below USD 300, AI-based picture enhancement in TVs, and inverter-driven AI control in air conditioners are reshaping product roadmaps for 2026 to 2028.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the India consumer electronics market, along with forecasts at the regional and country levels from 2026 to 2034. The market has been categorized based on category and distribution channel.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | 🔒 | 🔒 | 2025 |

| Category | Smart | 58.9% | 2025 |

| Distribution Channel | B2C | 78.6% | 2025 |

| End-Use | 🔒 | 🔒 | 2025 |

| Region | North India | 29.8% | 2025 |

By Category

Smart products lead the India consumer electronics market category with a 58.9% share in 2025. Demand is anchored by smartphone replacement cycles, expanding smart TV adoption, and the rise of AI-enabled appliances. The smart category is projected to grow at a 7.8% CAGR through 2030, outpacing the overall market.

To access detailed market analysis, Request Sample

Smart speakers, AI cameras, smartwatches, and 5G-enabled devices are the fastest-growing sub-categories. Premium smartphone shipments above USD 600 crossed 12 million units in 2024, supported by EMI-led affordability and aspirational positioning.

Conventional electronics retain 41.1% category share, sustained by Tier-3 and rural demand for entry-level refrigerators, single-door air conditioners, basic televisions, and feature phones. Conventional appliances posted 4.8% CAGR through 2030, supported by rural electrification and government appliance distribution programs.

By Distribution Channel

B2C is the dominant distribution channel at 78.6% of revenue in 2025. India’s e-commerce electronics GMV crossed USD 30 Billion in 2024, growing at 22% year-over-year. Modern retail chains such as Reliance Digital, Croma, and Vijay Sales contribute approximately 18% of B2C value.

Festive online sales events such as Amazon Great Indian Festival and Flipkart Big Billion Days deliver 28% to 32% of annual brand revenue in less than a month. No-cost EMI options now cover over 65% of online consumer electronics transactions.

B2B users represent 21.4% of distribution and remain a steady volume driver, supported by enterprise IT refresh cycles, hospitality renovations across 280 plus new hotels in 2024-2025, and central and state government procurement crossing USD 5.4 Billion in 2024. Healthcare and education institutions are increasingly specifying enterprise-grade displays, laptops, and conferencing systems.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

29.8% |

Delhi-NCR purchasing power, UP electronics manufacturing zones, Punjab-Haryana rural consumption |

|

South India |

27.4% |

Bengaluru tech hub, Chennai-Sriperumbudur ESDM cluster, Hyderabad smart-city investments |

|

West India |

24.6% |

Mumbai-Pune affluence, Gujarat semiconductor policy, Maharashtra appliance demand |

|

East India |

18.2% |

Kolkata urban demand, Odisha rural electrification, Bihar-Jharkhand smartphone growth |

North India commands 29.8% revenue share in 2025. The Delhi-NCR region accounts for a significant share of national consumer electronics demand, driven by relatively high household disposable incomes. Uttar Pradesh hosts the country’s largest mobile-phone manufacturing cluster in Noida, anchored by Samsung Electronics’ flagship plant. Punjab and Haryana contribute steady rural demand for refrigerators, washing machines, and televisions, with rural smartphone penetration crossing 64% in 2024.

South India holds 27.4% of national revenue, anchored by Bengaluru’s technology consumer base and the Chennai-Sriperumbudur ESDM cluster, which produces over 35% of India’s smartphone exports. Tamil Nadu hosts manufacturing operations for Foxconn, Pegatron, and Wistron. Hyderabad’s smart-city investments and Kerala’s high digital literacy reinforce premium electronics adoption.

West India accounts for 24.6%, led by Maharashtra and Gujarat. Mumbai-Pune metropolitan demand fuels premium electronics consumption, while Gujarat’s semiconductor and display fab policies, including the Tata-PSMC fab announcement of 2024, signal long-term industrial expansion. East India represents 18.2%, driven by Kolkata urban demand, Odisha’s rural electrification programs, and rapid smartphone-led adoption across Bihar and Jharkhand, where mobile internet users grew 16% year-over-year in 2024.

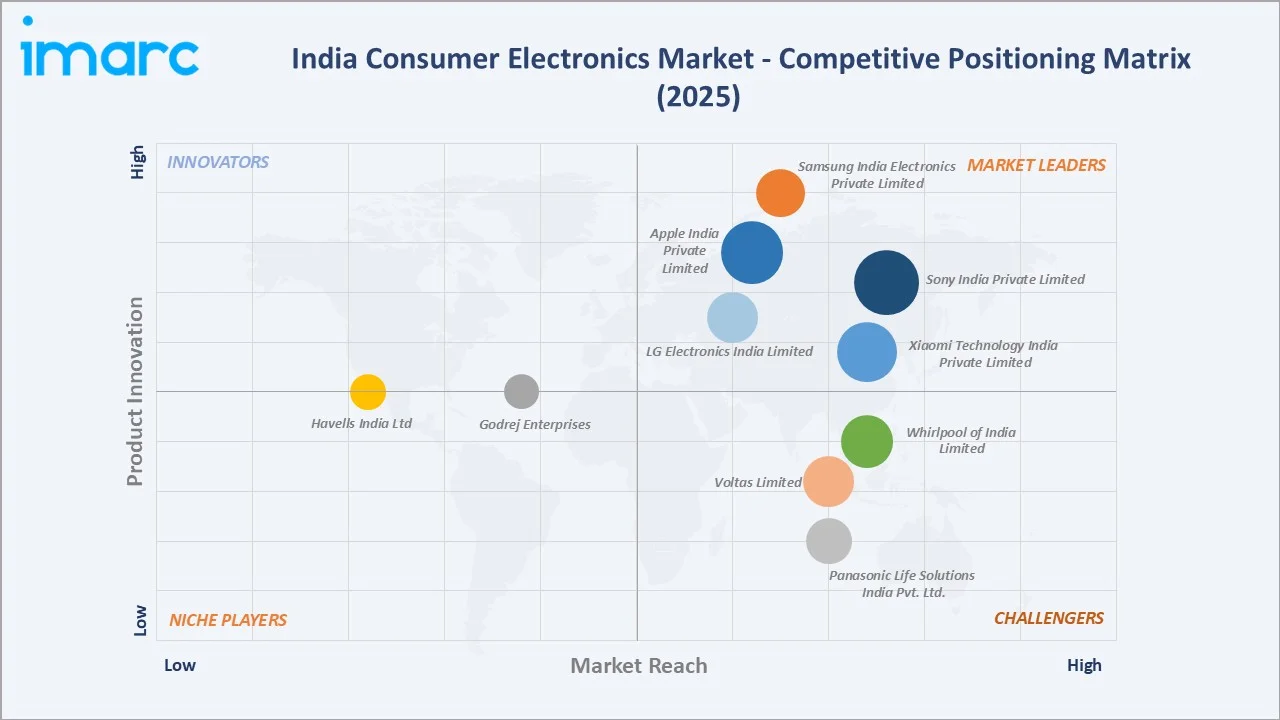

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Samsung India Electronics Private Limited |

Samsung |

Leader |

Smartphone leadership, smart TVs, premium appliances |

|

LG Electronics India Limited |

LG |

Leader |

OLED TVs, refrigerators, washing machines |

|

Sony India Private Limited |

Sony |

Leader |

Premium TVs, audio, gaming consoles |

|

Apple India Private Limited |

Apple |

Leader |

Premium ecosystem, retail expansion |

|

Xiaomi Technology India Private Limited |

Xiaomi, Redmi |

Leader |

Value smartphones, smart-home portfolio |

|

Whirlpool of India Limited |

Whirlpool |

Challenger |

Refrigerators, washing machines, microwave ovens |

|

Panasonic Life Solutions India Pvt. Ltd. |

Panasonic |

Challenger |

Air conditioners, TVs, kitchen appliances |

|

Voltas Limited |

Voltas, Voltas Beko |

Challenger |

Air conditioners, refrigerators - Tata-Arcelik JV |

|

Havells India Ltd |

Havells, Lloyd |

Emerging |

Air conditioners, small appliances, fans |

|

Godrej Enterprises |

Godrej |

Emerging |

Refrigerators, ACs, washing machines - rural strength |

The India consumer electronics market is moderately fragmented, with global majors competing alongside Indian conglomerates and Chinese-origin brands. Leading players compete on product innovation, channel reach, after-sales service, and PLI-backed manufacturing scale. Strategic moves are frequent - Tata Group acquired a controlling stake in Wistron India in 2023 to manufacture iPhones, and Reliance scaled the JioBharat phone in 2024.

Key Company Profiles

Samsung India Electronics Pvt. Ltd.

Samsung India, headquartered in Gurugram, is the country’s largest consumer electronics brand by revenue. It operates the world’s largest mobile-phone manufacturing facility in Noida, with annual capacity exceeding 120 million units.

- Product & Platform Portfolio: Galaxy smartphones, QLED and Neo QLED TVs, side-by-side and convertible refrigerators, AI-enabled washing machines, premium air conditioners, and Galaxy Watch / Buds wearables.

- Recent Developments: In 2025, Samsung India is advancing its smart home strategy through the launch of Bespoke AI appliances, integrating AI-driven automation, centralized device control, and SmartThings connectivity to deliver a unified, intelligent home ecosystem.

- Strategic Focus: Samsung’s strategy centres on premiumization, AI-driven device experiences, and deeper Tier-2 and Tier-3 distribution. The brand is also scaling display and semiconductor R&D investments under India’s electronics manufacturing policy.

LG Electronics India Pvt. Ltd.

LG Electronics India, headquartered in Greater Noida, is among the top three consumer electronics players in the country. It operates manufacturing facilities at Greater Noida and Pune and serves over 700 cities through 35,000 plus retail touchpoints.

- Product & Platform Portfolio: OLED and QNED TVs, inverter-driven refrigerators, front-load washing machines, dual-inverter air conditioners, microwave ovens, and the LG ThinQ smart-home platform.

- Recent Developments: In December 2024, LG India filed a draft red herring prospectus for an Indian IPO targeting USD 1.7 Billion. The company also expanded its OLED TV portfolio with G4 and C4 series for the Indian premium segment.

- Strategic Focus: LG’s strategy centres on premium home appliances, AI-enabled ThinQ ecosystem expansion, energy-efficient inverter technology, and IPO-funded capacity additions for refrigerators and washing machines.

Sony India Pvt. Ltd.

Sony India, headquartered in New Delhi, is a leading premium consumer electronics brand operating across television, audio, camera, and gaming categories. The company sells through 350 plus brand stores and a deep e-commerce footprint.

- Product & Platform Portfolio: BRAVIA OLED, Mini-LED and 4K LED TVs, Alpha mirrorless cameras, WH-1000X audio series, PlayStation 5 gaming consoles, and home-theatre soundbars.

- Recent Developments: In August 2024, Sony India expanded its premium television portfolio with the launch of the BRAVIA 9 series featuring Mini-LED display technology and AI-powered XR processing, aimed at enhancing cinematic viewing and gaming experiences.

- Strategic Focus: Sony’s strategy concentrates on premium TVs, content-led ecosystem differentiation through PlayStation and Sony Music, and direct-to-consumer expansion via Sony Center experience stores.

Market Concentration Analysis

The India consumer electronics market is moderately concentrated. The top five players - Samsung, LG, Sony, Apple, and Xiaomi - collectively account for approximately 42% to 48% of national market revenue in 2025. The remaining share is distributed across Whirlpool, Voltas, Havells, Godrej, Panasonic, and a wide base of regional and Chinese-origin brands.

The market is following a bifurcated dynamic. At the premium tier, consolidation is occurring around brand equity, AI ecosystem capability, and after-sales service depth. Simultaneously, value-segment competition is intensifying as Indian conglomerates such as Tata, Reliance, and Adani scale electronics manufacturing under PLI, creating new domestic challengers in mobile phones, TVs, and appliances through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Smart category devices are the highest-growth opportunity at approximately 7.8% CAGR through 2030. B2C distribution remains the fastest-growing channel at 6.9% CAGR, supported by e-commerce expansion. AI-enabled smartphones, smart TVs above 55 inches, and inverter-driven appliances represent the premium technology growth opportunity.

Emerging State and Regional Expansion

North India retains volume leadership, but the highest incremental growth is forecast in West India’s Gujarat-Maharashtra industrial belt and South India’s Tamil Nadu-Karnataka technology corridor. Tier-2 cities such as Indore, Lucknow, Coimbatore, and Bhubaneswar are forecast to grow at 18% to 22% annually.

PLI, Manufacturing, and Strategic Investments

PLI scheme commitments crossed USD 17 Billion by 2024 across mobile phones, IT hardware, and white goods. Strategic acquisitions are reshaping the landscape - Tata acquired Wistron’s India iPhone operations in 2023, while Reliance scaled JioBharat phone capacity. AI chip design, display fabs, and battery cell manufacturing are the primary venture and corporate capital focus areas through 2034.

Future Market Outlook (2026-2034)

The India consumer electronics market forecast projects steady value expansion from USD 89.48 Billion in 2025 to USD 158.44 Billion by 2034 at a CAGR of 6.56%. Smart products will retain dominance and accelerate structurally, while conventional electronics will sustain volume in rural and entry-tier segments.

Three key shifts will reshape the market through 2034. AI-enabled feature integration will become standard across smartphones, TVs, and appliances by 2028 to 2030. PLI-backed local manufacturing will drive domestic value addition past 35% across mobile phones and IT hardware. Tier-2 and Tier-3 premium adoption will narrow the urban-rural consumption gap, intensifying brand competition across all price tiers and regions.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024 to 2025 with industry stakeholders such as product directors at OEM manufacturers, category buyers at modern retail chains, e-commerce category managers, and senior officials at the Ministry of Electronics and IT. These insights validated market sizing, segmentation estimates, and category adoption timelines.

Secondary Research

Secondary sources include MeitY publications, NASSCOM reports, IBEF industry briefs, Reserve Bank of India consumption data, India Cellular and Electronics Association (ICEA) reports, company annual filings, and trade publications such as Economic Times Tech, Mint, and TechRadar India. Regional consumption data was triangulated using NielsenIQ retail audits.

Forecasting Models

Market sizing and growth projections were derived using a combined top-down and bottom-up approach, incorporating GDP growth rates, urbanization indices, household consumption expenditure, and historical category evolution. Scenario analysis (base, optimistic, conservative) was conducted to account for macroeconomic, currency, and policy uncertainty.

India Consumer Electronics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Categories Covered | Smart, Conventional |

| Distribution Channels Covered |

|

| End-Uses Covered |

|

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Samsung India Electronics Private Limited, LG Electronics India Limited, Sony India Private Limited, Apple India Private Limited, Xiaomi Technology India Private Limited, Whirlpool of India Limited, Panasonic Life Solutions India Pvt. Ltd., Voltas Limited, Havells India Ltd, Godrej Enterprises, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India consumer electronics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India consumer electronics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India consumer electronics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Consumer Electronics Market Report

The India consumer electronics market was valued at USD 89.48 Billion in 2025, driven by rising disposable incomes, smartphone adoption, e-commerce growth, and PLI-backed manufacturing scale.

The market is projected to reach USD 158.44 Billion by 2034, growing at a CAGR of 6.56% during 2026-2034, supported by AI-enabled devices, 5G adoption, and rising premium consumption.

The smart category leads with 58.9% share in 2025, driven by smartphones, smart TVs, AI-enabled appliances, wearables, and rapid 5G adoption across urban and Tier-2 households.

B2C is the dominant channel at 78.6% share in 2025, anchored by e-commerce platforms, modern retail chains, and deepening offline-online integration across 700 plus Indian cities.

North India dominates with 29.8% share in 2025. Delhi-NCR purchasing power, UP electronics manufacturing zones, and Punjab-Haryana rural consumption underpin its regional leadership.

Key drivers include rising disposable incomes, PLI manufacturing incentives, e-commerce maturity, 5G rollout, smart-home adoption, and rapid Tier-2 and Tier-3 premium product penetration.

Major players include Samsung India Electronics Private Limited, LG Electronics India Limited, Sony India Private Limited, Apple India Private Limited, Xiaomi Technology India Private Limited, Whirlpool of India Limited, Panasonic Life Solutions India Pvt. Ltd., Voltas Limited, Havells India Ltd, Godrej Enterprises

Fastest-growing trends include AI-enabled smartphones and TVs, 5G smart-home device adoption, premiumization in Tier-2 cities, energy-efficient appliances, and PLI-led local manufacturing scale.

Major challenges include import dependence on semiconductors and displays, counterfeit grey-market inflows, skill gaps in advanced manufacturing, and limited after-sales coverage in rural areas.

Key opportunities include AI-enabled device platforms, semiconductor and display manufacturing, Tier-2 and Tier-3 retail expansion, e-commerce direct-to-consumer growth, and export-oriented PLI-backed manufacturing.

PLI commitments crossed USD 17 Billion by 2024. The scheme has lifted mobile phone production to USD 49 Billion in FY2024, reducing imports and boosting exports of consumer electronics.

India had over 320 million connected smart-home devices in use by mid-2025, with shipments of 36 million units in 2024, growing 24% year-over-year, driven by 5G and IoT integration.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)