India Electric Vehicle Charging Station Market Size, Share, Trends and Forecast by Charging Station Type, Vehicle Type, Installation Type, Charging Level, Connector Type, Application, and Region, 2026-2034

India Electric Vehicle Charging Station Market Size, Share, Trends & Forecast (2026-2034)

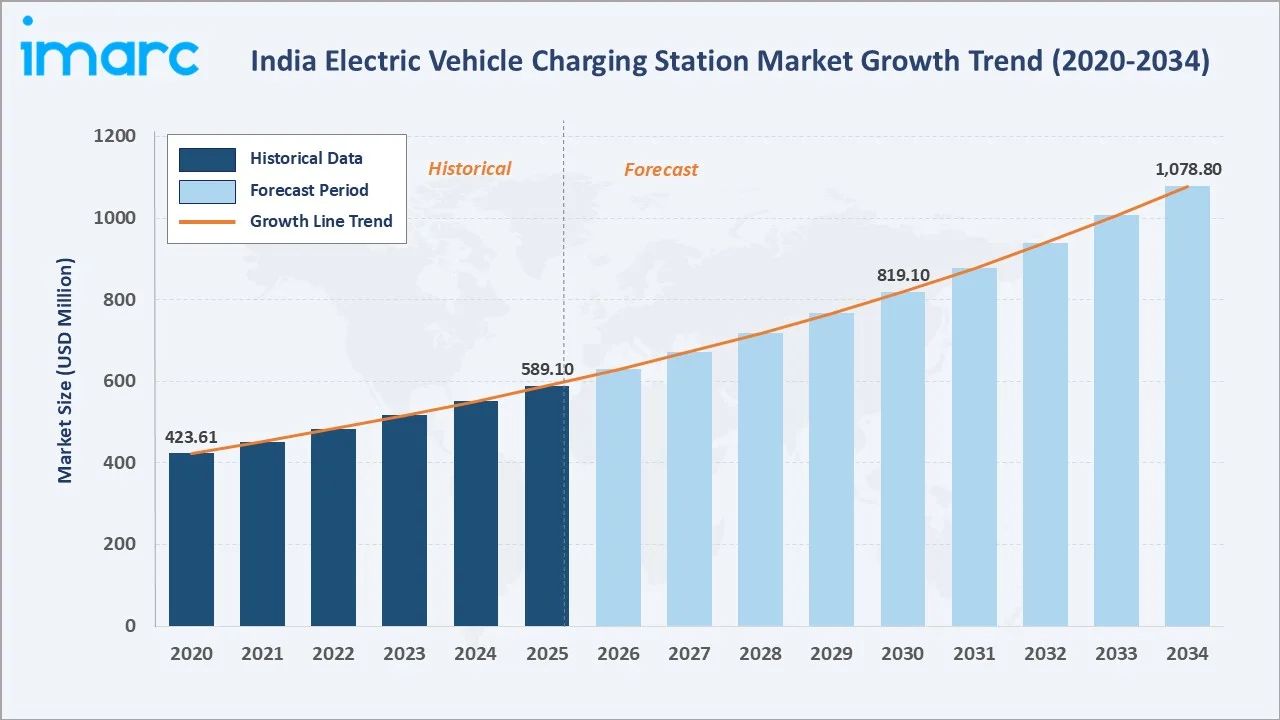

The India electric vehicle charging station market size was valued at USD 589.1 Million in 2025 and is projected to reach USD 1,078.8 Million by 2034, exhibiting a CAGR of 6.82% during 2026-2034. The market is driven by the rapid proliferation of electric vehicles across two-wheelers, three-wheelers, and passenger segments, underpinned by policy frameworks such as FAME II and PM e-DRIVE. Government mandates for public charging infrastructure, declining EVSE hardware costs, and aggressive fleet electrification by logistics and ride-hailing operators are reinforcing demand. Commercial applications command a dominant 79.2% share in 2025, while Level 3 leads at 58.7% of charging level by market value. North India holds the largest regional share at 33.8%, anchored by Delhi-NCR's high EV penetration and active policy environment.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 589.1 Million |

|

Forecast Market Size (2034) |

USD 1,078.8 Million |

|

CAGR (2026-2034) |

6.82% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (33.8% share, 2025) |

|

Fastest Growing Region |

East India (CAGR, 8.9%) |

|

Leading Application |

Commercial (79.2%, 2025) |

|

Leading Charging Level |

Level 3 (58.7%, 2025) |

The India electric vehicle charging station market growth trajectory from 2020 through 2034, contrasting consistent historical expansion base against a sustained forecast curve, is presented in Figure 1. The historical CAGR (2020–2025) reflects the initial infrastructure build-out phase, with the forecast period accelerating as highway corridor and fleet depot deployments scale.

To get more information on this market, Request Sample

Figure 2 below presents segment and region-level CAGR comparisons, highlighting Level 3 and East India as the two fastest-growing sub-categories within the India EV charging station market during the forecast period 2026–2034.

Executive Summary

The India electric vehicle charging station market is at a structural inflection point. The market grew from USD 423.6 Million in 2020 to USD 589.1 Million in 2025, representing a compound expansion driven by EV sales acceleration, government infrastructure mandates, and rising private sector participation.

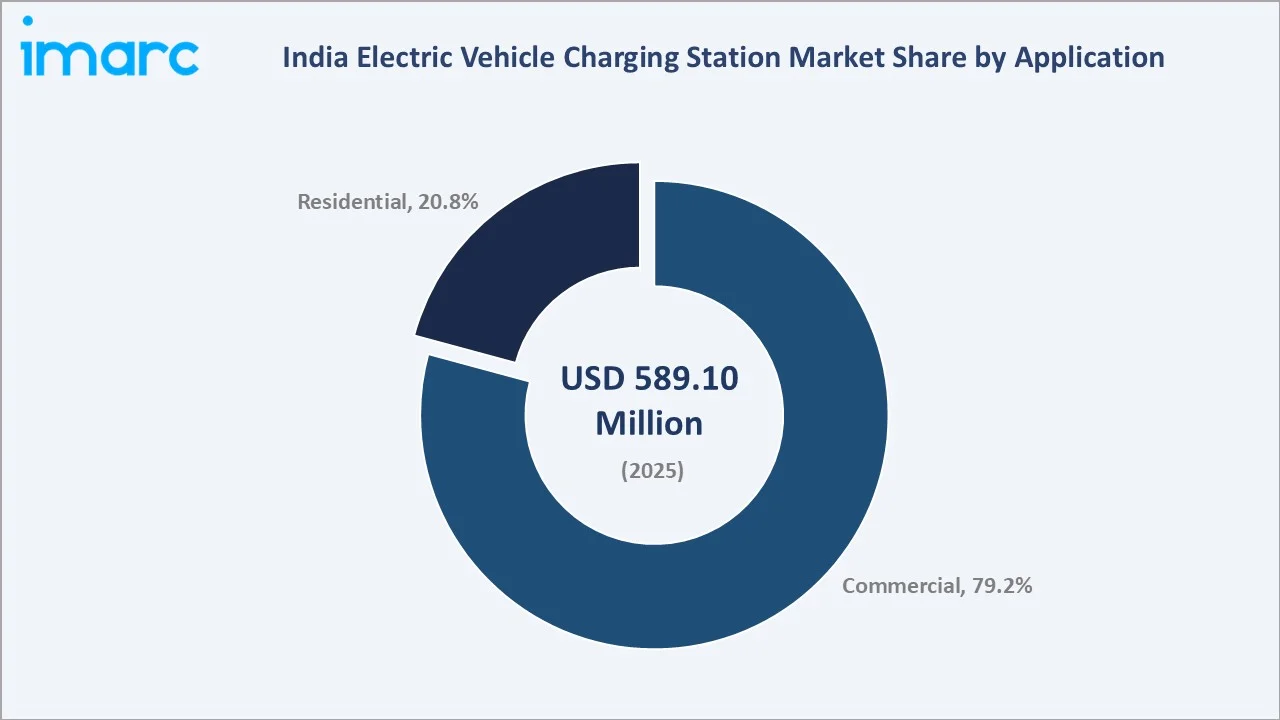

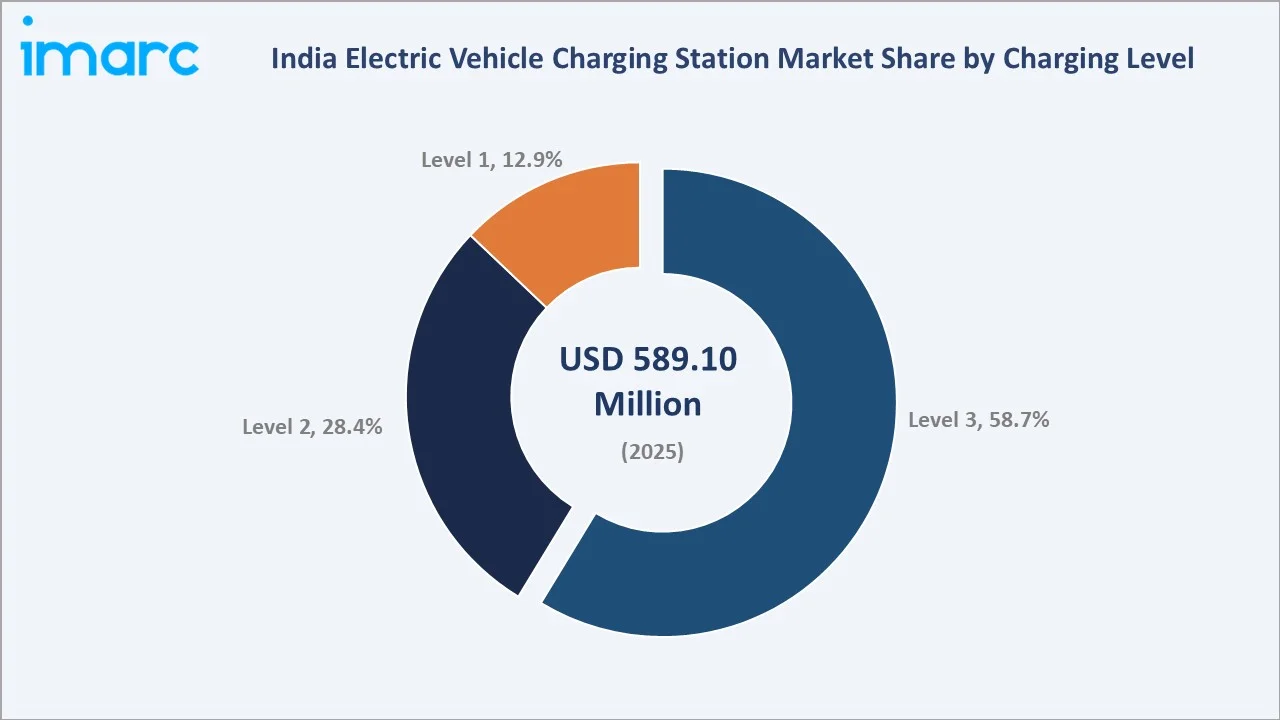

Commercial applications command a 79.2% majority market share in 2025, underpinned by fleet electrification commitments from logistics majors, e-commerce delivery operators, and cab aggregators. Residential charging at 20.8% is growing structurally as apartment developers integrate EV-ready infrastructure under RERA green-building norms. Level 3 leads at 58.7% of charging level by market value, driven by expressway corridor deployment and fuel retail network integration. Level 2 hold 28.4%, anchored by workplace and mall deployments. Level 1 at 12.9% serves the residential and semi-urban segment.

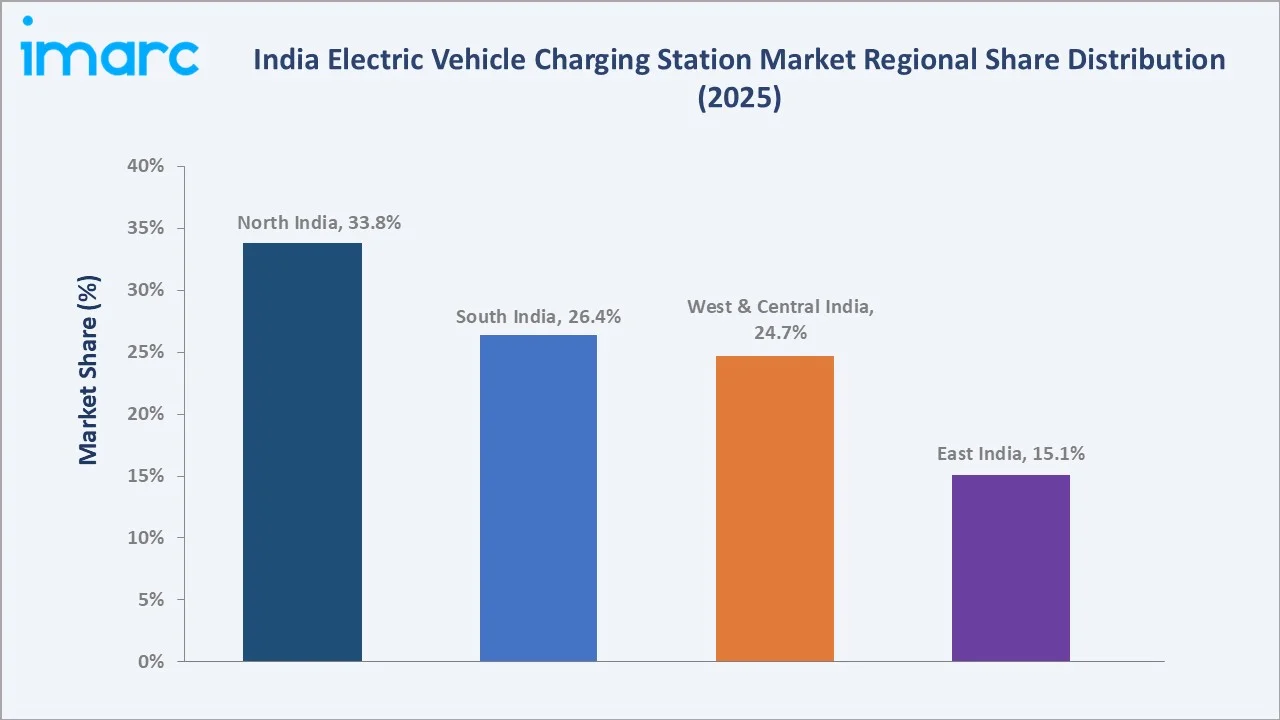

North India leads with a 33.8% regional share in 2025, anchored by Delhi-NCR's active EV policy environment and high EV concentration. South India follows at 26.4% with Bengaluru, Hyderabad, and Chennai as primary drivers. West and Central India holds 24.7%, supported by Maharashtra's industrial EV adoption and Gujarat's SEZ-based charging buildout. East India, at 15.1%, is the fastest-growing frontier, benefiting from state EV policy incentives in West Bengal and Odisha, combined with low base penetration.

Key Market Insights

|

Insight |

Data |

|

Largest Application Segment |

Commercial – 79.2% share (2025) |

|

Dominant Charging Level |

Level 3 – 58.7% share (2025) |

|

Leading Region |

North India – 33.8% revenue share (2025) |

|

Fastest Growing Region |

East India – above-market CAGR (2026-2034) |

|

Top Companies |

Tata Power, Tecso Charge Zone Limited, Sharify Services Pvt. Ltd., Fortum, and Kazam EV Tech Pvt. Ltd. |

Key Analytical Observations Supporting the Above Data:

- Commercial charging's 79.2% dominance in 2025 reflects fleet-first electrification by logistics majors – Zomato and Swiggy deployed 1 Lakh+ electric delivery vehicles requiring commercial hub charging in FY2025.

- Level 3 leads at 58.7% by market value due to high per-unit EVSE cost (INR 15–25 Lakh), not unit count – Level 2 remains the plurality in installed charger numbers at ~45% of all stations.

- North India's 33.8% leadership is anchored by Delhi-NCR, where registered EV penetration crossed 7% in 2024 – the highest of any Indian metro zone.

- East India's fastest-growing trajectory is underpinned by West Bengal's 100% road tax exemption on EVs and Odisha's industrial EV policy, creating above-market CAGR conditions through 2030.

- Residential charging at 20.8% is growing as RERA 2024 guidelines mandate EV-ready provisions in new housing developments above 50 units in Maharashtra and Delhi.

India Electric Vehicle Charging Station Market Overview

Electric vehicle (EV) charging infrastructure in India includes public stations, private depots, workplace chargers, and home wall-boxes that supply electricity to EVs across two-wheelers, three-wheelers, passenger vehicles, buses, and trucks. The ecosystem spans hardware (EVSE, connectors, meters), software (CPMS, interoperability, billing), and services (installation, O&M).

Deployment is currently concentrated in urban centers and highway corridors, aligned with demand density and utilization. Growth is driven by national EV adoption targets, improving battery economics, and policy support for domestic manufacturing. Rising electric two- and three-wheeler penetration is a key demand driver, accelerating the need for widespread, accessible charging infrastructure. The value chain spans power supply and grid integration, charging point operators, and end users.

Market Dynamics

To evaluate market opportunities, Request Sample

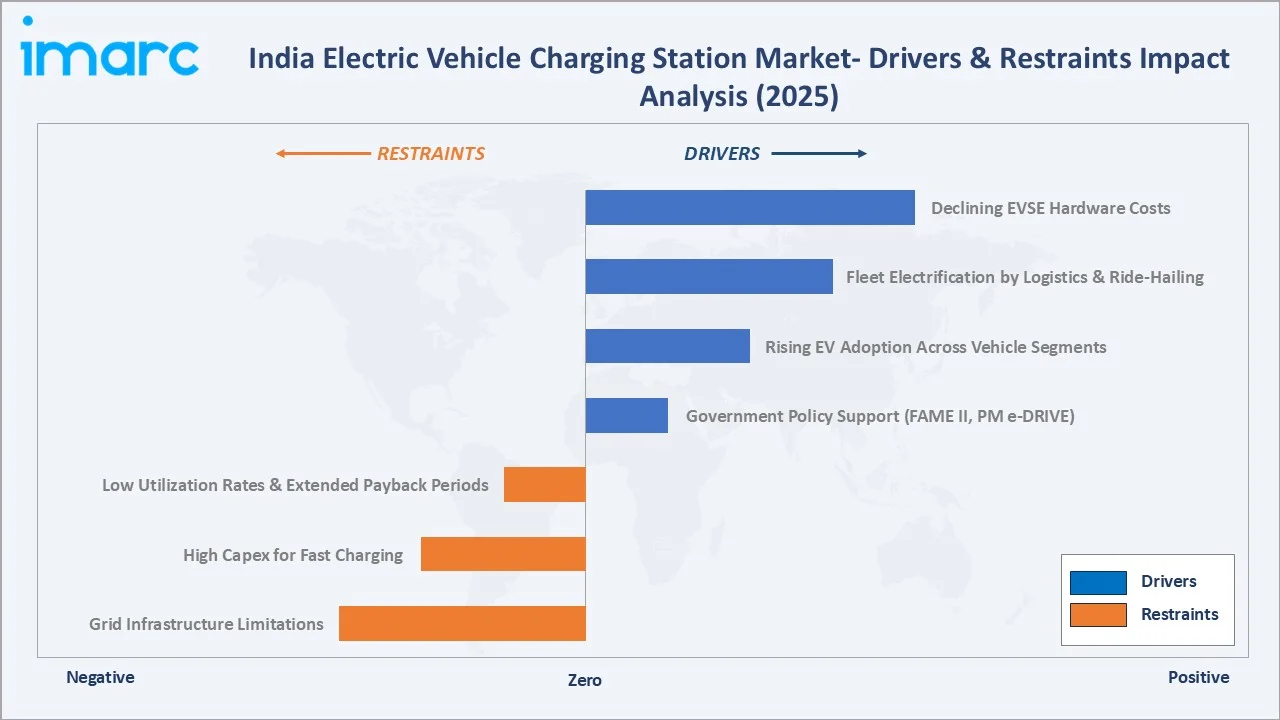

Market Drivers

- Government Policy Support: Schemes such as FAME II and PM e-DRIVE have accelerated charging infrastructure rollout through capital subsidies, public charging targets, and incentives for ecosystem participants, directly supporting CPO expansion and EVSE deployment.

- Rising EV Adoption: Strong growth in electric two- and three-wheelers, along with increasing penetration of passenger EVs, is structurally expanding charging demand across residential, commercial, and public networks.

- Fleet Electrification: Logistics, e-commerce, and ride-hailing operators (e.g., Ola Electric, BluSmart, Zomato, Swiggy) are transitioning to EV fleets, driving demand for depot-based and high-utilization charging infrastructure.

- Declining Hardware Costs: Localization and scale in EVSE manufacturing are reducing charger and installation costs, improving project viability, and accelerating network expansion.

Market Restraints

- Grid Infrastructure Limitations: Inconsistent power supply, limited transformer capacity, and elevated commercial tariffs in non-metro regions constrain reliable charger deployment and increase operating costs.

- High Capex for Fast Charging: DC fast chargers require significant upfront investment, limiting deployment primarily to well-capitalized operators and high-traffic locations.

Market Opportunities

- Highway Charging Expansion: Under-penetrated national highway networks present a significant opportunity for fast-charging deployment, supported by government mandates for corridor electrification.

- Renewable-Integrated Charging & V2G: Integration of solar-based charging and emerging vehicle-to-grid (V2G) models—being piloted by players like NTPC Limited and Tata Power—can reduce operating costs and unlock new revenue streams.

Market Challenges

- Low Utilization Rates: Early-stage demand results in low charger utilization, impacting standalone project economics and extending payback periods.

- Demand–Supply Mismatch in Tier 2/3 Cities: Limited charging visibility continues to hinder EV adoption in smaller cities, requiring proactive infrastructure deployment ahead of demand.

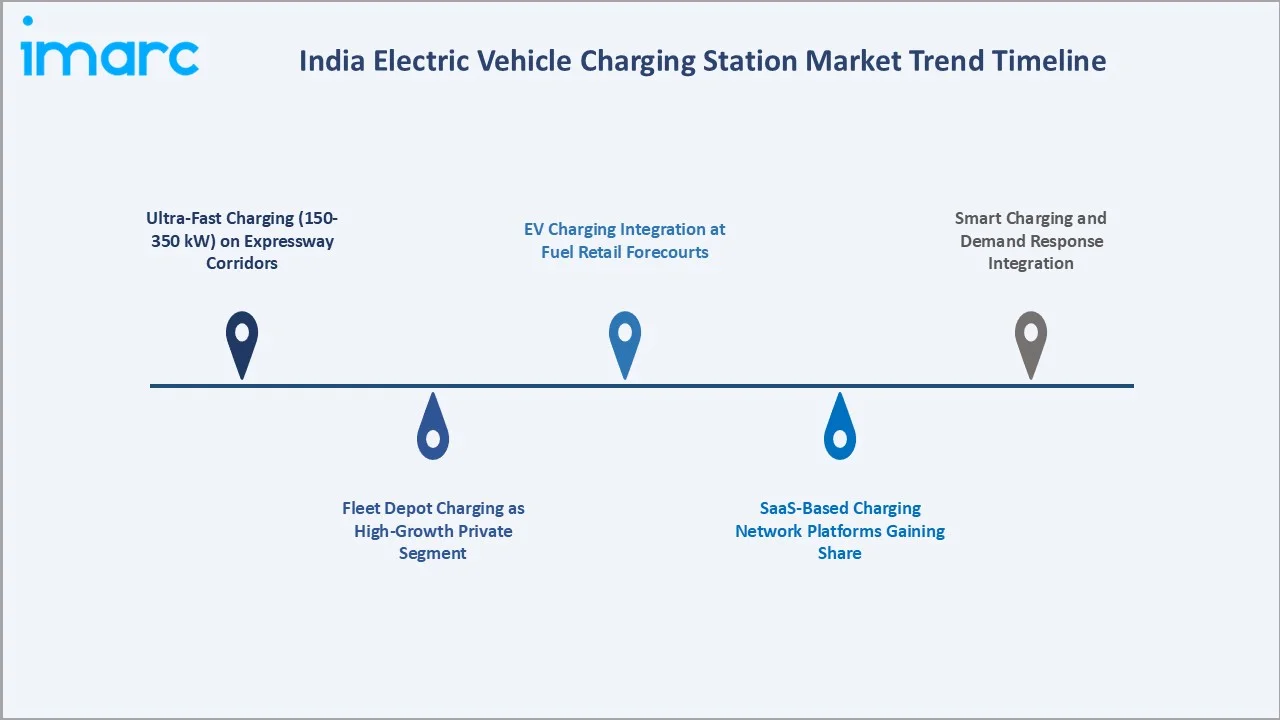

Emerging Market Trends

1. Ultra-Fast Charging (150–350 kW) Scaling on Expressway Corridors

Deployment of 150–350 kW chargers is accelerating along high-traffic corridors, led by players such as ChargeZone, NTPC Limited, and Fortum. These multi-port hubs are reducing charging time and enabling intercity EV travel, making expressways a priority deployment segment.

2. EV Charging Integration at Fuel Retail Forecourts

Oil marketing companies, including Indian Oil Corporation, Hindustan Petroleum Corporation Limited, and Bharat Petroleum Corporation Limited, are integrating EV chargers at existing fuel stations. Leveraging pre-built grid connectivity and land infrastructure enables faster, more capital-efficient rollout versus greenfield sites.

3. Smart Charging and Demand Response Integration

DISCOM-led pilots by BESCOM and Maharashtra State Electricity Distribution Company Limited are introducing Time-of-Use tariffs and load management systems. Smart charging is emerging as a key tool to shift EV demand to off-peak hours and support grid stability.

4. Fleet Depot Charging as a High-Growth Private Infrastructure Segment

Public transport and logistics fleets are driving captive charging infrastructure. Agencies such as BEST Mumbai, Delhi Transport Corporation, and Bangalore Metropolitan Transport Corporation, along with operators like Amazon and Delhivery, are prioritizing depot-based charging to ensure operational reliability and reduce dependence on public networks.

5. SaaS-Based Charging Network Platforms Gaining Share

CPOs such as Tata Power EZ Charge, Statiq, and Kazam are adopting SaaS-driven CPMS platforms. These enable interoperability, real-time monitoring, and subscription-based billing, with software emerging as a faster-growing layer of the value chain.

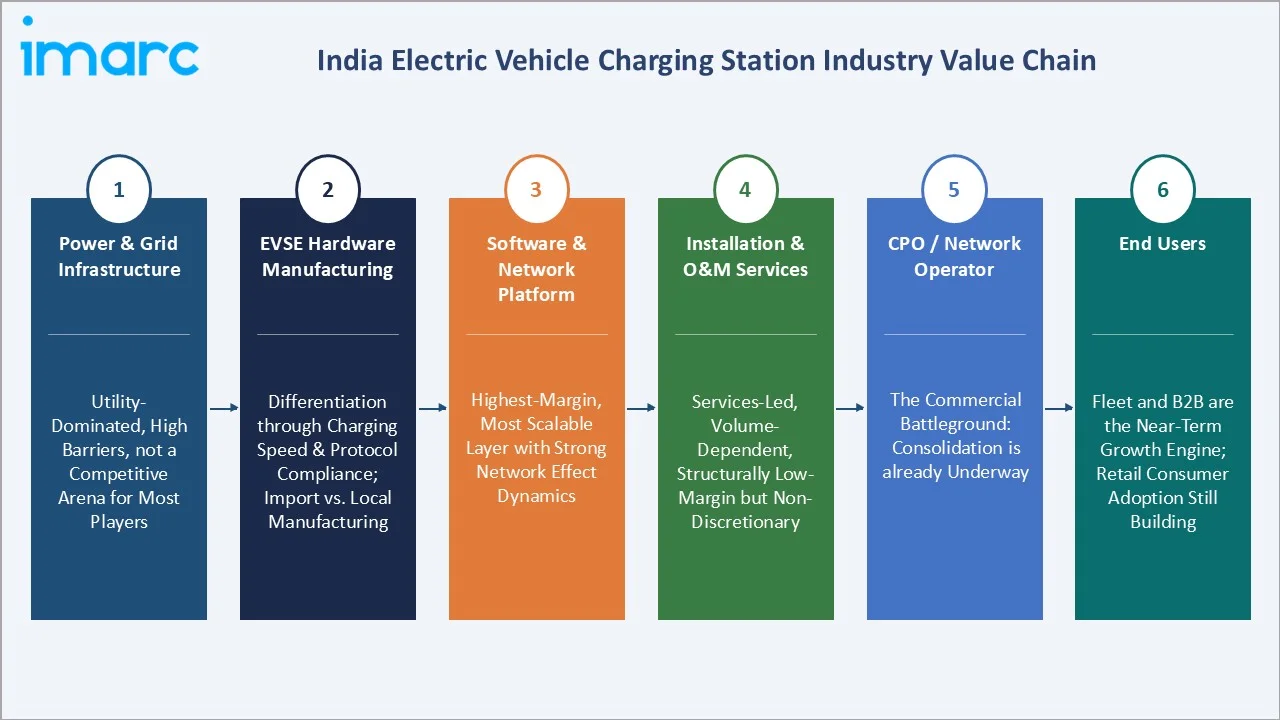

Industry Value Chain Analysis

The India EV charging station value chain spans six integrated stages from power supply through end-user engagement. Each stage represents distinct capital intensity, technology differentiation, and competitive dynamics for market participants.

|

Stage |

Key Players / Examples |

|

Power & Grid Infrastructure |

utility-dominated, high barriers, not a competitive arena for most players |

|

EVSE Hardware Manufacturing |

differentiation through charging speed and protocol compliance; import vs. local manufacturing is a live tension |

|

Software & Network Platform |

the highest-margin, most scalable layer with strong network effect dynamics |

|

Installation & O&M Services |

services-led, volume-dependent, structurally low-margin but non-discretionary |

|

CPO / Network Operator |

The commercial battleground: consolidation is already underway |

|

End Users |

fleet and B2B are the near-term growth engine; retail consumer adoption is still building |

Tier-1 EVSE manufacturers hold the highest technology differentiation in the value chain. Domestic players are capturing import substitution share under India's ALMM policy framework. Domestic manufacturing accounted for 44% of installed EVSE units in 2025, up from 28% in 2022 – a structural shift with margin implications for global EVSE suppliers.

The value chain diagram in Figure 6 illustrates the sequential flow from grid infrastructure through CPO operators to end users.

Technology Landscape in the India EV Charging Station Industry

Charging Hardware Standards: BIS IS 17017 and Bharat EV Charger Norms

India has adopted CCS Type 2 and CHAdeMO for DC fast charging and the Bharat EV Charger (BEV) standards for affordable domestic deployment. BIS updated IS 17017 norms in 2023, mandating minimum safety and interoperability requirements across all publicly accessible EVSE. Smart metering integration using AMI-compatible EVSE is now a procurement requirement under government tenders, ensuring remote diagnostics and tamper-proof billing.

OCPP 2.0.1 and Interoperability Mandates

OCPP 2.0.1 adoption is accelerating. Tata Power EZ Charge and ChargeZone migrated from OCPP 1.6 to 2.0.1 by 2025. The Ministry of Power's 2024 circular mandated OCPP compliance for all stations receiving government subsidy, covering 12,000+ stations. Open protocols reduce ecosystem fragmentation and improve consumer trust in public charging reliability.

Solar Integration and AI-Powered Load Management

Solar carport charging with behind-the-meter battery storage is gaining traction in high-irradiance states – Rajasthan, Gujarat, and Tamil Nadu. NTPC's solar charging hub in New Delhi generates 90% of its energy on-site at INR 2.80/unit. AI-driven CPMS platforms from Kazam and Chargegrid use ML models trained on traffic patterns and fleet schedules to reduce grid overage costs by 12–18%, as demonstrated in Bengaluru and Hyderabad pilots in 2024.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Charging Station Type |

DC Charging |

63.7% |

2025 |

|

Vehicle Type |

Battery Electric Vehicle (BEV) |

75.1% |

2025 |

|

Installation Typ |

Fixed Charger |

83.8% |

2025 |

|

Charging Level |

Level 3 |

58.7% |

2025 |

|

Connector Type |

Combines Charging Station (CCS) |

43.8% |

2025 |

|

Application |

Commercial |

79.2% |

2025 |

|

Region |

North India |

33.8% |

2025 |

By Application

To access detailed market analysis, Request Sample

Commercial charging dominance is underpinned by three structural forces: (1) fleet electrification commitments by logistics, ride-hailing, and delivery operators; (2) government mandates for EV charging at commercial complexes over 500 sq. meters effective from 2024; and (3) petrol station conversion programs by IOC and HPCL adding commercial EVSE at 5,000+ forecourts. Residential charging at 20.8% is gaining structural momentum, driven by premium housing developer mandates and RERA provisions requiring EV-ready parking in new developments above 50 units in major states.

By Charging Level

Level 3's 58.7% value dominance reflects high per-unit hardware cost, creating a value-weighted skew over unit-count distribution. By unit count, Level 2 represents approximately 45% of installed charger numbers. Level 2's 28.4% revenue share is anchored by workplace charging programs from IT majors in Bengaluru, Hyderabad, and Pune covering 300,000+ employees. Level 1's 12.9% share is structurally declining as EV battery capacities grow beyond practical Level 1 top-up efficiency, transitioning more residential consumers to Level 2 home wall-box installations.

Regional Market Insights

The India EV charging market exhibits significant regional variation driven by state-level EV policies, grid infrastructure quality, EV penetration rates, and urban density. The regional share distribution for 2025 is presented in Figure 9.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

33.8% |

Delhi-NCR EV density; Yamuna Expressway corridor; Delhi EV Policy 2020 |

|

South India |

26.4% |

Bengaluru IT campuses; Hyderabad logistics; Chennai OEM cluster; TN EV Policy |

|

West & Central India |

24.7% |

Maharashtra industrial EV; Gujarat SEZ charging; Pune two-wheeler OEM cluster |

|

East India |

15.1% |

Kolkata e-bus deployment; Odisha EV Policy; WB road tax exemption; low base advantage |

North India's 33.8% dominance is supported by Delhi-NCR's status as India's leading EV market, where DTC operated 1,500+ electric buses in 2025. South India's Bengaluru hosts over 60% of India's EV-tech startup ecosystem and leads in smart charging software innovation. West and Central India's 24.7% reflects manufacturing-driven demand from Gujarat's Surat-Ahmedabad corridor and Maharashtra's industrial clusters. East India, at 15.1%, represents the highest incremental growth potential through 2030, with state policy acceleration and low existing competition creating conditions for above-average CAGR.

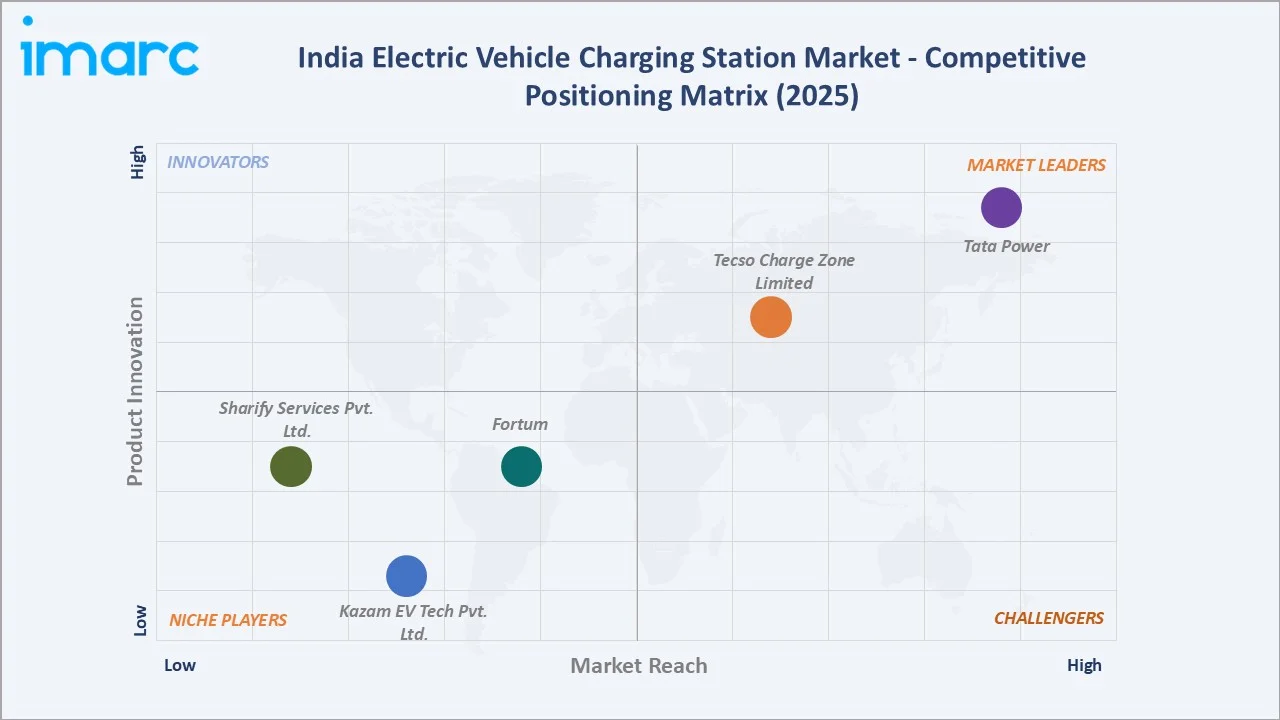

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Tata Power |

EZ Charge App |

Leader |

Widest public CPO network; multi-EV segment; OCPP 2.0.1 |

|

Tecso Charge Zone Limited |

ChargeZone |

Leader |

Highway fast charging leadership; Series C funded; pan-India |

|

Sharify Services Pvt. Ltd. |

Statiq: EV Charging Stations |

Emerging |

Urban smart charging; SaaS CPMS; enterprise workplace focus |

|

Fortum |

GLIDA |

Emerging |

European operator expertise; DC fast charging; Delhi-NCR focus |

|

Kazam EV Tech Pvt. Ltd. |

Kazam App |

Emerging |

AI-powered CPMS SaaS; white-label B2B charging management |

The India EV charging station competitive landscape is characterised by a mix of utility-backed incumbents, oil marketing company networks, and technology-led CPO startups. The market is less concentrated than global peers, with no single player holding above 20% network share. Tata Power, Tecso Charge Zone Limited, and Sharify Services Pvt. Ltd. represent the leading CPO platforms by installed station count and geographical coverage. BPCL, IOC, and HPCL are rapidly expanding through petrol station integration, leveraging existing real estate and grid access advantages.

Key Company Profiles

Tata Power

Tata Power’s EZ Charge is India's largest public EV charging network, operating over 4,500 public charging points across 500+ cities as of 2025. It is a subsidiary of Tata Power, one of India's leading integrated power companies.

- Platform & Network: EZ Charge App, AC & DC chargers, residential wall-box installations, fleet charging solutions.

- Recent Developments: In September 2024, Tata Power EZ Charge crossed 4,000 public charging points and signed an MoU with Tata Motors for integrated EV-charging ecosystem services across Tata vehicle buyers.

- Strategic Focus: Network breadth across Tier 1 and Tier 2 cities, OCPP 2.0.1 compliance, solar-integrated charging hubs, and OEM ecosystem partnerships.

Tecso Charge Zone Limited

ChargeZone is India's largest private CPO by highway fast charger count, with 2,700+ AC and DC charging points across 22+ states as of 2025. The company is Series C funded with investors including PGIM India and Archipelago Capital.

- Platform & Network: ChargeZone app, 25–150 kW DC fast chargers, multi-OEM compatibility, highway corridor specialisation.

- Recent Developments: In March 2026, ChargeZone plans to set up over 1,000 supercharging stations across key national highway corridors by FY27, as it looks to expand high-speed charging infrastructure in line with rising electric vehicle adoption.

- Strategic Focus: Highway corridor leadership, DC fast charging density, franchise-based expansion model, and inter-city EV travel enablement.

Sharify Services Pvt. Ltd.

Sharify Services Pvt. Ltd. is an India-based EV charging solutions provider focused on distributed, asset-light charging infrastructure. The company operates at the intersection of hardware deployment and software-led network management, targeting residential societies, commercial establishments, and fleet operators.

- Platform & Network: Sharify app-based charging access, AC slow and semi-fast chargers for apartments and workplaces, partner-led charger deployment model, and integrated CPMS for monitoring, billing, and user authentication.

- Recent Developments: In October 2025, Statiq is seeking to raise $15 to 18 million in funding from new and current investors.

- Strategic Focus: Decentralized charging network expansion, residential and workplace charging penetration, asset-light deployment via partnerships, and software-driven network optimization with a focus on improving charger utilization.

Market Concentration Analysis

The India EV charging station market exhibits low-to-moderate concentration, with no single CPO holding above 20% network share in 2025. The top five players – Tata Power, Tecso Charge Zone Limited, Sharify Services Pvt. Ltd., Fortum, and Kazam EV Tech Pvt. Ltd. – collectively account for approximately 55–60% of active public charging points. This fragmented structure reflects the market's early-stage maturity and the parallel participation of oil marketing companies, utility-backed operators, and venture-funded startups.

The market is experiencing a structural bifurcation. At the national CPO tier, consolidation is beginning: Tata Power's network scale and Tata Group ecosystem integration provide compounding advantages. In contrast, the highway and Tier 2/3 city segment is fragmenting, with franchise operators and local EPC companies establishing early-mover positions.

Investment & Growth Opportunities

Fastest-Growing Segments

Level 3 DC fast charging is emerging as the fastest-scaling hardware segment, driven by rising demand for high-power charging across highways, fuel retail outlets, and fleet depots. Deployment of 150–350 kW multi-port hubs is gaining traction, supported by corridor electrification initiatives and intercity EV adoption. Highway charging, backed by mandates from the National Highways Authority of India, represents a significant medium-term infrastructure opportunity due to current coverage gaps.

Emerging Market Expansion

Eastern India is evolving as a high-growth regional opportunity, supported by low existing charger density and proactive state-level EV policies in states such as West Bengal and Odisha. Urban centers like Kolkata are witnessing increasing EV adoption, creating early-mover advantages for charging operators. Additionally, battery swapping—led by players such as Sun Mobility—is gaining traction in two- and three-wheeler segments, opening adjacent opportunities in energy services and platform-based revenues.

Venture & Private Investment Trends

Investment activity is increasing across both hardware and software layers of the ecosystem. Key developments include funding rounds by ChargeZone and Statiq, as well as the public listing of Exicom Tele-Systems Limited. On the financing side, institutions such as the Indian Renewable Energy Development Agency and the Small Industries Development Bank of India are expanding access to green financing for EV infrastructure. Emerging investment themes include vehicle-to-grid (V2G) and renewable-integrated charging, with pilots led by NTPC Limited and Tata Power.

Future Market Outlook (2026-2034)

The India electric vehicle charging station market forecast projects steady value expansion from USD 589.1 Million in 2025 to USD 1,078.8 Million by 2034 at a CAGR of 6.82%. The market was anchored at USD 423.6 Million in 2020, reaching USD 819.1 Million in 2030 as an interim milestone. Near-term growth through 2027 will be driven by PM e-DRIVE implementation, fuel retail EVSE integration, and fleet depot buildout. Mid-term growth from 2028–2031 will shift towards smart charging, V2G monetization, and software platform scaling as CPO economics improve with rising utilisation rates. Long-term growth through 2034 will be defined by ultra-fast highway corridor expansion, cross-segment interoperability, and renewable-powered charging becoming the standard commercial model.

Three structural forces will most significantly reshape the market through 2034: (1) the transition from hardware-centric to software-platform-defined charging economics, where CPMS SaaS recurring revenue will increasingly dominate CPO profitability; (2) consolidation among top-tier CPOs as capital intensity creates scale advantages; and (3) the integration of EV charging with broader energy management systems including V2G, solar microgrids, and demand-response programs. By 2034, India's charging network is forecast to exceed 200,000 public charge points, transforming EV ownership economics and accelerating India's EV30@30 target achievement.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024–2025 with EV charging industry stakeholders, including CPO executives, EVSE manufacturers, utility company EV heads, fleet electrification managers, and DISCOM officials. Insights from primary respondents informed commercial model assumptions, utilisation rate benchmarks, and technology adoption timelines used in the forecasting models.

Secondary Research

Secondary sources include Ministry of Heavy Industries FAME II reports, PM e-DRIVE policy documents, BIS IS 17017 standards, NITI Aayog EV reports, Society of Manufacturers of Electric Vehicles (SMEV) sales data, IEA Global EV Outlook (2024), CEEW charging infrastructure studies, IRENA renewable energy cost data, and publicly available CPO network disclosures and annual reports.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models incorporating EV sales projections by vehicle category, average charging revenue per EV per year, CPO utilisation rate trajectories, EVSE hardware cost curves, government procurement mandates, and regional demand density mapping. Cross-validation was performed against comparable global market metrics from the IEA and BloombergNEF EV charging infrastructure outlook databases.

India Electric Vehicle Charging Station Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Charging Station Types Covered | AC Charging, DC Charging, Inductive Charging |

| Vehicle Types Covered | Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), Hybrid Electric Vehicle (HEV) |

| Installation Types Covered | Portable Charger, Fixed Charger |

| Charging Levels Covered | Level 1, Level 2, Level 3 |

| Connector Types Covered | Combines Charging Station (CCS), CHAdeMO, Normal Charging, Tesla Supercharger, Type-2 (IEC 621196), Others |

| Applications Covered | Residential, Commercial |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | Tata Power, Tecso Charge Zone Limited, Sharify Services Pvt. Ltd., Fortum, Kazam EV Tech Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India electric vehicle charging station market from 2020-2034.

- The India electric vehicle charging station market research report provides the latest information on the market drivers, challenges, and opportunities in the regional market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India electric vehicle charging station industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Electric Vehicle Charging Station Market Report

The India electric vehicle charging station market was valued at USD 589.1 Million in 2025, driven by accelerating EV adoption, FAME II policy support, and fleet electrification demand.

The market is projected to reach USD 1,078.8 Million by 2034, growing at a CAGR of 6.82% during 2026-2034, driven by highway corridor expansion, fleet depot buildout, and smart charging platform scaling.

Commercial applications lead with a 79.2% share in 2025, driven by fleet electrification commitments from logistics operators, ride-hailing platforms, and e-commerce delivery companies.

Level 3 leads with a 58.7% share by market value in 2025, driven by expressway corridor deployment, fuel retail integration, and fleet depot requirements for rapid charge cycles.

North India leads with a 33.8% share in 2025, driven by Delhi-NCR's high EV penetration (7%+ registered vehicle share), active state EV policy, and DTC's large e-bus fleet.

Key drivers include government policy (FAME II, PM e-DRIVE), rising EV sales, fleet electrification by logistics and ride-hailing platforms, and declining Level 2 EVSE costs.

East India is the fastest-growing region, supported by West Bengal's 100% road tax exemption for EVs, Odisha's EV policy, Kolkata e-bus deployment, and low base penetration creating above-market CAGR conditions.

Leading companies include Tata Power, Tecso Charge Zone Limited, Sharify Services Pvt. Ltd., Fortum, and Kazam EV Tech Pvt. Ltd.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade