India Data Center Cooling Market Size, Share, Trends and Forecast by Component, Type of Cooling, Cooling Technology, Type of Data Center, Vertical, and Region, 2026-2034

India Data Center Cooling Market Size, Share, Trends & Forecast (2026-2034)

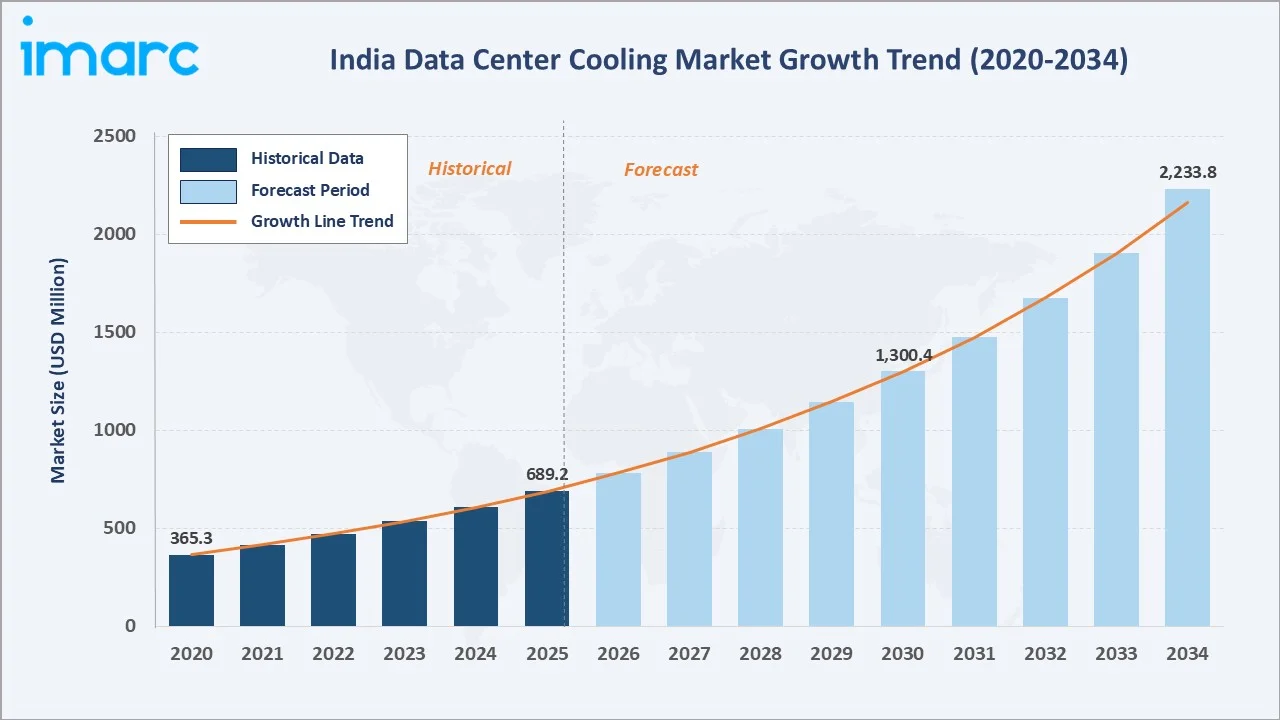

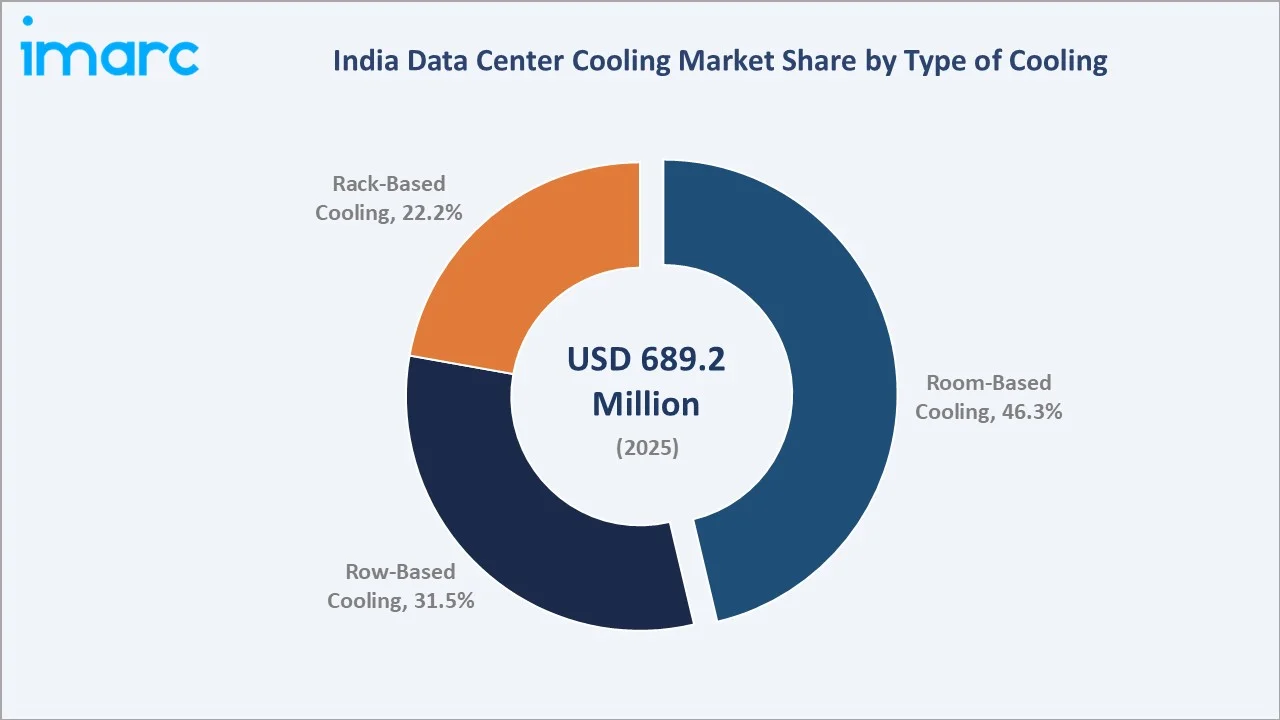

The India data center cooling market reached USD 689.2 Million in 2025 and is projected to reach USD 2,233.8 Million by 2034, growing at a CAGR of 13.54% during 2026-2034. Rapid expansion of hyperscale cloud facilities, surging AI and HPC workloads, government-backed data localization mandates, and the need for energy-efficient thermal management solutions are the primary growth catalysts. India's data center capacity is growing at one of the fastest rates in the Asia Pacific, directly driving demand across all cooling technology segments.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 689.2 Million |

|

Forecast Market Size (2034) |

USD 2,233.8 Million |

|

CAGR (2026-2034) |

13.54% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West and Central India (36.4% share, 2025) |

|

Fastest Growing Segment |

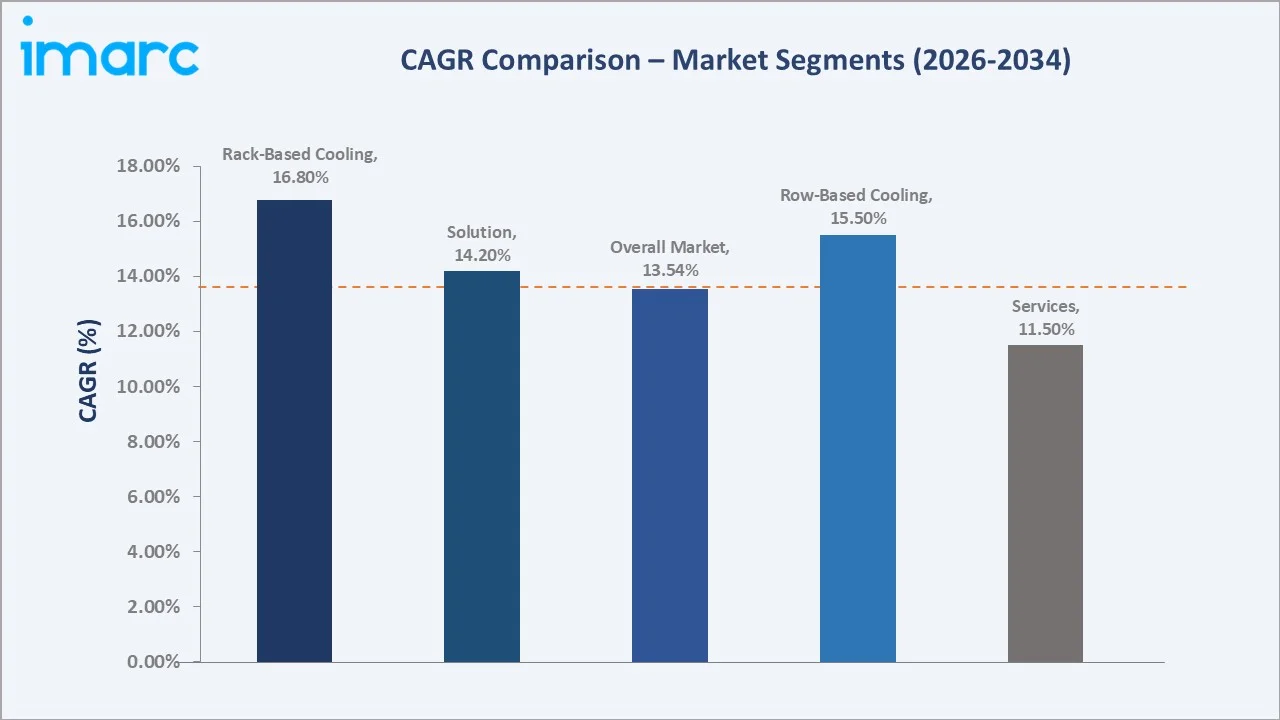

Rack-Based Cooling (~16.8% CAGR) |

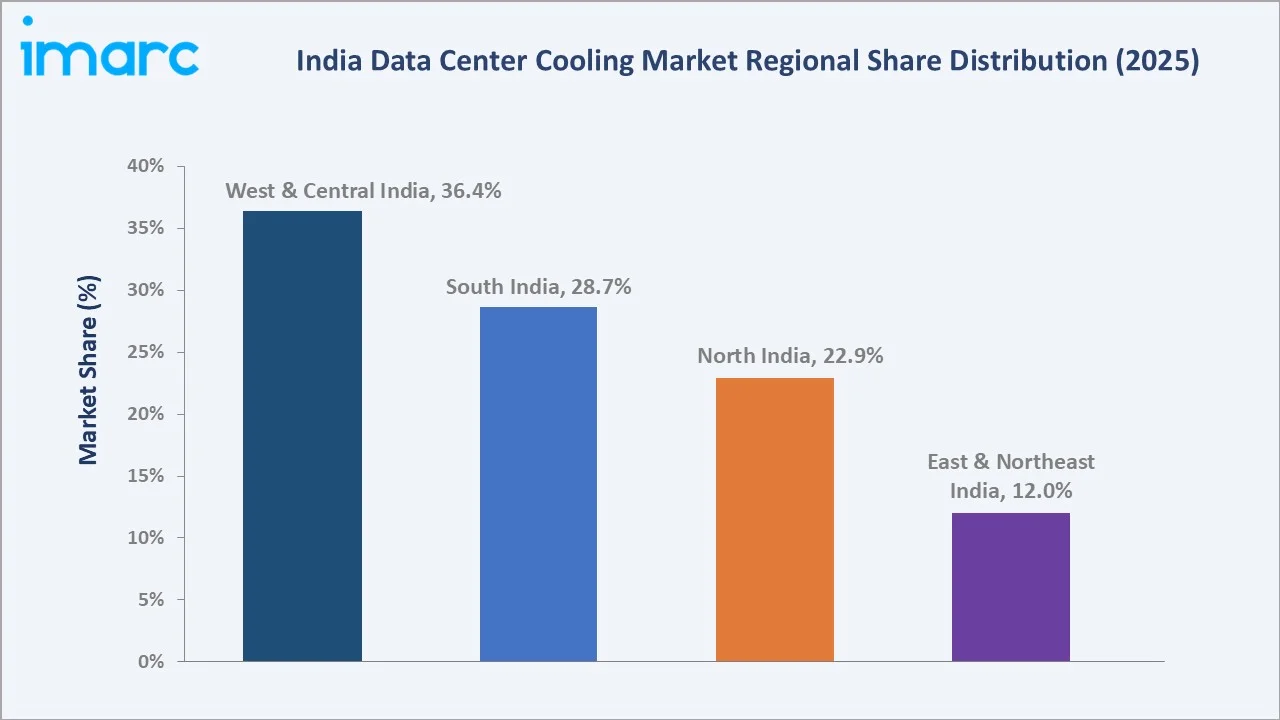

West and Central India lead regionally, holding a 36.4% market share in 2025, anchored by Mumbai's dense hyperscale and colocation data center cluster. The solution segment commands a dominant 72.4% share of the component breakdown, while room-based cooling retains the largest share among cooling types at 46.3%.

To get more information on this market, Request Sample

India's data center cooling market is underpinned by three structural forces: the country's emergence as a global cloud and AI infrastructure hub, rising rack power density driven by GPU-intensive workloads, and the government's push for sovereign data storage. Each force independently increases the density and technical complexity of thermal management requirements, collectively sustaining above-average CAGR through 2034.

Executive Summary

The India data center cooling market is experiencing accelerated expansion, driven by the convergence of hyperscale cloud investments, AI-driven infrastructure densification, and government-mandated data localisation. The market was valued at USD 689.2 Million in 2025 and is forecast to reach USD 2,233.8 Million by 2034, growing at a CAGR of 13.54%. This growth trajectory is anchored by India's data center capacity projected to grow nearly fourfold, reaching 4 GW by FY30, from 1.2 GW in fiscal 2025.

Solution-based cooling products dominate the component segment with a 72.4% share in 2025, encompassing hardware-intensive offerings such as CRAH/CRAC units, chillers, cooling towers, and liquid cooling distribution units. Room-Based Cooling leads the type segment at 46.3%, though row-based (31.5%) and rack-based (22.2%) cooling are growing fastest, driven by rack densities exceeding 20 kW in AI-focused deployments.

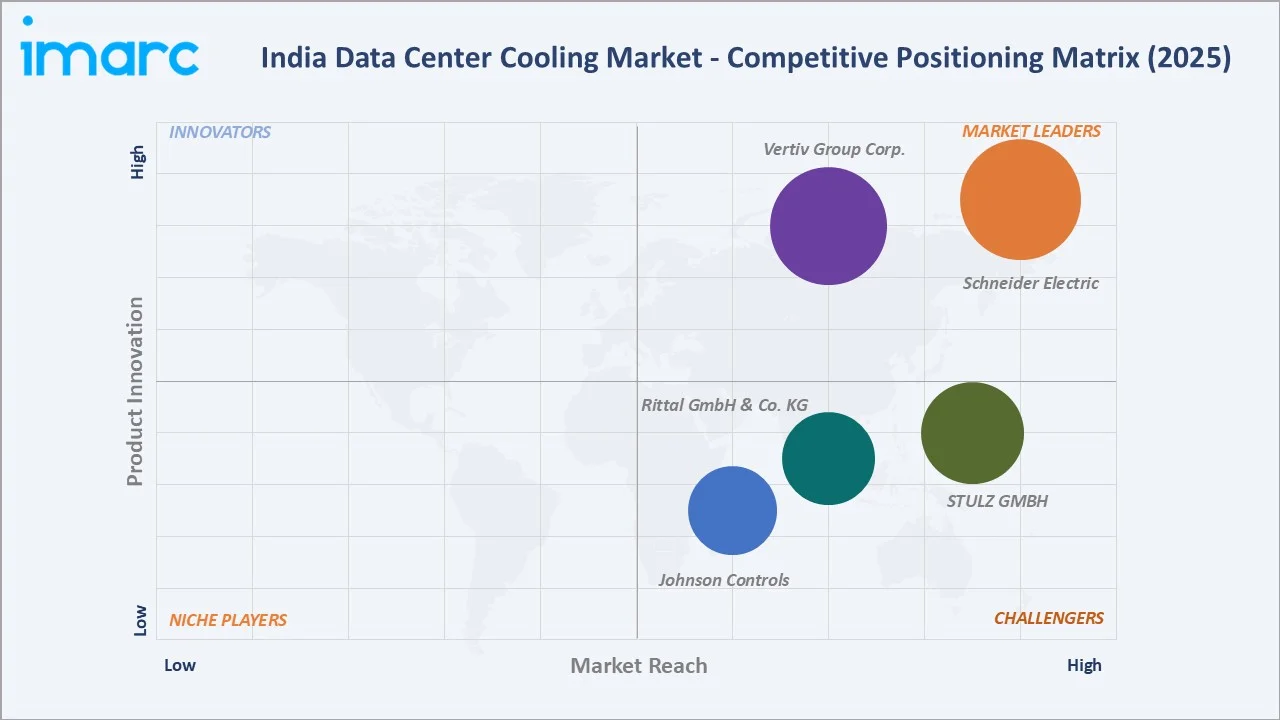

West and Central India lead regionally at 36.4%, anchored by Mumbai's dominant data center cluster hosting 60%+ of India's colocation capacity. South India follows at 28.7%, driven by Hyderabad and Chennai emerging as alternative data center hubs. Leading global vendors, including Schneider Electric, Vertiv Group Corp., STULZ GMBH, Rittal GmbH & Co. KG, and Johnson Controls, dominate the market, alongside India-specific players such as Blue Star, providing cost-competitive solutions for enterprise and mid-market segments.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Solution – 72.4% share (2025) |

|

Fastest Growing Component |

Solution – ~14.2% CAGR (2026-2034) |

|

Largest Type of Cooling |

Room-Based Cooling – 46.3% share (2025) |

|

Fastest Growing Type of Cooling |

Rack-Based Cooling – ~16.8% CAGR (2026-2034) |

|

Leading Region |

West and Central India – 36.4% share (2025) |

|

Top Companies |

Schneider Electric, Vertiv Group Corp., STULZ GMBH, Rittal GmbH & Co. KG, and Johnson Controls |

Key Analytical Observations Supporting the Above Data:

- Solution products account for 72.4% of India's data center cooling market in 2025. This dominance reflects the capital-intensive nature of new data center builds, with hardware solutions including CRAH units, chillers, and liquid cooling distribution units (CDUs) representing the primary expenditure category for hyperscale and colocation operators.

- Room-based cooling at 46.3% remains dominant due to its compatibility with India's existing data center infrastructure, lower upfront density requirements, and suitability for enterprise-class deployments managing mixed IT workload profiles at 5–10 kW per rack.

- Rack-based cooling's 22.2% share is growing fastest as GPU-intensive AI workloads from hyperscalers, including Google, Microsoft Azure, and AWS, push rack densities beyond 20–30 kW, necessitating direct-to-chip or rear-door heat exchanger solutions incompatible with room-level air management.

- West and Central India's 36.4% share reflects Mumbai's status as India's primary data center hub, with Navi Mumbai and Pune hosting over 400 MW of operational data center capacity in 2025. Maharashtra's data center policy incentives and proximity to the submarine cable landing stations at Mumbai drive operator preference.

India Data Center Cooling Market Overview

Data center cooling encompasses the systems, equipment, and services used to maintain optimal thermal conditions within computing facilities, preventing hardware failure and maximizing energy efficiency. India's cooling market spans precision air conditioning (CRAC/CRAH), chiller-based systems, cooling towers, liquid cooling distribution units, rear-door heat exchangers, and immersion cooling systems, serving hyperscale, colocation, enterprise, and edge data center segments.

Macroeconomic drivers include India's real-time data consumption growing at 25%+ annually, government mandates under the Digital Personal Data Protection Act (DPDPA) 2023 requiring onshore data storage, and India's hyperscale cloud market. Power Usage Effectiveness (PUE) regulations and green data center certifications (IGBC, LEED) are also compelling operators to upgrade from legacy air-based systems to more energy-efficient row-based and liquid cooling alternatives that can achieve PUE ratings of 1.014–1.15 versus 1.8+ for older room-cooling configurations.

Market Dynamics

To evaluate market opportunities, Request Sample

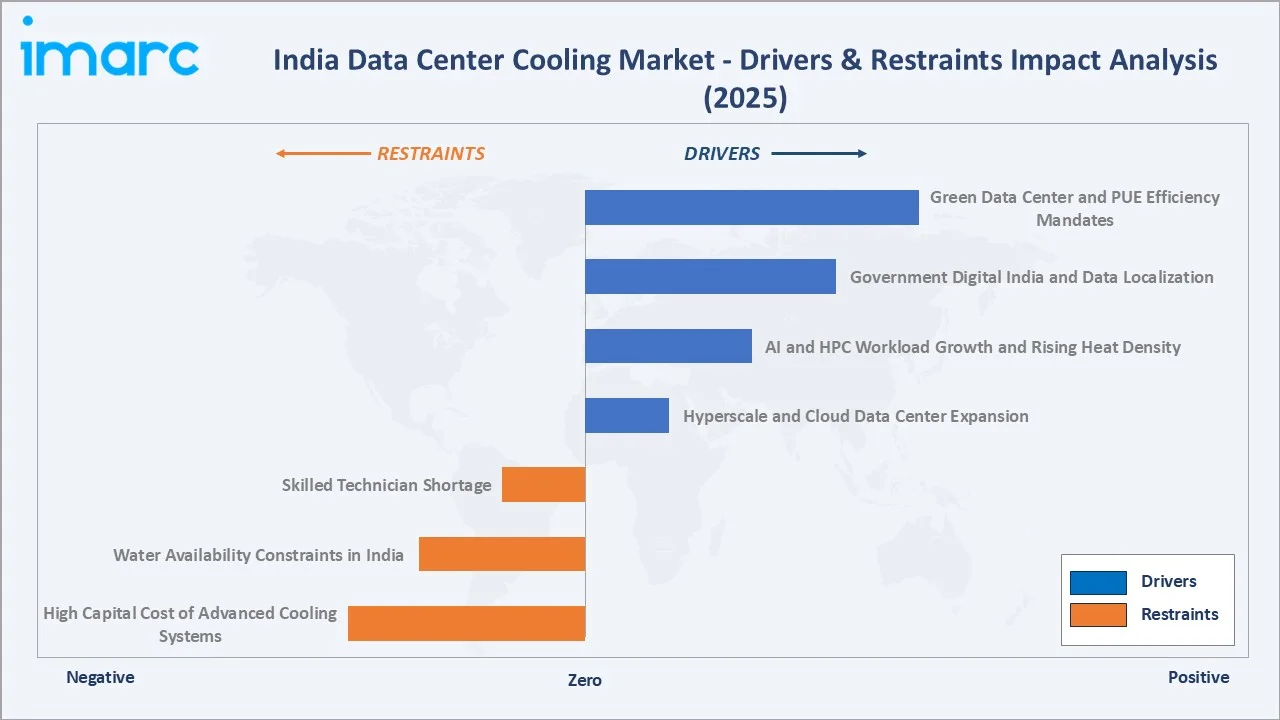

Market Drivers

- Hyperscale and Cloud Data Center Expansion: Global cloud giants, including Amazon Web Services, Microsoft Azure, Google Cloud, and Meta, have each committed multi-billion-dollar investments to India-specific infrastructure. Each MW of new hyperscale capacity requires approximately USD 250,000–400,000 in cooling infrastructure, directly translating to market demand growth.

- AI and HPC Workload Growth and Rising Heat Density: NVIDIA GB200 NVL72 installations, which Schneider Electric designed liquid-cooled architecture for in December 2024, require rack densities exceeding 132 kW, making traditional room-based air cooling physically incapable of maintaining safe operating temperatures.

- Government Digital India and Data Localization: The Digital Personal Data Protection Act (DPDPA) 2023 mandates onshore storage of Indian personal data, accelerating domestic data center investment. Additionally, the government's cloud-first policy for the MEITY-approved state data center policies in Maharashtra, Telangana, and Karnataka is channeling institutional demand toward Indian data center infrastructure.

- Green Data Center and PUE Efficiency Mandates: India's Bureau of Energy Efficiency (BEE) has introduced data center energy performance standards targeting PUE improvement across the sector. Operators achieving PUE below 1.5 qualify for green building incentives, creating a financial pull toward energy-efficient row-based and rack-based cooling systems.

Market Restraints

- High Capital Cost of Advanced Cooling Systems: Liquid cooling infrastructure, including direct-to-chip systems and immersion cooling tanks, commands a high capital cost premium over equivalent air-based systems. For mid-market colocation and enterprise operators in India with constrained CAPEX budgets, this cost differential remains a significant adoption barrier.

- Water Availability Constraints in India: Evaporative cooling towers and certain chiller configurations require substantial water volumes, with a typical 1 MW data center consuming 25–60 million liters of water annually. Water scarcity in interior Indian cities constrains the deployment of water-cooled systems.

- Skilled Technician Shortage: Advanced data center cooling systems, particularly liquid cooling installations incorporating CDUs, rear-door heat exchangers, and immersion tanks, require specialized commissioning and maintenance expertise. India's talent pool for cooling system certification remains limited relative to the pace of market expansion.

Market Opportunities

- Liquid Cooling for AI and GPU Workloads: India's GPU-intensive AI infrastructure investment, led by Sify Technologies' USD 5 Billion AI campus, is creating a substantial addressable market for direct-to-chip and immersion cooling systems.

- Edge Data Center Cooling Solutions: India's 5G rollout and IoT expansion are catalyzing edge data center deployments in 200+ Tier-2 and Tier-3 cities. Edge facilities managing 50–500 kW of IT load require compact, weather-resilient cooling solutions adapted to India's diverse climate zones.

- Free Cooling and Adiabatic Systems in Northern India: India's northern states, including Himachal Pradesh, Uttarakhand, and parts of Rajasthan, offer significant free cooling opportunities using outside air temperatures below 18 degrees Celsius for 3,000+ hours annually.

Market Challenges

- Power Grid Reliability and UPS Integration: India's data center operators face power availability challenges in secondary cities, with grid uptime averaging 95–97% versus the 99.98-99.99% reliability required for Tier III/IV facilities. Cooling systems must integrate with UPS and diesel generator backup configurations, adding engineering complexity and cost.

- Refrigerant Regulatory Transition: India's compliance with the Kigali Amendment to the Montreal Protocol requires phasing down high-GWP HFC refrigerants (R-22, R-410A) used in legacy CRAC/CRAH systems. Operators managing existing cooling fleets face retrofit costs of USD 50,000–200,000 per legacy unit to transition to low-GWP alternatives.

Emerging Market Trends

.webp)

1. Rapid Adoption of Liquid Cooling for High-Density AI Racks

In December 2024, Schneider Electric and NVIDIA collaborated to develop a liquid-cooled architecture for NVIDIA's GB200 NVL72 chips, capable of supporting rack densities exceeding 132 kW. Vertiv recorded a 60% jump in organic orders for high-density cooling platforms in Q1 2024, driven by hyperscale clients accelerating AI infrastructure procurement in India's emerging GPU cluster facilities in Mumbai, Hyderabad, and Chennai.

2. AI-Driven DCIM and Predictive Cooling Optimization

In February 2026, Schneider Electric inaugurated a Motivair liquid cooling solutions factory in Bengaluru, its first such production site in India and only the third globally, to support the country’s expanding AI‑ready, high‑density data center infrastructure by locally manufacturing advanced cooling systems.

3. Growth of Modular and Prefabricated Cooling Infrastructure

Prefabricated cooling modules can reduce on-site installation time by 40–60% versus traditional construction, enabling operators to commission capacity in Tier-2 cities, including Pune, Ahmedabad, and Kochi, within 90–120 days versus 18–24 months for ground-up builds.

4. Immersion Cooling for Ultra-High-Density GPU Applications

The Power Density Roadmaps for AI Clusters Using Immersion Cooling report shows that immersion cooling enables power densities of 100–200 kW per rack, a 3–5× improvement over traditional air cooling, helping data centers handle the high thermal loads of modern AI workloads while cutting cooling costs by ~25–40 %.

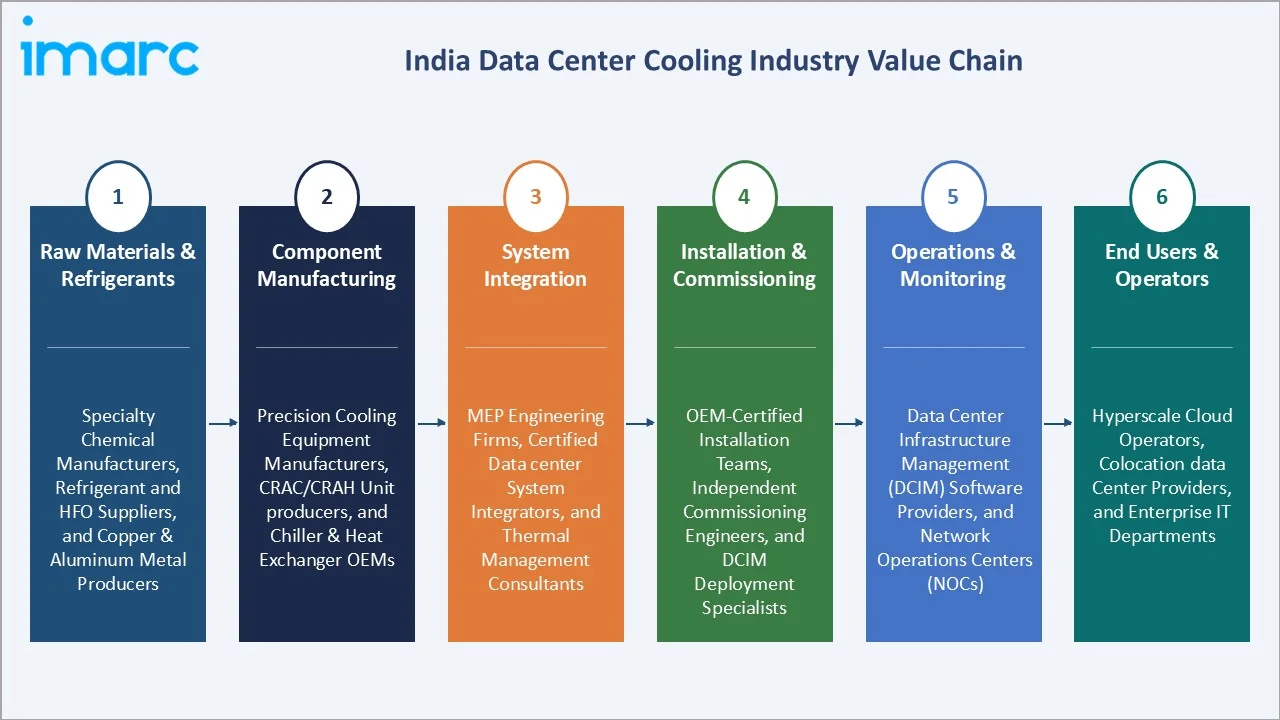

Industry Value Chain Analysis

India's data center cooling value chain spans refrigerant and metal input supply through end-user thermal management, with each stage occupied by specialized manufacturers, integrators, and service providers whose performance directly influences facility uptime, energy efficiency, and compliance outcomes.

|

Stage |

Key Players / Examples |

|

Raw Materials & Refrigerants |

Specialty chemical manufacturers, refrigerant and HFO suppliers, and copper & aluminum metal producers |

|

Component Manufacturing |

Precision cooling equipment manufacturers, CRAC/CRAH unit producers, and chiller & heat exchanger OEMs |

|

System Integration |

MEP engineering firms, certified data center system integrators, and thermal management consultants |

|

Installation & Commissioning |

OEM-certified installation teams, independent commissioning engineers, and DCIM deployment specialists |

|

Operations & Monitoring |

Data Center Infrastructure Management (DCIM) software providers, and network operations centers (NOCs) |

|

End Users & Operators |

Hyperscale cloud operators, colocation data center providers, and enterprise IT departments |

Technology Landscape in the India Data Center Cooling Industry

Precision Air Conditioning – CRAC and CRAH Systems

Computer Room Air Conditioning (CRAC) and Computer Room Air Handler (CRAH) units form the backbone of India's existing data center cooling infrastructure, accounting for the majority of room-based cooling installations. Leading vendors, including Vertiv, Schneider Electric, and STULZ, offer precision cooling units optimized for Indian climatic conditions, with variable-speed EC fans and hot/cold aisle containment configurations.

Chiller-Based and Free Cooling Systems

Chiller plants with water-cooled cooling towers and Computer Room Air Handlers (CRAHs) represent the dominant cooling architecture for large Indian hyperscale and colocation facilities above 5 MW of IT load. Trane Technologies, Johnson Controls, and Daikin offer large-tonnage centrifugal and magnetic bearing chillers optimized for Indian operating temperatures.

Liquid Cooling – Direct-to-Chip and Rear-Door Heat Exchangers

Vertiv's CoolPhase Flex platform and Schneider Electric's NetShelter Liquid Cooling solutions support direct-to-chip cooling for rack densities of 25–100 kW, while rear-door heat exchangers (RDHx) provide a retrofit-friendly path for existing air-cooled facilities. In May 2024, STULZ launched its CyberCool CMU Coolant Management and Distribution Unit, providing heat interchange within liquid-cooled systems with a small footprint specifically designed for high-density compute environments.

Immersion and Phase-Change Cooling

Single-phase and two-phase immersion cooling represent the frontier of Indian data center thermal management, targeting the ultra-high-density AI and HPC segment. Two-phase immersion cooling using dielectric fluids achieves cooling effectiveness exceeding 97% heat removal efficiency. With India's hyperscale AI investments accelerating rack densities beyond 30 kW, immersion cooling is projected to transition from pilot installations to commercial-scale deployments in 2027–2030.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Solution |

72.4% |

2025 |

|

Type of Cooling |

Room-Based Cooling |

46.3% |

2025 |

|

Cooling Technology |

🔒 |

🔒 |

2025 |

|

Type of Data Center |

🔒 |

🔒 |

2025 |

|

Vertical |

🔒 |

🔒 |

2025 |

|

Region |

West and Central India |

36.4% |

2025 |

By Component

The solution segment dominates with a 72.4% share in 2025. This segment encompasses all hardware-based cooling products, including CRAC/CRAH units, chillers, cooling towers, liquid cooling distribution units (CDUs), rear-door heat exchangers, and immersion cooling systems. The Solution segment's dominance reflects the capital-intensive greenfield data center construction cycle underway across India's primary and emerging data center markets.

.webp)

To access detailed market analysis, Request Sample

Services represent 27.6% of the market, encompassing installation and commissioning, preventive maintenance, DCIM software subscriptions, managed cooling-as-a-service, and cooling optimization consulting. The services segment is growing at approximately 11.5% CAGR as hyperscale operators shift from capital-intensive ownership models toward long-term service contracts with OEMs.

By Type of Cooling

Room-based cooling commands a 46.3% share in 2025. This segment includes precision air conditioners and CRAH units deployed at the room level, serving India's large base of enterprise data centers and legacy colocation facilities managing standard rack densities of 5–10 kW.

Row-based cooling represents 31.5%, as new data center builds adopt in-row cooling units placed within server rows for improved thermal efficiency and airflow precision. Rack-based cooling at 22.2% is the fastest-growing type segment, driven by the transition to direct-to-chip liquid cooling and rear-door heat exchangers for GPU-dense AI racks.

Regional Market Insights

West and Central India's market leadership (36.4%, 2025) reflects Mumbai's established status as India's primary data center hub. Mumbai's undersea cable connectivity, reliable power infrastructure, and Maharashtra's government incentive policy combine to sustain the region's dominant position through 2034.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West & Central India |

36.4% |

Dominant hyperscale data center cluster, state-level data center policy incentives, strategic submarine cable connectivity, and a large enterprise IT and colocation operator base |

|

South India |

28.7% |

Rapidly expanding AI and high-performance computing infrastructure, coastal geography enabling alternative cooling advantages, and a strong enterprise IT and technology park ecosystem. |

|

North India |

22.9% |

High-density enterprise data center concentration, large IT park, and government data center deployments, and select geographies offering free cooling potential due to cooler ambient temperatures |

|

East & Northeast India |

12.0% |

Emerging colocation and government data center activity, growing BFSI sector digitization, rising e-governance infrastructure investment, and expanding public sector digital connectivity programs |

South India at 28.7% represents India's fastest-growing data center geography. Hyderabad's transformation into a major AI infrastructure hub, exemplified by Sify Technologies' USD 5 Billion AI campus commitment, is catalyzing liquid cooling adoption at an unprecedented scale.

Competitive Landscape

India's data center cooling market exhibits moderate concentration, with the top five vendors (Schneider Electric, Vertiv Group Corp., STULZ GMBH, Rittal GmbH & Co. KG, and Johnson Controls) collectively holding approximately 50–55% of market revenue in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Schneider Electric |

Uniflair, APC |

Market Leader |

Integrated cooling and power; EcoStruxure DCIM; liquid cooling for AI |

|

Vertiv Group Corp. |

Vertiv, Liebert |

Market Leader |

Precision cooling breadth; 360AI platform; liquid cooling R&D with NVIDIA |

|

STULZ GMBH |

STULZ

|

Strong Challenger |

Precision air conditioning; CyberCool CMU liquid CDU; mission-critical focus |

|

Rittal GmbH & Co. KG |

Rittal’s Liquid Cooling Packages (LCPs), Rittal Blue e+ outdoor cooling, Rittal DLC |

Strong Challenger |

IT cooling enclosures; row-based and rack-based solutions; modular DCs |

|

Johnson Controls |

York, Silent Aire, M&M Carnot |

Challenger |

Chiller plants; integrated building management; large-tonnage systems |

Global OEMs dominate hyperscale and large colocation contracts through established supply chains, comprehensive product portfolios, and certified service networks. Regional players, including Blue Star, serve the enterprise and mid-market colocation segments with cost-competitive solutions tailored to Indian operating conditions.

Key Company Profiles

Schneider Electric

Schneider Electric, headquartered in Rueil-Malmaison, France, is the global leader in integrated data center cooling and power management solutions. Its EcoStruxure platform combines precision cooling, real-time energy optimization, and AI-driven thermal management.

- Product Portfolio: APC precision cooling, InRow cooling, EcoBreeze free cooling, EcoStruxure IT Expert Cooling DCIM, NetShelter liquid cooling for AI racks.

- Recent Developments: In February 2026, Schneider Electric launched a Motivair liquid cooling solutions factory in Bengaluru, its first such facility in India, to support high‑density AI and data center infrastructure with advanced cooling technology.

- Strategic Focus: AI-ready liquid cooling infrastructure; EcoStruxure DCIM SaaS growth; sustainability through low-GWP refrigerant transition.

Vertiv Group Corp.

Vertiv Group Corp., headquartered in Westerville, Ohio, is a global leader in critical digital infrastructure, providing power, cooling, and IT management systems for data centers. Vertiv's Liebert precision cooling is deployed across India's hyperscale and colocation facilities.

- Product Portfolio: Liebert CRAC/CRAH units, CoolPhase Flex hybrid air-liquid platform, Vertiv DCIM.

- Recent Developments: In April 2026, Vertiv strengthened its liquid cooling capabilities by acquiring Strategic Thermal Labs (STL), a move that enhances its thermal management solutions for high‑performance computing and data center environments.

- Strategic Focus: AI and HPC liquid cooling leadership; 360AI platform integrating power, cooling, and monitoring; India service network expansion.

STULZ GmbH

STULZ, headquartered in Hamburg, Germany, specializes in precision air conditioning and liquid cooling systems for mission-critical data center environments, with over 70 years of thermal engineering expertise. In India, STULZ operates through a direct sales and service network serving hyperscale, colocation, and telecom data center operators across major metros.

- Product Portfolio: CyberAir 3PRO precision air conditioners (R513A low-GWP compatible), CyberCool CMU liquid cooling distribution units, CyberRow in-row cooling units.

- Recent Developments: In September 2025, STULZ introduced a new water-cooled (fan-based cooling rack, CyberRack SideCooler, designed specifically for edge data centers, offering cooling capacity from 18-51 kW, with power consumption ranging from 0.7-2.6 kW.

- Strategic Focus: Liquid cooling CDU market penetration; low-GWP refrigerant transition; hyperscale colocation contract expansion in India.

Market Concentration Analysis

India's data center cooling market exhibits moderate concentration, with the top five global OEMs holding approximately 50–55% of total revenue in 2025. Below the top tier, a competitive mid-market of 15–20 specialized vendors and regional integrators serves enterprise, edge, and government data center segments with tailored solutions.

Consolidation is occurring primarily through the acquisition of liquid cooling capabilities by established air-cooling incumbents: Schneider Electric's acquisition of Motivair and STULZ's CDU product launches reflect a strategic pivot toward capturing the faster-growing liquid cooling sub-market without M&A of direct competitors.

Investment & Growth Opportunities

Fastest Growing Segments

Rack-Based Cooling and liquid cooling systems (~16.8% CAGR), AI-optimized DCIM software (22%+ CAGR), immersion cooling for GPU clusters (27%+ CAGR), and edge data center cooling solutions (22% CAGR) represent the highest-growth investment vectors through 2034. Together, these subcategories address a combined addressable market of approximately USD 650 Million by 2030 within India's data center cooling ecosystem.

Emerging Market Expansion

Hyderabad, Chennai, Pune, and Noida collectively represent an incremental USD 400+ Million data center cooling opportunity beyond Mumbai by 2034, as geographic diversification of India's hyperscale infrastructure accelerates. Entry strategies for cooling vendors targeting these emerging hubs include local stocking of critical spare parts, certified service engineer deployment, and partnership with regional data center developers who are committing capacity ahead of tenant demand.

Venture and Institutional Investment Trends

- Global hyperscaler CAPEX commitments to India exceed USD 15 Billion through 2030, directly translating to cooling infrastructure procurement pipelines for Tier-1 vendors. Multi-year supply contracts with hyperscalers are enabling OEMs to allocate larger R&D budgets to immersion and direct-to-chip systems.

- Government production-linked incentive schemes for electronics manufacturing create opportunities for localizing data center cooling component manufacturing in India, reducing import dependency for CRAC units and chillers currently sourced from Germany, Japan, and China.

- Cooling-as-a-Service (CaaS) business models are emerging where vendors retain cooling asset ownership and charge operators on a per-kW-cooled basis. This OpEx model reduces operator CAPEX barriers and enables OEMs to earn lifecycle service revenue, potentially commanding 30–40% revenue premiums over traditional equipment sales.

Future Market Outlook (2026-2034)

India's data center cooling market is positioned for sustained, high-growth expansion through 2034. From a base of USD 689.2 Million in 2025, the market is projected to reach USD 2,233.8 Million by 2034, representing total incremental value creation of USD 1,544.6 Million at a CAGR of 13.54%. This growth is structurally assured by the multi-year hyperscale capacity pipeline and India's irreversible trajectory toward becoming a top-5 global data center market by installed capacity.

The technology transition from air-based to liquid cooling will define the market's composition by 2034. Room-based cooling's share is projected to decline from 46.3% in 2025 to approximately 35% by 2034, while rack-based liquid cooling is expected to grow from 22.2% to 32%+. This technology shift creates replacement demand opportunities for incumbent vendors and market entry opportunities for liquid cooling specialists.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 110 industry participants in 2024–2025, including data center operators, cooling system vendors, installation contractors, energy efficiency consultants, and institutional investors across India, Europe, and the US. Expert input validated market sizing, technology adoption rates, and regional deployment trends.

Secondary Research

Secondary research encompassed vendor annual reports, ASHRAE and BICSI technical standards documentation, BEE energy efficiency reports, NASSCOM data center market surveys, international trade data (DGFT cooling equipment imports), and industry publications (Data Center Dynamics, DCD, Uptime Institute).

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating data center capacity additions (MW), cooling intensity per kW (USD/kW), technology mix transitions, and vendor revenue disclosures. A base-case CAGR of 13.54% reflects consensus estimates validated against announced capacity pipelines and cooling equipment procurement patterns from FY2020 to FY2025.

India Data Center Cooling Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Types of Cooling Covered | Room-Based Cooling, Row-Based Cooling, Rack-Based Cooling |

| Cooling Technologies Covered | Liquid-Based Cooling, Air-Based Cooling |

| Types of Data Center Covered | Small-Scale Data Center, Medium-Scale Data Center, Large-Scale Data Center |

| Verticals Covered | BFSI, IT and Telecom, Research and Educational Institutes, Government and Defense, Retail, Energy, Healthcare, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | Schneider Electric, Vertiv Group Corp., STULZ GMBH, Rittal GmbH & Co. KG, Johnson Controls, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India data center cooling market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India data center cooling market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India data center cooling industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Data Center Cooling Market Report

The India data center cooling market reached USD 689.2 Million 2025 and is projected to reach USD 2,233.8 Million by 2034.

The market is expected to grow at a CAGR of 13.54% during 2026-2034, driven by hyperscale expansion, AI workload densification, and liquid cooling adoption.

West and Central India lead with a 36.4% share in 2025, anchored by Mumbai's hyperscale data center cluster and Maharashtra's data center incentive policies.

Solutions dominate with a 72.4% share in 2025, encompassing CRAC/CRAH units, chillers, liquid CDUs, and other hardware-based cooling products.

Room-based cooling holds the largest share at 46.3%, driven by India's existing enterprise data center infrastructure managed at standard rack densities.

Key players include Schneider Electric, Vertiv Group Corp., STULZ GMBH, Rittal GmbH & Co. KG, and Johnson Controls.

Rack-based cooling is growing at approximately 16.8% CAGR because AI GPU clusters require rack densities of 20–132+ kW that exceed the thermal management capacity of room-level air cooling systems.

Key challenges include high capital costs of advanced liquid cooling, water availability constraints in secondary cities, refrigerant regulatory transition costs, and a shortage of skilled cooling technicians.

Liquid cooling for AI racks, immersion cooling for GPU clusters, edge data center cooling, AI-driven DCIM software, and Cooling-as-a-Service models represent the highest-growth investment opportunities.

AI workloads are raising rack power densities from 7–10 kW to 30–132+ kW, making traditional room-based air cooling technically insufficient and driving rapid adoption of row-based and rack-based liquid cooling systems.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade