India Drop Shipping Market Size, Share, Trends and Forecast by Product and Region, 2026-2034

India Drop Shipping Market Size, Share, Trends & Forecast (2026-2034)

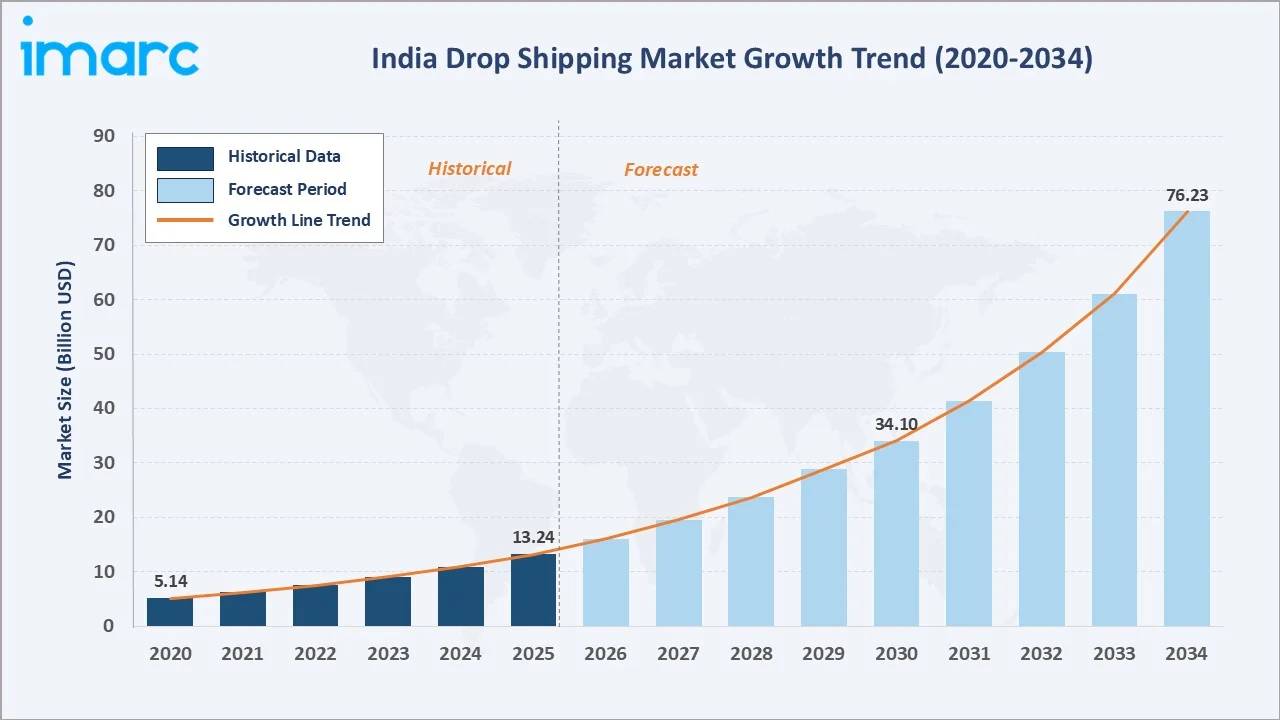

The India drop shipping market reached USD 13.24 Billion in 2025 and is projected to reach USD 76.23 Billion by 2034, growing at a CAGR of 20.83% during 2026-2034. Rising internet penetration, exponential growth of e-commerce platforms, increasing smartphone adoption, and the low capital entry barrier of the drop shipping model are the primary growth catalysts of the market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 13.24 Billion |

|

Forecast Market Size (2034) |

USD 76.23 Billion |

|

CAGR (2026-2034) |

20.83% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

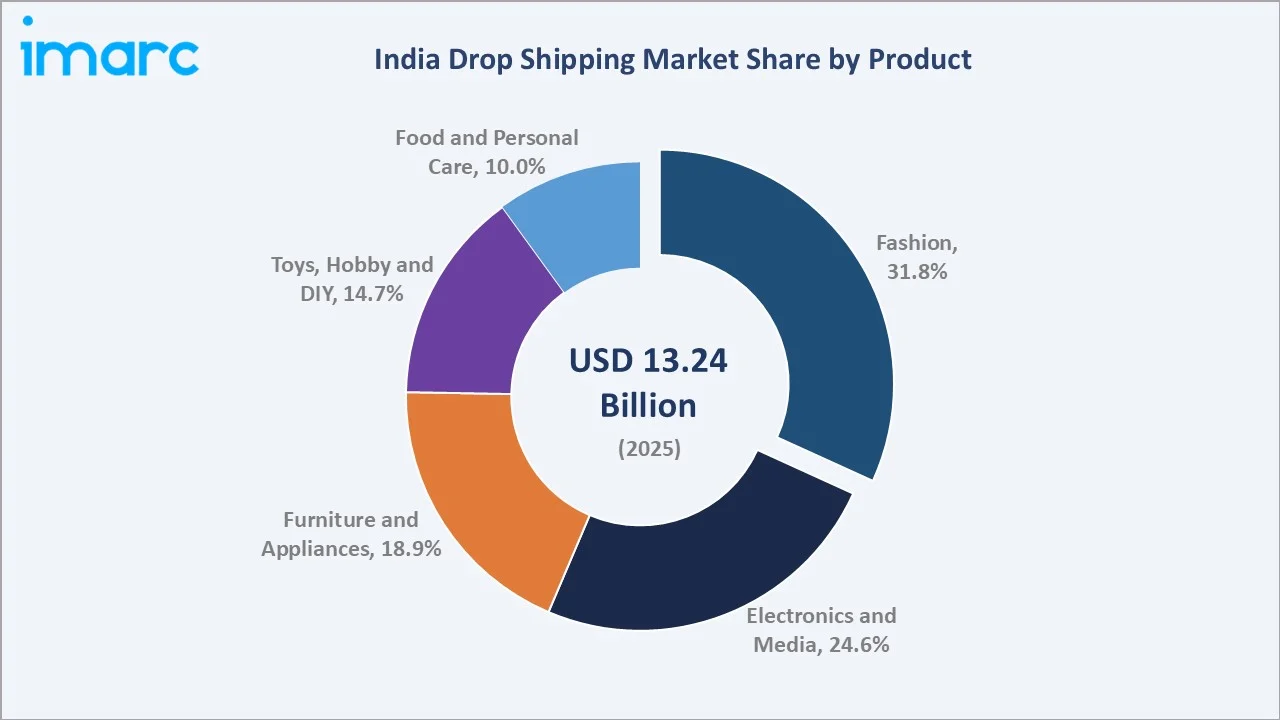

North India leads regionally, holding a 30.9% market share in 2025, anchored by its large urban consumer base, well-developed digital infrastructure, and high e-commerce adoption rates. The fashion segment commands the dominant 31.8% product share, while electronics and media follow with 24.6%, collectively accounting for over half of total market revenues in 2025.

To get more information on this market, Request Sample

India's drop shipping market is underpinned by three structural forces: the country's rapid digital infrastructure expansion, the entrepreneurial adoption of zero-inventory retail models by micro and small enterprises, and the sustained growth of India's e-commerce consumption base. Each force independently accelerates drop shipping adoption, collectively sustaining the CAGR of 20.83% through 2034.

Executive Summary

The India drop shipping market is experiencing high-growth expansion, driven by the convergence of rising internet penetration, the proliferation of e-commerce platforms, and the structural appeal of the zero-inventory business model for India's expanding micro-entrepreneur and SME community. The market was valued at USD 13.24 Billion in 2025 and is forecast to reach USD 76.23 Billion by 2034, growing at a CAGR of 20.83%.

Fashion leads the product segment with a 31.8% share in 2025, driven by high SKU diversity, low unit values enabling low-risk experimentation by resellers, and the social commerce trend accelerating fashion drop shipping through influencer-driven channels. Electronics and media follow at 24.6%, underpinned by consistent consumer demand for gadgets, accessories, and digital products at competitive online price points.

North India leads regionally at 30.9%, driven by Delhi-NCR's digital commerce hub status and strong consumer demand. Leading platforms such as Amazon, Meesho, and Shopify enable merchants to build drop shipping businesses at near-zero upfront capital investment. The competitive landscape is evolving rapidly, with social commerce and AI-driven automation tools expanding the accessible supplier and reseller base.

Key Market Insights

|

Insight |

Data |

|

Largest Product |

Fashion – 31.8% share (2025) |

|

Fastest Growing Product |

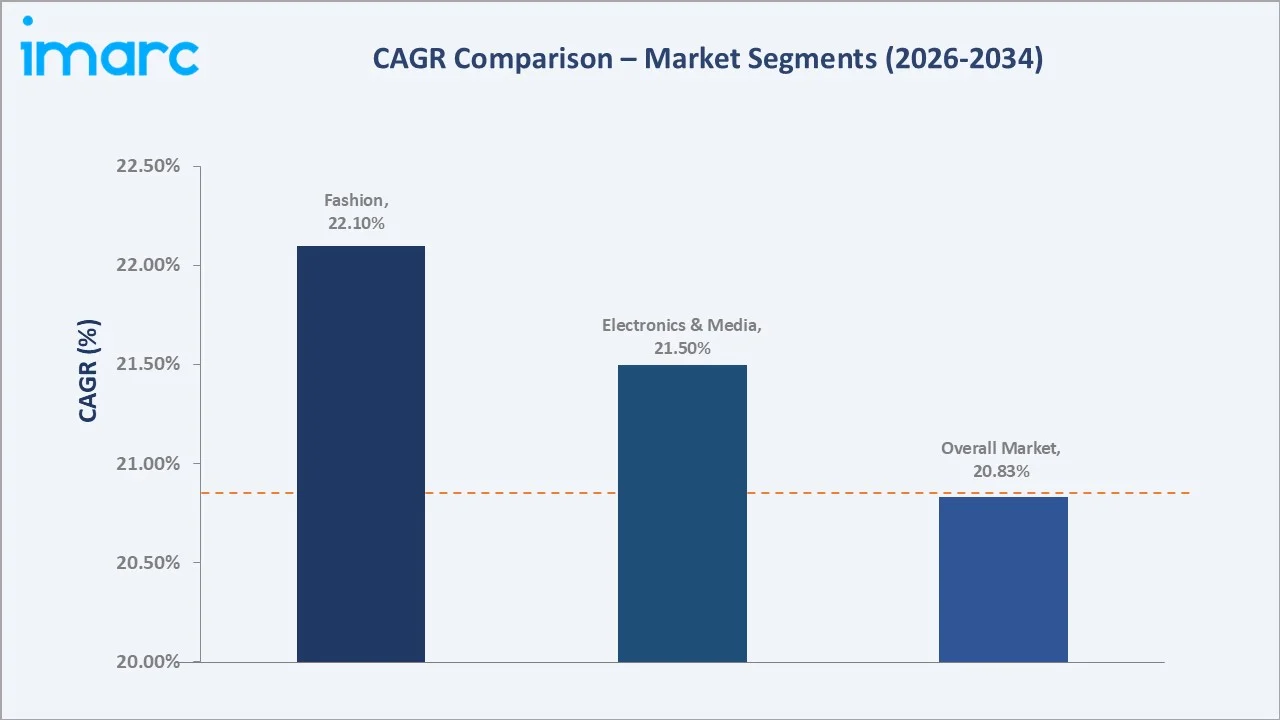

Fashion – ~22.1% CAGR (2026-2034) |

|

Second Largest Product |

Electronics and Media – 24.6% share (2025) |

|

Leading Region |

North India – 30.9% share (2025) |

|

Top Companies |

Amazon.com, Inc., Walmart, Meesho, Shopify Inc. |

Key Analytical Observations Supporting The Above Data:

- Fashion accounts for 31.8% of the India drop shipping market in 2025. This dominance reflects the category's high SKU variety, rapid trend cycles, and the social media-driven discovery model that makes fashion the most natural fit for influencer-led drop shipping reseller channels.

- Electronics and media’s 24.6% share (2025) reflects consistent and growing consumer demand for gadgets, mobile accessories, and electronics at competitive price points, where price-conscious Indian buyers actively seek online-only deals fulfilled through drop shipping models.

- Furniture and appliances at 18.9% (2025) are growing as home improvement demand rises and logistics infrastructure increasingly handles bulkier items, enabling merchants to drop ship home goods without warehousing overhead.

- North India's 30.9% share (2025) reflects Delhi-NCR's status as the primary digital commerce hub, with the highest concentration of e-commerce-active consumers, established logistics corridors, and a large base of online micro-entrepreneurs adopting drop shipping as a business model.

India Drop Shipping Market Overview

Drop shipping in India is a fulfilment model where online retailers sell products without holding inventory, relying on suppliers or manufacturers to ship directly to end consumers. The India market encompasses domestic drop shipping networks, cross-border drop shipping from international suppliers, and social commerce-driven models where individual resellers operate through WhatsApp, Instagram, and dedicated reseller platforms.

Macroeconomic drivers include India's e-commerce market projected to reach USD 325 Billion by 2030, internet penetration crossing 70% in 2025, and the government's Digital India program expanding broadband connectivity to Tier-2 and Tier-3 cities. The ONDC initiative is further reducing barriers for small merchants to participate in organized e-commerce, directly expanding the addressable merchant base for drop shipping platforms.

Market Dynamics

To evaluate market opportunities, Request Sample

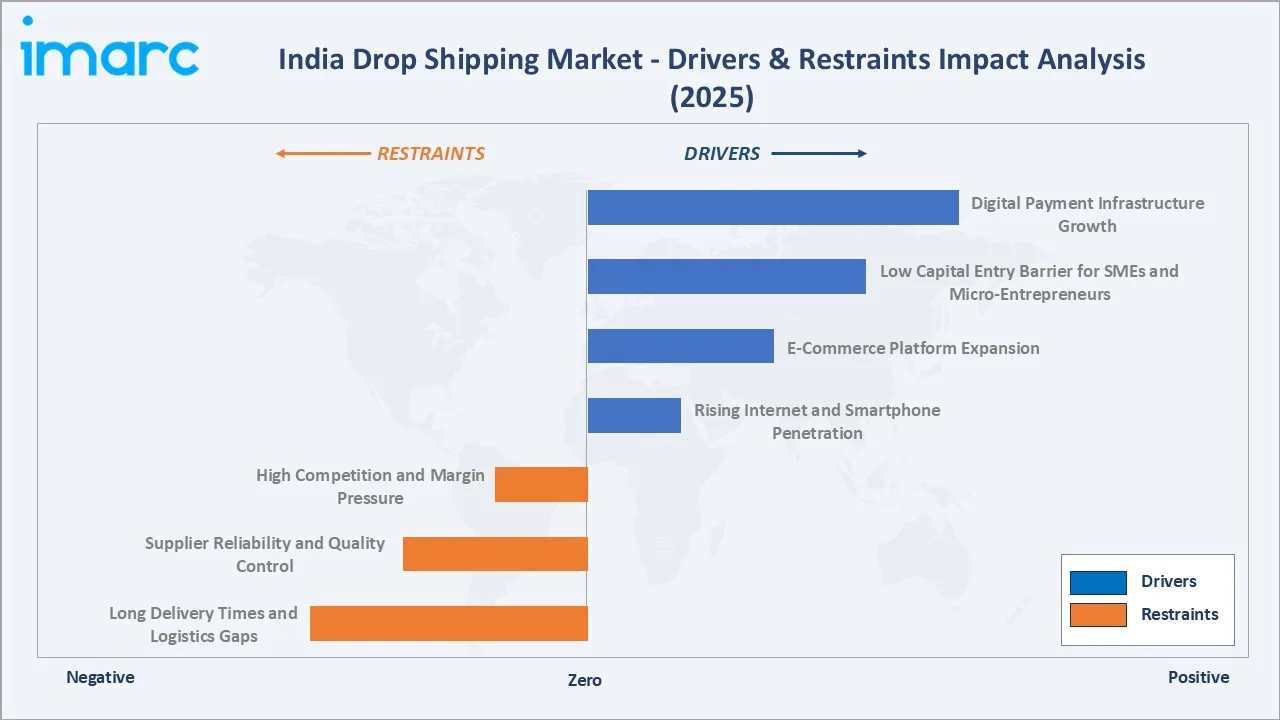

Market Drivers

- Rising Internet and Smartphone Penetration: According to the Internet in India Report 2025, Active Internet Users (AIU) in the country reached 958 Million in 2025, reflecting an approximate 8% year-on-year growth. This creates an ever-expanding addressable market for e-commerce consumption, directly translating to higher drop shipping order volumes across all product categories.

- E-Commerce Platform Expansion: The rapid growth of platforms, including Amazon, Flipkart, Meesho, and Shopify, has lowered the technical barriers for merchants to establish drop shipping businesses. Platform-native fulfilment and supplier matching tools reduce the expertise required to launch a viable drop shipping operation.

- Low Capital Entry Barrier for SMEs and Micro-Entrepreneurs: Drop shipping requires zero inventory investment, enabling India's large base of micro-entrepreneurs, homemakers, and first-generation business owners to enter online retail at negligible upfront cost. This structural advantage is a primary driver of market participant growth.

- Digital Payment Infrastructure Growth: Monthly prepaid payment instrument (PPI) transaction volumes rose from 4,640 lakh in November 2019 to about 8,750 lakh by March 2026. Along with this, the widespread adoption of digital payment methods has reduced transaction friction for both merchants and consumers, enabling seamless online purchase and supplier payment flows critical to the drop shipping model.

Market Restraints

- Long Delivery Times and Logistics Gaps: Drop shipping orders, particularly those sourced from cross-border suppliers, face delivery times of 7–21 days, well above consumer expectations established by marketplace leaders. This mismatch limits customer satisfaction and repeat purchase rates for drop shipping merchants.

- Supplier Reliability and Quality Control: Drop shipping merchants have limited control over product quality, packaging, and fulfilment accuracy. Supplier-side failures directly damage the merchant's brand reputation with customers, creating a structural risk that constrains adoption in quality-sensitive categories.

- High Competition and Margin Pressure: The low entry barrier of drop shipping creates intense competition, particularly in high-demand categories like fashion and electronics. Price competition between merchants selling identical products compresses margins, making profitability difficult for smaller operators without differentiated positioning.

Market Opportunities

- Tier-2 and Tier-3 City E-Commerce Expansion: India's rural regions now represent over 57% of the country’s AIUs and are expanding at nearly four times the growth rate of urban India. Furthermore, rural regions are demonstrating higher e-commerce growth rates than metro markets. Drop shipping platforms can capture this growth by enabling local micro-entrepreneurs to serve these markets with relevant product assortments.

- Social Commerce and Influencer-Driven Reselling: India's social commerce market, projected to reach USD 54.4 Billion by 2034, is creating a natural distribution channel for drop shipping. Influencers can operate as effective drop shipping resellers, combining content creation with automated supplier fulfilment.

- ONDC Integration and Government Digital Commerce Push: The Open Network for Digital Commerce is enabling small merchants to access multiple e-commerce platforms through a single integration. Drop shipping platforms integrating with ONDC can reach India's largest addressable merchant base at significantly lower acquisition costs.

Market Challenges

- Customs Duties and Cross-Border Regulatory Complexity: Cross-border drop shipping faces increasing regulatory scrutiny, including customs duties, GST compliance for imports, and import valuation rules. Policy uncertainty on cross-border e-commerce thresholds creates compliance risk for merchants sourcing internationally.

- Return Logistics and Reverse Fulfilment Costs: India's e-commerce return rates of 28–35% in fashion and 8-12% in electronics impose significant reverse logistics costs on drop shipping merchants who must manage returns without holding inventory, eroding profitability in high-return categories.

Emerging Market Trends

1. Social Commerce Integration with Drop Shipping

The integration of drop shipping fulfilment with social commerce channels, including Instagram Shopping, WhatsApp Business, and YouTube, is creating a new category of content-creator resellers. Platforms enabling direct supplier-to-consumer fulfilment through social media storefronts are growing at 25–30% annually, with fashion and beauty categories leading adoption among India's influencer community.

2. AI-Driven Product Discovery and Supplier Matching

Drop shipping platforms are increasingly deploying AI-powered tools for automated supplier matching, price optimization, and demand forecasting. These tools reduce the manual effort required to identify winning products and reliable suppliers, lowering the expertise barrier for new merchants and enabling existing operators to scale their catalogues efficiently across multiple niches.

3. ONDC-Enabled Open Commerce Access

The government's Open Network for Digital Commerce is enabling drop shipping merchants to access India's entire e-commerce buyer base through a single seller integration. This is democratizing access to large platform audiences previously available only through marketplace partnerships, accelerating the growth of independent drop shipping storefronts beyond the dominant marketplace ecosystem.

4. Domestic Supplier Network Expansion

India's growing domestic manufacturing and supplier base, particularly in fashion, home goods, and personal care, is reducing dependence on cross-border suppliers. Domestic drop shipping networks offer faster delivery times (1–3 days versus 7–21 days for imports), higher quality control, and simpler regulatory compliance, making them increasingly competitive with international supply chains.

Industry Value Chain Analysis

India's drop shipping value chain spans supplier networks through end-consumer fulfilment, with each stage occupied by specialized technology platforms, logistics providers, and marketing service operators. Supplier aggregator platforms and e-commerce enablers dominate the middle tier, while last-mile logistics providers and digital payment processors form the essential fulfilment infrastructure.

|

Stage |

Key Players / Examples |

|

Suppliers & Manufacturers |

Domestic and international product manufacturers, wholesalers, and third-party inventory holders |

|

Drop Shipping Platforms |

Technology-enabled platforms connecting retailers to suppliers, automating order routing, and providing catalogue management tools |

|

E-Commerce Retailers & Resellers |

Online storefronts, individual resellers, and SME merchants listing products without holding physical inventory |

|

Payment & Logistics Providers |

Digital payment processors, last-mile delivery partners, reverse logistics operators, and courier aggregators |

|

Marketing & Customer Acquisition |

Digital marketing agencies, social media platforms, influencer networks, and search engine optimization services |

|

End Consumers |

Urban and semi-urban online shoppers, SME businesses sourcing products, and Tier-2/3 city first-time e-commerce buyers |

Technology Landscape in the India Drop Shipping Industry

E-Commerce Platform Integration and APIs

Drop shipping in India is increasingly enabled by API-driven integrations between supplier catalogues, e-commerce storefronts, and marketplace platforms (Amazon, Flipkart). These integrations automate order routing, inventory synchronization, and tracking updates, enabling merchants to manage multi-supplier operations at scale without manual intervention.

Automation and AI-Powered Operations

AI-driven tools for product research, pricing optimization, and supplier vetting are transforming drop shipping operations. Automated repricing tools, demand prediction algorithms, and AI-generated product listings reduce the operational overhead per product, enabling merchants to profitably operate large catalogues across multiple niches and supplier networks.

Logistics Technology and Last-Mile Innovation

Courier aggregators provide drop shipping merchants with single-API access to multiple delivery partners, enabling competitive shipping rate selection and automated fulfilment. Emerging quick-commerce models and hyperlocal drop shipping networks are extending the model's applicability to time-sensitive product categories and perishable goods.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Fashion |

31.8% |

2025 |

|

Region |

North India |

30.9% |

2025 |

By Product

The fashion segment leads with a 31.8% share in 2025, valued at approximately USD 4.21 Billion. This dominance reflects fashion's natural compatibility with the drop shipping model, high SKU diversity, rapid trend cycles, social media-driven discovery, and low per-unit values that make individual order fulfilment economically viable. Fashion drop shipping is particularly prevalent on social commerce platforms and reseller networks targeting India's aspirational consumer base.

To access detailed market analysis, Request Sample

Electronics and media represents 24.6% of the market in 2025 (approximately USD 3.26 Billion), driven by consistent consumer demand for mobile accessories, gadgets, and audio equipment at online-competitive prices. Furniture and appliances at 18.9% are one of the fast-growing segments as logistics infrastructure increasingly accommodates bulkier items. Toys, hobby and DIY at 14.7% benefits from the gifting season demand peaks. The food and personal care segment, at 10.0% share, is constrained by shelf-life logistics complexity that limits drop shipping compatibility.

Regional Market Insights

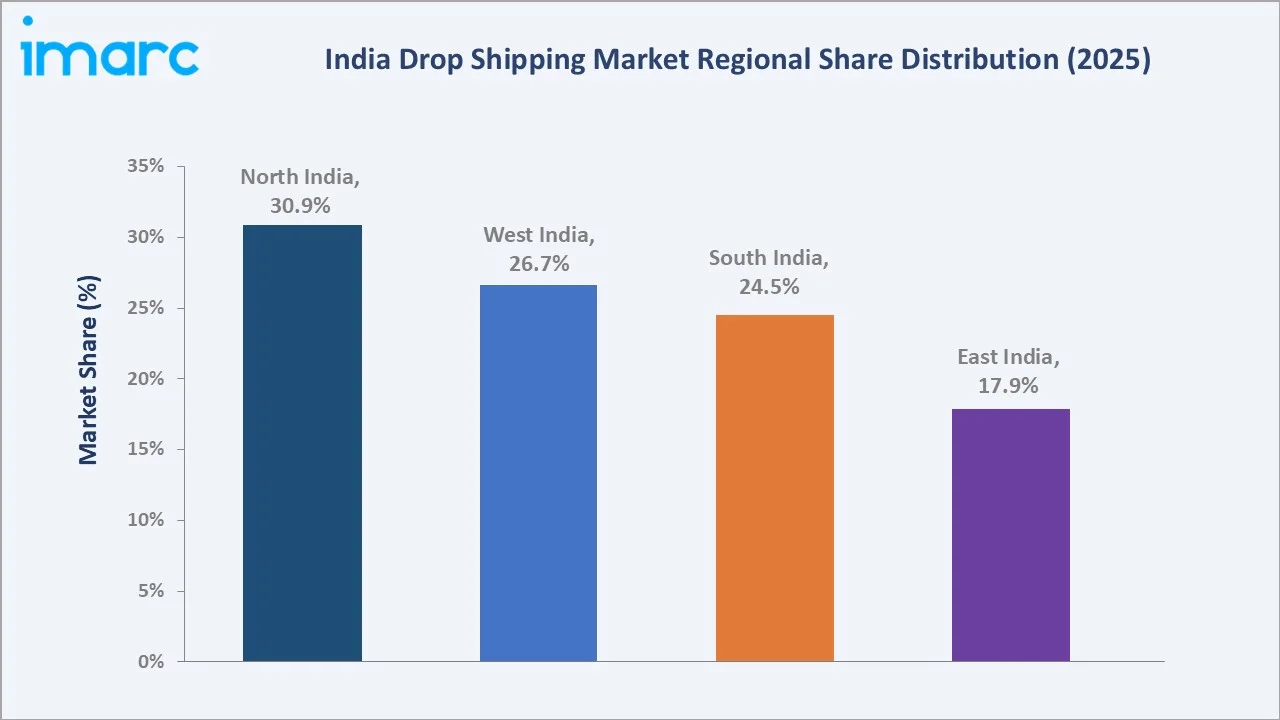

North India's market leadership (30.9%, 2025) reflects Delhi-NCR's status as India's primary digital commerce hub, with the highest density of e-commerce-active consumers, established logistics corridors, and a large base of online micro-entrepreneurs actively adopting drop shipping as a primary or supplementary income model.

West India at 26.7% is driven by Mumbai's established e-commerce ecosystem and Gujarat's strong entrepreneurial culture, with Surat and Ahmedabad emerging as significant fashion and textile drop shipping supplier hubs.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

30.9% |

Large urban consumer base, well-developed e-commerce infrastructure, high digital payment adoption, and strong demand across fashion and electronics categories |

|

West India |

26.7% |

Growing entrepreneurial ecosystem, rising SME adoption of online retail models, increasing smartphone penetration, and expanding logistics network |

|

South India |

24.5% |

High technology literacy among urban consumers, strong digital payment adoption, growing demand for niche and lifestyle products, and expanding last-mile delivery coverage |

|

East India |

17.9% |

Rising internet penetration in Tier-2 and Tier-3 cities, increasing e-commerce awareness, growing aspirational consumer base, and government digital inclusion initiatives |

South India, at 24.5%, is driven by high technology literacy in Bengaluru, Hyderabad, and Chennai. East India at 17.9% represents the market's emerging growth frontier, with rising internet penetration across West Bengal and Odisha creating new consumer demand and reseller adoption.

Competitive Landscape

India's drop shipping market exhibits moderate concentration, with large e-commerce marketplaces and platform enablers holding significant influence over merchant access to consumers and suppliers. The top four players collectively account for the majority of organized drop shipping transaction volumes in 2025.

|

Company Name |

Brand Names |

Market Position |

Core Strength |

|

Amazon.com, Inc. |

Amazon, Fulfilment by Amazon |

Market Leader |

Extensive supplier network, robust logistics infrastructure, and broad product catalogue coverage |

|

Walmart |

Flipkart, Myntra |

Market Leader |

Deep India-market penetration, strong fashion and electronics reach, and extensive Tier-2 city presence |

|

Meesho |

Meesho |

Strong Challenger |

Social commerce model and strong Tier-2/3 city reseller network |

|

Shopify Inc. |

Shopify |

Strong Challenger |

Self-hosted store capabilities, app ecosystem integration, and growing SME merchant adoption |

Large marketplace platforms dominate consumer-facing drop shipping by providing built-in fulfilment infrastructure, buyer trust, and traffic. Independent enablers, including Shopify, serve merchants seeking to build branded storefronts outside marketplace ecosystems.

Key Company Profiles

Amazon.com, Inc.

Amazon.com, Inc. is one of the market leaders in India's organized e-commerce and drop shipping ecosystem. Its Fulfillment by Amazon (FBA) and third-party seller programs enable tens of thousands of drop shipping merchants to list and fulfil products across India's broadest addressable consumer base.

- Product Portfolio: Multi-category marketplace spanning fashion, electronics, home goods, toys, personal care, and digital products, with seller-specific drop shipping fulfilment integrations.

- Recent Developments: In June 2026, Amazon.com, Inc. launched a 24/7 AI-powered Seller Assistant for 1.7 million Indian merchants to improve catalogue creation, inventory planning, onboarding, and advertising. The tool aims to cut operational effort by nearly 70% and support Amazon’s goal of impacting 15 million businesses by 2030.

- Strategic Focus: Expanding seller services for drop shipping merchants; deepening Tier-2 and Tier-3 market penetration; integrating AI-powered product listing and pricing tools for SME sellers.

Walmart

Walmart operates in India through its majority-owned subsidiary Flipkart Group, which includes Flipkart and Myntra. It provides a comprehensive drop shipping infrastructure across multiple consumer segments and price tiers.

- Product Portfolio: Fashion, electronics, home goods, grocery, and general merchandise across Flipkart marketplace; fashion-specific drop shipping via Myntra.

- Strategic Focus: Social commerce-enabled drop shipping through Shopsy; Tier-2 market reseller network expansion; fashion drop shipping leadership through Myntra supplier integration.

Market Concentration Analysis

India's drop shipping market exhibits moderate concentration, with large marketplace platforms holding significant transaction volume shares while a long tail of independent aggregators, domestic supplier platforms, and cross-border tools serves specialized merchant segments. The top four platforms collectively account for approximately 55–65% of organized drop shipping transaction volumes in 2025.

Consolidation is occurring through platform acquisitions and vertical integration. Flipkart's control of Myntra and the emergence of Meesho as a dominant social commerce drop shipping platform represent the primary consolidation vectors. The ONDC initiative is a counter-consolidation force, enabling smaller independent merchants to access multiple marketplace audiences through a single seller integration.

Investment & Growth Opportunities

Fastest Growing Segments

Social commerce-enabled drop shipping (~25–30% CAGR), tier-2 and tier-3 city reseller platforms (~22% CAGR), and AI-powered supplier matching tools (~28% growth) represent the highest-growth investment vectors through 2034. The domestic supplier aggregation segment is also growing above market rates as merchants shift from cross-border to domestic fulfilment for improved delivery times and reduced regulatory complexity.

Emerging Market Expansion

East India and rural tier-3 markets collectively represent a significant incremental drop shipping opportunity through 2034, as internet penetration deepens and first-time online buyers enter the market. Entry strategies include vernacular-language interfaces, regional supplier partnerships, and community-based reseller training programs enabling local micro-entrepreneurs to participate in organized drop shipping networks.

Venture and Institutional Investment Trends

- India's e-commerce market is projected to reach USD 325 Billion by 2030, directly expanding the transaction volume addressable by drop shipping platforms and creating significant revenue opportunities for both supplier aggregators and merchant enablement tools.

- Meesho's valuation trajectory is attracting venture and growth equity investment into social commerce-enabled drop shipping platforms targeting India's micro-entrepreneur demographic.

- ONDC adoption is creating investment opportunities in drop shipping middleware platforms that aggregate supplier catalogues and provide multi-channel order management, enabling merchants to serve ONDC, marketplace, and direct-to-consumer channels through unified operations.

Future Market Outlook (2026-2034)

India's drop shipping market is positioned for sustained high-growth expansion through 2034. From USD 13.24 Billion in 2025, the market is projected to reach USD 76.23 Billion by 2034, representing total incremental value creation of USD 62.99 Billion at a CAGR of 20.83%. This growth is structurally supported by India's e-commerce consumption base expanding toward 440 million online shoppers by 2030 and the continuing democratization of digital entrepreneurship.

Technology will increasingly define competitive differentiation. AI-driven product discovery, automated supplier vetting, predictive inventory tools, and integrated social commerce fulfilment will separate leading platforms from commodity drop shipping aggregators. Domestic supplier network quality and delivery speed will be key battlegrounds, with platforms delivering reliably within 24–48 hours commanding premium merchant loyalty and consumer satisfaction.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants in 2024–2025, including drop shipping platform operators, e-commerce merchants, logistics providers, supplier aggregators, and digital payment infrastructure executives across India's Tier-1 and Tier-2 markets. Expert input validated market sizing, segment growth rates, and regional penetration estimates.

Secondary Research

Secondary research encompassed platform annual reports and investor disclosures, NASSCOM e-commerce market reports, Ministry of Commerce digital trade data, TRAI internet subscriber statistics, India Brand Equity Foundation e-commerce surveys, and industry publications including YourStory, Inc42, and Economic Times e-commerce coverage.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating e-commerce GMV growth projections, drop shipping penetration rate modelling, active merchant count estimates, and average order value benchmarks. The base-case CAGR of 20.83% reflects consensus estimates validated against platform transaction growth disclosures and India's internet commerce expansion trajectory for 2026–2034.

India Drop Shipping Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Toys, Hobby and DIY, Furniture and Appliances, Food and Personal Care, Electronics and Media, Fashion |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Amazon.com, Inc., Walmart, Meesho, Shopify Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India drop shipping market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India drop shipping market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India drop shipping industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Drop Shipping Market Report

The India drop shipping market reached USD 13.24 Billion in 2025 and is projected to reach USD 76.23 Billion by 2034.

The market is expected to grow at a CAGR of 20.83% during 2026-2034, driven by rising internet penetration, e-commerce platform expansion, and increasing SME adoption of zero-inventory business models.

North India leads with a 30.9% share in 2025, anchored by Delhi-NCR's digital commerce hub status, established logistics corridors, and the highest concentration of e-commerce-active consumers and micro-entrepreneurs.

Fashion dominates with a 31.8% share in 2025, driven by high SKU diversity, rapid trend cycles, and social media-driven discovery that makes fashion the most natural fit for influencer-led reseller channels.

Some of the key players include Amazon.com, Inc., Walmart, Meesho, and Shopify Inc.

Key drivers include rising internet and smartphone penetration, e-commerce platform expansion, low capital entry barriers, and UPI-driven digital payment adoption.

Some of the key challenges include long cross-border delivery times, supplier reliability and quality control risks, intense price competition compressing merchant margins, and regulatory complexity around cross-border e-commerce imports.

Fastest-growing opportunities include social commerce-enabled drop shipping platforms, domestic supplier aggregation networks, AI-powered merchant tools, and Tier-2/3 city reseller community platforms growing at 22%+ CAGR.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)