India Eyewear Market Size, Share, Trends and Forecast by Product, Gender, Distribution Channel, and Region, 2026-2034

India Eyewear Market Size, Share, Trends & Forecast (2026-2034)

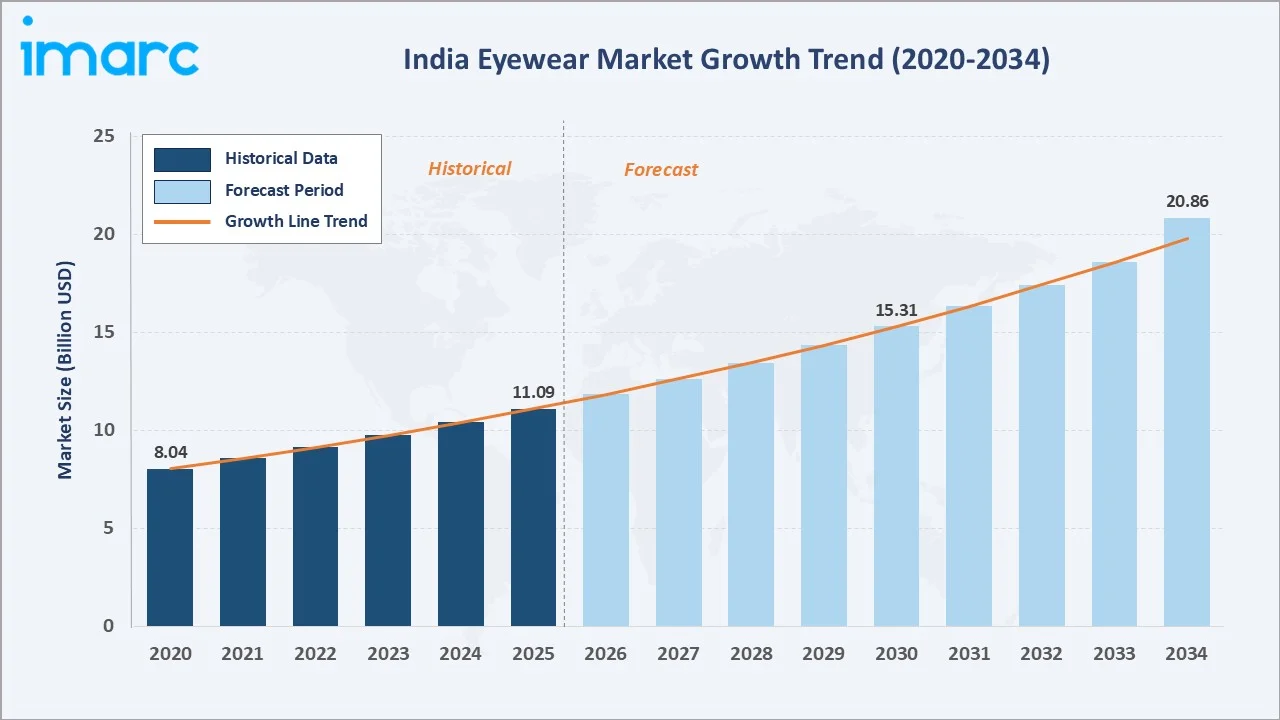

The India eyewear market size reached USD 11.09 Billion in 2025 and is projected to reach USD 20.86 Billion by 2034, exhibiting a CAGR of 6.66% during 2026-2034. Rising vision disorder incidence, growing fashion consciousness, e-commerce expansion, and digital eye strain awareness are the primary forces driving market growth.

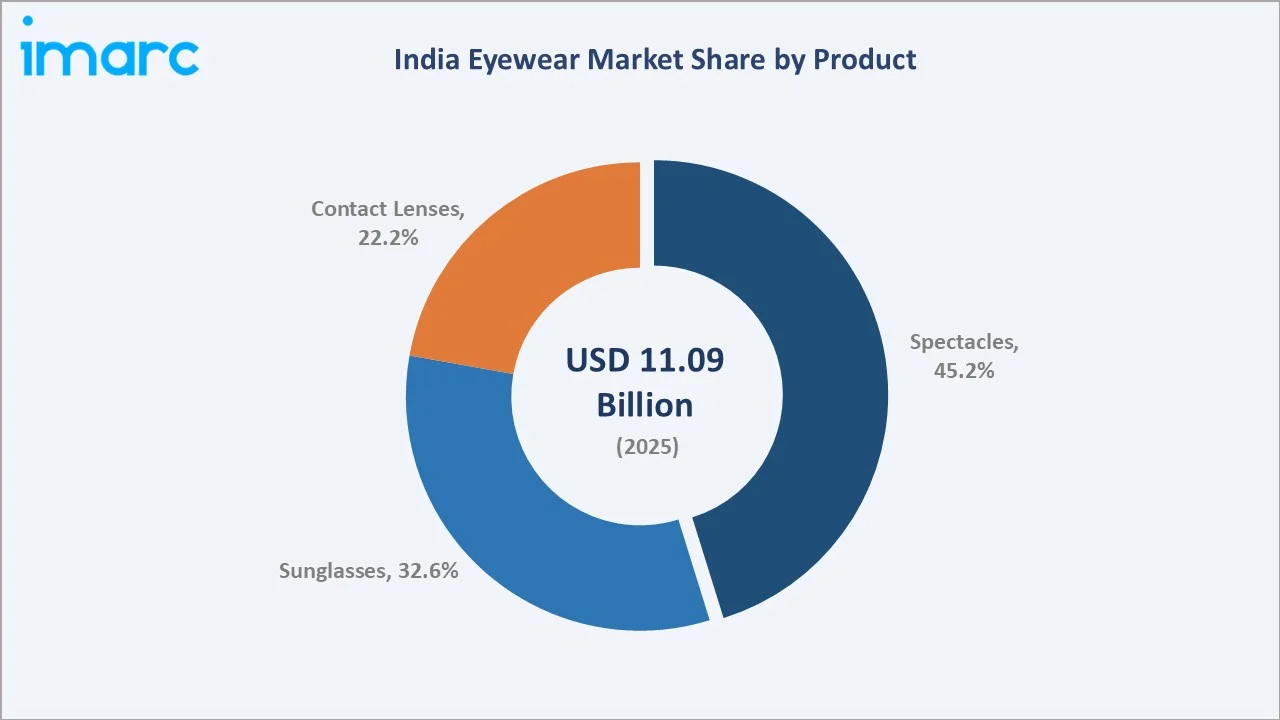

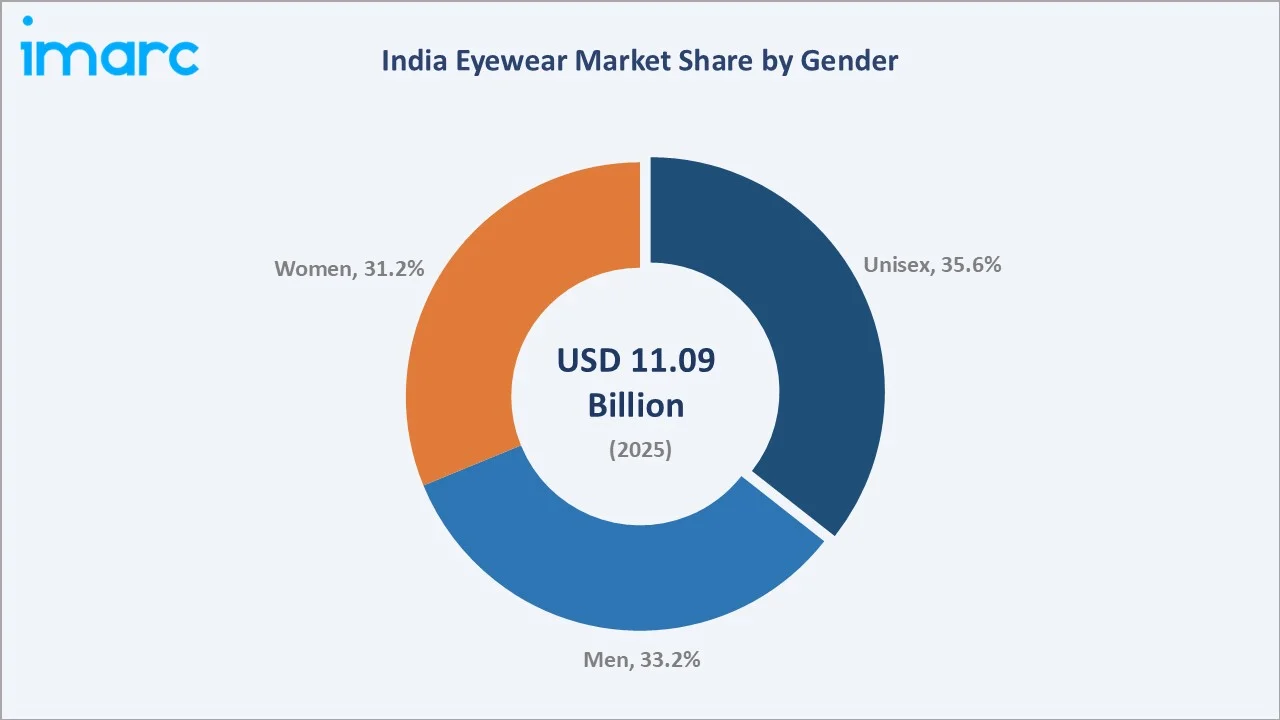

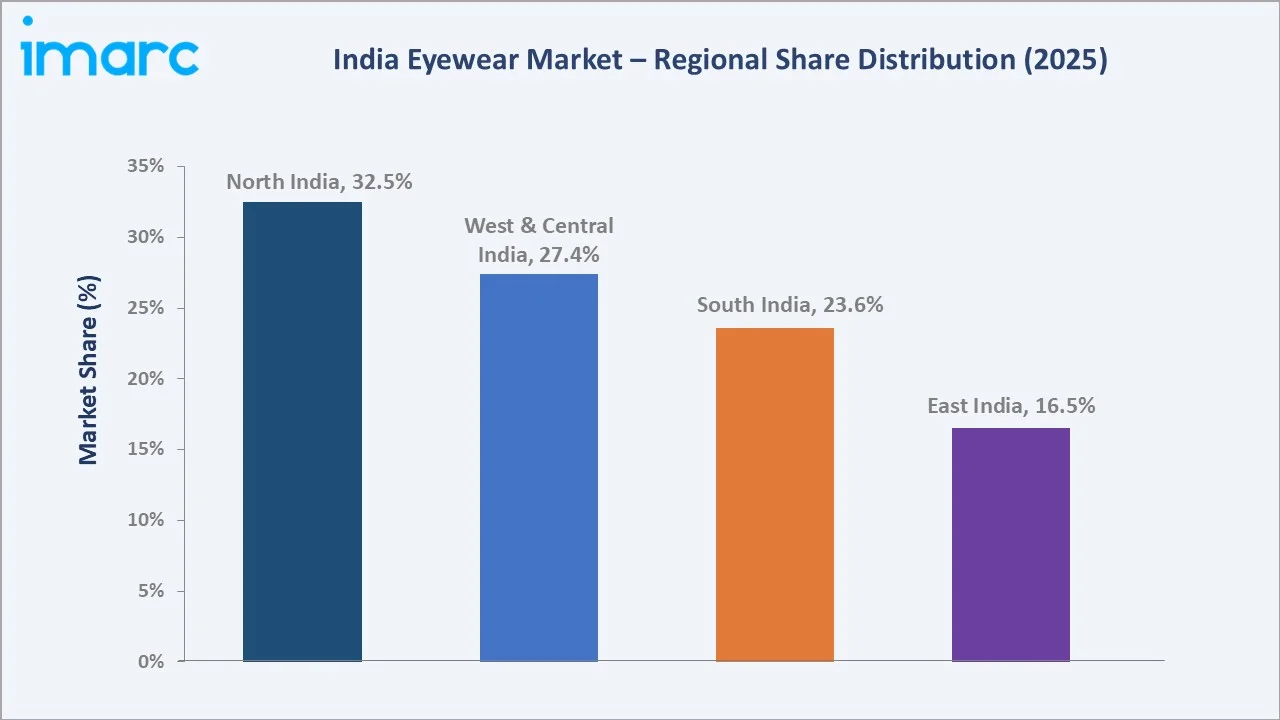

Spectacles dominate the product mix at 45.2% in 2025, while the unisex segment leads gender breakup at 35.6%. North India commands the largest regional share at 32.5% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 11.09 Billion |

|

Forecast Market Size (2034) |

USD 20.86 Billion |

|

CAGR (2026-2034) |

6.66% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Product |

Spectacles (45.2% share, 2025) |

|

Leading Gender Segment |

Unisex (35.6% share, 2025) |

|

Largest Region |

North India (32.5% share, 2025) |

|

Second Largest Region |

West & Central India (27.4% share, 2025) |

The India eyewear market growth trajectory from 2020 through 2034, with historical expansion to USD 11.09 Billion in 2025, reflects consistent demand driven by vision correction needs and lifestyle upgrades, while the forecast to USD 20.86 Billion captures accelerating online retail penetration, rising incomes, and technology-led product innovation.

To get more information on this market, Request Sample

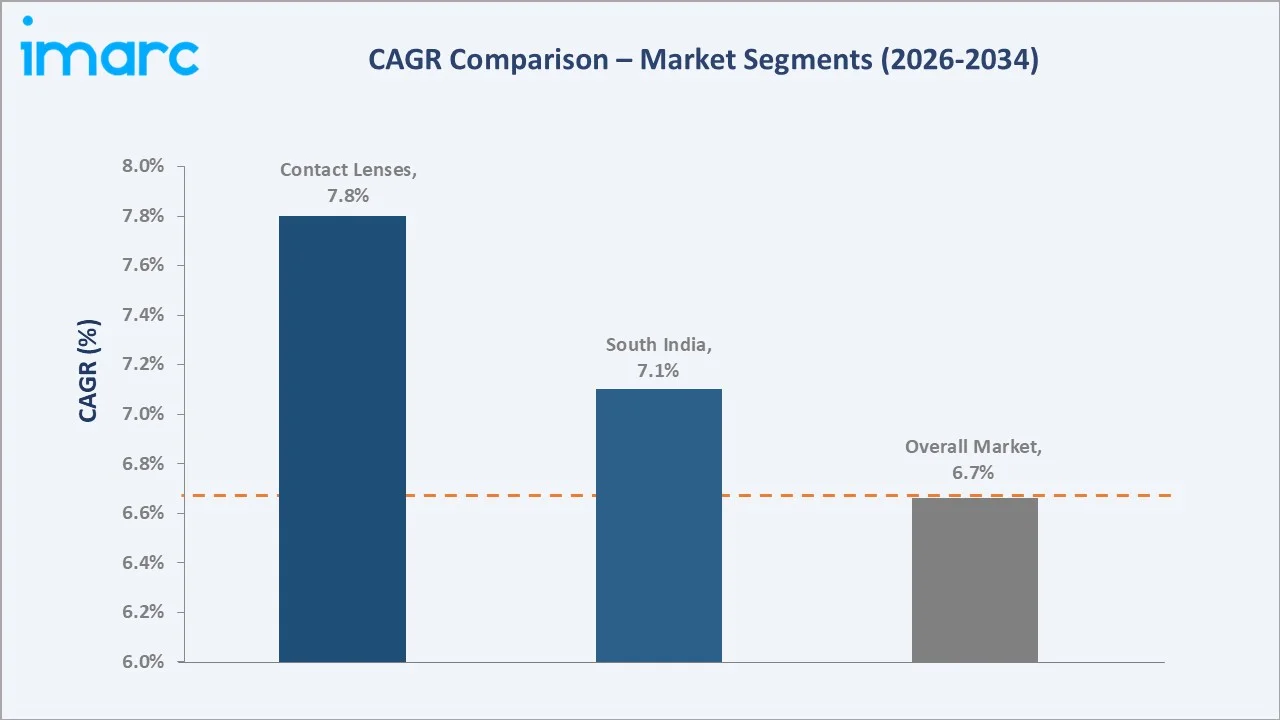

The CAGR trajectories across key product and gender sub-segments, with contact lenses at ~7.8% CAGR and South India at ~7.1% CAGR, represent the fastest-growing categories within the India eyewear industry analysis through 2034.

Executive Summary

The India eyewear market is on a sustained growth trajectory from USD 11.09 Billion in 2025 to USD 20.86 Billion by 2034. Eyewear, encompassing corrective spectacles, protective sunglasses, and contact lenses, serves both medical and lifestyle needs across India's rapidly urbanising population.

Spectacles dominate at 45.2% in 2025 due to high refractive error prevalence and affordability of prescription frames. Contact lenses at 22.2% are the fastest-growing segment driven by younger urban consumers seeking convenience and cosmetic appeal.

The unisex segment leads gender breakup at 35.6%. North India commands the largest regional share at 32.5% in 2025, reflecting high urban density and the strong presence of organised optical retail chains across Delhi-NCR, Chandigarh, and Lucknow.

Key Market Insights

|

Insight |

Data |

|

Leading Product |

Spectacles – 45.2% share (2025) |

|

Fastest-Growing Product |

Contact Lenses – ~7.8% CAGR (2026-2034) |

|

Leading Gender Segment |

Unisex – 35.6% share (2025) |

|

Largest Region |

North India – 32.5% share (2025) |

|

Top Companies |

EssilorLuxottica, Titan Company, Bausch + Lomb, Safilo Group S.P.A., IDEE Eyewear |

Key Analytical Observations Expanding on the Above Data:

- Spectacles, with 45.2% in 2025, dominate because prescription eyewear is the primary medical intervention for over 550–600 million Indians estimated to have uncorrected or under-corrected refractive errors, making it a fundamentally recurring demand driver across all income levels and geographies.

- Contact lenses, with 22.2% in 2025, are accelerating due to rising youth aspirations, expanding affordability of monthly disposable lenses, and growing comfort levels supported by e-commerce home delivery and digital consumer education.

- North India's 32.5% dominance in 2025 reflects the concentration of organised optical retail, higher average incomes in NCR and Tier-2 cities, and strong demand for both corrective and fashion eyewear from a youth-heavy consumer base.

- West & Central India at 27.4% benefits from Mumbai and Pune's fashion-forward consumer culture, strong corporate workforce demand for blue-light protective lenses, and Maharashtra's extensive optical retail ecosystem.

India Eyewear Market Overview

The India eyewear market encompasses the design, manufacture, import, distribution, and retail of optical products including prescription spectacles, fashion and protective sunglasses, and corrective contact lenses, along with allied optical accessories and lens care solutions. The ecosystem integrates international lens manufacturers, domestic frame producers, global luxury brand licensees, optical retail chains, independent opticians, e-commerce platforms, and end consumers spanning corrective, protective, and cosmetic eyewear needs.

Market Dynamics

To evaluate market opportunities, Request Sample

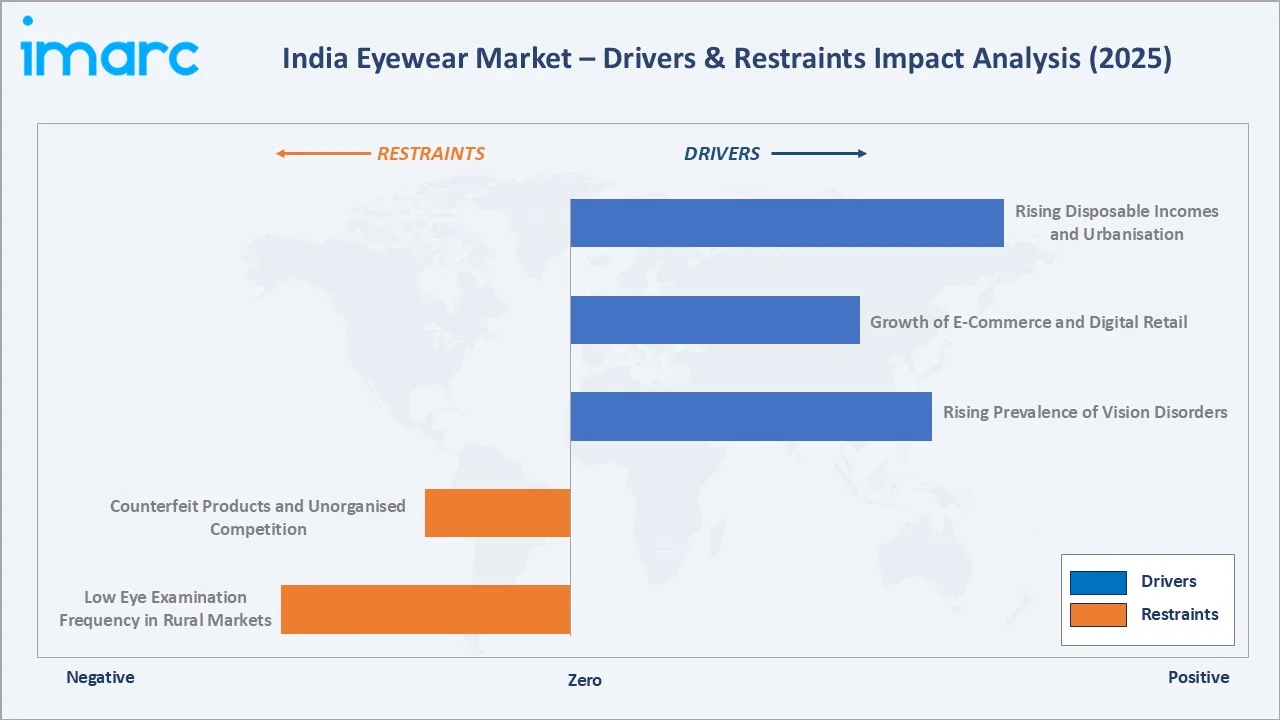

Market Drivers

- Rising Prevalence of Vision Disorders: India carries one of the world's highest burdens of uncorrected refractive errors, with an estimated 550–600 million people needing corrective eyewear. WHO data indicate myopia prevalence is rising sharply among the 10–35 age group due to increased screen time, directly expanding the addressable market for prescription spectacles and contact lenses.

- Growth of E-Commerce and Digital Retail: Rapid growth in online commerce and increasing digital adoption are enabling eyewear brands to expand beyond metro markets into smaller cities and underserved regions. Features such as virtual try-on experiences, home trial services, and seamless prescription upload options are helping improve customer convenience and reduce purchase barriers.

- Rising Disposable Incomes and Urbanisation: With more than 40% of India's population residing in urban areas in 2024 and urban disposable incomes rising steadily, consumers are trading up from basic prescription frames to premium progressive lenses, branded frames, and designer sunglasses, expanding average transaction values.

Market Restraints

- Low Eye Examination Frequency in Rural Markets: A significant portion of India's rural population does not undergo regular vision screening, limiting access to prescription eyewear despite underlying need. Poor optometry infrastructure outside urban centres constrains addressable market expansion.

- Counterfeit Products and Unorganised Competition: The prevalence of low-cost counterfeit frames and unbranded sunglasses through street vendors and unorganised retail puts downward pricing pressure on organised market players and erodes consumer willingness to pay for quality-certified eyewear.

Market Opportunities

- Blue-Light Blocking Lens Adoption: The growing awareness of digital eye strain among India's large working-age population, averaging 6–8 hours of daily screen time, presents a strong opportunity for blue-light blocking lens add-ons and specialised coatings, commanding significant premium pricing over standard lenses.

- Luxury and Designer Eyewear Segment: India's growing ultra-high-net-worth and affluent consumer base is driving demand for luxury eyewear brands. The expansion of luxury retail formats in metropolitan cities creates a premium segment with high-growth and high-margin characteristics.

Market Challenges

- Price Sensitivity and Market Fragmentation: Most Indian eyewear consumers remain price-sensitive, with independent opticians and unorganised vendors accounting for a substantial share of the market. Organised players face margin pressure while investing in store expansion, digital platforms, and product innovation simultaneously.

- Skilled Optometry Workforce Gap: Limited availability of qualified optometry and eye care professionals continues to constrain the expansion of organised vision care services, particularly in smaller cities and underserved regions. This talent gap impacts access to professional eye testing and prescription-based eyewear adoption.

Emerging Market Trends

1. Direct-to-Consumer (D2C) Disruption and Omnichannel Expansion

India's D2C eyewear revolution, led by the rapid omnichannel expansion of domestic eyewear brands, is reshaping competitive dynamics by combining online convenience with physical professional eye testing touchpoints, capturing consumers previously relying solely on independent opticians.

2. AI-Powered Virtual Try-On and Personalised Recommendations

Artificial intelligence tools enabling consumers to virtually try frames using smartphone cameras are significantly reducing online purchase hesitancy. Machine-learning algorithms analysing facial geometry and prescription requirements are personalising lens and frame recommendations, improving conversion rates on digital channels.

3. Premium Anti-Fatigue and Progressive Lens Adoption

India's growing middle-income professional population is increasingly adopting premium progressive and anti-fatigue lenses. Corporate wellness programs and employer-provided vision benefits are contributing to prescription lens upgrades among urban office workers seeking long-term visual comfort.

4. Fashion Collaboration and Affordable Luxury

Celebrity endorsements, Bollywood collaborations, and social media-driven fashion trends are elevating sunglasses from seasonal accessories to year-round fashion statements. Affordable luxury tier products are growing rapidly among India's aspirational millennial and Gen-Z consumer base.

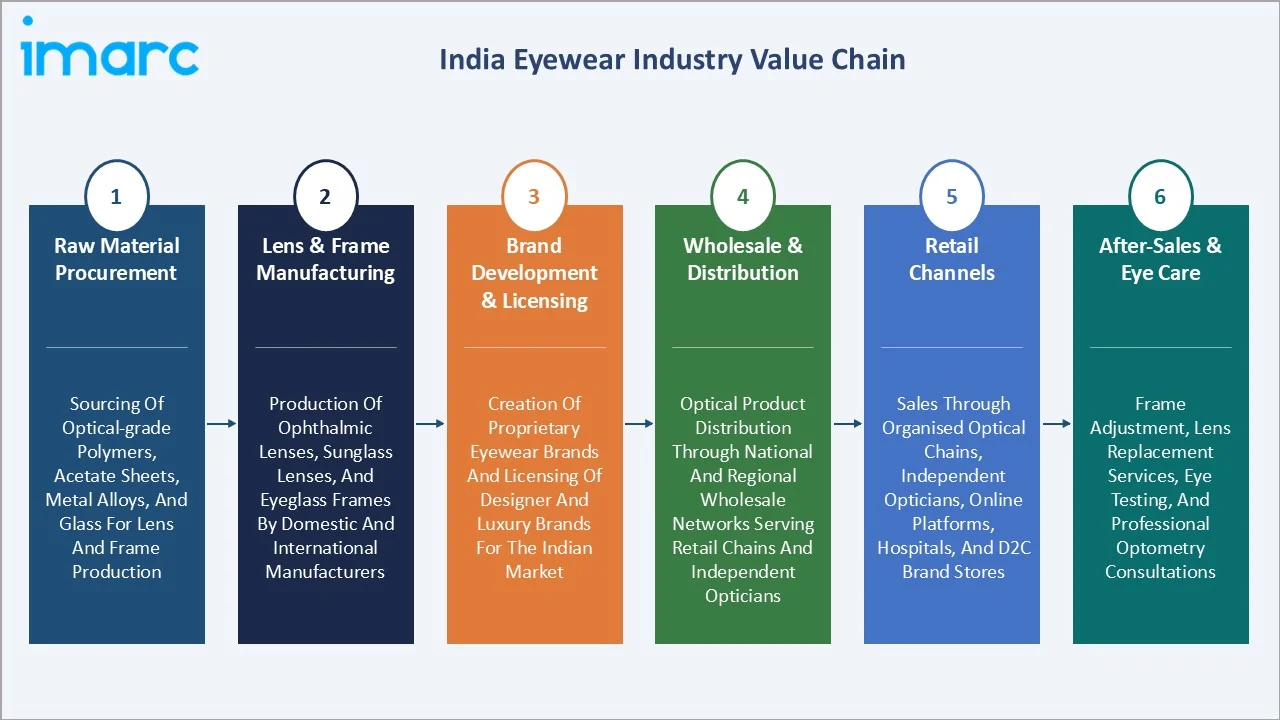

Industry Value Chain Analysis

The India eyewear value chain spans six stages from raw material procurement through after-sales services. Lens manufacturing and brand development capture the highest value-add margins, while distribution reach and e-commerce capabilities are critical differentiators for market share in India's geographically diverse retail landscape.

|

Stage |

Key Activities |

|

Raw Material Procurement |

Sourcing of optical-grade polymers, acetate sheets, metal alloys, and glass for lens and frame production |

|

Lens & Frame Manufacturing |

Production of ophthalmic lenses, sunglass lenses, and eyeglass frames by domestic and international manufacturers |

|

Brand Development & Licensing |

Creation of proprietary eyewear brands and licensing of designer and luxury brands for the Indian market |

|

Wholesale & Distribution |

Optical product distribution through national and regional wholesale networks serving retail chains and independent opticians |

|

Retail Channels |

Sales through organised optical chains, independent opticians, online platforms, hospitals, and D2C brand stores |

|

After-Sales & Eye Care |

Frame adjustment, lens replacement services, eye testing, and professional optometry consultations |

Technology Landscape in the India Eyewear Industry

Lens Manufacturing: From Glass to High-Index Polymers

The transition from glass lenses to high-index plastic polymers (1.56, 1.61, 1.67, 1.74 index) has fundamentally transformed India's prescription lens market. High-index lenses are lighter, thinner, and more cosmetically acceptable, enabling consumers with strong prescriptions to wear stylish, slim frames previously incompatible with standard CR-39 plastic lenses.

Photochromic, Polarised, and Blue-Light Blocking Coatings

Lens coating technology is the primary value-add and margin-expansion lever in the India eyewear industry. Photochromic lenses, blue-light blocking coatings, and anti-reflective multi-coat treatments carry 40–60% pricing premiums over standard clear lenses, driving average transaction value upward as consumer awareness of lens performance grows.

Digital Refraction and AI-Powered Eye Testing

Digital autorefractors and wavefront aberration measurement tools are improving prescription accuracy in Indian optical retail. AI-powered refraction platforms enabling faster and more standardised eye testing are being piloted by leading optical chains to reduce dependence on scarce optometrist manpower in high-volume retail formats.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Spectacles |

45.2% |

2025 |

|

Gender |

Unisex |

35.6% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

North India |

32.5% |

2025 |

By Product

Spectacles command a 45.2% majority share in 2025 owing to the high prevalence of myopia, hypermetropia, and astigmatism across India's population and the affordability of prescription spectacles relative to contact lenses for daily corrective use. Government school vision screening programs and healthcare outreach drives are also generating demand for corrective spectacles among previously undiagnosed consumers.

To access detailed market analysis, Request Sample

Sunglasses at 32.6% in 2025 are growing driven by UV protection awareness and fashion adoption, especially among younger urban consumers. Contact lenses at 22.2%, the fastest-growing segment, are expanding rapidly among millennials and Gen-Z consumers in metros seeking vision correction without the physical inconvenience of frames.

By Gender

The unisex segment leads gender breakup at 35.6% in 2025, primarily reflecting everyday prescription spectacles that transcend gender-specific styling. Unisex prescription frames dominate the volume tier of the Indian optical market, where functional correctness and value pricing outweigh gender-differentiated design as primary purchase criteria.

Men's eyewear at 33.2% is driven by prescription corrections and premium sunglass adoption. Women's eyewear at 31.2% is the fastest-growing gender segment as rising female workforce participation, fashion consciousness, and increasing online shopping comfort drive premium frame and contact lens purchases. Near-parity across all three segments reflects the broad-based nature of vision correction demand.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

32.5% |

High urban density and income; organised optical retail concentration; strong corporate eyewear demand |

|

West & Central India |

27.4% |

Fashion-forward consumer culture; large corporate workforce; premium lens upgrade demand from urban professionals |

|

South India |

23.6% |

Technology workforce driving blue-light lens adoption; growing health awareness; expanding D2C penetration |

|

East India |

16.5% |

Expanding urban retail presence in Tier-2 cities; growing first-time prescription adoption; e-commerce reach |

North India's 32.5% market dominance in 2025 is supported by the highest concentration of organised optical retail chains in India. Delhi-NCR, with its dense urban population, high per-capita income, and robust corporate sector, generates strong demand for both prescription eyewear upgrades and premium fashion sunglasses.

South India, with 23.6% in 2025, is experiencing strong intra-regional growth driven by Bangalore's large technology workforce, growing blue-light lens adoption, and expanding D2C eyewear penetration. West & Central India at 27.4% benefits from fashion-conscious Mumbai consumers and a growing corporate workforce demanding premium optical products.

Competitive Landscape

The India eyewear market is moderately consolidated among organised players, with leading D2C brands, national optical retail chains, and global eyewear conglomerates commanding significant shares of the organised segment. Independent opticians still account for a large portion of total market volume, representing a conversion opportunity through quality assurance and professional service positioning.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

EssilorLuxottica |

Ray-Ban, Oakley, Persol, Oliver Peoples, Vogue Eyewear, Arnette, Alain Mikli, Costa, Bliz |

Leader |

Global premium lens and iconic frame brand leadership; optical professional network expansion in India |

|

Titan Company |

Titan Eye+ |

Leader |

Pan-India optical retail chain; strong brand equity; wide coverage across urban and Tier-2 markets |

|

Bausch + Lomb |

SofLens, Ultra, BioTrue ONEday contact lenses |

Leader |

Contact lens specialist; clinical innovation; broad India retail distribution through optical professionals |

|

Safilo Group S.P.A. |

Carrera, Polaroid, Smith |

Challenger |

Licensed fashion and designer eyewear; global manufacturing with Indian optical wholesale distribution |

|

IDEE Eyewear |

Spectacles, Sunglasses |

Challenger |

Homegrown India eyewear brand; value-premium positioning; strong presence across organised optical retail chains and e-commerce platforms |

Key players include EssilorLuxottica, Titan Company, Bausch + Lomb, Safilo Group S.P.A., IDEE Eyewear, and others.

Key Company Profiles

EssilorLuxottica

The company integrates lens manufacturing, iconic frame brands, and a global retail network, with a growing India presence through licensed retail, wholesale optical partnerships, and a direct-to-professional lens sales network serving India's expanding optometry community.

- Product Portfolio: Ray-Ban, Oakley, Persol, Oliver Peoples, Vogue Eyewear, Arnette, Alain Mikli, Costa, and others.

- Recent Developments: In January 2024, EssilorLuxottica expanded its manufacturing footprint in India as part of its strategy to strengthen local production and tap into the country’s fast-growing eyewear market.

- Strategic Focus: EssilorLuxottica's India strategy targets the premium prescription lens upgrade cycle, driving consumers from basic single-vision lenses to high-value progressive and photochromic products. Partnerships with independent opticians and optical chains create a wide distribution net complementing its direct retail presence across metro India.

Bausch + Lomb

Bausch + Lomb is best known in India for its premium contact lens portfolio and lens care solutions, serving both independent opticians and organised optical retail chains through a well-established professional distribution network.

- Product Portfolio: SofLens, Ultra, BioTrue ONEday contact lenses, among others.

- Strategic Focus: Bausch + Lomb's India strategy is anchored in clinical credibility and eye care professional endorsement. By targeting ophthalmologists, optometrists, and optical retail professionals as primary influencers, the company drives premium contact lens trial and adoption among first-time and upgrading lens wearers. Investment in consumer education around lens hygiene and the convenience of daily disposables underpins its growth strategy in urban India.

Market Concentration Analysis

The India eyewear market exhibits a dual-tier structure: the organised segment is moderately concentrated among national optical chains, D2C brands, and global eyewear conglomerates, while the broader market remains fragmented with numerous independent opticians operating outside formal retail structures across Tier-2 and Tier-3 cities.

Leading domestic D2C brands and national optical retail chains represent the most significant organised consolidation forces in India's eyewear industry. Global players such as EssilorLuxottica and Safilo operate primarily through wholesale partnerships with Indian optical retailers, giving them market share in the lens and branded frame categories without requiring own-store capital investment at scale.

Investment & Growth Opportunities

Fastest-Growing Segments

Contact lenses at ~7.8% CAGR through 2034 represent the highest-growth product segment, driven by youth adoption, D2C subscription models, and expanding urban lifestyle alignment. South India at ~7.1% CAGR is the fastest-growing region, anchored by Bangalore's technology demographic and Kerala's health-conscious consumer base.

Emerging Markets

Tier-2 and Tier-3 cities across India represent the largest untapped opportunity in the eyewear market. Rapid smartphone penetration enabling e-commerce access, combined with first-time prescription adoption driven by government school vision programs, is opening addressable markets previously underserved by organised optical retail infrastructure.

Venture & Investment Trends

Investor appetite for D2C eyewear platforms in India remains strong. Optical retail chain consolidation, specialty contact lens subscription platforms, and AI-driven optometry technology startups are attracting venture and private equity attention. Vision insurance products and corporate vision benefit programs represent structural market-expansion levers being actively evaluated by healthcare-focused investment funds.

Future Market Outlook (2026-2034)

The India eyewear market is forecast to expand from USD 11.09 Billion in 2025 to USD 20.86 Billion by 2034 at a CAGR of 6.66%, adding approximately USD 9.77 Billion in incremental annual market value over the forecast period. This sustained growth reflects rising vision correction needs, fashion-lifestyle convergence in eyewear demand, and the ongoing digital transformation of retail distribution.

Three forces will most significantly shape the industry through 2034. Contact lens adoption will accelerate as daily disposable lens prices decline with domestic manufacturing scale-up and competitive online pricing. The premium lens upgrade cycle will add incremental value as consumers migrate from basic single-vision to progressive and coated lenses. Smart eyewear incorporating display overlays and health monitoring will create a new premium product category beyond traditional corrective and protective eyewear.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Indian optical retail chain managers, independent optometrists, brand representatives of leading eyewear companies, optical wholesale distributors, and consumer focus groups across North, South, West, and East India. Primary data validated market sizing, product and gender segment shares, regional demand estimates, and competitive positioning assessments.

Secondary Research

Key secondary sources include WHO Global Vision Database, National Programme for Control of Blindness (NPCB) India data, IMARC Group e-commerce market data, Worldometers India urbanisation statistics, Ministry of Health & Family Welfare reports, trade publications including Vision Monday and Optician International, and industry association data from the All India Opticians Association (AIOA).

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models incorporating India GDP growth projections, urbanisation indices, consumer expenditure data, eyewear penetration rates, and historical market evolution patterns. Scenario analysis encompassing base, optimistic, and conservative cases was performed to account for macroeconomic variability.

India Eyewear Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Spectacles, Sunglasses, Contact Lenses |

| Genders Covered | Men, Women, Unisex |

| Distribution Channels Covered | Optical Stores, Independent Brand Showrooms, Online Stores, Retail Stores |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | EssilorLuxottica, Titan Company, Bausch + Lomb, Safilo Group S.P.A., IDEE Eyewear, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India eyewear market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India eyewear market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India eyewear industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Indian Eyewear Market Research Report and Industry Forecast Report

The India eyewear market reached USD 11.09 Billion in 2025, reflecting consistent demand driven by rising vision disorder prevalence, growing consumer incomes, and expanding organised optical retail across urban and Tier-2 markets.

The market is projected to reach USD 20.86 Billion by 2034, growing at a CAGR of 6.66% during 2026-2034, driven by rising prescription eyewear adoption, e-commerce expansion, contact lens growth, and premiumisation of lens coatings and frame styles.

Spectacles lead with a 45.2% product share in 2025, driven by India's high burden of uncorrected refractive errors and the broad affordability of prescription frames through optical chains, online platforms, and government vision care programs.

The unisex segment leads with a 35.6% share in 2025, reflecting the broad-appeal nature of everyday prescription spectacles. Men hold 33.2% share while women hold 31.2%, with near-parity indicating that vision correction need is largely gender-neutral in India.

North India commands the largest regional share at 32.5% in 2025, driven by the concentration of organised optical retail in Delhi-NCR, Chandigarh, and Lucknow, higher per-capita incomes, and strong corporate and youth demand for both corrective and fashion eyewear.

Contact lenses are the fastest-growing product segment at approximately 7.8% CAGR through 2034, driven by younger urban consumers seeking convenience-oriented vision correction, expanding daily disposable lens affordability, and D2C subscription models making lenses accessible across Tier-2 cities.

Leading companies include EssilorLuxottica, Titan Company, Bausch + Lomb, Safilo Group S.P.A., IDEE Eyewear, and others.

Key applications include prescription vision correction (myopia, hypermetropia, astigmatism), UV and glare protection through sunglasses, digital eye strain management via blue-light blocking lenses, cosmetic contact lenses, and occupational safety eyewear in industrial and laboratory environments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)