India Ethanol Market Size, Share, Trends and Forecast by Type, Raw Material, Purity, Application, and Region, 2026-2034

India Ethanol Market Size, Share, Trends & Forecast (2026-2034)

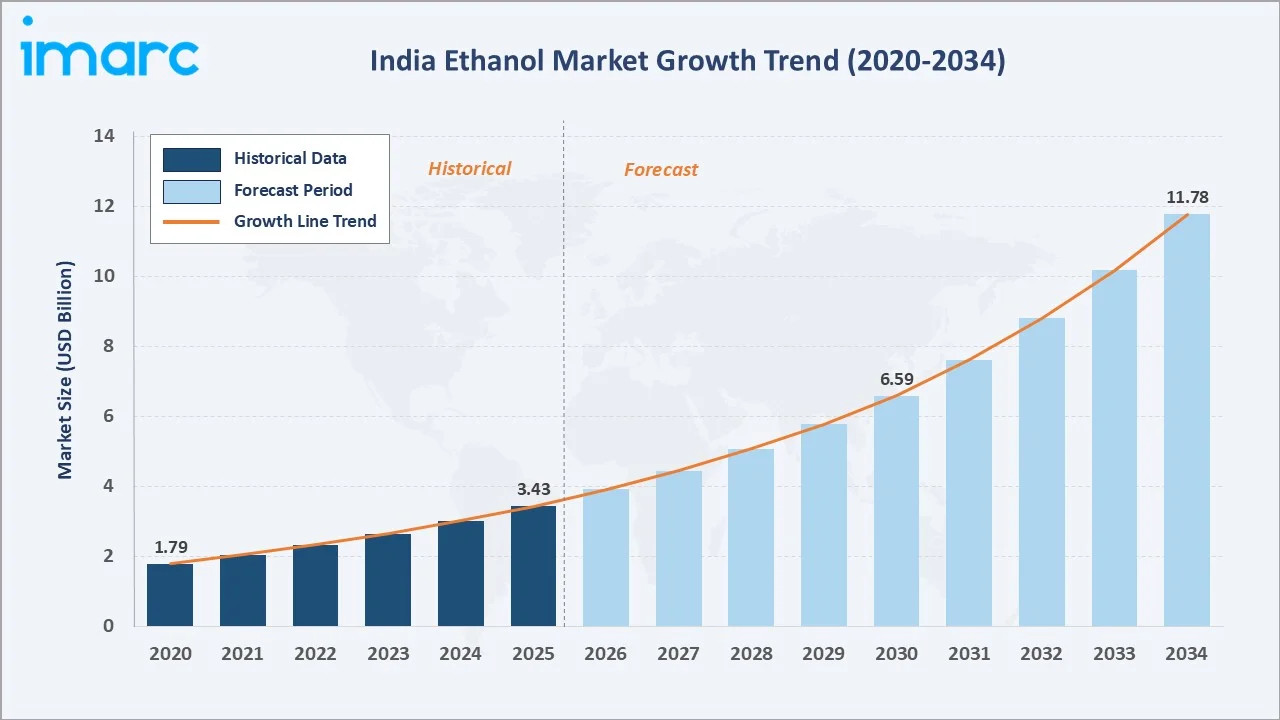

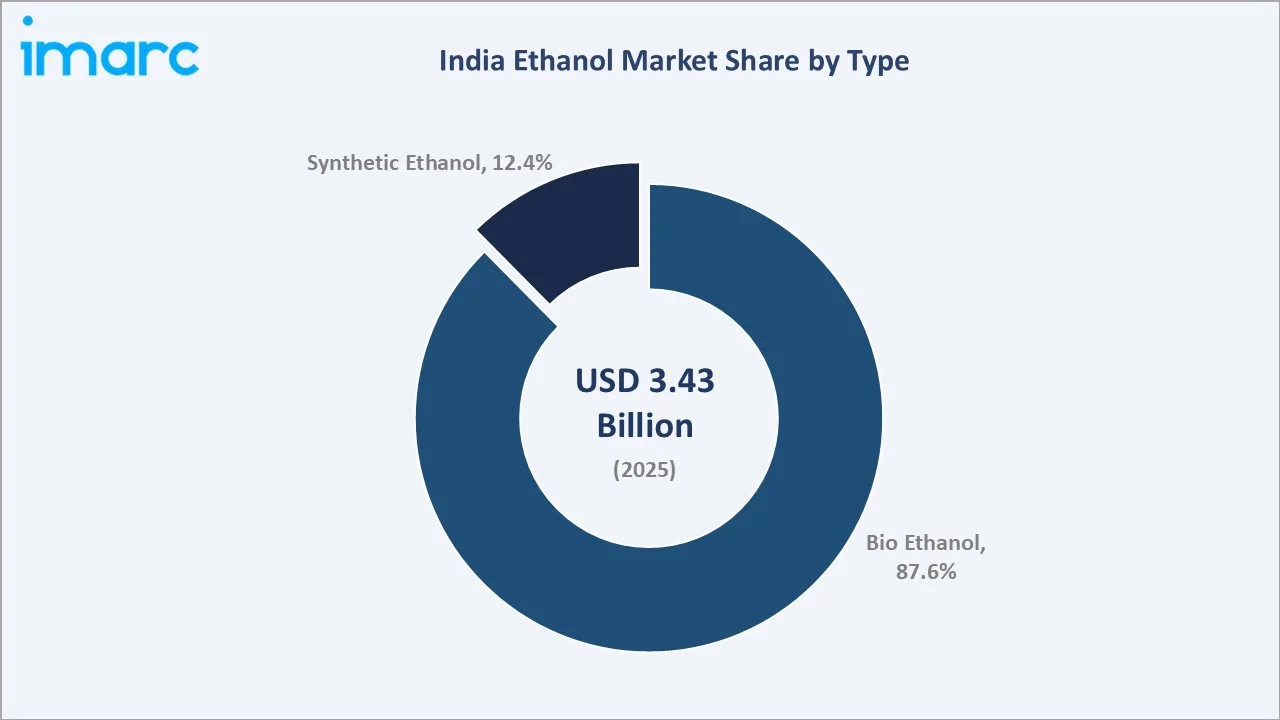

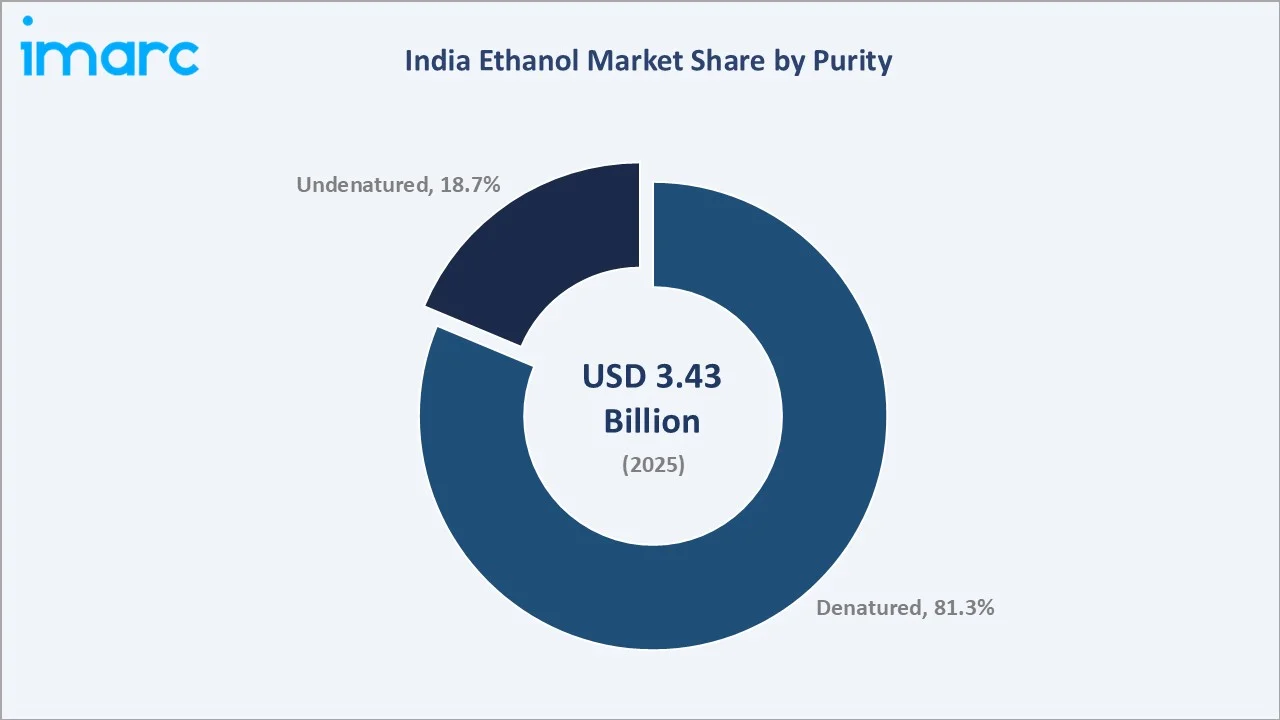

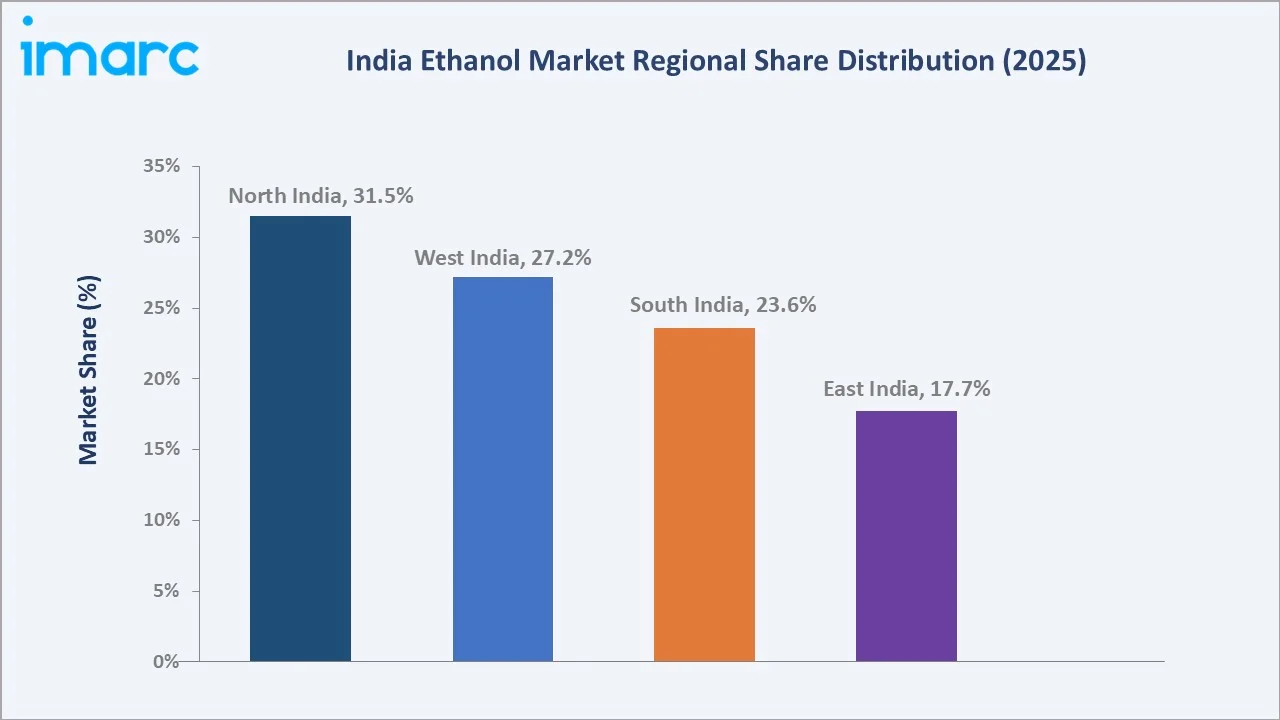

The India ethanol market size was valued at USD 3.43 Billion in 2025 and is projected to reach USD 11.78 Billion by 2034, exhibiting a CAGR of 13.95% during the forecast period 2026-2034. The Ethanol Blending Programme (EBP), the E20 fuel mandate, the National Biofuel Policy, and rising sugar surplus are powering India ethanol market growth. Bio-ethanol leads with 87.6% share in 2025, while denatured grades represent 81.3% of demand. North India dominates regionally with 31.5% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.43 Billion |

|

Forecast Market Size (2034) |

USD 11.78 Billion |

|

CAGR (2026-2034) |

13.95% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (31.5% share, 2025) |

|

Leading Type |

Bio Ethanol (87.6%, 2025) |

|

Leading Purity Grade |

Denatured (81.3%, 2025) |

The India ethanol market growth trajectory from 2020 through 2034 contrasts historical EBP-led expansion with a forecast curve powered by the E20 mandate, 2G bio-ethanol scale-up, and flex-fuel vehicle commercialization.

To get more information on this market, Request Sample

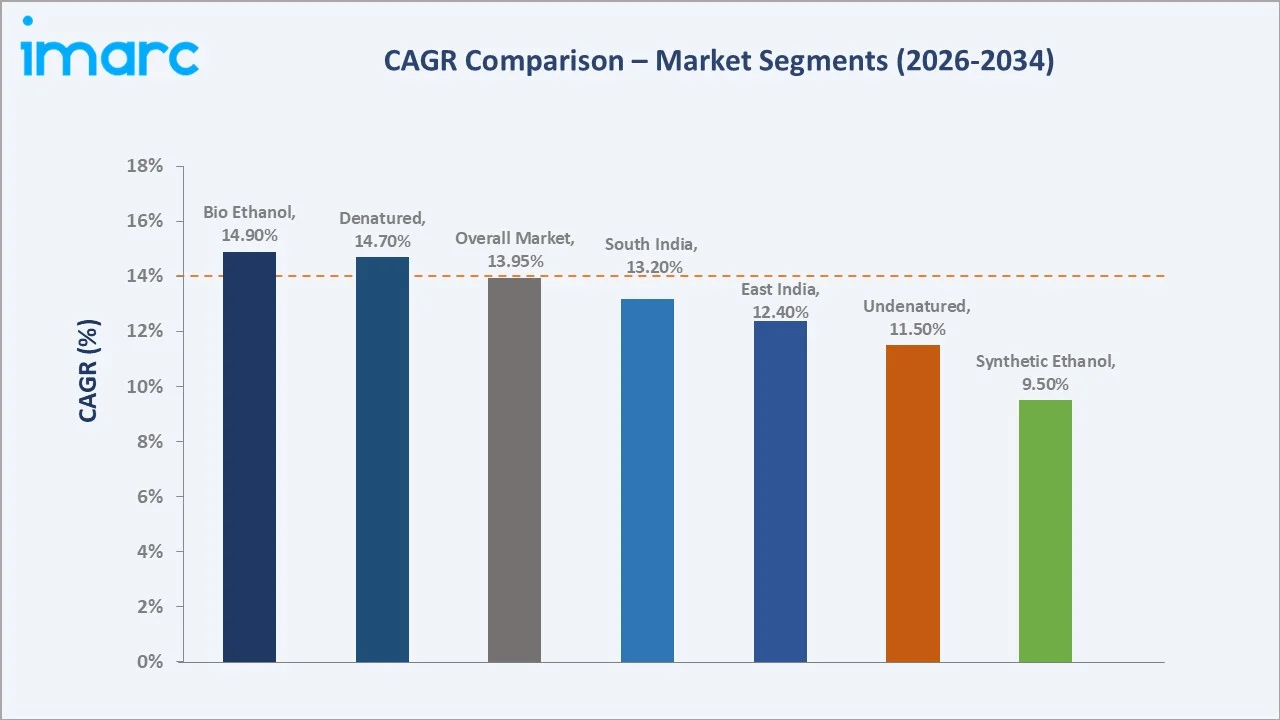

Segment-level CAGR comparisons highlight bio-ethanol and denatured grades as the fastest-growing sub-categories within the India ethanol market forecast through 2034.

Executive Summary

The India ethanol market is undergoing a structural shift. It is propelled by the Ethanol Blending Programme, the E20 fuel mandate, and India’s broader energy-transition agenda. Valued at USD 3.43 Billion in 2025, the market is projected to reach USD 11.78 Billion by 2034 at a CAGR of 13.95%.

Bio-ethanol dominates with an 87.6% share in 2025, drawn from sugarcane molasses, surplus sugar, damaged grains, and maize. Synthetic ethanol retains 12.4%, mainly serving industrial and pharmaceutical applications. Denatured ethanol commands 81.3% share, driven by fuel-blending offtake by oil marketing companies (OMCs), while undenatured grades support beverage and laboratory uses.

North India leads regionally at 31.5% share in 2025, followed by West India at 27.2%, South India at 23.6%, and East India at 17.7%. The India ethanol market outlook remains strongly positive as E20 fuel rolls out nationally, 2G bio-ethanol commercializes, and flex-fuel vehicle adoption accelerates.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Bio Ethanol - 87.6% share (2025) |

|

Second Type |

Synthetic Ethanol - 12.4% share (2025) |

|

Largest Purity Grade |

Denatured - 81.3% share (2025) |

|

Fastest Growing Type |

Bio Ethanol (~14.9% CAGR) |

|

Leading Region |

North India - 31.5% share (2025) |

|

Top Companies |

Praj Industries Ltd., Shree Renuka Sugars Ltd., Balrampur Chini Mills Limited, Triveni Engineering & Industries Ltd., Pioneer Industries Private Limited. |

|

Blending Achieved (2024) |

13.6% nationwide |

Key Analytical Observations Supporting the Data Above:

- Bio-ethanol dominance (87.6%) in 2025 reflects India’s feedstock structure built on sugarcane molasses (C-heavy and B-heavy), damaged food grains, and maize. Domestic ethanol supply to OMCs crossed 700 crore litres in ESY 2023-24.

- Synthetic ethanol share of 12.4% is sustained by industrial applications - paints, solvents, pharmaceuticals, and personal care - where production scale and consistent quality outweigh feedstock-based pricing.

- Denatured leadership at 81.3% is anchored by fuel-grade ethanol procurement under the EBP, where IOCL, BPCL, and HPCL collectively procured over 700 crore litres of denatured ethanol in 2024 for petrol blending.

- Undenatured share of 18.7% serves potable alcohol, beverages, pharmaceuticals, and laboratory grades. Excise-duty regimes and state-level licensing keep this segment commercially distinct from fuel-grade demand.

- North India leadership at 31.5% is powered by Uttar Pradesh’s sugarcane belt, which produces over 38% of India’s sugar, and the Punjab-Haryana grain corridor that supplies maize and damaged rice for grain-based distilleries.

- EBP momentum lifted blending to 13.6% in 2024 from 5.0% in 2019-20, per the Ministry of Petroleum & Natural Gas. The E20 (20% blending) target was advanced from 2030 to 2025-26, accelerating distillery capacity additions.

India Ethanol Market Overview

Ethanol in India is produced primarily from sugarcane molasses, surplus sugar, damaged food grains, and maize, with a smaller fraction made synthetically through ethylene hydration. The product is consumed across fuel blending, industrial chemicals, beverages, pharmaceuticals, and personal-care formulations.

The industry sits at the intersection of agricultural policy, energy security, and climate strategy. Growth is shaped by macroeconomic factors such as India’s n crude-import bill may rise by USD 70 Billion, the Ethanol Blending Programme targeting 20% by 2025-26, India’s 2070 net-zero pledge, and government initiatives that unlocked over INR 41,000 crore in distillery capacity loans by 2024.

Market Dynamics

To evaluate market opportunities, Request Sample

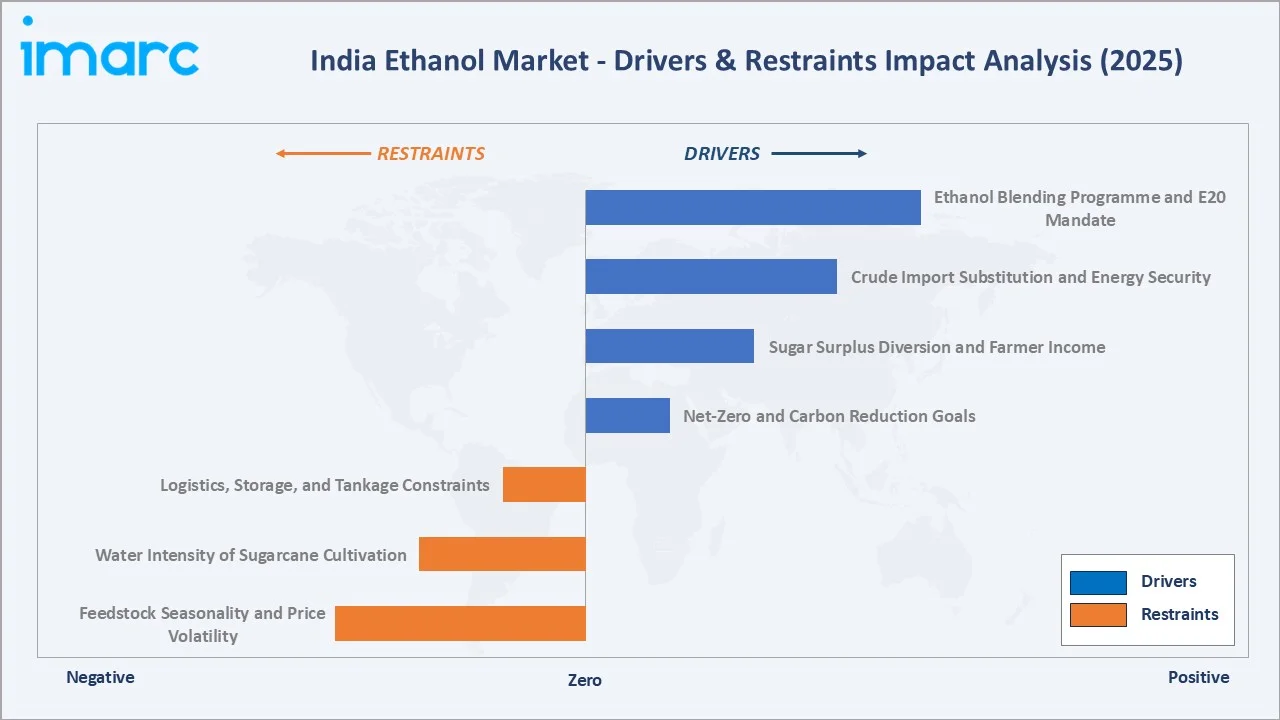

Market Drivers

- Ethanol Blending Programme and E20 Mandate: India achieved 13.6% petrol blending in 2024, up from 5.0% in FY2020. The government brought forward the E20 target from 2030 to 2025-26, requiring an estimated 1,623 crore litres of ethanol annually and anchoring long-term demand.

- Crude Import Substitution and Energy Security: India imported 234.3 million tonnes of crude oil in FY2024 at a cost of approximately USD 132 Billion. Ethanol blending has saved an estimated USD 12.4 Billion in foreign exchange between 2014 and 2024, per NITI Aayog.

- Sugar Surplus Diversion and Farmer Income: India’s sugar surplus often exceeds 6 million tonnes annually. Ethanol-linked revenue streams have strengthened sugar mill cash flows, leading to materially improved payment cycles and a structural reduction in cane arrears over recent years.

- Net-Zero and Carbon Reduction Goals: India committed to net-zero by 2070 and a 45% emissions intensity reduction by 2030. Ethanol blending is estimated to have reduced CO2 emissions by 519 lakh tonnes between 2014 and 2024, supporting transport-sector decarbonization.

Market Restraints

- Feedstock Seasonality and Price Volatility: Sugarcane crushing season runs October to May, creating supply gaps. Adverse monsoons in 2023 reduced sugar output by 9% and forced temporary curbs on sugarcane juice diversion to ethanol.

- Water Intensity of Sugarcane Cultivation: Sugarcane consumes nearly 2,000 litres of water per kilogram of sugar produced, raising sustainability concerns in groundwater-stressed states such as Maharashtra and Karnataka.

- Logistics, Storage, and Tankage Constraints: Ethanol movement requires dedicated stainless-steel tankers and bonded warehouses. India’s blending terminals number around 90, creating last-mile bottlenecks during peak procurement windows.

Market Opportunities

- 2G Bio-Ethanol from Agri-Residue: Pradhan Mantri JI-VAN Yojana supports 2G ethanol plants using rice straw, bagasse, and other lignocellulosic residues. IOCL’s Panipat 2G plant commissioned in 2022 has a 100 KLPD capacity and serves as a national template.

- Flex-Fuel Vehicle Commercialization: Toyota launched the Innova Hycross flex-fuel prototype in 2023; Maruti Suzuki and Hyundai followed in 2024-25. Mass adoption of E85 and E100 vehicles could expand ethanol demand by 4-5x beyond current E20 levels.

- Compressed Bio-Gas (CBG) and Bio-Refinery Integration: The SATAT initiative targets 5,000 CBG plants by 2025, many co-located with ethanol distilleries. This creates integrated bio-refineries with shared feedstock, reducing per-litre production costs.

Market Challenges

- Food vs Fuel Concerns: Diverting food grains such as rice and maize to ethanol production sparks public debate, particularly during years of food-price inflation. Government rice diversion to ethanol was temporarily restricted in late 2023.

- Capital Intensity of Distillery Capacity Additions: A 200 KLPD grain-based distillery requires INR 350 to 450 crore in capital. Smaller mills face working-capital strain despite the government’s interest-subvention scheme covering 6% of borrowing costs.

- State-Level Excise and Movement Permits: Ethanol pricing, excise duties, and inter-state movement rules vary across 28 states. This regulatory fragmentation complicates pan-India sourcing for OMCs and creates timing mismatches in procurement.

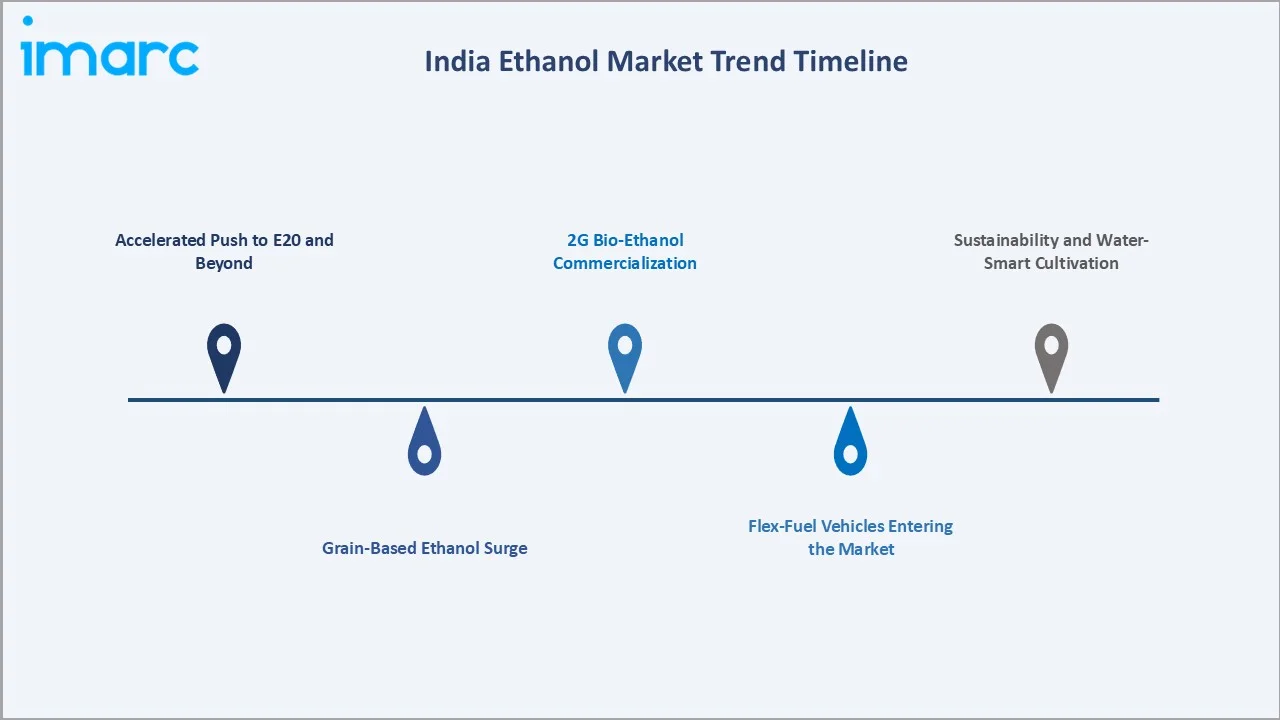

Emerging Market Trends

1. Accelerated Push to E20 and Beyond

India achieved 13.6% blending by 2024, with E20 fuel rolled out at over 12,000 retail outlets nationwide. The Ministry of Petroleum aims for full E20 availability by 2025-26, opening discussions on E27 and E85 pathways for the 2030 horizon.

2. Grain-Based Ethanol Surge

Grain-based ethanol now contributes nearly 48% of national supply, up from under 12% in 2019. Maize allocations to ethanol crossed 400 lakh tonnes in 2024, supported by new dedicated maize varieties developed by ICAR for distillery use.

3. 2G Bio-Ethanol Commercialization

IOCL’s Panipat 2G plant began commercial operations in 2022, processing rice straw into ethanol. Bharat Petroleum, HPCL, and Numaligarh Refinery are scaling similar plants in Bargarh, Bathinda, and Assam, each with 100 to 130 KLPD capacity.

4. Flex-Fuel Vehicles Entering the Market

Toyota Kirloskar, Maruti Suzuki, and Mahindra showcased E85 and E100 flex-fuel models at Auto Expo 2025. Ministry of Road Transport draft notifications target flex-fuel mandate compliance for new ICE vehicles from 2027.

5. Sustainability and Water-Smart Cultivation

Maharashtra and Karnataka are piloting drip-irrigation incentives for sugarcane farmers, targeting a 35% to 40% reduction in water use. ISMA has highlighted drip irrigation as a key lever to improve water efficiency and yields in sugarcane cultivation, with adoption increasing across major producing states.

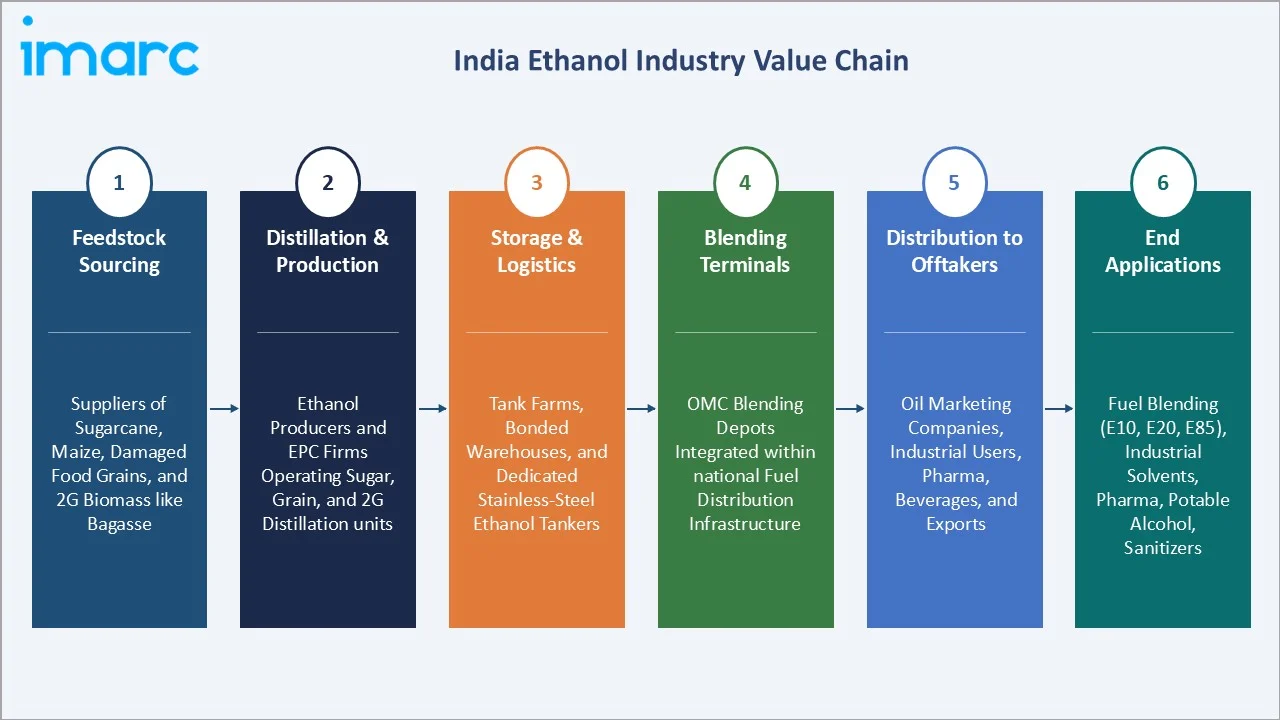

Industry Value Chain Analysis

The India ethanol value chain spans six integrated stages from feedstock cultivation through end-application offtake. Each stage carries distinct margin profiles, regulatory exposure, and capital requirements relevant to the India ethanol market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Feedstock Sourcing |

Suppliers of sugarcane, maize, damaged food grains, and second-generation biomass such as bagasse and agricultural residues |

|

Distillation & Production |

Ethanol producers and technology providers operating distillation units using sugar-based, grain-based, and 2G biomass processes |

|

Storage & Logistics |

Tank farm operators, bonded warehouse providers, and specialized transport networks including dedicated ethanol tankers |

|

Blending Terminals |

Fuel blending depots integrated within national fuel distribution infrastructure across key consumption centers |

|

Distribution to Offtakers |

Primary offtake by oil marketing companies, along with supply to industrial users, pharmaceutical companies, beverage manufacturers, and export markets |

|

End Applications |

Fuel blending (E10, E20, E85), industrial solvents, pharmaceutical ingredients, potable alcohol, and hygiene products such as sanitizers |

Distilleries hold the strongest strategic position by combining feedstock access, technology, and OMC offtake contracts. Technology providers such as Praj Industries are extending into 2G, while integrated sugar-ethanol players are scaling co-generation and CBG to capture additional revenue from the same crushing operation.

Technology Landscape in the Ethanol Industry

Fermentation and Distillation Technology

Continuous fermentation, multi-pressure distillation, and molecular-sieve dehydration are now standard for fuel-grade output. Indian distilleries achieve 99.8% purity at energy intensities below 2.0 kg steam per litre, comparable to global benchmarks.

Feedstock Innovation and 2G Pathways

Lignocellulosic 2G ethanol, which uses bagasse, rice straw, and corn stover, is moving from pilot to commercial scale. IOCL’s Panipat plant uses enzymatic hydrolysis from Praj Industries and processes around 2 lakh tonnes of biomass annually into 100 KLPD ethanol.

Smart Connectivity and Digital Process Control

Distributed control systems (DCS), AI-driven yield optimization, and IoT sensors for fermentation are being adopted across newer 60 to 200 KLPD capacities. Praj’s BluePrint digital platform reports 4% to 6% energy savings and 2% to 3% yield uplift.

Carbon Capture and Bio-Refinery Integration

Distilleries are piloting CO2 capture from fermentation streams for industrial gas customers. Co-located CBG plants under SATAT and bagasse-fired co-generation create integrated bio-refineries that improve plant economics by 8% to 12%.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the India ethanol market, along with forecasts at the regional and country levels from 2026 to 2034. The market has been categorized based on type and purity.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Bio Ethanol | 87.6% | 2025 |

| Raw Material | 🔒 | 🔒 | 2025 |

| Purity | Denatured | 81.3% | 2025 |

| Application | 🔒 | 🔒 | 2025 |

| Region | North India | 31.5% | 2025 |

By Type

Bio-ethanol leads the India ethanol market type with an 87.6% share in 2025. Demand is anchored by fuel-blending offtake by oil marketing companies under the EBP. Bio-ethanol is projected to grow at a 14.9% CAGR through 2030, outpacing the overall market on the back of E20 rollout.

To access detailed market analysis, Request Sample

Sugarcane molasses (B-heavy and C-heavy) supplies roughly 52% of feedstock in 2024, with grain-based routes (maize, damaged rice) supplying the balance. The shift toward dual-feed distilleries reduces seasonality risk and improves capacity utilization to 85% plus.

Synthetic ethanol retains 12.4% type share, sustained by industrial use cases that demand consistent quality and supply continuity. Producers serve the paints and coatings industry, pharmaceutical excipients, personal-care formulations, and laboratory-grade chemicals across India’s industrial belts.

By Purity

Denatured ethanol is the dominant purity grade at 81.3% of revenue in 2025. India’s OMCs procured over 660 crore litres of denatured ethanol in ESY 2023-24, growing at 21% year-over-year. The grade is denatured with isopropanol or other agents to make it unfit for human consumption and exempt from beverage excise.

Pricing for denatured fuel-grade ethanol is set by the Cabinet Committee on Economic Affairs, with separate tariffs for C-heavy molasses, B-heavy molasses, sugarcane juice, and grain-based ethanol. The 2024-25 price for B-heavy molasses ethanol was set at INR 60.73 per litre.

Undenatured ethanol represents 18.7% of demand and remains a steady volume driver, supported by potable alcohol, beverages, pharmaceuticals, and laboratory-grade chemicals. State-level excise regimes and licensing requirements differentiate this segment from fuel-grade demand. Pharmaceutical and hand-sanitizer demand expanded materially since 2020 and continues to grow at 9% to 11% annually.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

31.5% |

UP sugarcane belt, Punjab-Haryana grain corridor, Bihar maize feedstock, IOCL Panipat 2G plant |

|

West India |

27.2% |

Maharashtra sugar mills, Gujarat distilleries, Madhya Pradesh grain ethanol, OMC blending hubs |

|

South India |

23.6% |

Karnataka sugar belt, Tamil Nadu integrated mills, Andhra-Telangana grain ethanol projects |

|

East India |

17.7% |

Bihar grain ethanol cluster, West Bengal distilleries, Odisha-Jharkhand emerging capacity |

North India commands 31.5% revenue share in 2025. Uttar Pradesh alone accounts for over 38% of India’s sugar production and operates the largest cluster of B-heavy molasses distilleries. The Punjab-Haryana corridor is a key supplier of maize and damaged rice for grain-based plants. IOCL’s Panipat 2G ethanol plant, India’s first commercial 2G facility, anchors the region’s technology leadership and processes around 2 lakh tonnes of rice straw annually.

West India holds 27.2% of revenue, anchored by Maharashtra’s integrated sugar-ethanol mills, Gujarat’s standalone distilleries, and Madhya Pradesh’s expanding grain-based capacity. Maharashtra contributes nearly 30% of national ethanol output, with major operations from Bajaj Hindusthan, Shree Renuka, and Dwarikesh Sugar. Gujarat hosts strategic OMC blending depots near Hazira and Vadodara.

South India accounts for 23.6%, led by Karnataka and Tamil Nadu. Karnataka’s sugar belt around Belagavi and Bagalkot supports EID Parry and Bannari Amman operations, while Tamil Nadu hosts Bannari Amman, EID Parry, and Triveni-led capacity. Andhra Pradesh and Telangana are emerging as grain-ethanol hubs supported by maize cultivation. East India represents 17.7%, driven by Bihar’s grain ethanol cluster, West Bengal distilleries, and emerging capacity in Odisha and Jharkhand. Bihar attracted over INR 30,000 crore in distillery investment commitments under its 2021 Industrial Policy.

Competitive Landscape

|

Company Name |

Market Position |

Core Strength |

|

Praj Industries Ltd. |

Leader |

Global leader in ethanol technology and engineering; strong presence in 1G and 2G biofuel solutions |

|

Shree Renuka Sugars Ltd. |

Leader |

Integrated sugar and ethanol player with large refining capacity and strong export linkages |

|

Balrampur Chini Mills Limited |

Leader |

One of India’s largest sugar producers with significant ethanol capacity and efficient cane sourcing |

|

Triveni Engineering & Industries Ltd. |

Leader |

Diversified player with strong distillery operations and premium alcohol/ethanol portfolio |

|

Pioneer Industries Private Limited |

Leader |

Large-scale grain-based distillery with strong presence in ENA and ethanol production |

|

Radical Bio Organics Limited. |

Challenger |

Focus on organic and specialty bio-based products with niche ethanol and chemical applications |

|

Zenith Bio Chemical Industries Private Limited. |

Challenger |

Regional player with capabilities in industrial alcohol and bio-chemical production |

|

New Phaltan Sugar Works Distillery Division Ltd |

Challenger |

Integrated sugar mill with expanding distillery capacity and ethanol diversification strategy |

|

Indalc Spirits Pvt. Ltd |

Emerging |

Growing grain-based distillery with focus on ENA supply and regional market penetration |

|

Dalmia Bharat Sugar & Industries Ltd |

Emerging |

Diversified sugar player scaling up ethanol capacity under government blending initiatives |

The India ethanol market is moderately fragmented, with integrated sugar-ethanol producers competing alongside grain-based distilleries and technology providers. Leading players compete on feedstock access, distillery capacity, OMC offtake contracts, and technology adoption. Strategic moves are frequent - Praj Industries commissioned multiple grain and 2G ethanol plants in 2024, while Balrampur Chini and Triveni expanded capacities by 200 plus KLPD each in 2023-24.

Key Company Profiles

Praj Industries Limited

Praj Industries, headquartered in Pune, is India’s largest ethanol technology and engineering provider. Founded in 1985, the company has delivered over 1,000 ethanol and bioenergy plants across 100 plus countries with cumulative capacity exceeding 18 billion litres annually.

- Product & Platform Portfolio: BioPlants for 1G ethanol from molasses, grain, and sugarcane juice; Bharat 2G technology for lignocellulosic biomass; CBG plants under SATAT; sustainable aviation fuel (SAF) and ethanol-to-jet pathways.

- Recent Developments: In June 2025, Praj Industries partnered with International Air Transport Association and Indian Sugar & Bio-energy Manufacturers Association to accelerate the development of sustainable aviation fuel (SAF) in India. The collaboration focuses on conducting a lifecycle assessment of SAF produced from sugarcane via the ethanol-to-jet pathway and establishing an India-specific certification framework aligned with global standards such as ISCC and CORSIA.

- Strategic Focus: Praj’s strategy centres on 2G commercialization, ethanol-to-SAF technology, CBG-ethanol bio-refinery integration, and international expansion in Latin America and Southeast Asia.

Triveni Engineering & Industries Limited

Triveni Engineering, headquartered in Noida, is one of India’s largest integrated sugar producers and a key ethanol supplier in Uttar Pradesh. The company operates 7 sugar mills and 4 distilleries with combined ethanol capacity of 800 KLPD.

- Product & Platform Portfolio: Denatured fuel ethanol from B-heavy molasses, sugarcane juice, and grain; extra-neutral alcohol (ENA); refined sugar; and power co-generation from bagasse.

- Recent Developments: The company has announced plans to invest over ₹1,000 crore to scale ethanol capacity to 860 KLPD, while also progressing a composite scheme to amalgamate Sir Shadi Lal Enterprises with TEIL and demerge its Power Transmission business.

- Strategic Focus: Triveni’s strategy emphasizes capacity expansion to 1,200 KLPD by 2027, multi-feed flexibility, ENA exports, and integrated bio-refinery development at flagship UP sites.

Balrampur Chini Mills Limited

Balrampur Chini, headquartered in Kolkata, is among the largest integrated sugar producers in India, with 10 sugar mills concentrated in Uttar Pradesh and total cane crushing capacity of 80,000 TCD. Distillery capacity stands at 1,050 KLPD.

- Product & Platform Portfolio: Fuel-grade ethanol from sugarcane juice, B-heavy molasses, and grain; refined and pharmaceutical-grade sugar; ENA for industrial use; power co-generation; and PLA bioplastic via a strategic JV.

- Recent Developments: In 2026, Balrampur Chini Mills Limited is scaling its green manufacturing strategy through a large investment in polylactic acid (PLA) bioplastics, with an initial project outlay of around ₹2,850 crore in Uttar Pradesh. The company plans to further expand this capacity with an additional investment of ₹2,000–4,000 crore, driven by rising demand for sustainable, bio-based plastics and the need to build an integrated downstream ecosystem.

- Strategic Focus: Balrampur’s strategy is pivoting from a sugar-led to a bio-refinery-led portfolio, with PLA bioplastics, ethanol expansion, and integrated co-generation forming a balanced revenue mix by 2027.

Market Concentration Analysis

The India ethanol market is moderately concentrated. The top five players - Praj Industries Ltd., Shree Renuka Sugars Ltd., Balrampur Chini Mills Limited, Triveni Engineering & Industries Ltd., Pioneer Industries Private Limited - collectively account for approximately 32% to 38% of national ethanol revenue in 2025. The remaining share is distributed across Radical Bio Organics Limited., Zenith Bio Chemical Industries Private Limited., New Phaltan Sugar Works Distillery Division Ltd, Indalc Spirits Pvt. Ltd, Dalmia Bharat Sugar & Industries Ltd and a long tail of regional distilleries and grain-based independents.

The market is following a bifurcated dynamic. Integrated sugar-ethanol majors are consolidating capacity through brownfield expansions and multi-feed flexibility. Simultaneously, grain-based independents such as Globus Spirits are scaling rapidly under PMJI-VAN incentives and dedicated maize-distillery agreements with state governments. New 2G commercial plants by IOCL, BPCL, HPCL, and Numaligarh Refinery are introducing public-sector capacity into the mix through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Bio-ethanol is the highest-growth opportunity at approximately 14.9% CAGR through 2030. Denatured fuel-grade ethanol remains the fastest-growing purity segment at 14.7% CAGR, supported by E20 expansion. Grain-based and 2G ethanol pathways represent the premium technology growth opportunity, with 2G commercial capacity targeted to cross 12 plants by 2030.

Emerging State and Regional Expansion

North India retains volume leadership through UP sugarcane and Punjab-Haryana grain feedstock. The highest incremental growth, however, is forecast in Bihar, Madhya Pradesh, and Andhra Pradesh, where state industrial policies offer 25% to 35% capital subsidy on grain-distillery investments. Bihar alone attracted over INR 30,000 crore in distillery commitments by 2024.

Strategic and Public-Sector Investment Trends

Government-backed financing crossed INR 41,000 crore in interest-subvention loans by 2024 across more than 400 distillery projects. IOCL, BPCL, HPCL, and Numaligarh Refinery are scaling 2G commercial plants under JI-VAN. Strategic acquisitions and expansions by Praj, Balrampur, and Triveni are reshaping competitive intensity. SAF, ethanol-to-jet, and CBG integration are the primary venture and corporate capital focus areas through 2034.

Future Market Outlook (2026-2034)

The India ethanol market forecast projects strong value expansion from USD 3.43 Billion in 2025 to USD 11.78 Billion by 2034 at a CAGR of 13.95%. Bio-ethanol will retain dominance and accelerate structurally, while synthetic ethanol will sustain industrial-grade volumes for paints, pharmaceuticals, and personal-care applications.

Three key shifts will reshape the market through 2034. The E20 mandate will be fully achieved nationwide by 2025-26, with discussions advancing toward E27 and selective E85 deployment by 2030. 2G bio-ethanol from rice straw and bagasse will move from pilots to a 1,500 plus KLPD commercial fleet. Flex-fuel vehicles will gain market share as automakers comply with draft mandates effective from 2027, opening multi-fold demand expansion beyond the current blending base.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024 to 2025 with industry stakeholders such as managing directors of sugar-ethanol mills, technology heads at distillery EPC firms, ethanol procurement leads at OMCs, and senior officials at the Department of Food & Public Distribution and the Ministry of Petroleum & Natural Gas. These insights validated capacity, supply, and offtake assumptions.

Secondary Research

Secondary sources include Ministry of Petroleum & Natural Gas publications, NITI Aayog ethanol roadmap reports, ISMA (Indian Sugar Mills Association) data, FCI grain allocation notifications, company annual filings, and trade publications such as Chini Mandi, Biofuels International, and ICRA sector outlooks. Regional capacity data was triangulated using state excise department disclosures.

Forecasting Models

Market sizing and growth projections were derived using a combined top-down and bottom-up approach, incorporating fuel demand projections, blending percentages, distillery capacity additions, sugarcane and grain output forecasts, and CCEA price notifications. Scenario analysis (base, optimistic, conservative) was conducted to account for monsoon variability, policy shifts, and feedstock price volatility.

India Ethanol Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Bio Ethanol, Synthetic Ethanol |

| Raw Materials Covered | Sugar and Molasses, Cassava, Rice, Algal Biomass, Ethylene, Lignocellulosic Biomass |

| Purities Covered | Denatured, Undenatured |

| Applications Covered | Fuel and Fuel Additives, Beverages, Industrial Solvents, Personal Care, Disinfectants, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Praj Industries Ltd., Shree Renuka Sugars Ltd., Balrampur Chini Mills Limited, Triveni Engineering & Industries Ltd., Pioneer Industries Private Limited, Radical Bio Organics Limited., Zenith Bio Chemical Industries Private Limited., New Phaltan Sugar Works Distillery Division Ltd, Indalc Spirits Pvt. Ltd, Dalmia Bharat Sugar & Industries Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India ethanol market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India ethanol market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India ethanol industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Ethanol Market Report

The India ethanol market was valued at USD 3.43 Billion in 2025, driven by the Ethanol Blending Programme, the E20 fuel mandate, energy security needs, and rising sugar surplus diversion to fuel.

The market is projected to reach USD 11.78 Billion by 2034, growing at a CAGR of 13.95% during 2026-2034, supported by E20 rollout, 2G bio-ethanol scale-up, and flex-fuel vehicle adoption.

Bio-ethanol leads with 87.6% share in 2025, drawn from sugarcane molasses, surplus sugar, damaged grains, and maize. Synthetic ethanol retains 12.4% for industrial and pharmaceutical use.

Denatured ethanol dominates with 81.3% share in 2025, anchored by oil marketing company offtake under the EBP. Undenatured grades retain 18.7% for beverage and industrial applications.

North India dominates with 31.5% share in 2025. Uttar Pradesh sugarcane, Punjab-Haryana grain feedstock, and the IOCL Panipat 2G plant underpin its regional leadership.

Key drivers include the EBP and E20 mandate, crude import substitution, sugar surplus diversion, farmer income support, and India’s net-zero by 2070 commitment.

Major players include Praj Industries Ltd., Shree Renuka Sugars Ltd., Balrampur Chini Mills Limited, Triveni Engineering & Industries Ltd., Pioneer Industries Private Limited, Radical Bio Organics Limited., Zenith Bio Chemical Industries Private Limited., New Phaltan Sugar Works Distillery Division Ltd, Indalc Spirits Pvt. Ltd, Dalmia Bharat Sugar & Industries Ltd.

India achieved 13.6% ethanol blending in petrol in 2024, up from 5.0% in FY2020. The E20 (20%) target was advanced from 2030 to 2025-26 by the central government.

Major challenges include feedstock seasonality, water-intensity of sugarcane, food versus fuel concerns, capital intensity of distilleries, and state-level excise and movement-permit fragmentation.

Key opportunities include 2G bio-ethanol from biomass, flex-fuel vehicle commercialization, CBG-ethanol bio-refinery integration, grain-based distilleries in Bihar and MP, and SAF pathways.

The E20 mandate requires approximately 1,016 crore litres of ethanol annually by 2025-26, anchoring long-term offtake by IOCL, BPCL, and HPCL, and supporting distillery capacity expansion across India.

Second-generation ethanol uses agricultural residues such as rice straw and bagasse. IOCL’s 100 KLPD Panipat plant began commercial operations in 2022, with similar 2G plants by BPCL, HPCL, and NRL in scale-up.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)