India Diesel Generator Market Size, Share, Trends and Forecast by Capacity, Application, Mobility, End User, and Region, 2026-2034

India Diesel Generator Market Size & Forecast 2026-2034

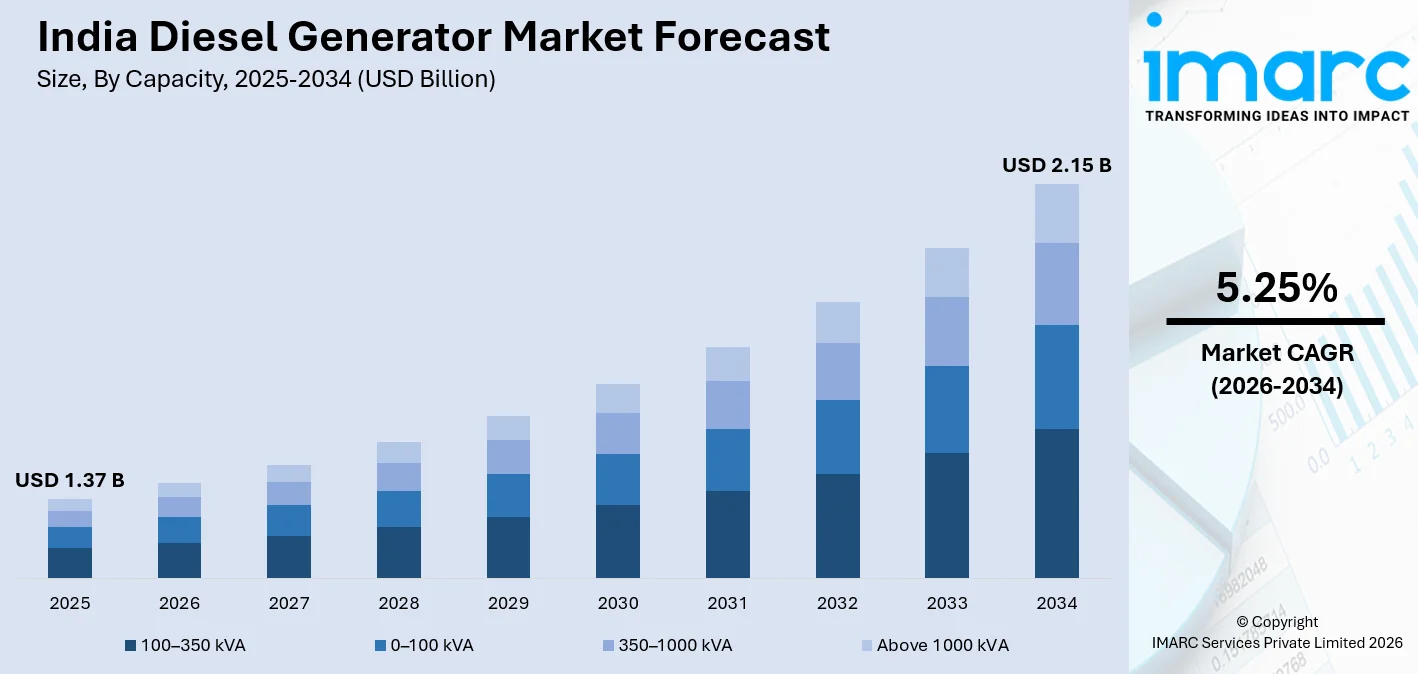

India diesel generator market size was valued at USD 1.37 Billion in 2025, and is projected to reach USD 2.15 Billion by 2034, growing at a CAGR of 5.25% during 2026-2034, driven by persistent grid reliability gaps, expanding industrial infrastructure, and rising power demand from data centers. India's electricity peak demand reached 250 GW in May 2024, surpassing projections by 6.3%, highlighting growing power supply pressures and strengthening the need for diesel generators as reliable backup power solutions across commercial, industrial, and infrastructure sectors.

To get more information on this market Request Sample

India Diesel Generator Industry Analysis - Key Insights

- 100–350 kVA commands the largest capacity share at 37.0% in 2025 - mid-range industrial applications dominate, with construction, hospitals, and commercial complexes driving steady demand for generators in this power band.

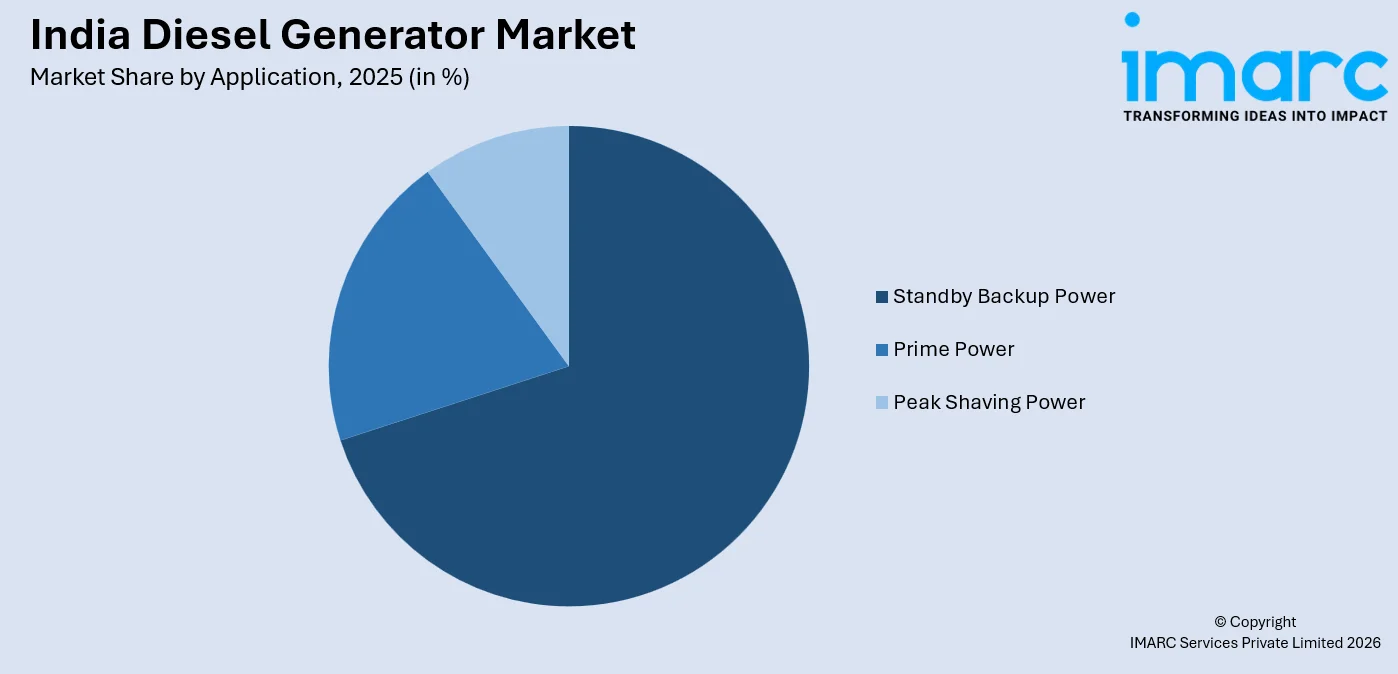

- Standby backup power holds a dominant 70.0% application share in 2025 - the structural preference for using generators as insurance against outages, rather than continuous workhorses, reflects India's improving but still unreliable grid.

- Stationary accounts 71.0% of the mobility segment in 2025 - fixed installations in factories, hospitals, and commercial complexes form the demand backbone, though portable units are gaining ground at construction sites.

- Industrial commands 42.0% of end user market share in 2025 - manufacturing, cement, textiles, and data centers rely on high-capacity gensets, with CPCB IV+ compliance deadlines reshaping procurement cycles.

- West India leads regionally at 31.0% in 2025 - Maharashtra and Gujarat's dense industrial clusters, combined with Mumbai's booming data center investments, make this the largest region and a premium-spec genset market.

India Diesel Generator Market Trends and Dynamics 2026

Market Trends

CPCB IV+ Emission Norms Triggering Fleet Upgrades Across India

India's diesel generator landscape is undergoing a structural shift following full enforcement of CPCB IV+ emission standards, which mandate selective catalytic reduction (SCR) and diesel particulate filters (DPF) across all power ratings. Factory prices have risen 15-20% as manufacturers integrate advanced after-treatment systems, triggering an accelerated replacement cycle across industrial and commercial fleet owners upgrading legacy genset units.

Hybrid and IoT-Enabled Systems Transforming the Genset Ecosystem

The convergence of digital connectivity and renewable energy integration is redefining India's diesel generator market trends, as manufacturers embed IoT gateways for real-time monitoring, predictive maintenance, and remote load management. India added 25.1 GW of non-fossil energy capacity in H1 2025, up 69% year-on-year, accelerating hybrid diesel-solar deployments across commercial and industrial installations.

- CPCB IV+ Compliance Wave: Emission norm upgrades are pushing fleet owners toward fuel-injected, filter-equipped gensets, benefiting OEMs with certified after-treatment capabilities.

- Hybrid Genset Adoption: Diesel-solar and diesel-battery configurations are gaining ground, particularly in telecom towers and industrial campuses aiming to cut operational costs and carbon footprint.

- Remote Monitoring and Predictive Maintenance: IoT-enabled cloud dashboards are now standard on premium gensets, reducing unplanned downtime across hospitals, data centers, and manufacturing plants.

- Fuel-Agnostic Engine Platforms: Leading OEMs are launching hydrogen-ready and CNG-compatible genset architectures to future-proof portfolios against tightening carbon regulations.

Growth Drivers

Government Infrastructure Push Anchoring Long-Term Demand

India's Union Budget 2025–26 allocated INR 11.21 trillion for capital expenditure on highways, metro rail, and industrial corridors, directly fueling the India diesel generator market growth by generating large-scale, sustained demand for on-site backup and prime power solutions at construction sites and newly commissioned industrial facilities across the country.

Data Centre Boom Creating Tier-1 Demand for High-Capacity Gensets

India's data center installed capacity reached approximately 1.5 GW by mid-2025, with projections to scale to 6.5 GW by 2030, according to CBRE and CEEW research. Each hyperscale campus requires massive on-site diesel backup to ensure zero-downtime SLAs, driving strong orders for high-capacity gensets in the 350 kVA–1,000+ kVA range from Maharashtra, Karnataka, and Telangana data center clusters.

- Urbanization and Commercial Growth: India's rapid urban expansion is generating consistent demand for mid-range gensets across hotels, malls, hospitals, and office complexes in Tier-2 and Tier-3 cities.

- Expanding Telecom Tower Infrastructure: India's 5G rollout and rural tower densification programs are creating additional backup power requirements at hundreds of thousands of remote telecom sites nationwide.

- Rural Electrification Gaps: Despite improving grid reach, power supply remains unreliable in semi-urban and rural areas, sustaining structural demand for entry-level and mid-range diesel gensets.

- Make in India and Industrial Policy: Government-backed industrial cluster policies and export-linked manufacturing incentives are expanding factory footprints, requiring robust prime-power and standby backup solutions.

Market Restraints

Stringent CPCB Emission Regulations and Compliance Costs: Meeting evolving CPCB IV+ emission norms requires manufacturers to invest in advanced exhaust after-treatment systems and redesigned engines. The resulting price increases reduce affordability for price-sensitive segments and create compliance barriers for smaller assemblers and regional distributors serving cost-constrained markets.

Growing Competition from Renewable Energy Alternatives: Solar photovoltaic systems, battery energy storage, and hybrid power solutions are increasingly cost-competitive alternatives to diesel generators, especially in grid-connected urban areas. As renewable adoption accelerates and battery costs decline, diesel gensets face growing substitution risk in residential and small commercial segments.

Diesel Fuel Price Volatility and High Operational Costs: Diesel is the primary operating cost for genset users, and price fluctuations from crude oil markets and domestic taxes directly affect total ownership costs. Fuel cost uncertainty discourages adoption in price-sensitive segments and weakens the economic argument for diesel backup against emerging alternatives.

India Diesel Generator Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Capacity | 100–350 kVA | 37.0% | 2025 |

| Application | Standby Backup Power | 70.0% | 2025 |

| Mobility | Stationary | 71.0% | 2025 |

| End User | Industrial | 42.0% | 2025 |

| Region | West India | 31.0% | 2025 |

Capacity Insights

100–350 kVA – 37.0% Market Share (2025) | Leading Capacity

The 100–350 kVA range commands the largest capacity share, serving hospitals, hotels, manufacturing plants, and IT parks requiring reliable mid-tier standby power. In line with the India diesel generator market outlook for emission-compliant solutions, GSP Power Projects, an authorized Mahindra & Mahindra dealer, launched a CPCB IV+ compliant lineup from 10 kVA to 320 kVA at Bari Brahmana, Jammu, and Faridabad in September 2024, featuring CRDI engines for superior fuel economy.

|

Segment Breakdown 100–350 kVA (37.0%) · 0–100 kVA · 350–1000 kVA · Above 1000 kVA |

Application Insights

Access the comprehensive market breakdown Request Sample

Standby Backup Power - 70.0% Market Share (2025) | Leading Application

Standby backup power commands India diesel generator application market, as businesses and institutions primarily treat diesel gensets as insurance against grid failures rather than as continuous power sources. India's IndiaAI Mission, backed by INR 103 billion (~USD 1.25 Billion) in government funding, is scaling AI-ready data center infrastructure nationwide, each facility mandating robust standby backup systems to ensure zero-downtime operational reliability.

|

Segment Breakdown Standby Backup Power (70.0%) · Prime Power · Peak Shaving Power |

Mobility Insights

Stationary - 71.0% Market Share (2025) | Leading Mobility

Stationary units hold the largest share of the India diesel generator mobility segment, anchored by fixed installations in factories, hospitals, commercial complexes, and data centers. India's residential rooftop solar capacity reached 3.2 GW by March 2024, accounting for 27% of India’s total rooftop solar capacity, which currently stands at nearly 11.9 GW. This is gradually reducing grid-connected residential genset needs while industrial and commercial stationary demand continues growing.

|

Segment Breakdown Stationary (71.0%) · Portable |

End User Insights

Industrial - 42.0% Market Share (2025) | Leading End User

Industrial end users account for the largest share of the India diesel generator market, dominated by cement, steel, chemicals, textiles, and auto manufacturing that depend on gensets for standby and prime-power needs. In 2024, Recon Technologies Pvt Ltd unveiled Mahindra Powerol CPCB IV+ compliant diesel gensets in Hyderabad, offering capacities up to 625 kVA, reflecting industrial buyers' growing preference for certified, high-performance backup power solutions.

|

Segment Breakdown Industrial (42.0%) · Residential · Commercial |

Regional Insights

West India - 31.0% Market Share (2025) | Leading Region

West India dominates the market, anchored by Maharashtra and Gujarat's dense industrial clusters spanning chemicals, pharmaceuticals, auto components, and petrochemicals. In March 2025, Amazon Web Services announced a USD 8.3 billion Maharashtra investment encompassing AI-focused data center campuses, dramatically increasing demand for high-capacity backup gensets to ensure uninterrupted operations.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

31.0%

|

|

Key States

|

Maharashtra, Gujarat, Goa, Rajasthan |

|

Major Growth Drivers

|

Industrial cluster expansion, data center investments, petrochemical sector growth, infrastructure development |

|

Outlook

|

Strongest demand growth from the data center sector |

|

Regional Breakdown West India (31.0%) · North India · South India · East India |

North India:

North India is a significant demand area for diesel generators in the mid-range segment, owing to driven by Uttar Pradesh's industrial concentration, Delhi-NCR's commercial growth, and Punjab and Haryana's agro-processing base. Peak demand variations in power supply and the need for constant expansions in industrial hubs are also contributing factors to the demand for diesel generators in this area. The rapid development of data centers, logistics parks, and real estate projects is also contributing to the demand for diesel generators in this area.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Delhi, Uttar Pradesh, Punjab, Haryana, Uttarakhand |

|

Major Growth Drivers

|

Highway and metro construction, industrial corridor development, commercial real estate expansion, agriculture sector electrification |

|

Outlook

|

High infrastructure-linked genset demand sustained |

South India:

The diesel generator market in South India is driven by Tamil Nadu's textile and automotive industries, Karnataka's IT complex, and Telangana's growing data center and pharmaceutical industries. In April 2025, NTT DATA and Neysa Networks signed an MoU with the Telangana government to invest INR 10,500 crore in a 400 MW AI-driven data center cluster in Hyderabad, anchoring sustained demand for high-capacity backup gensets.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Tamil Nadu, Karnataka, Andhra Pradesh, Telangana, Kerala |

|

Major Growth Drivers

|

IT and data center growth, export-oriented manufacturing, pharma cluster expansion, healthcare infrastructure |

|

Outlook

|

Fast-growing demand from digital infrastructure |

East India:

The diesel generator market in East India is a growing market driven by Odisha's mining industry, West Bengal's industries, and Jharkhand's manufacturing industries. The allocation of INR 19,000 crore by the Union government for Pradhan Mantri Gram Sadak Yojana in the Budget 2025-26 has a major allocation for Eastern India, driving infrastructure construction in rural India and creating a growing market for portable and stationary DG sets in this region.

|

Metric

|

Details

|

|---|---|

|

Key States

|

West Bengal, Odisha, Jharkhand, Bihar, Chhattisgarh |

|

Major Growth Drivers

|

Mining and steel sector power needs, rural infrastructure development, agricultural processing growth, and rising telecom tower penetration |

|

Outlook

|

Rising demand from rural and industrial segments |

Market Outlook 2026-2034

What is the future outlook of India diesel generator market?

India diesel generator market is expected to sustain steady revenue growth through 2034.

India's diesel generator market size is expected to experience a smooth growth trajectory until 2034, driven by the continued gap in grid reliability, increasing pace of industrial and data center capacity additions, and rising demand in the commercial segment of Indian cities. India diesel generator market forecast includes continued CPCB IV+ upgrade demand, rising hybrid genset-solar solutions, and increasing diesel genset market share in Tier 2 and Tier 3 cities, where stable power infrastructure remains a long-term challenge.

India Diesel Generator Market - Leading Key Players

India diesel generator market is moderately consolidated, with a number of global as well as local diesel genset manufacturers competing on technology, CPCB IV+ compliance, and service capabilities. The top-tier companies are investing heavily in CPCB IV+-compliant solutions, IoT capabilities, as well as service capabilities to target the high-growth potential of the Indian market.

| Company | Leading Brands | Highlights |

|---|---|---|

| Cummins India Ltd. | PowerCommand, CPCB IV+ Series | Launched CPCB IV+ gensets up to 800 kVA with OptiNAS+ filtration (July 2024); reported 30.8% revenue growth in Q2 FY25 driven by data-center and infrastructure orders. |

| Kirloskar Oil Engines Limited | Optiprime, KOEL Green / iGreen | Leading domestic OEM with IoT-enabled Optiprime smart gensets featuring remote monitoring and cloud dashboards; piloting hydrogen fuel-cell solutions to future-proof its product portfolio. |

| Mahindra Powerol Ltd. | Powerol CPCB IV+ Gensets | India's largest domestic genset brand by volume in sub-250 kVA; CPCB IV+ compliant lineup expanded in 2024 with hybrid and renewable-ready configurations for commercial and residential markets. |

Some of the existing key players in the market are Caterpillar Inc. (FG Wilson), Greaves Cotton Limited, Ashok Leyland Ltd., Jakson Group, Cooper Corporation, etc.

Latest Development & News

- In December 2025, Cummins India unveiled its CPCB IV+-compliant 82.5 kVA diesel genset at CII EXCON 2025 in Bengaluru. The genset features a compact footprint, superior fuel efficiency, and low-noise operation, targeting India's quick-commerce, construction, and infrastructure sectors. Cummins highlighted the product as part of its next-generation CPCB IV+ portfolio, combining cleaner performance with high reliability for continuous and prime-power applications.

- In January 2025, Cummins Group unveiled its next-generation HELM engine platforms at the Bharat Mobility Global Expo 2025. The platforms feature the high-performance L10 engine, an advanced Hydrogen Fuel Delivery System (FDS) with Type IV onboard storage vessels, and the B6.7N natural gas engine, positioning Cummins India for the transition to fuel-flexible and lower-emission power solutions across industrial and infrastructure segments.

- In January 2025, Ashok Leyland unveiled its SAATHI platform at the Bharat Mobility Global Expo 2025, integrating CPCB IV+ gensets with predictive maintenance software. The platform targets construction and logistics fleet operators, reducing unplanned downtime through real-time diagnostics and cloud-based service alerts, reinforcing Ashok Leyland's positioning in the industrial and infrastructure genset segment.

India Diesel Generator Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Capacities Covered | 0-100 kVA, 100-350 kVA, 350-1000 kVA, Above 1000 kVA |

| Applications Covered | Standby Backup Power, Prime Power, Peak Shaving Power |

| Mobilites Covered | Stationary, Portable |

| End Users Covered | Residential, Commercial, Industrial |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India diesel generator market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India diesel generator market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India diesel generator industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Diesel Generator Market Report

India diesel generator market was valued at USD 1.37 Billion in 2025.

The market is anticipated to reach a value of USD 2.15 Billion by 2034.

The 100–350 kVA segment dominates the market with a share of 37.0%, serving mid-tier commercial and industrial buyers, including hospitals, manufacturing plants, and IT parks that require high-volume standby power without the operational complexity of large-format generator sets.

The standby backup power segment commands the market with a share of 70.0%, reflecting the widespread practice of deploying diesel generators as insurance against grid failures rather than continuous-duty workhorses, particularly in commercial buildings, healthcare facilities, and industrial plants across India.

The stationary segment commands the market with a share of 71.0%, driven by strong demand for reliable backup power across commercial buildings, manufacturing facilities, healthcare institutions, and data centers amid grid instability and rising electricity consumption.

The industrial segment commands the market with a share of 42.0%, supported by expanding manufacturing activities, infrastructure development, and the need for continuous power supply in sectors such as construction, mining, oil & gas, and large-scale processing industries.

West India currently leads the market, accounting for a share of 31.0%. Maharashtra and Gujarat's dense manufacturing clusters, Mumbai's expanding data center ecosystem, and government infrastructure investments in the region underpin robust demand for both industrial-grade and high-capacity backup power solutions.

Some of the major players in the market include Cummins India Ltd., Kirloskar Oil Engines Limited, Mahindra Powerol Ltd., Caterpillar Inc. (FG Wilson), Greaves Cotton Limited, Ashok Leyland Ltd., Jakson Group, Cooper Corporation, etc.

India diesel generator market is being shaped by the rapid adoption of CPCB IV+-compliant technologies, the growth of diesel-solar hybrid configurations, and IoT-enabled remote monitoring systems.

India’s diesel generator market faces challenges, including escalating compliance costs from CPCB IV+ emission upgrades, increasing competition from solar-battery hybrid systems in urban and grid-connected markets, and diesel fuel price volatility that raises the total cost of ownership.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)